Abstract

The study revisits the position of the environmental Kuznets curve (EKC) hypothesis in India by incorporating the role of energy consumption and democratic regime in the environmental degradation function for the period 1971–2014. Employing Zivot–Andrews nonstationarity test, Bayer–Hanck cointegration test, autoregressive distributed lag (ARDL) model, and vector autoregressive model (VECM) Granger causality test, the results found the integration order of I(1) and a stable cointegration among the series. The result validates the EKC hypothesis for India and further divulges that while energy consumption increases environmental degradation both in the long run and short run; the effect of democracy in reducing environmental degradation is weak (statistically insignificant) in the long run but strong (statistically significant) in the short run. The finding from the VECM Granger causality test indicates a long-run causality between the fundamental variables and environmental degradation. Furthermore, the results of the short run show a unidirectional Granger causality running from energy consumption to environmental degradation, energy consumption to real income, and energy consumption to square of real income. Therefore, our findings suggest that energy conservation policy should be prioritized towards harnessing energy from clean sources to mitigate environmental degradation and spur economic growth.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

The need to address climate change has attracted global attention and intense research in the last three decades. This is largely because of the aggressive efforts by most countries of the world, particularly the developing countries towards accelerating the pace of economic growth. The pioneering work of Grossman and Krueger (1991) reveals the economic growth-environmental nexus in such that at the first stage of economic growth, environmental degradation increases, and then begins to decline at the later stage of economic growth. Generally, if economic activity increases, environmental pollution would increase as more inputs are employed. This is commonly referred to as the scale effect or pollution haven hypothesis in the literature (Dedeoglu and Kaya 2013; Stern and Van Dijk 2017). The composition effect occurs when the shares of the intensive pollutant goods in the production processes are reduced. This leads to a structural change from carbon-intensive country driven by agriculture, transport, and service to information-intensive country (see Antweiler et al. 2001; Stern 2007). Finally, because of this paradigm shift, producers move to an advanced stage where emphasis is to achieve cleaner production processes due to technological advancement. This stage is called the technique effects. Figure 1 discloses the schematic of an inverted U-shaped EKC hypothesis.

Schematic of inverted U-shaped EKC hypothesis (Sourced from Sarkodie and Strezov (2018))

Even though a large body of empirical research has studied the relationship between energy consumption and environmental pollution, a great number of it focus on environmental Kuznets curve (EKC) hypothesis by incorporating international trade, foreign direct investment, financial development, urbanization, education, population growth, and capital investment (see Shahbaz et al. 2013a, b; Rafindadi et al. 2014, Rafindadi 2016, Shahbaz et al. 2016, 2018; Gokmenoglu and Taspinar 2018; Mesagan et al. 2018; Katircioglu and Katircioglu 2018; Katircioglu et al. 2018; Emir and Bekun 2018; Alola 2019). These studies all provide interesting accounts of the effects of these variables on the EKC. In the case of India, most of the studies applied input–output analysis, although the results have been mixed. Some of the empirical studies indicate that EKC hypothesis does not hold (see Mukhopadhyay and Chakraborty 2005a, b; Dietzenbacher and Mukhopadhyay 2007; Mukhopadhyay 2008), while others confirm the validity of the EKC (Kanjilal and Ghosh 2013, (Khanna and Zilberman 2001; Bhattacharyya and Ghoshal 2010). There are also studies that claim a sound and vibrant environmental policy in India (Khanna and Zilberman 2001; Perkins 2007; Bhattacharyya and Ghoshal 2010; Kanjilal and Ghosh 2013). Yet, the research on the EKC in India is incomplete and therefore requires further investigation, especially the need to examine the pivotal role of socio-political variables such as democratic regimes on environmental pollution.

