Abstract

The article examines the problems of company growth, which are of particular relevance in the modern geopolitical environment. Analysis of the interactions of companies with the external environment that forms the local production system was carried out. Interactions are considered as prerequisites and conditions for growth. The main analyzed growth factors are the size of the company, its industry affiliation, the presence of agglomeration effects, affiliation with large integration entities, innovative focus, customer focus, competitive environment and investment activity. The focus is on high-tech enterprises. The empirical basis of the study was the results of a questionnaire survey of managers of 55 companies operating in the Siberian Federal District. The relationships between the identified factors and their impact on growth was studied by cluster analysis, as a result of which three clusters were formed. The first included high-tech growing companies located primarily in large cities, the second included nongrowing companies, and the third included growing low-tech companies. The sectoral specifics, size, and customer focus of the company turned out to be significant in clustering. State support is important for the development of high-tech companies; however, they do not count on direct financing, highly appreciating assistance in organizing external interactions. The results can be used to determine priorities and formulate measures for state industrial and innovation policy.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

INTRODUCTION

The need for Russia to move towards technological sovereignty has made it particularly relevant to study the conditions and opportunities for the growth of enterprises, and above all those that make up the high-tech and knowledge-intensive sectors of the Russian economy, in the new reality. This problem is not unique to Russia; the slowdown in the global economy and high uncertainty of the geopolitical situation are affecting the growth opportunities of companies worldwide. The consulting company McKinsey presented the results of a study of growth and efficiency models of 5000 of the world’s largest public companies over the past 15 years (Bradley et al., 2022). The typical company was growing at roughly 2.8% per year for the decade before the COVID-19 pandemic, with only 12% of companies posting more than 10% annual growth.

The history of research on company growth goes back several decades, but the high dependence of the results on the period of observation, the sectoral affiliation of companies, and the choice of growth indicators and assessment methods creates many options for answering the question of what conditions promote or limit company growth. The growth of an enterprise is influenced by many factors: macroeconomic (global and national), mesoeconomic (regional and sectoral), and microeconomic (strategic management system, manager’s personality) characteristics and other components of its external and internal environment. A variety of conditions manifest themselves differently for individual companies, creating unique combinations of factors that influence their development.

Among the first ideas about the growth of enterprises was put forward by R. Gibrat’s law on its stochastic nature, which in its simplest form states that the expected growth rate of an individual enterprise does not depend on its size at the beginning of the considered period. Numerous subsequent studies based on empirical data continued to analyze the relationship between company size and growth and expanded arguments for and against the postulated pattern. Today the prevailing belief, supported by a large amount of empirical data, is that small and young companies grow faster, but there are also alternative positions: a greater contribution to the growth of large companies is proven, and Gibrat’s law on stochastic growth is also confirmed (e.g., Gibrat’s law worked for large American companies (Hall, 1987)).

In the theory of firm growth, substantiated by E. Penrose, the growth of companies is interpreted as the result of translating accumulated knowledge into goods/services in demand by consumers, which are created through the effective management of company resources (Lau and Michie, 2022). Growth is driven by the application of management and engineering talent. Limitations on the human capital of managers and employees dictate growth limits that can be overcome to a certain extent through partner resources and new areas of expertise. I. Schumpeter’s theory of creative destruction considers that the main source of growth is a company’s innovative activity, since only innovation can ensure sustainable competitiveness.

Growth opportunities are supported or limited by a variety of factors that vary across companies of different sizes, ages, industries, etc. Whereas for small companies the obstacles are primarily the difficulty of attracting financing, for large companies, such factors as competition and attracting new employees become more important (for a detailed analysis of 44 000 Swedish small and medium-sized companies, see (Karlsson, 2021)). In a detailed review (Coad, 2009), the history of development of scientific ideas is outlined and areas that need additional research are highlighted. Subsequent empirical studies have led to much debate, adding to the range of growth determinants, but also providing new evidence for the random nature of growth (Coad and Srhoj, 2020).

Russian researchers in a more recent period also became interested in the problems of company growth, and their attention was directed primarily at fast-growing companies, including high-tech ones, as well as the conditions for the growth of small and medium-sized businesses. It is considered that fast-growing companies ensure the development of industries, the spread of technology and innovation, and the creation of new jobs (Zemtsov and Chernov, 2019; Zhiganov and Yudanov, 2019).

