Abstract

Governments around the world are seeking an effective mechanism to cope with air pollution and climate change. The allocation of emission allowances, which is a key mechanism in the cap-and-trade system, is an important and intricate puzzle faced by environmental agencies. In this paper, we build a Stackelberg model to explore the emission allowance allocation mechanism design from an operations perspective. We demonstrate the feasibility and effectiveness of a linear emission allowance allocation mechanism. The results show that the emission allowance allocated by the government should always be insufficient to satisfy the ex-post emission demand at the industry level, even with low-carbon investment. To analyze the impacts on firms’ decision-makings, we explore a scenario in which two firms in the same industry sell a homogenous product to the market. The optimal low-carbon investment and production decisions are significantly affected by these market and carbon-related factors. Numerical examples are presented to further demonstrate the results that our paper has derived and investigate the optimal operational decisions of the two firms. Several meaningful management insights on allocation mechanism design and low-carbon operations of firms are obtained.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In the twenty-first century, many Asian countries, such as China, India and Iran, have recently been disturbed by serious haze and smog, which is similar to the prolonged London smog event in 1952. In 2012, one of every nine people died from pollution-related conditions, among which approximately 3 million deaths were ascribed solely to ambient air pollution (WHO 2016). The Intergovernmental Panel on Climate Change (IPCC) report showed that climate change might cause an increase in ill-health in numerous regions. In addition to the damage to human health, these environmental issues that are mainly triggered by carbon emissions upset the ecological balance and impede economic growth. Hence, it is an inevitable trend for governments to cooperate to reduce emissions. In 2014, the Asia-Pacific Economic Cooperation (APEC) Economic Leaders’ Meeting held in Beijing, China and the U.S., the world’s first and second largest energy consumer and \(\hbox {CO}_2\) emitter, reached a ‘historic’ deal to cut emissions (MacLeod and Eversley 2014). According to the United Nations Framework Convention on Climate Change (UNFCCC), developed and developing countries will jointly shoulder the common but differentiated responsibilities for emission reduction (Pan et al. 2014; Kober et al. 2015).

Over the past several decades, rapid economic growth with a great deal of energy consumption has produced enormous carbon emissions, which are regarded as the main culprits for global warming. As more people have realized the urgency of addressing carbon emissions, it is both a golden opportunity and a bound duty for governments to implement policies for emission reduction. Taking China as an example, the State Council’s 13th Five-Year Plan for controlling greenhouse gas emissions has received extensive support from the public, and the Chinese government committed to cut its \(\hbox {CO}_2\) emissions per unit of GDP by 40–45% by 2020 (Yi et al. 2011). With the public worldwide paying more attention to this problem, various carbon regulations are designed and enacted in different regions, such as the well-known carbon tax, strict cap and cap-and-trade policy. Compared with the carbon tax and strict cap policies, the cap-and-trade system comprehensively utilizes the governmental control and market regulation, thereby providing a more efficient and systematic way to achieve the emission reduction target. Because of its flexibility and ease of implementation, the cap-and-trade system has received increasing attention from both scholars and government agencies (Tang and Zhou 2012). In practice, the cap-and-trade policy is widely adopted by many countries. To date, the European Union Emissions Trading System (EU-ETS) is the first and largest carbon trading system. China has launched its pilot ETS in 7 regions in 2013 and the national ETS will be established in 2017 (Zhou and Wang 2016). The Shenzhen carbon trading market is the first pilot emission trading system in a developing country.

Under the cap-and-trade policy, an emission cap is allocated for free to a firm by the government in each period. The emission trading system can be seen as a flexible tool that not only satisfies the requirement of each firm but also falls short of the total limited emission cap (Song et al. 2015). The carbon emission is an output of activities of firms, including procurement, production, inventory management and transportation (He et al. 2015; Song et al. 2016). Therefore, the emission allowance has become an essential and scarce operational resource in the cap-and-trade system, and firms have put growing emphasis on how the limited emission allowances would be allocated to them. Under the pressure of carbon emission control, firms can buy emission allowances in the carbon market and take low-carbon efforts to reduce carbon emissions. In this paper, we incorporate these two ways into the model setting to explore the optimal cap allocation mechanism.