The effect of democracy on environmental degradation is contentious. However, two major arguments stand out in the literature. One of the arguments submits that democratic countries tend to improve environmental quality because it gives impetus for the people to express their preferences and hence put pressures on the government through the protest mechanism to demand environmental protections (see Payne 1995; Torras and Boyce 1998; Barrett and Graddy 2000; Farzin and Bond 2006). The other argument is built on the positive relationship between income and democracy, which is a cornerstone for modernization theory (see Heilbronner 1974; Midlarsky 1998; Roberts and Parks 2007; Alhassan and Alade 2017). Based on this theory, environmental quality is threatened because as income increases with the level of democracy, environmental degradation increases. To this extent, the main objective of this paper is to revisit the pivotal effects of income, energy consumption, and the democratic regime on environmental degradation measured by carbon dioxide emissions (CO2) in the context of the EKC hypothesis. In other words, the paper incorporates energy consumption and democracy in the function of environmental degradation to revalidate the EKC hypothesis for India over the period 1971–2014. To achieve this objective, the Bayer and Hanck (2013) (B-H)–combined cointegration test is used with robustness test of autoregressive distributed lag (ARDL) bound testing of Pesaran et al. (2001). The ARDL and Granger causality under vector autoregressive model (VECM) are explored to determine the coefficients and direction of causality.

The remainder of this paper is organized and structured as follows: “Energy sector and Indian economy: a brief discourse” is a brief discourse of the energy sector and the Indian economy. “Data and methodology” describes the data and the methodology employed. “Empirical results and discussion” reports and analyzes the empirical results, and “Conclusion and policy implications” offers conclusions and policy implications.

Energy sector and Indian economy: a brief discourse

Over the years, the Indian economy has recorded a significant average growth rate of 6.8% between 2000 and 2007. According to the World Bank report in 2018, Indian growth rate in 2017 was 6.8%. It is predicted that Indian growth rate will jump to 7.3% in 2018 and 7.5% between 2019 and 2020. The per capita income in India rose to $6616 in 2017 despite her large population size of about 1.3 billion. Several studies have linked these successes to an increase in energy consumption (see Khanna and Zilberman 2001; Perkins 2007). Theoretically, an increase in energy consumption increases greenhouse gas (GHG) emissions. Between 1950 and 2008, Boutabba (2014) reveals that India was ranked the fifth largest emitter of CO2 in the world with an increase of fossil fuel CO2 emissions of about 125%. This situation portends worrisome implications for the well-being of the living world especially the threat it causes to human health. Therefore, the major challenge confronting the Indian economy remains how economic growth trajectory can be achieved without increasing carbon dioxide emissions to destabilize the earth’s biosphere.

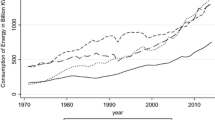

The government of Bharatiya Janata Party (BJP) in India, under the leadership of Narendra Modi, has been confronted with high demand for energy and its supply affordability since the inception in 2014. As reported by EIA (2018), the consumption of the primary energy in India increased astronomically between 1990 and 2013 to roughly 775 million tons of oil equivalent. The main reason is tied to its growing population size of about 1.4% each year and the subsequent expansion of economic activities (EIA 2018). Figure 2 presents energy production and consumption in India. Based on this figure, it is clear that the demand for energy is on the increase as the curve slopes upward, indicating excessive use of energy. According to EIA (2018), India was ranked as the third producer and consumer of coal in the world in 2013 and the largest importer of coal in 2015.

Energy production and consumption in India (2000–2017). Source: US Energy Information Administration, Short-Term Energy Outlook, May 2018

According to EIA’s report in 2018 as shown in Fig. 3, coal constitutes about 44% of energy consumption in India. This is followed by the biomass and waste, which is about 24%. Petroleum and other liquid consumption are about 23%. Other sources are very low such as natural gas, which is 6%; nuclear is 1%; hydroelectric is 2%, and other renewable is less than 1%.

