Abstract

As informational leakages become a common occurrence in economic and business settings, the impact of observability on behavior in adversarial situations assumes increased importance. Consider a two-player contest where there is a probabilistic information leak about one player’s action and the recipient of the information has the ability to revise his contest expenditure in response to the leaked rival choice. How does the ability to revise and resubmit affect each contestant’s behavior? We design a laboratory experiment to study this question for two well-known contest games: the lottery contest and the all-pay auction. Equilibrium predicts that compared to simultaneous moves, the strategic asymmetry arising from the ability to revise has no effect on expected expenditure in the lottery contest. In contrast, in the all-pay auction expected expenditure is decreasing in the probability of informational leakage. Experimental data support these predictions despite overexpenditure relative to equilibrium. Furthermore, the potential observability of the rival’s action confers an advantage on the informed player not only in the all-pay auction, as theory predicts, but also in the lottery contest if the probability of leakage is high.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In highly competitive or conflictual situations, the timing of decisions and the information about a rival’s actions play a fundamental role in shaping optimal strategies and influencing final outcomes. When a player has the ability to observe his rival’s action before making his choice, it creates an interesting strategic asymmetry between the two players. On the one hand, the recipient of his rival’s information can profitably employ it to create a second-mover advantage. On the other hand, if the rival knows that her information could be leaked, she may benefit from her ability to pre-commit to an action. This tradeoff has been explored in games of espionage (Solan & Yariv, 2004), in games with imperfectly observed actions (van Damme & Hurkens, 1997) and in other games of commitment (Morgan & Várdy, 2013). Informational leakages and observability are also important issues in areas such as R &D consulting (Baccara, 2007) and some applications of computer science (Alon et al., 2013).

The above considerations are particularly salient in the competitive settings commonly referred to as contests. Contest models have become a well-accepted approach for analyzing competitive behavior in a wide array of applications, such as lobbying, patent races, incentive systems within a firm or sports and non-price competition for market share (see for instance, Vojnovic, 2016). Although contest structure varies substantially across models, the existing literature has focused primarily on purely simultaneous moves contests (including multiple-stage contests with elimination) and purely sequential contests (where later players make decisions after observing the early players’ expenditure levels). These commonly employed timing assumptions are appropriate for a broad range of applications of contest theory. However, there exist situations where prior to the conclusion of a simultaneous moves contest, one of the contestants receives information about his rival’s plans and may have the opportunity to revise his initial choice. This informational leakage can be the result of a deliberate act of industrial espionage undertaken by a former employee, current management or third-party collaborator.Footnote 1 It may also occur as a result of collaboration on a joint venture by competing firms.Footnote 2 Finally, the informational breach could simply be caused by a careless technical glitch.Footnote 3 In its Risk Based Security Report, CNET states that 5,183 breaches were reported in the first nine months of 2019, exposing a total of 7.9 billion records. Although some of these breaches were due to active hacking, a vast majority of them were a result of unsecured databases. In each of these instances, the identities of the player whose information is leaked and the recipient of the leaked information are common knowledge.Footnote 4 However, it remains unclear whether the information can be of use to the recipient and cause the latter to revise their choice.

In this paper, we contribute to the contest literature by exploring the issues of informational leakages and observability. To model the uncertainty about the extent and the usefulness of the leaked information, we assume that the leakage is probabilistic. We consider situations where the contestant whose plans were leaked is either unaware of the breach or she has made an irrevocable commitment and consequently, may not be able to adjust her choice. In contrast, the recipient of the information may be able to revise his choice in response to the leaked rival information. As a consequence, a random informational leakage probabilistically turns a simultaneous moves contest into a leader-follower contest, thereby introducing a form of strategic asymmetry between otherwise symmetric players. The focus of our analysis is the extent to which this strategic asymmetry affects the ex-ante behavior of both players as well as the ability of the informed player to exploit the strategic asymmetry. To the best of our knowledge, this is the first paper to examine such a hybrid simultaneous-sequential moves game in the contest literature.

We explore the above questions by comparing two predominant winner-take-all contests: the all-pay auction and the lottery contest. These two contest mechanisms are among the most widely studied in the experimental literature and their popularity can be justified on the basis of their analytical tractability and their wide ranging applicability (Dechenaux et al., 2015). The fundamental difference between the two frameworks lies in their degree of competitiveness as measured by the marginal effectiveness of expenditure (Konrad, 2009; Faravelli & Stanca, 2014). The marginal impact of expenditure is lower, and accordingly competitiveness is lower, in the lottery contest than in the all-pay auction. That is because lottery contests are stochastic and higher expenditure does not guarantee a win, whereas all-pay auctions are deterministic and there is a clear incentive for a player to slightly outbid his competitor. Thus, these two frameworks epitomize contrasting philosophies that guide prize allocation. A priori, it is unclear whether one contest form outperforms the other when players are asymmetric. In a seminal study, Fang (2002) formally demonstrate that an all-pay auction may elicit a smaller amount of total effort when the players are sufficiently heterogeneous, but the result from the empirical literature is mixed (Orzen, 2008; Duffy & Matros, 2021).Footnote 5 Our work adds to this comparison, whereby players are not ex-ante heterogeneous but one of the players may have an advantage, probabilistically. Including both these frameworks in our analysis allows us to investigate how the impact of this strategic asymmetry between players depends on the degrees of competitiveness of the underlying contest.

We derive theoretical predictions and implement a laboratory experiment based on a 2x2 design by manipulating two treatment variables: the degree of competitiveness (lottery vs. all-pay auction) and the degree of strategic asymmetry (low vs. high probability of informational leakage). Theory predicts that when competition is relatively mild, as in the lottery contest, neither player benefits from strategic asymmetry. Indeed, the equilibrium outcome is the same as the outcome of the simultaneous moves game with symmetric players and the tradeoff between observability and commitment is nullified. In contrast, in the all-pay auction, which represents more intense competition, strategic asymmetry confers a strong advantage on the potentially informed player. We refer to this advantage as the ‘value of flexibility.’

The game proceeds as follows. Initially both players choose their contest expenditures simultaneously. Then, with some probability, one of the players’ expenditure is revealed to the rival player. We assume that expenditure is irreversible for the player whose information is leaked, but the player who receives the rival’s information may choose to revise his expenditure at no cost. In this setting, a natural question to ask is: if the leak occurs, does the informed player have an incentive to revise his expenditure? Our equilibrium analysis reveals that the answer depends on the type of contest. In the lottery contest, the equilibrium is in pure strategies. Hence the recipient of the rival’s information has no incentive to adjust expenditure. In contrast, in the all-pay auction, both players randomize in the initial stage and if information is leaked, the informed player can almost certainly guarantee a win by slightly outbidding his rival. This implies that the informed player has a strong incentive to revise, and indeed, in equilibrium, he almost always revises his expenditure when given the chance. Thus, informational leakage and the ability to revise impart a strategic advantage to the informed player in an all-pay auction, but not in a lottery contest.

The second related question is: how does strategic asymmetry affect each player’s expenditure choice in the initial simultaneous moves game? Again, the answer differs across the two contests. In the lottery contest, the potential ability to revise does not affect equilibrium behavior compared to the standard simultaneous moves game. Ex-ante, the expenditure profile is symmetric so that each player has an equal chance of winning, regardless of the probability of leakage. In sharp contrast, in the all-pay auction, there are multiple equilibria that feature randomization in the first round. In the Pareto dominant equilibrium, in expected terms, the committed player expends less than the other player. This yields the interesting result that the committed player is less likely to win than his rival, even if the rival does not get the opportunity to revise his expenditure. Furthermore, as the likelihood of informational leakage increases, the committed player reduces her expenditure and therefore, the other player is not only more likely to win but can do so at lower expenditure (in expected terms). Hence, it follows that in the all-pay auction, the potentially informed player earns strictly positive value from the flexibility of revising his choice. Moreover, this value of flexibility is increasing in the probability of leakage. In contrast, there is no value of flexibility in the lottery contest.

