Abstract

The innovation capability evaluation is in fact a multi-criteria decision-making problem that requires aggregating multiple innovation management practices into a composite innovation capability index. In such multi-criteria decision-making, assigning appropriate weights to criteria is a critical and difficult task. However, the literature related to innovation capability evaluation mainly used the weighting methods based on subjective expert opinions. These conventional methods have problems when dealing with complex multi-criteria data. This study aims to develop a method for automatically determining the weights of multiple innovation management practices for evaluating innovation capability in banking based on data envelopment analysis (DEA) model without input. The results will show the typical importance weights of innovation management practices for each bank which are then used to derive an aggregated index objectively representing the innovation capability level of each bank. A case study of three banks in Vietnam was adopted from the prior study to show the applicability of the proposed method.

Access provided by Autonomous University of Puebla. Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

The fourth industrial revolution with digitization and the explosion of many new technologies such as artificial intelligence, big data, and cloud computing brings great opportunities for the development in the production and business processes. Organizations across sectors have been putting many efforts into exploiting new technologies to innovate their products/services in order to survive in the digital economy. The pivotal role of innovation in the competitive advantage and success of a company is firmly confirmed in the literature [1, 2]. According to [3], a company can only effectively innovate if it has innovation capability (IC). IC is a significant determinant of continuous innovations to respond to the dynamic market environment and also firm performance [4, 5]. Therefore, the IC evaluation is a serious problem that organizations must consider to comprehend their IC levels and find out important areas in the innovation management process that should be focused on to improve the IC level for achieving better innovative performance as well as higher business performance.

Because IC is a multidimensional process [6, 7], the IC evaluation can be considered as a multi-criteria decision-making (MCDM) problem which requires taking into account multiple criteria (in this study, multiple innovation management practices (IMPs)). Some of the IMPs used for measuring IC in the prior studies are strategic planning [8, 9], organization [10, 11], resource management [12, 13], technology management [14, 15], research and development (R&D) [16, 17], knowledge management [13, 18], network and collaboration [8, 19]. In MCDM, weighting and aggregating of criteria are major tasks in developing composite indicators [20]. Especially, different sets of weights lead to different ranking outcomes, so the weighting method should be fair. To derive an overall evaluation on the IC of a company, we first need to determine the weights of different IMPs for each company that are then used for computing the composite innovation capability index (CICI) of that company.

In the literature on the IC evaluation, the widely used weighting methods have been relied on subjective opinions from experts such as the analytic hierarchy process (AHP) [10], fuzzy measures [17, 21]. However, it is difficult, time-consuming, and even costly to get such information from experts, especially in case there are complex and changing multiple criteria. One of the common subjective weighting methods is the AHP which requires subjective judgments of experts to make pairwise comparisons among criteria from which the weights of criteria are obtained. When the number of criteria is high, the experts may face difficulties to deal with many comparisons, sometime they may be confused. It is the reason why the weighting methods that require external or prior information was criticized by [22]. Moreover, the prior studies only applied the same set of weights for different companies. This may cause disagreement among the companies because each company may have its own business strategies that lead to different preferences in developing particular IMPs. To overcome the shortcomings of subjective weighting methods, further consideration can be placed on developing objective weighting methods that can endogenously drive the weights of criteria based on data without referring to any prior or external information. Up to now, far too little attention has been paid to applying data-driven weighting methods in the IC evaluation. This indicates a need to develop a weighting method based on the collected data of IMPs to be applied in evaluating the IC of companies. Several data-driven weighting methods such as DEA, or Genetic Algorithm (GA) can be considered.

The purpose of this paper is to develop a data-driven weighting method based on DEA to determine the typical set of weights of IMPs for each bank or the IMPs focused/ignored by each bank and thereby compute an overall IC evaluation (CICI) for each bank based on aggregating multiple IMPs and sub-IMPs. DEA is one of the popular methods for developing composite indices in MCDM, it can select the best possible weights of IMPs for each bank by giving higher weights for better IMPs and therefore give objective evaluations on the IC of banks. To illustrate the applicability and validity of the proposed method, the data of IMPs and sub-IMPs on a case study of three banks in Vietnam was taken from the literature [23]. The data on sub-IMPs were first averaged to obtain the scores of IMPs. The data-driven weighting method developed based on DEA model was then employed to determine the weights of IMPs for each bank that were finally used to aggregate IMPs into a composite index (CICI). The research findings could be used as a basis for benchmarking the most innovative banks and potentially support bank managers in proposing effective strategies for properly allocating innovation resources in order to upgrade their IC and achieve better innovative performance.