Energy consumption mix in India (2000–2017). Source: US Energy Information Administration, Short-Term Energy Outlook, May 2018

Data and methodology

Data

The data for this study is based on the annual time-series for the period 1971–2014. The variables used include environmental degradation measured by CO2 emissions in metric tons per capita, income per capita measured by gross domestic product (GDP) per capita (constant 2010 US$), squared GDP per capita (constant 2010 US$), energy consumption (kilotons of oil equivalent per capita), and the measure of democracy. To measure the degree of democracy, we used Polity2 with the scores ranging from − 10 for worst autocracy and + 10 for perfect democracy.Footnote 1 To this end, higher value corresponds to the regime that is more democratic. The data on democracy is obtained from the POLITY IV dataset: http://www.systemicpeace.org/polity/polity4.htm. The remaining variables are sourced from the World Bank—World Development Indicators’ database (2018). All the variables are expressed in natural logarithms except the measure of democracy.

Model specification

Following Lv (2017) and Shahbaz et al. (2017), the functional form of the EKC model with the incorporation of energy consumption and the degree of democracy is given as:

where β0 is the intercept; εt is the error term, assumed to have zero mean, environmental degradation is measured by CO2 emissions in metric tons per capita; Y denotes income, measured by GDP per capita (constant 2010 US$); Y2 is the square of income; EC means energy consumption while DEMO measures the degree of democracy. The transformation of the model in Eq. (1) based ARDL approach is presented as follows:

where, Δ represents the differences in the log of CO2 emissions, income and its square, energy consumption, and democracy. The dependent variable i.e. CO2 emissions might not immediately adjust to the path of its long-term equilibrium due to the changes in the explanatory variables. Therefore, the pace of adjustment to the long-run equilibrium level is captured by ECMt − 1, which is defined as the one period lagged residual in the long-run equation. Based on Eq. (2), we expect that β2 > 0 and β4 > 0, while β3 < 0 and β5 < 0. The same applies to the short-run part of the equation. To execute a cointegration test among variables, Pesaran et al. (2001) proposed an F-test. The H0 of this test is that β1 =β2 =β3 =β4 =β5 =0 and the alternative is that β1 ≠β2 ≠β3 ≠β4 ≠β5 =0.

Unit root tests

The paper uses the augmented Dickey–Fuller (ADF) and the Phillips–Perron (PP), to check the stationarity properties of data variables. These tests all assume a structural stability and linear adjustment, which is not often realistic; hence, the tests might provide biased and spurious results. Therefore, in order to provide information about structural break points in the series, Zivot–Andrews unit root test proposed by Zivot and Andrews (1992) is applied. The unit root test by Zivot and Andrews (1992) employed the following three main regression equations to test a null hypothesis of a unit root against the alternative of a onetime structural break. Equation (3) presents model A, which indicates only a break in the intercept; Eq. (4), which is model B, depicts a break only in trend, and Eq. (5) presents model C, which combines both break in intercept and trend.

where DUt is an indicator dummy variable for a mean shift that occurs at each possible breakpoint (Tjb). The corresponding to the mean shift is the trend variable denoted by DTt. DUt = 1 if t >Tjb, and 0 if otherwise. Similarly, ΦDTt = t − Tjb if t >Tjb, and 0 if otherwise. Note that Tjb represents the possible break point in the series. The null hypothesis is thatH0 : Φ = 0, implying that a unit root exists with a single breakpoint, while the alternative hypothesis is H1 : Φ< 0, i.e., no unit root exists with a single breakpoint.

Bayer and Hanck cointegration test

This study explores a cointegration test recently proposed by B-H (2013) to determine the long-run relationship between environmental degradation, income, squared of income, energy consumption, and democracy in India. This test is an advanced contegration test that combines the initial cointegration tests by Engle and Granger (1987), Johansen (1995), Boswijk (1994), and Banerjee et al. (1998). The major advantage of this test is that it combines all these initial cointegration tests and obtains a uniform and reliable result. Therefore, the test prevents arbitrary decision of which test to use if there is conflict in their various results. Specifically, this test uses the formula proposed by Fisher (1932) to combine the statistical significance level. The formula and the probability value for the separate cointegration test are as follows:

From Eqs. (6) and (7), EG denotes the cointegration test proposed by Engle and Granger (1987) while JOH is that of Johansen (1995) with their corresponding probability values shown by (PrEG) and (PrJOH), respectively. Likewise, BO is the cointegration test developed by Boswijk (1994) and BDM by Banerjee et al. (1998) with (PrBO) and (PrBDM) as the respective probability values. The test follows Fisher’s statistic in order to determine whether there is cointegration or not between the variables. The null hypothesis of no cointegration is obviously rejected if the critical values by B-H are greater than the calculated Fisher statistics.