1.1 Inspiration from the real case

In light of the practices in carbon emission trading markets in European Union and China, the free allocation of emission allowances accounts for a huge percentage at an earlier stage. Free allocation could relieve the cost pressures of firms and thereby preserve their competitiveness (Liao et al. 2015; Chiu et al. 2015). Hence, even if the proportion of auctions increases over time, free allocation will still be deemed a mainstream choice by 2020, especially by those countries that are exploring whether to establish a carbon trading market (Hong et al. 2014). Within the free emission allowance allocation, many studies have developed various allocation methods, but debates about existing allocation methods should be considered. The method of grandfathering, whereby free emission allowances are allocated based on the emission level of a firm in a reference year, is widely used by many countries. Nevertheless, it still has led to two problems: windfall profit and distorted investment decision (Ahn 2014). Questioning the sharp fluctuation in carbon price, it is believed that the traditional grandfathering method would have some hysteresis. For example, Hubei carbon trading marketing, the second largest pilot in China, has a drastically first-increases-then-decreases process in carbon price since 2014, which is attributed to the unreasonable allocation from grandfathering. The emission allowances granted to a firm with lower carbon emissions are less than those given to a firm with a higher carbon intensity. It is difficult for new entrants to achieve their emission reduction targets under this allocation scheme. In reality, governments have not yet found a perfect emission allowance allocation method. Thus, emission allowance allocation design is a difficult and core issue and is the primary concern of this paper.

The emission allowance allocation is the most difficult challenge in the design of a cap-and-trade system (Jin et al. 2014). To meet the national carbon emission reduction commitment, some scholars have confirmed that dividing emission reduction tasks among different provinces, regions, and industries is a wise choice for the government (Wang et al. 2013; Zhang et al. 2017). Several other researchers have also studied emission allowance allocation issue in the power, chemical, road transport industry and so on (Cong and Wei 2010; Qiu et al. 2017; Han et al. 2017). However, the existing studies have rarely considered the micro perspective and have not been concerned with the firms’ possible reaction. In addition, China is in the preparation phase of transitioning from carbon trading pilots to a national carbon trading market. National Development and Reform Commission (NDRC) indicates that the initial national carbon market should cover high energy-intensive industries, such as the chemical, non-ferrous metal, cement, power, and aviation industries. Because of the different attributes and positions of various industries in society, carbon emission reduction missions assigned to them should consider their different energy saving potentials, effects on social development and other factors. In both the 12th and 13th Five-Year working Plans, the State Council set different energy saving and emission reduction standards for each industry. For example, the cement industry is requested to reduce its energy consumption by 7% in 2020 compared to 2015, whereas the energy consumption of the pulp and paper industry must decrease by 50%. Because of the different industry-based emission reduction standards, the pressure among these industries changes significantly, which could accelerate industrial transformation orderly. In accordance with the above theoretical investigations and practical examples, we attempt to explore the carbon emission allowance allocation mechanism at the industry level in the context of newsvendor model.

1.2 Research question identification

Under the cap-and-trade policy, the more emission allowances are allocated to a firm, the more development chances and better competitive advantage this firm will have. From the perspective of governments, resolving the tension between economic development and environmental deterioration is always a serious challenge. On the one hand, more green processing leads to less carbon emissions, which means a decreased demand for emission allowances. On the other hand, emission allowances are equivalent to a subsidy in some sense, so it seems unreasonable to dampen the enthusiasm of these low-carbon firms by cutting their carbon emission allowances. An executable and scientific emission allowance allocation mechanism is urgently needed by governments. Motivated by the above considerations, this paper focuses on the following research questions:

-

1.

How should a carbon emission allowance allocation mechanism be designed from a low-carbon operations perspective? Which factors affect the allocation of emission allowances and how do they work?

-

2.

What is the optimal decisions of specific firms under our industry-level allocation mechanism? How can this allocation mechanism make a low-carbon improvement of these firms?

Considering the above factors collectively, we solve this emission allowance allocation problem using a game-theoretic analytical model. We select economic performance and carbon emission as the two main indexes underlying the government goal. Through the analysis, a linear form of emission allowance allocation mechanism is demonstrated to be a desirable and executable choice. The effect of this mechanism is verified by simulating the industry with two heterogeneous firms. The optimal low-carbon operations of firms are revealed in this mechanism. We derive and discover several interesting management insights and driven force on our mechanism design and firms’ low-carbon operations.

1.3 Contribution

contributions of our research can be divided into three aspects. First, although there are many studies that have incorporated carbon emission constraint into operations management, the emission cap is usually assumed to be exogenous. However, the emission allowances should be related to the firms’ actual operational decisions in reality. To solve this problem, a new Stackelberg game is constructed to investigate the interaction between the government and the industry. The industry-level emission allowance allocation mechanism is designed and obtained from a low-carbon operations perspective, where the emission allowances are combined with the industry average carbon performance. Second, we discuss the emission allowance allocation for a unit product at a unified industry level while jointly considering both fairness and efficiency principles (Zhou and Wang 2016). The extant literature usually examines the total emission allowances without considering firm actual production, so the firm may simply reduce production to achieve its carbon reduction target which is incongruent with the original intention. In contrast, our paper studies the emission allowances per product, which is more practical and can avoid the above problem. Third, we reveal the interaction between the mechanism design and the firms’ operational decisions which rarely receives attentions in most extant studies. In this paper, we explore how the government should allocate emission allowances according to the industry’s possible reaction. At present, some pilot programs in China have tried to make allocation rules from the perspective of industry, and our results can provide decision support for the relevant authorities. The results concerning the operational decisions of different types of firms also can guide these firms to adopt better low-carbon choices in practice. Some results of our paper are in accordance with the conceptual design of the cap-and-trade policy.

