Abstract

This study introduces a new research topic that investigates the relationship between fiscal development and carbon emissions in Turkey through testing Environmental Kuznets Curve (EKC) hypothesis. Annual data covering the period, 1960–2013, has been used and in addition to gross domestic product and energy consumption, fiscal policy variables have been regressed on the level of carbon emissions in Turkey. Results reveal that fiscal policies and carbon emissions are in long-term equilibrium relationship in Turkey; carbon dioxide emission level converges towards long-term paths as contributed by fiscal policy. The effects of fiscal aggregates on the level of carbon dioxide emissions are negatively significant revealing that growth in fiscal aggregates leads to declines on the levels of carbon emissions. This proves that as far as environmental effects are concerned, fiscal policies regarding energy sector is successful in Turkey. Thus, the major finding of this study confirmed the validity of the fiscal policy-induced EKC hypothesis in the case of Turkey.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

Studies for environmental concerns have garnered considerable attention from researchers among which pollution has taken an important place. Environmental Kuznets curve (EKC) theory has been extensively studied in order to investigate environmental effects of various aggregates such as energy consumption. Although conventional EKC models have been used in environmental studies for many years, sectoral effects or roles have been also initiated in the last decade. According to a simple EKC setting, energy consumption is the main driver of climate change and, therefore, pollution (Ozcan and Ari 2017; Istaiteyeh 2016; Anatasia 2015; Kalayci and Koksal 2015; Kapusuzoglu 2014; Borhan and Ahmed 2012). As also pointed out by Anatasia (2015) and Kapusuzoglu (2014), real income is the main driver for energy consumption and energy usage drives emissions. The main question here is how successfully and friendly is energy consumption since traditional fuel oil and gas consumption still dominates global energy markets (Akdeniz and Arsel 2011; Al-Abdulhadi 2014; Anoruo and Elike 2009). As many studies point out, in case countries invest on alternative energy systems rather than investing on traditional energy systems such as fuel oil, then real income will be positively related to energy consumption which in turn will positively affect the level of emissions. Such effect would denote failure of successful energy policies of countries (Istaiteyeh 2016; Katircioglu 2014). On the other hand, some newer studies tested the effects of other economic aggregates such as financial sector and tourism (See Katircioglu and Katircioglu 2017; Katircioglu 2017; Cetin and Ecevit 2017; Jalil and Feridun 2011; Katircioglu 2014). For example, Katircioglu and Katircioglu (2017) find positive effects of urbanization on the level of emissions which deteriorates environment quality. On the other hand, however, Jalil and Feridun (2011) finds negative effects of financial sector development on the level of carbon emissions in the case of China proving successful energy policies in this large country. Gokmenoglu et al. (2016) find that energy sector impact also on the development of agricultural sector while Kalayci and Koksal (2015) show that air transportation significantly drives carbon emissions.

The role of particular segments or sectors of the economy in the conventional EKC still deserves further attention. While studying the role of financial sector in the EKC, researchers used financial aggregates such as money supply, which is one of the important tools of monetary policy. The argument of those finance-EKC nexus studies is that monetary policy is likely to affect not only economic growth (Kaushal and Pathak 2015) but also energy consumption and, therefore, indirectly influences climate changes as proxied by carbon dioxide emissions (CO2) (See Jalil and Feridun 2011). The other alternative macroeconomic policy is fiscal policy; therefore, a similar argument might be initiated for the role of fiscal policy in environmental concerns since it is the major determinant of economic growth and therefore energy consumption. To put it clearer, studying the role of fiscal policy and fiscal aggregates on the EKC would be also an interesting research area in the energy economics literature. Government spending and taxation are the two major tools of fiscal policy which are likely to play a role in not only in economic growth and even current account balances (Bolat et al. 2014) but also in energy policy and energy consumption and, therefore, in the EKC. As fiscal policy is a major determinant of income growth, energy consumption will be affected from interaction between fiscal policy and economic growth in the countries; therefore, not only additional energy demand but also additional environmental concerns will be raised in the economy. On the other hand, Balcilar et al. (2016) argue that reduction in fiscal deficits is likely to increase the rate of capital accumulation leading to a higher rate of economic growth. Thus, in such a scenario fiscal policy is expected to indirectly affect energy demand due to higher economic activity. Dongyan (2009) argues that fiscal and tax policies support energy efficiency in the countries while Liu et al. (2017) document that fiscal incentives play role in the reduction of carbon emissions. As also mentioned by Vera and Sauma (2015), some countries have directed their environmental policies towards carbon taxes in order to reduce greenhouse gas (GHG) emissions. As Fisher and Fox (2012) document, the level of taxation is closely related to the level of energy consumption and therefore the level of carbon emissions; thus, taxation plays major role not only in the economy but also in environmental concerns. Fisher and Fox (2012) also mention that climate policies of the economies need to be well balanced with aggregate fiscal policies of governments. There are many studies on the effects of general and/or carbon taxation whose conclusions are of mixed findings; however, generally it is found that taxation is effective for environmental policies (Vera and Sauma 2015).

