Abstract

This paper establishes a reference chronology for the Russian economic cycle from the early 1980s to mid-2015. To detect peaks and troughs, we tested nine monthly indices as a reference series, three methods of seasonal adjustments (X-12-ARIMA, TRAMO/SEATS, and CAMPLET), and three methods for dating cyclical turning points (local min/max, Bry–Boschan method, and Markov-switching model). As these more or less formal methods led to different estimates, any sensible choice was only possible on the grounds of informal considerations. The final set of turning points looks plausible and separates expansions and contractions in an explicable manner, but further discussions are needed to establish a consensus between experts.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In reality, any economic process unfolds over time and it is commonly believed that the patterns of an economic process are strongly dependent on the phase of the national economic cycle. If levels of economic activity are high then expectations and actions of almost all economic agents would differ from the expectations and actions under conditions of low levels of economic activity. Hence, to monitor, analyze, understand, and forecast short- and medium-term economic processes one should discriminate between the phases of expansion and contraction in economic activity. The easiest way to do this is to use a reference chronology of turning points that separates cyclical phases from each other. So, it is not surprising that dating cyclical turning points is an issue that has attracted the attention of researchers for decades. In fact, this problem usually arises in two similar but still different situations.

First, if the “true” historical set of peaks and troughs is known, then the quality of one or the other formal method—its capability to reproduce this historical set and to identify a new turning point in real time—is in focus. A lot of papers devoted to the US business cycle are usually of this kind: they propose some new methods, new modifications of the old methods, compare several methods, and so on (see for example: Chaffin and Talley 1989; Stock and Watson 1993; Boldin 1994; Kim and Nelson 1998; Birchenhall et al. 1999; Filardo 1999; Layton and Katsuura 2001; Sarlan 2001; Sephton 2001; Camacho and Perez-Quiros 2002; Anas and Ferrara 2004; Peláez 2005; Chauvet and Hamilton 2006; Chauvet and Piger 2008; Hamilton 2011; Golosnoya and Hogrefe 2013; Liu and Moench 2016, and others). This is not surprising because the reference dates defined by the Business Cycle Committee of the National Bureau of Economic Research (NBER) are commonly accepted. From time to time, some authors (e.g. McNees 1987; Diebold and Rudebusch 1992; Boldin 1994; Romer 1994; Berge and Jordà 2011; Stock and Watson 2014) express their doubts on the accuracy of all the NBER’s estimates, but this has never had any practical outcome: as a rule, all subsequent research still uses exactly the same peaks and troughs.

The second situation is typical for countries with no established and/or commonly recognized set of cyclical turning points. In this case, a researcher may use strictly the same methods for dating peaks and troughs, but he has no formal criterion to prove the accuracy of his estimates. As a rule, the precision of these data sets may be challenged but authors have no real alternative except to apply one or more methods to several time series and to evaluate the results (see for example Layton 1997 for Australia; Mejía-Reyes 1999 for seven countries in Latin America; Christoffersen 2000 for four Nordic countries; Rand and Tarp 2002 for 15 emerging countries; Artis et al. 2004 for the Eurozone; Bruno and Otranto 2004 for Italy; Venter 2005 for South Africa; Andersson et al. 2006 for Sweden; Schirwitz 2009 for Germany; Fushing et al. 2010 for 22 OECD countries; Polasek 2010 for Iceland; Poměnková 2010 for the Czech Republic; Alp et al. 2012 for Turkey; Cross and Bergevin 2012 for Canada; Tsouma 2014 for Greece; Martínez-García et al. 2015 for 85 countries; Aastveit et al. 2016 for Norway). It can be argued that a reference chronology of cyclical turning points should be constructed for every country that has cyclical fluctuations.

But what may one do if different methods give different results (and the reality is always of this kind)? In fact, one may recognize that formal results depend heavily on at least seven alternatives (items) with corresponding a priori choices. They are:

-

1.

type of cycle (business cycle, growth or growth rate cycle);Footnote 1

-

2.

frequency (monthly or quarterly);

-

3.

general approach to dating cyclical turning points (special decisions of national or supranational dating committees;Footnote 2 extraction of unobservable cyclical factors from a multiplicity of various economic and financial indicators; using the concept of reference series)

-

4.

set of time series to be analyzed (GDP, industrial production, basic activities’ output, etc.);

-

5.

data vintages (real-time or the latest revision);

-

6.

method of seasonal adjustments (X-12 ARIMA, TRAMO/SEATS or some other); and

-

7.

method for detecting cyclical turning points (Bry–Boschan’s, Markov-switching model or some other).

In theory, the superiority of any alternative choice is not obvious; various decisions may be justified. As a palliative, one may check several concepts, indicators, and methods, and then make the final decision relying not only on quantitative but also on qualitative criteria. Of course, in this situation, there is not much sense in introducing a “more accurate” method for dating cyclical turning points: there are no “true” turning points to compare them with.

In Russia, there is no official or commonly recognized set of peaks and troughs.Footnote 3 Sometimes one or two turning points have been estimated inter alia (see, for example, Belyanova and Nikolaenko 2012; Smirnov 2014). Only Belyanova and Nikolaenko (2013) and Dubovskiy et al. (2015) were focused on dating turning points of the Russian economic cycle. Later on, we shall discuss their results in more detail and give some arguments for adopting them with caution. For now, we note only that the turning points proposed by the Organisation for Economic Co-operation and Development (OECD 2017) relate to the concept of growth (not business or economic) cycles, and that those proposed by the Economic Cycle Research Institute (ECRI 2016) are estimated using unknown procedures and on an unknown statistical basis and therefore cannot be independently reproduced by scientific methods.Footnote 4 Hence, dating of turning points for the Russian cycle is still a relevant issue. It is only in this way that all other research and expertise focused on Russian cyclical fluctuations can gain a solid foundation. Dating historical turning points—the main purpose of this paper—should be the first step, followed by testing the cyclical behavior of a wide range of indicators, the selection of leading, coincident, and lagging indices, the calculation of composite ones, and—the last and the most intriguing step—the forecasting of an oncoming turning point in real-time.

In the Sect. 2, we discuss our own a priori choices for the seven alternatives mentioned above and describe the exact time series used. In Sect. 3, we apply all the methods previously chosen to available time series and discuss the results: their initial diversity, additional informal criteria for choosing the most appropriate options, and the final set of Russian cyclical turning points. Section 4 concludes.

