Abstract

This paper uses a novel dataset of capital expenditures on housing, to study how foreclosures affect capital expenditure investments in residential properties. Empirical analysis discovers that foreclosures negatively affect capital expenditure investment through the following channels: (1) individual homeowners reduce their capital expenditures when home prices fall and the likelihood of foreclosure increases; (2) lenders pursue a strategy of low investment in real estate owned (REO) inventories; (3) the reductions in capital expenditures generate a negative externality by creating a disincentive for other homeowners to spend on home improvements; and (4) a cluster of foreclosures further worsens the reduced investment situation. Purchasers of REO properties spend more on capital expenditures than those of non-REO properties in 1 year after sales.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The decline in housing prices since 2006 has resulted in an unprecedented number of defaults and foreclosures. Central to concerns about the effect of the huge wave of foreclosures has been the fear of their negative impact on neighborhood properties and on the wider community. A number of papers have presented evidence that foreclosures seem to have a large and negative impact on the market value of neighboring properties (Immergluck and Smith 2006a; Campbell et al. 2011; Harding et al. 2009; Gerardi et al. 2015). This paper provides a new perspective by studying how foreclosures affect housing capital expenditures. It also provides evidence on how neighborhood capital expenditures affect individual homeowner’s capital expenditures.

There is a widespread recognition of the interaction between bankruptcy and reduced investment in finance theory. The notion of corporate debt overhang emphasizes that high leverage can cause firms to underinvest (Myers 1977),Footnote 1 since the benefits of new capital investments accrue largely to debt holders rather than equity holders. This paper applies the same thinking to study the role of foreclosures in determining housing capital expenditures. Data problems have complicated previous attempts to empirically identify this interaction. Typically, information on housing capital expenditures over time is unavailable. This study overcomes this data hurdle with a sample of building permit records for residential properties sold over time. Capital improvement projects on housing have both an investment-driven demand and a consumption-driven demand. By restricting the analysis to homes that were sold, this study focuses on the investment motivation. The consumption motivation is reduced due to the data limitation on factors more traditionally related to consumption (income, wealth, age of owner, family size etc.). Census block group (CBG) fixed effect, Zip code owner to tenant ratio (OT), and Zip code price trends are included to control for neighborhood effects. The CBG fixed effect helps in this regard to the extent that the demographics related to consumption motivation tend to cluster in a CBG. The new information allows me to test how foreclosures affect housing capital improvements and to link to neighborhood values.

The results show that capital expenditures are lower for real estate owned (REO) properties than those for non-foreclosed properties during 3 years before foreclosures and REO sales. Since the defaulting owner and the foreclosing lender either has control over the property during this period, there is a joint two-part explanation: defaulting homeowners reduce their investment before default or foreclosing lenders have less incentive to invest in their REO inventories. In order for the capital expenditures to be lower over the full period, the defaulting lender must adopt a marketing strategy of not significantly improving the property. The first factor could be attributed to default risk and limited liability in case of default (Harding et al. 2000), because the investment is an outlay that an owner is unlikely to recover in the event of default. Liquidity problem such as loss of income or a significant increase in other expenses (e.g., medical) could also prevent distressed owners from making capital improvement in their homes. And as for the second factor, after a property’s title is transferred to a foreclosing lender, it is costly to make capital improvement because such properties are usually at high risk because of vacancy or abandonment.

An individual property’s capital expenditure is shown to be positively related to its neighborhood counterpart. A cluster of new construction could contribute to this relation, because neighboring properties of similar ages require structural replacement at about the same time. Another possible explanation is imitative investment behavior among homeowners. On the positive side, homeowners who observe investment by their neighbors may be motivated to make their own capital investments in their homes. Conversely, if neighborhood investment declines, the investment incentive for homeowners declines. In combination, these two findings suggest the following mechanism by which foreclosures in a neighborhood can contribute to lower neighborhood housing values. It begins with increased foreclosures that lead to lower neighborhood capital expenditures because of reduced capital improvement in REO properties. These reduced investments then generate an externality by creating a disincentive for other homeowners to spend on home improvements. In other words, lower neighborhood capital expenditures discourage neighbors from investing. This finding suggests a self-reinforcing low investment behavior in declining neighborhoods.

The next section includes a literature review on this topic and hypotheses development. Data section describes the process of data collection and methods of constructing variables. Methodology and Results section presents the design of empirical testing, main empirical findings, and interpretations. Conclusions section contains my concluding remarks.

Literature Review and Hypothesis Development

The recent literature contains evidence that foreclosures negatively affect the market value of neighboring properties.Footnote 2 Immergluck and Smith (2006a) regressed sale price data in 1999 for single-family properties in Chicago to the number of foreclosures in the two preceding years at distances of one-eighth mile and one-quarter mile. They find that, on average, a foreclosure within one-eighth mile of a single-family house was associated with a 0.9 to 1.1 % price decline. The lower percentage occurs when the median price of houses in the census tract is controlled. Campbell et al. (2011) studied 20 years of single-family property sales in Massachusetts, measuring property and neighborhood characteristics only for 2007. They used two “differences-in-differences” approaches to net out effect and reverse causality from house prices to foreclosures and showed that a foreclosure within 0.05 miles of a house lowered the neighboring property price by 1 %, compared with the 7–9 % derived through Ordinary Least Squares estimation.

