Abstract

The adoption and ratification of relevant policies, particularly the household enrolment system metamorphosis in China, led to rising urbanization growth. As the leading developing economy, China has experienced a drastic and rapid increase in the rate of urbanization, energy use, economic growth and greenhouse gas (GHG) pollution for the past 30 years. The knowledge of the dynamic interrelationships among these trends has a plethora of implications ranging from demographic, energy, and environmental and sustainable development policies. This study analyzes the role of urbanization in decoupling GHG emissions, energy, and income in China while considering the critical contribution of energy use. As a contribution to the extant body of literature, the present research introduces a new phenomenon called “the environmental urbanization Kuznets curve” (EUKC), which shows that at the early stage of urbanization, the environment degrades however, after a threshold point the technique effects surface and environmental degradation reduces with rise in urbanization. Applying the autoregressive distributed lag model and the vector error correction model, the paper finds the presence of inverted U-shaped curve between urbanization and GHG emission of CO2, while the same hypothesis cannot be found between income and GHG emission of CO2. Energy use in all the models contributes to GHG emission of CO2. In decoupling greenhouse gas emissions, urbanization, energy, and income, articulated and well-implemented energy and urbanization policies should be considered.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Background

The past 3 decades have witnessed a drastic and fast increase in urbanization, energy use, and economic growth in many economies especially the developing and larger emerging economies, with China inclusive (Wang et al. 2016a, b and Zhu 2016). The adoption and signing of important blueprint policies, particularly the household enrolment system transformation, led to rising urbanization growth in China. Evidence suggests that urban population increased to 749.16 million in 2014, tripled the figure available in 1978. The speed of urbanization increased concurrently for about 36.9%, from 17.9 to 54.8% (National Bureau of Statistics 2015a, b). For the first time and in the year 2011, China’s urban population exceeded the rural population as a result of this developmental process (National Bureau of Statistics 2015a, b).

The results of the rising urbanization led to the increased in energy consumption and economic growth in China and the general development of the country (Han et al. 2012 and Liu et al. 2015). It is also in the record that by the year 2009, China economy transited to take the position as the second-biggest economy after the USA (World Bank 2009). Besides, between the period 1978 and 2015, China has recorded an increasing factor in its per capita GDP by 18.4%, an equivalent of 3.314 million Renminbi Chinese currencies (National Bureau of Statistics 2015a, b). Within the same period, there were a corresponding rise of 39.1 and 6.7% income amounting to per capita income of 2.47 and 0.85 (‘000) Renminbi for urban and rural residents respectively (National Bureau of Statistics 2015a, b).

The rise in energy use and CO2 emission is another circumstance apprehending the increase of urbanization and per capita GDP (Wang et al. 2012; Zhang and Da 2013). The International Panel on Climate change (IPCC) in 2004 submitted that the dominant GHG, which is CO2 emissions accounts for about 76.7% of the overall emissions (IPCC 2007). Also, the year 2003 marked the beginning of 50% of global CO2 emissions’ generation by emerging economies. Among these developing countries, emissions’ rating is China’s rate, which was ranked as number one in the world in 2006 for the first time. This trend increased to 9680 million tons by 2014, approximately six times the level available in 1978 (Global Carbon Project 2015). More so, China experienced a rise in per capita CO2 emissions, from 1.5 tons in 1978 to an extraordinary level of 7.8 tons in 2015 (Global Carbon Project 2015).

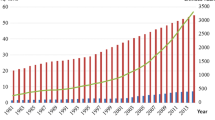

To portray the trend of the link between GHG emissions, income, energy use, and urbanization in China, Fig. 1 displays the trend of events. The observable trends of the variables indicate that GHG emissions, income, energy utilization, and urbanization exhibit similar increasing trends when converted to the same base over the periods 1980–2015. It is evident that during this period, China’s urbanization, energy use, income, and GHG multiplied at moderate degrees of 3.08, 8.05, and 4.95%, respectively. From the statistics given above, it is likely that a valid link prevails between the stated variables which needs to be verified and policy implications applied.

The trend of income, energy use, urban population, and greenhouse gas emissions

The link between per capita income/GDP and environmental ambiance has been reviewed in an episode of the environmental Kuznets curve proposition. These previous studies based their analyses on one assumption of a unidirectional Granger causality from per capita income of GDP to CO2 emissions (Chen et al. 2016). For example, the studies of Jalil and Mahmud (2009); Nasir and Rehman (2011); Govindaraju and Tang (2013); and Ozturk and Acaravci (2013) consistently consider income as the cause and CO2 emissions as a result. In a similar manner, studies, such as Martínez-Zarzoso and Maruotti (2011); Zhu et al. (2012); and Wang et al. (2015) also examine this relationship and consider urbanization and CO2 emissions. However, their studies could not provide any instrument of bidirectional relationship either CO2 emission and per capita GDP or CO2 emission and urbanization or energy consumption. In this circumstance, the employment of a variety of approaches, such as the ARDL and vector error correction model (VECM) Granger causality in the analysis guarantee the affirmation of granting a logical and dependable path to data details, prediction, presumption, and policy guidelines (Stock and Watson 2001).

Also, the simple scheme of these methods guarantees a standardized approach to proving actual progressive relationships beyond various time series (Zhang 2016). Scholars have since accepted the ARDL approach and VECM model and mainly utilized primarily in studying variables’ relationships with cause-effect directions. The present paper adopts the model of ARDL and VECM to examine the interrelationships among the variables of GHG emissions of CO2, income, urbanization, and energy use in one scheme, which can thus deal with the issue of one proposition and objectively reveal the general relationships among the variables of interest. In addition to the methodology, another contribution to the existing literature lies with the introduction of a new phenomenon known as the environmental urbanization Kuznets curve (EUKC) hypothesis. The present research follows the works of Martínez-Zarzoso and Maruotti (2011); Zhu et al. (2012); Wang et al. (2015); and Shahbaz et al. (2016) by considering urbanization in the CO2-growth hypothesis. However, this present study proposes the EUKC hypothesis. Just like the EKC, EUKC presupposes that at the early stage of urbanization, environment degrades by after a threshold point, the technique effects surfaces and environmental degradation reduces with increased urbanization. The theoretical explanation behind the EUKC is that, urbanization may likely create a more modern environment that can lead to improvements in efficiency and resource management.

The remainder of the paper is organized as follows: Following the introduction in “Background” is the presentation of an outstanding review of related literature. “Data, models specifications, and analysis” analyzes the research’s methodology comprises of the source of data and analysis of data. “Outcomes of the analysis and discussion of findings” discusses the results obtained in “Data, models specifications, and analysis,” while conclusion with policy recommendation is situated in “Conclusion and policy recommendations.”

Review of literature

This section reviews empirical literature related to the link between CO2 emissions, urbanization, energy use, and economic growth. However, most recent studies pay attention to the relationship between CO2 emissions and growth or CO2 emissions and urbanization. The present paper reviews literature on CO2 emissions, economic growth, urbanization, and energy use.

Empirical studies on the environment—economic growth-urbanization-energy use

The empirical studies about the link between urbanization, economic growth, and GHG emissions are divided into three strings. The first one considers the connection between urbanization and economic growth. The second one looks at the nexus between economic growth and GHG emissions, while the third one investigates the link between urbanization and GHG emissions.