Summarizing a brief overview of the main publications, we can highlight several stylized incidences related to the study of company growth:

• uneven and unstable growth;

• multiplicity of factors and conditions affecting the growth and development of companies;

• high differentiation of the results of the influence of factors and conditions on an individual company;

• nonlinearity of relationships between factors and conditions with resulting characteristics.

Thus, companies' growth trajectories are characterized by a high level of uncertainty. The proffered theoretical positions require new empirical research, which determines the relevance of this study.

Our research is aimed at analyzing the interactions of companies with the external environment that forms the local production system; we consider interactions as prerequisites and conditions for the growth of companies.

The main idea behind the study is to test the hypothesis of differences in significant environmental factors for companies with different growth trajectories, the factors being determined by the size and growth of companies.

The novelty of the study is the inclusion in the analysis of empirical data new for Russian enterprises (integral indicators reflecting the importance of interaction with scientific and material partners, as well as the location of companies).

The empirical base comprises the results of a survey of enterprise managers, conducted by the Institute of Economics and Industrial Engineering, Siberian Branch Russian Academy of Sciences. The survey covered a wide range of issues, with particular attention on the growth opportunities of companies in conditions of high uncertainty in the external environment. The data obtained relate to a 3-year period and reflect the state of companies in 2019–2021. The analyzed sample included 55 questionnaires from managers of enterprises of various industries and sizes located in the Siberian Federal District.

ANALYZED FACTORS

The factors for in-depth analysis were selected based on the results of previously completed studies, as well as with allowance for the characteristics of the information acquired by a survey of enterprise managers.

As a growth criterion, we consider the growth rate of the number of employees for 2019–2021. This is one of the most commonly used growth indicators, which is free of the distortions inherent to financial indicators (Anyadike-Danes et al., 2015).

Company Size and General Growth Characteristics. The sample represents companies of various sizes that demonstrate different employment dynamics: growing companies, stable ones and those reducing the number of employees (“declining”). From 2019 to 2021, the majority of companies (38%) showed growth, 35% were stable, and 27% were downsizing, with companies of different sizes in each group.

In the “declining” group, the reduction in the number of employees ranged from 1 to 50%, while in absolute numbers, the larger reduction affected large enterprises. The dynamics in the growing group were more active: approximately half the companies grew by more than 30% in 2 years, and the leaders increased their numbers by almost three times. Among the growth leaders are predominantly medium and small companies in terms of the number of employees.

Sectoral Affiliation. We considered companies from two sectoral groups: high-tech and knowledge-intensive companies and traditional companies in accordance with OKVED codes. High-tech companies play a major role in ensuring technological sovereignty; they can fill gaps in technological chains and replace products and services import of which is prohibited or restricted as a result of sanctions. A large-scale study of fast-growing Russian companies (Rossiiskie …, 2022) showed that growing companies are present in various industries, but high-tech companies are of particular importance for creating new jobs for qualified personnel, disseminating innovations, etc. So far, the share of such companies in Russia is small (1.42%), and about half of them did not demonstrate rapid growth until 2016. Among the companies in our sample, 40% belong to high-tech and knowledge-intensive industries.Footnote 1

Location and Agglomeration Effects. The size of a locality and the diversity of its economy can be important determinants of a company’s development, since large cities, due to the concentration of human, financial, and other resources, make it possible to attract workers with different qualifications, increase the likelihood of finding suppliers and other contractors, create ample opportunities for marketing products, and developed infrastructure makes it possible to reduce transaction costs (Acs et al., 2006; Kolomak, 2023; Kolomak and Sherubneva, 2023; Zemtsov and Maskaev, 2018). The size of a city’s population generally contributes to the diversification of its economy. Researchers have noted the relationship between the level of diversification of the regional economy and the innovative activity of companies, which in turn contributes to the growth of companies by acquiring a sustainable competitive advantage. At the same time, localization and diversification affect large and small companies in different ways: diversification contributes to the growth of small companies, and localization to medium and large companies (Zyuzin et al., 2020).

In our sample, half the enterprises are located in the largest cities (with populations of more than 1 mln people), 30% are in large and major cities, and about 20% are in cities with a population of less than 100 000 people.

The sample included enterprises from 13 cities and three other population centers (urban-type settlement, town, village) from seven regions of the Russian Federation. Among the cities, three are million-plus cities (Novosibirsk, Krasnoyarsk, and Omsk), two are major cities (Barnaul and Kemerovo), three are large cities (Abakan, Biysk, and Prokopyevsk), three are medium-sized cities (Gorno-Altaisk, Zheleznogorsk, and Chernogorsk) and two are small towns (Belokurikha and Guryevsk).