2 Background, Methods, and Data

2.1 Seven A Priori Choices

The first item we have to determine is which concept of cycle to choose: business (or economic), growth (mid-term fluctuations around the trend), or growth rate cycle. Each kind of cycle has its own set of turning points, and these may or may not coincide (see Zarnowitz and Ozyildirim 2002, p. 42); no empirical dating can be undertaken without a predetermined choice between these concepts and in some senses, this choice is arbitrary. Economic theory usually alludes to business cycles (ups and downs in economic activity). The NBER’s long empirical tradition for the US (it was inherited and supported by CEPR and CODACE for the Eurozone and Brazil, respectively) also follows this direction. But an alternative approach based on monitoring growth cycles is also widely recognized; in particular, it has been used by the OECD for decades and for dozens of countries, including Russia. Analyses of growth rate cycles are less common but also exist in China, for example (see Junli et al. 2014). This diversity means that the choice is not a foregone one and rather optional. On the other hand, it does not mean that it is fully arbitrary. The choice should depend upon those changes in economic trajectory that are commonly considered as important ones. If fast economic growth is permanent (like in China over the last 40 years), even a decrease in tempo from a “very high” to a “high” level may be felt as disturbing; in such a case the growth rate cycles may be the focus. If a slight positive trend is stable (many believe that this is typical for advanced economies), then an “excessive” or an “insufficient” growth would capture the attention, and the OECD’s choice of growth cycles would be suitable. Finally, if a national economy is sensitive to political, financial, technological, and/or other kinds of internal and external shocks; if there is no reliable estimation of the trend or there is no stable trend at all (as is typical for emerging economies, according to Aguiar and Gopinath 2007), then the concept of business or economic cycles will have priority.

In modern Russia, there is no stable output trend and growth rates are volatile. Hence, growth cycles and growth rate cycles are not very convenient. But the straightforward concept of business cycles is also questionable because—remember the classical definition—“business cycles are a type of fluctuation found in the aggregate economic activity of nations that organize their work mainly in business enterprises” (Burns and Mitchell 1946, p. 3). “Business enterprises” in the Russian economy are common nowadays, but they certainly did not exist during the Soviet period (until 1991) and were probably flawed during the transformation period (at least, until the mid-1990s). Is it enough to deny or doubt cyclicity in Russia? We insist that it is not. There were several recessions in Russia before the crash of the USSR and the long-run trajectory of the Russian economy is evidently a sequence of expansions and contractions.Footnote 5 Hence, the concept of economic cycles is suitable for the Russian context (let us not name them “business cycles”—to avoid solely terminological debates). There are definitely some mid-term ups and downs in the level of the Russian economic activity and turning points just on the edge between them. Dating those turning points is our aim.

The second item is about frequency. Our “strategic” long-term aim (but not the goal of this paper!) is to find leading indicators that are useful in predicting changes in the mid-term trajectory of the Russian economy. Taking into account the 1.5 month publication lag in regard to GDP (the most important quarterly macroeconomic indicator), the total delay in detecting a new turning point, using a GDP series, may be more than 4 months (and even twice that if one prefers to have information on two consecutive quarters). For monitoring economic activity in real time, this is too long a delay, and one would surely prefer monthly (not quarterly or annual) statistics. Hence, the basic data set of turning points for Russia (as for any other country) should also be at least monthly.

The third item concerns the general approach to dating turning points. Should the turning points be detected and declared by a special expert group (“dating committee”)? Or, perhaps, by extracting common (cyclical) waves from multi-indicator data sets with statistical methods? Or, alternatively, by referring to several (supposedly) coincident indicators? In Russia, there is a dearth of experts in economic cycles and most of the time series from available databases are too short. Hence, the first two opportunities are matters for the future. For now, referring to some coincident indicators is the only realistic way. Of course, there is some kind of circular reasoning here: it is rather justified to consider an indicator to be a coincident one if its turning points more or less coincide with the cyclical peaks and troughs of the total economy; but in our case just those peaks and troughs are unknown and have to be identified. The only way to exit this vicious circle is to date the Russian cyclical turning points with those indicators that are commonly considered as coincident.

Therefore, the fourth item is an outlining of a specific set of coincident monthly indicators for Russia. Naturally, the first idea is to try four indicators commonly used as coincident in other countries. They are: (a) employees on non-agricultural payrolls; (b) real personal income; (c) index of industrial production; and (d) manufacturing and trade sales. Belyanova and Nikolaenko (2013) was the first paper specially focused on dating turning points for the Russian economic cycle and it proposed just this logic in seeking the Russian analogues of these four indicators. However, this is not an easy task. First, there are some statistical shortages. In particular, any information on manufacturing sales is now absent in Russia, whereas all data on employment are very unreliable and subject to large revisions. Second, some of these indicators are scarcely coincident in Russia for economic reasons. Specifically, during recessions, Russian enterprises prefer to freeze or even cut wages and salaries rather than to fire employees (in market economies the opposite is usually true).Footnote 6 Besides, all “real” indicators adjusted for CPI are also not coincident (at least at peaks) because of significant devaluations that are usually lagging (owing to the Russian Central Bank’s unsuccessful efforts to avoid them). Those lagging devaluations have induced lagging inflation waves that shifted all “real” indicators to the right. That is why we decided to date turning points with indicators in “physical units” (these are described in detail in the next section).Footnote 7

The fifth item is the choice between “real time” and “latest available” time series. In the context of this paper, the answer is evident. As our aim here was to date turning points in a historical perspective, we preferred the latter (more precisely, as they were in August 2015). In the future, the final set of turning points should help to tune the system of leading indicators to be suitable for use in real time.

For the sixth and seventh items, we decided not to make a single choice but to test several options. For seasonal adjustments, we used three algorithms: X-12-ARIMA and TRAMO/SEATS (as they were implemented in the program Demetra, see Grudkowska 2011) as well as the lesser-known CAMPLET (see Abeln and Jacobs 2015). In the first two, a seasonal adjustment for any moment depends on the trajectory in future moments. For this reason, not only may a real-time estimate at the right end be unreliable, but historical estimates near cyclical turning points (peaks and troughs) might be biased: a peak shifted to the left and a trough to the right (see Bessonov and Petronevich 2013 for details). CAMPLET is supposedly free of this shortcoming; therefore, it may be helpful for controlling this effect.

