Abstract

Due to the complexity and heterogeneity of hedge fund strategies, the evaluation of their performance and risk is a challenging task. Starting from the standard mutual fund industry, the literature has evolved in the direction of refining traditional measures (e.g. the Sharpe Ratio) or introducing new ones. This paper develops an approach, based on the Principal Component Analysis, to uncover the relevant information for performance measurement and combine it into a unique rank.

Access provided by Autonomous University of Puebla. Download conference paper PDF

Similar content being viewed by others

Keywords

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

1 Introduction

In this paper the problem of performance assessment within the hedge fund industry is investigated. By combining commonly used and newly developed statistical performance indicators, a unique ranking of the industry is produced. A set of 18 indicators is firstly identified and then combined into a rank by a principal component analysis. This allows to detect the underlying drivers of the performance. Finally, a feature of the hedge funds that is not captured by this combination of indicators, namely the capability of raising the portfolio efficiency, is investigated. This is done by computing the upside gained by a balanced portfolio through the inclusion of a share of hedge funds.

Why should we not solely rely on the traditional risk adjusted measures to assess hedge funds performance? As a matter of fact, in the traditional mutual fund industry, performance is typically based on a version of the Sharpe Ratio (see for instance Morningstar and the well known star attribution system). Subscribing to the views expressed by Fung and Hsieh (1998, 1999), the transfer of this methodology to the hedge fund industry could be arduous, since hedge funds differ from mutual funds mainly because of the variety of strategies adopted. This leads to widely different returns and volatilities depending on the particular fund. Thus, some hedge funds may be non-directional and less volatile than traditional bond and equity markets, while others may be fully directional and display higher volatility. As widely discussed by Ineichen (2003), hedge fund differences from mutual funds hinge on their relationship with the broader environment of financial markets. Dynamic reallocation of portfolios can create non-linear patterns with respect to the market (Agarwal and Naik 2004). In addition, hedge funds structurally use leverage. As discussed in Brealey and Kaplanis (2001), even if the fund remains exposed to the same market, variation in leverage, obtained by changing the net exposure between short and long position, may introduce further non-linearities. Finally, hedge-funds may invest in non-traditional financial assets such as derivatives. Some of these instruments display non-linearities because of their implicit features (Mitchell and Pulvino 2001). The structural characteristics of hedge-funds mentioned above, strongly affect the standard techniques of evaluating mutual funds.

If the risk adjusted return insufficiently portrays the hedge fund performance, how may we satisfactorily assess it? An answer to this question must entail the investor point of view, which ultimately defines the characteristics of hedge funds. Indeed, a hedge fund portfolio manager, in order to charge higher fees than mutual funds, makes every effort to provide the fund with some superior characteristics which can be summarized as follows:

-

The capability of generating appealing absolute returns.

-

The capability of protecting capital.

-

The capability of raising the efficiency of a portfolio.

Generating appealing returns is attained by participating to the upside of a traditional investment, while protecting the capital may be achieved through an accurate hedging of the downside. These investment objectives cannot be reached through a linear exposure to the markets. By contrast, an asymmetric payoff resembling a call option is more suitable. In addition, the management of a hedge fund should result in a low correlation with “traditional” financial markets, thus increasing its appeal as a portfolio diversificator.

To address the problem of performance assessment, statistical indicators—chosen among widely used indicators—have been selected in accordance with the three identified features.

2 The Statistical Indicators

A burgeoning literature is currently discussing the appropriate tools for hedge fund performance measurement (Géhin 2004; Lhabitant 2004). The main problem hinges on the non-linear market exposure that often results in characteristics that limit the applicability of the classical bi-dimensional, risk and return, measures. In particular, the return distribution patterns, measured by moments higher than two, becomes relevant and could result in an over or underestimation of the performance. On this basis, measures that either come from the traditional investment world or have been accepted as useful tools to overcome the typical asymmetries of the hedge fund industryFootnote 1 are selected (Table 1).

Besides browsing among all the indicators, we reserve some notes on the measures capable of capturing the asymmetries typical of returns as it will turn out to be relevant in our application. Apart from skewness and kurtosis, a common solution to capture the shape of return distribution is attained by considering only the returns that lie below the average mean (Markowitz 1959). A measure that goes in this direction and, coherently with Kahnemann and Tversky (1979), that describes investors’ viewpoint in an appropriate way, is the negative semi deviation

where R t is the sequence of the hedge fund log-returns.

Together with negative semi deviation practitioners often analyze the downside exposure, through empirical measures like the maximum drawdownFootnote 2

or the value at risk

where \( {\mu_R} \) and \( {\sigma_R} \) are respectively the hedge fund average return and volatility and \( {z_{\alpha }} \) satisfies

where α is the desired percentile and Φ is the CDF of the standard normal distribution.