VECM Granger causality

In order to perform the causality test between the variables, we follow the error correction representation in a vector autoregressive model (VECM) since a cointegration has been established. This test has enviable advantages over the pairwise Granger causality. One of these advantages is that the test provides joint long-run and short-term causality between the variables. Therefore, if there is long-run relationship (cointegration) between the series then the VECM causality approach can be developed as follows:

where (1 − L) indicates difference operator, ECTt − 1 is the lag of error correction term obtained from the long-run equation. ε1t, ε2t, ε3t, ε4t, ε5t are the error terms which are assumed to have zero mean. If the value of ECMt − 1 is statistically significant by applying t statistic, it means that there is a valid long-run causality relationship between the variables. However, the evidence of the direction of a short-run causality is provided by the existence of a significant relationship in first differences of the variables. For example, real income per capita is said to Granger-cause environmental degradation if the prediction error of current environmental degradation changes by using past values of real income per capita in addition to the past values of environmental degradation. The short-run directional causality test uses the joint χ2statistic for the first differenced lag of exogenous variables.

Empirical results and discussion

Visual properties of the data

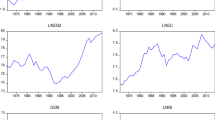

This section describes the visual properties of the time series variables for the possible existence of trend, drift, and structural breaks. The time plots of the variables are reported in Fig. 4. The time plots, therefore, suggest a trend in all the series with no clear evidence of breaks except the measure of democracy. This testifies to the fact that the economic growth and energy consumption have been increasing in India.

Time series plots of the lnCO2, lnY, lnY2, lnEC, and DEMO represent natural logarithms of carbon dioxide emissions, income, square of income, energy consumption, and democracy

Result of the unit root tests

Table 1 presents the results of the stationarity test. The results show that the variables are nonstationary in levels, but they became stationary by differencing the variables. This implies that all the series are integrated of order one or I(1). To circumvent the problem of low predicting power of this unit root test in the presence of structural breaks, Zivot–Andrews nonstationarity test is applied. The result of this test as shown in Table 1 indicates that the variables are nonstationary in their levels. They became stationary after first difference. This result confirms the result of the previous tests.

Results of the cointegration analysis

The result of the combined cointegration tests by B-H (2013) in Table 2 indicates that at 1% level of significance, the EG–JOH and EG–JOH–BO–BDM have four cointegration vectors. This implies that the null hypothesis of no cointegration is rejected in both EG–JOH and EG–JOH–BO–BDM tests. We further checked the robustness of this test by using a bound testing cointegration technique. The result presented in Table 2, panel B, shows that at 1% level of significance, the F statistic values for all the four equations exceed the critical values, indicating the rejection of the null hypothesis. Based on these results, we conclude that there is a valid long-run relationship between environmental degradation, income per capita, square of income per capita, energy consumption, and democracy in India from 1971 to 2014.