As for a method for detecting cyclical turning points, we used three methods: simply taking the local maximum/minimum of seasonally adjusted indices; the Bry–Boschan method; and the Markov-switching model. We applied each of these methods to all indicators available just after seasonally adjusting them with all the procedures mentioned.

2.2 Methods

At first glance, the most natural method for dating turning points is to choose local maxima as peaks and local minima as troughs. If one defines the word “local” as being higher/lower than n-months before and n-months after (for example, for n = 6), then all the calculations are rather simple. The limitation is that any observed value of a reference indicator is always a sum of a cyclical wave and a random factor (if we suppose that seasonality is removed in a proper way); if one is interested in cyclical peaks and troughs then he has to extract this cyclical wave in advance. So, strictly speaking, this method of dating is not correct; however, we tried it as an obvious benchmark.

Hence, we used Bry and Boschan’s (1971) method, which is specially designed for extracting cyclical waves from time series with the help of specific smoothing algorithms, so the turning points are then detected on this extracted wave.Footnote 8

We also compared the results of these two non-parametric methods with the results of the Markov-switching model proposed by Hamilton (1989). We used the basic intercept-adjusted specification of the Markov-switching model:

where t is the time period, \( y_{t} \) is the series under consideration, in growth rates, \( \mu_{{S_{t} }} \) is the switching constant, \( S_{t} = \{ 0;1\} \) is the Markov chain with constant transition probabilities indicating the phase of the cycle (0 corresponds to expansion, 1 to recession), \( \varphi_{1} \),…, \( \varphi_{p} \) are the autoregressive coefficients, and \( \varepsilon_{t} \sim{\text{N}}(0,\sigma_{s}^{2} ) \) is the stochastic component. The number of autoregressive lags was chosen by minimizing the Hannan–Quinn information criterion (as suggested by Kapetanios 2001).Footnote 9 We only introduced the switch to the constant, which is the usual practice for a macroeconomic time series.Footnote 10 The intercept-adjusted specification was chosen over the mean-adjusted specification in order to guarantee a smooth transition to the new conditional mean, which is usually observed in the data.Footnote 11 To ensure the comparability with the output of the non-parametric methods, we also imposed a restriction on the minimum duration of each phase (6 months).Footnote 12 The inference of the model comes in the form of the smoothed probability of recession \( \Pr [S_{t} = 1|I_{T} ] \), where I T is the information available at the last observed period T. We consider the economy to be in recession in period t if \( \Pr [S_{t} = 1|I_{T} ] > 0.5. \)

2.3 Data

Industry is usually the sector most sensitive to cyclical fluctuations; so, indices of industrial production are of special interest for us.Footnote 13 The value added in this sector was 24% of the Russian GDP in 2015 which is much less than in 1981 (37%, according to the nonofficial estimates of Ponomarenko 2002). This clearly means that industry is now not as overwhelmingly important for the Russian economy as it was in the early 1980s. On the other hand, historical time-series for monthly industrial indices are much longer than for any other indicator; it would be reckless to simply ignore this information.

The first official monthly industrial index for Russia began in 1993. In 2003, the industrial classification used by Rosstat (the Russian State Statistical Committee) changed from the so-called OKONH to OKVED (analogies of SIC and NACE, correspondingly) and a new index was begun; some time later, the old index was discontinued and the new one was re-estimated from 1999. The flaw of the official index is a lack of methodological information; this was the main reason for calculating alternative industrial indices based on official information on output (in physical units) of hundreds of industrial goods. This work has been done since the beginning of the 1990s; taken together, three indices constructed by the same group of researchers cover the whole period from 1990 until now. One additional non-official monthly index of industrial production covers the period from January 1981 to December 1992. No other published information for Russian monthly industrial production is available.

All six industrial indices mentioned above, as well as their statistical sources, are listed in Table 1. There are also three indices of output of “basic activities” in the table. Two of them are official but for different industrial classifications (and hence for different time periods); the third is non-official. The index for basic economic activities includes: industry, agriculture, construction, transportation, retail trade, and wholesale trade. The methodology for the construction of this aggregate has not been published (and therefore is not known exactly), but its trajectory is definitely closer to the trajectory of the whole economy (or GDP) than the one for industry alone.

Thus, monthly information on industrial production began in January 1981; monthly information on output of basic activities began in January 1995. No single monthly indicator has existed for the whole period from the 1980s up to the current time. For this reason, we propose to use all the above-mentioned indices as coincident cyclical ones: each index for its own time frame. Results for each index should confirm or clarify the others.

Most of the listed indices are published in non-adjusted form; some others are seasonally adjusted with different procedures. To make our comparisons more accurate, we adjusted all the indices for their seasonal variations ourselves and used three procedures for this. In general, the outputs of the seasonal adjustment procedures are alike but some differences in details do exist; as we will show later, this may be important when dating cyclical turning points. All indices in their seasonally adjusted forms are shown in Fig. 1.Footnote 14

Indices of industrial output (IO) and basic activities’ output (BAO), 1981–2015. Note For abbreviations and sources see Table 1. Grey ovals mark fragments of trajectories where turning points are possible

3 Dating Peaks and Troughs: 1981–2015

3.1 “Longlist” of Turning Points

Of course, the picture is too variegated to date turning points in a simple way, but three conclusions are clear.

First (and most important), any turning point for Russia may be sought only inside four time intervals (they are marked with grey ovals): (a) at the end of the 1980s; (b) from the middle to the end of the 1990s; (c) somewhere in 2007–2009; and (d) somewhere in 2013–2015. All turning points lying in other time spans (if any) should be considered false. In particular, the very end of the 1980s and the first half of the 1990s was a definite contraction, related to the crash of the planned economy and the ensuing transformation of the economic system. Most of the 1980s and the first half of the 2000s, on the other hand, were definite expansions, with no cyclical turning points in either of them. We also consider 2012–2013 as a period of stagnation of the Russian economy; in our opinion, several small positive and negative outliers during these years would not be recognized as cyclical turning points.Footnote 15

Second, dating the latest peak (that is, the beginning of the current recession) is especially difficult because of the preceding long stagnation. It is completely impossible to date the latest trough correctly just now: even if it happened somewhere in the past (for example, in the summer of 2016), too little time has passed since then.

Thirdly, each of the four “suspicious” time intervals has its own set of time series available. We propose to test each of them one by one.