The proponents of urbanization-growth thesis presuppose that the influence of urbanization on economic growth is that of positive one because economic activities are promoted by large labor force as they move from the traditional agricultural based areas to urban sectors that are industrial and mechanized based. For example, Hossain (2011) examined the compelling causal links between CO2 emissions, energy utilization, economic growth, trade openness, and urbanization for NIC (newly industrialized countries) applying yearly time series data over the period 1971–2007. The result finds that the long-run coefficient of CO2 emissions to energy use (1.2189) is bigger than the short-run coefficient of 0.5984. Kasman and Duman (2015) analyzed the link between energy use, CO2 emissions, GDP per capita, trade openness, and urbanization for a group of new EU member and candidate countries over the period 1992–2010. The main results provide evidence supporting the EKC hypothesis. Hence, there is an inverted U-shaped linkage between environment and income for the sampled countries. The result further supports the positive contribution of urbanization to economic growth in both European Union member and candidate countries. Moreover, similar researches focusing on Chinese economy, such as Liu (2009); Han et al. (2012); and Cheng (2013) confirmed the conclusion that economic growth is fostered by urbanization. On the contrary, the findings of Ghosh and Kanjilal (2014) and Pradhan et al. (2014) refuted the hypothesis that urban development fosters economic growth, rather a conservative theory is drawn that economic growth contributed to urbanization when Indian economy and the G20 economies were considered. Also, bidirectional causality between economic growth and urbanization is detected when Dogan and Turkekul (2016) analyzed the US economy. Dogan and Seker (2016a, b) and Dogan et al. (2017) looked at the determinants of CO2 emissions in both EU and OECD countries and stressed the role of energy, urbanization, and trade openness in determining the rate of CO2 emissions. In another development, a neutrality hypothesis between urbanization and economic growth is detected in the Japanese economy when Hossain (2012) analyzed the relationship between economic growth and urbanization. The result shows no causality at all. The same inference is drawn when Solarin and Shahbaz (2013) and Salim and Shafiei (2014) examined the Angolan economy and the Organization for Economic Cooperation and Development (OECD) countries respectively.

On the relationship between economic growth and CO2 emissions, several studies that used Granger causality analysis draw inferences that anthropogenic activities contribute to increased greenhouse gas emissions due to the fact that industrial development attract huge demands for energy use especially fossil fuels, which can promote environmental degradation. Dogan and Ozturk (2017); Dogan and Inglesi-Lotz (2017); and Inglesi-Lotz and Dogan (2018) examined the role of both renewable and non-renewable energy and income on CO2 emissions in the US economy, panel of biomass consuming countries and Sub-Saharan Africa Big 10 electricity generators. The results of their analysis confirmed the existence of EKC in the US economy, biomass consuming countries, and Sub-Saharan Big electricity generators respectively with policy implications on the role of renewable energy. Solarin (2014) investigated the determinants of carbon dioxide emission with particular emphasis on tourism development in the Malaysian economy. The results reveal long-run relationships between the series and a positive unidirectional long-run causality running from tourist arrivals and the other series to pollution. The study fails to establish any causal relationship between tourism and economic growth in the long run, while economic growth contributes to CO2 emissions. Other studies that obtain similar results and draw similar inferences in China include Chang (2010) and Jalil and Mahmud (2009). However, some studies also discovered a conservative hypothesis, i.e., a situation where CO2 emissions contribute to economic growth and not the other way round. Ang (2008); Menyah and Wolde-Rufael (2010); Pao and Tsai (2010); and Mehrara et al. (2011) confirmed the contribution of CO2 emissions to economic growth. Additionally, some of the studies indicate that a feedback effect exists between economic growth and CO2 emissions especially the findings of Halicioglu (2009); Ghosh (2010); and Long et al. (2015) for the Turkish, Indian, and Chinese economies respectively. Soytas and Sari (2006); Soytas et al. (2007); and Soytas and Sari (2009) in their curious studies showed that there is no cause-effect relationship between economic growth and CO2 emissions for the economies of China, the USA, and Turkey respectively. According to Richmond and Kaufmann (2006), there is a conservative hypothesis between economic growth and CO2 emissions indicating no causality at all between the two variables in a study that involves 36 advanced and developing economies. Besides, using panel data, Dinda and Coondoo (2006) examined the cause-effect relationship between economic growth and CO2 emissions in 88 European countries, Central American countries, and the economies of Africa respectively. The results indicate that a one-way causality runs from economic growth to CO2 emissions, another unidirectional relationship from CO2 emissions to economic growth and bidirectional causality between the two economic growth and CO2 emissions in European countries, Central American countries, and the economies of Africa respectively.

The following inference is used to surmise the relationship between urbanization and CO2 emissions. The level of urbanization determines greenhouse gas emissions because urbanization to a large extent affects the population and invariably the disposition of consumption. In this case, the intensification of production in the urban areas becomes necessary. In what follows as a result of urbanization is the increase in the rate of energy consumption especially non-renewable and harsh environmental challenges. The study of Wang et al. (2016a, b) and Wang et al. (2016a, b) unravel the contributions of urban development to massive CO2 emissions especially in emerging Southeast Asian countries and the BRICS (Brazil, Russia, India, China, and South Africa) countries in this order. Similarly, Kasman and Duman (2015) analyzed the relationship between urbanization and CO2 emissions in EU member and candidate countries and came up with the following submission: Urbanization is one of the leading causes of rising CO2 emissions. Al-mulali et al. (2012) analyzed the economies of the following countries: East Asia and the Pacific, Eastern Europe and Central Asia, Latin America and the Caribbean, the Middle East and Northern Africa, Southern Asia, Sub-Saharan Africa and Western Europe, and concur with the submission that urbanization is the cause of increasing CO2 emissions. The result further indicates that about 84% correlation between urbanization and CO2 emissions in the positive direction is found in these countries. In the context of China, Zhang and Lin (2012) asserted that an urbanization and CO2 emissions have a direct relationship. On the contrary, Hossain (2011) examined nine emerging-advanced economies and surmised that a conservative hypothesis exists between the development of urbanization and CO2 emissions. In other words, no causal inference is found from urbanization to CO2 emissions. Another dimension of the relationship between urbanization and CO2 emissions is feedback effects or bidirectional causality between urbanization and CO2 emissions. For example, Al-mulali et al. (2013) examined the economies of the Middle East and North Africa (MENA), and their results reveal what is known as feedback effect or two-way causality between urbanization and CO2 emissions. Similarly, Dogan and Turkekul (2016) in their study of the US economy maintain that a feedback effect exists between urbanization and CO2 emissions. But on the contrary, Hossain (2012) studied the Japanese economy to unravel the relationship between urbanization and CO2 emissions submits that no causal relationship is detected between urbanization and CO2 emissions. Masih and Masih (1996) Hondroyiannis et al. (2002); Payne (2010); Chen et al. (2016); and Zhang (2016) note that although a lot of studies regarding the nexus between greenhouse gas emissions, economic growth, and urbanization have been investigated, there has always been lack of consistency in most of the analytical outcomes. The lack of consistencies in the inferences drawn from these previous studies in relation to greenhouse gas emissions-growth-urbanization links may be attributed to so many reasons ranging from the choice of the regressors to be included in the model, the category of country (ies) chosen, the nature of data and the time frame of data that gives rise to the data generating process, and precisely the experimental formulation of the econometric model, which can lead to specification bias. Besides, China as the fast growing and emerging economy over the years have been facing the clashing objectives of economic expansion as well as ensuring environmental quality and drastic greenhouse gas emissions mitigation. As a result of this, there is the need for China to bring to light the real nexus between these variables of interest to help formulate not only environmental policy or growth policy but the energy and demographic policies as well. Some related studies, such as Zhang et al. (2014) find significant causal links from urbanization and economic growth to greenhouse gas emission depth and Liu et al. (2016) also indicated that variations in greenhouse gas are majorly caused by urbanization and economic growth in China but not the other way round. These related studies dwell on the aggregate perspective and mainly apply total economic indexes, such as GDP, which may be pushed by changes in the level of investment, incomes, energy use and by the industrial improvement. Hence, these aggregate economic indexes’ link to urbanization and greenhouse gas emissions may not be direct. To fill this literature and empirical gap, this present study dwells on the micro perspective mainly income from the masses, while adding energy consumption as another regressor that influences greenhouse gas emissions. The nexus between micro-income, urbanization, and greenhouse gas emissions is assumed to be firm. Urbanization may lead to an increase in both income and changes in household consumption structure and to an increase in energy consumption, which may invariably lead to massive greenhouse gas emissions. Meanwhile, the rise in income can motivate people to move to urban areas, which may result in an increase in the rate of urbanization and higher energy consumption. Unravel this nexus has a lot of policy implications.

