Abstract

In this paper, we analyze the relationship between industrial stagnation in the US economy and the financialization of nonfinancial firms by asking whether firms in industries experiencing a stronger post-1970 tendency towards stagnation allocate more funds to shareholder payouts and, specifically, share repurchases. While strands of the literature on financialization have long-emphasized the role of stagnation in driving financialization, fewer papers have considered this hypothesis empirically. Our paper speaks to this space in the literature, by linking industrial stagnation in capital accumulation to a firm’s decision to financialize. We, first, use firm-level data to construct an empirical measure of industrial stagnation. Drawing on insights from the Monopoly Capital School, we measure stagnation using the Baran ratio — which describes the average share of surplus allocated towards investment within an industry — and show a secular decline in the average Baran ratio since 1980. Second, we analyze if the tendency towards stagnation captured by the declining Baran ratio predicts the likelihood and magnitude of a firm’s shareholder payouts. We show that firms in industries with a stronger stagnation tendency (a lower Baran ratio) are more likely to repurchase stock and, among firms that do repurchase, that a lower Baran ratio predicts a higher magnitude of these shareholder payouts. These results suggest that a slowdown on the nonfinancial side of the economy is one factor underlying financialized firm behavior in the post-1980 USA.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In this paper, we explore links between stagnation and the financialization of US corporations by asking if firms in industries with a greater tendency towards stagnation are more likely to allocate funds towards financial outlets and, in particular, shareholder payouts. In the post-1980 US economy, nonfinancial firms have become increasingly intertwined with financial markets and oriented towards financial indicators of performance. These trends have led to a large empirical literature linking the financialization of nonfinancial firms to key long-term trends in the US economy, including slowing capital investment (e.g., Stockhammer 2004; Orhangazi 2008; van Treeck 2008; Davis 2018)Footnote 1 and worsening income distribution (e.g., Lin and Tomaskovic-Devey 2013; Dünhaupt 2017; Guschanski and Onaran 2018; Kohler et al. 2019). In the US context, these trends, also, exemplify a shift from a Fordist to a finance-led growth regime (Aglietta 2000; Boyer 2000). At the firm level, a major feature of US financialization has been growing shareholder value orientation, characterized by the emergence of a “downsize and distribute” corporate governance regime focused on releasing funds to shareholders (Lazonick and O’Sullivan 2000). In turn, the increasing entrenchment of shareholder value ideology is reflected in rising rentiers’ income (e.g., Onaran et al. 2011) and growing shareholder payouts, including own-stock buybacks, through which managers target stock market-based measures of firm performance (e.g., Lazonick 2014; Davis 2016).

At the same time, a branch of the theoretical literature on financialization emphasizes the role of stagnation in driving increasingly financialized firm behavior. Marxist political economists have long argued that periods of overaccumulation generate a tendency towards stagnation and slower economic growth, which leads capital to seek ways outside of industrial production to utilize surplus (Baran and Sweezy 1966). In this view, the “financial explosion” of the post-1980 period in the USA is a response to declining investment outlets (Magdoff and Sweezy 1987; Foster 2008; Magdoff and Foster 2014), explained by the emergence of monopolies that generate persistent excess capacity in production (Lapavitsas 2011; Despain 2015). Crotty (2003) and McDonough et al (2010) also emphasize that increased international competition and growth in the power of capital over labor, which has generated a secular decline in the labor share, have further depressed aggregate demand after 1980. While excess surplus not used for capital accumulation can be absorbed through various channels, such as expanded credit to workers or financial investments, a particularly prominent channel in the post-1980 period has been financialization (Magdoff and Foster 2014). Accordingly, the post-1980 transition towards finance may be driven, at least in part, by a deterioration on the real side of the economy pushing firms towards financial uses of funds.

Despite both the large empirical literature on financialization and the theoretical tradition arguing financialization is a response to stagnation in the US economy, the role of stagnation in explaining the financialization of US firms has not been considered using firm-level data. This paper fits into this space by empirically analyzing the implications of industrial stagnation in the post-1980 US economy for nonfinancial firms’ shareholder payouts. Following Xu (2019), we measure stagnation using the Baran ratio, or the investment share of surplus, wherein a falling Baran ratio captures a decline in the utilization of surplus for capital accumulation and, accordingly, a tendency towards stagnation. More specifically, we measure the Baran ratio at the industry level to capture both that the stagnation tendencies created by changes in monopoly power, excess capacity, and effective demand differ by industry and also that these processes are external to individual firms. These industry-level stagnation tendencies, in turn, impact individual firms’ decision-making. Thus, by measuring the Baran ratio at the industry level, we capture the implications of industry-wide stagnation tendencies for individual firms’ decisions to allocate funds towards shareholder payouts — not an individual firm’s decision to reallocate surplus away from capital accumulation (which is also endogenous to its payout decisions).

To construct this industry-level measure, we, first, use Compustat data to define the investment share of surplus at the firm level, and, second, we average these firm-level Baran ratios across the firms in each industry. To measure economic surplus, we again follow Xu (2019) and define surplus as the profit share of value added.Footnote 2 Because the data needed to calculate factor shares in Compustat data is notoriously incomplete, we follow the method in Donangelo et al. (2019) to impute firm-level labor and profit shares. Finally, we exclude each firm from the average Baran ratio calculated across all (other) firms in its industry, thereby ensuring that this Baran ratio is exogenous to individual firms in the econometric analysis.

Consistent with Xu’s (2019) macro-level analysis, we document a post-1980 decline in the Baran ratio across US industries, concentrated during the 1980s and 1990s, capturing a decline in profitable fixed investment opportunities relative to other uses of funds. In turn, in our econometric analysis, we show that this decoupling of investment from surplus predicts both the likelihood and magnitude of shareholder payouts and, in particular, repurchases. Notably, despite dramatic post-1980 growth in shareholder payouts, a sizeable share of firms continues to make zero payouts in any given year. Given this high incidence of zeros, we employ a two-part estimation strategy.Footnote 3 Using a series of linear probability models, we, first, show that a decline in the average industry-level Baran ratio is associated with a statistically and economically significant increase in firms’ propensity to make shareholder payouts. Second, we show that, among firms that do make shareholder payouts, this tendency towards industrial stagnation is also associated with a higher magnitude of these payouts, both contemporaneously and moving forward over time. Each of these relationships is, furthermore, driven by repurchases, more than dividends or total shareholder payouts, highlighting the particular importance of repurchases as an outlet for surplus in the years following a decline in the average industrial Baran ratio.

Together, these results suggest that stagnation is one factor precipitating the financialization of US firms. In each case, the average industry-level Baran ratio can be understood as a signal to individual firms that suitable investment opportunities within their industry are scarce, such that funds are better allocated towards alternative (financial) uses. In turn, firms have not only become more likely to release funds to shareholders, but are also more likely to release a larger quantity of funds to shareholders in any given year. There are at least two additional implications of these results. First, as the declining Baran ratio largely reflects growth in economic surplus (i.e., a rising profit share or declining labor share of income), these results suggest that rising shareholder payouts are one part of a larger-scale readjustment of priorities within firms, wherein shareholder payouts have come at the expense of labor (Lazonick 2009; Greenwald et al. 2019). Second, the fact that each set of econometric results is driven by repurchases, more than dividends or total shareholder payouts, suggests that repurchases are the key manifestation of shareholder value orientation in the post-1980 US economy. In other words, in the era of shareholder value, all types of shareholder payouts are not equivalent, and the impetus to financialize is best captured by payouts that prioritize capital gains.