The remainder of this paper is organized as follows. Section 2 provides a literature review of related research, and Sect. 3 presents the problem characteristics and describes the notations. In Sect. 4, we develop an analytical model to formally explore the optimal emission allowance allocation mechanism. In Sect. 5, we study the impacts of this optimal mechanism on the operational decisions of firms by simulating an industry with two firms. Numerical examples are provided in Sect. 6. Section 7 gives a further discussion to conclude the paper.

2 Literature review

Facing the reality of climate change caused by carbon emission, academics and practitioners have become increasingly conscious of carbon pollution concerns. This paper is closely related to two main streams of literature: (i) operational decisions under the cap-and-trade policy and (ii) the design and effect analysis of emission allowance allocation. In this section, we review some relevant research in each stream of literature and indicate how this paper differs from previous studies. The analytical framework of literature review is summarized in Table 1.

The cap-and-trade policy has been regarded as an effective way to reduce carbon emissions (Jaber et al. 2013; Xu et al. 2017; Xia et al. 2017). There are considerable literatures focusing on traditional operational decisions under the cap-and-trade policy (Brandenburg and Rebs 2015; Chang et al. 2015; Rezaee et al. 2017). Benjaafar et al. (2013) developed some stylized theoretical models under low-carbon policies to illustrate how carbon emission concerns could be integrated into operational decision-making. They showed that the operational adjustments and collaboration had a significant effect on carbon emission reduction. Focusing on minimizing carbon emissions in material procurement and logistics, Kaur and Singh (2016) proposed a dynamic non-linear mixed integer model under a cap-and-trade system. Toptal and Çetinkaya (2017) presented decentralized and centralized models for the buyer and the vendor to determine their ordering/production lot sizes under cap-and-trade and tax. Du et al. (2015) introduced an emission-dependent supply chain and showed that the permit supplier would lower the carbon price to encourage the manufacturer to increase production as market volatility increases. In addition to the concerns on the traditional issues under the cap-and-trade policy in the abovementioned operational research, the nascent literature has incorporated low-carbon investment into a decision-making framework, which is studied in this paper.

In the field of operational decisions with emission trading, some scholars have gradually focused on low-carbon efforts of firms. Du et al. (2016) investigated the optimal production decisions of emission-dependent manufacturer in making a tradeoff between emission trading and emission processing. They confirmed that if the consumers’ low-carbon preference exceeds a certain threshold, the manufacturer would prefer to choose low-carbon processing. Drake et al. (2016) studied how emissions tax and cap-and-trade regulation affect a firm’s technology choices and capacity decisions, where both the clean and dirty technologies are owned by the firm. The impact of a constant or growing price floor on investment decisions is examined by Brauneis et al. (2013). Their results showed that a carbon price floor could induce earlier low-carbon investment. Toptal et al. (2014) formalized a framework of joint decisions on inventory replenishment and emission reduction investment under three carbon policies. They found the investment could make the retailer further reduce emissions under the cap-and-trade policy, whereas the annual emissions level will not decrease under a fixed emissions cap policy. Sheu and Li (2013) adopted two strategies of carbon permit purchasing and green investment in their model setting, and observed that the profit of cost-efficient firms would increase as the green investment increases. By studying the investment in sustainable products, Dong et al. (2016) concluded that the optimal operational solutions would be greatly influenced by the investment. In contrast to the above studies, this paper attempts to investigate the government’s industry-level cap allocation mechanism from a low-carbon operations perspective. Treating firms in the same industry as a whole, we focus on the interaction between the firms’ operational decisions and the cap allocation mechanism set by the government. Moreover, we analyze the optimal decisions of two firms to simulate the entire industry and derived the low-carbon performance in this proposed allocation mechanism.

Another stream of literature closely related to this paper concentrates on the design of emission allowance allocation mechanism. The question of how to distribute emission allowances has aroused many scholars’ interests since the early 1990s. Zhou and Wang (2016) classified the existing emission allocation methods into four categories, i.e., indicator [such as the population-based rule in Zhou et al. (2013) and emission-based indicator in Schmidt and Heitzig (2014)], optimization (Gomes and Lins 2008; Wang et al. 2013), game theoretic (Filar and Gaertner 1997; Liao et al. 2015) and hybrid approaches (Yu et al. 2014; Zhang et al. 2014). Many scholars have analyzed this issue from different dimensions of the country and region (Winkler et al. 2002; Chen and Lin 2015). Some of the literature has also studied the emission allowance allocation from an industry perspective. Using the equity and efficiency principles, Zhang and Hao (2017) constructed a comprehensive index to allocate emission quotas among the 39 industrial sectors of China. Zhao et al. (2017) used an integrated method on the basis of an input-output analysis to distribute emission allowances among China’s 41 industries. Both of them believed that the emission reduction capacity, responsibility and potential, and energy efficiency should be considered by policy-makers in allocating emission allowances. A Stackelberg game model and hybrid algorithm were proposed by Hong et al. (2017) to investigate a policy-making problem considering environmental bearing capacities. Compared to the studies mentioned above, this paper belongs to the game theoretic category according to the classification of Zhou and Wang (2016). However, differing from the macro-level search for the optimal allocation of emission allowances or reductions among countries, regions or firms, this paper proposes a game-theoretic analytical model to explore the interaction between the government and the industry from a low-carbon operations perspective.