Our analysis focuses on how the likelihood of informational leakage (i.e., strategic asymmetry) affects ex-ante expenditure levels, the frequency of revisions and the value of flexibility. The experimental findings validate many of the comparative statics predictions, but there are a few key departures. Consistent with the theoretical predictions, we find that the strategic asymmetry arising from the ability to revise has no effect on ex-ante expenditure in the lottery contest but it has a significant effect in the all-pay auction. Average expenditure for both players is lower in all-pay auction when the probability of leakage is high. Overall, the observed expenditure behavior is consistent with prior literature whereby, in both contests, we observe widespread overdissipation relative to the risk neutral equilibrium prediction and wide variation in individual expenditure choices. In lottery contests, there is weakly greater dispersion in expenditure choices of the committed player, which can be traced back to their inherent disadvantage. In the all-pay auction, the distribution of expenditure choices exhibits a pronounced bimodal pattern, similar to prior experiments on symmetric all-pay auction with complete information. The committed players frequently submit zero expenditure thereby surrendering to their strategic disadvantage, but in other instances, they expended the maximum possible level.

In equilibrium, informed players always revise in the all-pay auction and they never do in case of lottery contest. We find that frequency of revision is 87.5% in the all-pay auction, and most of the revised expenditure levels are equal to the best response. In the lottery contest, the frequency of revision is strikingly high at 71%. However, this certainly can be rational behavior since the first round choices are off-the-equilibrium path. In testing this hypothesis, we find that lottery contest decisions are in fact sticky and revisions are less frequent than best response behavior would predict. Furthermore, the revised expenditure levels that are chosen with knowledge of the rival’s choice are substantially higher than the risk neutral best response.

Finally, we find that in the all-pay auction, the value of flexibility is strictly positive and increasing in the probability of leakage, although it is less than predicted by the Pareto dominant equilibrium. In a key departure from the prediction, we find that there is positive value of flexibility even in lottery contests when the probability of leakage is high. Together this suggests that the second mover advantage afforded by the informational leakage supersedes any possible value from pre-commitment in all-pay auctions, but also in lottery contests when strategic asymmetry is high.

The remainder of the paper is organized as follows. Section 2 describes how this study contributes to the existing literature on different contest structures as well as relates to prior work on the value of commitment. Section 3 presents the theoretical model and the testable hypotheses. Section 4 describes our experimental design and procedures. The results are in Sect. 5. Section 6 concludes.

2 Literature review

Our experiment contributes to the literature by interacting the degree of strategic asymmetry with the degree of competitiveness in two well-known contests. Both lottery contests and all-pay auctions are special cases of the Tullock model of rent-seeking (Tullock, 1980; Konrad, 2009) and have been applied extensively to the theoretical analysis of rent-seeking competitions, such as advertising, R &D, lobbying, political races, military conflict, litigation and status-seeking contests as well as the provision of public goods and charity. Experimental tests of these models systematically reveal significant overexpenditure relative to the risk neutral Nash equilibrium predictions (see 2015). However, in both types of contests, this overdissipation tends to be lower with heterogeneity among players, presumably because of the so-called “discouragement effect” (Konrad, 2009). Specifically, in contests with heterogeneous players, sufficiently large differences in players’ abilities, endowments or costs reduce the incentive to compete for the weaker player. As a result, the stronger player’s incentives for effort are also reduced, which leads to lower expenditure overall. Empirically, the discouragement effect has been documented both in field studies (Brown, 2011, Franke, 2012, for golf tournaments; Sunde, 2009, for tennis matches and Brown & Chowdhury, 2017, in horse racing) as well as in the laboratory (Davis & Reilly, 1998; Anderson & Stafford, 2003; Fonseca, 2009; Sheremeta, 2011; Kimbrough et al., 2014; Hart et al., 2015; Fehr & Schmid, 2017; Llorente-Saguer et al., 2022).Footnote 6

In this paper, we consider a novel form of asymmetry that arises due to a probabilistic informational leak. We assume that the players have identical costs and valuations for the rent, and initially, they make their expenditure decisions simultaneously. However, it is common knowledge that one of the players could be given the option to revise his choice after learning the other player’s action. In the all-pay auction, we show that in equilibrium, the player whose information may be leaked behaves as if she has a lower valuation for the prize than the rival player. Thus, the players’ initial choices resemble those in the standard asymmetric all-pay auction with complete information and reflect a form of discouragement effect (Baye et al., 1996). In contrast, in the lottery contest our model predicts that strategic asymmetry between players creates no discouragement effect. That is, the players’ predicted expenditure choices in the hybrid simultaneous-sequential moves game are the same as in the standard simultaneous moves game.

It is worth noting that much of the existing literature has focused on single rounds contests, with few studies considering sequential moves (Weimann et al., 2000; Fonseca, 2009; Nelson & Ryvkin, 2019) or endogenous timing, which can result in sequential moves (Shogren & Baik, 1992; Liu, 2018). Experimental studies of games with multiple rounds generally address elimination (Parco et al., 2005; Amaldoss & Rapoport, 2009) or best-of-N designs (Mago et al., 2013). The prior literature has also considered environments where players can carry over expenditure across multiple rounds with intermediate prizes (Schmitt et al., 2004) or raise their expenditure in response to feedback about the rival’s choice, as in the models of Yildirim (2005) or Hirata (2014). Thus, our informational leakage framework provides a novel hybrid between single and multiple rounds contests.

Finally, our study of the value of flexibility contrasts with the prior literature on the value of commitment in the so-called noisy leader game (Bagwell, 1995) and in games with costly information acquisition (Várdy, 2004). Bagwell (1995) and van Damme and Hurkens (1997) examine the conditions under which a potential first mover is able to exploit his Stackelberg leader advantage when the rival player only observes a noisy signal of the leader’s action. In a laboratory experiment, Huck and Müller (2000) find that contrary to Bagwell’s pure strategy equilibrium prediction, observed play converges to the Stackelberg outcome over time, thereby suggesting that there is strictly positive value to commitment in experimental noisy leader games. Várdy (2004) shows that insights from the noisy leader game carry over to settings where one of the players can incur a cost to learn his rival’s action. Experimental examination by Morgan and Várdy (2004) reveals that whether commitment value is preserved or lost depends on the cost of observation. If the observational cost is low, the value of commitment is preserved and it is lost if the cost is high (see also Morgan and Várdy 2007, 2013). We note that this literature highlights a tradeoff between the first-mover’s advantage due to commitment and the potential second-mover advantage conferred by observability (Solan & Yariv, 2004). In our model, the two competing effects cancel each other out in the lottery contest, while the observability effect dominates in the all-pay auction creating a clear second-mover advantage.

The related literature also includes work on games where timing is endogenous. Caruana and Einav (2008) study multi-period games in which a player who has already moved can switch to a different action at a cost that increases over time (i.e. as a final deadline approaches). More recently, Kamada & Moroni (2018) examine games in which the timing of moves is private information, but each player may choose to incur a cost to reveal his action to the other players.Footnote 7 Our approach is quite different from this stream of research. In our model, it is common knowledge that one of the players may become perfectly informed about the rival’s action. The informational leakage is a move by nature and when it occurs, the rival’s action is fully revealed to the player.

3 Theoretical model and testable hypotheses

3.1 The model

Two players, A and B, compete for an indivisible and commonly known rent of value V, hereafter referred to as the prize. The game has up to two rounds. In the first round, Player A chooses expenditure \(x_{A1}\) and Player B chooses expenditure \(x_{B}\). These expenditure choices are made simultaneously. With probability \(1-\alpha\), where \(\alpha <1\), the game ends after the first round. In this case, the probability that Player A wins the prize is \(p_{A}(x_{A1},x_{B})\) and the probability that Player B wins is \(p_{B}(x_{B},x_{A1})\). With probability \(\alpha\), the game proceeds to the second round where player A learns player’s B expenditure choice. Player B’s expenditure remains at \(x_{B}\). This captures the situation where player B is unaware of the leakage or she has made an irrevocable commitment and therefore cannot revise her expenditure choice. However, Player A can revise his choice in response to the leaked rival information. We allow player A complete flexibility in making this revision. Formally, player A chooses expenditure \(x_{A2}\), which may be less than, greater than or equal to \(x_{A1}\).Footnote 8 In round 2, the probability that Player A wins the prize is \(p_{A}(x_{A2},x_{B})\) and the probability that Player B wins is \(p_{B}(x_{B},x_{A2})\).