This study makes two contributions to the innovation literature as well as the practices of innovation management. First, this study can be considered as one of the first attempts that apply a data-driven weighting method (DEA without input) for evaluating IC. Second, this study will contribute to a deeper understanding of the important IMPs that each bank is focusing on and the corresponding IC levels of banks, based on which some useful lessons can be drawn for innovation management in banking.

The remaining part of this paper proceeds as follows: Sect. 2 reviews theories of IC evaluation and DEA models. Section 3 is concerned with the proposed method by this study. The empirical results of using the proposed IC evaluation method in the case study of three banks in Vietnam are displayed in Sect. 4. Section 5 presents the conclusions of this study.

2 Literature Review

2.1 IC Evaluation

Innovation can be defined as beneficial changes in organizations to create new or improved products/services and thereby to improve business performance [24,25,26,27]. Successful innovations require a wide combination of many different assets, resources, and capabilities that facilitate the development of new or improved products/services to better satisfy market needs (also known as IC) [16, 28,29,30,31]. According to [32], IC refers to the capability of utilizing innovation strategies, technological processes, and innovative behaviors. Lawson and Samson proposed seven constructs in developing IC including strategy, competence, creative idea, intelligence, culture, organization, and technology [14]. As IC is a complex concept that is multi-dimensional and impossible to be measured by a single dimension [33], multiple IMPs must be considered to evaluate the IC of a company.

On account of the role of improving IC for successful innovation, IC evaluation has become one of the dominant streams in the innovation research literature. The common approach for evaluating IC in the previous works was based on multiple IMPs to comprehensively apprehend all necessary capabilities for organizations to effectively innovate. However, particular authors may adapt different IMPs according to the research contexts and also used different techniques to aggregate all IMPs into a single index showing the IC level of a firm. Wang et al. [17] applied a non-additive measure and fuzzy integral method to evaluate the overall performance of technological IC in Taiwanese hi-tech companies. Five factors including innovation-decision, manufacturing, capital, R&D, and marketing capabilities with various qualitative and quantitative criteria were considered in their research. Cheng and Lin [21] proposed a fuzzy expansion of the Technique for Order of Preference by Similarity to Ideal Solution (TOPSIS) to measure the technological IC of Taiwanese printed circuit board firms taking into account seven criteria comprising planning and commitment of the management, knowledge and skills, R&D, marketing, information and communication, operation, and external environment. Wang and Chang [10] presented a hierarchical system to diagnose the innovation value of hi-tech innovation projects considering five main dimensions (strategy innovation, organization innovation, resource innovation, product innovation, and process innovation) and their fifteen secondary dimensions. By adopting the AHP, the main dimensions are found in the descending order of importance to the firm’s innovation performance: process innovation, resources innovation, product innovation, strategic innovation, and organizational innovation. Boly et al. [9] adopted a multi-criteria approach and value test method to measure the IC of French small and medium-sized manufacturing companies based on 15 IMPs: strategies management, organization, moral support, process improvement, knowledge management, competence management, creativity, interactive learning, design, project management, project portfolio management, R&D, technology management, customer relationship management, and network management. The evaluated companies were then categorized into four innovative groups (proactive, preactive, reactive, passive) based on their IC levels.

The literature review reveals that many attempts have been made to evaluate IC in manufacturing sectors [9, 17, 21]. However, there are limited numbers of studies that focus on IC evaluation in the service sector, particularly in the banking sector. In fact, banks are also keenly focusing on innovating their services by adopting new technologies to promptly deliver their services, improve banking experiences for customers, and thereby stay competitive in the market [34]. Innovation becomes a core business value of banks nowadays, it helps banks to explore new opportunities for stable development, and long-term success [35, 36]. It is widely approved that innovation in each sector has different unique characteristics [37]; therefore, banks cannot apply the same innovation management policies as manufacturing sectors when developing their new services. Thus, there is an emerging need for a study dedicated to evaluating the IC of banks. In an effort to fill this gap, this study will contribute a method for IC evaluation in banking by investigating the importance weights of IMPs in the banking context as well as determining the overall IC level of banks to be evaluated.

