Abstract

Solving complex credit-risk economic capital models requires the use of simulation methods. This powerful technique is nonetheless computationally slow. For certain applications—such as loan pricing and stress testing—it is far too slow to be of practical use. This creates a frustrating conceptual impasse: the only practicable solution method for our model stands in the way of our ability to perform critical applications. This chapter—to resolve this practical problem—constructs a fast, accurate, semi-analytic, instrument-level approximation of both default and migration economic capital. This is accomplished by exploiting our knowledge of the economic-capital model to build a structurally motivated statistical model. Not only does this approach facilitate a number of productive computations, it also provides additional insight into our base credit-risk framework.

It has long been an axiom of mine that the little things are infinitely the most important.

(Arthur Conan Doyle)

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

As the previous chapter makes abundantly clear, the computation of credit-risk economic capital is, irrespective of the approach taken, computationally intensive and slow. This is simply a fact of life. Clever use of parallel-processing and variance-reduction techniques can improve this situation, but they cannot entirely alleviate it. In some settings, however, speed matters. It would be extremely useful—and, at times, even essential—for certain applications, to perform large numbers of quick credit-risk economic-capital estimates. Two classic applications include:

-

Loan Pricing: computing the marginal economic-capital impact of adding a new loan, or treasury position, to the current portfolio; and

-

Stress Testing: assessing the impact of a (typically adverse) global shock to the entire portfolio—or some important subset thereof—upon one’s overall economic-capital assessment.

The needs of these applications are slightly different. Loan pricing examines a single, potential addition to the lending book; not much change is involved, but the portfolio perspective is essential.Footnote 1 Time is also very much of the essence. One simply cannot wait for 90 minutes (or so) every time one wishes to consider an alternative pricing scenario.Footnote 2 Stress-testing involves many, separate portfolio and instrument-level calculations; significant portfolio change and dislocation generally occurs.Footnote 3 One might be ready to wait a few days for one’s stress-testing results, but if one desires frequent, sufficiently nuanced, and regular stress analysis, such slowness is untenable. To be performed effectively—albeit for different reasons—both applications thus require swiftness.

Sadly, speed of execution is one element woefully lacking from our large-scale industrial credit-risk economic capital model. What is to be done? Since it is simply unworkable to use the simulation engine to inform these estimates, an alternative is required. The proposed solution involves the construction of a fast, first-order, instrument-level approximation of one’s economic-capital allocation. Approximation suggests the presence of some error, but in both applications an immediate, but slightly noisy, estimate is vastly superior to a more accurate, but glacially slow value.

This might seem a bit confusing. The economic-capital model is, itself, a simulation-based approximation. We would, in essence, be performing an approximation of an approximation. While there is some truth to this criticism, there is no other reasonable alternative. Failure to find a fast, semi-analytic, approximation would undermine our ability to sensibly employ our credit-risk economic capital model in a few important, and highly informative, applications.

Such an approach to this underling problem is not without precedent. Bolder and Rubin [7], for example, investigate a range of flexible high-dimensional approximating functions—in a rather different analytic context—with substantial success. Ribarits et al. [25] present—based on Pykhtin [23]—precisely such an economic-capital approximation for loan pricing. This work is a generalization of the so-called granularity adjustment—initially proposed by Gordy [13]—for Pillar II concentration-risk calculations.Footnote 4 This regulatory capital motivated methodology, while powerful, is not directly employed in our approach for one simple reason: we wish to tailor our approximation to our specific modelling choice and parametrization. A second reason is that we will require separate, although certainly related, approximations for both default and credit-migration risk. The consequence is that, although motivated by the general literature, much of this chapter is specific to the NIB setting. It will hopefully, however, stimulate ideas and provide a conceptual framework for others facing similar challenges.

1 Framing the Problem

Before jumping into specific approximation techniques, let’s try to frame the problem. To summarize, we require a fast assessment of the marginal economic-capital consumption—at a given point in time—operating at the individual loan and obligor level. We may ultimately apply it at the portfolio level, but it needs to operate at the individual exposure level.Footnote 5 The plan is to construct a closed-form—or, at least, semi-analytical—mathematical approximation of the economic-capital model allocations. There are, fortunately, many possible techniques in the mathematical and statistical literature that might be useful in this regard. Broadly speaking, there are two main approaches to such an approximation:

-

1.

a structural description; or

-

2.

a reduced-form—or, empirically motivated—approach.

The proposed economic-capital approximation methodology in this chapter is based, more or less, on the former method. That said, this need not be so. The sole selection criterion—ignoring, for the moment, speed—is predication accuracy. This suggests that we might legitimately consider reduced-form techniques as well.

This brings us to the general approximation problem. Let us begin by defining \(y\in \mathbb {R}^{I\times 1}\) as the vector-quantity that we are trying to approximate; this is basically our collection of I economic-capital estimates at a given point in time. We further denote \(X\in \mathbb {R}^{I\times \kappa }\) as a set of explanatory, or instrument, variables that can act to describe the current economic-capital outcomes.Footnote 6 Good examples of instruments would include the size of the position, its default probability, assumed recovery rate, industrial sector, and geographic region. Our available inputs thus involve I economic-capital allocations along with κ explanatory variables for each observation.

The (slow) simulated-based economic-capital model, f(X), is a complicated function of these explanatory variables. Conceptually, it is a mapping of the following form:

where 𝜖 is observation or measurement error.Footnote 7 In words, therefore, f(X) is basically the economic-capital model. Regrettably, we do not have a simple description of f; if we did, of course, we would not find ourselves in this situation! Practically, our approximation is attempting to bypass the unknown function, f, and replace it with an approximator. Conceptually, this replaces Eq. 5.1 with

where we denote our approximation as \(\hat {f}(X)\). The trick, and our principal task in this chapter, is to find a sensible, rapidly computed, and satisfactorily accurate choice of \(\hat {f}\). There are no shortage of potential candidates. Function approximation is a heavily studied area of mathematics. Much of the statistics literature relating to parameter estimation touches on this notion and the burgeoning discipline of machine learning is centrally concerned with prediction of (unknown and complicated) functions.Footnote 8

If y is the true model output, then our approximation can be characterized as:

We write this value without error, which is a bit misleading. There is, quite naturally, error associated with our new approximation. We prefer, however, to describe this directly in comparison to the observed y. Indeed, a useful choice \(\hat {f}\) involves a small distance between y and \(\hat {y}\); this includes the approximation error. There are a variety of ways to measure this distance, but one common, and useful, metric is defined as:

This is referred to as the mean-squared error. It is basically the average distance between the sum of the squared approximation errors. Squaring the errors has the desirable property of transforming both over- and underestimates into positive figures; it also helpfully generates a continuous and differentiable error function. The measurement error is also clearly inherited from the original (unknown) function f. The bottom line is that we seek an approximator, \(\hat {y}\), that keeps the error definition in Eq. 5.3 at a relatively acceptable level.

With some patience, the mean-squared error can also tell us something useful about our problem. Employing a few algebraic tricks, we may re-write the previous expression as:

Our measure of distance between the observed and approximated economic-capital values can be generally categorized into two broad categories: reducible and irreducible error.Footnote 9 Reducible error, which itself can be broken down into variance and bias—can be managed with intelligent model selection. Irreducible error stems from observation error; in our case, this relates to simulation noise.Footnote 10 This is something we need to either live with or, when feasible, actively seek to reduce. Bias describes fundamental differences between our approximation and true model. We might, for example, use a linear model to approximate something that is inherently non-linear. Such a choice would introduce bias. Variance comes from the robustness of our estimates across datasets. It seeks to understand how well, if we reshuffle the cards and generate a new sample, our approximator might perform. A low-variance estimator would be rather robust to changes in one’s observed data-set.

