Abstract

The current scenarios for the future of energy seem to suffer a kind of schizophrenia. Some experts do not venture into an uncertain future and prefer to stick to a business-as-usual scenario focused on fossil fuels like they are going to be used in the future with no limitations at all. According to this scenario fossil fuels are not a commodity bound for depletion in the next decades, but they are going to be used forever, and no “energy transition” is in sight for the foreseeable future. Some other experts depict a completely different scenario, where solar energy and electric vehicle are “disruptive” technologies that in a matter of few years will send out of the market both the power utilities like we intend them nowadays and internal combustion engine cars, determining the end of oil-age and nuclear-age. In our opinion both scenarios have some strengths but suffer of many weaknesses, and at the end of the day the “energy transition” from oil-age to renewable-age will happen during this century but probably it will not be so fast as some predict. The paper describes the strengths and weaknesses of the two scenarios and presents a feasible vision for the foreseeable future of world energy. Eventually, current research efforts under way at DIISM-UNIVPM will be presented, starting from the reasons why the topics are substantial for the energy transition to continue with the results expected from these researches.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

1 Introduction

On October 8, 2018 the Intergovernmental Panel on Climate Change (IPCC) released their “Special report on the impacts of global warming of 1.5°C above the pre-industrial levels” [1] where they present four “illustrative model pathways” (here shown as Fig. 1) for CO2 emission reductions that limit global warming to 1.5°C with “no or limited overshoot”.

Breakdown of contributions to global net CO2 emissions in four illustrative model pathways [1] (AFOLU: Agricolture, Forestry and Other Land Use; BECCS: BioEnergy with Carbon Capture and Storage)

According to the report and from an energy-planning point of view the most important mitigation measures for the short-medium term are the reduction in final use demand (32% reduction in 2050 for scenario P1) and the dramatic reduction of coal and oil uses. In other words, a strong decarbonisation.

Pope Francis came almost to the same conclusions in his Encyclical “LaudatoSì” [2] and the recent Club of Rome report on the limits of growth, entitled “Come on!” [3], proposes to completely abandon fossil fuels by 2050 as the only way to limit to 1.5°C the increase of the earth temperature.

All these alarming voices contain the same solution to the problem of climate change: phase out the fossil fuels and move towards renewables energies and a better efficiency in final uses, the so called “energy transition”.

This solution is now feasible, both in technical and in economic terms, and some observers believe that it will be implemented much faster than expected, due to some “technology disruptions” that are already happening. We will describe this scenario as “Disruptive scenario”.

On the other hand, in a kind of schizophrenic syndrome, so many observers think that the current energy scenario, based on fossil fuels, is here to stay as if no other future could be imagined.

Even if the situation is rapidly changing due to the abovementioned climate emergency, there is so much at stake that it is reasonable to think that the oil & gas industry will do whatever it takes to resist any quick change that could send them out of the market. While trying to adapt to the new situation oil & gas companies will try and convince public opinion that they are “too big to fail”, renewables are a just a toy for some “tree huggers” without feet on the ground and there is no way out of fossil fuels; therefore coal (maybe in its “clean” version), oil and natural gas will continue to play the most important roles for years to come. We will describe this scenario as “Business-as-usual scenario”.

As usual, things lie somewhere in between and an important “energy transition” will happen during the next decades. The reasons why the transition will not be so fast like some imagine and will take quite a lot of time are explained in the “Feasible scenario”.

Sideways to the scenarios description, research efforts currently carried out at DIISM-UNIVPM will be briefly described, namely Demand Side Management, Micro-Grids and Energy Storage, Wind Energy and Biofuels from Algae. All these research lines are meant for accompanying the “energy transition” by taking into account, studying in detail and giving feasible solutions to different aspects of energy conversion, transportation and final uses.

2 Disruptive Scenario

It is well known that in one single hour of any given day the Sun radiates to the Earth more energy than mankind can consume in one year.

Going into more detail, the shortwave radiation annually absorbed by the atmosphere and the planet’s surface, after considering that 30% of incoming radiation is reflected by clouds and surfaces, is about 4.1024 J. Energy consumed globally during the first decades of 21st century is of the order of 5.1021 J per annum. So, the energy consumed annually is something less than 0,015% of the solar irradiance [4].

Given these figures, it is immediately evident that exploiting solar energy is not a matter of energy balance but purely a matter of engineering and economics (and policies!).

As a matter of facts, a recent paper developed roadmaps to transform the energy infrastructure of 139 countries to 100% renewables by 2050 creating more than 24 million new jobs worldwide [5].

Putting together a number of considerations about the trends of some industries relevant to energy production, distribution and utilization, Tony Seba elaborated a revolutionary scenario [6, 7] that we will present here as “disruptive” because it is based upon the fast disruption of some consolidated industries, namely the internal-combustion-engine automotive industry, the oil & gas industry and the energy utilities industry, due to some emerging technologies able to present the consumer with more convenient and affordable services (something like what happened in the recent past with digital photography “disrupting” film photography and mobile telephone “disrupting” landline telephone).

Quoting Tony Seba [6], “the Stone Age did not end because humankind run out of stones. It ended because rocks were disrupted by a superior technology: bronze. Stones did not just disappear. They just became obsolete for tool-making purposes in the Bronze age. The horse and carriage era did not end because we ran out of horses. It ended because horse transportation was disrupted by a superior technology, the internal combustion engine.

The idea is not new: Sheikh Ahmed Zaki Yamani, minister of oil and mineral resources of the Kingdom of Saudi Arabia and influential personality within OPEC (Organization of the Petroleum Exporting Countries) during the 1973 oil crisis, used to say the same thing about Stone-age and Oil-age endings. The difference is that, according to this scenario, we are now on the verge of seeing the Oil-age actually end.

Tony Seba continues [6]: “The age of centralized, command-and-control, extraction-resource-based energy sources (oil, gas, coal and uranium) will not end because we run out of petroleum, natural gas, coal or uranium. It will end because these energy sources, the business models they employ, and the products that sustain them will be disrupted by superior technologies, product architectures and business models. Compelling new technologies such as solar, wind, electric vehicles and autonomous (self-driving) cars will disrupt and sweep away the energy industry as we know it”.

The reason why conventional energy framework is inevitably bound for disruption is that distributed solar generation, electric vehicle and autonomous vehicle are information products, subject to Moore’s law, like personal computer and tablets, and governed by information economics and “increasing returns”. Conventional energy resource economics, on the contrary, are governed by “decreasing returns”. They cannot compete with technologies based on increasing returns and their fate is written.

To explain the concept, we quote again Tony Seba [6]: “take the new darling of conventional energy: fracking. To “frack” a single oil or gas well requires hundreds of trucks, millions of gallons of water, and tons of sand with hundreds of chemicals blasted through the ground. You also need thousands of miles of pipelines, massive factories to liquefy or compress the gas before it can be shipped or stored, and massive ports with massive plants to decompress the gas and pipe it again to the power plant. Power generation can start only after all this process is complete.

The return on these wells start decreasing as soon as you start pumping the oil or gas. Despite all the talk of abundance and a “golden age of energy”, fracked wells may deplete by 60–70% the first year alone.

Also production from traditional wells declines by half in about two years, after which the wells drip on for a few more years.

Extraction economics is about decreasing returns:

-

The more you pump, the less each well produces;

-

The more you pump, the less the neighboring well gets;

-

The more you pump, the more each unit of energy will cost in the future.

Solar, electric vehicle and the clean disruption are about increasing returns.