2.2 DEA Models

DEA, proposed by [38], is used to measure the efficiency of decision-making units (DMUs) that is obtained as the maximum of a ratio of a weighted sum of outputs to a weighted sum of inputs. For each particular DMU, the weights are chosen to maximize its efficiency. For example, to calculate the efficiency of a DMU k in a set of all DMUs to be measured K:

subject to

where \(e_k\) and \(e_{k'} \) are the efficiency of DMU k and DMU \(k'\), k and \(k'\in K\); n and m are the number of outputs and the number of inputs, respectively; \(w_i\) and \(u_j\) are the weight of the i-th output (\(i=1,...,n\)) and the weight of the j-th input (\(j=1,...,m\)), respectively; \(\text {y}_{ik'}\) is the value of the i-th output of DMU \(k'\); \(\text {x}_{jk'}\) is the value of the j-th output of DMU \(k'\). The maximization (Eq. (1)) selects the most favorable set of weights for the DMU k whose score is being optimized while the constraints allow. To compute the efficiency of the other DMUs, it just needs to change what to maximize in Eq. (1). The advantage of the DEA model is that it can endogenously derive the different preference profiles for each DMU and thus provide a more objective evaluation for DMUs than the approaches that determine weights based on subjective information from experts.

DEA has become one of the commonly used techniques that can resolve the subjectivity problem in developing composite indicators. Although the original DEA requires outputs and inputs to be specified, several authors have proposed DEA-like models to solve the problems that there is no input. For instance, Zhou et al. [39] presented the best practice model in which a DEA-like model without input was used to obtain the different weights for each DMU. Their approach allows each DMU to pick its own most favorable weights to maximize its aggregated score. However, extreme weighting of sub-indicators may occur, so this approach becomes unrealistic and comes with low discriminating power. To alleviate this shortcoming, Hatefi and Torabi [40] proposed a common weights approach, the same weights are applied to compute scores for all DMUs, to improve discriminating power. The authors used an optimization model to select the weights that minimize the largest deviation among the scores’ deviations from 1. This means the selected weights will maximize the lowest score. Thus, this approach has a drawback as the worst performing DMU controls the final weights.

3 Data-Driven Weighting Method Based on DEA Model

In this study, a data-driven weighting method based on DEA model is proposed to compute composite indices representing IC levels of banks (CICI). However, in our formulation, the proposed DEA model has no input and several revisions in constraint conditions compared with the original DEA model.

The IC evaluation in banking follows the two-level hierarchy: the upper level contains IMPs and the lower level comprises the sub-IMPs related to each IMP in the upper level. The sub-IMPs are assessed using a five-point Likert scale (from 1-very bad to 5-very good) to show how efficiently those practices are achieved at the evaluated banks. Accordingly, there are two levels of aggregation to calculate the CICI of these banks. The first level of aggregation (lower level aggregation) is to aggregate sub-IMPs of an IMP to determine the development degree of this IMP at each bank. The second level of aggregation (upper level aggregation) aims to aggregate IMPs to derive the overall IC of each bank (CICI).

3.1 Lower Level Aggregation

Let B be the set of all banks to be evaluated. Considering a bank \(b \in B\), the development degree of IMP i at bank b is determined as follows:

where \(\bar{x}^{(b)}_i\) is the development degree of IMP i at bank b, \(\bar{x}^{(b)}_i \in [1,5]\); \(x^{(b)}_{ij}\) is the score of the j-th sub-IMP of the i-th IMP of bank b, \(x^{(b)}_{ij}\in [1,5]\); \(N_i\) is the number of sub-IMPs associated with IMP i; N is the number of IMPs.

According to Eq. (2), the development degree of an IMP is obtained by averaging the scores of all sub-IMPs related to this IMP, in other words, the weights of sub-IMPs are equal. Equal weighting is applied because the relation between IMPs and their measurement items (sub-IMPs) is not causal [9]. Moreover, we prioritize to determine the different weights of IMPs in the upper level of aggregation to specify critical IMPs that much decide the IC of banks.