Harding et al. (2009) used a repeat sale approach and simultaneously estimated the local price trends and the incremental price impact of nearby foreclosures. The authors showed that the contagion discount diminishes with distance and grows from the onset of distress through sales of the foreclosure and then stabilizes; this is consistent with the contagion effect as the visual externality associated with deferred maintenance and neglect. Gerardi et al. (2015) found that properties in virtually all stages of distress have significantly negative effects on nearby home values. The authors also document that the estimates are very sensitive to the condition of the distressed property, with a positive correlation existing between house price growth and foreclosed properties identified as being in “above average” condition. They argue that the externality results from reduced investment by owners of distressed properties. Their measurements of property condition and quality, however, fail to capture any potential change in condition and quality at various stages of distress that may stem from reduced investment.

The literature is in agreement on the correlation between bankruptcy and reduced corporate investment in firms (Myers 1977; Krugman 1988 and Sachs 1990). This paper applies the same thinking to study the role of foreclosures in determining housing capital improvement. Empirical evidences have documented an externality of housing capital improvement on values of neighboring properties. Pavlov and Blazenko (2005) suggested that an individual’s capital expenditure habits have a positive externality that exceeds the impact on his or her building alone because of their effect on a neighbor’s building. Rossi-Hansberg et al. (2010) looked at data on public neighborhood improvement spending and estimated that, over 6 years, a dollar spent on home improvement in the neighborhoods of interest generated between $2 and $6 in land value by way of externalities. This externality decreases by half approximately every 1000 ft. This paper utilizes a more micro data set of individual capital expenditure projects at property level to establish the investment externality among neighbors directly.

This study contributes to the current foreclosure literature by providing empirical evidence on the reduced investment associated with foreclosures. It also contributes to neighborhood study showing that an individual homeowner’s capital expenditure is positively related to its neighborhood counterpart, a form of investment externality. The two findings jointly suggest a self-reinforcing low investment behavior in declining neighborhoods, which links foreclosures to neighborhood values. The following paragraphs develop hypotheses of housing capital expenditures based on existing theories and empirical evidence.

-

H1: Foreclosure and the expectation of foreclosure have a significant negative impact on capital expenditure.

An owner who expects foreclosure has less (actually no) incentive to invest. This is because expenditure is an outlay he or she is unlikely to recover in foreclosure in case of limited liability (Harding et al. 2000). Distressed owners may also lack the financial resources to improve their properties. A lender that obtains title to a property through foreclosure may adopt a strategy of not investing in it or of quickly removing the ghost asset off his or her balance sheet to minimize the high holding cost of REO inventories, based on an assessment of the best marketing strategy for the REO. Given the incentives for defaulting owners and foreclosing lenders to reduce investment, we would expect foreclosure and the expectation of foreclosure to have a significant negative impact on capital expenditure investment.

-

H2: An individual homeowner’s capital expenditure is positively related to its neighborhood counterpart.

Capital expenditures in properties have both private and community benefits in that they enhance not only the value of the maintained property, but also the value of nearby buildings (Pavlov and Blazenko 2005; Rossi-Hansberg et al. 2010). Homeowners will adjust their capital expenditures according to what they observe their neighbors doing. If neighbors invest in the upkeep of their property, others will follow. Conversely, surrounded by numerous foreclosures that reflect reductions in investment, an individual will invest less in his property as the neighborhood becomes less desirable. This imitative investment behavior implies that an individual, in assessing alternative behavioral choices, will find a given behavior relatively more desirable if others have previously behaved or are currently behaving in the same way. To finish modeling residential neighborhoods, it is necessary to describe how beliefs about the behavior of others are determined. The benchmark assumption in the literature is that beliefs are rational (Durlauf 2003). The role of endogenous neighborhood effects is then reduced to the expected value of the average choices of others. This assumption reduces the possible endogenous effects to a single moment in the distribution of behaviors. The equation is often referred to as the linear-in-mean model and operates on the basic assumption that all endogenous effects work through expectations.

A cluster of new construction may also contribute to a positive relation between individual and neighborhood capital expenditures. Properties built in the same neighborhood age at a similar rate and are likely to suffer from common problems at about the same time. This would result in a positive relation among the investment schedules. For example, in the neighborhood of Zip code 53222, almost 90 % of 1300 homes in the sample were built 40–55 years ago. Because the average life of structures and appliances is similar, improvements in the neighborhood are expected to occur as a cluster at some point. For example, the permit-requiring projects may take place at the similar time for similar aged properties, such as repairs or replacement of any electrical system, any plumbing system and any mechanical system, including alterations, repairs, replacement, equipment, appliances, fixtures, fittings.

-

H3: Homeowner’s capital expenditure investment is negatively related to the number of neighboring foreclosures.