Affiliation reflects the participation of companies in various integrated structures (business groups, state corporations, holdings, etc.), the decision-making centers of which are located outside the companies in question. Affiliated companies have the opportunity to attract material and intangible resources of the parent company to ensure growth (Zhiganov and Yudanov, 2019). Involvement in vertically organized structures can promote growth as a result of participation in production chains (Zemtsov and Chernov, 2019). Companies that are leaders in efficiency are more common among large companies, as well as among those included in integrated groups (Karlova et al., 2022). In our sample, approximately half the companies are affiliated with and part of integrated structures.

Innovation is critical to the growth of high-tech companies. Such companies have higher expenditures on research and development, which serves as a source of innovation, and, accordingly, they can grow to a greater extent (Coad and Rao, 2008). Investments in new technologies and new products increase productivity and employment (Peters et al., 2014). However, firms are diverse and operate in different economic environments. The level of competition that businesses face can be an incentive for innovation (for companies on the technological frontier) but can also be a drag on companies that are catching up (Aghion et al., 2005). We considered assessments of the significance of companies' interactions with research organizations as indicators of their innovative orientation.

Customer focus of companies involves a deep understanding of market trends and customer needs and contributes to improved efficiency and growth of companies (Frambach et al., 2016). For the companies of the sample, the importance of customer relations is generally low.Footnote 2 Growing companies that need to attract new customers or increase consumption from existing ones are more customer-oriented.

Competition. Its pressure in general is also assessed as low; the actions of competitors do not have a significant impact on the activities of companies. The actions of competitors are somewhat more important for growing high-tech companies. For all companies, large businesses are more important as consumers, and large, small, and medium-sized enterprises act as competitors. Growing high-tech companies rate the importance of all types of competitors higher than other groups of respondents. This indirectly indicates that they are entering highly competitive markets or are ready to do so in the future. This feature was confirmed for both growing and declining enterprises. High-tech firms also showed interest in export operations.

It can be said that Russian companies exist in a sluggish market environment. This may be due to pandemic-related restrictions and gradual adaptation to new operating conditions.

RESULTS OF CLUSTER ANALYSIS

For a more in-depth study of the interrelations of many factors influencing the growth of companies, a cluster analysis was performed to assess the structure of the sample data set. The factors included:

(1) the growth rate of the number of employed over two years;

(2) number of employees in 2021;

(3) the company’s affiliation to a high-tech business;

(4) population of the city/town in which the company is located;

(5) the company’s inclusion into a business group, state corporation, holding company, or other integrated organization/affiliation;

(6) assessment of the significance/importance of partners from the field of science and education;

(7) assessment of the significance/importance of consumers;

(8) assessment of the significance/importance of competitors;

(9) investments made within the last three years.

Since the factors include both qualitative and quantitative variables, we used a two-stage clustering procedure in the SPSS statistical package; as a result, three clusters of companies were formed. The quality of clustering is assessed as average, the silhouette measure of connectivity and separation of clusters exceeds 0.4.

Of the 55 companies in the sample, 21 were included in the first cluster, four in the second, and 30 in the third. Table 2 presents the means and standard deviations for quantitative variables, and Table 3 shows the distribution of enterprises in clusters according to qualitative characteristics. Table 4 presents the territorial distribution of companies in clusters, and Table 5, the estimated significance of the assessments.

Table 5 shows the statistics (F-statistic for continuous variables and χ2-statistic for categorical variables) and significance level. When forming clusters at the 1% level, such factors as the average for consumers, the number of employees, belonging to a high-tech business, and the enterprise’s inclusion in a business group turned out to be significant.

Although there was no clear division of the clusters into three groups (growing, stable, declining), the first cluster consists largely of growing companies (10 out of 21 firms); the second cluster can be classified as a stable group, although one company has a growth rate growth which is less than 100%; the third cluster includes companies of all three groups in almost equal parts: growing 33%, stable 40%, declining 27%. Therefore, it is better to judge the growth characteristics by the first cluster. Thus, sector, size, location, and affiliation are important determinants of a company’s growth trajectory.

Let us characterize the resulting clusters.