The probability of reaching the second round, or the probability of informational leakage \(\alpha\), represents the degree of strategic asymmetry between players A and B. For \(i\in \{A,B\}\), the probability \(p_i (\cdot )\) is the contest success function (CSF) that represents the degree of competition.

In the all-pay auction, the CSF is deterministic and given by

where \(p_i(x,x)=1/2\) if the game ends after the first round, for \(i,j \in \{A,B\}\), \(i\ne j\). For technical reasons, if round 2 is reached and player A is allowed to revise his expenditure, we assume that player A receives the prize with probability one in case of a tie.

In the lottery contest, the CSF is probabilistic and given by

if the sum of \(x_{i}\) and \(x_{j}\) is strictly positive and \(p_{i}(0,0)=1/2\).

Denote a player’s expected payoff in round t by \(u_{it}(x_{it},x_{jt})\) where \(t \in \{1,2\}\).Footnote 9 That is

Then player i’s ex-ante expected payoff (from the standpoint of the first round) is

for \(i,j \in \{A,B\}\), \(i\ne j\).

3.2 Equilibrium expenditure

We summarize the subgame perfect equilibrium for each contest in the following propositions. To determine the equilibrium prediction, we assume that both players are risk neutral. All proofs are in the Appendix in online supplementary materials.

Proposition 1

In the Pareto dominant subgame perfect equilibrium of the all-pay auction, in the first round, player A randomizes uniformly on the support \([0,(1-\alpha )V]\), player B has a mass point at \(x_B=0\) and randomizes uniformly on \((0,(1-\alpha )V]\). Expected expenditure levels are given by

In the second round, player A sets his expenditure equal to player B’s first round expenditure (to win the contest with certainty), so that

In this equilibrium, player A’s ex-ante expected payoff is equal to \(U_{A}^{APA}=\frac{\alpha V}{2}(3-\alpha ^2)\) and player B’s ex-ante expected payoff is \(U_{B}^{APA}=0\).

In the proof of Proposition 1, we show that in the all-pay auction, there exist multiple equilibria, but in all equilibria player B’s expected payoff is zero. Our prediction in Proposition 1 is based on the equilibrium in which player A’s expected payoff is highest.Footnote 10 In contrast, in the lottery contest, there is a unique subgame perfect equilibrium.

Proposition 2

In the subgame perfect equilibrium of the lottery contest, the players’ expenditure levels are given by

In equilibrium, player i’s expected payoff is equal to \(U_{i}^{L}=\frac{V}{4}\) for \(i\in \{A,B\}\).

These propositions make clear the distinction between the two types of contests. First, in the lottery contest, equilibrium is in pure strategies while in the all-pay auction, the players randomize in round 1. Second, in the lottery contest, despite very distinct round 1 expected payoff functions, both players expend the same amount, whereas in the all-pay auction, player A expends greater expenditure than player B.Footnote 11 Third, comparing across the two rounds, we note that in equilibrium, player A’s expenditure will be the same in rounds 1 and 2 of the lottery contest but will almost certainly differ in the all-pay auction. The fact that player A does not revise expenditure in round 2 of the lottery contest is due to the ‘no regret’ property of Nash equilibrium in pure strategies. In contrast, in the all-pay auction both players invest according to non-degenerate distributions in the first round and the ‘no regret’ property does not apply.

Based on the results from Propositions 1 and 2, we now compute the ex-ante expected value to player A of having the opportunity to revise his choice. We refer to this as the value of flexibility.

3.3 The value of flexibility

We define the value of flexibility as the difference between player A and player B’s ex-ante expected payoffs, \(\Delta ^{c}=U_{A}^{c}-U_{B}^{c}\), \(c\in \{L,APA\}\). In the all-pay auction, player A’s equilibrium expected payoff is strictly positive while player B’s is zero. Based on the expression in Proposition 1, in the Pareto dominant equilibrium of the all-pay auction, the value of flexibility is \(\Delta ^{APA}=\frac{\alpha V}{2}(3-\alpha ^2)\). Furthermore, not only is the value of flexibility strictly positive whenever \(\alpha >0\), but it is also increasing in the probability of informational leakage, \(\partial \Delta ^{APA}/\partial \alpha =(3V/2)(1-\alpha ^{2}) >0\).

In the lottery contest, in equilibrium player A does not benefit from the ability to revise his expenditure. Therefore the value of flexibility is zero, i.e. \(\Delta ^{L}=0\).

3.4 Hypotheses

In the experiment we set \(V=100\) and implement two different probabilities of an informational leakage, \(\alpha =0.25\) and \(\alpha =0.75\). Table 1 summarizes the equilibrium predictions assuming that players are risk neutral and that the Pareto dominant equilibrium is played in the all-pay auction. Our first hypothesis compares the initial round expenditure of the committed player (type B) and the player who may have the option to revise (type A).

Hypothesis 1

In the all-pay auction, on average a type A player’s contest expenditure is higher than a type B player’s expenditure in the round 1 simultaneous moves game. In the lottery contest, on average a type A player’s contest expenditure is the same as a type B player’s expenditure in the round 1 simultaneous moves game.

Our second hypothesis considers the impact of the probability of informational leakage (also referred to as degree of strategic asymmetry) on contest expenditure.

Hypothesis 2

In the all-pay auction, for both types of players, average contest expenditure is higher when the probability of informational leakage is low (\(\alpha =0.25\)) than when it is high (\(\alpha =0.75\)). In the lottery contest, for both types of players, average contest expenditure is independent of the probability of informational leakage.

Our third hypothesis focuses on the probability of revisions. Recall that Player A is predicted to revise his expenditure in round 2 with certainty, whereas the likelihood of revision in the lottery contest is zero. We propose the following qualitative hypothesis instead of the strong point prediction derived from the model.

Hypothesis 3

(a) Regardless of the probability of an informational leakage, a type A player is more likely to revise his expenditure in the all-pay auction than in the lottery contest. (b) In both contests, the likelihood of revisions is independent of the probability of informational leakage.

Finally, our fourth hypothesis deals with the value of flexibility.

Hypothesis 4

The value of flexibility is higher in the all-pay auction than in the lottery contest. In the all-pay auction, a type A player’s average payoff is higher than a type B player’s. In the lottery contest, both players earn the same payoff.

We now turn to the experimental design and the procedures that we implemented to test the above hypotheses.

4 Experimental design and procedures

The experiment was conducted at the Vernon Smith Experimental Economics Laboratory at Purdue University. A total of 128 subjects participated in sixteen sessions with eight subjects in each session. All subjects were students at Purdue University and were recruited via ORSEE (Greiner, 2015).Footnote 12 No subject participated in more than a single session. The experiment was programmed and conducted with the software z-Tree (Fischbacher, 2007).

To test our hypotheses, we conducted four treatments using a \(2\times 2\) design where we varied the type of contest (all-pay auction vs. lottery) and the probability \(\alpha\) of learning the rival’s expenditure. Each session employed a single type of contest and we varied the probability of leakage between \(\alpha = 0.25\) and \(\alpha = 0.75\) within session. Having the same set of subjects make decisions under both probability levels directly controls for subject variability. However, it may also result in hysteresis, with subjects’ experience in one treatment influencing their behavior in the other treatment. To account for such sequencing effects, we employ an A-B/B-A design structure. Table 2 summarizes the experimental design and shows how treatments were run in different orders in different sessions.