Fisher and Fox (2012) also mentioned that public sector revenues play an important role in climate policy making. Ryan et al. (2009) find that taxes an impact on energy consumption and CO2 emissions. Goulder (2013) studies on the interactions between climate change policy and fiscal system. Wirl (1993) suggests that energy taxes are superior for governments compared to the other sectoral taxes due to the fact that energy products have low price elasticity and, therefore, provide higher tax revenues. Thus, the literature studies document that fiscal policy plays significant role in environmental concerns and energy sector. On the other hand, governments do also use environmental taxes in via a broader fiscal system in order to raise revenues for closing public debt (Rausch 2013). As mentioned by Rausch (2013), searching the economic effects of such strategy deserves attention from researchers.

Many studies have tested the validity of the environmental Kuznets curve (EKC) hypothesis, which investigates the relationship between environmental pollution and real income growth (Kapusuzoglu 2014; Coondoo and Dinda 2002; Dinda 2004; Grossman and Krueger 1991; Luzzati and Orsini 2009; Stern 2004). It would be reasonable to predict that macroeconomic policy including fiscal policy might exert effects on carbon emission level through energy sector and change in income level. Against this backdrop, this new article investigates the role of fiscal policy in the EKC of Turkey, which has a developing economy with a current gross domestic product of 208.76 billion USD (World Bank 2016). To the best of the authors’ knowledge, this study is the first of its kind as far as modeling approach is concerned. On the other hand, Halkos and Paizanos (2016) studied the effects of fiscal policy on CO2 emissions in the case of the USA by employing different econometric approach found that fiscal aggregates exerted significant effects on the level of CO2 emissions.

As also mentioned by Kaya and Yılar (2011a, b), Turkish economy has shown significant progress in stronger fiscal policies over the last two decades in addition to developments in financial sectors with lower risks (Erol et al. 2013). The adoption of fiscal rules as a new anchor in public finances is still at the agenda of Turkish authorities. Over the last decades, Turkish governments have been successful in adopting fiscal policies, which are mainly a result of strong fiscal adjustment process. Thus, fiscal policy is a major macroeconomic policy in Turkey over many years. After applying excessive deficit financing and experiencing recessions due to public deficits during 1990s, Turkey went through fiscal transformation by means of a comprehensive reform agenda and adopted a tightened fiscal policy in line with certain overall fiscal limits during 2000s (Kaya and Yılar 2011a, b).

On the other hand, tax rates as a part of fiscal policies might play a significant role in energy efficiency and environmental protection. Aytac (2011) suggests that high-energy taxation does not necessarily mean an indication of a priority being attributed to energy efficiency and environmental protection. With this respect, European Union (EU) hints on the introduction of an implicit tax rate on energy for the purpose of providing energy efficiency and reducing environmental pollution. Aytac (2011) concludes that implicit taxation significantly affects energy efficiency and environmental pollution in the EU countries while it does not in the case of Turkey.

Furthermore, empirical studies show that Turkey does not possess the EKC characteristic in the tourism sector. Although Katircioglu (2014) finds that income, energy consumption, and tourism growth contributes to changes in CO2 emissions significantly, the EKC is not inverted U-shaped one; thus, the EKC hypothesis via tourism growth could not be validated in Turkey. On the other hand, Katircioglu and Taspinar (2017) could not also validate the EKC in Turkey through controlling financial sector development although financial sector exerts significant direct and moderating effects on the EKC; they find that the EKC of Turkey is not again inverted U-shaped in the existence of financial sector. Then, an important research question is arised: “which sector(s) or economic factor(s) might lead to an inverted U-shaped EKC?”. This research question is not only new research impetus but also would be very interesting for such an interesting country context like Turkey which has a developing and dynamic economy.

The rest of the article is structured as follows. Section 2 describes the theoretical setting of the study; section 3 introduces the data and methodology; section 4 presents the empirical results and discussion, and section 5 concludes the study.

Theoretical setting

As advised in the literature, environmental pollution has been proxied by CO2 (carbon dioxide) emissions (kt). The present study raises a new research question if fiscal development might be a determinant of carbon emission level through exerting effects on real income and energy consumption levels. Real income is the main variable in the conventional EKC setting, therefore, another important determinant of CO2 emissions, as suggested in the literature as well, is energy consumption. The simple EKC theory implies that there exists an inverted U-shaped pattern between real income and emission level (see Stern 2004). This study revisits the conventional EKC model by adding fiscal policy variable as shown below:

where CO2 is carbon dioxide emissions (kt), E is energy consumption (kt of oil equivalent), y is real income, y 2 is the squared real income, and FP stands for fiscal policy proxy. β1, β2, β3, and β4 are the coefficients of regressors.