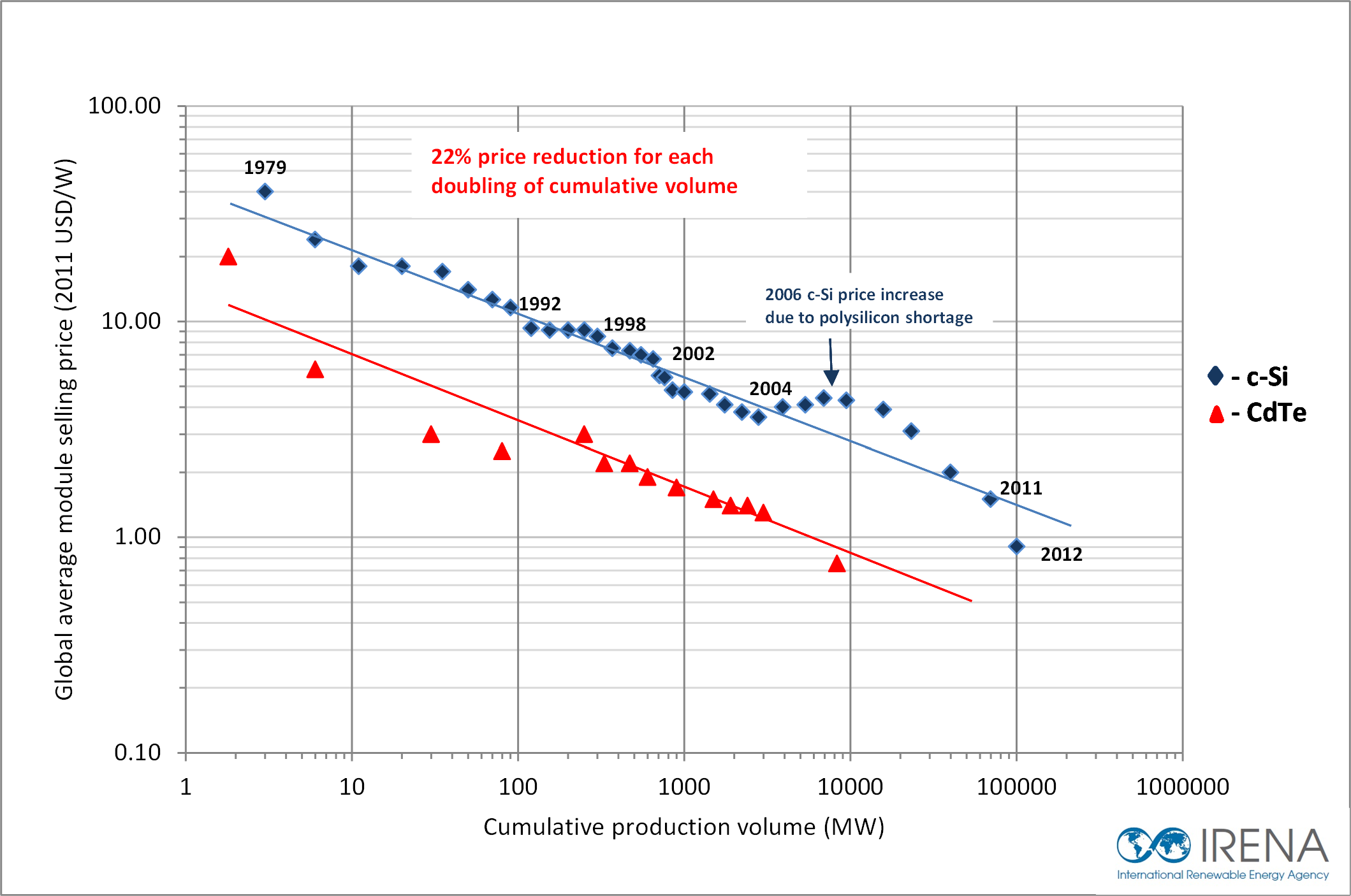

Solar PhotoVoltaic (PV) panels have a “learning curve” of 22%. PV production costs have dropped by 22% with every doubling of the infrastructure (Fig. 2).

Learning curve of PV technology [source: IRENA] (http://www.irena.org/-/media/Images/IRENA/Costs/Chart/Solar-photovoltaic/fig-62.png)

The more demand there is in the market, the less your neighbor pays for her panels, and the more your neighbor benefits. Every time a solar panel is built in Germany, Californians benefit from lower costs when the next solar power plant is built. Every solar panel sold in Australia cuts the cost of the next solar panel in South Africa. Lower costs benefit all new solar customers.

Every large solar power plant in the desert benefits not only the people who buy its power, but everyone who buys solar power in the future.

The higher the demand for solar PV, the lower the cost of solar for everyone, everywhere. Your neighbor benefits, the warehouse owner in Australia benefits, and future buyers of solar benefit from lower costs. All this enables more growth in the solar marketplace, which, because of the solar learning curve, further pushes down costs.

This mutually beneficial arrangement is the opposite of extraction industries like oil & gas. When China’s demand for oil surged in the last decade, world prices for oil went up by a factor of ten. The higher the demand for oil in Beijing, the higher gasoline prices are in Palo Alto and Sydney.

This is not just a theoretical framework. Solar PV has improved its cost basis by more than five thousand times relative to oil since 1970. By 2020, as the market for solar expands, solar will improve its cost basis relative to oil by twelve thousand times.

The economics of energy resource extraction, based on decreasing returns, just cannot compete with the economics of technology industries and its increasing returns.

The fossil fuels industry is pushed not just to extract more wells but to dig deeper, use harsher chemicals and create more wastelands. The fuel industry has to do this just to stay afloat. The BP Gulf Oil disaster and the monstrosity of Alberta Oil sands are not exceptions; they are the inevitable routine.”

“The century-old energy and transportation industries are on the cusp of disruption. The transition has already started and the disruption will be swift. Conventional energy sources are already obsolete or soon to be obsolete. The business model that enables them cannot compete with the disruptive force of technologies like solar, electric vehicles and self-driving cars.”

3 Business-as-Usual Scenario

Going back to the figures given at the beginning of the previous Section it is possible to say that the total resources of fossil fuels are maybe as large as 200.1021 J [4] and it means that, at the current rate of consumption, fossil fuels could satisfy the needs for the next 400 years.

It is quite common among some of the observers the position that renewable energies would never be able to completely replace fossil or nuclear energies [8], while others are issuing warnings on how difficult would be for the renewable energies to cover the needs of modern world [9]. In many cases the solution of the energy problem had been envisioned in nuclear energy, but that was before the Fukushima disaster, which silenced most of pro-nuclear choir. And it was before the “unconventional” oil & gas reserves had started to be exploited.

That leaves the sole fossil fuels to lead the current scenario of energy. Actually, the mutual role of coal, oil and natural gas has changed during the years but in 2017 they, as a whole, still represented almost 85% of global share of primary energy [10] and getting rid of them is easily said but not easily done. Moreover, the crude oil consumption rate does not show any signal of crisis whatsoever: from 2014 the global consumption has increased by 8 million barrels per day, topping at about 100 million barrels per day [11].

The oil & gas industry are aware that fossil fuels are heavily contributing to the global warming but their recipes for contrasting the phenomenon are quite naïve, such as a massive reforestation of the size of Amazon rainforest, or pro-domo-sua, such as the promotion of a continued investment in oil & gas resources which are “essential to meeting the dual challenge of providing billions of people with more energy while drastically lowering carbon emissions” [12].