Each session proceeded in six parts. Subjects received written instructions, available in Appendix B, at the beginning of each part and these were also read aloud by the experimenter. In Parts 1 and 2, we asked the subjects to make decisions in a series of 20 lottery pairs that were designed to measure subject risk and loss aversion.

Parts 3 and 4 were designed to test our hypotheses. Each part lasted for 20 periods and corresponded to one of two leakage probabilities implemented in different orders. At the beginning of each period, subjects received an endowment of 100 experimental francs and were not allowed to choose expenditure levels exceeding that amount. Each contest period proceeded along two decision-making rounds. In round 1, subjects learned their type, A or B, for the period and then both players were asked to make their expenditure decisions simultaneously. While round 1 actions were revealed to both players regardless of type, decisions in round 2 differed depending on a player’s type. The type B player did not have any expenditure decision to make. However, upon learning his paired type B player’s round 1 expenditure, type A players were given a chance to revise their expenditure. Type A players could choose to leave their round 1 expenditure unchanged or revise it to a different amount.

The subjects were told that the computer would randomly determine which expenditure level, round 1 or round 2, would be used as the actual contest expenditure for the type A player. Instructions made it explicitly clear that the type B player’s round 1 expenditure was irreversible, but that with a 25% or a 75% chance depending on the treatment, the type A player’s round 2 expenditure would be used to determine the winner. Thus in every period, we collected expenditure decisions for both round 1 and round 2 for every type A player.Footnote 13

We employed a quasi strategy method because it allowed us to systematically compare initial and revised choices in every period, irrespective of whether the round 2 choice was used to determine the winner. This elicitation method has the distinct advantage in that it “may lead subjects to make more thoughtful decisions and, through the analysis of a complete strategy, may lead to better insights into the motives and thought-processes underlying subjects’ decisions. At the same time, it allows for a more economical data-collection process" (Brandts and Charness 2011, pp. 377 ). However, while in game-theoretic view, strategy method should yield similar decisions as the ‘direct response’ method (type A makes round 2 decision with probability \(\alpha\)), it can be criticized on behavioral grounds as an abstraction of real-world setting. In this regard, it is useful to note that Brandts and Charness (2011) conduct an expansive survey with twenty-nine studies that compare behavior using the two methods. They find that there are more studies that find no difference across the elicitation methods than studies that do find a difference, thereby “dispelling the impression that strategy method inevitably yields results that differ” (pp. 395). Furthermore, they report that there is no study where a treatment effect found with the strategy method is not observed with the direct response method. Analyzing the specific design features, they find that both multiple period interaction and role-reversal reduce difference across these methods.Footnote 14 Our design choice was also motivated by the desire to create a uniform learning environment for both player types.

At the end of each period, the computer displayed both players’ expenditure choices, the winner of the contest as well as the subject’s own payoff. We include the full profile of expenditure choices to facilitate greater learning of the strategic incentives inherent in our environment. Instructions were detailed with illustrative examples to ensure subjects’ comprehension.

Subjects were randomly and anonymously re-paired at the beginning of each period. As our theoretical model is based on one-shot interactions, random matching helps reduce repeated game incentives during the experiment.Footnote 15 Subjects were also informed that their player type was determined randomly and thus each subject is equally likely to be type A or B in every period. We chose to randomly assign roles in each period to ensure that each subject in the experiment would become equally experienced in both roles. This served two purposes. First, it likely helped the subjects learn the strategic implications of their choices since they experienced the game from the perspective of both types. Second, in the all-pay auction it addressed fairness concerns since the equilibrium predicts that on average type A players earn higher payoffs than type B players.

Part 5 of the experiment was designed to elicit subjects’ non-monetary utility for winning. Following Sheremeta (2010), subjects were given 100 francs and were asked to invest for a prize of 0 franc. The conjecture is that a subject who derives utility from winning the contest will expend a strictly positive amount even though there is no monetary reward. This expenditure level is used as a measure of utility for winning. The session concluded with Part 6 where subjects answered a demographic questionnaire as well as a short survey about the intensity of emotions they experienced following particular outcomes of the contest.Footnote 16

At the end of the experiment, one period was randomly selected for payment in each of Parts 3 and 4. The sum of the earnings for these two periods as well as earnings from the contest for a zero prize were exchanged at the rate of 10 experimental francs \(=\) $1US. Subjects were also paid for one randomly selected lottery choice in each of Parts 1 and 2. Total earnings from the experiment, including a $5 participation fee, averaged $25.76 for sessions that lasted approximately 90 min.

5 Results

The results are organized as follows: We begin our analysis by focusing on round 1 expenditure and examine how a player’s potential ability to revise affects expenditure choices in the ex-ante simultaneous moves game. The next two sections focus on round 2. Section 5.2 examines the likelihood of revision and Sect. 5.3 describes round 2 expenditure choices. In Sect. 5.4, we compare the value of flexibility across the two contest types.

5.1 Round 1 expenditure

5.1.1 Comparison to equilibrium

We compare observed to predicted expenditure levels across types of players, \(\alpha\) treatments and in both types of contests. Figure 1 displays equilibrium expenditure levels and observed averages.Footnote 17 The first striking feature of the data is that aggregate expenditure is higher than predicted in all treatments. Formal tests confirm this visual observation. Table 3 reports average expenditure levels in all four treatments as well as the results of the non-parametric Wilcoxon signed-rank tests with \(n=8\) using data for from all periods. Note that we compute the averages within each session across multiple rematched groups and we treat each session average as an independent observation. We find that all differences from the equilibrium prediction are statistically significant at the 5% level or less.Footnote 18 Such significant overexpenditure relative to the risk neutral Nash equilibrium prediction emerges as an empirical regularity in the experimental literature on both lottery contests and all-pay auctions (Dechenaux et al., 2015).

Treatment effects

Result 1

Round 1 expenditure levels are higher than the equilibrium prediction.

5.1.2 Treatment effects

Our first comparative statics result focuses on the relative expenditure levels of the two player types. Hypothesis 1 states that a type A player will be more aggressive than a type B player in round 1 of the all-pay auction but expenditure choices are the same across player types in the lottery contest. Non-parametric tests included in Table 4 indicate that in both contests and for both values of \(\alpha\), average round 1 expenditure is not significantly different between type A and type B players (p-value \(\ge 0.12\)). Thus there is support for Hypothesis 1 in the case of the lottery contest but not in the all-pay auction.

Result 2

In round 1, there is no significant difference in the average expenditure choices of type A and type B players.

Our second comparative statics result examines the impact of the probability of informational leakage, \(\alpha\). We find strong support for Hypothesis 2. On the one hand, in the all-pay auction, round 1 expenditure is lower for both types of players when \(\alpha = 0.75\) compared to \(\alpha = 0.25\). Wilcoxon signed-rank tests included in Table 4 show that this difference is significant at the 5% level of significance. This stands in sharp contrast to the lottery contest where consistent with the theoretical predictions, we find no statistically significant difference across the two levels of \(\alpha\). We further support these conclusions by estimating a regression model that accounts for a potential time trend and subject heterogeneity. Using round 1 expenditure data for all 20 periods, we estimate the following equation

for each player type. The treatment effect is captured by a dummy variable (\(\alpha 75\)) that is equal to 1 if \(\alpha =0.75\) for subject i in period t and to 0 otherwise. To account for learning over time, we include the inverse of the period number (\(1/\text {period}\)). Finally, we include session dummies. The regression results are shown in Table 5. The estimates of the coefficient on \(\alpha 75\) reaffirm the results from the non-parametric tests. The regression results also indicate that expenditure declines over time as subjects become better acquainted with the strategic environment. This decline in overdissipation is a consistent observation in the existing literature (e.g. Fallucchi et al., 2013, Lugovskyy et al., 2010, Mago and Sheremeta, 2019).