Data, models specifications, and analysis

Source of data

This paper obtains relevant documented data from 1978 to 2015 from National Bureau of Statistics of China (2015a, b) and World Development Indicators of the World Bank, 2017. Meanwhile, in decoupling greenhouse gas emissions and economic growth, the study considers the intermediary roles of urbanization and energy consumption. Urbanization rate is the ratio of urban resident population to the total resident population.

Model specification

In line with the objective of the study, which is to examine the role of urbanization in decoupling greenhouse gas emissions of CO2 and economic growth with energy use as another determinant of greenhouse gases of CO2, the studies of Grossman and Krueger (1991); Martínez-Zarzoso and Maruotti (2011); Saboori and Sulaiman (2013a, b); Saboori and Sulaiman (2013a, b); Al-Mulali et al. (2015); Shahbaz et al. (2016); and Miao (2017) are adopted. The CO2 emission was predicated by income rise, and it is assumed that a dynamic linear relationship exists between the two variables. However, the hypothesis of ecological permutation is used to produce a link between greenhouse gas emissions of CO2 with income, urbanization, and energy use. The theory surmises that urbanization is a demographic index, which raises urban density and converts the system of rational manner, through affecting household energy utilization (Poumanyvong and Kaneko 2010 and Sadorsky 2014). In the present stage, the direct link between greenhouse gas emission of CO2 and urbanization is uncertain; a downturned U-shape could surface which is extremely dependent on the development level. Shahbaz et al. (2016) applied a simple quadratic function to estimate the dynamic link between CO2 emissions and urbanization. Following these theorists and in line with the objective of the study, the present research also follows the Stochastic Impacts by Regression on Population, Affluence and Technology (STIRPAT) model introduced by Dietz and Rosa (1994) and York et al. (2005). This model is rapidly examined in existing literature to investigate impact of socioeconomic changes on environmental degradation. Often, population is treated as independent variable to examine its impact on environmental quality. This model corrects the weakness of EKC where income per capita is used as independent variables and CO2 emissions per capita as dependent variables but substitute the population variable with urbanization while keeping the impact of population on environment unit elastic. The point is that population elasticity of energy remains same in developed and developing economies. The STIRPAT model, in its general form, can be expressed as follows:

where GHE is pollutants, ENR is energy consumption, P is population, A is affluence (economic growth), T is technology and ν is a stochastic term. The research extends this model by incorporating urbanization. Urbanization may likely create a more modern environment that can lead to improvements in efficiency and resource management. Urbanization may affect energy consumption via income effect, technique effect and composite effect and hence greenhouse gas emissions CO2. The augmented version of STIRPAT model with urbanization is given below:

where GHE, INC, URB, and ENR represent greenhouse gas emissions of CO2, income, urbanization, and energy use respectively. The βs represent coefficients of the relationship among greenhouse gas emissions of CO2, income, income square, urbanization, urbanization square, and energy use respectively. To estimate the EKC as well as the new version of the EKC with urbanization (EUKC) and interpreted the statistical meanings of the coefficients as elasticities, the logical, and adequate model of the non-linear function (Eq. 2) is transformed to a linear, logarithmic designation by taking the natural logarithm and is presented as follows:

where α = constant. The coefficients βi are the elasticities of the dependent variables on the independent variables.

Estimation analysis

In line with the objective of the study which is to scrutinize the role of urbanization in unyoking greenhouse gas emissions of CO2 and economic growth with energy as an important variable, the study begins with a unit root test to check the stationary nature of the variables under consideration.

Stationarity test

The conventional procedure to test for cointegration between variables is to first test the stationary properties of each variables. The most frequently used tests for this analysis are the Dickey and Fuller (1981); Phillips and Perron (1988); Elliott et al. (1996); and Ng and Perron (2001). However, findings from these stationarity tests could be biased under many fronts. For instance, these test results suffer from small sample size bias and poor power properties as stated by Dejong et al. (1992). Thus unit root tests, such as ADF, PP, and DF-GLS may lead to over-rejection of the true null hypothesis or accepting the null when it is false. Although Ng and Perron (2001) unit root test does not suffer from this particular problem, it provides biased results when structural breaks are present in the series. Under such circumstances, a more appropriate test is Zivot and Andrews (1992) and Clemente et al. (1998) test, which takes care of the problems resulting from structural breaks and it has more power compared to the Perron and Volgelsang (1992) ADF, PP, and Ng-Perron unit root tests. The limitation of Perron and Volgelsang (1992) and Zivot and Andrews (1992) unit root tests is that they are appropriate if the series has one potential structural break. This study utilized an Ng-Perron test and Zivot-Andrews (Z-A) because of its capacity to surmount the challenge of low power and size bias. It makes use of the concept of a GLS (generalized least squares) de-trending to enhance the ability of the analysis and to develop the scheme for selecting the truncation lag by adjusting the lag choice to produce a supplementary size bias in the non-stationary analysis (Ng and Perron 2001; Zivot and Andrews 1992).