Therefore, the “longlist” of our preliminary estimates (plausible peaks and troughs) refers to nine indicators (six for industrial and three for basic activities’ output), each handled with three procedures of seasonal adjustment and three methods of dating turning points. Some months occur in this list several times. If the frequency is equal to zero, then the corresponding month never appears in the list of potential turning points. If the frequency is equal to 100 (for peaks) or −100 (for troughs), then all of the indicators, the procedures for seasonal adjustments, and the methods of dating turning points show strictly in one direction. The frequencies for each month are plotted in Fig. 2.

Source Appendix

Appearances in the “longlist” of peaks and troughs, frequency. Note See text for explanations. The months with the highest frequencies in each cluster are marked.

3.2 Qualitative Considerations and Choices

There are four preliminary findings from the “longlist” of possible turning points (see Appendix).

First, not all of the methods recognized all of the turning points, and thus all of the historical Russian cycles. For example, for many indicators, the Markov-switching model does not detect the peak and the trough in the second half of the 1990s or the peak in 2014. For several options, it does not even consider September 1998 (which is the global minimum for all indicators used) as a trough. This is because the estimates of the Markov-switching model depend on the values of all observations in a time series. So, for the series that underwent substantial volatility during the transition crisis in the first half of the 1990s, the expansion of 1997 seems not like a separate cyclical phase but rather as a part of a more general wave. Similarly, for the series that fell significantly in 2008–2009, the current downturn does not seem serious enough yet to be considered as a new recession.

Second, while there are no doubts among Russian experts about the current contraction (everybody agrees that somewhere in the end of 2014 or in the beginning of 2015 the Russian economy slipped down into recession), some doubts do exist about the recovery in 1997. In our opinion, those doubts are baseless because this expansion is seen from the annual data for real GDP (+1.4%) or industrial production (+1.0%) as well as from the trajectories of financial indicators (in 1997, there were steady tendencies of rising stock prices and of declining interest rates). But if there had been an expansion somewhere in 1997, then there was a trough in the beginning and a peak at the end! Hence, our task is to date them.

Third, the peaks/troughs of the time series seasonally adjusted with X-12 ARIMA or TRAMO/SEATS are sometimes really shifted to the left/right for several months relative to the turning points of the same time series adjusted with CAMPLET. This may mean that the first two give biased estimates of cyclical turning points. Conversely, this may also mean that CAMPLET gives biased estimates. We believe that this issue deserves special consideration; here we will assume that the time series adjusted with CAMPLET could give the earliest estimates for peaks and the latest for troughs.

Fourth, there is no turning point (even the trough of September 1998) that had a frequency equal to 100 and was thus indisputable. In most instances, various combinations of indicators, procedures of seasonal adjustment, and methods of dating gave slightly different results and we had to choose between them. It was not an easy task because other available economic and financial indicators with evident cyclical fluctuations (stock-market indices, interest and exchange rates, level of international exchange reserves, number of imported autos, etc.) were of no help: they are usually leading or lagging, not coincident. Therefore, we had to make our choices using only our two groups of indicators (basic activities’ and industrial output).

In order to avoid complete arbitrariness we followed three criteria:

-

1.

if levels of the same indicator at two moments differed by less than 1.5% we usually preferred the later one;

-

2.

estimates derived from the trajectory of basic activities are “more important” for us than those from industry alone (we believe that basic activities are “closer” to the whole economy);

-

3.

turning points derived from monthly time series (basic activities’ and industrial output) had to be in accord with turning points derived from quarterly real GDP.

All alternatives ever detected are shown in Table 2, along with our final choice and its justification.

3.3 Final Set of Cyclical Turning Points

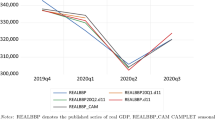

All appropriate indicators for 1995–1998, 2007–2009, and 2013–2015 along with detected turning points are shown in Figs. 3, 4, and 5 (the areas from peaks to troughs, which are recessions, are colored with grey).

The final set of turning points corresponds to the following phases of the Russian economic cycle:

-

The beginning of the 1980s–January 1989 long expansion after short recession in 1979 (there are no monthly time series for 1979–1980 but annual data point to 1979 as a year of contraction);Footnote 16 this period of growth ended as the drivers of the Soviet planned economy had been exhausted.

-

February 1989–November 1996 there were two stages of this extra-long (8 years) Great Russian Depression. The first one—the death throes of the planned economy—lasted until December 1992 (de jure dissolution of the USSR). The second one was a painful transformation from a planned to a market economy. The trough of November 1996 was preceded by Boris Yeltsin’s winning a second presidential term in the July election, which made any return to a planned system impossible and therefore stimulated business activity. Naturally, there were no turning points between the two stages of this contraction.

-

December 1996–November 1997 short recovery interrupted by the South East Asian financial crisis.

-

December 1997–September 1998 sharp contraction caused by capital outflow from emerging markets; it ended 1 month later than the default on the Russian Government’s bonds and notes.

-

October 1998–May 2008 long expansion initially driven by the almost fourfold devaluation of the ruble and subsequently by the extraordinary growth of oil prices and consumer credit afterward.

-

June 2008–May 2009 recession caused by the world financial crisis, especially after the Lehman Brothers’ bankruptcy.

-

June 2009–December 2014 this post-crisis recovery evolved into stagnation in 2012 as the period of oil prices consistently rising had ended.

-

January 2015–??? contraction caused by wide oppression of the entrepreneurial spirit and worsened by the decline of oil prices, trade and financial sanctions from the West, as well as self-sanctions on imports.

The overall characteristics of the Russian economic cycle for the last 35 years are summarized in Table 3.

Of course, “three and a half pairs” of peaks and troughs are not enough to make definite conclusions about the profile of the Russian economic cycle. We may only adduce the average lengths of the US post-war contractions (11 months) and expansions (59 months). If we exclude the prolonged Russian expansion in the 1980s (the end of the planned economy) and the Great Russian Depression (the prolonged transition crisis up to the middle of the 1990s), the average duration of Russian recessions will be close to the American ones, and the average duration of Russian expansions will be slightly longer than the American ones. Current developments may confirm or destroy this hypothesis.

4 Conclusions

Since the trajectory of the Russian economy may be described as a sequence of expansions and contractions, the practical task of discerning cyclical turning points in real time arises. The first step in reaching this goal is the dating of turning points for historical time series at monthly intervals. We took this step and proposed a set of peaks and troughs that looks explainable and interpretable. Now it may be used for analyses of cyclical fluctuations of a multitude of economic and financial indicators, and particularly for searching of leading indicators and estimating their predictive powers while approaching a cyclical turning point.