These results contribute to the existing empirical and theoretical literatures on financialization that emphasize the drivers of the financialization of nonfinancial firms. Much of the empirical literature on financialization emphasizes the consequences of post-1980 changes in firm financial behavior. Here, we aim instead to contribute to discussions on the underlying drivers of these changes. The main explanation to date of these underlying drivers emphasizes institutional and regulatory changes that shift power to shareholders, thereby entrenching shareholder orientation among firm managers (Lazonick and O’Sullivan 2000; Stockhammer 2004, 2005; Lazonick 2014). These wide-reaching changes include SEC rules making it easier to repurchase stock; an expansion in stock-based executive pay; and the emergence of an active market for corporate control (for a discussion, see the survey in Davis 2017). Our results complement the literature establishing this channel, by suggesting that stagnation is an additional factor contributing to the shift in managerial priorities towards releasing funds to shareholders in the post-1980 US economy. Specifically, while institutional and regulatory changes have made large-scale stock buybacks possible, our results suggest that managerial responsiveness to these institutional changes has also been shaped by weakening opportunities for capital accumulation. In other words, our results suggest that — in the absence of a tendency towards industrial stagnation (or, conversely, in an economy with high and rising real profitability) — the reorientation of managerial priorities towards shareholder value orientation over this period may have been weaker.

The paper is organized as follows: In Sect. 2 we introduce the data and document the decline in the Baran ratio and growth in shareholder payouts that motivate our empirical analysis. In Sect. 3 we turn to our econometric hypotheses and ask if the Baran ratio predicts, first, firms’ growing propensity to repurchase shares in Sect. 3.1 and, second, the rising magnitude of these shareholder payouts in Sect. 3.2. Section 4 concludes and suggests directions for future research.

2 Data and stylized facts

We begin by laying out the stylized facts that motivate our empirical hypotheses and strategy. We, first, construct an empirical measure of industry-level Baran ratios based on firm-level data and show a pronounced tendency towards industrial stagnation (a decline in the Baran ratio), occurring largely during the 1980s and 1990s. Second, we describe the evolution of shareholder payouts made by US nonfinancial firms. We show a post-1980 expansion in both the magnitude of shareholder payouts and in the annual share of firms making shareholder payouts. We, also, show that growth in total shareholder payouts primarily reflects stock buybacks (rather than dividend payments), suggesting the particular importance of repurchases in the era of financialization. We draw on these two sets of stylized facts in Sect. 3 to econometrically explore whether a falling industry-level Baran ratio predicts firms’ decisions to make shareholder payouts and, in particular, repurchase stock.

Our analysis uses a firm-level panel of publicly traded nonfinancial corporations from the Compustat database. We include all nonfinancial corporations incorporated in the USA with non-negative sales, total assets, or financial payouts (repurchases, dividends, or interest payments).Footnote 4 We introduce the Baran ratio and shareholder payout variables in Sects. 2.1 and 2.2, below. In the econometric analysis in Sect. 3, we also consider controls for total assets (Compustat variable AT); total debt (DT, or the sum of current debt, DLC, and long-term debt, DLTT); the profit rate (which we define as operating income before depreciation, OIBDP, relative to the stock of physical capital, PPENT); and a financial profit rate (non-operating income, NOPI, relative to the stock of financial assets).Footnote 5 We deflate money values using the GNP deflator and trim firm-level ratios at the 1st and 99th percentiles to account for outliers.Footnote 6 Our final sample spans 1971 (the first year repurchase data is available) through 2019. We summarize these variable definitions in Appendix Table 5 and show descriptive statistics in Table 6.

2.1 An empirical measure of industrial stagnation

Our key explanatory variable of interest is an industry-level measure of the Baran ratio, which we use to describe the tendency towards industrial stagnation in the US economy. The Baran ratio is defined as the investment share of surplus, such that a falling Baran ratio indicates that a declining share of total surplus is allocated towards investment. To construct this measure, we, first, construct firm-level measures of surplus (which we capture using the profit share, following Xu 2019) and investment. The main obstacle to doing so lies in that Compustat data on labor expense is sparsely reported. As a result, the literature on financialization in the US context has not used profit or labor shares in firm-level analyses. To circumvent this issue, we follow the method in Donangelo et al. (2019) to construct an imputed labor share for firms that do not report labor costs using industry averages. Second, we aggregate these firm-level measures of the Baran ratio to the sectoral level to describe the evolution of industrial stagnation.

We, therefore, begin by constructing firm-level measures of the profit share:

where \(P{S}_{i,t}\) and \(L{S}_{i,t}\) denote the profit share of firm \(i\) in year \(t\), and value added is the value of production less the cost of intermediate goods. Following Donangelo et al. (2019), value added can be written in terms of Compustat variables as:

In Eq. 2 the first term in parentheses measures the value of production (where \(SAL{E}_{i,t}\) denotes the gross sales of firm \(i\) in year \(t\) and \(\Delta INVF{G}_{i,t}\) denotes the change in inventories of finished goods), and the second term measures the cost of intermediate goods, defined as sales less profits and labor costs.Footnote 7 We capture profits using operating income before depreciation (\(OIBDP\)), which measures total sales after the costs of goods sold and after general and administrative expense. Labor costs (\(XLR\)) measure the annual cost of employees’ wages and benefits.Footnote 8 Simplifying the expression in Eq. 2 shows that value added is the sum of payments to capital, payments to labor, and changes in inventories of finished goods (Eq. 3). In turn, the profit share of firm \(i\) in year \(t\) is one less the ratio of labor costs (\(XLR\)) to value added, where value added depends on profits, labor costs, and inventories of finished goods.

We, next, use the method in Donangelo et al. (2019) to calculate labor share measures for observations that do not report labor costs. As noted above, only a small share of firm-year observations report labor costs (11.03% of the sample). To address this limitation of the Compustat data, Donangelo et al. (2019) present a method of imputing the labor share based on industry-level averages, which they show has a strong and highly statistically significant correlation with Census-based measures of the labor share and which they conclude is an appropriate measure of the labor share for researchers using Compustat data. For each firm \(i\) with missing labor expense data, we impute labor expense using the average wage across the \(j\) firms in that industry \(k\) that do report labor expense in year \(t\) (\({\overline{Wage}}_{t}^{ k}\)) and average employment (\(EMP\)) in firm \(i\) between years \(t-1\) and \(t\):

where \({\overline{Wage}}_{t}^{ k}\) is the average of:

across the \(j\) firms in each industry \(k\) that report labor expense. We use average employment between years \(t-1\) and \(t\) because employment is reported as year-end values and classify each industry \(k\) using 2-digit SIC codes that distinguish 67 industries in our sample.Footnote 9 We use these imputed labor costs to calculate value added and, in turn, the labor and profit shares for firms with missing values of \(XLR\).

In turn, we measure the investment share, which is the numerator of the Baran ratio, as capital expenditure (\(CAPX\)) relative to value added.Footnote 10 Finally, we aggregate these firm-level Baran ratios using a trimmed industry-level mean by, first, trimming the firm-level measures of the Baran ratio to account for outliers and, second, averaging at the industry level by 2-digit SIC codes.Footnote 11 To ensure that the industry-level measure of stagnation tendency is fully exogenous to the individual firm, we exclude each individual firm from the calculation of the industry average that is applied to that observation. As such, this variable allows us to consider the hypothesis that industrial stagnation contributes to rising shareholder payouts, while mitigating reverse causality concerns stemming from the fact that higher shareholder payouts restrict an individual firm’s available funds for investment.