Cointegration test

The F-bounds analysis within the ARDL scheme is applied because of its capacity to remove the limitations of other long run relationships’ procedures of Engle and Granger (1987); Johansen and Juselius (1990). In the same manner, Bekhet and Matar (2013); Begum et al. (2015); Ivy-Yap and Bekhet (2016); Shahbaz et al. (2016); Bekhet et al. (2017) listed quite some advantages that are associated with the procedure of ARDL. According to these researchers, the technique can be applied to measure the short and long run estimates concurrently. The problem of autocorrelation and endogeneity is solved with the joint application of short- and long-term components, coupled with the appropriate number of lags which ordinarily could lead to biasedness in the estimation procedure. Other researchers, such as Narayan (2005) and Farhani et al. (2014) attest to the fact that F-bounds test is appropriate for small sample sizes probably that falls between 30 and 80 inclusive and is also far better than Johansen multivariate cointegration. Equation (4) specified the dynamic link among greenhouse gas emissions of CO2, income, urbanization, and energy use:

where Δ is the first difference operator, αs represent the intercepts, and βijs and ϕijs denote the long- and short-run elasticities of the variables respectively. Ψits describe the error terms, p is the ideal lag length, and l indicates the optimal number of lag (Engle and Granger 1987; Johansen and Juselius 1990; Sugiawan and Managi 2016). The hypothesis to be tested is as follows: H0: βijs = 0 against H1: βijs ≠ 0, and H0: ϕijs = 0 against H1: ϕijs ≠0, respectively. The long- and short-run significance of the estimates can be tested using the F statistics and the inference to reject or not to reject the H0 is dependent upon the following procedure (Pesaran et al. 2001; Shahbaz and Lean 2012; Bekhet et al. 2017):

-

If F statistics > upper limit critical value, H0 is rejected for cointegration exists;

-

If F statistics < lower limit critical value, H0 is not rejected for cointegration does not exist; and

-

If F statistics falls between the lower and upper limits critical values, then no inference can be drawn and therefore the decision is inconclusive (Narayan 2005).

However, in a situation where the result is inconclusive, the stationary nature of the residuals is tested. If the residuals are found to be stationary, the variables have a long-run relationship, and the revised is the case (Ivy-Yap and Bekhet 2015, 2016). Where the dynamic link between the variables mentioned above is confirmed, the long-run greenhouse gas of CO2 elasticity toward the variations in its factors can be measured (Begum et al. 2015; Dogan and Turkekul 2016; Ivy-Yap and Bekhet 2015, 2016). The direction of the causal link between greenhouse gas emissions of CO2, income, urbanization, and energy use can be determined by using the VECM structure (Bekhet and Al-Smadi 2015; Bekhet and Al-Smadi 2017; Bekhet et al. 2017). Hence, Eq. (5) is specified to estimate a long- and short-run causality between the variables under consideration.

Equation (5) shows the ECTt-1s which are lagged error correction terms extracted from the cointegration link. In the words of Masih and Masih (1996), the long-run causality relationship can be established via the parameters ηis of ECTt-1 by applying the t statistic. On the other way round, the reliability of the elasticity, βij for each determinant by joint Wald-F or chi-square statistic shows the short-run directional relationship. Then, the ζi are the white-noise residuals, which are assumed to be normally distributed with zero mean and constant variance, non-heteroscedastic, non-serial correlated, and absence of multicollinearity. However, the violation of anyone of the previous benchmarks means the model could be confronted with biasedness in its parameters and become inefficient while producing an invalid inference. Thus, to make sure that the estimated model does not encounter the above-mentioned challenges, diagnostic analyses of ARCH (conditional), Breusch–Godfrey (heteroscedasticity) Breusch–Pagan–Godfrey (for autocorrelation), and RAMSEY-Reset (for stability) tests are carried out to ascertain the validity of the model (Brown et al. 1975; Bekhet and Matar 2013; Abid 2015).

Outcomes of the analysis and discussion of findings

The results of the data analysis including the discussion of the main findings are presented in this section. It begins with the descriptive analysis, followed by the stationary test of variables. Long-run relation analysis supersedes the unit root test, while the estimation of structural parameters and lastly Granger causality follow suit.

Descriptive and correlation tests results

The discussion on the nature of variances in the variables begins with the description of the investigated variables. Table 1 describes the descriptive analysis of the variables.

A look at the descriptive analysis shows that the investigated variables display some insignificant variances in the statistics. The average and standard deviation values of greenhouse gas emission of CO2 are 1.1004 and 0.5339 respectively. The average and standard deviation values of income stand at 7.2242 and 0.9452 respectively. Urbanization and energy use have mean values of 3.4772 and 6.8992 respectively, while the respective standard deviations stand at 0.3415 and 0.4439 respectively. The large standard deviations of the variables are indications of large variations of the values around their averages, hence, large disparities. However, the Jarque-Bera values alongside the probability values greater than the 5% critical values indicate the normality properties of the models’ distributions.

Table 1 further shows the correlation coefficients of the interrelated variables. Due to the high correlation between the independent variables which could lead to the econometric problem of multicollinearity, the data is transformed by finding the natural logarithm. The correlation coefficient between greenhouse gas emission of CO2 and income is 0.8766 implying that the relationship between greenhouse gas emission of CO2 and income 87.66%. The relationship between greenhouse gas emission of CO2 and urbanization is approximately 79.88% in a positive direction, while the relationship between greenhouse gas emission of CO2 and energy is positively strong at 97.64%. The correlation coefficient of income and urbanization stands at 0.6287 (62.87%). The correlation coefficients of income and energy and between urbanization and energy are 0.5460 (54.64%) and 0.5954 (59.54%) respectively.

Stationary test results

Although the present research utilizes the Ng-perron, it further compliments it with the Zivot-Andrews (Z-A) structural breaks unit root tests to examine the stationary nature of the investigated variables. The reason behind the Z-A structural unit root test is to overcome the problem of outliers and structural breaks in time series data in which augmented Dickey-Fuller (ADF), Phillips Perron (PP), and DF-GLS test by Elliott et al. (1996) cannot overcome. The exact data about the structural break would assist policy to consider these structural breaks when formulating a thorough urbanization, energy, and growth policies in the economy.

The results of the unit root in Table 2 show that only LINC is significantly stationary at level [I(0)] at the 5% level, while LGHE, LURB, and LENR are substantially stationary at first difference; [I(1)] and at the 1% level. These results are in line with the perception that most of the macroeconomics variables are non-stationary at level (have unit root), however, become stationary at either first (Bekhet and bt Othman 2011; Riti and Shu 2016; Riti et al. 2017a, b).

The structural breaks unit root test of Zivot-Andrews (Z-A) in Table 3 also supports the notion that only LINC is stationary at level while the remaining variables become stationary at order one. LGHE is integrated of order one and has its break points in 2006 at levels and 2002 at first difference. LINC is integrated at the level and has its break points in 2002 at levels and 2012 at first difference respectively. LURB, on the other hand, is integrated of order one and has its break points in 2011 at level and 2008 at first difference, while LENR is integrated of order one and has its breakpoints occur in 2001 at the level and 2002 at first difference. These break points happen mostly in the 2000s which coincide with the period in which energy, urbanization policies’ impacts are manifesting.

Long-run relationship test results

Lütkepohl (2011); Bekhet and Al-Smadi (2015); Riti and Shu (2016); and Sugiawan and Managi (2016) argue that the F-bounds test is the most appropriate procedure to analyze cointegration test if there is the mixture of level, I(0) and first difference, I(1) variables couple with a small sample size. The present study follows the argument of Alkhathlan et al. (2012); Bekhet and Al-Smadi (2015); and Sugiawan and Managi (2016) because of the small sample of the present study, which is comparatively small, and the existence of I(0) and I(1) in the variables.