Result 3

In the all-pay auction, for both types of players, round 1 expenditure is lower when \(\alpha = 0.75\) than when \(\alpha = 0.25\). In the lottery contest, round 1 expenditure levels are independent of \(\alpha\).

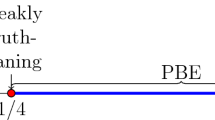

In order to better understand subjects’ round 1 behavior, we take a closer look at the distribution of expenditure choices and draw a contrast between the two types of contests. We begin with lottery contests where round 1 expenditure is predicted to be 25 for both player types and for both leakage probabilities. Figure 2 shows histograms of round 1 expenditure levels and indicates substantial dispersion in expenditure choices. Contrary to the subgame perfect equilibrium in pure strategies, we find that individual expenditure ranges from 0 to 100 with large standard deviations (see Table 3), resulting in averages significantly greater than 25 (see Result 1). This finding has been well documented in the literature and common explanations include non-monetary utility of winning (Sheremeta, 2013), confusion and mistakes (Anderson et al., 1998; Lim et al., 2014), risk and loss aversion (Shupp et al., 2013), impulsiveness (Sheremeta, 2018), maximization of relative payoffs (Herrmann & Orzen, 2008; Mago et al., 2016), gender differences (Mago & Razzolini, 2019) and heterogeneous beliefs (Konrad & Morath, 2020).

Round 1 expenditure distributions. The horizontal line shows the upper bound of the equilibrium distribution

An implication of these findings is that dispersion in expenditure choices can arise because of within-subject variation as well as between-subject heterogeneity. We follow (Chowdhury et al., 2014) and construct box plots of subject expenditure for each type of player and probability of leakage in the last ten periods of lottery contests. In addition to the median, interquartile range and outliers (blue circles), Fig. 3 also shows the mean expenditure level as a red diamond for each subject. As noted by Chowdhury et al., the red diamonds trace out the (inverse) cumulative distribution of mean expenditure. The figures provide compelling visual evidence of both within-subject variability, especially for Type B players when \(\alpha = 0.75\), and across subject heterogeneity.

We also compute the measures of within-subject dispersion and across-subject heterogeneity proposed by Chowdhury et al. (2014). We refer to the measures as \(D_s\), equal to the median of the standard deviation of expenditure by subjects in session s, and \(H_s\), equal to the standard deviation of median expenditure by subjects in session s. For session s, \(D_s\) measures the degree of within-subject dispersion and \(H_s\) measures the degree of across-subject heterogeneity. Table 6 reports the average values of these two measures as well as results from signed-rank tests with \(n=8\). Type B players generally exhibit greater average dispersion and heterogeneity than Type A players, although the only significant difference pertains to between-subject heterogeneity when \(\alpha = 0.25\). Hence, the factors that explain expenditure variability in lottery contests (Sheremeta, 2013) seem to impact the strategically disadvantaged Type B players at least as much as Type A players.

Finally, we note that in lottery contests expenditure choice of zero is not part of the equilibrium. However, Figure 2 shows that fraction of players, both type A and B, chose not to spend any resources.Fallucchi et al. (2021, p. 246) argue that “zero expenditures are indeed a frequent, sometimes modal, choice” in lottery contest. The documented rationales for this zero-expenditure strategy are (a) the best response to over-dissipation and (b) experiential learning or reinforcement heuristic ‘win-stay, lose-shift’ such that expenditures decline significantly with an increase in prior accumulated losses. In our framework, these remains valid for both player types. The more often a type B player loses, the more she will discourage positive expenditures up to non-participation. Similarly, when faced with repeated losses with round 1 expenditure choice, Type A would rather ‘drop out’ in round 1 and then best respond to the known rival’s choice in round 2.

Turning to the all-pay auction, in contrast to the lottery contest, dispersion is part of equilibrium behavior since both players randomize in round 1. However, Figs. 2 and 3 reveals some key departures from the prediction, especially at the extremes of the distributions. The prior literature indicates that bimodal bidding, whereby a large number of bids are concentrated near zero and near the value of the prize, is a common finding in the symmetric all-pay auction with complete information (Gneezy & Smorodinsky, 2006; Ernst & Thöni, 2013). We first consider expenditure choices between zero and five, which may be interpreted as quitting or dropping out. Note that a mass point at zero is part of the Pareto dominant equilibrium profile for type B players, but not for type A players.Footnote 19 Accordingly, in the experiment, we find that the proportion of choices between zero and 5 depends both on the player’s type and the probability of leakage. For type A players, the proportions are 20% when \(\alpha = 0.25\) and 37% when \(\alpha = 0.75\). For type B players these proportions rise to 34% when \(\alpha = 0.25\) and 44% when \(\alpha = 0.75\). Thus, compared to the Pareto dominant equilibrium, we find that type A players drop out of the contest too often (p-value \(=\) 0.04 when \(\alpha = 0.25\) and p-value \(=\) 0.02 when \(\alpha = 0.75\)), while for type B players the rates are either close to the equilibrium prediction (p-value \(=\) 0.18 when \(\alpha = 0.25\)) or sharply below it (p-value \(=\) 0.01 when \(\alpha = 0.75\)).

In addition to the equilibrium explanation, type B players’ choices at or near zero can be rationalized by the anticipation of all-pay loser regret, where losing bidders regret not expending zero (Hyndman et al., 2012). Type B players have a clear incentive to refrain from investing high amounts given the risk of a sure loss in case of an informational leakage. Indeed, if a type B player expends a moderately high amount, she runs the risk of being outspent and losing in round 2. The only way to avoid this loser regret is to invest nothing. This is also similar to the calm-down effect, wherein a weak player bids low in anticipation of being beaten by a stronger opponent later (Konrad & Leininger, 2007; Jian et al., 2017). Low expenditure choices by type A players, on the other hand, are not rooted in equilibrium. Nevertheless, it is plausible that behavioral biases responsible for bimodal bidding in existing experiments may drive expenditure choices in our contest environment as well. For instance, Gneezy and Smorodinsky (2006) attribute the observed bimodal distributions to a two-step decision-making process by the subjects, while Ernst and Thöni (2013) identify loss aversion from prospect theory as an explanation. In our framework, these low choices may also be responses to type B players’ observed choices. Other factors, including overplacement, whereby an advantaged player overestimates his chance of an easy win (e.g. Jian et al., 2017), may also have contributed to the high incidence of near zero expenditure by type A players.

We note that the large proportion of near-zero expenditures cannot be interpreted as evidence of tacit collusion in the all-pay auction. These near-zero expenditures are dispersed across the subject pool. Only 11 out of 64 (\(\alpha =0.25\)) subjects and 21 out of 64 subjects (\(\alpha =0.75\)) chose near-zero expenditures more than half the time. The vast majority of the subjects chose such a low expenditure level 25% of the time or less. We also find no evidence of subjects alternating across periods, taking turns to be the contest winner. Regression results in Appendix C in supplementary materials show that the likelihood of choosing near zero expenditure is more likely when \(\alpha =0.75\) and for Type B players, both of which are consistent with the equilibrium prediction in the all-pay auction. Finally, subjects’ payoffs are low, even in comparison to the equilibrium of the one-shot game, suggesting that even if these low expenditure choices were attempts at collusion, they were not successful.

Moving to the other extreme of the expenditure distribution, for type A players, round 1 expenditure choices between 95 and 100 are rarely observed (5% of the time when \(\alpha = 0.25\) and 6% when \(\alpha = 0.75\)). For type B players, the proportion is 8% when \(\alpha = 0.25\), but it rises to 19% when \(\alpha = 0.75\). The fact that almost one fifth of type B players’ expenditure choices are at or slightly below the value of the prize when \(\alpha = 0.75\) is a clear departure from the Pareto dominant equilibrium. In fact, for this value of \(\alpha\), Proposition 1 shows that the upper bound of a type B player’s equilibrium distribution is predicted to be equal to \((1-\alpha )V=25\). One may view this as the most meaningful departure from the equilibrium predictions because such behavior robs the type A players of their second-mover advantage. We offer two sets of explanations for this deviation. One arises from equilibrium behavior and the other is behavioral. First, it is possible to construct equilibria in which type B player places a mass point at \(V=100\) (see the Appendix). In these Pareto dominated equilibria, the size of the mass point at 100 can be as large as the value of \(\alpha\) and the size of the mass point at zero is reduced accordingly. Since a type B player’s expected payoff is zero regardless of which equilibrium is played, the Pareto criterion cannot rule out type B players using strategies from a dominated equilibrium. Stated succinctly, expending an amount equal to the value of the prize may constitute optimal behavior for type B players.