The proposed EKC model in Eq. (1) can be expressed in logarithmic form to capture the growth impacts in the economic long-term period:

where at period t, lnCO2 is the natural log of carbon dioxide emissions, lny is the natural log of real income, lny2 is the natural log of squared real income, lnE is the natural log of energy consumption, lnFP is the natural log of the fiscal policy variable, and ε is the error disturbance.

As also mentioned by Katircioglu (2010), the dependent variable in Eq. (2) might not immediately adjust to its long-term equilibrium level following a change in any of its explanatory factors (regressors). Therefore, the speed of adjustment between the short-term and the long-term levels of the dependent variable could be captured by estimating the following error correction model:

where Δ represents a change in the CO2, y, y 2, E, and FP variables and εt − 1 is the one period lagged error correction term (ECT), which is estimated from Eq. (2). The ECT in Eq. (3) shows how fastly the disequilibrium between the short-term and the long-term values of the dependent variable (CO2) is eliminated each period. The expected sign of ECT in the economerics theory is negative (Gujarati 2003).

Data and methodology

Data

Annual data covering the years between 1960 and 2013 has been used in this study; The variables of the study are carbon dioxide emissions (CO2) (kt), constant GDP in USD (2010 = 100) (y), squared constant GDP (2010 = 100) (y 2), energy use (E) (kt of oil equivalent), and overall government spending (G) as percent of GDP as a first proxy of FP and overall tax revenues as percent of GDP (T) and as a second proxy of FP. Two more proxies also have been used for fiscal policy: firstly, fiscal policy index (FI) has been constructed via principal components analysisFootnote 1 that made use of G and T variables given above. Secondly, following the work of Baltagi et al. (2008), interaction variable of Fiscal Policy (FPI) has been constructed by multiplying G and T together in logarithmic forms. FPI would be also a proxy of the overall FP. Data for CO2, y, and E have been gathered from the World Bank (2016) while data for G and T have been gathered from TURKSTAT (2016).

Methodology

This study revisits the conventional EKC model in the case of Turkey by imposing fiscal policy constraint. Thus, new approaches in time series analysis are adapted to the study in order to provide contemporary results on the model estimations. The process is explained below in summary:

The quasi-GLS unit root tests under multiple structural breaks

New unit root tests allow researchers to consider breaks in the series. Among them are Perron (1989), Zivot and Andrews (1992), Lumsdaine and Papell (1997), Perron (1997), and Ng and Perron (2001) that all allow one break in the tests while Lee and Strazicich (2003) allow till two breaks in the series during unit root tests. As also mentioned by Katircioglu (2014), unlike the other approaches, Carrion-i-Silvestre et al. (2009) provide the latest approach for unit root tests that allow structural breaks in the series till five. Thus, the quasi-GLS-based unit root tests as investigated by Carrion-i-Silvestre et al. (2009) will be employed in this study in order to estimate the stationary nature of series under inspection. When Fig. 1 of this study is evaluated, it is observed that specially fiscal series exhibit considerable break points over the periods; thus, it would be a right choice to adapt the quasi -GLS-based unit root tests that consider these breaks till five in this study.

Time series plot of series at the natural logarithm

Bound tests to level relationships and Maki’s (2012) cointegration test under multiple structural breaks

Cointegration among non-stationary series needs to be investigated by further tests. This study will employ two different tests in order to detect a possible cointegration in Eq. (1) previously mentioned. Firstly, the bounds test within the autoregressive distributed lag (ARDL) approach which was developed by Pesaran et al. (2001) has been adopted and could be applied regardless of the order of integration of the variables (whether regressors are purely I (0), purely I (1), or mutually co-integrated). The ARDL approach for estimating level relationships for the present study can be written as follows:

where ∆ is the difference operator and εt is the serially independent random error with mean zero and a finite covariance matrix.

In bounds tests, the F test is adapted to investigate a (single) long-term relationship in Eq. (4) (Katircioglu 2010). The null hypothesis of this test in the present study is H0: σ1 = σ2 = σ3 =σ4 =σ5 = 0 while the alternative hypothesis of a level relationship is H1: σ1 ≠ σ2 ≠ σ3 ≠ σ4 ≠ σ5 ≠ 0.

Secondly, a newer test that takes multiple break points in the series will be adopted in this study for a possible cointegration in Eq. (1). Westerlund and Edgerton (2006) suggest that cointegration tests for non-stationary series that do not consider the existence of structural breaks might provide biased results. Among newer approaches that allow breaks in the series are Gregory and ve Hansen (1996), Carrion-i-Silvestre and Sansó (2006), Westerlund and Edgerton (2006), and Hatemi-J (2008) which allow only a single break during cointegration tests. On the other hand, Maki (2012) proposed a new approach which internally considers structural breaks until five different points in time. Thus, this study will employ cointegration test proposed by Maki (2012) in order to investigate a possible long-term association in Eq. (1).