In the following we will try and give a role to different fossil fuels in a Business-as-usual environment.

3.1 The Role of Coal

Contrary to common belief, coal’s role has accelerated since year 2000, notwithstanding its well known contribute to climate change and many others bad effects on the environment, doubling to 1.5 billion tonnes per year its penetration in the energy markets [13]. This is mostly due to the rising demand within Asia, met by supplies from Indonesia and Australia.

Developed countries are trying and push the decommissioning of as much coal plants as possible: in 2017, UK saw the first “coal-free” day since the start of Industrial Revolution and 2018 saw 42 days powered without coal, expediting the path towards a coal-free economy, that should be reached, according to plans, in 2025. Similar commitment is shared across the OECD (Organisation for Economic Co-operation and Development), also due to the fact that “over half of Europe’s coal fired power stations are now loss-making, and almost all will be by 2030” [13].

China and India, facing very heavy pollution problems, are committed in phasing down coal plants growth as well, but this seems effective only within the respective borders, because the economic support for coal continues for plants to be built abroad, mostly in order to sustain mining industry which, in China alone, occupy three million workers.

As a result, up to 500 million tonnes of new coal capacity is currently under consideration, with an estimated investment in new coal projects of 24 billion USD, more than 90% of which coming from China, Japan, South Korea and India [13].

In this environment, the Trump administration support to coal sector, even if it employs only 50,000 workers in the US, is a new variable whose outcome is unknown.

Adding to the picture the scarce results from research efforts aimed at obtaining a “clean coal” and effective CCS (Carbon Capture and Sequestration) technologies does not call for optimism on environmental terms.

3.2 The Role of Oil

Since the second half of last century crude oil has surpassed coal to become the “world’s leading source of primary energy, with its share of the global energy supply peaking during the late 1970s at about 44%” [10].

The oil share has decreased since then, down to 32% in 2010; nevertheless, during the last fifty years, oil has played the role of “largest component of the global primary energy supply, and its consumption rose from about 1.6 to 4.3 Gtonnes per year (the last figure is referred to 2015, and it means about 31.5 billion barrels per year), nearly a 2.7-fold increase” [10].

“In the last decades liquid fuels have retreated from electricity generation (less than 7% of all refined fuels were burned in power plants in 2015) and residential uses such as heating and cooking (now also less than 7% of global demand for liquids). The consumption of refined oil products has become even more concentrated in the transportation sector: all major forms of moving goods and people—be it shipping, railroads, trucking, automobiles and flying—rely overwhelmingly on refined oils” [10].

“And it must be repeated that this importance goes beyond the reliance on high-performance fuels in all forms of transportation:

-

Oil-derived lubricants are indispensable for countless industrial tasks;

-

Modern transportation infrastructures are unthinkable without oil-derived paving materials; and

-

Syntheses of scores of plastics begin with oil-derived feedstocks” [10].

Given the importance of oil in modern societies and the awareness that it is present in this planet Earth as a finite quantity, many worried about how long its supply will last for the benefits of mankind.

The “oil peak” theory, due to Marion King Hubbert [14], is the most renowned theory about the fate of oil (and also of other fossil fuels). Even though Hubbert’s production curve shapes have had to be changed after the discoveries of “unconventional” sources, some observers believe that the principles behind Hubbert’s theory still hold [15], while others [10] base their criticism on the incorrectness of such predictions.

The exploitation of “unconventional” resources have changed the terms of the debate about the “oil peak”, and also the recent developments about renewables and electric mobility have contributed to this change of paradigm. In this context, the Hubbert’s theory has somewhat lost part of its importance, and this is why we won’t go here into any details about it.

The “unconventional” resources, on the other hand, deserve some focus, because they have actually changed the role of oil and gas in energy scenarios. Oil sands, tight oil, shale oil and also shale gas have changed the fossil fuels paradigm because since when they have started to be exploited, mainly in Canada and US at the end of the first decade of this century, the world framework of energy markets has profoundly changed, making, for example, the US an exporter after that they had acted as importer for decades.

But, even though in quantitative terms the future of “unconventional” resources seems bright, many shadows haunt them. Environmental impacts associated with the extraction processes, the use of chemicals, the heavy consumption of fresh water, the greenhouse gases (GHG) emissions are very concerning.

And the economics of the industry are somewhat concerning too. A recent report from the Institute of Energy Economics and Financial Analysis (IEEFA) [16] wonders “if the industry is still not profitable—after a decade of drilling, after major efficiency improvements since 2014, and after a sharp rebound in oil prices—when will it ever be profitable? Is there something fundamentally problematic about the nature of shale drilling, which suffers from steep decline rates over relatively short periods of time and requires constant spending and drilling to maintain?” [17]. The law of “diminishing returns” definitely applies here.

Liquid fuels are peculiar for some applications, for example marine and air transportation and road heavy transportation, and there is no fully available substitute to fossil fuels at present. LNG (Liquefied Natural Gas) and biomass may play a role, but it is difficult to say how big.

When thinking also at other applications where it does not exist a feasible substitute (petrochemistry) it is easy to predict to crude oil a life that goes well beyond the end of this century.

3.3 The Role of Natural Gas

Natural gas is the last-comer among the fossil fuels and also the most promising, raising from 10% of the global primary energy supply in 1950 to approach 25% in 2013 [18].

Its success depends upon many factors, one of them being that it is considered “the bridge fuel” to a low carbon energy system, due to the fact that its combustion emits less carbon dioxide than coal [19]. As a matter of fact “the European Union’s 2050 energy strategy aims to reduce greenhouse gases emissions by between 80 and 95% when compared to 1990 and in its Energy Roadmap 2050 [20, 21]. The European Commission says it views natural gas as a key factor in achieving this reduction, at least in the medium term.”

The EU document states that “gas will be critical for the transformation of the energy system. Substitution of coal (and oil) with gas in the short to medium term could help to reduce emissions with existing technologies until at least 2030 or 2035” [20].

What will be the fate of natural gas on the long term, i.e. after 2035, is a matter for debate. Some consider the huge quantities made available by shale formations through fracking technologies and the flexibility guaranteed by LNG the reasons for a long term success, notwithstanding the problems haunting the shale gas (similar to those affecting unconventional oil as explained in the previous Section) and the LNG (energy and environmental costs associated with the liquefaction process) [18]. The huge infrastructure already in place for gas distribution is another reason in favor of natural gas in a decarbonisation context, at least until 2050 [22].

Some others, concerned with the environmental impact that natural gas brings (being anyway a fossil fuel) foresee as its long-term role that of a simple “flexible back-up and capacity balance where renewable energy supplies are variable” [20]. This line of thought questions the role of natural gas as “bridge fuel”, especially as an alternative to oil in the transportation sector [23]. The positive figures in terms of greenhouse gases emissions derived from the analysis of combustion are penalized when the whole life cycle is taken into account, due to the natural gas leaks in the supply chain, amounting up to 3.2% of global production. Any leak of natural gas before combustion is a great boost in GHG emissions, because it has a Global Warming Potential (GWP) which is 72 times higher than carbon dioxide over a 20 years time horizon (and 25 times higher over 100 years), and a leak of 3% can bring down its climate benefit over other fossil fuels [6, 24].

4 Energy Transition: A Feasible Scenario

After describing, as extremes, a scenario as revolutionary as possible and a scenario relying on the status quo as much as possible, it is time to take into account all the strengths and weaknesses of the two extremes and design the path forward. We will do that by listing the variables to be taken into account, leaving the reader with the choice of his best solution.