Within the research of emission allowance allocation, the influence of the detailed allocation policies has been widely discussed. Zhao et al. (2010) created a nonlinear complementarity model to investigate the effect of different allocation methods on investment, operations, and product pricing decisions in the electric power markets. Ji et al. (2017) found that the benchmarking can push manufacturers/retailers to produce/promote low-carbon products more effectively than the grandfathering with comparing the impacts of two allocation methods on the firm’s decisions, profits and social welfare. Zhang et al. (2015) developed a multi-stage profit model to explore how China’s carbon allowance allocation rules affect product prices and emission reduction behaviors of enterprises. They noted that when the carbon emission cap decreases, the firm will reduce carbon emission more actively. When the emission allowances depended on the output, Rosendahl and Storrøsten (2015) observed that the output-based allocation would stimulate investment in clean technologies under ex-ante regulation, because emission subsidy led to more production that increases carbon price. Free emission allowance allocation still plays a dominant role in emission trading scheme in covered countries. Goulder et al. (2010) concluded that allocating fewer than 15% of the emission allowances freely could prevent profit losses in the most vulnerable U.S. industries. However, these industries would be overcompensated if all of the allowances were free for them. Consistent with this insight, we also conclude that the allocated emission allowances per product granted by the government should always be less than the ex-post emission demand at the industry level. In most of the abovementioned studies, the emission cap is often regarded for simplification as an exogenous parameter, which both is impractical and produces some arguable conclusions. In contrast to these papers, we focus on the emission allowance allocation mechanism design in which the emission allowance is directly related to the firm’s low-carbon performance. Moreover, we investigate the effect of the emission allocation mechanism on the firm’s operational decisions.

3 Problem characteristics and notations

This paper focuses on the emission allowance allocation mechanism design problem concerning the industry’s carbon emission reduction level. The low-carbon efforts of every firm in the same industry are included in the mechanism. This feature of the allocation mechanism helps the government allocate emission allowances accurately according to the actual carbon emission. Compared with the independent allocation of emission allowances to each firm with respective emission allocation methods, our method is more practicable and fairer in that the government implements a unified rule for all firms in the same industry. For example, although the allocation plans of each pilot in China are different, the government has set similar allocation rules for firms of the same industry in a certain pilot region (Xiong et al. 2017). The historical emissions-based allocation methods are used in Beijing, in which the government considers both average emissions and decline coefficient while allocating allowances to existing manufacturing facilities or other industrial and service sectors. In addition, each firm has an equal right to get the same carbon emission allowances per product in the same industry.

In this research, we consider an emission-dependent supply chain with a government and a certain industry. We develop a Stackelberg game to approximately simulate the relationship between the two participants. First, the government announces the emission allowance allocation mechanism. Then, the industry makes operational decisions on production quantity and emission reduction investment to maximize its profit under this mechanism. We assume that the players are fully rational and that all the information is common knowledge to all players. Therefore, the government can choose the optimal emission allowance allocation mechanism based on the anticipated reaction behavior of the industry.

The government is dedicated to design an efficient emission allowance allocation mechanism to balance economic and environmental goals. We use \(K\left( {\rho \left( \theta \right) } \right) \), which can be interpreted as the carbon emission allowances per product, to represent this mechanism. Meanwhile, \(\delta \) stands for the government’s weighting factor on the environment. It reflects the marginal environmental damage (Meunier et al. 2014) and takes a different value in different industries. With limited emission allowances, the eco-friendly industry is motivated to enhance the green attributes of products by taking low-carbon efforts. Let \(\theta \) denote the industry’s investment per product. The carbon emissions per product with and without the low-carbon investment are assumed to be \(e\left( \theta \right) \) and \({e_o}\), respectively. Then, the carbon emission reduction rate can be expressed as \(\rho \left( \theta \right) = 1 - \frac{{e\left( \theta \right) }}{{{e_o}}}\), i.e., \(e\left( \theta \right) = {e_o}\left( {1 - \rho \left( \theta \right) } \right) \), which satisfies \(\rho '\left( \theta \right) > 0,\rho ''\left( \theta \right) < 0,\rho \left( 0 \right) = 0,\mathop {\lim }\nolimits _{\theta \rightarrow \infty } \rho \left( \theta \right) = 1\). It also implies that the more the industry spends on low-carbon investment, the higher the carbon emission reduction rate is. Hence, the inverse cost function is a concave function that is increasing in \(\theta \), where \(0 \le \rho \left( \theta \right) < 1\).