Conditional error correction models and granger causality tests

In the case of a long-term relationship in Eq. (1), the conditional error correction model (ECM) for short-term coefficients and speed of adjustment using the ARDL approach will be estimated via Eq. (3) in addition to level coefficients in Eq. (2) with different lag structures for regressors (see Pesaran et al. 2001). As Katircioglu (2010) also mentions, the short-term deviations of series from their long-term equilibrium paths can be captured by including an error correction term in Eq. (3).

Furthermore, conditional Granger causality tests under the ARDL mechanism will be carried out to investigate the direction of association among series under inspection via the following matrix mechanism:

In Eq. (5), ∆ stands for the difference operator. The ECTt − 1 denotes the lagged error correction term derived from Eq. (2). On the other hand, ε1,t, ε2,t, ε3,t, ε4,t, and ε5,t are serially independent random errors with mean zero and a finite covariance matrix. As a result of the ECMs for causality tests, obtaining statistically significant F statistic(s) for each pair of variables and statistically significant t statistic(s) for ECTt − 1 in Eq. (5) would meet the condition of having short-term and long-term causation(s), respectively (Katircioglu 2014).

In the final step, the variance decompositions regarding Eq. (1) will be estimated, which infers what percentage of the forecast error variance of the dependent variable can be explained by exogenous shocks to independent variables. Following variance decompositions, impulse response interactions will be estimated to see how the selected variable under consideration reacts to the exogenous shocks in the others.

Results and discussion

Table 1 presents the GLS-based unit root test results as modeled by Carrion-i-Silvestre et al. (2009) for the series of the study. The second generation unit root tests gave evidence of five successful and significant break points in the series as illustrated in Table 1. Results of the GLS-based unit root tests give strong evidence that all of series under inspection are integrated of order one, I (1); this means series are not stationary at levels but become stationary when differencing at first degrees. Thus, it is suggested that Eq. (1) of the present study might be a cointegration model (Katircioglu 2014).

All series in the present study are integrated of the same order; thus, bounds test for Eq. (1) under the ARDL approach would be suitable in this study. Results of bounds F and t tests are presented in Table 3:

Critical values for F and t statistics for smaller samples are also provided in Table 2 as tabulated from Narayan (2005). Bounds tests have been carried out under three scenarios as suggested by Pesaran et al. (2001: 295–296); they are (1) with restricted deterministic trends (F IV), (2) with unrestricted deterministic trends (F V) and (3) without deterministic trends (F III). It is important to mention that intercept terms in these models are all unrestricted.Footnote 2

Results in Table 3 provide strong evidence on the level relationship for Eq. (2) of this study. This is because the null hypothesis of H0: σ1 = σ2 = σ3 =σ4 =σ5 = 0 in Eq. (4) can be rejected according to the bounds test results in Table 3. Results suggest that CO2 emissions in Turkey are in a long-run relationship with its regressors including different proxies of FP. Furthermore, the results of the bounds t tests in Table 3 do also suggest for the imposition of the trend restrictions in the models since they are strongly and statistically significant (See Pesaran et al. 2001: 312).

Secondly, structural break points as observed in the series via Fig. 1 are now considered in cointegration tests by Maki (2012) to see if results from bounds tests would be confirmed. Results in Table 4 show that the null hypothesis of no cointegration can be again rejected through the existence of various structural break years in the models suggested by Maki (2012). Results from Maki (2012) also give a strong evidence that Eq. (1) is a cointegration model and estimating long-run parameters in Eq. (2) would be robust as a further step.

Both bounds test and Maki (2012) cointegration test results provided a very strong level relationship for Eq. (2) in the study; this allows for estimating the level coefficients via the ARDL approach as discussed in Pesaran and Shin (1999) and formulated in Eq. (2). Results of long-run coefficients in Eq. (2) for different proxies of FP are given in Table 5:

Firstly, it is observed that coefficients of GDP (without squaring) is highly elastic, statistically significant while that of squared GDP (GDP2) is negative and again significant in all of four models. This finding strongly confirms the suitability of coefficients according to setting of the inverted U-shaped EKC hypothesis in the case of Turkey. Energy consumption, on the other hand, exerts positively significant effects on the level of carbon emissions. Most importantly, the coefficients of four different proxies of fiscal policy is negative and statistically significant; this finding suggests that fiscal aggregates in Turkey exerts negatively significant effects on climate changes that signals for successful fiscal policies as far as environmental issues are concerned. Finally, the coefficients of intercept in Table 5 are negatively significant showing that without any change its determinants in Eq. (1) of this study, carbon emissions are likely to decline considerably.