Long- and short-term coefficients

Table 3 provides the long-run coefficients using ARDL approach as described in Eq. (2). The results of the ARDL show that income per capita has an inelastic and positively significant relationship with lnCO2 emissions. Specifically, a 1% increase in income per capita increases environmental degradation by 0.113%. Remarkably, the coefficient of the square of income per capita is negative, elastic, and statistically significant at 1% level. This suggests that the association between CO2 emissions and income per capita in India is an inverted U-shaped. The finding implies that the Indian economy is affected by the scale effect, where an increase in income results to an increase in environmental degradation. This result concurs with the findings of Apergis et al. (2018) and Alola (2019) that economic growth measured by GDP notably exerts pressure on increasing environmental degradation, which hampers sustainability of the environment. More so, this finding concurs with Khanna and Zilberman (2001), Bhattacharyya and Ghoshal (2010), Kanjilal and Ghosh (2013), and Ozatac et al. (2017) who established the existence of the EKC hypothesis for India and Turkey. This finding is further agreed with Aslan et al. (2018) who confirmed that the EKC in USA is an inverted U-shape. However, our result contradicts the findings of Mukhopadhyay and Chakraborty (2005a, b), Dietzenbacher and Mukhopadhyay (2007), and Mukhopadhyay (2008) who failed to validate the EKC hypothesis in India. Furthermore, our results divulge that energy consumption is elastic, positive, and statistically significant while the effect of democratic regime is negative, inelastic, and statistically insignificant, indicating a weak effect of democracy on CO2. The reason for this result could be traceable to the dominance of a single party—the Indian National Congress, since its first general elections in 1951 until 1977 when a noncongress government emerged in the history of India and the subsequent rise of coalition governments in 1990s. The dominance of a single party could undermine the efficacy of democracy especially in the developing countries where most leaders exhibit corrupt practices. This finding is, therefore, not in line with the theory of modernization, which infers a positive relationship between income and democracy, and hence increases environmental degradation. More so, our result supports Torras and Boyce (1998), Barrett and Graddy (2000), and Farzin and Bond (2006) who reported that democracy puts pressure on the government of the day to improve environmental quality through effective designing of stringent environmental policies that reduce changes in natural levels and distribution of chemical elements that threaten the well-being of the people.

For the short-run coefficients, the empirical result of the error correction term (ECM) coefficient as provided in Table 3 shows that the ECM is − 0.989 and it is statistically significant, easily passing the 1% significance level. This suggests that environmental degradation converges to long-run equilibrium by about 98.9% through the channels of income per capital and its squared term, energy consumption, and democratic regime. The short-term coefficient of income per capita is inelastic, positive, and statistically significant, suggesting that a 1% increase in income per capita would increase environmental degradation by 0.159%. The coefficient of the squared term of income per capita is inelastic, positive, and statistically significant suggesting that the EKC hypothesis is not validated in the short-run for India. The result furthermore shows that the short-term coefficient of energy consumption is elastic, positive, and significant. This indicates that if energy consumption increases by 1%, pollutant emissions would increase by 1.791%. Finally, the result of the effect of democracy is inelastic, negative, and significant, suggesting that as the pace of democracy increases, environmental degradation decreases through effective implementation of economic policies, which redirect resources to environment friendly developmental plans. Therefore, the result is consistent with Shahbaz et al. (2013a) and Lv (2017) who submitted that effective democratic government reduces carbon dioxide emissions since the people can express their wishes on the government to improve environmental quality. On the other hand, our result is not consistent with Heilbronner (1974) and Midlarsky (1998) who assert that democracy affects environmental quality through the channel of income. As income increases, more unsafe energy is consumed and hence reduces environmental quality.

The diagnostic test results conducted show that the error terms are normally distributed and as such have no evidence of serial correlation based on Breusch–Godfrey Langrage multiplier test, heteroscedasticity based on ARCH test for conditional heteroscedasticity, and the Ramsey RESET test for the functional form of the model. Finally, the cumulative sum (CUSUM) and cumulative sum of squares (CUSUMsq) tests in Fig. 5 suggest stability of the parameters.