The production cost of unit product is c, and the corresponding price is p. The industry determines the production quantity q according to the market demand that may occurs. During the selling season, the industry faces a stochastic demand x, which follows a probability density distribution function \(f\left( \cdot \right) \) and cumulative distribution function \(F\left( \cdot \right) \). For the sake of simplicity, we suppose that the holding cost of residual inventory, the salvage value of unsold product and the shortage cost can be ignored. In addition, we assume that there is no gap between the carbon purchase price and the sale price in the carbon trading system. This assumption is widely used in some literatures about the cap-and-trade policy (Zhang and Xu 2013; Chang et al. 2015). The industry can buy or sell the emission allowance in the carbon emission trading system with a carbon price of \({p_e}\), which for simplicity is assumed to be an exogenous parameter. The transaction cost of carbon emission allowances in this system is also ignored.

In investigating how the government should design the mechanism, the following points should be noticed. With a higher carbon reduction rate, the industry would have a better carbon performance, indicating that it requires less carbon permit. However, it is obviously unfair to arbitrarily take away the emission savings, which will discourage low-carbon firms. The government must design a detailed allocation mechanism to promote the entire industry carbon reduction without hurting the low-carbon firms’ motivation. From now on, we concentrate on an allocation mechanism design and carbon related decisions. The decision variables and the model parameters are summarized in Table 2.

4 Model formulation and solution analysis

In this section, we consider both the ecological protection and industry benefit to explore the optimum emission allowance allocation mechanism chosen by the government. The emission allowances are allocated to the industry with no fees charged. To address this issue, we construct a linear form of the emission allowance allocation mechanism and discuss the feasibility and effectiveness of this form. At the same time, we will investigate how the industry responds to the emission allowance allocation mechanism.

Next, the equilibrium solution of this game is obtained via backward induction. On the basis of the above statement, the industry’s total amount of emissions, the allocated total carbon emission cap and the quantity of tradable emission allowances are given by \(qe\left( \theta \right) ,qK\left( {\rho \left( \theta \right) } \right) \) and \(q\left( {K\left( {\rho \left( \theta \right) } \right) - e\left( \theta \right) } \right) \), respectively. With the emission allowance constraint, firms will assume environmental responsibility and make a choice between low-carbon investment and emission purchase, satisfying the production requirement. Therefore, the total cost per product includes production cost and carbon-related cost. The profit function of the industry is as follows:

Economic growth and environmental protection are the two main goals of the government in this paper. The economic goal is represented by \({G_1}\) and the environmental goal by \({G_2}\). In line with actual practice, the weights of these two goals vary for different industries owing to the different positions and developmental levels of these industries in society. Here, we take the total carbon emissions of production to capture environmental damage. Consequently, the economic goal function and the environmental goal function are given as follows:

This paper formulates the negative environmental impact as \(\delta {G_2}\), where the parameter \(\delta \) reflects the monetary loss of environmental disruption caused by one unit of carbon emission (Du et al. 2017b; Hong et al. 2017). This parameter alternatively indicates the government’s cost of addressing environmental problems. The higher \(\delta \) is, the more financial and human resources the government should spend on environmental control. The government should weigh the economic and environmental benefits, so the objective function of the government has the following structure:

As mentioned before, equity and efficiency principles should be applied proportionately in designing a carbon allocation mechanism. Based on the industry average performance of carbon reduction, our mechanism focuses on the emission allocation for a unit product. The government hopes to stimulate the industry to raise the carbon emission reduction level while keeping a careful balance between the actual demand and reward. Here, a linear form conjecture is tentatively proposed to reflect the above relation, which is described as follows:

In this setting, a is a linear coefficient and should be derived from the analysis. \({K_o}\) is the initial emission allowances without a low-carbon investment and \({\rho (\theta )}\) represents the industry-level carbon emission reduction rate. Substituting Eq. (5) into Eq. (1), the profit function of the industry becomes

Next, we study the decision problem of the industry. Under the specific carbon emission regulation, the industry will choose the low-carbon investment per product and make the production decision. After verifying the Hessian matrix (see “Appendix A”), the optimal low-carbon investment and production quantity can be derived by the first order differential condition of the profit function as follows.

where \({q^*}\left( {{K_o},a} \right) \) and \({\theta ^*}\left( {{K_o},a} \right) \) are the optimal reaction functions of the industry given \({K_o}\) and a. The optimization problem faced by the government is:

Then, the first-order conditions of the objective function of the government with respect to \({K_o}\) and a respectively are:

Equations (7) and (9) above are simultaneously solved to yield the equilibrium solutions of this game. The optimal decisions for the government and the industry are:

Through the analysis, we conclude that the linear form of emission allowance allocation mechanism is credible and valid, which is useful and executable to encourage the industry to assume environmental responsibility. As a result, carbon emission is significantly reduced. In this section, the low-carbon investment and production quantity are also uniquely determined. The emission allowance allocation mechanism takes the following form:

Proof

See “Appendix A” for detailed proofs and for a further discussion of the existence and uniqueness of the solutions. \(\square \)

In this paper, we also try to explore other forms of the emission allowance allocation mechanism; for example, we have considered and verified the quadratic form as a natural extension. After a systematic derivation, however, we find that the strict quadratic form has no feasible solution. The linear form is a special case obtained when the quadratic term coefficient is zero, which also demonstrate that the linear form of the allocation mechanism is feasible in reality (the detailed analysis and results are shown in “Appendix B”). Owing to the effectiveness and ease of implementation of the mechanism design, we focus on the linear form of allocation mechanism to obtain a deeper analysis.

Proposition 1

In this mechanism, the carbon emission allowances depend on the weighting factor \(\delta \), carbon price \({p_e}\), and actual carbon emissions \(e\left( \theta \right) \). The final emission allowance allocation mechanism is as follows:

To guarantee the positivity of \(K\left( {\rho \left( \theta \right) } \right) \), \({p_e}\) should be greater than \(\delta \).

Proposition 1 shows that the detailed emission allowance allocation should be closely related to the industry attributes: the worse the industry’s ex-ante carbon performance is (i.e., \(e_o\) is higher), the more allowances should be allocated, where this process should be adjusted and controlled by the weighting factor \(\delta \) chosen by the government. The carbon emission allowances per product increases with the average actual emissions of the industry \(e\left( \theta \right) \). The carbon price \(p_e\) should always be greater than \(\delta \) to guarantee the positivity of \(K\left( {\rho \left( \theta \right) } \right) \), which is consistent with the motivation for this mechanism (in this paper, we assume that the industry cannot survive with no carbon emissions). Compared to a firm whose actual carbon reduction rate is greater than the industry average rate, a firm whose carbon reduction rate is lower than the average rate should incur more additional cost to narrow the gap between its actual emissions and the obtained emission allowances. With this mechanism, a continuous low-carbon investment is advocated to achieve a balance between the economy and the environment.

Corollary 1

In this mechanism, the allocated emission allowances (\(K\left( {\rho \left( \theta \right) } \right) \)) should always be less than the industry average actual carbon emissions (\(e\left( \theta \right) \)) to induce a low-carbon improvement. Although the allocated emission allowances are decreasing in the carbon reduction rate (\(\rho (\theta )\)), which seems to curb the incentive to make a low-carbon investment, the gap the industry has to buy decreases as ex-post carbon performance improves.

Since \(\rho \left( \theta \right) = 0\), we know from Eq. (12) that \(K\left( {\rho \left( \theta \right) } \right) = {K_o} = {e_o} - \delta {e_o}/{p_e}\). This shows that the allocated carbon emission allowances will not meet the emission production demands with no low-carbon investment and the gap will therefore be maximal (i.e., \(\delta {e_o}/{p_e}\)), which can be considered punishment for low-carbon inaction. Moreover, we observe that the allocated carbon emission allowances would always be less than the actual carbon emissions of the industry, even with a low-carbon investment. The gap is positively associated with the industry average actual carbon emissions, which means that the gap gradually narrows as low-carbon performance improves. Therefore, this mechanism can significantly reduce carbon emissions by offering an economic incentive for making a low-carbon investment. In the extreme cases where \(\rho \left( \theta \right) = 1\), we get \(K\left( {\rho \left( \theta \right) } \right) = 0\), which is a perfect albeit unattainable result in reality and means that no emission allowances need to be allocated.

Proposition 2

Under the allocation mechanism, the optimal production quantity and low-carbon investment of the industry are given by:

Proof

See “Appendix A” for proofs. \(\square \)

It can be easily observed that the industry-level optimal low-carbon investment \({\theta ^*}\) is determined mainly by \(\delta \) and \({e_o}\). The industry-level optimal production \({q^*}\) is generally determined by c, p, \(\delta \) and \({e_o}\). To derive the relationship between the optimal solutions and these parameters, we employ an exponential form of the inverse cost function to capture the relationship between the carbon emission reduction rate and the low-carbon investment, which is widely used in the operations management literature (Jeuland and Shugan 1988; Du et al. 2017a). We thereby obtain explicit solutions of low-carbon investment and production quantity (presented in “Appendix C”). Eventually, we obtain the following results.

Corollary 2

The industry’s optimal low-carbon investment \({\theta ^*}\) is increasing in the initial carbon emissions \({e_o}\) and the environmental weighting factor \(\delta \). The optimal production \({q^*}\) is increasing in the product price p but decreasing in the production cost c, initial carbon emissions \({e_o}\) and weighting factor \(\delta \).