Statisticians and data scientists speak frequently of a variance-bias trade-off. This implies that simultaneous reduction of both aspects is difficult (or even impossible). Statisticians, with their focus on inference, tend to accept relatively high bias for low variance. Machine-learning algorithms, due to their flexibility, tend to have lower bias, but the potential for higher bias.Footnote 11 The proposed approximation model—leaning towards the classical statistical school of thought—employs a multivariate linear regression with structurally motivated response variables. In principle, therefore, this choice involves a reasonable amount of bias. Our credit-risk economic-capital model is not, as we’ve seen, particularly linear in its construction. The implicit logic behind this choice, of course, is that it provides a stable, low-variance estimator.

Colour and Commentary 53

(Approximating Economic Capital) : There is a certain irony in expending—in the previous chapters—such a dramatic amount of mental and computational resources for the calculation of economic capital, only to find it immediately necessary to approximate it. This is the dark side associated with the centrality of credit-risk economic capital. Determining the marginal economic-capital consumption associated with adding (or changing) one, or many, loans has a broad range of useful applications. Examples include risk-adjusted return computations, loan pricing, stress testing, sensitivity analysis, and even loan impairments. The slowness of the base simulation-based computation makes—using the simulation engine—such rapid and flexible marginal computations practically infeasible. Their impossibility does not, of course, negate their usefulness. As such, the most logical, and pragmatic, course of action is to construct a fast, accurate, semi-analytic approximation to permit such analysis. Moreover, such effort is not wasted. Not only does it facilitate a number of productive computations, but it also provides welcome, incremental insight into our modelling framework.

2 Approximating Default Economic Capital

We’ve established that we need an approximation technique that, given the existing portfolio, can operate at the instrument level. As established in previous chapters, there are two distinct flavours of credit-risk economic capital: default and migration. While we need both, different strategies are possible. We could group the two together and construct a model to approximate the combined default and migration economic capital. Alternatively, we could build separate approximators for each element. Neither approach is right or wrong; it depends on the circumstances. Our choice is for distinct treatment of default and migration risk.Footnote 12 As a consequence, we’ll develop our approximators separately beginning with the dominant source of risk: default.

2.1 Exploiting Existing Knowledge

As a general tenet, if you seek to perform an approximation of some object, it is wise to exploit whatever knowledge you have about it. Specific qualities and attributes about the economic-capital model can thus help inform our approximation decisions. We know that our production credit-risk model is a multivariate t-threshold model. We also know that threshold models essentially randomize the conditional probability of default—and thereby induce default correlation—through the introduction of common systemic variables.Footnote 13 Extreme realizations of these systemic variables push up the (conditional) likelihood of default and disproportionately populate the tail of any portfolio’s loss distribution. This link between systemic factors and tail outcomes seems like a sensible starting point.

This brings us directly to the latent creditworthiness state variable introduced in Chap. 2. To repeat it once again for convenience, it has the following form:

for i = 1, …, I. For our purposes, it will be useful to simplify somewhat the notation and structure of the model. These simplifications will enable the construction of a stylized approximator. In particular, the product of systemic factors and their loadings is, by construction, standard normally distributed; that is, \(\mathrm {B}_i\Delta z\sim \mathcal {N}(0,1)\). To reduce the dimensionality, we simply replace this quantity with a single standard normal random variable, z. Moreover, to underscore the distance to the true model and make it clear we are operating in the realm of approximation, let us set Δw i = υ i and ΔX i = y i. This yields

which amounts to a univariate approximation of our multivariate t-threshold model. Some information is clearly lost with these actions, most particularly relating to regional and sectoral aspects of each credit obligor. This will need to be addressed in the full approximation.

A few additional components bear repeating from Chap. 2. The default event (i.e., \(\mathcal {D}_i\)) occurs if y i falls below a pre-defined threshold, \(K_i=F_{\mathcal {T}_{\nu }}^{-1}(p_i)\) or,

which allows to get a step closer to our object of interest. The default loss for the ith obligor, \(L_i^{(d)}\), can be written as

where \(\mathcal {R}_i\), γ i, and c i denote (as usual) the recovery rate, loss-given-default, and exposure-at-default of the ith obligor, respectively. The d superscript in Eq. 5.9 explicitly denotes default to keep this estimator distinct from the forthcoming migration case; despite the additional notational clutter, it will prove useful throughout the following development. The magnitude of the default loss thus ultimately depends upon the severity of the common systemic-state variable (i.e., z and W) outcomes. Equations 5.6 to 5.9 thus comprise a brief, somewhat stylized representation of our current production model.

The kernel of previous knowledge that we wish to exploit relates to the interaction between systemic variable outcomes and the conditional probability of default. This relationship is captured via the so-called conditional default loss. Conditionality, in this context, involves assuming that our common random variates, z and W, are provided in advance; we will refer to these given outcomes as z ∗ and w ∗. Under this approach to the problem, we can derive a fairly manageable expression for this quantity as

given that υ i follows, by construction, a standard normal distribution. This expression—or, at least, a variation of it—forms the structural basis for much of current regulatory guidance.Footnote 14 Equation 5.10 also plays a central role in our default economic-capital approximation.

To move further, we first need to be a bit more precise on the actual values associated with our conditioning variables. Equation 5.10 applies to any loss associated with arbitrary systemic-variable realizations. If we may select any choice of z ∗ and w ∗—and we’re interested in worst-case default losses—why not pick really bad ones? Indeed, why not use the same level of confidence (i.e., 0.9997) embedded in our economic-capital metrics, which we will generically denote as α ∗. If we seek an extreme downside observation for the common systemic risk factor, a sensible choice is

where \(\alpha ^*_z\) denotes the confidence level associated with z. For the common mixing variable, a natural choice would be

where again \(\alpha ^*_w\) is separately defined. In principle, we would prefer that \(\alpha ^*_z=\alpha ^*_w\). As is often the case, the situation is a bit more nuanced. While the choice of systemic-state variable outcome is quite reasonable, unfortunately, the value in Eq. 5.12 does not perform particularly well for estimating worst-case default loss. In some cases, it works satisfactorily, whereas in other settings it is far too extreme and leads to dramatic overestimates of the conditional default loss.

This brings us to an interesting insight into the t-threshold model. The larger the confidence interval used to evaluate Eq. 5.12, the smaller the value of the common mixing variable, w ∗. The smaller the w ∗ outcome, the smaller the ratio \(\sqrt {\frac {w^*}{\nu }}\), which in turn modifies the default threshold. Reducing the size of the threshold, essentially amounts to a reduction in the creditworthiness of the obligor; making default more probable.Footnote 15 The conditional default probability associated with extreme outcomes of z ∗ and w ∗ is thus hit from both ends: on one side there is a nasty systemic state variable outcome, while on the other the threshold goal-line has been moved closer. Setting them both to extreme values can, in many cases, lead to really dramatic default losses.

The best way, perhaps, to understand the nature of this calculation is to consider a practical example. Table 5.1 summarizes all of the key inputs for an illustrative, but arbitrary, credit obligor. Three levels of \(\alpha ^*_w\) confidence interval are provided for the w ∗ outcomes, but the z ∗ outcomes are held constant. Key components of the computation are displayed illustrating the impact of w ∗ and the sensitivity of overall results to this choice. Innocently moving \(\alpha ^*_w\) from 0.6667 to 0.9997—all else equal—leads to fairly dramatic increases in the default loss estimate.