Foreclosures may hurt neighborhoods as much as they hurt the individuals who lose their homes. For instance, foreclosed properties typically suffer from certain damage and stay empty for a time, which reduces the visual appeal of the neighborhood and encourages crime (Immergluck and Smith 2006b). When the number of neighboring foreclosures increases, the remaining homeowners have less incentive to invest in their properties as the neighborhood becomes less appealing to potential buyers.

-

H4: Buyers of REO properties invest more on capital expenditures than buyers of non-REO properties.

As discussed previously, the capital improvement for an REO property is likely to be lower than that of a regular sale before a sale. Thus, purchasers of REO properties may invest more on capital improvement than those of regular sales after their purchases, to catch up to regular sales on property quality.

Data

Sample Construction

The sample includes single-family house transactions in the City of Milwaukee from January 2005 to December 2009. The transaction data was provided by the Wisconsin Multiple Listing Service (MLS),Footnote 3 including listing price, sale price, location, and various dimensional attributes (e.g., lot size, number of rooms, etc.).

A novel dataset of capital expenditures between 1999 and 2011 was collected from the tax assessor’s office in Milwaukee. The dataset tracks capital expenditures on each property, such as expenditure types, amounts,Footnote 4 and records the dates. A longer sample period of permit data aims to generate different measures of capital expenditure invested in a property before and after sale. The data covers capital improvements that required building permits from the tax assessor’s office but excludes routine maintenance. The permit data could be a proxy for the improvements from capital expenditure and link to neighborhood values. Table 1 lists the building and construction activities in Milwaukee that require permits, but other jurisdictions may have different requirements. Most of the permit data used in this paper falls into the four categories of electronic, plumbing, construction (boiler), and construction (construction). The permit-requiring investment activities in Table 1 are also relevant to the underlying issue of neighborhood values. For example, attic alternation or conversion, drive way and public way projects, fence, garage replacement, and new roof construction all affect the value of the property itself and the desirability of the neighborhood. Activities outside these categories, such as projects associated with electronics and plumbing are more closely related to the normal functioning of a house and are more closely aligned with daily maintenance. It is not uncommon for a typical house to undergo a project that requires a permit (Fig. 1). Figure 2 shows that around 80 % of the houses sold in the 2005–2009 period underwent a permit-requiring project in the 3 years before their sales. It is true that this permit data does not include data on daily maintenance and all investment activities. However, it does serve its purpose as a good proxy for overall capital improvement spending and as a link to neighborhood values.

Distributions of permit records. This table provides a histogram of the distribution of permit records at different value ranges and the type of activities. The top figure shows the distribution of permit records at different value ranges. The x axis is the value range of dollar amounts in a permit record. The y-axis is the number of records reporting in the corresponding value range. The bottom figure shows the distribution of permit records reporting different activities. The axis is the type of activity. The y-axis is the number of records reporting each activity

Distribution of capex. This table shows a histogram of the distribution of capex, which is the sum of capital expenditures invested in the 3 years before a property’s sale date. The 3-year time window is defined as 3 years between the permit record date and the property’s sale date. The x-axis is the dollar amount of the capex. The y-axis is the number of units falling in a value range

Equation (1) defines the calculation of capital expenditure flow for a property in a certain time window with permit data. For a property \( \mathrm{p} \) sold at time \( \mathrm{t} \), the total capital expenditure back to date \( \mathrm{j} \) in terms of dollar value at \( \mathrm{t}\kern0.28em {\mathrm{Capex}}_{\mathrm{p},\mathrm{t}}^{\mathrm{j}} \) is calculated with the following equation:

where \( i \) is the recorded permit completion date, \( t \) is the transaction date, \( j \) denotes a past date at which the capital expenditure became of interest, and 2.5 % is the depreciation rate.Footnote 5 The left side variable is the depreciated stock of past capital expenditures. The right side is the sum of investment flow (\( {\mathrm{FCapex}}_{\mathrm{p},\mathrm{t}}^{\mathrm{i}} \)) during the time window in which depreciation is treated as an expense for every incremental investment. Figure 2 shows that around 5 % of the properties involve capital expenditures in excess of $5000 with this measurement.

The neighborhood capital expenditure is normalized over all properties in each Zip code. For each Zip code, I calculated the number of all sold properties and randomly drew a similar number of unsold properties. Average capital expenditures were calculated for all properties in a pool including both sold and unsold properties. The motivation to include this neighborhood variable is to study the relationship between individual homeowner’s capital expenditure investment and the neighborhood counterpart. The result provides a new evidence of investment externality in the form of a direct link between capital expenditure investments among neighbors. It contributes to existing literature (Pavlov and Blazenko 2005; Rossi-Hansberg et al. 2010), which documented that individual capital expenditure improvement generates externality through influencing market value of neighboring properties.

A REO sale is identified by a record of a sheriff’s deed,Footnote 6 provided by the Milwaukee tax assessor’s office. It is a deed issued to the buyer of a property that was sold under a court order to pay off a debt. Until such a sale occurs, the office of the register of deeds has no knowledge of the default. A property owner normally has a 6-month redemption period from the date of the foreclosure sale to redeem, or buy back, his or her property in the city of Milwaukee. This can be done through the bank that foreclosed on the mortgage or through the register of deeds office. The owner must pay the loan balance due on the mortgage, which includes all accrued interest, late fees, attorney fees and other costs incurred by the lender, in cash or certified funds.