Proof

See “Appendix C” for proofs. \(\square \)

Corollary 2 implies that the industry should make a higher investment in carbon reduction if the initial emissions per product are larger. The industry will also improve its carbon reduction level because of the constraint on emission allowances. When the government pays more attentions to the environmental damage caused by the industry, the industry will become more committed to reducing carbon emissions. It is intuitive that the industry will raise production with a gradually increasing product price. However, the production quantity will decrease with the production cost, which is consistent with previous studies. With this allocation mechanism, both the rising initial carbon emissions \({e_o}\) and the weighting factor \({\delta }\) contribute to a higher carbon-related cost, similar to the traditional production cost c, which also has a negative effect on the equilibrium production quantity \({q^*}\).

5 The analysis of the allocation mechanism

In this section, we further examine the practical application of the optimal allocation mechanism presented above. Here, we consider two firms with different low-carbon technological levels to simulate the entire industry, where \(\beta _1 < \beta _2 \). The firms produce a homogenous product to the market. We explore the optimal carbon-related decision of each firm. Without loss of generality, we also assume that all information is known to both the government and firms.

Let \({\theta _i}\) denote the low-carbon investment per product of firm \(i{(i=1,2)}\). We denote the carbon emission reduction rate with a low-carbon investment of the two firms as \({\rho _1}\left( {{\theta _1}} \right) \) and \({\rho _2}\left( {{\theta _2}} \right) \), respectively. Firm i’s gap between the per-product actual carbon emissions and the allocated allowances is denoted by \(\Delta {e_i}\). For the sake of tractability, we adopt the exponential form to represent the inverse cost function, i.e., \({\rho _i}\left( {{\theta _i}} \right) = 1 - {e^{ - {\beta _i}{\theta _i}}}, (i = 1,2)\). This form exhibits the aforementioned properties and is widely used in other studies (Gallego and Ryzin 1994; Jeuland and Shugan 1988; Du et al. 2017a). The factor \({\beta _i}\) stands for firm i’s carbon reduction technological level, and \({\beta _i} = \left| {\frac{{\partial \ln e\left( {{\theta _i}} \right) }}{{\partial {\theta _i}}}} \right| \), satisfying the form of semi-elasticity, captures the fact of boundary values and the law of diminishing marginal return. For simplification, we assume that the industry demand is split deterministically (Lippman and McCardle 1997) such that the market share of firm 1 is \( \lambda \), which is bounded within the interval [0, 1] (i.e., \(\lambda _1 = \lambda \in [0,1] \)), and that firm 2’s market share is \({\lambda _2 = 1 - \lambda } \) of the industry demand. Meanwhile, the two firms independently decides the production quantities \({q_1}\) and \({q_2}\) in accordance with the market demand. The definitions of other notations used later in the paper are the same as in Sect. 3.

In this case, the government announces the emission allowance allocation mechanism according to the industry average carbon reduction rate. Here, the average carbon reduction rate is \(\rho =\lambda {\rho _1} + \left( {1 - \lambda } \right) {\rho _2}\). Therefore, the carbon emission allowances per product is:

Under this allocation mechanism, the firms must make decisions according to their situation and the market demand. The profit of each firm could be expressed as follows:

Substituting Eq. (14) into Eq. (15), we have

From the first-order conditions of \({\pi _i}\) with respect to \({\theta _i}\), we have the following results.

Proposition 3

Under this allocation mechanism, the firms’ optimal low-carbon investment is determined mainly by the carbon price \({p_e}\), the initial carbon emissions without low-carbon investment \({e_o}\), the market share \(\lambda \), the government’s environmental weighting factor \(\delta \) and the technological level of each firm \({\beta _i}\). The optimal investment of each firm can be derived as follows:

Accordingly, the carbon emission reduction rate of each firm is:

Proof

See “Appendix D” for proofs. \(\square \)

Corollary 3

To ensure the stability and effectiveness of the allocation mechanism, the realized carbon reduction rate of each firm should satisfy \(\rho _i \in [0,1)\), so the boundary conditions of carbon price could be derived as follows:

Proof

See “Appendix E” for proofs. \(\square \)

Under these conditions, each firm’s actual carbon emissions per product are, at most, the same as the initial emissions without a low-carbon investment, rather than more than the initial emissions. In the cap-and-trade scheme, carbon emission trade occurs frequently, where the carbon price significantly affects the low-carbon efforts of every firm. Recalling the crash of carbon price in EU-ETS [the price of carbon emission per ton had soared above $ 40 in 2008 but drastically dropped below $ 4 in 2013 (Du et al. 2016)], we recognize that if the carbon price is too low, the mechanism might fail to achieve low-carbon economic transition. This corollary reveals the boundary condition necessary to induce the firms to make a low-carbon investment.