Figure 5.1 explores this question in more detail by widening our gaze. It displays, for three different choices of \(\alpha ^*_w\), the normalized estimated and observed default loss values across the entire portfolio.Footnote 16 The clear conclusion is that the estimated value increases steadily—and ultimately rather significantly exceeds the observed outcomes—for larger values of \(\alpha ^*_w\). The degree of sensitivity of the conditional default probability to the choice of confidence level for the mixing variable is rather surprising. It seems that this variable’s principle role is not to generate extreme loss outcomes, but rather simply to induce a joint t distribution; and, as a result, tail dependence.Footnote 17 For the remainder of this analysis, therefore, we will use the more neutral, but slightly conservative, value of \(\alpha ^*_w=0.6667\). Different values are naturally possible, and this is by no means an optimized choice, but it performs quite reasonably.

Choosing \({\alpha ^*_w}\): The preceding graphic displays, for three different choices of \(\alpha ^*_w\) used to identity w ∗, the normalized estimated and observed default loss values. The larger the choice of \(\alpha ^*_w\), the more extreme the default-loss estimates.

Colour and Commentary 54

(The t-threshold Mixing Variable) : In the Gaussian threshold model, the conditional probability of default depends solely on the provided realization of the systemic risk factor (or factors). Intuition about the randomization of the (conditional) default probability—and the inducement of default correlation—is straightforward: extreme systemic factor realizations lead to correspondingly high probabilities (and magnitudes) of default loss. Moving to the t-threshold setting complicates things. A second conditioning variable—the χ 2 -distributed quantity—must also be revealed. One’s first reaction is to simultaneously draw an extreme mixing-variable outcome. Our analysis demonstrates that this yields unrealistically large default loss probabilities. a This appears to suggest that the mixing variable’s role is not to generate extreme outcomes, but rather to alter the joint distribution and induce tail dependence. For this reason, when using the conditional default probability of the t-threshold model for our approximation analysis, we assume a relatively neutral draw from the χ 2 -distributed mixing variable.

aEffectively, extreme mixing variable outcomes pull in the default threshold for all obligors. Combined with a simultaneously bad draw from the systemic state variable, obligors are hit from both sides and the impact is excessive.

2.2 Borrowing from Regulatory Guidance

Equation 5.10 actually turns out to be a critical ingredient of our initial closed-form—although, admittedly simple—approximation of the marginal economic-capital consumption associated with a given exposure. A few additional steps are nonetheless required. Let us define \(\mathcal {A}_i^{(d)}(\alpha ^*)\) as the observed default economic-capital allocation associated with the ith obligor computed at confidence level, α ∗. Recall that economic-capital is, conceptually, written as

For the (Pillar I) computation of minimum regulatory capital requirements—see Chap. 11 for much more on these ideas—the internal ratings-based approach offers the following exposure-level formula for the direct computation of this quantity:

which basically amounts to the difference between conditional and unconditional default loss. This quantity is, in the classical sense, a VaR-related measure of risk.Footnote 18

Exploitation of Eq. 5.14 leads us to the kernel of the approximation method. The mathematical structure of the approximation is

for i = 1, …, I risk-owner risk contributions. To be fair, the previously described unexpected loss expression does not precisely coincide with the regulatory definition in Eq. 5.14. The t-threshold model leads to a few conceptual changes. The most important is the presence of our common mixing variable, w ∗. For this computation, as already indicated, we will set w ∗ at a fixed, reasonably neutral quantity—to induce tail dependence—and treat the \(\alpha ^*_z\) and z ∗ as the true variables of interest.Footnote 19 Collecting our thoughts, Eq. 5.15 is an analytical representation of a regulatory capital, VaR-based economic-capital allocation. The intuition is that a worst-case outcome for the default loss is inferred from a catastrophically bad outcome of the systemic variable, z ∗. Subtracted from this is the expected loss computed by averaging over all possible outcomes of the systemic state variable.Footnote 20

There is a definitional issue associated with the approximation in Eq. 5.15: it is based on the idea of a VaR unexpected-loss estimator. We use, as highlighted in previous chapters, the expected-shortfall metric. Using the definition of expected-shortfall, and applying it to Eq. 5.15, this can be rectified as

There is both good and bad news. The good news is that, when moving to the expected-shortfall setting, the basic form of our approximation is preserved. The bad news is that the integral \(\tilde {p}_i(\alpha ^*_z)\) is not, to the best of our knowledge, available in closed form. Computation of this quantity requires solving a one-dimensional numerical-integration problem. To solve 500+ individual problems, this takes a bit less than 2 seconds. For large-scale approximations—such as stress-testing calculations—this has the potential to slow things down somewhat, but no real damage is involved. For an individual loan, thankfully, this numerical element requires only a fraction of a second.Footnote 21 As a consequence, this semi-analytic twist to our approximation does not delay the associated applications in any appreciable way.

Table 5.2 takes the simple example introduced in Table 5.1 and—with the help of Eqs. 5.10 and 5.16—provides some insight into how well the approximations actually work. The true model-based default economic-capital value is about EUR 4 million amounting to roughly 6\(\frac {1}{2}\)% of the position’s overall exposure. This figure seems sensible for a position falling, albeit slightly, below investment grade. The VaR-based approximation, from Eq. 5.15, also generates an estimate a bit north of EUR 4 million or around 6.7%. The VaR estimator, in this case, thus generates a marginal over-estimate. Incorporation of the expected-shortfall element—using, in this case, the numerical-integration estimator introduced in Eq. 5.16—yields a rather higher estimate of about EUR 5.4 million or in excess of 8%. This represents a rather significant overstatement of the model-based economic capital.

Our simple example illustrates that, as a generic approximation, the presented results appear to be in the vicinity. That said, the VaR estimator seems to outperform the expected-shortfall calculation. To make a more general statement, of course, it is necessary to look beyond a single instance. We need to systemically examine the relationship between actual economic-capital estimates and our approximating expressions. Figure 5.2 consequently compares our regulatory motivated economic-capital approximations—computed with Eq. 5.16—to the true simulation-model outcomes. Since the actual levels of economic capital are unimportant, the results have again been normalized. The left-hand graphic outlines the comparative results on a normalized basis similar to Fig. 5.1. Visually, the agreement appears sensible, although there are numerous instances where individual estimates deviate from the observed values by a sizable margin. Interestingly, at the overall portfolio level, despite the approximation noise, there is a really quite respectable cross-correlation coefficient of 0.98. This suggests that, although Eq. 5.16 may not always capture the level of default risk, it does catch the basic pattern.

Degree of agreement: The preceding graphics, in raw and logarithmic terms, illustrate the degree of agreement between our (normalized) approximation in Eq. 5.16 and the (normalized) observed simulation-based economic-capital contributions. The overall level of linear correlation is fairly respectable.

A related issue is the broad range of economic-capital values. For some obligors, the allocation approaches zero, whereas for others it can be one (or more) orders of magnitude larger. This stems from the exponential form of default probabilities as well as concentration in the underlying portfolio. This fact, combined with the the patchy performance of the approximation in Eq. 5.16, can lead to scaling problems. As a consequence, the right-hand graphic illustrates the approximation fit when applying natural logarithms to both (normalized) observed and approximated default-risk values. This simple transformation smooths out the size dimension and increases the correlation coefficient to 0.99. Although far from perfect, we may nonetheless cautiously conclude that there is some merit to this basic approach.

Colour and Commentary 55

(The Approximation Kernel) : The central component of the default economic capital approximator is pinched directly from the logic employed in the Basel Internal-Rating Based (or IRB) approach. More specifically, worst-case default losses are approximated via the conditional probability of default associated with a rather highly adverse realization of the systemic risk factor. a While sensible and intuitive, this is not an assumption-free choice. As covered in detail in Chap. 11 , Gordy [ 13 ] shows us that the IRB model is only consistent with the so-called single-factor asymptotic risk-factor model. The principal implication is that this modelling choice focuses entirely on systemic risk; it ignores the idiosyncratic effects associated with portfolio concentrations. The strength of this assumption—as well as the concentrations in our real-life portfolio—implies that this base structure can only take us so far. It will be necessary, as we move forward, to adjust our approximation to capture the ignored idiosyncratic elements.

aWe also draw a more neutral-valued χ 2 mixing variable to accommodate the t-threshold structure of our production model.