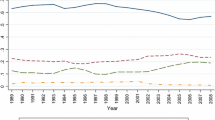

In Fig. 1, we plot the industry-level Baran ratio, averaged across industries in our sample, between 1971 and 2019. This figure shows a marked decline in the Baran ratio across US industries after the early 1980s, from an average of 72.1% during the 1980s to an average of 51.9% after 2010, with the majority of this decline taking place during the 1980s and 1990s.Footnote 12 Thus, while almost three quarters of surplus is allocated towards investment during the 1980s, this share subsequently falls by almost thirty percent, with only half of surplus allocated towards physical investment in more recent years.Footnote 13 This trend is consistent with Xu’s (2019) aggregate results for the US economy, which show the Baran ratio rising during the (late) 1970s before trending downwards after 1980 and settling at a lower level since the mid-2000s.

Industry-level Baran ratio, average across industries (1971–2019). Notes: This figure shows the industry-level Baran ratio (the investment share of surplus), averaged across industries between 1971 and 2019, and shown as a percent (%). Industries are defined using 2-digit SIC codes. For details on the sample and variable definitions, see Sect. 2

This decline in the Baran ratio suggests a tendency towards stagnation in the post-1980 US economy, wherein declining investment opportunities within US industries have led capital to seek alternative routes for surplus absorption (Baran and Sweezy 1966). This trend, also, occurs as concentration and monopoly power in the US economy rise (Grullon et al. 2019; Davis and Orhangazi 2020) and, consistent with Monopoly Capital Theory, this decline in the Baran ratio is stronger within industries that are relatively more skewed towards large firms. Specifically, consider a measure of within-industry skew defined as the ratio of assets at the top 20th percentile in an industry to assets at the 50th percentile in that industry in each year. Industries with greater skew in total assets (or, more within-industry size inequality) are arguably characterized by more monopoly power. Among industries with the greatest skew (in the top 20% of industries ranked by skew), the Baran ratio declines from an average of 82.3% in the 1980s to 40.4% since 2010. Conversely, the Baran ratio of the median industry when ranked by skew is far more stable, averaging 68.6% in the 1980s and 58.6% since 2010. Thus, industries with greater inequality in total assets — or, conversely, more monopoly power — drive the post-1980 decline in the Baran ratio across the US nonfinancial corporate sector shown in Fig. 1.

2.2 Shareholder payouts and stock repurchases

Next, we turn to shareholder payouts. A major strand of the literature on financialization emphasizes that shareholder orientation — and, in particular, growing managerial attention to stock-based indicators of firm performance — is a defining aspect of the financialization of US nonfinancial firms (e.g., Aglietta 2000; Lazonick and O’Sullivan 2000; Stockhammer 2004; Crotty 2003; Davis 2017). The growing entrenchment of shareholder value orientation has been supported by a series of wide-reaching institutional and regulatory changes including the emergence of an active market for corporate control (Fligstein 1990; Aglietta and Bretton 2001); growth in institutional investors and increasingly short-term stock ownership (Aglietta 2000; Crotty 2003); and an expansion in stock-based executive pay (Lazonick and O’Sullivan 2000).Footnote 14 Together, these changes have generated a shift in managerial priorities towards greater emphasis on shareholder interests and, in particular, the interests of short-term shareholders (e.g., Stout 2012).

In turn, the entrenchment of shareholder value norms is reflected in firm financial behavior, including a post-1980 expansion in shareholder payouts driven, specifically, by own-stock buybacks. In fact, growth in repurchases has been so dramatic that net equity issues of the US nonfinancial corporate sector are negative in much of the post-1980 period (see Lazonick 2014). We show this trend in Fig. 2, which plots net equity issuance as a share of outstanding equity between 1971 and 2019 and which highlights that — in most years after 1983 — the nonfinancial corporate sector repurchased more from the stock market than it issued in new stock.Footnote 15 As such, the standard logic wherein the stock market acts as a source of funding for nonfinancial firms has flipped: nonfinancial corporations now pull more out of the stock market via repurchases than they receive in new financing.

Net equity issuance (1971–2019). Notes: This figure shows net equity issuance as a percent of outstanding equity. The series is calculated as total equity issuance (Compustat item SSTK) less gross repurchases (PRSTKC) relative to total outstanding equity (SEQ) in each year between 1971 and 2019, with each variable summed across all firms in our Compustat sample. For details on the sample, see Sect. 2

We, also, show the evolution of shareholder payouts at the firm level in Fig. 3. To begin, consider the solid black line in Fig. 3a, which plots total shareholder payouts over time. Total shareholder payouts include both repurchases and dividends, where repurchases are any use of funds decreasing a firm’s outstanding common or preferred stock (Compustat variable \(PRSTKC\)) and dividends measure total cash dividends on both common and preferred stock (\(DV\)). We normalize each series by total assets to capture firm size and plot yearly weighted means across all firms in our sample.Footnote 16 Figure 3a shows that total shareholder payouts rise 60% between the 1970s and the post-2010 years, when they average 2.8% and 4.4% per year when normalized by assets, respectively. This rise in shareholder payouts is consistent with the entrenchment of shareholder value norms over this period, and a corresponding shift in corporate governance strategy towards one increasingly oriented towards generating shareholder returns.

The evolution of shareholder payouts (1971–2019). a Shareholder payouts relative to total assets. b Shares of firms making shareholder payouts (%). Notes: This figure shows the evolution of buybacks, dividends and total payouts (the sum of buybacks and dividends) across firms between 1971 and 2019. Panel (a) shows the magnitude of payouts relative to total assets, where each series is shown as across-firm yearly weighted means. Panel (b) shows the annual share of firms (as a percent) that repurchased stock, payed dividends, and that made any type of shareholder payout (repurchases and/or dividends). For details on the sample and variable definitions, see Sect. 2

Figure 3a, also, highlights that buybacks are an increasingly preferred method of distributing payouts to shareholders by US firms. In fact, the post-1970 increase in total payouts is driven entirely by repurchases. Figure 3a highlights that repurchases first rise appreciably in 1983, following the implementation of SEC Rule 10b-18, which protects managers from insider trading charges when repurchasing shares (Grullon and Michaely 2002; Davis 2016). Thereafter, repurchases measured relative to assets rise ten times, from close to zero through the 1970s to an annual average of 2.2% in the 2010s. In contrast, dividend payouts decline modestly between the early 1980s and early 2000s, thereby somewhat offsetting this rise in shareholder payments. Despite a modest recovery after 2000, post-2010 dividend payouts remain lower than they were in the early 1970s (dividends fall from an average of 2.5% relative to assets between 1971 and 1979 to 1.9% since 2010). Accordingly, the weight of dividends in total shareholder payouts diminishes markedly after 1970: while dividends account for 92.1% of shareholder payouts in the 1970s, this share falls to 62.6% by the 1990s and to 44.0% since 2010.