The cointegration among variables is analyzed over the period 1978–2015 at 5% significant level (Table 4). The literature of Arvin et al. (2015); Kasman and Duman (2015); Shahbaz et al. (2016); Sodri and Garniwa (2016); and Wang et al. (2016a, b) provide similar findings. The F-bounds tests of Table 3 reveal interesting long-run relationships in all the models except the model of GHE = INC, INC2 which cointegration does not exist. All the other models reject the null hypothesis of no cointegration and show that the F statistic values are greater than the upper bounds value at either 1 or 5% respectively. The implication is that various long-run vectors exist between the dependent variable of greenhouse gas emissions of CO2 and the underlying determinants of same.

Results of short- and long-run elasticities

Based on the above findings, the long-run elasticities and the existence of an inverted U-shaped relationship between greenhouses gas emissions of CO2 and both income and urbanization are measured using different models.

Model 1 in Table 5 specifies greenhouse gas emissions of CO2 as a function of income, urbanization, and energy use. The model shows that only energy is statistically significant in explaining the variations in greenhouse gas emissions of CO2 in both short and long run with the appropriate signs. A 1% increase in energy all things being equal would lead to a 0.908 and 1.984% increase in greenhouse gas emissions of CO2 in the short and long run respectively. Urbanization is only found to be significant in the short run, while a long-run analysis shows that the variable does not cause fluctuations in greenhouse gas emissions of CO2. Income however in model 1 does not show any significance influence on greenhouse gas emissions of CO2. The adjustment mechanism of short-run distortions, while negatively signed hovers around 2.365%.

Model 2 specifies greenhouse gas emissions of CO2 as a function of income and income squared. The coefficient of income and income squared display signs contrary to expectation although significant in the long run, while insignificant in the short run. The long-run coefficient of income and income squared show that greenhouse gas emissions of CO2 reduces and increases by 21.09 and 1.168% with a 1% increase in income and income squared respectively. This notion contradicts the environmental carbon Kuznets curve (ECKC) when income is considered. The error correction mechanism (ECM) that signifies the restoration of dynamic distortions from the short to long run is approximately 2.618%.

Model 3 of Table 4 specifies greenhouse gas emissions of CO2 as a function of urbanization and its squares. The model displays an insignificant effects of urbanization on greenhouse gas emissions of CO2 in the long run. The short-run analysis, however, shows that a 1% increase in urbanization would lead to 2.288% rise in greenhouse gas emissions of CO2.

Model 4 formulates greenhouse gas emissions of CO2 as a function of income, its squares, and energy use. The result only validates energy environment-hypothesis, where energy is the primary determinants of greenhouse gas emissions of CO2. Income, however, is statistically insignificant in both short and long runs. A 1% increase in energy would lead to a 0.943 and 1.251% rise in greenhouse gas emissions of CO2. The rate of restoration of the variables is 4.484% in the event of an adjustment to the long run.

Model 5 of Table 4 specifies greenhouse gas emissions of CO2 as a function of urbanization, its squares, and energy use. The findings indicate that while the square of urbanization is significant in the long run, its short-run coefficient and the coefficient of urbanization proper are insignificant statistically. The coefficients of energy use in both short run and long run indicate significance implying that energy is a major determinant of greenhouse gas emissions of CO2, without which the models suffer variable omission bias. A 1% increase in the square of urbanization would lead to a 1.318 decrease in greenhouse gas emissions of CO2 revealing the EUKC when urbanization is considered with energy as an additional variable. The model also shows that greenhouse gas emissions of CO2 increases by 0.704 and 3.008% with an increase in energy use by 1% in both short and long run respectively. The model short-run distortion is corrected at a speed of 37.10% to the long term. The influence of energy use on greenhouse gas emissions of CO2 is reiterated in the studies of (Riti and Shu 2016 Riti et al. 2017a, b and Riti et al. 2018).

Model 6 analyses greenhouse gas emissions of CO2 as a function of income, urbanization, their squares, and energy use. The outcome of the analyses confirms that urbanization and energy are the major contributors to greenhouse gas emissions of CO2 rise, while income shows insignificant influence on greenhouse gas emissions of CO2. Energy use in model 6 contributes 0.678 and 1.503% to greenhouse gas emissions of CO2 rise in the short and long runs. Urbanization and its square, however, are significant in the long run in affecting greenhouse gas emissions of CO2. The coefficients of urbanization and its square are found to significantly contribute to greenhouse gas emissions of CO2 rise of about 5.104 and 1.318% in the positive and negative directions respectively, which support the inverted U-shaped relationship between greenhouse gas emissions of CO2 and urbanization in the long run. The findings of this research agree with the results of Wang et al. (2015) for OECD countries and Shahbaz et al. (2016) for the Malaysian economy on the relationship between CO2 and urbanization. The findings also agree with Martínez-Zarzoso and Maruotti (2011) for 88 developing economies and the outcomes of Zi et al. (2016) for the Chinese economy. However, the result contradicts that of He et al. (2017) for the Chinese economy and Shahbaz et al. (2016) for the Malaysian economy. These shreds of evidence propose that CO2 emissions increase at the initial stage of urbanization and suddenly decrease at higher stage of urbanization. The result is also in line with the hypotheses of demographic, ecological modernization, and environmental transition.

Overall, the selected regression models met all the diagnostic conditions. The Ramsey RESET and the autoregressive conditional heteroscedasticity (ARCH) analyses show that the chosen models are free from the overall model formulation problems and also ARCH challenges. In conclusion, the Breusch-Godfrey LM test cannot reject the null hypothesis of autocorrelation up to second order, meaning that the selected models do not suffer from autocorrelation econometric complication. Therefore, the chosen models are appropriately formulated and can be used for policy frameworks (Fig. 2).

Long-run coefficients of greenhouse gas emissions of CO2 and its determinants. Single, double, and triple asterisks indicate significance of the elasticities at 1, 5, and 10% significance level respectively

The negative relationship between the variables as mentioned earlier at the higher level of urbanization is a result of Chinese authority’s interference through its energy, demographic, and environment policies.

Results of vector error correction mechanism Granger causality test

Furthermore, causality data is important for policymakers to identify the directions of causality among the variables to control reasonable policies. Table 5 shows the multivariate causal relationship among the variables

The results in Table 6 and Fig. 3 indicate the long-run bidirectional causal relationships between greenhouse gas emissions of CO2 and the explanatory variables of income, energy, and urbanization. Long-run causality signifies that LGHE and its determinants are 2.76% and significant at 5% levels, while LINC and its determinants are 0.20% and significant at 1%. Long-run causality of LENR and its determinants is 2.83% and significant at 1% while long-run causality of LURB and its determinants is 0.01% and significant at 5%. The short-run causality indicates that a unidirectional causality runs from LGHE to LENR showing a conservative hypothesis, while bidirectional causality is detected between LINC and LENR revealing a feedback effects relationship. The feedback causality relationship between urbanization and greenhouse gas emissions of CO2 is consistent with the studies of Zhang et al. (2014) and Al-mulali et al. (2012) for the case of seven regions, and Al-mulali et al. (2013) for the case of MENA countries. However, the outcome of the analysis is not in line with the works of Wang et al. (2016a, b); Wang et al. (2016a, b) and Shahbaz et al. (2016) for the case of BRIC economies, ASEAN economies, and Malaysian economy respectively.