Second, a combination of utility of winning and fairness concerns likely drive some type B players to expend such high amounts, especially when \(\alpha = 0.75\). Specifically, given the structure of the game, it should be clear to the subjects that the type A player has a substantial second-mover advantage at the revisions round. As \(\alpha\) increases, it becomes more likely that this player will be able to exercise his advantage and earn a strictly positive payoff at the expense of the type B player. By expending 100, a type B player ensures a fair outcome in the sense that both players will likely earn payoffs of zero if the game proceeds to round 2. Similarly, type B players may also earn non-pecuniary utility of winning from thwarting type A players. Indeed these two explanations are consistent with the rationale proposed by Weimann et al. (2000) to explain punishing behavior by first movers in a highly competitive sequential contest with otherwise symmetric players. In fact in our experiment, when type B players choose an expenditure near 100, which occurred 18% of the time when \(\alpha = 0.75\), the type A players respond by dropping out in 65% of cases.Footnote 20\(^,\)Footnote 21

Round 1 expenditure dispersion and heterogeneity. The horizontal line shows the upper bound of the equilibrium distribution

In summary, our analysis of round 1 behavior reveals conformity to the equilibrium prediction in terms of comparative statics, but also some substantial quantitative departures. We now examine whether a type A player’s likelihood of revising expenditure depends on the type of contest and on the probability of informational leakage.

5.2 Likelihood of revisions

In both contests, on the subgame perfect equilibrium path, the likelihood that a player alters his round 1 expenditure choice does not depend on the treatment variable, \(\alpha\). Specifically, player A always revises his expenditure in round 2 in the all-pay auction while in the lottery contest, he never does. Table 3 includes the frequency of revisions for each treatment separately and reports results of the equilibrium comparison from non-parametric tests based on session averages. In our data for the all-pay auction, the overall rate of revisions is 87.5% and thus appears to be in line with the prediction. In the lottery contest, the observed rate of revisions is 71%. Given the off-equilibrium round 1 choices, it is not surprising that the data strongly reject the strict equilibrium prediction in the lottery contest. Nonetheless, comparing the all-pay auction to the lottery contest, we find that for both \(\alpha = 0.25\) and \(\alpha = 0.75\) treatments, revisions are more likely in the all-pay auction than in the lottery contest (Wilcoxon-Mann Whitney ranksum test with \(n=m=8\), p-value \(< 0.01\) if \(\alpha = 0.25\) and p-value \(= 0.04\) if \(\alpha = 0.75\)).

Next, we focus on the comparative statics across the \(\alpha\) treatments. Figure 4 shows the aggregate frequencies of revisions for each value of \(\alpha\) and it appears that \(\alpha\) has at best a small effect on the frequency of revisions. Formal tests included in Table 4 support these results. In the case of the all-pay auction, as predicted non-parametric tests fail to reject the null hypothesis of no difference between \(\alpha = 0.25\) and \(\alpha = 0.75\). However, in the lottery contest, the difference in the frequency of revision across \(\alpha\) treatments is small but statistically significant.

Frequency of revisions

Given that the observed frequency of revisions is so far removed from the equilibrium prediction in the lottery contest, we also run Probit regressions to better understand subject behavior. Results are shown in Table 7. Consistent with the non-parametric test results, the coefficient estimate of the "dummy for \(\alpha = 0.75\)" is significantly different from zero and positive in all specifications.Footnote 22 In the second column, we introduce the absolute value of the difference between round 1 expenditure and the best response. We also include the squared distance to allow for non-monotonicity. As one would expect, estimates reveal a hill-shaped relationship between the two variables. Subjects are most likely to revise when the distance to the best response is large, but not too large. If the distance is very large, subjects fail to revise. It is likely that these latter deviations from the optimal risk neutral decision originate from objectives other than expected payoff maximization, such as maximizing the probability of winning. In addition, the dummy variable for \(x_{A1}>x_B\) controls for whether type A is more likely than type B to win in round 1. The negative coefficient indicates that if the type A player’s round 1 choice exceeded the type B player’s, type A players are less likely to revise. Finally, the results in the third column show that both risk and loss tolerance are significant. The former is associated with a lower probability of revision, while the latter is associated with a higher probability. We note that effect of loss tolerance is small (a two point increase in the probability) and the coefficient is imprecisely estimated.

Result 4

Type A players engage in more frequent revisions in the all-pay auction than in the lottery contest. In the all-pay auction, the frequency of revisions does not depend on the probability of informational leakage. In the lottery contest, increasing \(\alpha\) has a small but positive impact on the likelihood of revisions.

5.3 Expenditure choices in round 2

5.3.1 Treatment averages

Table 4 and Fig. 1 show average round 2 expenditure by type A players across treatments. Similar to round 1 expenditure, we find that round 2 expenditure is significantly higher than the risk neutral equilibrium prediction. Signed-rank tests confirm that the difference between the observed and predicted expenditure levels is statistically significant for each of the \(\alpha\) treatments and for both types of contests.Footnote 23

In round 2, a type A player observes his rival’s expenditure and can respond to it. However, the nature of best response behavior differs substantially across the all-pay auction and lottery contests. Therefore in the next section, we analyze each contest separately.

5.3.2 Round 2 behavior in the all-pay auction

For the all-pay auction, regardless of risk aversion, a player’s best response is to outspend her rival by 0.01 as long as the other player’s expenditure is between 0 and 99.98. If the other player’s expenditure is 99.99, then the best response is either 0 or 100. Finally, if the other player’s expenditure is 100, then the unique best response is 0. Figure 5 shows type A players’ round 2 expenditure levels as a function of type B players’ round 1 expenditure. Panel (a) includes all observations and panel (b) only includes observations where the type A player actually revised in round 2. The circles depict the observed data and the x’s illustrate the theoretical best response which, as expected, mostly lies slightly above the 45-degree line.

Observed round 2 expenditure and best response in the all-pay auction

As mentioned earlier, the aggregate frequency of revisions by type A players is 87.5%, which is less than the strict prediction. When revising, type A players often outspend their rival by a small amount possibly greater than 0.01. Consistent with our earlier discussion, we consider outspending by an amount less than or equal to 5 and find that 78% of subjects play the best response. When conditioned on revising, this amounts to a rate of rational responses of 89%. Thus, in the all-pay auction, most of the round 2 expenditure levels are consistent with the best response, especially when they are revisions from the round 1 choice.

A puzzling fact is that 12.5% of the time type A players choose not to revise. Best response behavior implies that not revising was optimal in only 3% of the cases. The remaining 9.5% are broken down as follows. In 2.6% of the cases, the type A player’s round 1 expenditure was below the type B player’s and the type A chose to concede without revising (including 1.1% of cases where \(x_B=100\) and the type A player chose not to revise all the way down to zero). More importantly, in 6.9% of the cases, the type A player’s round 1 expenditure was already strictly above the type B player’s. In these cases, the type A player is outspending his rival with his round 1 expenditure, but fails to revise it downward to reduce his payment, thus burning money in the process.Footnote 24 Such decisions to not revise explain some of the excessive outspending visible in Fig. 5. Comparing the two panels shows that differences clearly in excess of 5 occur with a higher frequency in panel (a) than in panel (b).