When talking about energy alternatives, we have taken into account just renewables and fossil fuels. Nuclear fission (even if unconventional fuels such as thorium are used) and nuclear fusion (even in the LENR, Low Energy Nuclear Reaction, version, also known as cold fusion) are now marginal voices in the debate on energy because they suffer a series of problems [15], among them being safety and how to dispose of nuclear wastes, that have prevented so far their introduction into markets and do not let foresee any important development in the near future. This is the reason why we have left them out of the picture.

The same can be said about hydrogen and everything revolving around it, the so called “hydrogen economy” [25]. The peculiar properties of the substance and the need for a dedicated infrastructure, too difficult and expensive to be built from scratch, have cancelled also this option, at least for the time being.

The main weaknesses ascribed to renewable energies(in particular to solar, wind and biomasses, because the hydroelectric source is considered to have reached its plateau), that make them unable to cover the whole load and render them a “big illusion”, are well known and can be summarized as follows [8]:

-

They are diluted in time and space and require huge surfaces to catch the needed quantities;

-

They are irregular and unreliable and cannot be easily stored;

-

Deriving from solar radiation, they are thermal energies and the efficiency of the conversion into mechanical or electric energy is limited by the 2nd law of thermodynamics.

There are many arguments that demonstrate that such weaknesses are not anymore able to obstacle renewables growth and success, both in technical and economic terms. We will list some of them in the following.

On the technical side the first argument in favor of renewables is EROEI, or Energy Return On Energy Invested. EROEI is defined as the ratio between the amount of energy delivered from a specific energy resource and the energy used to obtain that amount of energy resource. The minimum EROEI value that an energy resource must possess to be considered viable is 3. If EROEI ≤ 1 then we have an energy sink. Table 1 presents the EROI of currently used energy resources [15].

As far as the efficiency of the renewables is concerned, the recent report “Global renewable energy trends” [26, 27], released by Deloitte Insights, describes the advancements in terms of efficiency reached by innovative materials. It is very interesting the notation about perovskite, which “has been the fastest-developing solar technology since its introduction, making efficiency gains that took silicon over half a century to achieve in less than a decade. In June 2018, a British and German startup demonstrated a record 27.3 percent conversion efficiency on perovskite-on-silicon tandem cells in laboratory settings, beating the laboratory record of standalone silicon cells. Belgian researchers achieved similar efficiency the following month, and both claim that over 30 percent efficiency is within reach. Perovskite has a simpler chemistry, the ability to capture a greater light spectrum, and higher efficiency potential than silicon. Perovskite can also be sprayed onto surfaces and printed in rolls, enabling lower production costs and more applications. Perovskite modules may be commercialized as early as 2019”.

To complete the argument about materials, Fig. 3 shows the trend, over the years, of PV cell efficiencies. It is evident the dramatic growth in efficiency that the PV technology has undergone in the last 40 years.

Trend of PV research-cell efficiencies over the years [source: NREL] (https://www.nrel.gov/pv/assets/pdfs/pv-efficiencies-07-17-2018.pdf)

One last word on technology is about the energy storage. The presence of unreliable energy sources, such as wind and PV, coupled with the path towards EoE (Electrification of Everything) requires the large availability of means of energy storage, in particular electric storage. The huge market penetration of electric vehicle expected within the disruptive scenario depicted in Sect. 2 can itself represent an important way to store electric energy. Apart from that, several R&D efforts are under way as reported in the literature [28, 29]. Figure 4 shows the status of the different technologies under investigation in terms of readiness level.

Readiness level of energy storage technologies [29]

One important signal about the importance of storage in the whole energy context is the news released by Bloomberg [30] about the huge investment opportunities presented by this technology. Bloomberg forecasts 620 billion USD in investment on energy storage from now to 2040. And this brings us to the economic side of the frame.

The already mentioned Deloitte Insights report on “Global renewable energy trends” [26, 27], states that “three key enablers—price and performance parity, grid integration, and technology—allow solar and wind power to compete with conventional sources on price, while matching their performance.” In addition, “as technologies such as blockchain, artificial intelligence (AI), and 3-D printing continue to advance the deployment of renewables, prices will likely continue to fall, and accessibility will improve.”

Deloitte notes that “Longstanding obstacles to greater deployment of renewables have receded as a result of three key enablers:

-

Reaching price and performance parity: The unsubsidized cost of solar and wind power has become comparable or cheaper than traditional sources in much of the world. New storage options are now making renewables more dispatchable—once an advantage of conventional sources.

-

Cost-effective and reliable grid integration: Once seen as an obstacle, wind and solar power are now viewed as a solution to grid balancing. They have demonstrated an ability to strengthen grid resilience and reliability and provide essential grid services. Smart inverters and advanced controls have enabled wind and solar to provide grid reliability services related to frequency, voltage, and ramping as well or better than other generation sources. When combined with smarter inverters, wind and solar can ramp up much faster than conventional plants, help stabilize the grid even after the sun sets and the wind stops, and, for solar PV, show much higher response accuracy than any other source.

-

The impact of technology: Technology is accelerating the deployment of renewables: automation and advanced manufacturing are improving the production and operation of renewables by reducing the costs and time of implementing renewable energy systems; AI can finetune weather forecasting, optimizing the use of renewable resources; blockchain can enable energy attribute certificate (EAC) markets to help resolve trust and bureaucratic hurdles; and advanced materials are transforming the materials of solar panels and wind turbines.”

The endorsement of renewables from Deloitte does not come alone. Several signals from the financial community inform that many investors are shifting from oil & gas to more environmentally sustainable initiatives: the path towards renewables is irreversible, as demonstrated by the number of such investments [31]. The announcement that the World Bank Group [32] will end financing oil & gas extraction is an important signal in this direction, like it is the news from the Financial Times [33] that Blackstone, one of the world’s leading investment firms, will launch an investment fund worth hundreds of millions, named Zarou, in renewable electricity generation assets in Africa and like it is the establishment of a task force on climate-related financial disclosures [34].

The Deloitte report [27] points out the importance that a tool like corporate Power Purchase Agreements (PPAs) may have for the development of a market devoid of incentives. According to many renewable energies operators corporate PPAs are the right tool for such a market where energy produced is not supported anymore by incentives.

As a matter of fact, analyses on the Levelized Cost Of Energy (LCOE) performed by Lazard [35] demonstrate that, even without any subsidy, the cost of energy produced by renewable technologies is fully comparable with the LCOE of energy produced with conventional sources, as shown in Fig. 5. As already mentioned, this is also due to the dramatic decrease in the cost of renewables, like, for example, the 99% reduction in the cost of PV modules in the last 40 years [36].

Levelized cost of energy comparison-sensitivity to fuel prices [35]

In summary, energy transition is already a fact, and this is demonstrated by so many signals. What it is uncertain is the speed at which it will move and it is unlikely that it will accelerate like the scenario presented in Sect. 2 predicts. It will not be a matter of one or two decades and probably it will span throughout the whole present century.

5 Current Research on Energy at DIISM-UNIVPM

Several research groups at the Dipartimento di Ingegneria Industriale e Scienze Matematiche (DIISM) of Università Politecnica delle Marche are involved in activities aimed at accompanying the energy transition [37].

Topics are substantial to such goal and are studied in order to investigate feasible solutions to different aspects of energy conversion, transportation and final uses. In the following the lines of research are described in details, giving the reasons why they are addressed and the results sought.