The foreclosure timeline in Wisconsin is as follows. It takes 9 months between the time the lender gets a property through a foreclosure sale and the time the property is listed as a REO sale, including the 6 months redemption period and another 2 to 3 months for the lender to prepare a listing. It takes about 6 months from the time a lender sends a default notice until conclusion of a sheriff’s sale. This period includes filing for foreclosure, responses from an owner, court hearings, etc. Normally, an owner must miss three monthly payments to trigger issuance of a default notice. The date of sheriff’s sale falls at the end of the foreclosure arrow.

Knowledge of specific property addresses enabled me to use a geographic information system (GIS) to measure the distance between any two properties in the sample. Information on the sale date of a subject property and the REO sale date of a nearby foreclosure enabled me to identify the time window between the REO sale of a nearby foreclosed property and the sale of a subject property. The number of nearby REOs is counted in three different time windows and five distance radii, as shown in Fig. 3.Footnote 7

Count of nearby foreclosures. This graph describes the approach toward counting the number of nearby foreclosures in the two dimensions of time windows and distance radii. There are three different time windows for counting the number of neighboring foreclosures based on the time gap between a previous REO sale date and the sale date of a subject property: (1) less than 1 month; (2) 1 to 6 months; (3) 6 months to 1 year. Five concentric rings with different distance radii around a subject property at each time window as discussed above are defined as following: (1) 0 to 300 ft; (2) 300 to 500 ft; (3) 500 to 1000 ft; (4) 1000 to 2000 ft; and (5) 2000 to 3000 ft

The Grade and Condition, Desirability, and Utility (CDU) are property condition variables provided by the Milwaukee tax assessor’s office.Footnote 8 Grade describes the overall construction quality of a property; CDU represents its attributes as the name implies and, takes into consideration its age and type. Both are updated when properties are revaluated by the assessor’s office. The evaluation can be done annually or periodically as deemed necessary. Because the dates these condition variables were recorded are unavailable, I used these variables as broad indicators of quality. Figure 4 provides a histogram of the distribution of both variables for the full sample, foreclosure subsample, and non-foreclosure subsample. It shows that the properties are concentrated in the category of average quality, with few observations of quality at either extreme. The foreclosure sample has a higher proportion of low quality properties than the non-foreclosure sample in terms of both Grade and CDU.

CDU & grade distribution. This table provides a histogram of the distribution of CDU and Grade as furnished by the tax assessor’s office for the City of Milwaukee. The top figure reports the percentage distribution of the variable CDU. There are eight categories for the CDU variable: excellent (EX), very good (VG), Good (GD), average (AV), fair (FR), poor (PR), very poor (VP), and unsound (UN). The x-axis denotes each category. The y-axis is the percentage distribution. The bottom figure shows the percentage distribution of grade. There are six categories for Grade, ranging from high to low, AA to E. The x-axis is the category of the variable. The y-axis is the percentage of units falling in a category

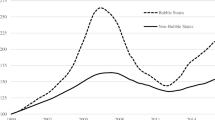

The Case-Shiller monthly Zip code level price index is provided by Fiserv. This index contains average monthly property price changes at the Zip code level and captures the effect of Zip code level price trends.Footnote 9 Based on the rate of price appreciation, Zip code price trend (Ni) is defined as the top quartile (TQ), middle quartile (MQ), and bottom quartile (BQ) in each period.

Besides Zip code property price trends, the CBG fixed effect is also included in the capital expenditure equation. The capital improvement also has a component of consumption demand. This demand is likely driven by the demographic characteristics of the homeowners, including their age, education, family size, income and wealth. The CBG fixed effect helps in this regard to the extent that such demographics tend to cluster in a CBG.

Zip code owner-to-tenant ratios, obtained from the U.S. Census Bureau, are included to control for the impact on investment of the residential composition of Zip codes. Homeowners have different incentives for capital improvement for owner-occupied and renter-occupied units. There is no consumption-driven demand for improvements by a landlord when a unit is tenant occupied. The investment component is also low, because it is hard to monitor property quality and condition for tenant-occupied units. Moreover, some leases require a tenant to return the property to its original state when the lease expires. Such a requirement may discourage tenants from making temporary improvements.

Descriptive Statistics

To construct the final sample for analysis, properties with addresses that could not be geo-coded are excluded. Transactions are omitted if their recorded prices, dates or structure characteristics were missing or recorded as zero. The final sample from 2005 to 2009 contains 13,191 single-family house transactions, including 2308 sales recorded with a sheriff’s deed. Twelve thousand four hundred eleven distinct homes account for the 13,191 transactions and 2106 distinct homes account for the 2308 foreclosure sales. Eighty percent of distinct homes undergo capital improvement in the 3 years before sale date. After excluding missing values and merging this dataset with MLS data, there were 30,210 valid permit records requested between 1999 and 2011 that were associated with properties sold between 2005 and 2009 and 41,208 permit records for unsold properties during the same period.