The growing centrality of repurchases is consistent with post-1980 institutional changes in the USA that encourage managerial attention to the stock price as a primary metric of shareholder value. The fact that repurchases, unlike dividends, can (at least temporarily) drive up a firm’s stock price implies that, in the era of shareholder value ideology, each dollar of shareholder payouts does not equivalently raise the key metric of shareholder value, namely, the stock price. These patterns are, furthermore, consistent with evidence that US firms repurchase shares with funds that would otherwise be used for dividends (Skinner 2008; Grullon and Michaely 2002; Jiang et al 2013).Footnote 17

The importance of repurchases is, also, corroborated by the shares of US nonfinancial corporations paying dividends and repurchasing stock annually, shown in Fig. 3b.Footnote 18 These trends highlight that the annual share of firms repurchasing stock increases markedly from the 1980s and accelerates after 2009, from an average of 30.1% of firms in 1980 to 70.2% in 2019. Thus, there is a marked increase in both the annual share of firms repurchasing stock and in the average size of these repurchases. At the same time, while three quarters (75.1%) of firms make dividend payments in 1971, this share falls through the 1990s to barely more than a third (35.3%) of firms at its minimum in 2003. Thus, during the decades that shareholder value ideology first becomes entrenched, firms’ propensity to pay dividends declines and, despite a recovery after 2003, there is a clear and substantive decline in the share of firms making dividend payments over the shareholder value era. The evolution of firms’ propensities to make repurchases versus pay dividends captures the importance of repurchases as a key indicator of shareholder value orientation.

2.3 Industrial stagnation and shareholder value orientation?

These trends in the Baran ratio and shareholder payouts point us to our main question: Does the tendency towards industrial stagnation captured by the Baran ratio act as an impetus for firms to turn to shareholder payouts as an outlet for surplus? To describe the relationship between these key trends, Fig. 4 begins by presenting scatterplots comparing the average industry-level Baran ratio and mean shareholder payouts between 1971 and 2019. In Fig. 4a we consider total shareholder payouts and in Fig. 4b we focus on stock buybacks. Each figure, also, includes a linear best fit line summarizing the (unconditional) correlation between these two variables. Finally, to clarify the co-movement of these variables, we distinguish three sub-periods suggested by the time path of the Baran ratio in Fig. 1. In particular, Fig. 1 indicates that the Baran ratio first rises through the 1970s to reach 70.4% in 1980, falls rapidly between 1980 and 2003, and is then largely steady at an average of 50.9% since 2003.

Scatterplot of shareholder payouts and the industry-level Baran ratio (1971–2019). a Total shareholder payouts. b Stock buybacks. Notes: These figures show scatterplots of the annual relationship between the average industry-level Baran ratio and total shareholder payouts (in panel (a)) and repurchases (in panel (b)) between 1971 and 2019. Each figure also includes a linear best-fit line. For details on the sample and variable definitions, see Sect. 2

Figure 4 suggests a negative correlation between the average industrial Baran ratio and both total shareholder payouts and repurchases. During the 1980s and 1990s, as the average across-industry Baran ratio declines and payouts rise, we move up and to the left along these best-fit lines. Since 2004, the Baran ratio is steady and lower, generating a cloud of points towards the upper left corner of the scatterplots. Thus, as the Baran ratio falls after 1980, indicating a decline in the average allocation of surplus to capital accumulation across US industries, the average firm’s allocation of surplus towards shareholder payouts — and, in particular, buybacks — rises. In contrast, the 1970s were a period of low buybacks and a rising Baran ratio; these years lie consistently below the best-fit lines. Finally, the best-fit line in Fig. 4a for total shareholder payouts has a higher intercept (reflecting higher total payments when aggregating repurchases and dividends) but a flatter slope than the best-fit line in Fig. 4b. This comparison indicates that repurchases have a stronger unconditional correlation with the Baran ratio.

3 Empirical framework and results

Does the tendency towards stagnation captured by the Baran ratio predict the likelihood and intensity with which firms opt to allocate funds to shareholders via repurchases? To consider this question in this section, we present two sets of econometric specifications. Our two-part estimation strategy accounts for that a sizeable share of firms each year do not repurchase stock or pay dividends (as shown in Fig. 3b), implying that the zero observations are likely governed by a different data generating process than the positive values of payouts (Belotti et al. 2015). We, first, use a series of linear probability models to consider whether firms in industries with a greater stagnation tendency are more likely to make these shareholder payouts. We show that a lower industry-level Baran ratio is associated with a statistically and economically significant increase in firms’ propensities to make shareholder payouts and, in particular, to repurchase shares, both on impact and over time. Second, we turn to the set of firms that do make these payouts and show that — among these firms — the magnitudes of both dividends and repurchases are also larger, and also that a particularly substantive rise occurs in repurchases over time as firms readjust their priorities in response to industrial stagnation.

3.1 Industrial stagnation and firms’ propensity to repurchase shares

We begin by asking whether a stronger tendency towards stagnation implies firms are more likely to make shareholder payouts and, in particular, repurchase stock. To consider this question, we estimate linear probability models that regress the likelihood that a firm makes shareholder payouts on its industry-level Baran ratio and a set of controls:

In this specification, the dependent variable \(Paidou{t}_{i,t}\) is a binary variable identifying whether firm \(i\) made shareholder payouts in year \(t\); \(Bara{n}_{k,t}\) is the average Baran ratio in year \(t\) across the firms in its industry \(k\), but excluding firm \(i\); \({\mathrm{ln}\left(assets\right)}_{i,t}\) denotes the natural log of assets; and \({X}_{i,t}^{^{\prime}}\) is a vector of firm-level controls.Footnote 19 Note that, by excluding each firm \(i\) from the key explanatory variable (\(Bara{n}_{k,t}\)), we construct this explanatory variable to be exogenous with respect to the dependent variable (\(Paidou{t}_{i,t}\)).Footnote 20 We also control for firm fixed effects (\({\alpha }_{i}\)) and year fixed effects (\({\gamma }_{t}\)), and cluster standard errors at the firm level. The firm fixed effects, in particular, control for time-invariant unobservable factors related both to the firm itself and, also importantly, to the industry in which that firm operates.Footnote 21

In Tables 1 and 2, we show results of this specification for three versions of the dependent variable, which measure if a firm repurchased shares (Columns 1–2), paid dividends (Columns 3–4), or made any form of shareholder payouts (Columns 5–6). In Table 1, the dependent variables are equal to one if firm \(i\)made shareholder payouts in year \(t\) and zero otherwise. In Table 2 we instead set the dependent variable equal to one if firm \(i\) made shareholder payouts in year \(t\), \(t+1\), and/or \(t+2\). This second set of specifications accounts for lags in the impact of industrial stagnation on firm decision-making, as well as lumpiness in share repurchase plans, wherein — even among firms that do repurchase shares — years with repurchases tend to be followed by years without. This lumpiness suggests that a 3-year window may more fully capture repurchase decisions than a 1-year relationship. A specifically 3-year interval is indicated by Stephens and Weisbach (1998), who show that firms acquire an average of 74% to 82% of the shares in their repurchase targets within 3 years of a repurchase announcement (see also Bhargava 2010).

To begin, consider Columns 1 and 2 of Table 1, in which the dependent variable is defined by whether firm \(i\) repurchased shares in year \(t\). The main coefficient of interest is \({\beta }_{1}\), which describes the relationship between the average industry-level Baran ratio and the likelihood that a firm repurchases shares. Following the discussion above, we expect that firms in industries with greater declines in the average share of surplus allocated towards physical investment are more likely to target shareholder value by repurchasing stock. In other words, a decline in the Baran ratio can be interpreted as an industry-level signal about investment opportunities: as other firms in firm \(i\)’s industry invest less surplus in physical capital, firms take this as a signal that such investment is a poor use of funds and instead allocate these funds towards shareholder payouts.