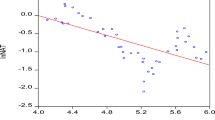

Before the ECM regressions, it will be good to provide the EKC figures in the case of Turkey induced by fiscal policy proxies. The EKC figures are useful by providing a very clear idea to readers if the economy of country under inspection would be fitting with conventional EKC. Therefore, Fig. 2 plots the EKC in four different EKC model options with this respect: (1) EKC induced by fiscal index; (2) EKC induced by government spending; (3) EKC induced by tax revenues; and (4) EKC induced by overall fiscal policy (with interaction variable). Although all panels show similar evidence on the shape of EKC, model estimations with fiscal index in panel (a) gave better EKC plot where estimated CO2 emission from the EKC model induced by fiscal index starts to move towards horizontal path and gets closer to its peak point as theoretized in the conventional EKC models. However, it is very clear from Fig. 2 that the inverted U-shaped EKC is not unfortunately available for Turkey through the channels of fiscal policy aggregates. This major finding is parallel to the findings of Katircioglu (2014) and Katircioglu and Taspinar (2017) again in the case of Turkey.

Plots of EKCs with fiscal policy

The ECM regressions as modeled in Eq. (3) are presented in Table 6. Firstly, all the ECT terms as shown in Eq. (3) are not so high but negatively significant as expected throughout four models. For example, the ECT term in the first model where fiscal index is the proxy of fiscal policy is − 0.406, statistically significant, and negative (β = − 0.406, p < 0.000). This implies that lnCO2 (carbon dioxide emission) converges towards its long-term equilibrium path by 40.6% speed of adjustment through the channels of energy consumption, real income, and fiscal policy aggregates. The other ECTs in the remaining three model options in Table 6 gave similiar evidence. This finding shows that fiscal policy in Turkey significantly contributes to the EKC to reach its long-term equilibrium path. On the other hand, the short-term coefficients in Table 6 again give strong evidence on behalf of the EKC of Turkey since the coefficients of the level of real income are positive while the coefficients of squared real income are negative.

In the next step, the direction of causality will be searched within the Granger causality tests through the ARDL error correction mechanism for the short-term and long-term periods. t statistics for long-term and F statistics for short-term causations are presented in Table 7 as estimated via Eq. (5).

Results in Table 7 provide strong evidence on long-term causality that runs from the EKC regressors including fiscal policy to CO2 emissions. Any change in these regressors would lead to changes in the level of CO2 emissions in the case of Turkey. This is because t statistics for the ECT term in all of four models are negatively significant. Results of -tests in Table 7 show that changes in fiscal policy aggregates in particular leads to changes in the level of CO2 emissions in the short-term periods. Granger causality test results in Table 7 suggest that CO2 emissions in Turkey are not only the EKC regressors-driven but also fiscal policy-driven.

Table 8 presents the variance decomposition results, which show that in the initial periods, low levels of the forecast error variance of CO2 emissions are explained by exogenous shocks to energy consumption, output, and fiscal policy variables. These ratios start to increase in the later periods. For example, the forecast error variance of CO2 emissions due to a shock to the interaction variable of fiscal policy is slightly the highest compared to the other fiscal policy proxies, which is 12.775% in period 10. This shows that, for example, 12.775% of the forecast variance of CO2 emissions can be explained by a shock (upwards/downwards) in fiscal policy aggregates. On the other hand, it is also observed that the forecast error variance of CO2 emissions due to a shock to energy consumption is the highest compared to all the other regressors, which is 13.506% in period 10.

Finally, Fig. 3 plots impulse responses among CO2 emissions, energy consumption, output, and fiscal policy proxies. As observed from the figures, the response of CO2 emissions to a shock in fiscal developments in Turkey is insignificantly negative as far as government spending and tax revenues are concerned; however, this response becomes significantly positive when overall fiscal index and interaction variable are concerned. It is worth noting that the response of CO2 emissions to GDP and squared GDP are respectively positive and negative in parallel to the EKC setting.

Impulse responses in the revised EKC model

Conclusion

This new research paper empirically investigated the fiscal policy-induced EKC hypothesis in the case of Turkey. Annual data covering the period 1960–2013 have been selected and constructed for this purpose. The long-term equilibrium relationship and the direction of causality between fiscal development and carbon dioxide emissions through the channels of energy consumption and real income growth have also been studied in this research paper. The theoretical EKC framework has been taken into consideration in empirical analysis in order to investigate these relationships. The results of the present study are of interest to both scholars and policy makers due to the reason that fiscal policies are one of two major macroeconomic policy tools and their role in the sectors is important; therefore, this study contributed for the first time to the relevant literature by augmenting fiscal policy aggregates into the theoretical EKC setting in order to investigate if fiscal developments in Turkey exert significant effects on the level of carbon dioxide emissions.