Table 2 contains summary statistics for the whole sample, and Table 3 exhibits summary statistics for the foreclosure and non-foreclosure subsamples. As shown in Table 2, the sample consists of a diverse range of properties. Their average age is 65.8 years.Footnote 10 The mean size is 1264 square feet. In the 2 years before its sale, the capital expenditure invested in a property averaged $1825. The amount increases to $2850 for a 3-year time window before a sale. There is a large standard deviation for capital expenditures, suggesting a divergence in capital expenditure investment. Within 1 year after a sale, the capital expenditure invested by the purchaser averaged $1075.

Table 3 shows that foreclosed properties differed from non-foreclosed properties in several ways. Foreclosed properties were on average 5.25 years older and larger than those in the non-foreclosure group. Foreclosed properties also had 0.11 more bedrooms. Foreclosed properties on average were less desirable in terms of quality and physical condition as measured by CDU and Grade. The findings on capital expenditure are interesting. Capital expenditure in 2 years before a sale for foreclosure group is 6.6 % of that for non-foreclosures. Capital expenditures in 3 years before sale date are also less than that for non-foreclosures. As mentioned previously, the time window in Milwaukee between a borrower’s delinquency and a REO sale is about 3 years. During this time frame, lenders control the investment decision for roughly the last 18–12 months preceding a REO sale. The defaulting owner controls the decision in months 36–24 before most likely. One hypothetical explanation for the low investment for foreclosure group in 2 years shortly before REO sale is that lenders adopt a strategy of low investment after they take title to foreclosed properties. Moreover, borrowers reduce their spending if they foresee foreclosure or their financial condition deteriorates. It is a hypothetical explanation that is nevertheless consistent with the lower investment observed for the foreclosure group in the years before delinquency. HOWEVER, there is no significant difference in capital expenditures between these two groups for earlier years. These results indicate that homeowners reduce their capital expenditures when they become financially distressed, can foresee an eventual foreclosure, or when their financial conditions eventually deteriorate to the point that they cannot afford any investment at all. I take the results of Table 3 as initial evidence of reduced investment by foreclosing lenders and defaulting homeowners. The table also shows that purchasers of foreclosed properties spend more on capital expenditures than purchasers of regular sales within 1 year after sale.

Methodology and Results

Methodology

The incentives for capital improvement have basically two components: investment and consumption. By restricting the sample to sold properties, I focus on the investment component. The factors associated with consumption are not discussed in this paper due to data availability. CBG fixed effect is included to control for demographic factors more traditionally related to consumption (income, wealth, age of owner, family size etc.).

A foreclosure indicator (\( {Foreclosure}_i \)) is included as explanatory variable to test Hypothesis 1, which states the impact of foreclosure and expectation of foreclosure on capital improvement. This indicator takes a value of 1 for a foreclosure sale and 0 otherwise. There may be an endogeneity problem with including the foreclosure indicator. It is reasonable to believe that owners who sell their property will invest less in capital improvements just before the sale, because they have little consumption benefit. The decision to sell is also different for foreclosed properties than normal owner transactions. Thus, the foreclosure dummy could be a proxy for those differences in the decision to sell. The spending during the time period the lender controls the property has a different dimension. The lender chose to foreclose and also makes the decision about capital investment before the REO sale. So the endogeneity is less a concern as there is a significant time lapse between the decision to foreclose and the decision about capital investment. A Heckman selection model is estimated for defaulting as a robustness check.

The average Zip code capital expenditure (\( {NCapex}_i \)) is included to test the investment externality in Hypothesis 2. A measure of neighboring foreclosures (\( {NF}_{itd} \)) is one explanatory variable to test Hypothesis 3. Zip code price trend (\( {N}_i \)) defined as TQ, MQ and BQ based on the rate of price appreciation in each period is included to control for the price trend in local housing market. As discussed previously, the owner to tenant ratio (\( {OT}_i \)) in the Zip code is likely to affect capital improvement decision of individual homeowner and is thus an explanatory variable for the capital expenditure. A vector of structural characteristics (\( {Z}_i \)) serves as control variables, including grade, CDU, square footage, age, number of bedrooms, number of bathrooms and number of garage. In addition, CBG fixed effect is included to control for demographic factors more traditionally related to consumption (income, wealth, age of owner, family size etc.).

The linear function to estimate property capital expenditures could be specified as follows:

To test Hypotheses 1 to 3, the dependent variable is the dollar amount of capital expenditures in 3 years before a sale. To test Hypothesis 4 concerning purchasers of foreclosed properties’ capital expenditure, the dependent variable is the capital expenditures within 1 year after their purchases. \( {NCapex}_i \) is defined in the same time window as that of the dependent variable.

Figure 2 shows that the capital expenditure variable is left censored. The OLS estimation will be biased and inconsistent in this case. I turned to a Tobit model (Wooldridge 2002) to estimate the censored capital expenditure decision. The structure equation in the Tobit model is:

\( {Capex}_i^{*} \) is a latent variable that is observed for capital expenditure values greater than zero and censored otherwise. The observed capital expenditure \( {Capex}_i \) is defined by the following equation:

Maximum likelihood estimation is implemented to estimate the parameters in Eq. (3).