3.2 Upper Level Aggregation

For the upper level aggregation, we first determine the optimal set of weights of IMPs for each bank so that it will maximize the CICI of the bank being evaluated. The optimal weights for each bank is calculated based on the data of IMPs obtained in the lower level aggregation.

Considering a bank \(b \in B\) (B is the set of all banks to be evaluated), let \(W^{(b)}=\{w^{(b)}_1,\dots ,w^{(b)}_N\}\) be the optimal set of weights for maximizing the CICI of bank b, \(CICI^{(b)} \in [1,5]\). The optimal set of weights for bank b is determined by solving the optimization problem below:

subject to

where \(\bar{x}^{(b)}_i\) is the development degree of IMP i at bank b, \(\bar{x}^{(b)}_i \in [1,5]\); \(w^{(b)}_i\) is the weight of IMP i in the optimal set of weights \(W^{(b)}\) for bank b; N is the number of IMPs. The above optimization problem is converted into a linear programming problem that can be solved by a linear programming solver (such as Scipy package for Python).

It is worth noting that the most ideal CICI value that a bank can reach is 5, but in practice, the CICI values are usually lower than 5. Therefore, we set the threshold of CICI as \(5\,-\,\epsilon , \epsilon \in [0,4]\). One more constraint condition is added to solve the above optimization problem: The CICI values of all banks in the set B must be equal or lower than \(5 - \epsilon \) when applying the optimal weights for bank b being optimized.

It is clear that, if the value of \(\epsilon \) is low, extreme weighting may occur with higher weights for better IMPs, which leads to a high standard deviation of weight values. When \(\epsilon \) is increased, the standard deviation of weight values will be reduced. At the standard deviation of weight values equals 0, equal weighting happens. The selection of \(\epsilon \) is optional, depending on the evaluator’s preference. \(\epsilon \) can be chosen so that the corresponding standard deviation of weight values is in the range between its highest value and its lowest value. If the evaluator prefers the weights toward extreme weighting to clearly show the best practices of each bank, \(\epsilon \) is selected at the corresponding standard deviation of weight values near its highest value. In contrast, in case the evaluator prefers the weights toward equal weighting, \(\epsilon \) is chosen so that the corresponding standard deviation of weight values is close to its lowest value. In this study, we tend to choose the standard deviation of weight values in the middle area of its possible range to balance extreme weighting and equal weighting.

The optimal set of weights for a bank can disclose which IMPs that this bank is focusing on. By comparing with other banks, we can explore the strengths and weaknesses of each bank on different IMPs.

4 An Illustrated Example

This example is adopted from the research of [23] on evaluating the IC of three banks in Vietnam. The concept of IC in their research was defined based on the Pareto analysis - a statistical technique to select the major tasks which the management should put more effort into. As a result, 11 IMPs were chosen as critical practices in innovation management process: managing strategy (MS), managing resource (MR), organizing (OR), managing idea (MI), improving process (IP), marketing (MA), R&D (RD), interactive learning (IL), managing portfolio (MP), managing knowledge (MK), and managing technology (MT). The 44 measurement items/sub-IMPs measuring the 11 IMPs were adapted from [8,9,10,11,12,13, 15, 16, 19, 41,42,43,44,45,46,47], which ensures the reliability and validity of the measurement scale as they were verified through peer-reviewed previous research (see Table 1). In their data collection [23], five experts in banking fields individually responded to the questionnaire to rate the development degrees of sub-IMPs in the three evaluated banks, enormously called Bank a, Bank b, and Bank c, using a five-point Likert-scale ranging from 1 (very bad) to 5 (very good). The final scores of 44 sub-IMPs for the three banks (shown in Table 2) were obtained by averaging the assessment scores of the five experts.

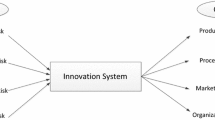

The IC evaluation for the three banks is composed of two levels of aggregations as shown in Fig. 1. In the lower level aggregation, the 4 sub-IMPs associated with each IMP at each bank are aggregated. Eq. (2) with the values of Table 3 gives the average scores of the 11 IMPs for the three banks in the sample.