Results of the present study confirm the validity of fiscal policy-induced EKC hypothesis and reveal that a long-term equilibrium relationship exists between fiscal development and carbon emission level in Turkey through the channels of energy consumption and real income growths. The level of carbon dioxide emissions in Turkey significantly converge to long-term equilibrium paths as contributed by fiscal developments. The long-run effects of fiscal policy on climate changes in Turkey are negative proving that fiscal policies are effectively adopted in reducing pollution levels. At the further levels of income and energy consumption as stimulated by fiscal policy, CO2 emissions in Turkey tend to decline over time. It can be argued in this study that fiscal policies in Turkey are environmentally successful. Results of this study sufficiently reveal that environmental conservation policies are well balanced with fiscal policies in Turkey. However, it is clearly found that fiscal policy does not impact on the levels of CO2 emissions at very high levels to reach inverted U-shaped EKC. This major finding provided similar evidence as compared with the results of Jalil and Feridun (2011) for China, and Katircioglu (2014), and Katircioglu and Taspinar (2017) for the case of Turkey.

Granger causality tests suggest long-term causality that runs from fiscal aggregates, GDP, and energy consumption to CO2 emissions in Turkey; furthermore, there also exist causality that runs from fiscal aggregates to CO2 emissions and GDP in the short-term periods. On the other hand, the response of CO2 emissions to given shocks in fiscal policy in Turkey is negative but insignificant as far as government spending and tax revenues are concerned; however, the response becomes positive and significant when overall fiscal index and interaction variable are concerned. It is also found that the response of CO2 emissions to shocks in GDP and squared GDP are respectively positive and negative through the EKC setting.

Although this study finds negative effects of fiscal developments on the levels of carbon emissions in Turkey, still there arise important messages for policy makers; that is, fiscal aggregates in Turkey exerts significant but low effects on carbon emissions through real income and energy consumption. Thinking that the Turkish authorities extensively adapt fiscal policies to manage the economy, such policies related with energy sector might be improved at further levels such as tax regulation for the energy sector, further government investment and participation in alternative energy systems other than fuel oil, and encouragement of private sectors (through tax and incentive programs) towards investing on alternative energies and even foreign direct investments (FDI) due to the fact that FDI might drive real income (Gungor et al. 2014; Gungor and Katircioglu 2010) and energy sectors. Such improvements in fiscal policies towards public and private sectors will lead to better effect in the energy sector and achieving downward sloping of the EKC as presented in Fig. 2 of this study would be possible.

Since this study has introduced a new and important research area in the energy economics literature as mentioned before; further researches (i.e., for the other countries or regions) will be needed for comparison purposes. Furthermore, different methodological approaches not only via time series data but also panel data can be also adapted as further researches in order to investigate the role of fiscal policy in environmental concerns of countries again for comparison purposes.

References

Akdeniz HA, Arsel I (2011) The economic analysis of supplying necessary electricity for watering fruit garden with photovoltaic cells system established in Izmir. Int J Econ Perspect 5(1):17–27

Al-Abdulhadi DJ (2014) An analysis of demand for oil products in Middle East countries. International. J Econ Perspect 8(4):5–12

Anatasia V (2015) The causal relationship between GDP, exports, energy consumption, and CO2 in Thailand and Malaysia. Int J Econ Perspect 9(4):37–48

Anoruo E, Elike U (2009) An empirical investigation into the impact of high oil prices on economic growth of oil-importing African countries. Int J Econ Perspect 3(2):121–129

Aytac D (2011) Türkiye’de Enerji Etkinliğini Sağlama ve Çevresel Kirlenmeyi Engellemede Enerji Üzerindeki Zımni Vergi Oranlarının Etkisi. Maliye Dergisi 160:392–410

Balcilar M, Ciftcioglu S, Gungor H (2016) The effects of financial development on Investment in Turkey. Singapore Econ Rev 61(4):1650002. https://doi.org/10.1142/S0217590816500028

Baltagi BH, Demetriades PO, Law SH (2008) Financial development and openness: evidence from panel data. Center for Policy Research Paper 60

Bolat S, Emirmahmutoglu F, Belke M (2014) The dynamic linkages of budget deficits and current account deficits nexus in EU countries: bootstrap panel granger causality test. Int J Econ Perspect 8(2):16–26

Borhan HB, Ahmed EM (2012) Simultaneous model of pollution and income in Malaysia. Int J Econ Perspect 6(1):50–73

Carrion-i-Silvestre JL, Sansó A (2006) Testing the null of cointegration with structural breaks. Oxf Bull Econ Stat 68(5):623–646. https://doi.org/10.1111/j.1468-0084.2006.00180.x