The first cluster included high-tech companies (it contains 95.5% of the high-tech companies in the sample) with different growth rates, including those with the highest growth, located in large cities, mainly in Novosibirsk (42.9% of the cluster companies). About half (48%) of all affiliated enterprises were in this cluster. The importance of partnerships with consumers is assessed lower by companies in this cluster than by companies in other clusters. It is likely that joining organizationally integrated groups reduces the need to develop interactions with actors external to the group. In addition, the specifics of high-tech innovative business includes the imperfection of the product market, which requires buyers in this market to adapt to price and quality in order to establish competitive demand. Location in a large city makes it easier to find new partners, which may also be a reason for lower ratings of the importance of existing interactions. More than 80% of companies are involved in the implementation of investment projects.

The second, smallest, cluster included large companies in Krasnoyarsk krai and Kemerovo oblast, mainly low-tech ones. They have lower growth rates, which confirms the negative relationship between growth and company size. All enterprises of this group are part of integrated structures and make investments. These are enterprises in the raw materials sector that have stable connections with a limited number of regular large consumers and a stable cash flow.

The third cluster included smaller firms that did not belong to high-tech businesses. Half of the cluster companies are located in Altai krai, the Republic of Khakassia, and the Altai Republic. The majority of companies of the cluster (70%) are not part of integrated structures. Since the average number of employees is significantly lower than in other clusters, it can be suggested that the higher average growth rates of firms in this group compared to enterprises in the second cluster are associated with the low base effect. Companies in the third cluster are characterized by a higher assessment of the importance of consumers and competitors compared to companies in other clusters.

Particularly noteworthy is the investment activity of enterprises, which is demonstrated by almost all companies in the sample and which is not a cluster-forming factor. Although growth rate was not a significant factor in the cluster analysis results, there were significant differences in the areas of investment and sources of investment financing between companies with different growth trajectories.

Investments made shape the possible future of a company. In conditions of high uncertainty, the planning horizon is shortened; however, the vast majority of companies in the sample (87%) had made investments over the past three years.

Priority areas of investment vary depending on the development trajectory of companies. The focus of investments allows us to judge with a certain degree of confidence both the most significant problems that companies need to solve, and the prospects for their further development. If we follow McKinsey’s analytical framework, organic growth in an enterprise’s output can occur by expanding the output of already developed products, related diversification, and development of new products (Bradley et al., 2022). The listed areas differ primarily in the level of risk associated with the uncertainty of market conditions and the level of investment costs. Most companies are expanding the production of already familiar goods or services, a minority are diversifying their products, and even fewer are entering the market with new products.

Our sample showed high differentiation between the identified groups: Fig. 1 shows the directions of investments made over the past three years. The group of declining companies invests less than other groups in improving the skills of employees and significantly more in modernizing and updating facilities. Given the lower level of investment in the development of new technologies and the production of new products, we see that enterprises support the production of traditional products and experience difficulties with financing (Fig. 2). Most companies in this group use their own funds, and only 20% financed investments using bank loans. Thus, companies find themselves in a trap: insufficient investment financing does not allow for growth, and the reduction in activity volumes further reduces the likelihood of attracting bank loans. Budget funds also do not support the investments of these companies.

Directions of investment, share of companies, %.

Sources of investment financing, share of companies, %.

Among growing companies, most invest in the development and production of new products and in the corresponding development of new production technologies (see Fig. 1). This allows the entry into new markets and acquisition of new expertise, which includes improvement in personnel qualifications and attraction of new employees. Among this group, investments in intangible assets are more common.

The group of stable companies occupies an intermediate position, with the exception of higher investments in personnel development and low investments in intangible assets. It is possible that enterprises in this group are focused on intensive development, choosing not to increase the number of employees, but to improve the qualifications of existing personnel.

Almost all companies use their own funds for investment (except for two companies that use only bank loans for investment) however, whereas among the declining companies only 20% were able to attract bank loans and the rest had to rely only on their own savings, in other groups, the palette of available sources of investment financing is much wider (see Fig. 2). Growing companies use bank loans the most; they also have access to funds from regional and federal budgets, and in addition, they issue securities. Stable companies also use all of the above sources, but to a slightly lesser extent.

Bank loans support the growth of mid-size companies and are least accessible to companies with shrinking workforces. This suggests that in this group, downsizing represents a reduction in activity rather than an increase in productivity.

An important condition for the development of any enterprise can be the participation of the state. The identified differences in the development trajectories of companies also imply differentiation of their needs for support from authorities and management, which should be taken into account when choosing tools and methods of this support. Of particular interest is the query from growing high-tech firms included in the first cluster.