5.3.3 Round 2 behavior in the lottery contest

For the lottery contest, on the equilibrium path a type A player does not revise his round 1 expenditure choice. In stark contrast, the observed frequency of revisions in our experiment is 71%. However, given that round 1 expenditure levels differ substantially from the risk neutral equilibrium prediction, this high rate of revisions may be rational given non-equilibrium round 1 behavior by both player types. A risk neutral expected utility maximizer would set his round 2 expenditure according to the following best response function

Rational play then suggests that risk neutral subjects should revise at the rate of 99% when \(\alpha = 0.25\) and 98% when \(\alpha = 0.75\). Figure 4 shows that the observed rate of revision is lower than the rational rate. Non-parametric tests confirm that this difference is statistically significant across both \(\alpha\) treatments (p-value \(=\) 0.01).

To gain further insight into how round 2 expenditure levels correspond to the best response behavior, we estimate a regression equation that is based on the above functional form. This approach is similar to Fonseca (2009). Specifically, for each value of \(\alpha\) we estimate

where \(x_{i,t}\) is a subject’s round 2 expenditure if the subject was of type A in period t and \(x_{-i,t}\) is the other player’s round 1 expenditure. We include the square root of the type B player’s expenditure to account for the predicted non-monotonicity. Table 8 shows the results using all observations in the first two columns and using only revised expenditure choices in the last two columns. For both values of \(\alpha\), the estimated coefficients on the rival’s expenditure and its square root are significant. The former is negative and the latter is positive, as predicted by the model.

Figure 6 shows the scatter plot of round 2 choices (depicted by circles), the graph of the above best response function as well as the expenditure functions estimated from the data for each value of \(\alpha\).Footnote 25 The figures show that round 2 choices are quite dispersed, whether or not they are revised from round 1. However, a large proportion of expenditure levels are on or above the 45-degree line (in panel (a), 72% of choices are above the type B player’s round 1 expenditure, with 19% of choices exceeding it by less than 5). This feature of the data clearly stands out in panel (b) which includes only revised choices, and therefore suggests that "outspending the rival", even slightly, drives the type A players’ expenditure choices. As a consequence, the opportunity to revise after observing the rival’s expenditure does not eliminate overexpenditure. Indeed for both levels of \(\alpha\), there is a statistically significant difference between observed revised expenditure and the risk neutral best response (a signed-rank test with \(n = 8\) rejects equality at the 1% level).

Observed round 2 expenditure, estimated and risk neutral best response functions in the lottery contest. The term \(\beta _3 (1/\text {period})\) is set equal to zero for the figures

A natural question to ask is, although revised expenditure levels differ from the risk neutral best response, are they closer to the best response than the initial choice, as learning direction theory would predict (Selten, 1998)? Given that a revision occurs, we compute the fraction of the time the revised expenditure was closer to the best response than the initial expenditure. The frequency is 57% when \(\alpha = 0.25\) and 46% when \(\alpha = 0.75\). Therefore, the subjects are no more likely to adjust their expenditure in the direction of the best response than away from it. Not surprisingly, subjects are more than twice as likely to move towards the best response when their round 1 expenditure is higher than their rival’s than when it is lower. Specifically, when a type A player’s round 1 expenditure is higher than her rival’s, she moves in the direction of the best response 77% of the time, but if round 1 expenditure is below the rival’s then only 33% of revisions are in the direction of the best response. Furthermore, when subjects move away from the best response, they almost always raise their expenditure. Specifically, given that a revision occurs and was further away from the risk neutral best response than the initial expenditure, the fraction of the time the revised expenditure was higher than the initial expenditure is 90% for \(\alpha = 0.25\) and 91% for \(\alpha = 0.75\). To summarize, half of the revisions that occur move away from the best response and they display two important characteristics. First, they occur mainly when the subject’s round 1 expenditure was below her rival’s. Second, they consist primarily in subjects raising their expenditure in response to their rival.

Result 5

In the all-pay auction, most of the revised expenditure levels are equal to the best response. In the lottery contest, the observed rate of revisions is lower than the rational rate and the revised expenditure levels are significantly higher than the risk neutral best response. Moreover, revisions are equally likely to move closer or move away from the risk neutral best response. When moving away from the best response, subjects tend to raise their expenditure compared to their round 1 expenditure.

Our results for expenditure and revisions behavior indicate that while comparative statics predictions are borne out by the data in the all-pay auction, there are substantial departures from the theory, especially in the lottery contest. In the next section, we examine the value of a type A player’s probabilistic informational advantage in each contest.

5.4 The value of flexibility

As stated earlier, the value of flexibility reflects the interplay between first mover advantage gained from commitment and second mover advantage afforded by observability. Our theoretical model predicts that in the lottery contest, the two effects cancel each other out and there is no value of flexibility. However, in the all-pay auction, the second mover advantage yields a value of flexibility that is strictly positive and increasing in the likelihood of reaching the revision round.

We begin our analysis by comparing the probability of winning across the two player types. Table 9 displays winning rates for type A players when the game ends in round 1 and when it ends in round 2. Overall, the observed behavior seems to conform to the prediction. In the lottery contest, both players are equally likely to win, especially in round 1. In the all-pay auction, the potentially informed player has a clear advantage even if the game does not reach round 2. The only key departure is the fact that in the all-pay auction, a type A player’s winning rate in round 2 is less than one.

The probability of winning has direct implications for the value of flexibility, as shown in the average payoff differences reported in Table 9. In all comparisons, on average, type A player earns a higher payoff compared to type B player. Consistent with Hypothesis 4, we find that for both values of \(\alpha\), there is greater value of flexibility in the all-pay auction than in the lottery contest. It is worth noting that despite the substantial departures in expenditure levels, these qualitative predictions from the model are largely supported by the data. Furthermore, in both all-pay auction and lottery contest, the value of flexibility is increasing in the probability of informational leakage.

Result 6

The value of flexibility is higher in the all-pay auction than in the lottery contest regardless of the leakage probability.

Next, we focus on the quantitative predictions as our benchmark for the value of flexibility. Table 3 contains Wilcoxon signed-rank tests comparing the observed levels with the equilibrium prediction. In the all-pay auction, there is a clear second mover advantage as the value of flexibility is positive. However, for both levels of \(\alpha\), the observed strategic advantage is significantly lower than predicted. A more distinct departure is observed in the lottery contest, where contrary to the prediction, the value of flexibility is positive for both levels of \(\alpha\) (although the difference is quite small and only marginally significant when \(\alpha = 0.25\)). Thus, our empirical results show that the committed player is substantially worse off than her rival in the all-pay auction and in the lottery contest with high incidence of informational leakages.

The reason for the positive value of flexibility in lottery contests appears to be as follows. In round 1, there is no significant difference in the average expenditure choice of type A and type B players and so, they are both equally likely to win (see, Table 8). However, contrary to prediction, type A players revise their choices 71% of time and thereby gain a slight edge in round 2. The likelihood of winning for type A players increases from equal odds to approximately 60%, and this is reflected in the higher average payoff of type A player relative to type B player. In summary, our empirical results show that the committed player is substantially worse off than her rival, both in the all-pay auction and in the lottery contest with high incidence of informational leakages.