2.3 A First Default Approximation Model

Raw use of Eq. 5.16 is likely to be sub-optimal. Its high correlation with observed values, however, suggests that it makes for a useful starting point. What we need is the ability to allow for somewhat more approximation flexibility in capturing individual differences. In other words, we seek an approximation model. This is the underlying motivation behind transforming Eq. 5.16 into an ordinary least-squares (OLS), or regression, estimator. The presence of regression coefficients allows us to exploit the promising correlation structure and also increases the overall fit to the observed data.

The basic linear structure follows from Eq. 5.16 and we use the logarithmic operator to induce an additive form as

Equation 5.17 is an approximation. If we re-imagine this linear relationship with an intercept and error, we have

for i = 1, …, I risk-owner risk contributions.Footnote 22 The left-hand side of Eq. 5.18 is a transformation of the observed default economic-capital estimates, while the elements of our approximation from Eq. 5.16 have become additive explanatory variables.

Equation 5.18 directly translates, of course, into the classical ordinary least squares setting and reduces to the familiar model,

where

and

and \(\epsilon ^{(d)}\sim \mathcal {N}(0,\sigma ^2 I)\) for \(\sigma \in \mathbb {R}_+\). The OLS estimator for \(\Xi =\begin {bmatrix}\xi _0 & \xi _1 & \xi _2 & \xi _3 \end {bmatrix}^T\) determined, as usual, through the minimization of (y (d) − X (d) Ξ)T(y (d) − X (d) Ξ) is thus simply the well-known least-squares solution:

Standard errors and test-statistic formulae also follow from similarly well-known results.Footnote 23 As discussed previously, this does not imply that our model is inherently linear, but rather that we are knowingly accepting a certain degree of model bias for low variance and the ability to use statistical-inference techniques.

Table 5.3 summarizes the results of fitting the previously described approximation model to observed economic-capital allocation data associated with an arbitrary date in 2020. All four of the parameter estimates are strongly statistically significant. The actual parameter values are also positive for the conditional default probability, loss-given-default, and exposures, which seems plausible. The R 2 statistic of roughly 0.9 suggests that the amount of total variance explained by a simple linear model is encouraging.

The actual calculation of approximated (i.e., predicted) default-risk values actually involves a small bit of algebraic gymnastics. In particular,

where \(\widehat {\mathcal {E}^{(d)}(\alpha ^*_z)}\) and \(\mathbb {E}\left (L^{(d)}\right )\) denote the I-dimensional vectors of approximated default economic-capital values and expected losses, respectively. Equation 5.23 permits computation of root-mean-squared, mean-absolute and median-absolute error measures. The results are provided, in Table 5.3, in (proportional) percentage terms rather than logarithmic or currency space.Footnote 24 These goodness-of-fit measures—assessing the (in-sample) correspondence between observed and predicated values—unfortunately paint a less rosy picture. The mean-absolute error is roughly 20%; implying that, on average, the approximation misses its mark by about one fifth. If we turn to the median-absolute error, it improves to one tenth; this strongly suggests the presence of a few large outliers. Our suspicion is confirmed with the—notoriously sensitive to outliers—root-mean-squared error taking a dreadful value of 45%.Footnote 25

Figure 5.3 looks into the outlier question more carefully by illustrating the collection of proportional approximation errors.Footnote 26 The left hand graphic indicates a general trend towards over-estimation and a handful of extreme outliers.Footnote 27 The right-hand graphic provides some insight into the outliers; they appear to all relate to small, below average economic-capital allocations. This is one of the dangers of using proportional errors; a large proportional error can, when considered in currency terms, be economically immaterial.

Initial error analysis: The preceding graphics display the model errors—estimated less observed values—organized by both individual credit obligor and normalized default economic capital. The handful of extreme outliers are presented separately.

Despite an R 2 figure exceeding 0.9, there is work to be done; the proportional errors—even when excluding the outliers—are simply too large to be practically useful. Thankfully, there are good reasons to suspect that the model is incomplete. The approximation is founded on a one-dimensional model, which (by construction) completely ignores concentration, provides no information on random recovery, and fails to incorporate a broader default-correlation perspective. Our approximation model can thus be further improved.

Colour and Commentary 56

(A First Default Approximation Model) : Our regulatory capital motivated first-order approximation of default economic capital is readily generalized into a linear regression model. This permits calibration to daily data and provides diagnostics on the strength of specific parts of the approximation. The initial results are mixed. On the positive side, the percentage of variance explained exceeds 90% and the individual regression variables are highly statistical significant. More negatively, proportional goodness-of-fit measures suggest an unacceptable level of inconsistency. Part of the problem is explained by a handful of outliers, but the model also has difficulty with a sizable subset of individual obligors. In many ways, this is not a surprise. The explanatory variables in this initial model capture, literally by their definition, only the systemic aspect of economic capital. This suggests identification and incorporation of idiosyncratic and concentration related explanatory variables as a sensible avenue towards improvement of our initial model.

2.4 Incorporating Concentration

Our first naive default approximation model is unfortunately, in its current form, not quite up to the task. This is not just due to a deficiency of the underlying regulatory capital computation, but it is rather a structural issue. Gordy [13]—in his excellent first-principle analysis of the Basel-IRB methodology—demonstrates that this regulatory formula is equivalent to using Vasicek [28]’s single-factor asymptotic risk-factor model (ASRF). This has two immediate consequences. First, it requires that one’s portfolio is—in practical terms—extremely well diversified across many credit obligors. Second, as the name suggests, there is only a single source of risk. As such, there is simply no mechanism to capture regional, sectoral, or firm-size effects. To be blunt, this implies that our initial model in Eq. 5.18 is simply not equipped to capture concentration effects.

Most real-world financial institutions—and NIB is no exception in this regard—have regional and sectoral concentrations. Ignoring this dimension leads, as became clear in the previous section, to structural bias in our economic-capital approximations. The most natural route, remaining in the regulatory area, would involve the so-called granularity adjustment. This quantity, introduced by Gordy [13], is an add-on to the base regulatory capital computation to account for concentration.Footnote 28 After significant experimentation, we rejected this path. The principal issue is that it does not (easily, at least) have the requisite flexibility to handle either multiple risk factors or readily incorporate regional and sectoral information.Footnote 29

We opt to follow an alternative, and perhaps more intuitive, strategy. The idea is to assign a concentration score to each individual set of lending exposures sharing similar regional and structural characteristics. We can then include this score as an explanatory variable in our regression model in Eq. 5.18. If done correctly, this would help to incorporate important idiosyncratic features of one’s exposures into our approximation.

There is a rich literature on concentration. Concentration and Lorenz curves, Herfindahl-Hirschman indices and Gini coefficients are popular tools in this area.Footnote 30 The challenges with these methods, for our purposes, are twofold. First, they require full knowledge of the economic-capital weights, which will not always be (logically) available to us. Second, and perhaps more importantly, we seek a concentration measure that incorporates aspects of our current model with a particular focus on sectoral and regional dimensions.

The proposed score, or index, is a function of three pieces of information about the obligor. These include:

-

1.

geographic region;

-

2.

industrial sector; and

-

3.

public-sector or corporate status.

The measure is specialized to the current credit-risk economic-capital model’s factor structure. It does not stem from any current literature, but should rather be viewed as something of a heuristic concentration metric.