The last indicator has the same previously outlined problems in case returns exhibit non-normal features. To accomplish this problem, it is convenient to approximate the quantiles of the distribution via Cornish–Fisher approximations, which corrects the distortion in the returns distribution of the fund by integrating the effect of the moments of order greater than two on the left tail.Footnote 3 According to Hill and Davis (1968), it is called Cornish–Fisher percentile at the α significance level the α standard normal percentile corrected by the skewness \( \mathit{Skew}(R) \) and the kurtosis \( \mathit{Kurt}(R) \) effectFootnote 4:

The value at risk correction is then:

Another important group of indicators refers to risk-adjusted measures. Beyond the Sharpe ratio that, in the case of hedge funds, provides a consistent under/over estimation of the risk adjusted performance, the two selected measures are the Sortino ratio

and the Cornish–Fisher Sharpe ratio

where \( {R_F} \) is the risk-free return.

3 Ranking the Hedge Fund Industry

To uncover most of the relevant information scattered across the statistical indicators adopted we have used the Principal Component Analysis (PCA). It may help to identify the implicit factors that significantly explain the overall variability, included in the variance and covariance matrix. Each of these factors consists of a linear combination of the original indicators. The proportion of variability explained by each of the factors is a natural way to estimate their relative strength. Moreover the components turn out to be uncorrelated among themselves so that they may be aggregated into a unique performance rank.

To explore whether the proposed ranking method can be applied within the hedge fund industry two different index families—CS (Credit Suisse/Tremont) and HFR (Hedge Fund Research)—are considered.Footnote 5 The data consist of monthly returns (from January 1994 to July 2011) of the universe of the two types of indices (55 for the CS and 32 for the HFR type respectively) and the ranking exercise is performed three times in July of the last 3 years.Footnote 6 The principal component technique, applied to the set of indicators previously normalized in the interval [0,10], extracts four factors that explain on average the 89 % of the total industry variability (Table 2).

To characterize the four components, it is convenient to analyze the correlations of the rotated component matrix.Footnote 7 In Table 3 results obtained in the 2009 analysis are reportedFootnote 8 where correlations, between factors and observed variables, in absolute value greater than 0.7 are shown in italics. The component structure is amenable to interpretation:

-

Factor 1: Appealing returns and Capital Protection. Represents absolute returns and captures the fund downside exposure (Annualized and Median return, Frequency of positive returns; Annualized volatility, Negative semi-deviation; Maximum drawdown and Value at Risk).

-

Factor 2: Asymmetry. Measures the ability that the fund payoff resembles a call: consistent right tailed distribution, i.e. positive skewness/negative kurtosis (Skewness, Kurtosis, Normality and Cornish Fisher quantile).

-

Factor 3: Risk Adjusted Performance. Captures the fund capability of balancing risk against reward (Sharpe ratio; Sortino; Adjusted and Cornish Fisher Sharpe ratio).

-

Factor 4: Market correlation. This component is self-explanatory and is approximated by the considered market proxies.

Since the components are by construction uncorrelated, the intuition suggests to assemble a ranking index, by linearly combining for each hedge fund the score of each factor with its weight, given by the percentage of variance explained. To facilitate the construction of a ranking grid, the score is replaced with its rank. In Table 4 the final ranking for the first ten positions of the HFR and CS indexes in 2009 is reported for explanatory purposes.

As a final test, we used the Spearman Rank correlation to compare previous and subsequent classifications. Our results indicate a strong correlation if 1 year lagged rankings are compared whereas—if a 2-year lagged ranking is considered—the null hypothesis of no persistence can be accepted with at least 95 % confidence in all the two types of the considered indices. Moreover, in the HFR analysis, the 2-year lagged rankings were found to be of opposite sign, though these results lacked statistical significance.

4 Raising Portfolio Efficiency

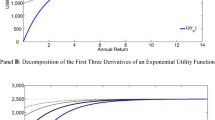

Assessing the ability of hedge funds to raise portfolio efficiency requires a separate analysis. The methodology originally developed by Modigliani and Modigliani (1997) is adapted to compare a balanced portfolio with another where 30 %Footnote 9 of the traditional investments are replaced by hedge funds. The efficiency spread is measured by the Modigliani–Modigliani index, that is the difference between the potential return of the (de)leveraged portfolio containing hedge funds and the return of the balanced portfolio. The former is (de)leveraged to the point where its volatility is equal to the balanced portfolio volatility. From this perspective, the Modigliani–Modigliani index can be interpreted as the return spread at the same level of volatility. The return spread is expected to be higher, the lower the correlation with traditional investments. It is important to bear in mind that the correlation effect is more important than the risk/return profile, since it acts directly on the volatility by reducing the systematic portfolio risk. Even if the hedge fund (HF), as in Fig. 1, is Pareto dominated by the balanced portfolio (P) it can happen that the combined portfolio (P +) shares a sufficiently limited volatility to have a positive return spread.