5.1 Wind Energy

Wind energy is one of the main players in the scenario depicted in Sect. 2 and it is predicted to become the largest power source in the European Union in a 2040 horizon, according to World Energy Outlook 2018 by the International Energy Agency (IEA) [38] (see Fig. 6).

Share of electricity generation by source in European Union, 2017–40 [38]

Research on wind energy at DIISM-UNIVPM is carried out along different lines, which are described in the following.

Low Noise Wind Turbine Blade project: new wind farms are frequently sited near inhabited places so the noise emissions control is a very important challenge for the blade designers. Our research is focused on the design and test of aerodynamic devices able to reduce acoustic mid frequency emissions from wind blade. An extensive campaign of measurements in semi anechoic room is occurring on an instrumented small scale wind blade. At the same time the understanding of noise generation mechanisms of wind turbine blades is very complex due to its aerodynamic nature. For this reason its prediction demands the access to sophisticated numerical tools. Thermofluids group of the UNIVPM is active on the development of innovative models and solution algorithms to simulate the aeroacoustic sound produced by wind turbine blades. More in depth non-reflective boundary treatment was considered in our numerical code as well as accurate approximation schemes able to avoid artificial acoustic waves dissipation. The subject of the ongoing work is related to simulation of wind turbine airfoils self-noise which is a hot topic in wind energy community. Future work will address the numerical design of control devices of the aerodynamic sound produced by the blades.

Morphing Wing project: the pitch controlled wind turbine is the main technology today used to control the power produced. In order to improve the aerodynamic performance of the blades, in this project a flexible airfoil geometry is developed. Numerical and experimental tests are planned on new airfoil shapes equipped with smart materials. The results of the research will allow to develop a new integrated control system in order to increase the aerodynamic efficiency of the blades rotor.

CFD studies on wind turbines performances: currently available software packages used by wind energy analysts suffer of the lack of availability of accurate wake models. Well established tools, such as FAST of NREL [39], adopt the dynamic wake modeling which underestimates the power produced by downstream waked turbines. This is a critical issue for wind energy community. Thermofluids research group of the UNIVPM is active on the development of several innovative fluid flow models and solution algorithms [40,41,42]. The long term goal of this research is to merge the software modules to produce a high-fidelity simulation tool of wind farms overcoming the current limitations.

In situ measurements of power produced by wind turbines: The UNIVPM research centre WEST-lab, operates in this research area realizing tests and simulations on small and large wind turbines.

ADELE (Aerial Drone for Environment and Energy) project: wind turbine drone inspection and evaluation will help to identify and prevent root causes of cascading events that contribute to failure modes. This will significantly reduce downtime of turbines. More detailed information on wind turbine performances will allow operators to develop more site-specific lifetime management strategies. Better knowledge of the properties, degradation and failure mechanisms of materials provides new opportunities for weight and cost reductions, higher reliability and improved manufacture of components and structures. Increased accuracy and robustness of the remote sensors measuring the performance and health of turbines and their components will form the basis of high quality and low cost data collection. The aerial fleet of ADELE is designed to operate at hostile ambient conditions in order to perform visible and infrared inspections of the main wind turbines components.

5.2 Smart Grid and Energy Storage

The increasing penetration of intermittent Renewable Energy Sources (RES) may introduce uncertainty in the available production capacity and require backup power and energy storage systems to ensure a reliable power supply.

The example of such behavior is the famous “duck curve”. The duck curve is the graphic representation of higher levels of wind and solar on the grid during the day resulting in a high peak load in mid to late evening. The difference in the duck curve and a regular load chart is that the duck curve shows two high points of demand and one very low point of demand, with the ramp up in between being extremely sharp. It looks like a duck! (Fig. 7) [43].

The “duck curve” predicted for the California electric system [43]

This behavior introduces uncertainties that challenges the traditional paradigm of the electric energy system based on a “demand following” generation. In the traditional paradigm, the aggregated demand curve of electricity was quite easy to predict since it was variable during the day but almost non-elastic with the season and the typology of day (working day, weekend or holiday).

On the contrary, with the increasing penetration of renewables the uncertainty related to their energy production reflects in the energy system, both on supply and on demand side. For this reason, “the generation following” paradigm is making its way in the energy system. The idea is to provide flexibility to the energy system by compensating the uncertainty of production from renewables by modifying the energy demand so that the centralized power plant could efficiently work without following the sudden changes that happens on both supply and demand side due to the variability of not predictable renewable sources. In this context, micro grids and energy storage are key technologies for providing flexibility to the energy systems. According to the Microgrid Exchange Group (MEG), “A microgrid is a group of interconnected loads and distributed energy resources within clearly defined electrical boundaries that acts as a single controllable entity with respect to the grid” [44, 45]. Within a microgrid it is possible to test and consequently envisage at smaller scale what could be the future large scale “smart grids” by optimally managing distributed energy systems, energy storage and active loads in order to fully exploit the potential of renewable energy without giving back electricity to the grid.

However, in recent years, in the context of the energy transition, the scientific literature introduced the concept of smart multi energy systems [46] in order to go beyond the only electric sector and to include all the potential synergies between different energy networks (natural gas, district heating and cooling) and all the “connecting technologies” such as cogeneration and trigeneration (connecting gas, electric, thermal and/or cooling networks), heat pumps (connecting electric and thermal networks); energy storages (thermal and electric).

Ongoing research activities at DIISM-UNIVPM are focused on optimal design and management of microgrid and smart multi energy systems at different scale: residential [47] and industrial [48] microgrids equipped with renewables, energy storage and heat pumps; urban scale multi energy systems [49]. Also, energy storage plays an important role in the research activity [50]. In particular, thanks to the cooperation with the Nanyang Technological University of Singapore, the use of thermal energy storage in tropical climates [51] and liquid air energy storage are investigated [52, 53]. A recent research activity on energy storage relates to electric mobility in urban systems; indeed, electric vehicles batteries could be seen as distributed energy storages for the electric system in vehicle-to-grid (V2G) and vehicle-to-building (V2B) applications [54].

5.3 Demand Side Management (DSM)

In the same context of large RES penetration it is paramount the availability of energy flexibility at the demand side. Demand Side Management (DSM) is defined as all those actions aimed at modifying the electricity demand to increase customer’s satisfaction and simultaneously produce the desired changes in the electric utilities load in magnitude and shape [55]. DSM can be beneficial to the power system thanks to: (i) reduced electric power peak demands; (ii) higher operational efficiency in production, transmission and distribution of electric power; (iii) lower investments for new power capacity; (iv) lower price volatility; (v) lower electricity costs and (vi) a more cost-effective integration of highly intermittent renewables [56,57,58]. In the literature, three broad categories of DSM are identified: energy efficiency and conservation, on-site back up through local generation or storage and demand response [57]. In particular, given also the relevance of the energy demand in buildings [59], the management of thermostatically controllable loads in the built environment has a central role.

Focus of our research was indeed the investigation of the DSM potential of thermal energy storage systems and heat pumps [60, 61]. Buildings can provide flexibility through the passive storage inherent in their envelope or by means of external active storage systems. An example of inherent storage is represented by Thermally Activated Building Systems (TABS), which require properly designed control systems in order to implement DSM strategies and maintain the internal comfort, given their high thermal inertia [62]. On the other hand, heat pumps are efficient devices, electrically driven, which are easily coupled with building thermal mass, energy storage or RES [48]. They allow to implement DSM strategies in the built environment, both residential and industrial, and to exploit, more generally, the flexibility of the refrigeration sector [63].