Results

Table 4 reports the marginal effect in the Tobit model on unconditional expected value for capital expenditures before a sale. Table 5 reports that for capital expenditures by purchaser of a property. As shown in Table 4, the coefficient of the foreclosure indicator is negative and statistically significant.Footnote 11 It suggests that capital expenditures for foreclosed sales are lower than for non-foreclosures, which is consistent with Hypothesis 1. The reduced investment in foreclosed properties ranges on average from $700 to $900, varying with \( {NF}_{id} \) counted during different time windows before the subject property’s sale date. To better understand this reduced investment, it is important to be clear on the investment decision-making process in Milwaukee during the 3-year time window between a borrower’s delinquency and a REO sale. As discussed previously, lenders control the investment decision for roughly the last 18–12 months before the REO sale, while the defaulting owner most likely controls the decision in months 36–24 before the sale. Given this time frame, one hypothetical explanation for the low investment for a foreclosure group before a REO sale is that lenders adopt a strategy of low investment after they take title to foreclosed properties. Another hypothetical explanation for a foreclosure group in the years before delinquency is that homeowners reduce their spending if they foresee foreclosure or if their financial condition deteriorates because of their limited liability in the case of default. As a robustness check for the above arguments, I separated the \( {Capex}_i \) spending into two smaller buckets: the last 18–1 months before the REO sale, when lenders control the investment decision; and the months 36–19 before the REO sale, when the defaulting owners are in control. The results show that both the defaulting owners and the foreclosing lenders contribute to the reduced investment for foreclosures. The findings support the two hypothetical explanations for the low investment for foreclosure groups over 3 years before sale. Both findings are consistent with the prediction that foreclosed properties are less well maintained than non-foreclosed properties and that the observed “foreclosure discount” associated with the sales prices of foreclosed properties is at least in part due to reduced capital investment.

The results show that individual capital expenditure increases by $0.15 when its neighborhood counterpart increases by $1, supporting Hypothesis 2. The increase could be because of higher average spending on each project or reflect an increase in the number of projects. The first possible explanation for this increase presumes a general increase in spending. For example, if the neighborhood average increases by $1000, each homeowner will spend $150 more on capital improvements. A second and alternative explanation is the probability that a few large improvement projects will be started. For example, 1 in 100 homeowners may undertake a $15,000 project. The mechanism involved varies from neighborhood to neighborhood. The first mechanism works when most residents invest in a neighborhood during a similar time window, and the second works when a majority of residents do not invest but a few make large improvements. The distribution of \( Capex \) in Fig. 2 shows that most of the capital expenditures involve improvements less than $5000. Given this distribution, a neighborhood investment externality is more likely to work through the first mechanism. The second mechanism is more likely to work through after a sale than before a sale. The Tobit estimates for the probability of Capex being uncensored shows that the impact of \( N Capex \) on the probability of being uncensored is larger for the purchasers than for the previous owners.Footnote 12 This finding is consistent with the observation that buyers tend to make more capital improvement after their purchases than sellers do before sales.

The coefficients of nearby foreclosures are not statistically significant, meaning Hypothesis 3 is not supported. This finding suggests that the negative impact of foreclosures on neighboring properties is likely to take place by affecting the neighborhood capital expenditure, Zip code price trend, and CBG fixed effect. When those neighborhood attributes are controlled for, foreclosure itself does not become contagious. The results also show that capital expenditure relates negatively to Grade.Footnote 13 One explanation could be that a property with better overall construction quality requires less improvement. A robustness check that includes CDU and Grade as categorical variables shows that investment in both the high and low categories is higher than in the medium category. The finding that homeowners of properties in the high category invest more could be attributable to a wealth effect. Homeowners of properties in the low category may invest more to maintain the regular functioning of these low quality properties. On average, homeowners invest less in aged properties.Footnote 14 This does not support the traditional wisdom that older homes need more major renovations than newer homes. This finding may be attributable to the homes in the sample being so old already (a quarter of them are 52 years old) that they need major renovation. The positive coefficient on the size variable suggests larger properties require larger capital expenditures. The size of a home is more likely a proxy for the wealth and income of the owners. This paper uses the CBG fixed effect to control for the demographic variables that are missing from the data. Properties in MQ neighborhoods have more investment than those in LQ neighborhoods. One possibility is that residents in low value neighborhoods are less wealthy than those in other neighborhoods and cannot afford to invest in capital expenditures.Footnote 15

Table 5 exhibits the estimation results for capital expenditures by purchasers of properties after a sale. On average, the purchaser of a REO property spends $196 more than that of a non-REO within 1 year after purchase; this supports Hypothesis 4. The extra spending after purchases by those who buy REO properties is small relative to the reduced investment in the 3 years before a sale. One hypothetical explanation is that in general, purchasers of REO properties may have less wealth and income than buyers through regular sales. Consequently, they are more likely to spend their limited resources on improvements associated with the basic functioning of the REO properties than on fully recovering the lower investment before foreclosures and REO sales. Both TQ and BQ neighborhoods have higher capital expenditures 1 year after a sale than MQ neighborhoods. The higher investment in TQ neighborhoods could be attributed to a wealth effect. Capital improvements by purchasers of REO properties in a BQ neighborhood to catch up in property quality could contribute to this finding. Consistent with the findings on capital expenditures before a sale, a large property requires a higher capital expenditure by purchasers. Neighborhood capital expenditures positively affect individual homeowner’s capital expenditure. The magnitude of investment externality after a sale is larger than that before a sale. This is consistent with a general observation that purchasers are more likely to make capital improvements when they move into a new property than the sellers who are getting rid of it.