ASSESSMENT OF STATE SUPPORT MEASURES

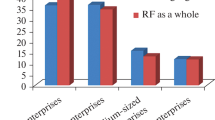

We asked respondents to evaluate support measures and choose the most important for their enterprises. The list of support measures includes direct financial assistance (state orders, tax breaks, investments) and various measures to create a favorable external environment. The following are estimates for the entire sample and individual groups (Figs. 3, 4).

Average assessments of government support measures for companies with different development trajectories.

Average assessments of government support measures for growing companies.

All companies need support, and the greatest need is for tax benefits and assistance in training personnel at all levels. Companies rate the attractiveness of government orders the lowest. This may be due to the predominance of small-sized companies in the sample that have no possibiltiy of receiving government orders and, accordingly, do not consider them as an anticipated support measure. Other areas of support attract companies in high-tech and other industries to varying degrees. High-tech companies rate the attractiveness of government investments even lower, as they are commonly associated with high regulatory costs and risks of failure to achieve the planned investment results.

All growing companies generally rate infrastructure development significantly higher: industrial parks, technology parks, etc. The development of a regional innovation system is an important condition for expanding activities.

Growing high-tech companies rate most of the measures considered higher than growing companies in general, regardless of their sector. It should be noted that all areas of personnel support and tax benefits received the highest possible rating of importance. The importance of government assistance in organizing interaction with research and educational institutions and participation in exhibitions turned out to be higher for such companies than for growing ones in general. Our results show that government support is important for the development of high-tech companies, although they do not rely on direct financing.

In general, for all companies, the importance of government support significantly exceeds the importance of both consumers and competitors. Perhaps this paternalistic model of interactions reflects the situation of the pandemic and recovery from it, when it was the efforts of the state contributed to maintaining business activity in unfavorable conditions.

CONCLUSIONS

The results demonstrate the diversity of companies' growth trajectories. It makes sense to take the identified differences into account when determining priorities and developing measures of state industrial and innovation policy at the federal and regional levels. Large cities generally provide more favorable conditions for the development and growth of high-tech and knowledge-intensive companies, but smaller cities may have the advantage of specialization in certain market segments, so special support measures are required for companies from small cities, including the formation of infrastructure, support for cluster development, stimulation of intra- and interregional cooperation of companies. Reducing the tax burden and assistance in training personnel at all levels: workers, specialists and managers are important for all companies. For growing companies, the development of innovation and production infrastructure is of great importance (companies of the first and third clusters), while for high-tech growing companies, interaction with organizations involved in research and development (companies of the first cluster) is important. Government procurement and public investment are less important in supporting growth, perhaps due to limited access to such instruments, as well as high regulatory burden. The institutional environment, reflected in the regulatory and legislative field, also requires changes. Note that although the empirical testing of our hypotheses is based on an unbalanced sample of companies, the results make a certain contribution to the formation of ideas about the characteristics of the development of companies in an unstable external environment.

In the current situation, the search for missing expertise to restore destroyed ones and build new technological chains to achieve technological sovereignty is particularly important. This requires supporting the interaction of large integrated structures with small and medium-sized businesses, as well as incentivizing long-term cooperation between companies, universities, and research organizations as sources of knowledge and technological innovation.

Notes

In accordance with OKVED codes.

Experts rated the importance/significance of interactions with various partners on a scale from 0 to 3: 3, significant; 2, somewhat significant; 1, somewhat insignificant; 0, insignificant.

REFERENCES

Acs, Z., Armington, C., and Zhang, T., The determinants of new-firm survival across regional economies, in Papers on Entrepreneurship, Growth and Public Policy, Jena: Max Planck Institute of Economics, 2006, no. 0407.

Aghion, P., Bloom, N., Blundell, R., Griffith, R., and Howitt, P., Competition and innovation: An inverted-U relationship, Quart. J. Econ., 2005, vol. 2, no. 120, pp. 701–728.

Anyadike-Danes, M., Bjuggren, C.M., Gottschalk, S., Holzl, W., Johansson, D., Maliranta, M., et al., An international cohort comparison of size effects on job growth, Small Business Econ., 2015, vol. 4, no. 44, pp. 821–844. https://doi.org/10.1007/s11187-014-9622-0

Bradley, C., Doherty, R., and Northcote, N., The ten rules of growth, 2022. https://www.mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/the-ten-rules-of-growth/. Cited August 1, 2023.