Through a comparative study, the different effects produced on the energy demand by the three different DSM categories highlighted in literature (energy efficiency, energy storage and demand response, (DR)) were investigated [64]. It was possible to conclude that: (i) Energy efficiency actions can produce mainly peak shaving and energy conservation; (ii) Energy storage systems allow load shifting; (iii) DR operates an active load shifting to off-peak hours (valley filling) and peak shaving.

Eventually, an integrated environment, where the demand side and the supply side can interact and mutually affect each other is necessary in order to properly quantify the benefits produced by DSM actions on the overall power system (in terms of operational costs reduction, avoided RES curtailment, peak shaving…) [65, 66]. Furthermore the final users participation share into demand side management programs has a high relevance [67]. Results show that increasing the number of consumers participating into DSM programs increases the flexibility of the system and, therefore, reduces the overall operational costs, while decreasing the benefit per individual participant, since a reduced effort from each consumer is needed.

Further investigations are necessary to define optimal strategies to use the available flexibility provided by heat pumps and thermal energy storage systems. This is particularly true with the advent of integrated energy systems, which consist of multi-carrier energy systems characterized by a mutual dependence among the infrastructures of the different systems. Heat pumps and energy storage systems can indeed affect positively the operation of the overall energy system and especially its reliability [68,69,70].

5.4 Biofuel from Algae

In Sect. 3 it was already pointed out that some applications, namely marine and air transportation, will hardly be able to get rid of liquid fuels, mostly due to the energy intensity that they can carry in their unit of volume. This leaves way to only two solutions for the long-term: either we keep on relying on fossil fuels or we switch to liquid biofuels.

Biofuels are a fascinating alternative to fossil fuels, but, if they are produced from superior plants grown in temperate climates, they can dangerously conflict with food agriculture and their EROI easily approaches the lower limit of convenience of 3 [15].

A feasible alternative seemed to be biofuel extracted from algae and microalgae, which guarantee a higher lipids content with respect to superior plants [71]. This is why a research line was started at DIISM-UNIVPM aimed at investigating the feasibility of producing biodiesel from microalgae.

Initially the research dealt with the biodiesel production methods [72,73,74] but when realizing that fuel derived from algae was far more expensive than fossil fuels and even than biodiesel from superior plants, the activity was put in stand by [75].

6 Conclusions

The speed at which energy transition will proceed during the 21st century, floating between the two extreme scenarios described in Sects. 2 and 3 of the present paper, will be dictated by many variables. Technology innovations and economics will drive the transition but policies will play a fundamental role as well [76].

In this sense reports from International Energy Agency (IEA) could help governments to establish such policies, especially those more innovative, courageous and, let’s say, disruptive.

The last IEA World Energy Outlook was released on November 13, 2018 [38] and was not fully appreciated by those [77] who want an acceleration of the transition process, also in order to keep pace with the goal of maintaining the global warming below the 1.5 °C limit.

The IEA Sustainable Development Scenario (SDS) pursue the limit of 1.7–1.8 °C global warming and recognizes that “continued investment in oil & gas supply, however, remains essential even in the Sustainable Development Scenario to 2040, as decline rates at existing fields leave a substantial gap that needs to be filled with new upstream projects”.

Is this a too conservative scenario? Only time will tell.

References

IPCC (2018) Global warming of 1.5 °C: an IPCC special report on the impacts of global warming of 1.5 °C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development, and efforts to eradicate poverty. Available via DIALOG. http://report.ipcc.ch/sr15/pdf/sr15_spm_final.pdf. Accessed October 20, 2018

Pope Francis (2015) Encyclical Laudato sì, Libreria Editrice Vaticana, Città del Vaticano. Available via DIALOG. http://w2.vatican.va/content/dam/francesco/pdf/encyclicals/documents/papa-francesco_20150524_enciclica-laudato-si_it.pdf. Accessed October 21, 2018

Von Weiszacker EU, Wijkman A (2018) Come on!: Capitalism, short-termism. Population and the destruction of the planet. Springer Science + Business Media, New York. ISBN 978-1-4939-7418-4

Smil V (2007) Energy in nature and society, MIT Press, Cambridge, Mass., p. 29, ISBN: 978-02-62693-56-1

Jacobson MZ et al, 100% Clean and renewable wind, water, and sunlight all-sector energy roadmaps for 139 countries of the world, Joule, 1(1):108–121, doi:http://dx.doi.org/10.1016/j.joule.2017.07.005

Seba T (2014). Clean disruption of energy and transportation. Lightning Source Inc., ISBN: 978-06-92210-53-6

Arbib J, Seba T (2017) Rethinking transportation: the disruption of transportation and the collapse of the internal-combustion vehicle and oil industries. RethinkX. ISBN: 978-09-99401-60-6

Battaglia F (2007) L’illusione dell’energia dal sole (in Italian), 21mo Secolo, Milan. ISBN: 978-88-87731-34-7

MacKay DJC (2009). Sustainable energy-whitout the hot air, UIT Cambridge, ISBN: 978-09-54459-23-3

Smil V (2017) Oil. Oneworld publications, London. ISBN 978-1-78607-286-3

Dagospia (2018) Pompa funebre. Estratto dall’articolo di Luigi Grassia per LaStampa (in Italian), October 11, 2018. Available via DIALOG. http://www.dagospia.com/cerca?s=pompa+funebre. Accessed November 16, 2018

Beckman K (2018) IPCC climate alarm: what next for energy? Energy post weekly, October 16, 2018. Available via DIALOG. https://energypostweekly.eu/ipcc-climate-alarm-what-next-for-energy-oil-industry-dont-call-us-well-call-you/. Accessed November 16, 2018

Bradley S (2018). What is the future of coal? energypost.eu, October 10, 2018. Available via DIALOG. https://energypost.eu/what-is-the-future-of-coal/. Accessed November 16, 2018

Hubbert MK (1956). Nuclear energy and the fossil fuels. Presented at the Spring meeting of the Southern Division of American Petroleum Institute, San Antonio, TX, March 1956. Available via DIALOG. http://www.hubbertpeak.com/Hubbert/1956/1956.pdf. Accessed November 16, 2018

Bardi U (2011) La Terra svuotata (in Italian). Editori Riuniti University Press, Rome. ISBN 978-88-6473-067-7

Williams-Derry C, Hipple K and Sanzillo T (2018) Energy market update: Red Flag on U.S. Fracking. Institute for Energy Economics and Financial Analysis and Sightline Institute, October 2018. Available via DIALOG. http://ieefa.org/wp-content/uploads/2018/10/Red-Flags-on-U.S.-Fracking_October-2018.pdf. Accessed November 16, 2018

Cunningham N (2018) US shale has a glaring problem. oilprice.com. October 21, 2018. Available via DIALOG. https://oilprice.com/Energy/Energy-General/US-Shale-Has-A-Glaring-Problem.html. Accessed November 16, 2018

Smil V (2015) Natural gas. Fuel for the 21st Century. John Wiley & Sons, Chichester. ISBN: 978-1-11901-286-3

Deign L (2018) What role for gas in Europe’s 2050 energy system? energypost.eu, September 20, 2018. Available via DIALOG. http://energypost.eu/what-role-for-gas-in-europes-2050-energy-system/. Accessed November 16, 2018