Short- and long-run VECM Granger causality directions. The inner arrows indicate short-run causality, while the outer ones show long-run causality

Conclusion and policy recommendations

This study scrutinizes the role of urbanization in unyoking greenhouse gas emissions and income by examining the dynamic relationships among the variables with the inclusion of another possible determinant of greenhouse gas emissions of CO2 (energy use). The study utilizes the F-bounds test and VECM Granger causality to achieve the objective of the role of urbanization in unyoking greenhouse gas emissions of CO2 and economic growth in China. While the inverted down turned environmental Kuznets curve could not be detected between income and greenhouse gas emissions of CO2, the results reveal the existence of dynamic relationship among variables and the inverted down turned U-shaped relationship between greenhouse gas emissions of CO2 and urbanization in the long run. Also, the greenhouse gas emissions of CO2—urbanization coefficient is detected to be positively elastic at the initial stage of urbanization (17.3957); after reaching the turning point, it turns out to negative elastic (− 2.7103) implying that the environmental urbanization Kuznets curve exists. In term of causality relationship, although no short-run causality exists between urbanization and greenhouse gas emissions of CO2, a long-run significant bidirectional causality is detected between the two variables at 5%. Moreover, this study has captured the significant influence of energy use on greenhouse emissions of CO2 in the all the six models. The implication of this result is that energy is a significant variable in greenhouse gas emissions of CO2 model, its absence which means an important variable is omitted (variable omission bias). The insignificance of income in the models implies that income is rather an effect than a cause variable in the growth-environment hypothesis especially when greenhouse gas emission of CO2 is considered.

The presence of the EUKC shows that China’s adoption and ratification of relevant household enrolment policies is in the right direction since urbanization in the long run does not harm the environment. This implies that urbanization is not a major problem of environmental degradation, but the type of energy produced and consumed is a major factor to put into scrutiny. These results could serve as a policy framework for handling urbanization development, taking into consideration the clean venture and other green countenances. Thus, the economic development and environmental quality can be equalized while unyoking greenhouse gas emissions of CO2 and income. By developing and executing stringent policies, such as carbon taxation and carbon emissions trading, China through its authority could unswervingly mitigate greenhouse gas emissions of CO2. Under scenario of environmental regulatory reforms, those enterprises that are culpable of emitting greenhouse gas emissions of CO2 would settle for their polluting manners. This is because the settlements of environmental costs prompt firms to employ clean techniques and develop efficiency in their energy utilization. Concurrently, firms should raise the collective culture of protecting the environment and thereby become ethically liable by and setting-up environmental funds. On the other hand, individuals should act as a matter of necessity to set-up the consumption behaviors of environmental preservations, which imply that bettering the energy utilization network and raising green consumption should be taking into consideration. This further means that individuals need to consume more energy-efficient products.

As a suggestion for further research in environmental urban Kuznets curve hypothesis, the functional model of the present research should be extended to capture other variables that are likely to account for CO2 emissions. In addition, micro-stage data of the various Chinese regions should be used to check the existence and non-existence of EKC aggregation bias.

References

Abid M (2015) The close relationship between informal economic growth and carbon emissions in Tunisia since 1980: the (ir) relevance of structural breaks. Sustain Cities Soc 15:11–21

Alkhathlan K, Alam M, Javid M (2012) Carbon dioxide emissions, energy consumption and economic growth in Saudi Arabia: a multivariate cointegration analysis. Br J Econ Manag Trade 2(4):327–339

Al-mulali U, Sab CNBC, Fereidouni HG (2012) Exploring the bi-directional long run relationship between urbanization, energy consumption, and carbon dioxide emission. Energy 46(1):156–167

Al-mulali U, Fereidouni HG, Lee JY, Sab CNBC (2013) Exploring the relationship between urbanization, energy consumption, and CO2 emission in MENA countries. Renew Sust Energ Rev 23:107–112

Al-Mulali U, Weng-Wai C, Sheau-Ting L, Mohammed AH (2015) Investigating the environmental Kuznets curve (EKC) hypothesis by utilizing the ecological footprint as an indicator of environmental degradation. Ecol Indic 48:315–323

Ang JB (2008) Economic development, pollutant emissions and energy consumption in Malaysia. J Policy Model 30(2):271–278

Arvin MB, Pradhan RP, Norman NR (2015) Transportation intensity, urbanization, economic growth, and CO2 emissions in the G-20 countries. Util Policy 35:50–66

Begum RA, Sohag K, Abdullah SMS, Jaafar M (2015) CO2 emissions, energy consumption, economic and population growth in Malaysia. Renew Sust Energ Rev 41:594–601

Bekhet HA, Al-Smadi RW (2015) Determinants of Jordanian foreign direct investment inflows: bounds testing approach. Econ Model 46:27–35

Bekhet HA, Al-Smadi RW (2017) Exploring the long-run and short-run elasticities between FDI inflow and its determinants in Jordan. Int J Bus Glob 18(3):337–362

Bekhet HA, bt Othman NS (2011) Causality analysis among electricity consumption, consumer expenditure, gross domestic product (GDP) and foreign direct investment (FDI): case study of Malaysia. J Econ Int Finance 3(4):228

Bekhet HA, Matar A (2013) FV and causality analysis between stock market prices and their determinates in Jordan. Econ Model 35:508–514

Bekhet HA, Matar A, Yasmin T (2017) CO2 emissions, energy consumption, economic growth, and financial development in GCC countries: dynamic simultaneous equation models. Renew Sust Energ Rev 70:117–132

Brown RL, Durbin J, Evans JM (1975) Techniques for testing the constancy of regression relationships over time. J R Stat Soc Ser B Methodol: 149–192

Chang CC (2010) A multivariate causality test of carbon dioxide emissions, energy consumption and economic growth in China. Appl Energy 87(11):3533–3537

Chen PY, Chen ST, Hsu CS, Chen CC (2016) Modeling the global relationships among economic growth, energy consumption and CO2 emissions. Renew Sust Energ Rev 65:420–431

Cheng C (2013) Dynamic quantitative analysis on Chinese urbanization and growth of service sector. LISS 2012, Springer: 663–670

Clemente J, Montañés A, Reyes M (1998) Testing for a unit root in variables with a double change in the mean. Econ Lett 59(2):175–182

Dejong DN, Nankervis JC, Savin NE (1992) Integration versus trend stationarity in time series. Econometrica 60:423–433

Dickey DA, Fuller WA (1981) Likelihood ratio statistics for autoregressive time series with a unit root. Econometrica 49:1057–1079

Dietz T, Rosa EA (1994) Rethinking the environmental impacts of population, affluence, and technology. Hum Ecol Rev 1(2):277–300