At the same time, the proposed set of turning points is not indisputable. Almost any peak or trough (except, possibly, the trough of September 1998) may be shifted 2–3 months to the left (or to the right) without losing meaningfulness and plausibility. Different reference indicators, different procedures for seasonal adjustments, and different formal methods for detecting turning points all bring slightly different estimates of turning points. What is more, this variability cannot be fully removed with more sophisticated methods because really significant uncertainty and diversity always exist in initial statistical information. We believe that the way out of this confusing situation would be more refined qualitative analyses of economic tendencies, not more refined formal methods. If the proposed set of turning points is adequate, then the detected peaks and troughs would introduce a reasonable order in the chaos of the manifold fluctuations of indicators; a differentiation between leading, lagging, and coincident indicators would look reasonable.

We believe that in any country a simple consensus among experts is the most important argument in dating cyclical turning points. All formal procedures and methods are only instruments to form individual estimates made by experts and to provide them some arguments for a common discussion. The ideal solution for these discussions would be an authoritative Economic Cycle Dating Committee. Today, it seems unrealistic for Russia because there are too few experts in the field of Russian cycles. On the other hand, an exchange of experts’ opinions may take less straightforward forms; for example, the form of consecutive publications. We hope to make an important step in this direction.

Notes

A business cycle is formed from a sequence of expansions and contractions in general economic activity; growth cycle represents waves of positive and negative deviations from the long-run trend; and growth rate cycle (or acceleration cycle) is a sequence of accelerations and decelerations of economic dynamics. Sometimes the turning points of all these cycles coincide, sometimes not. For more details see Mazzi and Ozyildirim (2017), esp. pp. 51–56.

The NBER US Business Cycle Dating Committee; The CEPR Euro Area Business Cycle Dating Committee; the Brazilian Business Cycle Dating Committee (O Comitê de Datação de Ciclos Econômicos (CODACE); the Investigation Committee for Business Cycle Indicators ESRI (Japan), etc.

And more, there is even a certain skepticism concerning the cyclicity of the modern Russian economy. Some academics differ between system, structural, external, and cyclical crises and hesitate to declare if there have been any cyclical (in this narrow sense) crises in Russia. See Poletaev and Savelieva (2001), Bessonov (2005), Entov (2009), Belyanova and Nikolaenko (2012, 2013).

This does not mean that all of them are incorrect but at least one (the trough in January 1999) seems very strange.

In the past few decades, there have been several important works published concerning the economic dynamics of the USSR (see Nutter 1962; Moorsteen and Powell 1966; Greenslade 1976; Kurtzweg 1990; Noren and Kurtzweg 1993; Kholodilin 1997; Solntsev and Kholodilin 2000; Suhara 2007) or of the Russian Federation as a part of the USSR (see Alekseev 1994; Suhara 2000; Ponomarenko 2002; Smirnov 2015). Many of these were very significant in that they refuted the myth of the crisis-free planned Soviet economy. On the other hand, they always used annual time-series and hence did not allow for the monitoring of the economic activity in real time or for constructing a system of leading indicators.

See Gimpelson and Kapeliushnikov (2013) for details.

The only other paper devoted to dating cyclical turning points for Russia is Dubovskiy et al. (2015). Most of the peaks and troughs estimated by them are similar (while not identical in all cases) to the ones from our list of possible turning points (see below).

As this method is well known, there is no need to add anything except that we used its implementation in Grocer 1.5 in the Scilab 5.3.3 environment. The main concepts implemented in this procedure (see Bry and Boschan 1971, p. 21) are rather technical and may be applied not only to mature economies but also to emerging economies with a sequence of mid-term expansions and contractions in their dynamics as well. Besides the Bry–Boschan method we also tried the similar Harding and Pagan (2002) method in its monthly (modified) form, also from the same package. Usually, the results were alike to Bry–Boschan’s but there were several false turning points for the period of stagnation in 2012–2013. Hence, we did not use the turning points detected by the Harding–Pagan method in our further analysis.

For all series under consideration in this paper, HQ criterion indicated two autoregressive lags.

We have nevertheless estimated the model with switches both in mean and in variance. As expected, this specification does not improve the fit.

This implies the use of the Markov chain of order 6 with restrictions on the transition probability matrix.

Anywhere in this paper “industry” includes: mining and quarrying; manufacturing; and electricity, gas and water supply.

Only the indices adjusted with X-12-ARIMA are shown. The charts for TRAMO/SEATS and CAMPLET are available upon request. We did not perform the calendar adjustment since it requires (unavailable) time series at a much lower level of aggregation in order to generate reasonable results.

Dubovskiy et al. (2015) dated September 2012 and February 2014 as additional peaks and June 2013 as an additional trough. We think this result is owing to a short time perspective (their time series ended in the middle of 2014) and to non-critical belief in the estimates received with formal methods.

See Smirnov (2015) for details.

References

Aastveit, K. A., Jore, A. S., & Ravazzolo, F. (2016). Identification and real-time forecasting of Norwegian business cycles. International Journal of Forecasting, 32(2), 283–292.

Abeln, B., & Jacobs, J. P. A. N. (2015). Seasonal adjustment with and without revisions: A comparison of X-13 ARIMA-SEATS and CAMPLET. CIRANO working paper 2015 s-35.

Aguiar, M., & Gopinath, G. (2007). Emerging market business cycles: The cycle is the trend. Journal of Political Economy, 115(1), 69–102.

Alekseev, A. V. (1994). Aльтepнaтивныe oцeнки poccийcкoгo экoнoмичecкoгo pocтa [Alternative Estimates of the Russian Economic Growth]. ECO, 11, 94–108.

Alp, H., Baskaya, Y. S., Kılınç, M., & Yüksel, C. (2012). Stylized facts for business cycles in Turkey. Central Bank of the Republic of Turkey. Working Paper No. 12/02.

Anas, J., & Ferrara, L. (2004). Detecting cyclical turning points: The ABCD approach and two probabilistic indicators. Journal of Business Cycle Measurement and Analysis, 1(2), 193–225.

Andersson, E., Bock, D., & Frisén, M. (2006). Some statistical aspects of methods for detection of turning points in business cycles. Journal of Applied Statistics, 33(3), 257–278.

Artis, M., Massimiliano, M., & Proietti, T. (2004). Dating business cycles: A methodological contribution with an application to the Euro area. Oxford Bulletin of Economics and Statistics, 66(4), 537–565.