European Union (2012) Energy roadmap 2050. ISBN: 978-72-79-21798-2 Available via DIALOG. https://ec.europa.eu/energy/sites/ener/files/documents/2012_energy_roadmap_2050_en_0.pdf. Accessed November 16, 2018

European Commission (2018) 2050 Energy Strategy. Available via DIALOG. https://ec.europa.eu/energy/en/topics/energy-strategy-and-energy-union/2050-energy-strategy. Accessed November 21, 2018

Trinomics, (2018) Trans-European gas infrastructure in the light of the 2050 decarbonisation targets. Final report. September 24, 2018. Available via DIALOG. http://trinomics.eu/wp-content/uploads/2018/11/Final-gas-infrastructure.pdf. Accessed November 21, 2018

Bardi U (2017) Viaggiare elettrico (in Italian). Luce edizioni, Massa. ISBN 978-88-97556-24-4

Arteconi A, Brandoni C, Evangelista D, Polonara F (2010) Life-cycle greenhouse gas analysis of LNG as a heavy vehicle fuel in Europe. Appl Energy 87:2005–2013. https://doi.org/10.1016/j.apenergy.2009.11.012

Rifkin J (2002) The hydrogen economy. Penguin, New York. ISBN 978-1-58542-193-0

Beckman K (2018) The age of renewables is here-I-renewables make the grade in price performance and reliability. Energy post weekly, September 18, 2018. Available via DIALOG. https://energypostweekly.eu/the-age-of-renewables-is-here-i-renewables-make-the-grade-in-price-performance-and-reliability/. Accessed November 17, 2018

Motyka M, Slaughter A and Amon C (2018). Global renewable energy trends. Solar and wind move from mainstream to preferred. Deloitte Insights. Available via DIALOG. https://www2.deloitte.com/insights/us/en/industry/power-and-utilities/global-renewable-energy-trends.html. Accessed November 17, 2018

International Energy Agency (2014). Technology Roadmap. Energy storage. Available via DIALOG. https://www.iea.org/publications/freepublications/publication/TechnologyRoadmapEnergystorage.pdf. Accessed November 17, 2018

EASE-EERA (2018). European Energy Storage Technology Development towards 2030—Update. Available via DIALOG. https://www.eera-set.eu/wp-content/uploads/. Accessed November 17, 2018

Bloomberg (2018). Energy Storage is a $620 Billion Investment Opportunity to 2040. Bloomberg NEF, November 6, 2018. Available via DIALOG. https://about.bnef.com/blog/energy-storage-620-billion-investment-opportunity-2040/. Accessed November 17, 2018

Beckman K (2018). The age of renewables is here-II-More deals, more zero-subsidy, more PPAs, more grid integration. Energy post weekly, September 18, 2018. Available via DIALOG. https://energypostweekly.eu/the-age-of-renewables-is-here-ii-more-deals-more-zero-subsidy-more-ppas-more-grid-integration/. Accessed November 17, 2018

The World Bank (2017) World Bank Group Announcements at One Planet Summit. Press release, December 1, 2017. Available via DIALOG. http://www.worldbank.org/en/news/press-release/2017/12/12/world-bank-group-announcements-at-one-planet-summit. Accessed November 18, 2018

TCFD (2018) Task Force on Climate-related Financial Disclosures-2018 Status Report. September 2018. Available via DIALOG. https://www.fsb-tcfd.org/wp-content/uploads/2018/08/FINAL-2018-TCFD-Status-Report-092518.pdf. Accessed November 17, 2018

Espinosa J, Raval A (2018) Blackstone launches Africa-Middle East power venture. Financial Times, October 8, 2018. Available via DIALOG. https://www.ft.com/content/e9097070-c9ff-11e8-b276-b9069bde0956. Accessed November 18, 2018

LAZARD (2018) Lazard’s Levelized Cost of Energy Analysis-Version 12.0. November 2018. Available via DIALOG. https://www.lazard.com/media/450784/lazards-levelized-cost-of-energy-version-120-vfinal.pdf. Accessed November 17, 2018

Kavlak G, McNerney J, Trancik JE (2018) Evaluating the causes of cost reduction in photovoltaic modules. Energy Policy 123:700–710. https://doi.org/10.1016/j.enpol.2018.08.015

Brebbia C, Magaril E, Passerini G, Polonara F (eds) (2014) Energy production and Management in the 21st Century II. WIT Press, Southampton (UK). ISBN 978-1-78466-107-6

International Energy Agency (2018). World Energy Outlook 2018, November 13, 2018. Available via DIALOG. https://webstore.iea.org/world-energy-outlook-2018. Accessed November 18, 2018

National Renewable Energy Laboratory, (2018). NWTC Information Portal (FAST). Available via DIALOG. https://nwtc.nrel.gov/FAST. Last modified January 4, 2018; Accessed November 21, 2018

D’Alessandro V, Montelpare S, Ricci R (2016) Detached-eddy simulations of the flow over a cylinder at Re = 3900 using OpenFOAM. Comput Fluids 136:152–169. https://doi.org/10.1016/j.compuid.2016.05.031

D’Alessandro V, Montelpare S, Ricci R, Zoppi A (2017) Numerical modeling of the flow over wind turbine airfoils by means of Spalart-Allmaras local correlation based transition model. Energy 130:402–419. https://doi.org/10.1016/j.energy.2017.04.134

D’Alessandro V, Binci L, Montelpare S, Ricci R (2018) On the development of OpenFOAM solvers based on explicit and implicit high-order Runge-Kutta schemes for incompressible flows with heat transfer. Comput Phys Commun 222:14–30. https://doi.org/10.1016/j.cpc.2017.09.009

Energy Alabama (2017) The Duck Curve: what is it and what does it mean? acse.org, May 29, 2017. Available via DIALOG. https://alcse.org/the-duck-curve-what-is-it-and-what-does-it-mean/. Accessed November 18, 2018

Office of Electricity Delivery and Energy Reliability Smart Grid R&D Program (2011) DOE Microgrid Workshop Report. San Diego, California, August 30–31, 2011. Available via DIALOG. https://www.energy.gov/sites/prod/files/Microgrid%20Workshop%20Report%20August%202011.pdf. Accessed November 18, 2018

Esposito F, Mancinelli E, Morichetti M, Passerini G and Rizza U (2018) A cogeneration power plant to integrate cold ironing and district heating and cooling. Int J Energy Prod Manag 3(3):214–225, https://doi.org/10.2495/eq-v3-n3-214-225

Lund H, Østergaard PA, Connolly D, VadMathiesen B (2017) Smart energy and smart energy systems. Energy 137:556–565. https://doi.org/10.1016/j.energy.2017.05.123

Comodi G, Giantomassi A, Severini M, Squartini S, Ferracuti F, Fonti A, Nardi Cesarini D, Morodo M, Polonara F (2015) Multi-apartment residential microgrid with electrical and thermal storage devices: Experimental analysis and simulation of energy management strategies. Appl Energy 137:854–866. https://doi.org/10.1016/j.apenergy.2014.07.068

Arteconi A, Ciarrocchi E, Pan Q, Carducci F, Comodi G, Polonara F, Wang R (2017) Thermal energy storage coupled with PV panels for demand side management of industrial building cooling loads. Appl Energy 185:1984–1993. https://doi.org/10.1016/j.apenergy.2016.01.025

Comodi G, Lorenzetti M, Salvi D, Arteconi A (2017) Criticalities of district heating in Southern Europe: Lesson learned from a CHP-DH in Central Italy. Appl Therm Eng 112:649–659. https://doi.org/10.1016/j.applthermaleng.2016.09.149