To aggregate the 11 IMPs in the upper level, we first need to determine the optimal weights of the 11 IMPs for each of the three banks by solving model (3) under the constraints (4) and (5). \(\epsilon \) in the constraints (5) was run with the initial value of 0 and the increased step size of 0.05. Figure 2 shows different values of \(\epsilon \) and corresponding standard deviations of weight values. In this study, we chose \(\epsilon =0.85\) for Bank a, \(\epsilon =0.65\) for Bank b, and \(\epsilon =0.70\) for Bank c so that the corresponding standard deviations of weight values are in the middle area of its possible range. Table 4 displays the optimal set of weights for each bank at the chosen \(\epsilon \). As a final result, the CICI values of Bank a, Bank b, and Bank c were determined to be 4.15, 4.35, and 4.30, respectively using each bank’s optimal sets of weights. According to that, Bank b is the most innovative bank among the three evaluated bank. This results were verified by comparing with the ranking of the same three banks based on subjective models in [23].

Hierarchical structure of IMPs and sub-IMPs for evaluating IC in banking

Different \(\epsilon \) values and corresponding standard deviations of weight values

Weights of IMPs in three banks in Vietnam

5 Conclusion

This study proposes a data-driven weighting method based on DEA to solve a multi-criteria problem that is then applied in evaluating the IC of the three banks in Vietnam. The proposed method can determine the optimal set of weights for maximizing each bank’s IC. This way contributes an objective evaluation or ranking approach on IC without bias toward any banks. Based on the optimal set of weights of each bank, we can point out which IMPs each bank is focusing on (strengths) or ignoring (weaknesses). Particularly, by applying the proposed method in the case of the three banks in Vietnam, we found distinctive IMPs of each bank as follows:

-

Bank a: This bank was found to pay attention to only two IMPs (MK “managing knowledge” and MS “managing strategies”) while almost neglecting the rest of IMPs. It must be noted that most IMPs in Bank a have the least implemented levels among the three banks, except for MK. Generally, the IC level of Bank a is lower than the other two banks.

-

Bank b: Except for MI “managing ideas” where its score is a bit lower than other IMPs, Bank b widely develops other IMPs, especially focuses on managing strategies, marketing, R&D, managing technologies, and improving processes. Most IMPs have the implemented levels generally higher than the other banks. Globally, this bank may be considered as being most seriously pursuing innovation activities.

-

Bank c: This bank puts more efforts into managing resources, managing strategies, and managing portfolio while keeping good levels on improving processes, marketing, interactive learning, and managing knowledge. It is at low levels in organizing, managing ideas, R&D, and managing technologies.

-

It can also be noticed that all of the three banks, specially the most innovative bank (Bank b) give prominence to managing strategies in innovation management, which proves that strategies management is an important practice in innovation management in Vietnamese banks. The above-mentioned points are graphically described in Fig. 3.

The research results also reveal the ranking of the three banks based on their IC. In details, Bank b is the most innovative bank among the three banks, the next is Bank c, and Bank a was ranked last. The findings provide a basis for bank managers to improve their innovation management policies to upgrade their IC. Specifically, to increase the IC level, a bank can strengthen its IC by prioritizing to allocate more resources into the most important IMPs that have the strongest weights such as strategies management, marketing, and R&D as the most innovative bank (Bank b) does.

This study is limited by the a small sample size with only three banks in Vietnam. The future study should use a bigger sample size to establish a greater degree of applicability and validity of the proposed method. In addition, the discriminating power among the evaluated banks is still low (in case of comparing the IC levels between Bank b and Bank c). Considerably more work will need to be done to develop other methods that can create a more distinguishable ranking, for example using multi-objective approach.

References

Crossan, M.M., Apaydin, M.: A multi-dimensional framework of organizational innovation: a systematic review of the literature. J. Manage. Stud. 47(6), 1154–1191 (2010)

Soliman, F.: Does innovation drive sustainable competitive advantages? J. Mod. Account. Audit. 9(1), 130–143 (2013)

Laforet, S.: A framework of organisational innovation and outcomes in SMEs. Int. J. Entrepreneurial Behavior Res. 17(4), 380–408 (2011). https://doi.org/10.1108/13552551111139638

Slater, S.F., Hult, G.T.M., Olson, E.M.: Factors influencing the relative importance of marketing strategy creativity and marketing strategy implementation effectiveness. Ind. Mark. Manage. 39(4), 551–559 (2010)