We take a slow, methodical, and constructive approach to development of our concentration metric. The first step in the fabrication of our index begins by assigning, at a given point in time, total portfolio exposure (i.e., exposure-at-default) to our J systemic state variables. Since our I credit obligors may simultaneously be members of both a region and an industrial sector, managing this seems a bit challenging. How, for example, do we allocate our exposure to these risk factors? The solution is to use the factor loadings—these quantities determine the relative importance of the region and industry systemic factors. Recall, from Chap. 3, that one half of an obligor’s weight is allocated to its geographic region, while the remaining half is assigned to its industrial sector. At most, therefore, an individual obligor’s exposure can be assigned to two distinct factors. A public-sector entity, which has no obvious industrial classification, receives a full weight to its region. An advantage of this approach is the incorporation of the obligor’s factor loadings (indirectly) into our index.

Mathematically, this jth risk factor’s exposure assignment—which we will denote as \(\bar {\mathcal {V}}_j\)—is thus simply,

for j = 1, …, J and where, as usual, c i denotes the ith obligor’s exposure at default. In other words, we basically weight the individual exposure estimates by their factor loadings. In practice, this is a very straightforward matrix multiplication,

where \(\bar {\mathcal {V}}\in \mathbb {R}^{J\times 1}\), \(c\in \mathbb {R}^{I\times 1}\) are \(\mathrm {B}\in \mathbb {R}^{I\times J}\).Footnote 31 One might be tempted to replace exposure with economic capital (i.e., \(\mathcal {E}_i(\alpha ^*)\)) in Eq. 5.26; it is, in fact, economic-capital concentration that we seek to describe. This turns out to be a bad idea. Were we to use economic-capital in the construction—even indirectly—in the establishment of our concentration metric, we would find ourselves awkwardly having economic-capital embedded in both sides of our regression relationship. Lesser indiscretions have been classified as a criminal act in statistical circles.

Figure 5.4 summarizes, for an arbitrary portfolio during 2020, the percentage allocation of exposure—following from Eq. 5.26—to our J = 24 regional and sectoral categorizations. Since the actual amounts and systemic-risk factor identities are relatively unimportant—but we wish to be able to compare to further transformations—the values are illustrated in numbered percentage terms. The top four categories consume almost half of the total exposure. While concentration is typical in most real-life commercial lending and investment portfolios, we should be cautious to read too much into Fig. 5.4. In this intermediate step, we use only the relatively uninformative factor loadings.

Exposure by risk factor: The preceding graphic displays, for an arbitrarily selected portfolio from 2020, the percentage factor-loaded exposure allocations by systemic risk factor computed using Eq. 5.26.

Having used factor loadings to aggregate portfolio exposure, the next step involves the incorporation of the systemic-factor dependence structure. Technically, this takes the form of a projection. In particular, the next step is

where \(\Omega \in \mathbb {R}^{J\times J}\) is the factor-correlation matrix estimated in Chap. 3 and \(\tilde {\mathcal {V}}\in \mathbb {R}^{J\times 1}\) is a projected vector of exposure amounts. Technically, \(\tilde {\mathcal {V}}\) is a linear projection of \(\bar {\mathcal {V}}\) using the projection matrix, Ω—it is essentially a linear (dimension-preserving) mapping from \(\mathbb {R}^{J\times 1}\) to \(\mathbb {R}^{J\times 1}\). If all of the systemic factors were to be orthonormal, then Ω would be an identity matrix, and the original exposure figures would be preserved. If there is strong positive correlation between the systemic risk factors, conversely, we would expect to see a relative increase in the relative allocation to each risk-factor category.

To see the implications of projecting correlation information onto our factor-arranged exposure outcomes, let’s directly compare the allocations \(\bar {\mathcal {V}}\) and \(\tilde {\mathcal {V}}\) in percentage terms. These results are summarized in Fig. 5.5. Projecting the correlation matrix onto the exposure amounts clearly, and dramatically, changes the concentration profile. Specifically, projecting \(\bar {V}\) flattens out the profile implying, when taking into account factor correlations, that the deviations in concentration are rather different than those suggested by the factor-loading-driven result in Fig. 5.4.

Incorporating systemic dependence: The preceding graphic reproduces the percentage factor-loaded exposure allocations from Fig. 5.4, but also adds in the percentage correlation-matrix projected outcomes from Eq. 5.27. The positively correlated risk-factor system flattens out the concentration profile.

What exactly is going on? The answer, of course, begins with the structure of the systemic risk-factor correlation matrix itself. The risk factors are, as indicated and discussed in previous chapters, a positively correlated system. We can make this a bit more precise. Using an eigenvalue decomposition, it is possible to orthogonalize a correlation matrix into a set of so-called principal components.Footnote 32 A useful byproduct of this computation is that one can estimate the amount of variance, in the overall system, explained by each individual orthogonal factor. This provides useful insight into the degree of linear correlation between the raw variables in one’s system. Table 5.4 reviews the results of this analysis—applied to our factor correlation matrix, Ω—for the five most important orthogonal factors. The single, most important, orthogonal factor explains in excess of 50% of the overall variance, while the top five (of 24) principal components cover about three quarters of total system variance.

The results in Table 5.4 strongly underscore the rather dependent nature of our risk-factor system and help explain Fig. 5.5. A few systemic risk factors appear to demonstrate a high degree of correlation when we simply sum over the exposures. Controlling for the (generally high) level of linear dependence between these individual systemic risk factors, however, is essential to capturing the model’s picture of portfolio concentration.

The final step involves the transformation of the individual values in Eq. 5.27 into a readable and interpretable index. This basically amounts to normalization; it is consequently transformed into a value in the unit interval as,

Other normalizations are certainly possible. The largest concentration index value takes, of course, a value of unity. \(\hat {\mathcal {V}}_j\) thus represents the final concentration-index value for the jth risk factor.

Figure 5.6 illustrates, using Eq. 5.28, the set of J distinct concentration index values displayed in descending order. These values are, once again, conditional on our arbitrary 2020 portfolio, although the results do not appear to vary considerably across time. This is certainly due to high levels of persistence in the portfolio and infrequently updated through-the-cycle parameters.Footnote 33 Actual concentration values for a given risk-owner, or exposure, fall in the range [0.36,1] with a mean of about 0.75. The ordering is broadly similar to that observed in Fig. 5.4, but there are a few surprises.

The concentration index: The preceding graphic displays—conditional on our arbitrarily selected portfolio from 2020—the set of J distinct concentration index values arranged in descending order.

A separate concentration index is required for each individual credit obligor, but there are only J concentration-index values. The factor-loading matrix comes, once again, to the rescue by offering a logical approach to allocation of the sectoral and regional concentration values to the obligor level. Practically, this amounts to (yet) another matrix multiplication,

where \(\mathcal {V}\in \mathbb {R}^{I\times 1}\) is the final concentration index. Each element of \(\mathcal {V}\) thus provides some assessment of the relative concentration of this individual position. The larger the value, of course, the more a given position leans towards the portfolio’s inherent concentrations.

Having constructed the concentration index outcomes, it may still not be immediately obvious what is going on. To provide a bit more transparency, and hopefully insight, we will begin from Eq. 5.29, and gradually work forward as follows, while keeping all the individual ingredients

An element in the preceding decomposition of the \(\mathcal {V}\) computation should look familiar. \(\mathrm {B} \Omega \mathrm {B}^T\in \mathbb {R}^{I\times I}\) is the normalized, factor-loaded, systemic risk-factor correlation matrix. A standardized factor-loaded correlation matrix is thus projected onto the vector of exposure contributions, c, to yield our proposed concentration index. While not perfect, it does appealingly capture a number of key elements of concentration: current portfolio weights, systemic factor loadings, and the correlation structure of these common factors.