Conclusions

Recent research has found evidences that a foreclosed home is contagious and reduces the price of neighboring properties. This study focuses on the role of foreclosures in determining housing capital expenditures.

With a novel dataset that tracks housing capital expenditures over time, this paper models that capital expenditures in the 3 years before a sale as a function of average neighborhood capital expenditures, an indicator of whether the home is subsequently foreclosed upon by the lender, the Zip code price trend, the number of nearby foreclosed properties, the owner/tenant ratio of the Zip code and selected house characteristics—including an assessment of the grade and quality of the home. The empirical results confirm that owners of homes that are foreclosed upon spend less on capital improvements in the 3 years prior to the subsequent foreclosure and REO sale. Since the lender controls the property for roughly half of the 3 year window prior to the REO sale, the results also show that lenders do not make capital improvements after obtaining title but prior to disposing of the property.

On average, the purchasers of foreclosed properties make more capital improvements in the year after their purchases than do buyers of non-foreclosures, but the additional investment is less than the reduced investment before the sale. One possible explanation is purchasers of foreclosed properties may spend their limited financial resources on the basic improvements with being financially unable to fully recover the reduced investment before a sale. Both findings are consistent with the prediction that foreclosed properties are less well maintained than non-foreclosed properties and that the observed “foreclosure discount” associated with the sales prices of foreclosed properties is at least in part due to reduced capital investment.

The reduced capital expenditures in REO sales also generate a negative externality by creating a disincentive for other homeowners to spend on home improvements. An individual’s capital expenditure decision is positively related to its neighborhood counterpart. Clusters of new construction and investment externalities may contribute to this positive relationship. Nearby foreclosures do not affect capital investment in a property when neighborhood attributes are controlled for, such as neighborhood capital expenditure, Zip code price trends and CBG fixed effect.

These findings show that foreclosure plays a significant role in determining housing capital expenditures. This evidence is important for the design and evaluation of foreclosure-related policies. The main channel for the foreclosure contagion effect on neighboring properties is through a reduced investment associated with foreclosures. Self-reinforcing investment behavior may further accelerate deferred investment in declining neighborhoods; this adversely affects housing quality and ultimately stimulates further waves of foreclosures. Based on these findings, the options for sensible policy prescriptions to stabilize housing prices include prevention of the foreclosure process, support for struggling homeowners so they can invest in their properties and shortening the foreclosure process so purchasers of foreclosed properties can invest in repairing any damage to them.

Notes

Keynes (1919), Krugman (1988) and Sachs (1990) show that heavy public debt loads reduce incentives for both public sector and private sector investments. For household finance decision, negative equity homeowners have less incentive to improve the property, since doing so makes the debt claim more secure and valuable without necessarily increasing the asset’s value to the owner.

Previous studies have used different data on sample periods and locations and different approaches to define foreclosures, distance radii, and time windows. But, in general, all of them have found a negative correlation between foreclosures and the market value of their neighboring properties.

Despite the lack of data on FSBO sales, Hendel et al. (2009) reports that MLS sales accounted for 86 % of all transactions sold from 1998 to 2005 in Madison, WI, a city near Milwaukee.

Amounts reported in the permit records are estimated costs provided by permit applicants. When a building permit is filed, the estimated cost of construction is entered on the application. The applicant may change the amount at any time. It is the responsibility of the applicant to submit the changes before issuance of a certificate of occupancy and/or before completion of construction. In practice, the assessor’s office flags unfinished permit activities and tracks the status of such flags by their expected completion dates to ensure permit activities are conducted as reported.

Harding, Rosenthal, and Sirmans (2007) estimated a 2.5 % overall rate of depreciation for the complete bundle of house attributes (including land). I have applied this overall estimate to all individual capital improvements. Capital expenditures may depreciate at a higher rate, but 2.5 % sets a boundary for this depreciation.

Major lenders sell their REO property via MLS listings. Merging sheriff’s deeds with MLS sales listings shows that 90 % of properties with a sheriff’s deed could be matched with an MLS sale.

The innermost ring with the shortest time radius includes in each direction the two or three nearest neighboring properties that have been sold shortly before potential buyers are visiting a subject property. The second ring could include foreclosures on the same block as the subject property. These foreclosures are unlikely to be visible from a subject property, but nevertheless, may be seen by prospective buyers visiting it. Foreclosures in the outer rings are not visible from the subject property, but may change buyers’ perceptions of the neighborhood or provide alternatives for buyers.