Dinda S, Coondoo D (2006) Income and emission: a panel data-based cointegration analysis. Ecol Econ 57(2):167–181

Dogan E, Inglesi-Lotz R (2017) Analyzing the effects of real income and biomass energy consumption on carbon dioxide (CO2) emissions: empirical evidence from the panel of biomass-consuming countries. Energy 138:721–727

Dogan E, Ozturk I (2017) The influence of renewable and non-renewable energy consumption and real income on CO2 emissions in the USA: evidence from structural break tests. Environ Sci Pollut Res 24(11):10846–10854

Dogan E, Seker F (2016a) Determinants of CO2 emissions in the European Union: the role of renewable and non-renewable energy. Renew Energy 94:429–439

Dogan E, Seker F (2016b) An investigation on the determinants of carbon emissions for OECD countries: empirical evidence from panel models robust to heterogeneity and cross-sectional dependence. Environ Sci Pollut Res 23(14):14646–14655

Dogan E, Turkekul B (2016) CO2 emissions, real output, energy consumption, trade, urbanization and financial development: testing the EKC hypothesis for the USA. Environ Sci Pollut Res 23(2):1203–1213

Dogan E, Seker F, Bulbul S (2017) Investigating the impacts of energy consumption, real GDP, tourism and trade on CO2 emissions by accounting for cross-sectional dependence: a panel study of OECD countries. Curr Issue Tour 20(16):1701–1719

Elliott GR, Thomas J, Stock JH (1996) Efficient tests for an autoregressive unit root. Econometrica 64:813–836

Engle RF, Granger CW (1987) Co-integration and error correction: representation, estimation, and testing. Econometrica 55:251–276

Farhani S, Shahbaz M, Sbia R, Chaibi A (2014) What does MENA region initially need: grow output or mitigate CO2 emissions? Econ Model 38:270–281

Ghosh S (2010) Examining carbon emissions economic growth nexus for India: a multivariate cointegration approach. Energy Policy 38(6):3008–3014

Ghosh S, Kanjilal K (2014) Long-term equilibrium relationship between urbanization, energy consumption and economic activity: empirical evidence from India. Energy 66:324–331

Global Carbon Project, 2015. Global carbon atlas 2015. http://www.globalcarbonatlas.org/?q=en/emissions. Accessed 29 April, 2017

Govindaraju VC, Tang CF (2013) The dynamic links between CO2 emissions, economic growth and coal consumption in China and India. Appl Energy 104:310–318

Grossman GM, Krueger AB (1991) Environmental impacts of a North American free trade agreement, National Bureau of Economic Research

Halicioglu F (2009) An econometric study of CO 2 emissions, energy consumption, income and foreign trade in Turkey. Energy Policy 37(3):1156–1164

Han X, Wu PL, Dong WL (2012) An analysis on interaction mechanism of urbanization and industrial structure evolution in Shandong, China. Procedia Environ Sci 13:1291–1300

He Z, Xu S, Shen W, Long R, Chen H (2017) Impact of urbanization on energy related CO2 emission at different development levels: regional difference in China based on panel estimation. J Clean Prod 140:1719–1730

Hondroyiannis G, Lolos S, Papapetrou E (2002) Energy consumption and economic growth: assessing the evidence from Greece. Energy Econ 24(4):319–336

Hossain MS (2011) Panel estimation for CO2 emissions, energy consumption, economic growth, trade openness and urbanization of newly industrialized countries. Energy Policy 39(11):6991–6999

Hossain S (2012) An econometric analysis for CO2 emissions, energy consumption, economic growth, foreign trade and urbanization of Japan. https://doi.org/10.4236/lce.2012.323013

Inglesi-Lotz R, Dogan E (2018) The role of renewable versus non-renewable energy to the level of CO2 emissions a panel analysis of sub-Saharan Africa’s Βig 10 electricity generators. Renew Energy 123:36–43

IPCC (Intergovernmental Panel on Climate Change) (2007) Climate change 2007: the physical science basis. Cambridge Press, New York

Ivy-Yap LL, Bekhet HA (2015) Examining the feedback response of residential electricity consumption towards changes in its determinants: evidence from Malaysia. Int J Energy Econ Policy 5(3):772–781

Ivy-Yap LL, Bekhet HA (2016) Modelling the causal linkages among residential electricity consumption, gross domestic product, price of electricity, price of electric appliances, population and foreign direct investment in Malaysia. Int J Energy Technol Policy 12(1):41–59

Jalil A, Mahmud SF (2009) Environment Kuznets curve for CO2 emissions: a cointegration analysis for China. Energy Policy 37(12):5167–5172

Johansen S, Juselius K (1990) Maximum likelihood estimation and inference on cointegration—with applications to the demand for money. Oxf Bull Econ Stat 52(2):169–210

Kasman A, Duman YS (2015) CO2 emissions, economic growth, energy consumption, trade and urbanization in new EU member and candidate countries: a panel data analysis. Econ Model 44:97–103

Liu Y (2009) Exploring the relationship between urbanization and energy consumption in China using ARDL (autoregressive distributed lag) and FDM (factor decomposition model). Energy 34(11):1846–1854

Liu TY, Su CW, Jiang XZ (2015) Is economic growth improving urbanization? A cross-regional study of China. Urban Stud 52(10):1883–1898

Liu Y, Yan B, Zhou Y (2016) Urbanization, economic growth, and carbon dioxide emissions in China: a panel cointegration and causality analysis. J Geogr Sci 26(2):131–152

Long X, Naminse EY, Du J, Zhuang J (2015) Nonrenewable energy, renewable energy, carbon dioxide emissions and economic growth in China from 1952 to 2012. Renew Sust Energ Rev 52:680–688

Lütkepohl H (2011) Vector autoregressive models. Springer, Berlin Heidelberg, pp 1645–1647

Martínez-Zarzoso I, Maruotti A (2011) The impact of urbanization on CO2 emissions: evidence from developing countries. Ecol Econ 70(7):1344–1353

Masih AM, Masih R (1996) Energy consumption, real income and temporal causality: results from a multi-country study based on cointegration and error-correction modelling techniques. Energy Econ 18(3):165–183

Mehrara M, Sharzei G, Mohaghegh M (2011) The relationship between health expenditure and environmental quality in developing countries. J Health Adm 14(46)

Menyah K, Wolde-Rufael Y (2010) Energy consumption, pollutant emissions and economic growth in South Africa. Energy Econ 32(6):1374–1382

Miao L (2017) Examining the impact factors of urban residential energy consumption and CO2 emissions in China–evidence from city-level data. Ecol Indic 73:29–37

Narayan PK (2005) The saving and investment nexus for China: evidence from cointegration tests. Appl Econ 37(17):1979–1990

Nasir M, Rehman FU (2011) Environmental Kuznets curve for carbon emissions in Pakistan: an empirical investigation. Energy Policy 39(3):1857–1864

National Bureau of Statistics of the People’s Republic of China (2015a) China statistical yearbook 2015. China Statistics Press, Beijing

National Bureau of Statistics of the People’s Republic of China (2015b) New China in 65 years. China Statistics Press, Beijing

Ng S, Perron P (2001) Lag length selection and the construction of unit root tests with good size and power. Econometrica 69(6):1519–1554