Baranov, E. F., Bessonov, V. A., Roskin, A. A., Ahundova, T. A., & Beznosik, V. I. (2011b). Индeкcы интeнcивнocти пpoмышлeннoгo пpoизвoдcтвa (экcпepтныe oцeнки). HИУ BШЭ. Eжeмecячный дoклaд. Янвapь 2000 – мaй 2011 [Indices of industrial production (expert estimates). HSE monthly report. January 2000–May 2011]. http://www.hse.ru/data/2012/05/29/1252460613/text.pdf.

Baranov, E. F., Bessonov, V. A., Roskin, A. A., Ahundova, T. A., Beznosik, V. I., & Ahundova, O. V. (2011a). Индeкcы интeнcивнocти выпycкa тoвapoв и ycлyг пo бaзoвым видaм экoнoмичecкoй дeятeльнocти. HИУ BШЭ. Eжeмecячный дoклaд. Янвapь 2000 – нoябpь 2011. [Indices of basic activities’ production. HSE monthly report. January 2000–November 2011]. http://www.hse.ru/data/2012/05/24/1253784638/metod.pdf.

Belyanova, E. V., & Nikolaenko, S. A. (2012). Экoнoмичecкий цикл в Poccии в 1998–2008 гoдax: зapoждeниe внyтpeнниx мexaнизмoв цикличecкoгo paзвития или импopтиpoвaниe миpoвыx пoтpяceний? [The economic cycle in Russia in the years 1998–2008: The emergence of internal mechanisms for cyclic development or importation of the global turmoil?]. HSE Economic Journal, 1, 31–52.

Belyanova, E. V., & Nikolaenko, S. A. (2013). O дaтиpoвкe экoнoмичecкиx циклoв: миpoвoй oпыт и вoзмoжнocти eгo иcпoльзoвaния в poccийcкиx ycлoвияx [Business cycle dating: International experience and possibilities for its application in Russia]. Voprosy Statistiki, 8, 30–41.

Berge, T. J., & Jordà, Ò. (2011). Evaluating the classification of economic activity into recessions and expansions. American Economic Journal: Macroeconomics, 3(2), 246–277.

Bessonov, V. A. (2005). Пpoблeмы aнaлизa poccийcкoй мaкpoэкoнoмичecкoй динaмики пepexoднoгo пepиoдa. [Problems of analysis of Russia’s macroeconomic dynamics in transitional period]. Moscow: IET.

Bessonov, V. A., & Petronevich, A. V. (2013). Ceзoннaя кoppeктиpoвкa кaк иcтoчник лoжныx cигнaлoв [Seasonal adjustment as a source of spurious signals]. HSE Economic Journal, 4, 554–584.

Birchenhall, C. R., Jessen, H., Osborn, D. R., & Simpson, P. (1999). Predicting U.S. business-cycle regimes. Journal of Business & Economic Statistics, 17(3), 313–323.

Boldin, M. D. (1994). Dating turning points in the business cycle. The Journal of Business, 67(1), 97–131.

Bruno, G., & Otranto, E. (2004). Dating the Italian business cycle: A comparison of procedures. ISAE. Working Paper 41.

Bry, G., & Boschan, C. (1971). Cyclical analysis of time series: Selected procedures and computer programs. Technical Paper 20, National Bureau of Economic Research.

Burns, A. F., & Mitchell, W. C. (1946). Measuring business cycles. New York: National Bureau of Economic Research.

Camacho, M., & Perez-Quiros, G. (2002). This is what the leading indicators lead. Journal of Applied Econometrics, 17(1), 61–80.

Chaffin, W. W., & Talley, W. K. (1989). Diffusion indexes and a statistical test for predicting turning points in business cycles. International Journal of Forecasting, 5(1), 29–36.

Chauvet, M. (1998). An econometric characterization of business cycle dynamics with factor structure and regime switching. International Economic Review, 39(4), 969–996.

Chauvet, M., & Hamilton, J. D. (2006). Dating business cycle turning points. In M. Costas, P. Rothman, & D. van Dijk (Eds.), Nonlinear time series analysis of business cycles (pp. 1–54). Amsterdam: Elsevier.

Chauvet, M., & Piger, J. (2008). A comparison of the real-time performance of business cycle dating methods. Journal of Business & Economic Statistics, 26(1), 42–49.

Christoffersen, P. F. (2000). Dating the turning points of nordic business cycles. University of Copenhagen. EPRU Working Paper Series WP 00–13.

Cross, P., & Bergevin, P. (2012). Turning points: Business cycles in Canada since 1926. C.D. HOWE Institute. Commentary No. 366.

Diebold, F. X., & Rudebusch, G. D. (1992). Have postwar economic fluctuations been stabilized? American Economic Review, 82(4), 993–1005.

Dubovskiy, D. L., Kofanov, D. A., & Sosunov, K. A. (2015). Дaтиpoвкa poccийcкoгo бизнec-циклa [Dating of the Russian business cycle]. HSE Economic Journal, 4, 554–575.

ECRI. (2016). International business and growth rate cycle dates. https://www.businesscycle.com/ecri-business-cycles/international-business-cycle-dates-chronologies.

Entov, R. M. (2009). Heкoтopыe пpoблeмы иccлeдoвaния дeлoвыx циклoв [Some problems in business cycles studies]. In E. T. Gaidar (Ed.), Financial crisis in Russia and in the world (pp. 6–42). Moscow: Prospect.

Filardo, A. J. (1999). How reliable are recession prediction models? Economic Review, Federal Reserve Bank of Kansas City, 2nd Quarter, 35–55.

Fushing, H., Chen, S.-C., Travis, J., Berge, T. J., & Jordà, Ò. (2010). A chronology of international business cycles through nonparametric decoding. Federal Reserve Bank of Kansas City. Research working paper WP 11–13.

Gimpelson, V. E., & Kapeliushnikov, R. (2013). Labor market adjustment: Is Russia different? In S. Weber & M. V. Alexeev (Eds.), The Oxford handbook of the Russian economy (pp. 693–724). Oxford: Oxford University Press.

Golosnoya, V., & Hogrefe, J. (2013). Signaling NBER turning points: A sequential approach. Journal of Applied Statistics, 40(2), 438–448.

Greenslade, R. V. (1976). The real national product of the USSR, 1950–1975. In Soviet economy in a new perspective: a compendium of papers. Joint Economic Committee of the United States Congress (pp. 269–300). Washington: U.S. G.P.O.