Colour and Commentary 57

(Indexing Concentration) : A central task of the credit-risk economic-capital simulation engine is to capture the interplay between diversification and concentration in one’s portfolio. This aspect needs to be properly reflected in any approximation method. It takes on particular importance given our previous decision to lean heavily upon a regulatory motivated approximation that entirely assumes away idiosyncratic risk. A possible solution to this question involves the construction of a concentration index, which can act as an additional explanatory variable in our regression model. Our proposed choice involves a linear projection of the individual credit obligor exposures at default. The projection matrix is a function of the (normalized) factor loadings and the factor correlation. In this way, the resulting index directly incorporates three important drivers of concentration risk: the factor loadings, systemic correlations, and the current portfolio composition.

2.5 The Full Default Model

We’ve clearly established the need to incorporate additional idiosyncratic explanatory variables into our base regression model. The previously defined concentration index is a natural candidate; there are many others. Indeed, there is no shortage of possibilities. This means that model selection is actually hard work. The consequence is a very large set of possible extensions and variations to consider.Footnote 34 This situation can only be resolved with a significant amount reflection, examination of error graphics and model-selection criteria as well as trial-and-error. Ultimately, we have opted for six new explanatory variables to add to our original Eq. 5.18. Despite our best efforts, the revised and extended model should not be considered as an optimal choice. It is better to view it as a sensible element of the set of possible approximation models. With this in mind, it is described as

for i = 1, …, I risk-owner risk contributions.

Table 5.5 summarizes the parameter and goodness-of-fit statistics associated with the revised model. Comparing the results to the base approximation summary found in Table 5.3 on page 18, we observe a number of differences. First of all, there is significant improvement in the (in-sample) goodness-of-fit measures. The proportional root-mean squared error is reduced by a factor of five, while our two proportional absolute errors are cut by more than half. The median absolute error is now only about 4% of the base estimate. The amount of variance explained also increases sharply to 0.99. Finally, all of the new parameters are statistically significant and there is no dramatic (economic) change in the ξ 1 to ξ 3 parameters.Footnote 35 By almost any metric, the extended model represents a serious upgrade.

The new explanatory variables warrant some additional explanation beyond the brief descriptions provided in Table 5.5. The concentration index was already defined in the previous section and, as we had hoped, turns out to be extremely statistically significant. It clearly provides additional information to the model not encapsulated in the systemic-risk-focused extreme conditional default probability. The obligor credit rating, entered as an integer from 1 to 20, somewhat surprisingly improves the overall fit. We would expect—and, in fact, find in Fig. 5.7—positive correlation between the credit rating and the extreme conditional default probability. Despite a slight danger of collinearity, the addition of this piece of information appears to improve the overall model.Footnote 36

Default instrument correlation: This heat-map illustrates the cross-correlation between the key explanatory variables included in the extended regression model summarized in Table 5.5.

We also found it extremely useful to add three additional indicator (i.e., dummy) variables. The first identifies public-sector entities in the portfolio as

The second isolates particularly large firms with the following logic:

or, in words, the largest 10% of credit exposures are flagged. The small exposure flag works in the same manner on the smallest 10% of exposures. For completeness, it is defined as

While these three choices are clearly important, statistically significant explanatory variables, it is difficult to directly understand their role. Examination of the initial model results suggests that the regulatory capital computation has particular difficulty with public-sector, unusually large, and quite small exposures. This probably relates to underlying concentration and parameter-selection questions. We can conceptualize these final three explanatory variables as allowing the model to better handle exceptions. These indicator variables also do not, as seen in Fig. 5.7, exhibit much correlation with the other explanatory variables. The only exception is, unsurprisingly, the large-exposure indicator and the exposure-at-default variable.

One area of investigation is conspicuous by its absence: random recovery. Nothing in our instrument-variable selection provides any insight into this important dimension. A number of avenues was nonetheless investigated. Key parameters—such as the shape parameters of the underlying beta distribution or the recovery volatility—were added to the model without success. Modified, more severe, loss-given-default values were also explored—again using the characteristics of the underlying beta distributions—without any improvement in model results. On the contrary, these efforts generally led to a deterioration of the overall fit.

Figure 5.8 revisits the error analysis performed in Fig. 5.3 using our extended regression model summarized in Eq. 5.31. To aid in our interpretation, the original outliers—from the base default model—are also displayed. Although the general pattern is qualitatively similar, the range of estimation error is reduced by an order of magnitude. While much of the impact relates to improved handling of the outliers, there is also a more general effect. The difficulty of approximating small, below-average economic-capital allocations is not entirely resolved; part of the issue relates to the proportional nature of the error measure, but it remains a weakness.

While imperfect, we conclude that this is a satisfactory approximation model. It exploits some basic relationships involved in the computation of economic capital, is relatively parsimonious, and generates a reasonable degree of fit and statistical robustness. Some weaknesses remain; most particularly relatively high cross correlation between a few explanatory variables as well as a tendency to significantly overestimate a subset of below-average exposures.

Colour and Commentary 58

(A Workable Default Approximation Model) : Given the complexity of the credit-risk economic-capital model, we should not expect to be able to construct a perfect approximator. a Exploiting our knowledge of the problem nonetheless allows us to build a regression model with fairly informative systemic and idiosyncratic explanatory variables. The final result is a satisfactory description of the underlying model. Satisfactory, in this context, implies a median proportional approximation error in the neighbourhood of 4%. While a lower figure would naturally be preferable, we can live with this result. Construction of such models, it should be stressed, is not a one-off exercise. The approximation model is re-estimated daily and the error structure is examined within our internal diagnostic dashboards. On an annual basis, a more formal model-selection (or rather verification) procedure is performed. Ultimately, we are always on the lookout for ways to improve this approximation.

aIf we could, then we might wish to dramatically rethink our model-estimation approach.

3 Approximating Migration Economic Capital

The preceding approximation is focused entirely on the notion of credit-risk economic-capital associated with default events. While it might be tempting to fold in the migration element into the previous approximation model, there, at least, two reasonably compelling reasons to separately approximate the default and migration effects. First, although default is a special case of migration, the loss mechanics differ importantly. This makes constructing a joint approximation more difficult. Although presumably still possible, separate structurally motivated approximation models are more natural to construct and easier to follow.

The second reason is more practical. Distinct default and migration models permit autonomous prediction of these two effects. This may be interesting for analytic purposes; understanding the breakdown between these two sources of risk can provide, for example, incremental insight into the model outcomes. It may also be necessary from a portfolio perspective. In certain stress testing or loan-impairment calculations, for example, we may not be directly interested in the migration allocation. In other cases, we may be interested only in migration effects. A joint model would make it difficult to manage such situations.

3.1 Conditional Migration Loss

Having justified this choice, let us turn our attention to a possible migration-approximation model. We begin, as in the default setting, by trying to exploit our knowledge of the basic calculation and adding some structure to the migration problem. Denoting \(L_{i}^{(m)}\) as the credit-migration loss associated with the ith credit obligor at time t + 1, we recall that it has the following form,

where \(\mathbb {S}_i\) is the credit spread, S i,t is the credit state at time t, τ i is the modified spread duration, and c i is the exposure of the ith position. The time-homogeneous credit spread, of course, is determined directly by the credit state.Footnote 37 The spread change (i.e., \(\Delta \mathbb {S}_i\)) is thus determined by any movement in an obligor’s credit state from one time step to the next. The spread movement is then multiplied by the modified spread duration and position exposure to yield an approximation of the migration loss.

Can we construct, using similar logic to the default case, a conditional migration loss estimate? The short answer is yes, there is clearly some conditionality in the migration loss. We will denote, to ease the notation, the current credit state, at time t, as S i0. This is known. The actual loss outcome depends upon the credit-state value at time t + 1; we’ll call this S i+. To formalize this idea, let us rewrite Eq. 5.35 in a similar form and applying the expectation operator to both sides,

While perhaps not earth-shattering, this expression underscores the fact that the only really uncertain element in the credit-migration calculation is the future credit-state value, S i+.Footnote 38 The million dollar question relates to our choice of conditioning variable, s. One option would be to set \(s=\mathbb {E}(S_{i+})\).