CDU and Grade are used by tax assessors in the City of Milwaukee. They are assigned the first time a property is inspected. Each time thereafter, when assessors review a property, they evaluate whether to keep or change its CDU. Grade rarely changes, because it reflects construction quality. The assessors do not change CDU without an inspection of the property. The Guide to the Property Assessment Process for Wisconsin Municipal Officials (http://www.revenue.wi.gov/pubs/slf/pb062.pdf) has specified the annual assessor requirements by assessment type and list when full evaluation is appropriate.

The S&P/Case-Shiller home indices methodology is available at http://us.spindices.com/index-family/real-estate/sp-case-shiller . The indices are calculated monthly, using a 3-month moving average algorithm. The index point for each reporting month is based on sales pairs accumulated in rolling 3-month periods. This averaging methodology is used to offset delays that can occur in the flow of sales price data from county deed recorders, to keep sample sizes large enough to create meaningful price change averages, and to mitigate concern over the volatility of the value of indices at the Zip code level.

The average age of properties in the sample is older than those in other studies. It is consistent with American Housing Survey (AHS), which shows that Milwaukee’s housing stock is older than the national average.

As discussed previously, endogeneity could be an issue because of the inclusion of foreclosure as an indicator variable in the model of Eq. (3). A Heckman selection model was estimated for a robustness check of this issue. In the first stage, the foreclosure likelihood was estimated with a probit model. The explanatory variables include property structure characteristics (\( {\mathrm{Z}}_{\mathrm{i}} \)), neighboring foreclosures (\( {\mathrm{NF}}_{\mathrm{itd}} \)), ZIP code price trend (\( {\mathrm{N}}_{\mathrm{i}} \)), ZIP code owner-to-tenant ratio (\( {\mathrm{OT}}_{\mathrm{i}} \)), and CBG fixed effect. The predicted foreclosure probability was then included in the second stage estimation for \( {\mathrm{Capex}}_{\mathrm{i}} \). The main findings remained the same under the Heckman model.

The supplemental result on the marginal effect in the Tobit model on the probability of being uncensored for capital expenditures before a sale and after a sale is available upon request.

The results remain the same under the following robustness checks: inclusion of CDU only; inclusion of both CDU and Grade; exclusion of both CDU and Grade.

The results remain the same when both age and age squared are included as explanatory variables.

The following robustness checks are also estimated: the inclusion of time fixed effect; the inclusion of the categorical variable of garage; the exclusion of CBG fixed effect. The main findings of the model were unchanged.

References

Campbell, J. Y., Giglio, S., & Pathak, P. (2011). Forced sales and house prices. American Economic Review, 101(5), 2108–2131.

Durlauf, S. (2003). Neighborhood effects. In J. V. Henderson & J.-F. Thisse (Eds.), Handbook of regional and urban economics (Vol. 4). Amsterdam: North-Holland.

Gerardi, K. E., Rosenblatt, P.S. Willen, Yao, V. (2015). Foreclosure externalities: new evidence. Journal of Urban Economics, forthcoming.

Harding, J., Miceli, T. J., & Sirmans, C. F. (2000). Deficiency judgments and borrower capital expenditure. Journal of Housing Economics, 9(4), 267–285.

Harding, P., Rosenthal, S. S., & Sirmans, F. (2007). Depreciation of housing capital, capital expenditure, and house price inflation: estimates from a repeat sales model. Journal of Urban Economics, 61(2), 193–217.

Harding, J. P., Rosenblatt, E., & Yao, V. (2009). The contagion effect of foreclosed properties. Journal of Urban Economics, 66(3), 164–178.

Hendel, I., Nevo, A., & Ortalo-Magné, F. (2009). The relative performance of real estate marketing platforms: MLS versus FSBOMadison.com. American Economic Review, 99(5), 1878–1898.

Immergluck, D., & Smith, G. (2006a). The external costs of foreclosure: the impact of single-family mortgage foreclosures on property values. Housing Policy Debate, 17(1), 57–79.

Immergluck, D., & Smith, G. (2006b). The impact of single-family mortgage foreclosures on neighborhood crime. Housing Studies, 21(6), 851–866.

Keynes, J. M. (1919). The economic consequences of the peace. New York: Harcourt, Brace and Howe.

Krugman, P. R. (1988). Financing vs. forgiving a debt overhang. Journal of Development Economics, 29(3), 253–268.

Myers, S. C. (1977). Determinants of corporate borrowing. Journal of Financial Economics, 5(2), 147–175.

Pavlov, A., & Blazenko, G. W. (2005). The neighborhood effect of real estate maintenance. Journal of Real Estate Finance and Economics, 30(4), 327–340.

Rossi-Hansberg, Sarte, & Owens, III. (2010). Housing externalities. Journal of Political Economy, 118(3), 485–535.

Sachs, J. D. (1990). A strategy for efficient debt reduction. Journal of Economic Perspectives, 4(1), 19–29.

Wooldridge, J. (2002). Econometric analysis of cross section and panel data. Cambridge: MIT Press.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Li, L. The Role of Foreclosures in Determining Housing Capital Expenditures. J Real Estate Finan Econ 53, 325–345 (2016). https://doi.org/10.1007/s11146-015-9505-4

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-015-9505-4