In Column 1, we begin by showing the relationship between the average industry Baran ratio and the probability of repurchasing shares, controlling for firm assets to capture firm size. Consistent with the hypothesis above, the key coefficient of interest indicates that a decline in the average Baran ratio across firms in industry \(k\) (excluding firm \(i\)) is associated with a statistically significant increase in the probability that firm \(i\) repurchases stock. The magnitude of the estimate is, also, economically meaningful. To highlight economic magnitudes, we report standardized coefficients for the Baran ratio, as well as the unconditional probability of repurchasing shares, in the bottom panel of Table 1.Footnote 22 The estimates in Column 1 indicate that a one standard deviation decline in the Baran ratio is associated with a 2.78 percentage point higher likelihood of repurchasing shares; given the unconditional likelihood that 31.1% of firms repurchase shares, this estimate is economically meaningful.

In turn, Column 2 shows that this result is strongly robust to the inclusion of additional firm-level controls that may also explain a firm’s likelihood of repurchasing stock, including the (natural log of) debt, the profit rate on fixed capital, and financial profitability.Footnote 23 Controlling for debt accounts for a firms’ capital structure and the possibility that managers may elect to repurchase shares in order to modify the relative shares of equity and debt (e.g., by borrowing in order to repurchase stock). Firms with higher debt burdens may, furthermore, be more constrained in their ability to allocate funds towards shareholder payouts, all else equal. Consistent with this expectation, the estimates in Column 2 indicate that higher debt is associated with a lower (and statistically significant) probability of repurchasing shares. In turn, the relationship between profitability and repurchases is a priori less clear. On the one hand, higher profitability may capture strong firm-level investment opportunities, independently of the average tendency in an industry to allocate surplus towards investment. Strong investment opportunities may make firms less likely to direct resources towards repurchases. On the other hand, by increasing the pool of available funds, higher profitability could also increase a firm’s propensity to repurchase shares. The estimates in Column 2, however, suggest an effectively zero (albeit imprecisely estimated) relationship between the firm-level profit rate on fixed capital and the likelihood of buying back stock. Finally, Column 2 captures a positive and strongly significant relationship between financial profitability and the probability of repurchasing shares, suggesting that higher financial profitability does direct firms towards shareholder payouts, either by increasing the pool of available funds or by reinforcing a reorientation towards financial activities.

The results in Columns 1 and 2, therefore, indicate that firms in industries with a stronger stagnation tendency are more likely to repurchase stock and, thereby, target shareholder value. These results are consistent with the theoretical hypothesis that stagnation is one factor underlying firms’ propensity to financialize and, in particular, underlying the financial behavior associated with shareholder value orientation. In the remaining columns of Table 1, we compare this result to estimations that instead consider the probability of paying dividends or of making any type of shareholder payout.Footnote 24 To begin, consider Columns 5 and 6, which focus on total shareholder payouts. These estimates highlight that, while a decline in the average industry-level Baran ratio is associated with a (statistically significant) increase in the probability of making shareholder payouts, the magnitude of this estimate is considerably smaller than in the case of repurchases. Specifically, a one standard deviation decline in the Baran ratio is associated with only a 0.91 percentage point higher probability of making any form of shareholder payouts, and this estimate must be evaluated relative to a far higher unconditional probability of making some sort of shareholder payouts (53.5%). In turn, Columns 3 and 4, which focus on the probability of paying dividends, capture an even smaller relationship between the industrial Baran ratio and the likelihood of dividend payouts, with a standardized coefficient of 0.38 percentage points. Thus, Columns 3–6 of Table 1 indicate that, when firms make shareholder payouts in the era of financialization, they aim to target the stock price, not simply release funds to shareholders. The prioritization of repurchases over dividends is consistent with the institutional changes surrounding executive pay and stock market turnover, discussed above.

These conclusions are reinforced by the results in Table 2, which replace the dependent variable with an indicator equal to one if firm \(i\) repurchases shares either in year \(t\), \(t+1\), or \(t+2\). These estimations consider the possibility of a lagged (or dynamic) relationship between the industrial Baran ratio and the likelihood of making shareholder payouts, wherein the signal created by a falling average share of surplus reinvested in fixed capital across other firms in the industry leads to higher repurchases either contemporaneously, or with a 1- or 2-year lag. Like in Table 1, Columns 1 and 2 of Table 2 show a negative and statistically significant relationship between the average industrial Baran ratio and the probability of repurchasing stock. These coefficients are, furthermore, on a similar order of magnitude to those in Table 1, wherein a one standard deviation decline in the average industrial Baran ratio is associated with a 2.99 percentage point increase in the probability of repurchasing shares (and 53.7% of firms repurchase shares in at least 1 of the 3 years \(t\), \(t+1\), and \(t+2\)). The fact that this magnitude is similar, despite the higher unconditional probability, indicates that much of this relationship is driven by the contemporaneous results in Table 1. In other words, when facing evidence of industrial stagnation over this period, firms quickly reorient their attention to improving their stock market performance.

In turn, Columns 3 and 4 of Table 2 turn to the probability of paying dividends over at least one of these 3 years. Like in Table 1, these estimates suggest a negative and statistically significant relationship between industrial stagnation and the probability of paying dividends, wherein a one standard deviation decline in the average industry-level Baran ratio is associated with a 0.74 percentage point higher probability of paying dividends over at least one of the next 3 years. Furthermore, this magnitude is almost twice as large as the estimate in Table 1, indicating that industrial stagnation not only makes firms more likely to pay dividends, but that this relationship also strengthens over time. Even with this increase, however, the coefficient remains only a quarter as large as that for the relationship between the average industry-level Baran ratio and the propensity to repurchase stock, suggesting that the key link lies in stock buybacks. Thus, these results capture that a decline in the average industry-level Baran ratio is associated with a robust increase in firms’ propensity to make shareholder payouts that is driven, most strikingly, by an increased probability of repurchasing stock.

In the appendix, we also show that these results are robust to alternative specifications, including a logistic specification; using an alternative measure of the Baran ratio defined as investment relative to the sum of profits and the change in inventories of final goods; and to specifications that impute zeros for missing values of repurchases and dividends (to consider the possibility that firms with missing values do not report these variables because they did not make these types of payments).Footnote 25

3.2 Does a stagnation tendency help explain the magnitude of share repurchases?

Finally, we turn to the magnitude of shareholder payouts, to ask if the average industrial Baran ratio is also associated with larger overall payouts. We estimate a similar specification to that in Sect. 3.1, but replace the binary left-hand side variable with a continuous variable describing the magnitude of repurchases:

where the dependent variable is the natural log of shareholder payouts for firm \(i\); the remaining regressors are defined equivalently to those in Sect. 3.1; and the log transformation adjusts for substantial skew in the level of shareholder payouts (even when restricting our attention to non-zero values). We, again, cluster standard errors at the firm level.

As in Sect. 3.1, we independently analyze repurchases, dividends, and total shareholder payouts and consider two variations of each dependent variable: First, in Table 3 we consider the natural log of payouts in period \(t\). Second, in Table 4 we use a forward-looking 3-year moving average of payouts over years \(t\), \(t+1\), and \(t+2\).Footnote 26 Like in Sect. 3.1, this 3-year moving average accounts for lumpiness in repurchase activity and considers the possibility that repurchases rise over time in response to a decline in the industrial Baran ratio. Finally, in each of these regressions, we restrict our attention to observations describing firms that do repurchase shares (or pay dividends or make shareholder payouts, depending on the dependent variable).