Plots of CUSUM and CUSUM square of recursive residuals

The VECM Granger causality analysis

The fact that there exists a long-run relationship between the variables, the causality of the variables is performed through the VECM Granger causality approach. The results of the long-run causal relationship as shown in Table 4 suggest the existence of a unidirectional Granger causality running from real income per capita, square of real income per capital, energy consumption, and democracy to environmental degradation. This result concurs with the existence of EKC hypothesis in India as reported by Ghosh (2010). Our result also agrees with Bekun et al. (2019) that the pursuit of growth in the 16 EU countries exert upward pressure on environmental degradation. Turning to the short-run causality in Table 4, the results show that there is unidirectional Granger causality running from energy consumption to environmental degradation and from energy consumption to real income per capita as well as its square. The implication for the results is that the past values of the income and its square, energy consumption, and democracy have additional information regarding the future values of CO2 emissions in India in the long run while in the short run, only the past value of energy consumption can be used to CO2 emissions, income, and square of income. Therefore, the finding is consistent with Ghosh (2010), Alam et al. (2011), and Shahbaz et al. (2017) who reported that a unidirectional Granger causality runs from energy consumption to carbon dioxide emission.

Conclusion and policy implications

This present study investigates the validity of the EKC hypothesis in India by incorporating energy consumption and democratic regime in the environment-growth function for the period 1971–2014. The study employed both the convention unit root tests (ADF and PP) and the Zivot and Andrews (1992) nonstationarity test with single structural break. The results showed that all the variables were nonstationary in levels but turned out to be stationary after differencing all the variables. This implies that all the series were I(1). To achieve robust estimates, we employed the recently developed combined cointegration tests by B-H (2013) to test the existence of cointegrating relationship among the variables. The results in this regard revealed a valid long-run relationship between environmental degradation, income per capita, square of income per capita, energy consumption, and democracy in India. The empirical results validated the EKC hypothesis for India. The results further divulged that energy consumption was attributed to increase in environmental degradation both in the long and short run. The effect of democracy in reducing environmental degradation was weak (statistically insignificant) in the long run but strong (statistically significant) in the short-run. The finding of the long-run VECM Granger causality test indicated that the lagged error correction term, ECMt−1 was significant in the CO2 emissions equation, implying that income, squared income, energy consumption and democracy caused CO2 emissions in the long run. The results also showed that energy consumption caused CO2 emissions, and income as well as square of income in the short run. The implication for our findings was that, in the long run, the past value of income, square of income, energy consumption, and democracy invariably predicted changes in CO2 emissions, while the past value of economic consumption predicted CO2 emission, income, and square of income in the short run in India. Therefore, for India to reduce CO2 emissions and increase growth, effort should be made to reduce energy consumption from fossil fuels, which is a major determinant of carbon emissions. To this extent, an appropriate energy policy should be anchored on expanding the use of energy from renewable sources. Expanding the use of energy from renewables may also lead to a decrease in the dependence on fossil energy and ensure energy security for the country. In addition, environmental policy of taxes on carbon emissions could be considered for India. However, a care must be taken so that the taxes on carbon emissions will not drive away the firms and industries from the country. In this case, we suggest that all the stakeholders in environment and energy must be given an opportunity to participate in crafting of such policy.

Furthermore, Indian’s democratic institutions should be strengthened in order to accelerate and stabilize economic growth. We also suggest based on our findings that Indian policymakers should pay particular attention to energy policy and strengthening democracy to reduce carbon emissions and stimulate economic growth. The experience of Romania after the abolition of communism in 1989 has demonstrated the efficacy of democratic regime in reducing pollutant emissions as revealed by Shahbaz et al. (2013a). This is also consistent with Lv (2017) that democracy downwardly pressurizes CO2 emissions in the emerging countries.

Notes

To void the negative sign of value, rescaling approach is usually applied to convert the measure of democracy to values ranging from zero and above in order to provide nonspurious results. However, in the case of India, all the values are positives; hence, we used the variable directly without rescaling.