Grudkowska, S. (2011). Demetra+ user manual. National Bank of Poland. http://vesselinov.com/DemetraPlusManual.pdf.

Hamilton, J. (1989). A new approach to the economic analysis of nonstationary time series and the business cycle. Econometrica, 57, 357–384.

Hamilton, J. D. (2011). Calling recessions in real time. International Journal of Forecasting, 27(4), 1006–1026.

Harding, D., & Pagan, A. (2002). Dissecting the cycle: A methodological investigation. Journal of Monetary Economics, 49(2), 365–381.

Junli, Z., Degang, J., & Wei, C. (2014). China’s economic cycles: Characteristics and determinant factors. Unpublished manuscript.

Kapetanios, G. (2001). Model selection in threshold models. Journal of Time Series Analysis, 22(6), 733–754.

Kholodilin, K. (1997). Экoнoмичecкaя динaмикa CCCP в 1950–1990 гoдax: oпыт иcчиcлeния eдинoгo экoнoмичecкoгo пoкaзaтeля [Economic dynamics in the USSR, 1950–1990: An experience of a composite economic indicator estimation]. Voprosy Statistiki, 4, 64–75.

Kim, C.-J., & Nelson, C. R. (1998). Business cycle turning points, a new coincident index, and tests of duration dependence based on a dynamic factor model with regime switching. The Review of Economics and Statistics, 80(2), 188–201.

Kim, M.-J., & Yoo, J.-S. (1995). New index of coincident indicators: A multivariate Markov switching factor model approach. Journal of Monetary Economics, 36(3), 607–630.

Krolzig, H. M. (1998). Econometric modelling of Markov-switching vector autoregressions using MSVAR for Ox. https://www.researchgate.net/publication/246006071_Econometric_Modeling_of_Markov-Switching_Vector_Auto-regressions_using_MSVAR_for_Ox.

Kurtzweg, L. (1990). Measures of Soviet gross national product in 1982 prices. A study prepared for the use of the Joint Economic Committee. Congress of the United States. Washington: U.S. G.P.O.

Layton, A. P. (1997). A new approach to dating and predicting Australian business cycle phase changes. Applied Economics, 29(7), 861–868.

Layton, A. P., & Katsuura, M. (2001). Comparison of regime switching. Probit and logit models in dating and forecasting US business cycles. International Journal of Forecasting, 17(3), 403–417.

Liu, W., & Moench, E. (2016). What predicts US recessions? International Journal of Forecasting, 32(4), 1138–1150.

Martinez-Garcia, E., Grossman, V., & Mack, A. (2015). A contribution to the chronology of turning points in global economic activity (1980–2012). Journal of Macroeconomics, 46, 170–185.

Mazzi, G. L., & Ozyildirim, A. (2017). Business cycles theories: An historical overview. In G. L. Mazzi (Ed.), Handbook on cyclical composite indicators. http://unstats.un.org/unsd/nationalaccount/consultationDocs/draft_HandbookCCI.pdf.

McNees, S. K. (1987). Forecasting cyclical turning points: The record in the past three recessions. New England Economic Review, 2, 31–40.

Mejía-Reyes, P. (1999). Classical business cycles in latin America: Turning points, asymmetries and international synchronization. Estudios Económicos, 14(2), 265–297.

Moorsteen, R., & Powell, R. (1966). The Soviet capital stock, 1928–62. Homewood, IL: R. D. Irwin.

Noren, J., & Kurtzweg, L. (1993). The Soviet economy unravels: 1985–1991. In R. F. Kaufman & J. P. Hardt (Eds.), The former Soviet union in transition. Joint Economic Committee. Congress of the United States (pp. 8–33). Washington: U.S. G.P.O.

Nutter, G. W. (1962). Growth of industrial production in the Soviet union. Princeton, NJ: NBER.

OECD. (2017). OECD composite leading indicators: Turning points of reference series and component series. January 2017. http://www.oecd.org/std/leading-indicators/CLI-components-and-turning-points.pdf.

Peláez, R. F. (2005). Dating business-cycle turning points. Journal of Economics and Finance, 29(1), 127–137.

Polasek, W. (2010). Dating and exploration of the business cycle in Iceland. The Rimini Centre for Economic Analysis (RCEA) WP 10–13.

Poletaev, A. V., & Savelieva, I. M. (2001). Cpaвнитeльный aнaлиз двyx cиcтeмныx кpизиcoв в poccийcкoй иcтopии (1920-e и 1990-e гoды) [Comparative analysis of two system crises in Russian history (1920s and 1990s)]. In Yu. A. Petrov (ed.), Economic history. Yearbook. 2000 (pp. 98–134). Moscow: ROSSPEN.

Poměnková, J. (2010). An alternative approach to the dating of business cycle: Nonparametric kernel estimation. Prague Economic Papers, 19(3), 251–272.

Ponomarenko, A. N. (2002). Peтpocпeктивныe нaциoнaльныe cчeтa Poccии: 1961–1990 [Retrospective national accounts of Russia, 1961–1970]. Moscow: Finansy i statistika.

Rand, J., & Tarp, F. (2002). Business cycles in developing countries: Are they different? World Development, 30(12), 2071–2088.

Romer, C. D. (1994). Remeasuring business cycles. Journal of Economic History, 54(3), 573–609.

Sarlan, H. (2001). Cyclical aspects of business cycle turning points. International Journal of Forecasting, 17(3), 369–382.

Schirwitz, B. (2009). A comprehensive German business cycle chronology. Empirical Economics, 37(2), 287–301.

Sephton, P. (2001). Forecasting recessions: Can we do better on MARS? Federal Reserve Bank of St. Louis Review, 83(2), 39–49.

Smirnov, S. V. (2013). Cyclical mechanisms in the US and Russia: Why are they different? Working Paper WP2/2013/01. National Research University “Higher School of Economics”, Moscow.

Smirnov, S. V. (2014). Russian cyclical indicators and their usefulness in real time: An experience of the 2008–09 recession. Journal of Business Cycle Measurement and Analysis, 1, 103–128.

Smirnov, S. V. (2015). Economic fluctuations in Russia (from the late 1920s to 2015). Russian Journal of Economics, 1(2), 130–153.