In Columns 1 and 2 of Table 3 we begin with results for estimations in which the dependent variable is (the natural log of) repurchases in period \(t\). Column 1, which begins by controlling only for total assets, captures that — among firms that repurchase shares — a decline in the average industrial Baran ratio is associated with a positive and statistically significant increase in the level of repurchases. The estimate implies that a one standard deviation (0.29) decline in the average Baran ratio across all firms (excluding firm \(i\)) in firm \(i\)’s industry \(k\) is associated with 6.3% higher repurchases. In Column 2, we show that this estimate is strongly robust to also including the additional controls introduced in Sect. 3.1 (the natural log of debt, the profit rate, and the financial profit rate). In turn, Columns 1 and 2 of Table 4 show that, when we consider average repurchases over not just the current period but also the next 2 years, the magnitude of this estimate increases markedly. In each case, the estimates imply that a one standard deviation unit decline in the average industrial Baran ratio is associated with a 9.2% rise in average repurchases over this 3-year span. Thus, these results suggest that industrial stagnation is not only a contemporaneous signal to allocate surplus towards targeting shareholder value, but also leads to a longer-term readjustment of managerial priorities.

In turn, the remaining columns of Tables 3 and 4 compare these results to those obtained when, instead, considering (the natural logs of) dividends and total shareholder repurchases. Consider, first, dividend payments. Columns 3 and 4 of Table 3 capture a statistically significant, inverse relationship between dividend payments and the industry-level Baran ratio in any period \(t\), and the corresponding columns in Table 4 highlight that this relationship strengthens when considering average dividends over a 3-year period. More specifically, a one standard deviation decline in the Baran ratio is associated with a contemporaneous increase in dividends of 5.4% and 5.5% in Columns 3 and 4 of Table 3, respectively. In turn, the magnitude of this relationship strengthens over the forward-looking 3-year interval, to 7.7% and 7.8% in Columns 3 and 4 of Table 4. Like with repurchases, a tendency towards industrial stagnation is, therefore, associated with larger dividend payouts to shareholders. However, while the contemporaneous coefficients on repurchases and dividends are of very similar magnitudes (6.3% and 5.4%, respectively), there is a greater differential between the longer-term estimates for repurchases and dividends in Table 4 (9.2% and 7.7%, respectively). This differential captures that repurchases respond relatively more strongly than dividends to the industrial stagnation tendency captured by the Baran ratio over time.Footnote 27

Thus, the tendency towards stagnation reflected in the declining industry-level Baran ratio is associated with larger shareholder payouts, and, over time, these payouts are increasingly dominated by repurchases. These results build on the intuition from the linear probability models in Sect. 3.1, which indicate that a decline in the average industrial Baran ratio increases a firm’s likelihood of making shareholder payouts and, in particular, repurchasing shares. In turn, the fixed effects results indicate that, among firms that do make these payouts, the level is also higher and rises over time. Thus, the post-1980 tendency towards stagnation in the US economy has not only led more firms to repurchase stock, but has also driven larger payouts as firms increasingly direct their attention towards maximizing shareholder value. Finally, while firms initially release more funds to shareholders as both dividends and repurchases, they subsequently focus their attention on buybacks, which directly target stock price-based measures of shareholder value.

4 Discussion and conclusions

The discussion and estimation results in this paper provide empirical support for the hypothesis that a post-1980 tendency towards industrial stagnation in the US economy, defined as an average decline in the utilization of surplus for capital accumulation within an industry, contributes to both the likelihood that firms buyback stock and to the magnitude of shareholder payouts. We, first, show that a decline in the average share of surplus allocated towards investment within an industry is associated with a higher probability of repurchasing shares. This result links firms’ growing tendency to allocate surplus to shareholders via shareholder payouts — and, in particular, via repurchases — in the era of financialization to a signal provided by a decline in the average industry-level Baran ratio that investment opportunities within that firm’s industry are lacking.

Second, this tendency towards industrial stagnation also helps explain the rising magnitude of shareholder payouts. A fall in the average industry-level Baran ratio is associated with a contemporaneous rise in both repurchases and dividends, indicating that — upon the signal that a firm’s industry is stagnating — firms allocate more funds (conditional on firm size) towards these payouts. This increased allocation of funds towards shareholder payouts rises over time and, in the process, becomes increasingly dominated by repurchases. These results suggest that, while the flexibility of dividend payments allow firms to release funds to shareholders on impact, firms increasingly prioritize repurchases over time (where repurchase plans are generally announced in advance to take place over a pre-specified number of years).

By drawing a new empirical link between industrial stagnation and financialization in the post-1980 US economy, these results provide empirical support for an important theoretical hypothesis regarding the drivers of the financialization of nonfinancial firms. In doing so, these results complement the existing literature on financialization. To date, this literature has focused largely on the consequences of increasingly “financialized” firm behavior, finding evidence, for example, that greater financial payouts and/or repurchases are associated with an investment slowdown (see, e.g., Stockhammer 2004; Orhangazi 2008; and Davis 2018 in the US context). Less empirical work has focused, however, on the factors that have generated increasingly “financialized” firm behavior. The most well-developed explanation lies in a wide-reaching set of institutional and regulatory changes that have both encouraged and made it easier for managers to repurchase stock. As discussed in Sect. 2.2, above, these changes include a growing market for corporate control, changes in SEC rules and regulations, and the emergence of stock-based executive pay.

Our results add an additional layer to this interpretation: as these institutional changes have encouraged shareholder value orientation among firm managers, managers’ sensitivity to these institutional changes has also been shaped by weakening opportunities for capital accumulation. These results, therefore, suggest that if these institutional changes had occurred in the context of strong and growing opportunities for real investment (i.e., in the absence of stagnation), managerial responsiveness to these changes may have been weaker. Put differently, our results suggest that a post-1980 stagnation tendency strengthens managerial responsiveness to these institutional changes, further encouraging managers to release funds to shareholders via stock repurchases.

Finally, the discussion in this paper suggests at least two directions for future research. First, the results raise further questions about the intersection between industrial stagnation, financialization, and rising industrial concentration. Insofar as monopoly power creates the excess capacity that drives the stagnation tendency emphasized in this paper, the results suggest a role for further analysis of the intersection between rising industrial concentration in the US economy and financialization. Theory, also, suggests that, while the “financial explosion” in the post-1980 US economy has provided an outlet for surplus absorption, these outlets may also be unstable and portend future crisis (e.g., Foster 2008). This possibility raises important questions about the interactions between financialization, instability, and the tendency towards stagnation. Second, the results in this paper raise questions of whether differing degrees of industrial stagnation across economies help explain differing degrees of financialization. While our analysis (and data) is specific to the US case, the mechanisms we explore raise the possibility that differing degrees of stagnation across countries may also contribute to different trajectories of, or experiences with, financialization. The relationship between stagnation, stages of economic development, and financialization in a comparative international perspective is an exciting area for future research.

Notes

Xu (2019)’s analysis is at the macroeconomic level and uses the profit share of GDP. We use the profit share of value added to translate this concept to firm-level accounting data.

We drop observations classified as finance, insurance, or real estate by either SIC or NAICS codes (SIC codes 6000–6799, and NAICS codes with first two digits of 52 or 53) and restrict to firms incorporated in the USA and reporting in US dollars (using Compustat variables FIC and CURCD). We, also, drop observations with negative sales, total assets, or financial payouts (repurchases, dividends, or interest payments) (0.07% of the sample), each of which is conceptually restricted to be greater than or equal to zero.