Carrion-i-Silvestre JL, Kim D, Perron P (2009) GLS-based unit root tests with multiple structural breaks under both the null and the alternative hypotheses. Economet Theor 25(6):1754–1792. https://doi.org/10.1017/S0266466609990326

Cetin M, Ecevit E (2017) The impact of financial development on carbon emissions under the structural breaks: empirical evidence from Turkish economy. Int J Econ Perspect 11(1):64–78

Chen M-H (2010) The economy, tourism growth and corporate performance in the Taiwanese hotel industry. Tour Manag 31(5):665–675. https://doi.org/10.1016/j.tourman.2009.07.011

Coondoo D, Dinda S (2002) Causality between income and emission: a country group specific econometric analysis. Ecol Econ 40(3):351–367. https://doi.org/10.1016/S0921-8009(01)00280-4

Dinda S (2004) Environmental Kuznets curve hypothesis: a survey. Ecol Econ 49(4):431–455. https://doi.org/10.1016/j.ecolecon.2004.02.011

Dongyan L (2009) Fiscal and tax policy support for energy efficiency retrofit for existing residential buildings in China’s northern heating region. Energy Policy 37(6):2113–2118. https://doi.org/10.1016/j.enpol.2008.11.036

Erol C, Seven U, Aydogan B, Tunc S (2013) The impact of financial restructuring after 2001 Turkey crisis on the risk determinants of Turkish commercial Bank stocks. Int J Econ Perspect 7(4):94–103

Fisher C, Fox A (2012) Climate policy and fiscal constraints: do tax interactions outweigh carbon leakage? Enery Econ 34:218–227

Gokmenoglu KK, Bekun FV, Taspinar N (2016) Impact of oil dependency on agricultural development in Nigeria. Int J Econ Perspect 10(2):151–163

Goulder LH (2013) Climate change policy's interactions with the tax system. Energy Econ 40(1):3–11

Gregory AW, ve Hansen BE (1996) Residual-based tests for cointegration in models with regime shifts. J Econ 70(1):99–126. https://doi.org/10.1016/0304-4076(69)41685-7

Grossman GM, Krueger AB (1991) Environmental impacts of a north American free trade agreement. NBER working papers. 3914, National Bureau of economic research, Inc

Gujarati DN (2003) Basic econometrics, 4th edn. Mc Graw-Hill International, New York

Gungor H, Katircioglu S (2010) Financial development, FDI and real income growth in Turkey: an empirical investigation from the bounds tests and causality analysis. Actual Problems Econ 11(114):215–225

Gungor H, Katircioglu ST, Mercan M (2014) Revisiting the nexus between financial development, FDI, and growth: new evidence from second generation econometric procedures in the Turkish context. Acta Oeconomica 64(1):73–89. https://doi.org/10.1556/AOecon.64.2014.1.4

Halkos GE, Paizanos EA (2016) The effects of fiscal policy on CO2 emissions: evidence from the U.S.A. Energy Policy 88:317–328. https://doi.org/10.1016/j.enpol.2015.10.035

Hatemi-J A (2008) Tests for cointegration with two unknown regime shifts with an application to financial market integration. Empir Econ 35(3):497–505. https://doi.org/10.1007/s00181-007-0175-9

Istaiteyeh RMS (2016) Causality analysis between electricity consumption and real GDP: evidence from Jordan. Int J Econ Perspect 10(4):526–540

Jalil A, Feridun M (2011) The impact of growth, energy and financial development on the environment in China: a cointegration analysis. Energy Econ 33(2):284–291. https://doi.org/10.1016/j.eneco.2010.10.003

Kalayci S, Koksal C (2015) The relationship between China’s airway freight in terms of carbon-dioxide emission and export volume. Int J Econ Perspect 9(4):60–68

Kapusuzoglu A (2014) Causality relationships between carbon dioxide emissions and economic growth: results from a multi-country study. Int J Econ Perspect 8(2):5–15

Katircioglu ST (2010) International tourism, higher education, and economic growth: the case of North Cyprus. World Econ 33(12):1955–1972. https://doi.org/10.1111/j.1467-9701.2010.01304.x

Katircioglu ST (2014) International tourism, Energy Consumption, and Environmental Pollution: The Case of Turkey. Renew Sustain Energy Rev 36:180–187

Katircioglu S (2017) Investigating the role of oil prices in the conventional EKC model: evidence from Turkey. Asian Econ Financ Rev 7(5):498–508. https://doi.org/10.18488/journal.aefr/2017.7.5/102.5.498.508

Katircioglu S, Katircioglu ST (2017) Testing the role of urban development in the conventional environmental Kuznets curve: evidence from Turkey. Appl Econ Lett. https://doi.org/10.1080/13504851.2017.1361004