References

Alam MJ, Begum IA, Buysse J, Rahman S, Van Huylenbroeck G (2011) Dynamic modeling of causal relationship between energy consumption, CO2 emissions and economic growth in India. Renew Sust Energ Rev 15(6):3243–3251

Alhassan A, Alade AS (2017) Income and democracy in sub-Saharan Africa. Journal of Economics and Sustainable Development 8(18):67–73

Alola AA (2019) The trilemma of trade, monetary and immigration policies in the United States: accounting for environmental sustainability. Sci Total Environ 658:260–267

Antweiler W, Copeland BR, Taylor MS (2001) Is free trade good for the environment? Am Econ Rev 91(4):877–908

Apergis N, Jebli MB, Youssef SB (2018) Does renewable energy consumption and health expenditures decrease carbon dioxide emissions? Evidence for sub-Saharan Africa countries. Renew Energy 127:1011–1016

Aslan A, Destek MA, Okumus I (2018) Bootstrap rolling window estimation approach to analysis of the environment Kuznets curve hypothesis: evidence from the USA. Environ Sci Pollut Res 25(3):2402–2408

Banerjee A, Dolado J, Mestre R (1998) Error-correction mechanism tests for cointegration in a single-equation framework. J Time Ser Anal 19(3):267–283

Barrett S, Graddy K (2000) Freedom, growth, and the environment. Environ Dev Econ 5(4):433–456

Bayer C, Hanck C (2013) Combining non-cointegration tests. J Time Ser Anal 34(1):83–95

Bekun FV, Alola AA, Sarkodie SA (2019) Toward a sustainable environment: Nexus between CO2 emissions, resource rent, renewable and nonrenewable energy in 16-EU countries. Sci Total Environ 657:1023–1029

Bhattacharyya R, Ghoshal T (2010) Economic growth and CO2. Environ Dev Sustain 12(2):159–177

Boswijk HP (1994) Testing for an unstable root in conditional and unconditional error correction models. J Econ 63:37–60

Boutabba MA (2014) The impact of financial development, income, energy and trade on carbon emissions: evidence from the Indian economy. Econ Model 40:33–41

Dedeoglu D, Kaya H (2013) Energy use, exports, imports and GDP: new evidence from the OECD countries. Energy Policy 57:469–476

Dietzenbacher E, Mukhopadhyay K (2007) An empirical examination of the pollution haven hypothesis for India: towards a green Leontief paradox? Environ Resour Econ 36(4):427–449

Emir F, Bekun FV (2018) Energy intensity, carbon emissions, renewable energy, and economic growth nexus: new insights from Romania. Energy Environ 0958305X1879310. https://doi.org/10.1177/0958305X18793108

Energy Information Association (EIA) (2018) Short-term energy outlook, May 2018

Engle RF, Granger C (1987) Cointegration and error correction representation: estimation and testing. Econometrica 55:251–276

Farzin YH, Bond CA (2006) Democracy and environmental quality. J Dev Econ 81(1):213–235

Fisher R (1932) Statistical methods for research workers. Oliver and Boyd, London

Ghosh S (2010) Examining carbon emissions economic growth nexus for India: a multivariate cointegration approach. Energy Policy 38:3008–3014

Gokmenoglu KK, Taspinar N (2018) Testing the agriculture-induced EKC hypothesis: the case of Pakistan. Environ Sci Pollut Res 25:1–13. https://doi.org/10.1007/s11356-018-2330-6

Grossman GM, Krueger AB (1991) Environmental impact of a North American free trade agreement. (No. w3914). National Bureau of Economic Research

Heilbronner RL (1974) An inquiry into the human prospect. Norton, New York

Johansen S (1995) A statistical analysis of cointegration for I(2) variables. Economet Theor 11:25–59

Kanjilal K, Ghosh S (2013) Environmental Kuznet’s curve for India: evidence from tests for cointegration with unknown structural breaks. Energy Policy 56:509–515

Katircioglu S, Katircioglu S (2018) Testing the role of fiscal policy in the environmental degradation: the case of Turkey. Environ Sci Pollut Res 25(6):5616–5630

Katircioglu S, Katircioglu S, Kilinc CC (2018) Investigating the role of urban development in the conventional environmental Kuznets curve: evidence from the globe. Environ Sci Pollut Res 25(15):15029–15035