Mone, M.A., McKinley, W., Barker, V.L., III.: Organizational decline and innovation: a contingency framework. Acad. Manage. Rev. 23(1), 115–132 (1998)

Raghuvanshi, J., Garg, C.P.: Time to get into the action: unveiling the unknown of innovation capability in Indian MSMEs. Asia Pac. J. Innov. Entrep. 12(3), 279–299 (2018). https://doi.org/10.1108/APJIE-06-2018-0041

Saunila, M., Ukko, J.: A conceptual framework for the measurement of innovation capability and its effects. Balt. J. Manage. 7(4), 355–375 (2012)

Rejeb, H.B., Morel-Guimarães, L., Boly, V., et al.: Measuring innovation best practices: improvement of an innovation index integrating threshold and synergy effects. Technovation 28(12), 838–854 (2008)

Boly, V., Morel, L., Camargo, M., et al.: Evaluating innovative processes in French firms: methodological proposition for firm innovation capacity evaluation. Res. Policy 43(3), 608–622 (2014)

Wang, T., Chang, L.: The development of the enterprise innovation value diagnosis system with the use of systems engineering. In: Proceedings 2011 International Conference on System Science and Engineering, pp. 373–378. IEEE (2011)

Yam, R.C., Lo, W., Tang, E.P., Lau, A.K.: Analysis of sources of innovation, technological innovation capabilities, and performance: an empirical study of Hong Kong manufacturing industries. Res. Policy 40(3), 391–402 (2011)

Tidd, J., Thuriaux-Alemán, B.: Innovation management practices: cross-sectorial adoption, variation, and effectiveness. R&D Manag. 46(S3), 1024–1043 (2016)

Liu, L., Jiang, Z.: Influence of technological innovation capabilities on product competitiveness. Ind. Manag. Data Syst. 116(5), 883–902 (2016)

Lawson, B., Samson, D.: Developing innovation capability in organisations: a dynamic capabilities approach. Int. J. Innov. Manag. 5(03), 377–400 (2001)

Koc, T., Ceylan, C.: Factors impacting the innovative capacity in large-scale companies. Technovation 27(3), 105–114 (2007)

Guan, J.C., Yam, R.C., Mok, C.K., Ma, N.: A study of the relationship between competitiveness and technological innovation capability based on DEA models. Eur. J. Oper. Res. 170(3), 971–986 (2006)

Wang, C.-H., Lu, I.-Y., Chen, C.-B.: Evaluating firm technological innovation capability under uncertainty. Technovation 28(6), 349–363 (2008)

Yang, C., Zhang, Q., Ding, S.: An evaluation method for innovation capability based on uncertain linguistic variables. Appl. Math. Comput. 256, 160–174 (2015)

Sumrit, D., Anuntavoranich, P.: Using DEMATEL method to analyze the causal relations on technological innovation capability evaluation factors in Thai technology-based firms. Int. Trans. J. Eng. Manag. Appl. Sci. Technol. 4(2), 81–103 (2013)

Saisana, M., Tarantola, S.: State-of-the-art report on current methodologies and practices for composite indicator development, vol. 214. Citeseer (2002)

Cheng, Y.-L., Lin, Y.-H.: Performance evaluation of technological innovation capabilities in uncertainty. Proc. Soc. Behav. Sci. 40, 287–314 (2012)

Chung, W.: Using DEA model without input and with negative input to develop composite indicators. In: 2017 IEEE International Conference on Industrial Engineering and Engineering Management (IEEM), pp. 2010–2013. IEEE (2017)

Ngo, N.D.K., Le, T.Q., Tansuchat, R., Nguyen-Mau, T., Huynh, V.-N.: Evaluating innovation capability in banking under uncertainty. IEEE Trans. Eng. Manag. 1–18 (2022). https://doi.org/10.1109/TEM.2021.3135556

Damanpour, F.: Organizational complexity and innovation: developing and testing multiple contingency models. Manag. Sci. 42(5), 693–716 (1996)

Rogers, M.: The definition and measurement of innovation. Melbourne Institute of Applied Economic and Social Research, University of Melbourne, Melbourne (1998)

Du Plessis, M.: The role of knowledge management in innovation. J. Knowl. Manag. 11(4), 20–29 (2007)