Total debt is the sum of current debt (DLC) and long-term debt (DLTT) if these variables are non-missing; if (at least one of) these variables are missing and total debt (DT) is non-missing, we use DT to define total debt. This definition of the financial profit rate and financial assets (the sum of receivables, RECT; cash and short-term investments, CHE; other current assets, ACO; investments and advances, IVAEQ and IVAO; and other assets, AO) follows Davis (2017).

The choice of deflator does not affect our results.

Following Donangelo et al. (2019), we set \(\Delta INV{G}_{i,t}\) to zero when either \(INVF{G}_{i,t}\) or \(INVF{G}_{i,t-1}\) is missing.

Because the variable XLR includes all labor costs, including those for supervisory workers, it implies an upper (lower) bound on the labor (profit) share.

The employment variable includes all employees of consolidated subsidiaries; part-time and seasonal employees; officers; and full-time equivalent employees. It does not include consultants, contract workers, or employees of unconsolidated subsidiaries. While there is no way to distinguish between part- and full-time employment using Compustat data, Donangelo et al. (2019) show that this measure of average employment provides a good proxy for labor costs. Donangelo et al. (2019) use the Fama–French 17-industry categories; our measure of the Baran ratio is robust to these classifications. We use 2-digit SIC codes to ensure comparability with the rest of our analysis, below.

We, also, compare our main econometric results to an alternative measure of the Baran ratio that does not rely on this imputation method, defined as investment relative to the sum of profits and the change in inventories (see Appendix Tables 8, 10, and 11). In the main body of the paper, however, we define the profit share as the residual of the labor share to explicitly emphasize the role of increased worker exploitation (i.e., stagnant wages despite rising productivity) (Kotz 2008) in driving the stagnation tendency emphasized in this paper.

The first two digits of SIC codes distinguish major groups within economic divisions (e.g., the chemicals industry is a major group within the manufacturing division). We use SIC codes because Compustat has a far higher incidence of missing NAICS codes. However, the regression results are highly robust to 2-digit NAICS classifications.

This trend occurs across sectors; thus, the declining across-industry average is not the artifact of a major decline within a single large industry or sector (such as manufacturing).

In Figure 5 in the appendix, we plot the evolution of the numerator (investment share) and denominator (profit share, or surplus) of the Baran ratio. These trends highlight that, while both a falling numerator and rising denominator contribute to the declining Baran ratio over this period, the profit share plays a particularly key role. Thus, the falling Baran ratio reflects, in large part, a falling labor share of income.

For a survey discussing this institutional evolution in more detail, see Davis (2017).

Net equity issuance is new stock issues (Compustat item SSTK) less gross repurchases (PRSTKC), normalized by total equity (SEQ). To aggregate each component variable, we first sum across all firms in each year, and then construct the final series. This series, therefore, measures net equity issuance at the sector level.

When interpreting magnitudes, note that shareholder payouts are part of a firm’s cash flows and, therefore, are not shares of assets. Normalizing by total assets ensures that the ratios in Fig. 3a are positive for each firm in each year, thereby avoiding complications in interpretation of the results that arise when normalizing by firm-level equity (which can be negative). The overall trends, however, are insensitive to this choice of normalization.

Tax code changes may, also, have played a role in this substitution of share repurchases for dividends. First, capital gains are taxed at more favorable rates than ordinary income (which includes dividend income), creating an incentive for managers to substitute share repurchases for dividends to maximize shareholder returns (Grullon and Michaely 2002). Even after the Tax Reform Act of 1986 reduced the relative tax advantage of capital gains, the gap between these two tax rates remained. Second, a 1993 change to the tax code stipulating a $1 million cap on the tax deductibility of nonperformance-based pay, without a similar cap on “performance-based” pay (including stock-based pay that increases with the stock price) also reinforced growing managerial orientation to shareholder value and the stock price as measures of firm performance (Stout 2012; Davis 2016).

Because a firm can repurchase shares and pay dividends in the same year, the sum of the shares of firms repurchasing shares and paying dividends will generally not equal the share of firms making any shareholder payouts.

We use linear probability models rather than logistic regressions both because they have a more intuitive interpretation and because, in our case, none of the predicted probabilities fall outside of the unit interval, such that the estimates are considered largely unbiased and consistent. Linear probability models with robust standard errors provide a good guide in applications for which the results do not produce a large share of predicted values outside the zero–one range (Cameron and Trivedi 2005; Horrace and Oaxaca 2006). The results are, however, robust to instead using a logistic specification; we report these results in Table 7.

Nonetheless, we avoid making causal claims in the interpretation of these regressions. If, for example, shareholder value orientation is also clustered by industry, then reverse causality problems may persist despite the exclusion of each individual firm from the industry-level measure. In this regard, it is relevant to note that the descriptive evidence in Davis (2016), for example, finds that repurchase growth follows similar trends across industries, suggesting a lack of industry-level clustering. Nonetheless, the extent to which shareholder value orientation is clustered by industry is an important issue for future research aiming to untangle causality in empirical work on financialization.

Time-invariant industry-level factors beyond the Baran ratio, which may also explain a firm’s tendency towards financialization, are absorbed by these firm fixed effects. We include firm-level, rather than industry-level, fixed effects because firm fixed effects also pick up firm-specific factors that are not captured by industry dummies.

The unconditional probabilities in Table 1 differ somewhat from those reported in the descriptive statistics in Appendix Table 6 because the calculations in Table 6 do not restrict to non-missing observations of the regression variables in Columns 1 and 2. These differences in sample do not affect the interpretation of results.

We use a log plus one transformation for debt to avoid dropping observations with zero debt from the regression.

The observation count in Columns 3–4 is higher than in Columns 5–6 due to missing values. To be included in Columns 5–6 either (i) dividends are positive (in which case repurchases can be positive, zero, or missing), or (ii) repurchases are positive (in which case dividends can be positive, zero or missing), or (iii) both dividends and repurchases are zero. This third criterion, which avoids assuming missing values of repurchases or dividends are zero, is stricter than in Columns 1–4 (which require non-missing data on repurchases or dividends). These results are, however, strongly robust to replacing missing values of repurchases and dividends with zeros (i.e., assuming that firms that do not report repurchase or dividend data did not make this type of payment) and, thereby, using identical samples across specifications. We show these results in Appendix Table 9.

Table 7 shows estimates that use a logistic specification; Table 8 measures the Baran ratio as investment relative to the sum of profits and the change in inventories of final goods; and Table 9 shows results that impute zeros for missing values of repurchases and dividends. In the interest of space, we only include results for the contemporaneous version of the dependent variable.

To construct this variable, we assign any missing observations a value of zero to avoid restricting the sample to firms with non-missing values of repurchases for all 3 years (\(t\), \(t+1\), and \(t+2\)).

In Tables 10 and 11, we show these results are robust to instead measuring the Baran ratio as the ratio of investment to the sum of profits and the change in inventories of final goods for both the contemporaneous dependent variable (Table 10) and the 3-year moving average (Table 11). While the coefficients describing the contemporaneous link between this alternative measure of the Baran ratio and repurchases are statistically insignificant in Table 10, the sign of the estimate is preserved and total payouts are significant. The 3-year estimates in Table 11, also, retain their statistical significance, reiterating that a dynamic readjustment towards repurchases takes place after a decline in the Baran ratio. Finally, note that, as we restrict the sample used for the fixed effects regressions to non-zero observations of shareholder payouts, we do not include results imputing zeros for missing values of shareholder payouts.