Khanna M, Zilberman D (2001) Adoption of energy efficient technologies and carbon abatement: the electricity generating sector in India. Energy Econ 23(6):637–658

Lv Z (2017) The effect of democracy on CO2 emissions in emerging countries: does the level of income matter? Renew Sust Energ Rev 72:900–906

Mesagan E, Isola W, Ajide K (2018) The capital investment channel of environmental improvement: evidence from BRICS. Environ Dev Sustain 24:1–22

Midlarsky MI (1998) Democracy and the environment: an empirical assessment. J Peace Res 35(3):341–361

Mukhopadhyay K (2008) Air pollution and income distribution in India. J Asia Pac 15(1):35–64

Mukhopadhyay K, Chakraborty D (2005a) Environmental impacts of trade in India. Int Trade J 19(2):135–163

Mukhopadhyay K, Chakraborty D (2005b) Is liberalisation of trade good for the environment? Evidence from India. J Asia Pac 12(1):109–135

Ozatac N, Gokmenoglu KK, Taspinar N (2017) Testing the EKC hypothesis by considering trade openness, urbanization, and financial development: the case of Turkey. Environ Sci Pollut Res 24(20):16690–16701

Payne RA (1995) Freedom and the environment. J Democr 6(3):41–55

Perkins R (2007) Globalizing corporate environmentalism? Convergence and heterogeneity in Indian industry. Comparative International Development 42(3/4):279–309

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econ 16(3):289–326

Rafindadi AA (2016) Revisiting the concept of environmental Kuznets curve in period of energy disaster and deteriorating income: empirical evidence from Japan. Energy Policy 94:274–284

Rafindadi AA, Yusof Z, Zaman K, Kyophilavong P, Akmat G (2014) The relationship between air pollution, fossil fuel energy consumption, and water resources in the panel of selected Asia-Pacific countries. Environ Sci Pollut Res 21:11395–11400

Roberts JT, Parks BC (2007) A climate of injustice: global inequality, north-south politics, and climate policy. MIT Press, Cambridge

Sarkodie SA, Strezov V (2018) Empirical study of the environmental Kuznets curve and environmental sustainability curve hypothesis for Australia, China, Ghana and USA. J Clean Prod 201:98–110

Shahbaz M, Mutascu M, Azim P (2013a) EKC in Romania and the role of energy consumption. Renew Sust Energ Rev 18:165–173

Shahbaz M, Ozturk I, Afza T, Ali A (2013b) Revisiting the environmental Kuznets curve in a global economy. Renew Sust Energ Rev 25:494–502

Shahbaz M, Loganathan N, Muzaffar AT, Ahmed K, Jabran MA (2016) How urbanization affects CO2 emissions in Malaysia? The application of STIRPAT model. Renew Sust Energ Rev 57:83–93

Shahbaz M, Khan S, Ali A, Bhattacharya M (2017) The impact of globalization on CO2 emissions in China. Singap Econ Rev 62(04):929–957

Stern N (2007) The economics of climate change: the Stern review. Cambridge University Press, Cambridge

Stern DI, Van Dijk J (2017) Economic growth and global particulate pollution concentrations. Clim Chang 142:391–406. https://doi.org/10.1007/s10584-017-1955-7

Torras M, Boyce JK (1998) Income, inequality, and pollution: a reassessment of the environmental Kuznets curve. Ecol Econ 25(2):147–160

Zivot E, Andrews D (1992) Further evidence on the great crash, the oil-price shock, and the unit-root hypothesis. J Bus Econ Stat 10(3):251–270

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Muhammad Shahbaz

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Usman, O., Iorember, P.T. & Olanipekun, I.O. Revisiting the environmental Kuznets curve (EKC) hypothesis in India: the effects of energy consumption and democracy. Environ Sci Pollut Res 26, 13390–13400 (2019). https://doi.org/10.1007/s11356-019-04696-z

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-019-04696-z