Formally:

A classification based on the Modigliani–Modigliani index may stress which are the hedge funds that contribute to portfolio diversification. We have computed, for each balanced portfolio obtained by replacing the 30 % with hedge funds, the Modigliani–Modigliani index.

In Tables 5 and 6 rankings, only for the first ten positions, obtained according to the Modigliani–Modigliani index respectively for the HFR and CS indices are reported and compared to the ones retrieved from the previous analysis. It seems, as one may grasp from the results, that this technique points out that portfolio diversification is independent from the properties that the funds share as pure hedge funds.

Return spread and Modigliani–Modigliani index

Are hedge funds that have appealing performances alone also good contributor to portfolio diversification? Intuition may suggest that this cannot be true: appealing performance profile results from a non linear exposition to the market and this in some cases may affect portfolio risk. Moreover, the analysis of ranking permutations, accomplished by Spearman Rho, confirms that few average performing hedge funds display a consistent advantage in diversification: all the coefficients, albeit positive, are below 0.3 and indicate that the correlation is weak in all of the 3 years considered in the analysis.

Notes

- 1.

MSCI World Index and Barclays Euro Aggregate (BEA) are chosen to represent correlation with Equity and Bond market.

- 2.

It should be pointed out that maximum drawdown is an empirical measure, without any statistical consistency.

- 3.

A different solution can be found in Bramante and Zappa (2011).

- 4.

Kurtosis are translated to zero.

- 5.

These are the two widely recognized hedge fund index providers in the industry.

- 6.

Since the ability of this method in summarizing common patters depends on whether data contain strongly correlated variables, average partial correlation between variables was computed across the three considered years. Above all, the largest ones are between the three “Cornish Fisher” indicators and within the risk variables (Annualized Volatility, Negative Semi Deviation and Value at Risk 5 %).

- 7.

A varimax rotation was performed.

- 8.

Similar results, referred to the remaining two scenarios, are omitted.

- 9.

30 % is arbitrarily chosen. However, empirical simulations show that 30 % of asset allocation in hedge funds seems to be closed to the optimum, in terms of the distance from the efficient frontier.

References

Agarwal, V., & Naik, N. Y. (2004). Risk and portfolio decisions involving hedge funds. Review of Financial Studies, 17(1), 63–98.

Bramante R., & Zappa, D. (2011). Value at risk estimation in a mixture normality framework. In Proceedings of the Eighteenth International Conference Forecasting Financial Markets—Advances for Exchange Rates, Interest Rates and Asset Management, Marseille.

Brealey, R. A., & Kaplanis, E. (2001). Hedge funds and financial stability: An analysis of their factor exposures. International Finance, 4(2), 161–187.

Fung, W., & Hsieh, D. A. (1998). Performance attribution and style analysis: From mutual funds to hedge funds. Working paper, Duke University, Fuqua School of Business.

Fung, W., & Hsieh, D. A. (1999). A primer on hedge funds. Journal of Empirical Finance, 6, 309–331.

Géhin, W. (2004). A survey of the literature on hedge fund performance. Nice: EDHEC Risk and Asset Management Research Centre, EDHEC Business School Lille.

Hill, G. W., & Davis, A. W. (1968). Generalized asymptotic expansions of Cornish–Fisher type. Annals of Mathematical Statistics, 39, 1264–1273.

Ineichen, A. M. (2003). Absolute returns: The risk and opportunities of hedge fund investing. Hoboken: Wiley.

Kahnemann, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263–292.

Lhabitant, F. S. (2004). Hedge funds, quantitative insights. Chichester: Wiley.

Markowitz, H. (1959). Portfolio selection. Journal of Finance, 17(1), 77–91.

Mitchell, M., & Pulvino, T. (2001). Characteristics of risk in risk arbitrage. Journal of Finance, 56, 2135–2175.

Modigliani, F., & Modigliani, L. (1997). Risk-adjusted performance—how to measure it and why. Journal of Portfolio Management, 23(2), 45–54.

Acknowledgments

The development of this paper benefited significantly from the input and support of Alessandro Cipollini and Antonio Manzini.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2013 Springer International Publishing Switzerland

About this paper

Cite this paper

Bramante, R. (2013). An Approach to Ranking the Hedge Fund Industry. In: Giudici, P., Ingrassia, S., Vichi, M. (eds) Statistical Models for Data Analysis. Studies in Classification, Data Analysis, and Knowledge Organization. Springer, Heidelberg. https://doi.org/10.1007/978-3-319-00032-9_8

Download citation

DOI: https://doi.org/10.1007/978-3-319-00032-9_8

Published:

Publisher Name: Springer, Heidelberg

Print ISBN: 978-3-319-00031-2

Online ISBN: 978-3-319-00032-9

eBook Packages: Mathematics and StatisticsMathematics and Statistics (R0)