References

Aglietta M (2000) Shareholder value and corporate governance: some tricky questions. Econ Soc 29(1):146–159

Aglietta M, Bretton R (2001) Financial systems, corporate control and capital accumulation. Econ Soc 30(4):433–466

Akkemik K, Özen S (2014) Macroeconomic and institutional determinants of financialization of non-financial firms: case study of Turkey. Soc Econ Rev 12(1):71–98

Baran P, Sweezy P (1966) Monopoly Capital. Monthly Review Press, New York

Barradas R, Lagoa S (2017) Financialization and Portuguese real investment: A supportive or disruptive relationship? J Post Keynesian Econ 40(3):413–439

Belotti F, Deb P, Manning W, Norton E (2015) twopm: two-part models. The Stata Journal 15(1):3–20

Bhargava A (2010) An econometric analysis of dividends and share repurchases by US firms. J R Stat Soc Ser A Stat Soc 173(3):631–656

Boyer R (2000) Is a finance-led growth regime a viable alternative to Fordism? A Preliminary Analysis. Econ Soc 29(1):111–145

Cameron C, Trivedi P (2005) Microeconometrics: Method and applications. Cambridge University Press, New York

Crotty J (2003) The neoliberal paradox: the impact of destructive product market competition and impatient finance on nonfinancial corporations in the neoliberal era. Rev Radic Polit Econ 35(3):271–279

Davis L (2016) Identifying the ‘financialization’ of the nonfinancial corporation in the US economy: a decomposition of firm-level balance sheets. J Post Keynesian Econ 39(1):115–141

Davis L (2017) Financialization and investment: a survey of the empirical literature. J Econ Surv 31(5):1332–1358

Davis L (2018) Financialization and the non-financial corporation: an investigation of firm-level investment behavior in the United States. Metroeconomica 69(1):270–307

Davis L, Orhangazi Ö (2020) Competition and monopoly in the U.S. economy: what do the industrial concentration data show? Compet Chang 25(1):3–33

Deb P, Norton EC (2018) Modeling health care expenditures and use. Annu Rev Public Health 39(1):489–505

Demir F (2009) Financial liberalization, private investment, and portfolio choice: financialization of real sectors in emerging markets. J Dev Econ 88(2):314–324

Despain H (2015) Sweezyian financial instability hypothesis—Monopoly Capital, inflation, financialization, inequality and endless stagnation. Int Crit Thought 5(1):67–79

Donangelo A, Gourio F, Kehrig M, Palacios M (2019) The cross-section of labor leverage and equity returns. J Financ Econ 132(2):497–518

Dünhaupt P (2017) Determinants of labour’s income share in the era of financialization. Camb J Econ 41(1):283–306

Fligstein N (1990) The Transformation of Corporate Control. Harvard University Press, Cambridge

Foster J (2008) The financialization of capital and the crisis. Mon Rev 59(11):1–19

Greenwald D, Lettau M, Ludvigson S (2019) How the wealth was won: factor shares as market fundamentals. NBER Working Paper No. 25769

Grullon G, Michaely R (2002) Dividends, share repurchases, and the substitution hypothesis. J of Fin 57(4):1649–1684

Grullon G, Larkin Y, Michaely R (2019) Are U.S. industries becoming more concentrated? Rev Finan 23(4):697–743

Guschanski A, Onaran Ö (2018) The labor share and financialisation: evidence from publicly listed firms. Greenwich Papers in Political Economy No GPERC59

Horrace W, Oaxaca R (2006) Results on the bias and inconsistency of ordinary least squares for the linear probability model. Econ Lett 90(3):321–327

Jiang Z, Kim K, Lie E, Yang S (2013) Share repurchases, catering, and dividend substitution. J Corp Finan 21:36–50

Kohler K, Guschanski A, Stockhammer E (2019) The impact of financialisation on the wage share: a theoretical clarification and empirical test. Camb J Econ 43(4):937–974

Kotz DM (2008) Contradictions of economic growth in the neoliberal era: accumulation and crisis in the contemporary U.S. economy. Rev Radic Polit Econ 40(2):174–188

Lapavitsas C (2011) Theorizing financialization. Work Employ Soc 25(4):611–626

Lazonick W (2009) Sustainable prosperity in the new economy? Business organization and high-tech employment in the United States. Kalamazoo: W.E. UpJohn Institute

Lazonick W (2014) Innovative enterprise and shareholder value, Academic-Industry Research Network (AIR) Working Paper #14–03/01

Lazonick W, O’Sullivan M (2000) Maximizing shareholder value: a new ideology for corporate governance. Econ Soc 29(1):13–35

Lin KH, Tomaskovic-Devey D (2013) Financialization and U.S. income inequality, 1970–2008. Am J Sociol 118(5):1284–1329

Magdoff F, Foster J (2014) Stagnation and financialization: the nature of the contradiction. Monthly Review 66(1):1–24

Magdoff H, Sweezy PM (1987) Stagnation and the financial explosion. Monthly Review Press

McDonough T, Reich M, Kotz K (2010) Contemporary capitalism and its crises: social structure of accumulation theory for the 21st century. Cambridge University Press

Onaran Ö, Stockhammer E, Grafl L (2011) Financialisation, income distribution and aggregate demand in the USA. Camb J Econ 35(4):637–661

Orhangazi O (2008) Financialisation and capital accumulation in the non-financial corporate sector. Camb J Econ 32(6):863–886

Seo H, Kim H, Kim J (2016) Does shareholder value orientation or financial market liberalization slow down Korean real investment? Rev Radic Polit Econ 48(4):633–660

Skinner DJ (2008) The evolving relation between earnings, dividends, and stock repurchases. J Financ Econ 87(3):582–609

Stephens C, Weisbach M (1998) Actual share reacquisitions in open-market repurchase programs. J Financ 53(1):313–333

Stockhammer E (2004) Financialisation and the slowdown of accumulation. Camb J Econ 28(3):371–404

Stockhammer E (2005) Shareholder value orientation and the investment-profit puzzle. J Post Keynesian Econ 28(2):193–215

Stout L (2012) The shareholder value myth: how putting shareholders first harms investors, corporations and the public. Berett-Koehler Publishers Inc, San Francisco

Tori D, Onaran Ö (2018) The effects of financialization on investment: evidence from firm-level data for the UK. Camb J Econ 42(5):1393–1416

Tori D, Onaran Ö (2020) Financialization, financial development and investment: evidence from European non-financial corporations. Soc Econ Rev 18(3):681–718

Van Treeck T (2008) Reconsidering the investment-profit nexus in finance-led economies: an ARDL-based approach. Metroeconomica 59(3):371–404

Xu Z (2019) Economic surplus, the Baran ratio, and capital accumulation. Mon Rev 70(10):25–39

Author information

Authors and Affiliations

Corresponding author

Additional information

We would like to thank Randy Albelda for detailed comments on previous drafts of this article.

Appendices

Appendix A

The investment share of value added and the profit share (1971–2019). a Investment share of value added. b The profit share. Notes: This figure disaggregates the numerator of the Baran ratio (capital expenditure relative to value added) in panel (a) from the denominator (the profit share of value added, defined as one minus the labor share of income) in panel (b). Each ratio is trimmed at the 1st and 99th percentile to account for outliers. For variable definitions, see Sect. 2

Appendix B, robustness checks

Rights and permissions

About this article

Cite this article

Davis, L., McCormack, S. Industrial stagnation and the financialization of nonfinancial corporations. Rev Evol Polit Econ 2, 459–491 (2021). https://doi.org/10.1007/s43253-021-00043-6

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s43253-021-00043-6