Comodi G, Carducci F, Sze JY, Balamurugan N, Romagnoli A (2017) Storing energy for cooling demand management in tropical climates: a techno-economic comparison between different energy storage technologies. Energy 121:676–694. https://doi.org/10.1016/j.energy.2017.01.038

Comodi G, Carducci F, Balamurugan N, Romagnoli A (2016) Application of cold thermal energy storage (CTES) for building demand management in hot climates. Appl Therm Eng 103:1186–1195. https://doi.org/10.1016/j.applthermaleng.2016.02.035

Borri E, Tafone A, Romagnoli A, Comodi G (2017) A preliminary study on the optimal configuration and operating range of a “microgrid scale” air liquefaction plant for Liquid Air Energy Storage. Energy Convers Manag 143:275–285. https://doi.org/10.1016/j.enconman.2017.03.079

Tafone A, Borri E, Comodi G, van denBroek M, Romagnoli A (2018) Liquid Air Energy Storage performance enhancement by means of Organic Rankine Cycle and Absorption Chiller. Appl Energy 228:1810–1821. https://doi.org/10.1016/j.apenergy.2018.06.133

Comodi G, Caresana F, Salvi D, Pelagalli L, Lorenzetti M (2016) Local promotion of electric mobility in cities: Guidelines and real application case in Italy. Energy 95:494–503. https://doi.org/10.1016/j.energy.2015.12.038

Gellings C (1985) The concept of demand-side management for electric utilities. Proc IEEE 73(10):1468–1470. https://doi.org/10.1109/PROC.1985.13318

Strbac G (2008) Demand side management: Benefits and challenges. Energy Policy 36(12):4419–4426. https://doi.org/10.1016/j.enpol.2008.09.030

Warren P (2014) A review of demand-side management policy in the UK. Renew Sustain Energy Rev 29:941–951. https://doi.org/10.1016/j.rser.2013.09.009

Pina A, Silva C, Ferrao P (2012) The impact of demand side management strategies in the penetration of renewable electricity. Energy 41(1):128–137. https://doi.org/10.1016/j.energy.2011.06.013

EU (European Union), 2018. Energy efficiency—Buildings. Available via DIALOG. https://ec.europa.eu/energy/en/topics/energy-efficiency/buildings. Accessed November 18, 2018

Arteconi A, Hewitt NJ, Polonara F (2012) State of the art of thermal storage for demand side management. Appl Energy 93:371–389. https://doi.org/10.1016/j.apenergy.2011.12.045

Arteconi A, Hewitt NJ, Polonara F (2013) Domestic Demand-Side Management (DSM): Role of Heat Pumps and Thermal Energy Storage (TES) systems. Appl Therm Eng 51:155–165. https://doi.org/10.1016/j.applthermaleng.2012.09.023

Arteconi A, Costola D, Hoes P, Hensen JLM (2014) Analysis of control strategies for thermally activated building systems under demand side management mechanisms. Energy Build 80:384–393. https://doi.org/10.1016/j.enbuild.2014.05.053

Arteconi A, Polonara F (2017) Demand side management in refrigeration applications. Int J Heat Technol 35(1):S58–S63. https://doi.org/10.18280/ijht.35Sp0108

Arteconi A, Polonara F (2018) Assessing the Demand Side Management Potential and the Energy Flexibility of Heat Pumps in Buildings. Energies 11(7):1846. https://doi.org/10.3390/en11071846

Patteeuw D, Bruninx K, Arteconi A, Delarue E, D’haeseleer W, Helsen L (2015) Integrated modeling of active demand response with electric heating systems coupled to thermal energy storage systems. Appl Energy 151:306–319. https://doi.org/10.1016/j.apenergy.2015.04.014

Patteeuw D, Henze GP, Arteconi A, Corbin CD, Helsen L (2018) Clustering a building stock towards representative buildings in the context of air-conditioning electricity demand flexibility. J Build Perform Simul, published online, https://doi.org/10.1080/19401493.2018.1470202

Arteconi A, Patteeuw D, Bruninx K, Delarue E, D’haeseleer W, Helsen L (2016) Active demand response with electric heating systems: impact of market penetration. Appl Energy 177:636–648. https://doi.org/10.1016/j.apenergy.2016.05.146

Adefarati T, Bansal RC (2017) Reliability assessment of distribution system with the integration of renewable distributed generation. Appl Energy 185:158–171. https://doi.org/10.1016/j.apenergy.2016.10.087

Li G, Bie Z, Kou Y, Jiang J, Bettinelli M (2016) Reliability evaluation of integrated energy systems based on smart agent communication. Appl Energy 167:397–406. https://doi.org/10.1016/j.apenergy.2015.11.033

Shariatkhah MH, Haghifam MR, Parsa-Moghaddam M, Siano P (2015) Modeling the reliability of multi-carrier energy systems considering dynamic behavior of thermal loads. Energy Build 103:375–383. https://doi.org/10.1016/j.enbuild.2015.06.001

Borowitzka MA, Moheimani NR (eds) (2013) Algae for Biofuels and Energy. Springer, Netherlands. ISBN 978-94-007-5478-2

Di Nicola G, Pacetti M, Polonara F, Santori G andStryjek R (2008) Development and optimization of a method for analyzing biodiesel mixtures with non aqueous reversed phase liquid chromatography. J Chromatogr A, 1190:120–126, https://doi.org/10.1016/j.chroma.2008.02.085

Santori G, Di Nicola G, Moglie M and Polonara F (2012) A review analyzing the industrial biodiesel production practice starting from vegetable oil refining. Appl Energy 92:109–132, https://doi.org/10.1016/j.apenergy.2011.10.031

Santori G, Franciolini M, Di Nicola G, Polonara F, Brandani S, Stryjek R (2014) An algorithm for the regression of the UNIQUAC interaction parameters in liquid-liquid equilibrium for single- and multi-temperature experimental data. Fluid Phase Equilibria, pp 79–85, https://doi.org/10.1016/j.fluid.2014.04.014

Rapier R (2018) The Death of Algal Biofuels, oilprice.com. October 27, 2018. Available via DIALOG. https://oilprice.com/Alternative-Energy/Biofuels/The-Death-Of-Algal-Biofuel.html. Accessed November 18, 2018

European Political Strategy Center (2018) 10 Trends Reshaping Climate and Energy. Available via DIALOG. https://ec.europa.eu/epsc/publications/other-publications/10-trends-reshaping-climate-and-energy_en. Accessed December 8, 2018

Muttitt G (2018) The IEA Comes Up Short on Climate (Again). Oil Change International, November 12, 2018. Available via DIALOG. http://priceofoil.org/2018/11/12/business-as-usual-iea-climate/. Accessed November 18, 2018

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2019 Springer Nature Switzerland AG

About this chapter

{kind=link}

Cite this chapter

Arteconi, A. et al. (2019). Energy Scenarios for the Future of Mankind. In: Longhi, S., Monteriù, A., Freddi, A., Frontoni, E., Germani, M., Revel, G. (eds) The First Outstanding 50 Years of “Università Politecnica delle Marche”. Springer, Cham. https://doi.org/10.1007/978-3-030-32762-0_13

Download citation

DOI: https://doi.org/10.1007/978-3-030-32762-0_13

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-32761-3

Online ISBN: 978-3-030-32762-0

eBook Packages: EducationEducation (R0)