For most credit counterparties—save those already at the extremes of the credit scale—credit migration can involve either an improvement or deterioration of their credit quality. This, in turn, implies either profit or loss associated with the associated credit-migration effects described in Eq. 5.36. Naturally, when looking to the extreme tail of the loss distribution, we would expect the vast majority of credit-migration outcomes to involve downgrade, credit-spread widening, and ultimately loss. We will thus, for our purposes, focus our attention predominately on extreme downside outcomes.

Let’s begin with the basics. S i+ is a random variable and its expectation will depend upon an entity’s appropriate transition probabilities. Its unconditional expectation is

recalling that q = 21 is the number of distinct credit states (including default) and where the individual transition probabilities (i.e., the p’s) are simply elements from the S i,tth row of the transition matrix, P. The expected one-step forward credit state is simply the transition-probability-weighted sum of the possible future credit states. Transition matrices nonetheless exhibit a significant amount of inertia.Footnote 39 The actual expected credit state, in one period’s time, is unlikely to stray very far away from the current credit state. Consequently, Eq. 5.37—in its current form—will generally not be terribly informative about credit-migration economic-capital outcomes.

How might we resolve this issue? The worst-case migration loss should logically occur when the (unknown) future credit state, S i+, takes its worst possible level. Under our t-threshold credit risk model, the actual credit-state outcome depends on draws from the systemic-risk and mixing-variable distributions. We might, therefore, employ the same trick as we used in the default setting; select an extreme systemic risk-factor variable outcome, z ∗. The conditional expectation of S i+ for the ith credit obligor, given z ∗ is a better candidate for the as-yet-undetermined s in Eq. 5.36. It can be correspondingly written as

where

is the ith obligor credit-migration threshold for movement into state j.Footnote 40 As in the default setting, we use a fixed, relatively neutral realization of the mixing variable, w ∗. Equation 5.38 is a rather unwieldy expression, but we already have experience with these conditional-default probability expressions and, perhaps most importantly, they are readily and quickly computed.

We are not quite ready for prime-time usage. The approximation in Eq. 5.38 is a bit too conservative; the simple reason is that it includes the default probability. This component, by construction, will be carved out of the credit-migration economic-capital and allocated to the default category. If we exclude the final default term, however, our expectation will lose a significant amount of probability mass. To solve this, we simply rescale our conditional probabilities excluding the default element. This amounts to an expected downside non-default transition. Practically, this is easily accomplished by defining,

for k = 1, …, q − 1 and then writing our (revised) conditional non-default credit state expectation as,

We have thus made a slight, but important change, from the base definition in Eq. 5.38. Equation 5.41 describes the expected (non-default) credit state for the ith obligor in the next period, conditional on an unpleasant realization of the systemic risk factor.Footnote 41 This shift in focus is captured by the use of \(S_{i+}^{(m)}\) rather than the original S i+ notation.

Equipped with this, model consistent, estimator for the worst-case (non-default) credit deterioration, we may return to the business of approximating credit-risk economic-capital allocation. Again, we motivate our approach through the Basel IRB method. If we denote the capital allocation associated with migration risk as \(\mathcal {A}_{i}^{(m)}(\alpha ^*_z)\), we might approximate it as,

Unlike the default case, we ignore the unconditional expected loss. Since it is generally quite close to zero, we exclude it from our basic structure.Footnote 42

While Eq. 5.42 appears to be a sensible construct—built in the image of the default-risk approximation—it has an important potential structural disadvantage. There are only 20 (non-default) credit states that can be forecast with a correspondingly small number of spread outcomes. Equation 5.40 will, without some form of intervention, thus produce only a small number of discrete credit-spread outcomes for a given obligor’s modified spread duration and exposure. The credit-migration economic-capital engine, however, operates under no such constraint. It can provide a (quasi-)continuum of possible migration–risk allocations. This would suggest that our approximation—even if it differs by one notch on the credit-state forecast—can exhibit rather important approximation errors. Our solution is to simply permit non-integer (i.e., fractional) credit-state forecasts and determine the appropriate spread outcome through the use of linear interpolation. This is essentially a trick—a fractional credit rating does not really exist—permitting us to transform our estimator from discrete to continuous space. This small adjustment provides our estimator with significantly more flexibility.

We have also ignored the expected-shortfall dimension. Practically, Eq. 5.42 is a quantile-based estimator. If we wish to consider the expected shortfall metric, then we will need to solve the following integral:

Practically, only a small amount of incremental effort is required to numerically integrate Eq. 5.43. We thus employ the integrated worst-case spread change, \(\Delta \tilde {\mathbb {S}}_i(z^*)\), as the base migration loss estimator found in Eq. 5.43.

To better understand the kernel of our approximation, we return to our simple example introduced in Table 5.1 on page 10. Naturally, we will now consider the case of credit-migration economic capital. Some of the credit obligor’s details are reproduced for convenience and its modified spread duration has also been added. Unsurprisingly, the unconditional expected rating remains extremely close to the original level. Conditional on extreme outcomes of our systemic and mixing variables, however, the expected (or shocked) credit state belongs to PD class 13. If we use the integrated, expected-shortfall form, from Eq. 5.43, this increases to a 13.2 rating. Of course, such a PD categorization does not actually exist. Through appropriate interpolation along the spread curve, however, this leads to a 56 and 63 basis-point credit widening for the VaR-motivated and integrated worst-case spread movements, respectively. These values translate into forecast credit losses of about EUR 0.94 and 1.05 billion. Since the actual economic-capital value is roughly EUR 0.87 million, both of these forecasts appear to overshoot the target.Footnote 43

Figure 5.9 provides a potentially helpful visualization of the difference between unconditional and conditional (non-default) transition probabilities. Using our sample obligor from Table 5.6, the three flavours of transition probability are plotted side-by-side across the entire (non-default) credit spectrum. The unconditional transition probabilities, as one would expect, are roughly symmetric and centred around the current credit state: PD11.Footnote 44 The α ∗ confidence-level (non-default) migration probabilities—both VaR-motivated and integrated from Eqs. 5.42 and 5.43—behave in a decidedly different fashion. The likelihood of remaining in the current credit state is dramatically reduced and the remaining probability mass is skewed strongly toward downgrade. The skew is slightly more pronounced for the integrated conditional transition likelihoods. It is precisely this information that we are attempting to harness for the approximation of credit migration. These worst-case transition probabilities thus—in a manner similar to conditional default probabilities in our earlier discussion—form the kernel of the migration-loss approximation.

Credit-migration conditionality: The preceding figure compares the unconditional transition probabilities to the \(\alpha ^*_z=0.9997\) confidence-level (non-default) conditional transition probabilities for the sample obligor highlighted in Table 5.6. The unconditional, VaR-motivated, and integrated versions of these migration probabilities are displayed. The conditional quantities are, in stark contrast to their rather symmetric unconditional equivalents, skewed towards credit deterioration.

Figure 5.10 generalizes the single obligor example in Table 5.6 to the entire portfolio. As before, the results are provided in raw and logarithmic normalized units. The idea is to help understand the general degree of agreement between our approximation in Eq. 5.43 and the observed simulation-based migration economic-capital contributions. The overall level of linear correlation is fairly respectable at 0.92 and 0.99 on the raw and logarithmic scales, respectively.

Degree of migration agreement: The preceding graphics, in raw and logarithmic normalized units, illustrate the degree of agreement between our approximation in Eq. 5.43 and the observed simulation-based economic-capital contributions. The overall level of linear correlation is fairly respectable, although there is a decided tendency to overstate the level of risk.