Katircioglu ST, Taspinar N (2017) Testing the moderating role of financial development in an environmental Kuznets curve: empirical evidence from Turkey. Renew Sustain Energy Rev 68(1):572–586. https://doi.org/10.1016/j.rser.2016.09.127

Kaushal LA, Pathak N (2015) The causal relationship among economic growth, financial development and trade openess in Indian economy. Int J Econ Perspect 9(2):5–22

Kaya F, Yılar S (2011a) Fiscal transformation in Turkey over the last two decades. OECD J Budg (1):59–74

Kaya F, Yılar S (2011b) Fiscal transformation in Turkey over the last two decades. OECD J Budg (1):62

Lee J, Strazicich M (2003) Minimum lagrange multiplier unit root test with two structural breaks. Rev Econ Stat 85(4):1082–1089

Liu Y, Han L, Yin Z, Luo K (2017) A competitive carbon emissions scheme with hybrid fiscal incentives: the evidence from a taxi industry. Energy Policy 102:414–422. https://doi.org/10.1016/j.enpol.2016.12.038

Lumsdaine RL, Papell DH (1997) Multiple trend breaks and the unit root hypothesis. Rev Econ Stat 79(2):212–218. https://doi.org/10.1162/003465397556791

Luzzati T, Orsini M (2009) Natural environment and economic growth: looking for the energy-EKC. Energy 34(3):291–300. https://doi.org/10.1016/j.energy.2008.07.006

Maki D (2012) Tests for cointegration allowing for an unknown number of breaks. Econ Model 29(5):2011–2015. https://doi.org/10.1016/j.econmod.2012.04.022

Narayan PK (2005) The saving and investment nexus for China: evidence from cointegration tests. Appl Econ 37(17):1979–1990

Ng S, Perron P (2001) Lag length selection and the construction of unit root tests with good size and power. Econometrica 69(6):1519–1554. https://doi.org/10.1111/1468-0262.00256

Ozcan B, Ari A (2017) Nuclear energy-economic growth nexus in OECD countries: a panel data analysis. Int J Econ Perspect 11(1):138–154

Perron P (1989) Testing for a unit root in a time series with a changing mean, Working papers 347. Princeton, Department of Economics-Econometric Research Program

Perron P (1997) Further evidence on breaking trend functions in macroeconomic variables. J Econ 80(2):355–385. https://doi.org/10.1016/S0304-4076(97)00049-3

Pesaran MH, Shin Y (1999) An autoregressive distributed lag modelling approach to cointegration analysis. In: Strom S (ed) Econometrics and economic theory in the 20th century: the Ragnar Frisch centennial symposium. Cambridge University Press, Cambridge. https://doi.org/10.1017/CCOL521633230.011

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econ 16(3):289–326. https://doi.org/10.1002/jae.616

Rausch S (2013) Fiscal consolidation and climate policy: an overlapping generations perspective. Energy Econ 40:S134–S148. https://doi.org/10.1016/j.eneco.2013.09.009

Ryan L, Ferreira S, Convery F (2009) The impact of fiscal and other measures on new passenger car sales and CO2 emissions intensity: evidence from Europe. Energy Econ 31(3):365–374. https://doi.org/10.1016/j.eneco.2008.11.011

Stern DI (2004) The rise and fall of the environmental Kuznets curve. World Dev 32(8):1419–1439. https://doi.org/10.1016/j.worlddev.2004.03.004

TURKSTAT (2016) Statistical indicators. Retrieved July 16, 2013 from the TURKSTAT website: http://www.turkstat.gov.tr/Start.do;jsessionid=LMv8SHyTQlD7550d7gM3vN8K74d5z0KCzlf3m7rYKG5cP1f5XQ23!-1846445386

Vera S, Sauma E (2015) Does a carbon tax make sense in countries with still a high potential for energy efficiency? Comparison between the reducing-emissions effects of carbon tax and energy efficiency measures in the Chilean case. Energy 88:478–488

Westerlund J, Edgerton D (2006) New improved tests for cointegration with structural breaks. J Time Ser Anal 28(2):188–224

Wirl F (1993) Energy pricing when externalities are taxed. Resour Energy Econ 15(3):255–270. https://doi.org/10.1016/0928-7655(93)90008-I

World Bank (2016) World development indicators. Retrieved from: http://www.worldbank.org

Zivot E, Andrews DWK (1992) Further evidence on the great crash, the oil price shock and the unit root hypothesis. J Bus Econ Stat 10:251–270

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Philippe Garrigues

Rights and permissions

About this article

Cite this article

Katircioglu, S., Katircioglu, S. Testing the role of fiscal policy in the environmental degradation: the case of Turkey. Environ Sci Pollut Res 25, 5616–5630 (2018). https://doi.org/10.1007/s11356-017-0906-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-017-0906-1