As a final point, we consider the implications of our findings for average rent dissipation in both types of contests and for each of the \(\alpha\) treatments. Rent dissipation is equal to total expenditure. This variable may be of interest both to a contest designer who wants to increase the players’ effort levels or a social planner who wants to minimize rent-seeking expenditure. We compute average realized rent dissipation, which accounts for whether the contest employed round 1 or round 2 expenditure levels. Table 9 summarizes the results. Given the degree of overexpenditure in both contests, it is not surprising that rent dissipation exceeds the equilibrium prediction. More significantly though, we find that a higher probability of informational leakage reduces rent dissipation in the all-pay auction but has no impact in the lottery contest. In fact, the decrease in expenditure in the all-pay auction is large enough that rent dissipation becomes significantly lower than in the lottery contest. This is notable because all-pay auctions reliably generate higher expenditure than lottery contests when players are symmetric (Davis & Reilly, 1998; Faravelli & Stanca, 2014) but the evidence is mixed when players are asymmetric (Orzen, 2008; Duffy & Matros, 2021).Footnote 26

6 Conclusion

In today’s world where informational leakages are a norm rather than an exception, the question of observability and its impact on behavior assumes increased importance. In this paper, we study how the strategic asymmetry between players that emerges from a probabilistic information leak interacts with the degree of competitiveness, as captured by different types of contests. Our theoretical model predicts that in the lottery contest, the information leakage confers no strategic advantage on the recipient of the information. However, in the all-pay auction, the ability to observe the rival’s action and revise expenditure is highly advantageous. Furthermore, this advantage is increasing in the (exogenous) probability of informational leakage. Thus, our model predicts that the value of flexibility is positive and increasing in the all-pay auction, but not in the lottery contest.

While some of these predictions are borne out in our laboratory data, the substantial empirical departures we observe have important implications for the contest literature. First, we find that an informational leakage about the rival’s action and the subsequent opportunity to revise own expenditure do not significantly reduce the phenomenon of excess dissipation (relative to the equilibrium with risk neutral players). In the all-pay auction, we find that the distribution of expenditure choices exhibits a pronounced bimodal pattern, similar to prior experiments on symmetric all-pay auction with complete information. In the lottery contest, overexpenditure occurs both ex-ante and ex-post, when the informed player knows his rival’s choice. Thus in our rent-seeking contests strategic asymmetry between players does not contribute to reducing overdissipation. Second, in both contests, a significant value of flexibility emerges from the potential observability of the rival’s action and this value is strictly increasing in the probability of informational leakage. Results in this experiment suggest that the option to ‘revise and resubmit’ confers a strategic advantage on the potentially informed player not only in the all-pay auction (as theory predicts), but also in the lottery contest if the probability of leakage is sufficiently high. Thus, consistent with the literature, we find that strategic asymmetry between players creates a strong discouragement effect for the potentially disadvantaged player. Third, several studies have shown that when players are symmetric, all-pay auctions generate higher expenditure than lottery contests (e.g. Davis and Reilly, 1998, Faravelli and Stanca, 2014). In our contests, players have symmetric costs and valuations, but a probabilistic information leak creates a strategic asymmetry between players. We find that a higher probability of informational leakage reduces rent dissipation in the all-pay auction to such an extent that it becomes significantly lower than in the lottery contest. Thus, consistent with prior literature and as predicted by our model, which contest mechanism generates the largest aggregate expenditure depends on the structure of the game.

The results in this paper help to improve our understanding of how observability influences behavior in competitive situations, with possible applications to industrial espionage and the protection of sensitive data. We add to the existing experimental literature on the value of commitment, which for the most part has focused on market games with strategic complements (Morgan & Várdy, 2004). Our experiment also contributes to the literature on heterogeneity and exogenously given advantages in contests (Chowdhury et al., 2022) as well as to the discussion of contest mechanism selection (Faravelli & Stanca, 2014; Corazzini et al., 2010).

Our results also offer some avenues for future research. One possible extension is to examine the role of incumbents in design or innovation contests (Jiang et al., 2022). In our model, the identity of the type A player, the potentially informed player, is known to both players. This plausibly relates to a scenario where player B is an entrant and player A is an incumbent who owes his informational advantage to an existing relationship with the contest designer. Another possible extension would be to examine how ex-post asymmetry emerging from informational leakage counteracts an ex-ante asymmetry between players resulting from differing costs or valuation for the prize. This would be especially useful to researchers and practitioners interested in mechanisms that level the playing field to restore competitive balance. Finally, in this paper we examine a probabilistic informational leakage from a single player. It would be interesting to analyze the case of two-sided leakages in which both players may have the opportunity to revise. Unlike in this experiment, with two-sided leakages, the players are symmetric and neither has a strategic advantage. The behavioral impact of informational leakages and revision opportunities in this environment is a question for future research.

Notes

An example in baseball involves the St Louis Cardinals’s hacking of a database maintained by the Houston Astros (New York Times, 6/16/2015). Employees at the Cardinals allegedly gained access to the Astros database by using the passwords of former Cardinals managers who had since been hired by the Astros. Similarly, in 2004, WestJet executives used a former employee’s passwords to tap into an internal Air Canada site and cull sensitive passenger data. In 2001, third party contractors rummaged through trash cans outside the offices of Unilever and provided confidential, though legally obtained, information to its competitor, Procter and Gamble.

For example, Toshiba entered into partnership with Lexar in 1997 and one of its executives sat on Lexar’s board of directors. Through that position Toshiba gained access to the Lexar’s technology and business plans, while at the same time it was working with Lexar’s rival, SanDisk Corporation, to jointly develop flash memory chip (New York Times, 3/25/2005).

Consider, for instance, the incident involving Hillary Clinton and Bernie Sanders during the 2016 Democratic presidential primary. Because of an error by a third party, members of Bernie Sanders’s staff accidentally obtained access to strategically sensitive information belonging to the Clinton campaign. As reported by NBC News, “The breach happened after a software error at the technology company NGP VAN, which provides campaigns with voter data.” As a result of the glitch, at least four individuals affiliated with the Sanders campaign including the campaign’s national data director “conducted searches and saved the Clinton campaign’s lists of potential voters" (NBC News, 12/18/2015). Another instance is where database of Virgin Media Co. was left unsecured and accessible online for ten months. The company reported that the database had been "incorrectly configured" by a member of staff not following the correct procedures and the information was accessed “on at least one occasion" by an unknown user (BBC News, 03/05/2020).

For instance, in the above examples, one can argue that the Astros team was more vulnerable to an informational leakage than the Cardinals, due to the Astros’s ownership of the critical database. Similarly, given th3 Sanders campaign’s purported technological advantages, it was better positioned to exploit any potential data leakage.

Fu & Wu (2022) argue that ‘the comparison of all-pay auctions and lottery contests deserves to be reexamined when the underlying contest models are allowed to be infused with design elements: When a contest designer is able to award preferential treatment to contestants that manipulates contestants’ relative competitiveness on the playing field to correct for the anti-competitive effect of heterogeneity, would a generalized lottery contest-with inherent noise to balance the playing field-still outperform an all-pay auction?”

Balafoutas et al. (2021) state that the evidence from the field is mixed and inconclusive. For instance, a number of studies were unable to replicate the results of Brown (2011). These include Guryan et al. (2009) and Connolly and Rendleman (2014) who examine golf tournaments in different contexts and Babington et al. (2020) who in addition the original environment of men’s golf include women’s golf and World Cup Alpine skiing for both genders. Possible reasons for these discrepancies are inadequate experimental control (e.g., results are not robust to changes in sample specification) and the presence of externalities. Our lab environment, on the other hand, provides cleaner evidence of the discouragement effect.

Matsui (1989) examines informational leakages of supergame strategies prior to the start of an infinitely repeated game. Kamada and Kandori (2020) derive necessary and sufficient conditions for cooperation to be sustained in what they call revision games. In a revision game, players adopt initial actions but opportunities to revise arise randomly until a deadline is reached, at which time players must make a final commitment to an action. In this model, players recognize that revisions may be used to punish deviations from cooperation.

In the Appendix in online supplementary materials, we examine the equilibrium predictions when player A is only allowed to revise the expenditure upwards. We show that the subgame perfect Nash equilibrium does not change in case of lottery contest, and is qualitatively similar in case of all-pay auction.

Specifically, there exist other equilibria in which the support of player B’s equilibrium distribution is \([0,(1-\alpha )V] \cup \{V\}\) and this player has mass points both at zero and V. In some of these equilibria, the ranking of expected expenditure levels across players and the comparative statics results with respect to \(\alpha\) differ from those in the Pareto dominant equilibrium. We include a discussion in the section on experimental results.