Coad, A., The growth of firms: A survey of theories and empirical evidence, in Papers on Entrepreneurship, Growth and Public Policy, Jena: Max Planck Institute of Economics, 2009.

Coad, A. and Rao, R., Innovation and firm growth in high-tech sectors: A quantile regression approach, Res. Pol., 2008, vol. 4, no. 37, pp. 633–648.

Coad, A. and Srhoj, S., Catching gazelles with a lasso: Big data techniques for the prediction of high-growth firms, Small Business Econ., 2020, vol. 3, no. 55, pp. 541–565.

Frambach, R., Fiss, P., and Ingenbleek, P., How important is customer orientation for firm performance? A fuzzy set analysis of orientations, strategies, and environments, J. Business Res., 2016, vol. 4, no. 69, pp. 1428–1436.

Hall, B.H., The relationship between firm size and firm growth in the US manufacturing sector, J. Ind. Econ., 1987, vol. 4, no. 35, pp. 583–606.

Karlova, N., Puzanova, E., and Bogacheva, I., Problems of instability of effective companies: survey results: Analytical note, Central Bank of Russia, 2022. https://cbr.ru/content/document/file/140375/analytic_note_20221005_dip.pdf. Cited July 20, 2023.

Karlsson, J., Firm size and growth barriers: A data-driven approach, Small Business Econ., 2021, vol. 3, no. 57, pp. 1319–1338.

Kolomak, E.A., Assessment of the influence of agglomeration factors on the economic activity of the Angara–Yenisei region, Zh. Sib. Fed. Univ. Guman. Nauki, 2023, vol. 9, no. 16, pp. 1560–1566.

Kolomak, E.A. and Sherubneva, A.I., Assessing the significance of agglomeration effects in the south of Siberia, Prostranstv. Ekon., 2023, vol. 19, no. 1, pp. 52–69.

Lau, Ch. and Michie, J., Penrose’s theory of the firm in an era of globalization, Int. Rev. App. Econ., 2022, pp. 1–20. https://doi.org/10.1080/02692171.2022.2117284

Peters, B., et al., Firm Growth, Innovation and the Business Cycle: Background Report for the 2014 Competitiveness Report, Mannheim: Zentrum fur Europaische Wirtschaft-sforschung (ZEW), 2014.

Rossiiskie bystrorastushchie kompanii: razmer populyatsii, innovatsionnost’', otnoshenie k gospodderzhke (Russian Fast-Growing Companies: Population Size, Innovativeness, Attitude to Government Support), Analytical Reports of the Higher School of Business of the Higher School of Economics, Medovnikov, D.S., Rozmirovich, S.D., Oganesyan, T.K., , Eds., Moscow: Vyssh. Shk. Ekon., 2022, vol. 2.

Zemtsov, S.P. and Maskaev, A.F., Fast-growing companies in Russia: Characteristics and growth factors, Innovatsii, 2018, vol. 236, no. 6, pp. 30–38.

Zemtsov, S.P. and Chernov, A.V., Which high-tech companies are growing faster in Russia and why, Zh. Nov. Ekon. Assots., 2019, vol. 41, no. 1, pp. 68–99.

Zyuzin, A.V., Demidova, O.A., and Dolgopyatova, T.G., Localization and diversification of the Russian economy: regional and sectoral features, Prostranstv. Ekon., 2020, vol. 16, no. 2, pp. 39–69.

Zhiganov, A.V. and Yudanov, A.Yu., Fast-growing companies in Russia: The influence of affiliation on growth factors, Ross. Zh. Menedzh., 2019, vol. 17, no. 3, pp. 287–308.

Funding

The study was carried out according with the research plan of the Institute of Economics and Industrial Engineering, Siberian Branch, Russian Academy of Sciences (project “Theory and Methodology of Research on Sustainable Development of High-Tech and Knowledge-Intensive Companies in the Context of Global Challenges of the External Environment, Technological, Organizational and Institutional Shifts,” no. 121040100260-3.

Author information

Authors and Affiliations

Corresponding authors

Ethics declarations

The authors of this work declare that they have no conflicts of interest.

Additional information

Publisher’s Note.

Pleiades Publishing remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Kravchenko, N.A., Yusupova, A.T., Ivanova, A.I. et al. Location, Technological Level, and Partnerships as Conditions for Company Growth. Reg. Res. Russ. 14, 306–315 (2024). https://doi.org/10.1134/S207997052460015X

Received:

Revised:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1134/S207997052460015X