Solntsev, V. N., & Kholodilin, K. A. (2000). O пpoявлeнияx дoлгocpoчныx тeндeнций в coвpeмeннoм экoнoмичecкoм кpизиce в Poccии [On manifestations of long-term tendencies in the modern economic crisis in Russia]. Ekonomika i Matematicheskie Metody, 36(2), 57–62.

Stock, J. H., & Watson, M. W. (1993). A procedure for predicting recessions with leading indicators: Econometric issues and recent experience. In J. Stock & M. Watson (Eds.), Business cycles, indicators and forecasting (pp. 95–156). Chicago: University of Chicago Press.

Stock, J. H., & Watson, M. W. (2014). Estimating turning points using large data sets. Journal of Econometrics, 178(Part 2), 368–381.

Suhara, M. (2000). Oцeнкa пpoмышлeннoгo пpoизвoдcтвa Poccии: 1960–1990 гoды [An estimate of russian industrial production: 1960–1990]. Voprosy Statistiki, 2, 55–63.

Suhara, M. (2007). An estimation of production indexes for Soviet industry: 1913–1990. Research Institute of Economic Science, College of Economics, Nihon University. Working Paper Series, No. 07–01 (in Japanese).

Tsouma, E. (2014). Dating business cycle turning points: The Greek economy during 1970–2012 and the recent recession. Journal of Business Cycle Measurement and Analysis, 1, 1–24.

Venter, J. C. (2005). Reference turning points in the South African business cycle: Recent developments. Quarterly Bulletin, South African Reserve Bank, 237, 61–70.

Zarnowitz, V., & Ozyildirim, A. (2002). Time series decomposition and measurement of business cycles, trends and growth cycles. NBER Working Paper No. 8736.

Author information

Authors and Affiliations

Corresponding author

Additional information

The support from the Basic Research Program of the National Research University Higher School of Economics is gratefully acknowledged.

Appendix: “Longlist” of Russian Peaks and Troughs: 1981–2015

Appendix: “Longlist” of Russian Peaks and Troughs: 1981–2015

Short name of index | Time-span | TP | Local max/min | Bry–Boschan | Markov-switching | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

X-12 | T/S | C | X-12 | T/S | C | X-12 | T/S | C | |||

The end of the 1980s | |||||||||||

IO-SS | 01/81–12/92 | P | 02/88 | 01/89 | 01/89 | 12/88 | 01/89 | 01/89 | 01/90 | 08/90 | 08/90 |

Second half of the 1990s | |||||||||||

IO-RS_1 | 01/93–12/04 | T | 08/96 | 08/96 | 08/96 | 08/96 | 08/96 | 08/96 | 01/94 | 01/94 | 03/94 |

P | 11/97 | 11/97 | 11/97 | 11/97 | 11/97 | 11/97 | 03/98 | – | – | ||

T | 09/98 | 09/98 | 09/98 | 09/98 | 09/98 | 09/98 | 09/98 | – | – | ||

IO-B&B_1 | 01/90–02/07 | T | 11/96 | 11/96 | 02/97 | 11/96 | 11/96 | 02/97 | 09/94 | 05/94 | 08/94 |

P | 09/97 | 11/97 | 11/97 | 09/97 | 11/97 | 11/97 | – | – | – | ||

T | 09/98 | 09/98 | 09/98 | 09/98 | 09/98 | 09/98 | – | – | – | ||

IO-B&B_2 | 01/95–08/09 | T | 11/96 | 11/96 | 02/97 | 11/96 | 11/96 | 02/97 | – | – | 07/96 |

P | 10/97 | 11/97 | 11/97 | 11/97 | 11/97 | 11/97 | – | – | 03/98 | ||

T | 09/98 | 09/98 | 10/98 | 09/98 | 09/98 | 10/98 | – | – | 01/99 | ||

BAO-RS_1 | 01/95–06/07 | T | 06/97 | 11/96 | 08/96 | 08/96 | 11/96 | 08/96 | 08/96 | 08/96 | – |

P | 10/97 | 09/97 | 12/97 | 10/97 | 09/97 | 12/97 | 10/97 | 12/97 | 12/97 | ||

T | 09/98 | 09/98 | 09/98 | 09/98 | 09/98 | 09/98 | 09/98 | 09/98 | 09/98 | ||

2007–2009 and 2013–2015 | |||||||||||

IO-RS_2 | 01/99–10/14 | P | 02/08 | 02/08 | 02/08 | 02/08 | 02/08 | 02/08 | 07/08 | 07/08 | 07/08 |

T | 01/09 | 01/09/ | 08/09 | 01/09 | 01/09 | 08/09 | 01/09 | 01/09 | 01/09 | ||

P | 12/14 | 10/14 | 12/14 | 12/14 | 10/14 | 12/14 | – | – | 12/14 | ||

IO-B&B_3 | 01/00–10/14 | P | 05/08 | 06/08 | 06/08 | 02/08 | 06/08 | 06/08 | 07/08 | 07/08 | 08/08 |

T | 01/09 | 01/09 | 05/09 | 01/09 | 01/09 | 08/09 | 01/09 | 01/09 | 02/09 | ||

P | 05/14 | 04/14 | 05/14 | 05/14 | 04/14 | 05/14 | – | – | – | ||

BAO-RS_2 | 01/03–10/14 | P | 05/08 | 05/08 | 09/08 | 05/08 | 05/08 | 09/08 | 07/08 | 07/08 | 09/08 |

T | 05/09 | 05/09 | 05/09 | 05/09 | 01/09 | 05/09 | 01/09 | 01/09 | 05/09 | ||

P | 09/14 | 05/14 | 12/14 | 09/14 | 05/14 | 12/14 | 12/14 | – | 12/14 | ||

BAO-B&B | 01/00–10/14 | P | 05/08 | 05/08 | 09/08 | 05/08 | 05/08 | 09/08 | 07/08 | 07/08 | 09/08 |

T | 05/09 | 05/09 | 08/09 | 05/09 | 05/09 | 08/09 | 02/09 | 02/09 | 05/09 | ||

P | 09/14 | 10/13 | 10/13 | 10/13 | 10/13 | 10/13 | 09/14 | 09/14 | 01/15 | ||

Rights and permissions

About this article

Cite this article

Smirnov, S.V., Kondrashov, N.V. & Petronevich, A.V. Dating Cyclical Turning Points for Russia: Formal Methods and Informal Choices. J Bus Cycle Res 13, 53–73 (2017). https://doi.org/10.1007/s41549-017-0014-9

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s41549-017-0014-9