Ozturk I, Acaravci A (2013) The long-run and causal analysis of energy, growth, openness and financial development on carbon emissions in Turkey. Energy Econ 36:262–267

Pao HT, Tsai CM (2010) CO2 emissions, energy consumption and economic growth in BRIC countries. Energy Policy 38(12):7850–7860

Payne JE (2010) A survey of the electricity consumption-growth literature. Appl Energy 87(3):723–731

Perron P, Volgelsang TJ (1992) Nonstationarity and level shifts with an application to purchasing power parity. J Bus Econ Stat 10(3):301–320

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econ 16(3):289–326

Phillips PC, Perron P (1988) Testing for a unit root in time series regression. Biometrika 75(2):335–346

Poumanyvong P, Kaneko S (2010) Does urbanization lead to less energy use and lower CO2 emissions? A cross-country analysis. Ecol Econ 70(2):434–444

Pradhan RP, Arvin MB, Norman NR, Bele SK (2014) Economic growth and the development of telecommunications infrastructure in the G-20 countries: a panel-VAR approach. Telecommun Policy 38(7):634–649

Richmond AK, Kaufmann RK (2006) Is there a turning point in the relationship between income and energy use and/or carbon emissions? Ecol Econ 56(2):176–189

Riti JS, Shu Y (2016) Renewable energy, energy efficiency, and eco-friendly environment (R-E5) in Nigeria. Energy Sustain Soc 6(1):1–16

Riti JS, Shu Y, Song D, Kamah M (2017a) The contribution of energy use and financial development by source in climate change mitigation process: a global empirical perspective. J Clean Prod 148:882–894

Riti JS, Deyong S, Shu Y, Kamah M (2017b) Decoupling CO2 emission and economic growth in China: is there consistency in estimation results in analyzing environmental Kuznets curve? J Clean Prod 166:1448–1461

Riti JS, Deyong S, Shu Y, Kamah M, Atabani AA (2018) Does renewable energy ensure environmental quality in favour of economic growth? Empirical evidence from China’s renewable development Quality and Quantity (International Journal of Methodology), https://doi.org/10.1007/s11135-017-0577-5

Saboori B, Sulaiman J (2013a) CO2 emissions, energy consumption and economic growth in Association of Southeast Asian Nations (ASEAN) countries: a cointegration approach. Energy 55:813–822

Saboori B, Sulaiman J (2013b) Environmental degradation, economic growth and energy consumption: evidence of the environmental Kuznets curve in Malaysia. Energy Policy 60:892–905

Sadorsky P (2014) The effect of urbanization on CO2 emissions in emerging economies. Energy Econ 41:147–153

Salim RA, Shafiei S (2014) Urbanization and renewable and non-renewable energy consumption in OECD countries: an empirical analysis. Econ Model 38:581–591

Shahbaz M, Lean HH (2012) Does financial development increase energy consumption? The role of industrialization and urbanization in Tunisia. Energy Policy 40:473–479

Shahbaz M, Loganathan N, Muzaffar AT, Ahmed K, Jabran MA (2016) How urbanization affects CO2 emissions in Malaysia? The application of STIRPAT model. Renew Sust Energ Rev 57:83–93

Sodri A, Garniwa I (2016) Attractnesia. Procedia Soc Behav Sci 227:728–737

Solarin SA (2014) Tourist arrivals and macroeconomic determinants of CO2 emissions in Malaysia. Anatolia 25(2):228–241

Solarin SA, Shahbaz M (2013) Trivariate causality between economic growth, urbanisation and electricity consumption in Angola: cointegration and causality analysis. Energy Policy 60:876–884

Soytas U, Sari R (2006) Can China contribute more to the fight against global warming? J Policy Model 28(8):837–846

Soytas U, Sari R (2009) Energy consumption, economic growth, and carbon emissions: challenges faced by an EU candidate member. Ecol Econ 68(6):1667–1675

Soytas U, Sari R, Ewing BT (2007) Energy consumption, income, and carbon emissions in the United States. Ecol Econ 62(3):482–489

Stock JH, Watson MW (2001) Vector autoregressions. J Econ Perspect 15(4):101–115

Sugiawan Y, Managi S (2016) The environmental Kuznets curve in Indonesia: exploring the potential of renewable energy. Energy Policy 98:187–198

Wang Z, Zhang B, Yin J (2012) Determinants of the increased CO2 emission and adaption strategy in Chinese energy-intensive industry. Nat Hazards 62(1):17–30

Wang Y, Zhang X, Kubota J, Zhu X, Lu G (2015) A semi-parametric panel data analysis on the urbanization-carbon emissions nexus for OECD countries. Renew Sust Energ Rev 48:704–709

Wang Y, Chen L, Kubota J (2016a) The relationship between urbanization, energy use and carbon emissions: evidence from a panel of Association of Southeast Asian Nations (ASEAN) countries. J Clean Prod 112:1368–1374

Wang Y, Li L, Kubota J, Han R, Zhu X, Lu G (2016b) Does urbanization lead to more carbon emission? Evidence from a panel of BRICS countries. Appl Energy 168:375–380

World Bank (2009) 2015. Data bank: China. http://data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=CN. Accessed 29 April, 2017

York R, Rosa E, Dietz T (2005) The ecological footprint intensity of national economies. J Ind Econ 2005(8):139–154

Zhang H (2016) Exploring the impact of environmental regulation on economic growth, energy use, and CO2 emissions nexus in China. Nat Hazards 84(1):213–231

Zhang YJ, Da YB (2013) Decomposing the changes of energy-related carbon emissions in China: evidence from the PDA approach. Nat Hazards 69(1):1109–1122

Zhang C, Lin Y (2012) Panel estimation for urbanization, energy consumption and CO2 emissions: a regional analysis in China. Energy Policy 49:488–498

Zhang YJ, Liu Z, Zhang H, Tan TD (2014) The impact of economic growth, industrial structure and urbanization on carbon emission intensity in China. Nat Hazards 73(2):579–595

Zhu J (2016) Making urbanisation compact and equal: integrating rural villages into urban communities in Kunshan, China. Urban Stud: p. 0042098016643455

Zhu HM, You WH, Zeng ZF (2012) Urbanization and CO2 emissions: a semi-parametric panel data analysis. Econ Lett 117(3):848–850

Zi C, Jie W, Hong-Bo C (2016) CO2 emissions and urbanization correlation in China based on threshold analysis. Ecol Indic 61:193–201

Zivot E, Andrews D (1992) Further evidence of great crash, the oil price shock and unit root hypothesis. J Bus Econ Stat 10:251–270

Acknowledgements

The authors of this paper acknowledged with thanks the contributions of anonymous reviewers of the manuscript for their valuable editorial comments which significantly improved the manuscript.

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Philippe Garrigues

Rights and permissions

About this article

Cite this article

Wang, T., Riti, J.S. & Shu, Y. Decoupling emissions of greenhouse gas, urbanization, energy and income: analysis from the economy of China. Environ Sci Pollut Res 25, 19845–19858 (2018). https://doi.org/10.1007/s11356-018-2088-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-018-2088-x