Our base migration-risk approximator has, similar to the result from Table 5.6, a decided tendency to somewhat misstate the precise level of risk. This is likely a structural feature of the approach culminating in Eq. 5.43. As in the default setting, conditioning solely on the systemic risk factor ignores idiosyncratic effects. Given the more symmetric nature of migration risk—relative to the skewed nature of default—restricting our approximation to downside systemic risk appears to manifest itself as overly conservative initial estimates. Figure 5.10 nonetheless suggests that, these shortcomings aside, it is a useful starting point.

Colour and Commentary 59

(The Migration Kernel) : The decision to separately approximate migration and default, while sensible, presents a dilemma. We need to identify a reasonable first-order migration-loss approximator. A natural starting point is to lean on the default-approximation kernel and see how it might be generalized. Happily, the notion of a conditional migration loss makes both logical and empirical sense. The only unknown quantity in migration loss is the obligor’s future credit rating. Unconditionally, this is rather uninteresting, but the situation improves if we condition on an extreme outcome of the common systemic risk factor. a Extending this idea leads to downward-skewed transition probabilities as well as worst-case rating downgrade and credit-spread estimates. These quantities are readily combined to produce an entirely reasonable, if somewhat conservative, initial migration-risk economic-capital approximator.

aAs in the default setting, the χ 2-distributed mixing variable is fixed at a fairly neutral value.

3.2 A First Migration Model

It will come as no surprise that we use the same linear regression structure—given its reasonable degree of success—as employed in the default setting. Indeed, we now have all of the necessary constituents to construct a base credit-migration approximation model. Consider the following form:

for i = 1, …, I. Again applying natural logarithms, we have a similar form to the earlier default approximation in Eq. 5.18. This directly translates, of course, into the familiar OLS setting and reduces to the usual linear model,

where

and

As before, we need only employ the standard OLS estimator for \(\Theta =\begin {bmatrix}\theta _0 & \theta _1 & \theta _2 & \theta _3\end {bmatrix}^T\). Although the inputs are rather different, the base migration model is conceptually equivalent to the default case.

Table 5.7 provides the usual summary for our base, structurally motivated, credit-migration model shown in Eq. 5.45. All four regression coefficients are strongly statistically significant. The percentage of variance explained (i.e., R 2) attains a decent level. The other goodness-of-fit measures, however, show room for improvement. The proportional root-mean-squared value of almost 40% is somewhat better than in the base default model, but it suggests the presence of important outliers. Having already been in this situation, let’s skip directly to the extension of Eq. 5.45 to include a wider range of idiosyncratic explanatory variables.

3.3 The Full Migration Model

As in the default case, an extension of the base model is necessary. The full migration-risk regression model—which is once again the result of a significant amount of analysis—is described as:

for i = 1, …, I risk-owner risk contributions. The interesting part of Eq. 5.48 relates to the identity of the additional explanatory variables.

Table 5.8 displays the results of the final credit-migration economic-capital approximation model. All model parameters are statistically significant. Coincidentally, five additional explanatory variables were also selected. As in the default setting, the integer-valued credit rating and the concentration index turn out to be surprisingly useful in explaining credit-migration risk outcomes. Two additional indicator (i.e., dummy) variables also prove helpful. The first identifies public-sector entities in the portfolio exactly as in Eq. 5.32 in the default setting.Footnote 45 The second high-risk indicator is defined as

Obligors at the very low end of the credit spectrum are, as one might expect, dominated by default risk. As a consequence, identifying them for different treatment improves the overall approximation. As before, these indicator variables are based on a certain logic, but their success likely depends on rather complicated non-linear aspects of the production t-threshold model.

The systematic weight parameter, the final addition to our approximating regression, also provides value in describing migration risk. Its role in determining the relative importance of systemic and idiosyncratic factors makes it important in both the migration and default settings. It is excluded in the full default model, because it is ultimately captured by other explanatory variables.

Figure 5.11 provides a heat-map of the cross correlation associated with our migration explanatory variables. The only potential danger point—in terms of multicollinearity—arises between the credit rating and public-sector variables. With this borderline exception, the remaining descriptive variables all appear to capture different systemic and idiosyncratic elements of migration-risk economic capital. This is underscored by the goodness-of-fit measures in Table 5.8. In addition to a fairly healthy increase in the R 2 measure, the proportional root-mean-square errors are reduced by a factor of three; the mean and median absolute errors, perhaps the most important dimensions, are cut in half. The results are broadly comparable—although marginally worse—than the full-default model outcomes presented in Table 5.5.

Migration instrument correlation: This heat-map illustrates the cross-correlation between the key migration risk explanatory variables included in the extended regression model summarized in Table 5.8.

Figure 5.12 concludes our examination of the migration-approximation model through a detailed examination of the error profiles. In particular, it highlights the error plots (estimated less observed) for the base and full migration-risk approximation models. Each perspective considers the individual obligor and (normalized) size dimensions. A small number of model outliers are identified in the base model and inherited in the extended model graphics; in all cases, the additional explanatory variables improve the situation. Overall, a threefold reduction in the scale of error is provided with the extended model. Although it struggles in certain situations, and there is stubborn tendency to overestimate risk, the general performance of the approximation can be considered to be satisfactory.

Migration-error analysis: The preceding graphics highlight the error plots (estimated less observed) for the base and full migration-risk approximation models. Each perspective consider the individual obligor and (normalized) size dimensions. A threefold reduction in the scale of error is provided with the extended model.

Colour and Commentary 60

(A Workable Migration Approximation Model) : Migration-risk economic capital is not easier to predict than its default equivalent. a Analogous to the default case, one can nonetheless construct a fairly defensible regression model involving meaningful systemic and idiosyncratic explanatory variables. The results are satisfactory; in particular, the R 2 approaches 0.98 and the median proportional approximation error comes out—not quite on par with the full default model—at around 9%. Migration risk approximation nevertheless remains a constant struggle. The model is re-estimated daily, parameters are stored in our database, and the results are carefully monitored via our internal diagnostic dashboards. A more formal model-selection procedure is performed on an annual basis.

aTo repeat, if it was, then we could perhaps dispense with our complicated simulation algorithms.

4 Approximation Model Due Diligence

Lawyers talk about the idea of a standard of care and due diligence in a very technical and specific way. These ideas can, if we’re careful with them, be meaningfully applied to the modelling world. We have, as model developers, a certain responsibility to exercise a reasonable amount of prudence and caution in model selection and implementation. Despite having invested a significant amount of time motivating and deriving our approximation models, we cannot yet be considered to have entirely performed our due diligence. The reasons are fairly simple: to this point, we have only examined their performance on an in-sample basis for a single point in time. To appropriately discharge our responsibility for due diligence, this section will address the two following questions:

-

1.

How do our default and model approximations perform over a lengthier time interval?

-

2.

What is the relative performance of our approximations—again over a reasonable length of time—along both the in- and out-of-sample dimensions?

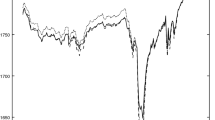

Let’s begin with the first, more easily addressed, issue. The default and migration approximation models were fit—using the ideas from the previous sections—to a sequence of portfolios. Figure 5.13 illustrates the results by focusing on the daily evolution of the four resulting goodness-of-fit criteria over a roughly 130 business-day (i.e., six-month) period. The results are fairly boring; the root-mean, mean-absolute, and median-absolute error estimates remain resolutely stable over the entire period. The default R 2 never deviates, in any meaningful way, from 0.99. The only slightly interesting result is a downward jump in the migration R 2 stemming from a hard-to-approximate addition to the portfolio earlier during our horizon of analysis.

A historical perspective: Using the portfolio data over each date in a six-month period straddling 2020 and 2021, the full default and migration models are estimated and the evolution of our four main goodness-of-fit measures are displayed. The results indicate a relatively high degree of stability over time.