Baregheh, A., Rowley, J., Sambrook, S.: Towards a multidisciplinary definition of innovation. Manag. Decis. 47, 1323–1339 (2009)

Sen, F.K., Egelhoff, W.G.: Innovative capabilities of a firm and the use of technical alliances. IEEE Trans. Eng. Manag. 47(2), 174–183 (2000)

Christensen, J.F.: Asset profiles for technological innovation. Res. Policy 24(5), 727–745 (1995)

Szeto, E.: Innovation capacity: working towards a mechanism for improving innovation within an inter-organizational network. TQM Mag. 12(2), 149–158 (2000)

Burgelman, R., Christensen, C., Wheelwright, S.: Strategic Management of Technology and Innovation. Mc-Graw-Hill, New York (2009)

Wang, C.L., Ahmed, P.K.: The development and validation of the organisational innovativeness construct using confirmatory factor analysis. Eur. J. Innov. Manag. 7(4), 303–313 (2004)

Guan, J., Ma, N.: Innovative capability and export performance of Chinese firms. Technovation 23(9), 737–747 (2003)

Parameswar, N., Dhir, S., Dhir, S.: Banking on innovation, innovation in banking at ICICI bank. Glob. Bus. Organ. Excell. 36(2), 6–16 (2017)

Ikeda, K., Marshall, A.: How successful organizations drive innovation. Strategy Leadersh. 44(3), 9–19 (2016). https://doi.org/10.1108/SL-04-2016-0029

Tajeddini, K., Trueman, M., Larsen, G.: Examining the effect of market orientation on innovativeness. J. Mark. Manag. 22(5–6), 529–551 (2006)

Drejer, I.: Identifying innovation in surveys of services: a Schumpeterian perspective. Res. Policy 33(3), 551–562 (2004)

Charnes, A., Cooper, W.W., Rhodes, E.: Measuring the efficiency of decision making units. Eur. J. Oper. Res. 2(6), 429–444 (1978)

Zhou, P., Ang, B., Poh, K.: A mathematical programming approach to constructing composite indicators. Ecol. Econ. 62(2), 291–297 (2007)

Hatefi, S., Torabi, S.: A common weight MCDA-DEA approach to construct composite indicators. Ecol. Econ. 70(1), 114–120 (2010)

Cooper, R.G., Edgett, S.J., Kleinschmidt, E.J.: Benchmarking best NPD practices-II. Res. Technol. Manag. 47(3), 50–59 (2004)

Easingwood, C.J.: New product development for service companies. J. Prod. Innov. Manag. 3(4), 264–275 (1986)

Oke, A.: Innovation types and innovation management practices in service companies. Int. J. Oper. Prod. Manag. 27(6), 564–587 (2007)

Kuczmarski, T.: Winning new product and service practices for the 1990s. Kuczmarski & Associates, Chicago (1994)

Cooper, R.G., Edgett, S.J., Kleinschmidt, E.J.: Benchmarking best NPD practices-I. Res. Technol. Manag. 47(1), 31–43 (2004)

Griffin, A.: PDMA research on new product development practices: updating trends and benchmarking best practices. J. Prod. Innov. Manag. Int. Publ. Prod. Dev. Manag. Assoc. 14(6), 429–458 (1997)

Yam, R.C., Guan, J.C., Pun, K.F., Tang, E.P.: An audit of technological innovation capabilities in Chinese firms: some empirical findings in Beijing, China. Res. Policy 33(8), 1123–1140 (2004)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2022 Springer Nature Switzerland AG

About this paper

Cite this paper

Ngo, N.D.K., Huynh, VN. (2022). A Data-Driven Weighting Method Based on DEA Model for Evaluating Innovation Capability in Banking. In: Honda, K., Entani, T., Ubukata, S., Huynh, VN., Inuiguchi, M. (eds) Integrated Uncertainty in Knowledge Modelling and Decision Making. IUKM 2022. Lecture Notes in Computer Science(), vol 13199. Springer, Cham. https://doi.org/10.1007/978-3-030-98018-4_5

Download citation

DOI: https://doi.org/10.1007/978-3-030-98018-4_5

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-98017-7

Online ISBN: 978-3-030-98018-4

eBook Packages: Computer ScienceComputer Science (R0)