Corollary 4

Given the constraint of this allocation mechanism, firm i’s optimal low-carbon investment \({{\theta _i}^ * }\) (\(i=1,2\)) is increasing in the carbon price \({p_e}\), the government’s weighting factor \(\delta \) and the initial emissions per product \({e_o}\), respectively, but is decreasing in its respective market share \(\lambda _i \). However, firm i’s technological level of carbon reduction \(\beta _i\) has a piecewise impact on its low-carbon investment decision \({{\theta _i}^ * }\). More specifically,

-

1.

When \({\beta _i} \ge \frac{e}{{{p_e}{e_o}\left( {1 - {\lambda _i}\left( {1 - \frac{\delta }{{{p_e}}}} \right) } \right) }}\), the low-carbon investment \({{\theta _i}^ * }\) decreases with \({\beta _i}\).

-

2.

When \(\frac{1}{{{p_e}{e_o}\left( {1 - {\lambda _i}\left( {1 - \frac{\delta }{{{p_e}}}} \right) } \right) }} \le {\beta _i} < \frac{e}{{{p_e}{e_o}\left( {1 - {\lambda _i}\left( {1 - \frac{\delta }{{{p_e}}}} \right) } \right) }}\), the low-carbon investment \({{\theta _i}^ * }\) increases with \({\beta _i}\).

Proof

See “Appendix E” for proofs. \(\square \)

Corollary 4 is consistent with the intuition that if the carbon price increases, the government places more weight on the environmental damage caused by the industry, or the initial carbon performance of the industry is poor, the firms should naturally improve their low-carbon investment to take responsibility. Corollary 4 also reveals that a firm will reduce its low-carbon investment when its market share increases.

Corollary 4 implies that each firm will make a first-increases-then-decreases low-carbon investment when the technological level of carbon reduction increases. When the firm’s technological level is relatively low, it will be more profitable to increase the low-carbon investment as the technological level increases which further mitigate the gap of the emission allowances. However, beyond a critical point, the low-carbon efficiency is sufficiently high. If the firm continues to increase its low-carbon investment, the industry average performance of carbon reduction will be rapidly improved which leads to a more strict carbon allocation. In this case, the firm would decrease the low-carbon investment appropriately to avoid the dramatic reduction of the free emission allowances and save the cost. Firm i’s critical point of carbon reduction technological level is donated as \({\hat{\beta }_i}=\frac{e}{{{p_e}{e_o}\left( {1 - \lambda _i \left( {1 - \frac{\delta }{{{p_e}}}} \right) } \right) }}(i=1,2)\) and will be analyzed in more detail in Corollary 5 below.

Corollary 5

The critical point of firm i’s carbon reduction technological level, \({\hat{\beta }_i}\) (\(i=1,2\)), is decreasing in the carbon price \({p_e}\), the government’s environmental weighting factor \(\delta \) and the initial emissions per product \({e_o}\) respectively. In contrast, \({\hat{\beta }_i}\) is increasing in the firm’s market share \(\lambda _i \).

Proof

See “Appendix E” for proofs. \(\square \)

Corollary 5 shows that the critical point of firm i’s carbon reduction technological level depends mainly on common factors (i.e., \(p_e\), \(\delta \) and \(e_o\)) and that the only factor related to itself is its market share. This is consistent with the reality that the developing company (with growing market share) would be more willing to increase its input to make full use of its technical advantages. This corollary reveals another low-carbon issue, i.e., that if a firm could determine its technological level, it would need to balance between technology innovation and low-carbon operational investment.

Based on Proposition 3, we obtain the optimal low-carbon investment and the carbon emission reduction rate of each firm. Substituting Eq. (17) into Eq. (14), we can derive the optimal carbon emission allowances per product allocated by the government as follows:

Accordingly, the gap between the actual carbon emissions and the allocated emission allowances of each firm can be expressed as follows:

Corollary 6

The gap between the actual carbon emissions and the allocated emission allowances, \(\Delta {e_i}\) (\(i=1,2\)), is decreasing in the firm’s own carbon reduction technological level \({\beta _i}\) but increasing in the carbon reduction technological level of the other firm. In addition, the gap \(\Delta {e_i}\) will increase with the market share \(\lambda _i \) and the weighting factor \(\delta \), respectively.

Proof

See “Appendix E” for proofs. \(\square \)

From Corollary 6, we notice that although the firm’s obtained emission allowances will decrease when its carbon reduction technological level improves, the gap between the firm’s actual carbon emissions and the obtained emission allowances will become narrow. Instead, as the competitor’s technological level increases, the allocated allowances will decrease, which means that there will be a greater pressure from carbon constraint. Concretely speaking, when the market shares of these two firms are close, the firm with a higher technological level (firm 2 in this paper) would have a distinct advantage, which would allow it to provide less payment for the emission gap in most cases, and it could even earn money from the surplus of its allocated allowances when its technological level is significantly beyond that of firm 1. Meanwhile, the disadvantaged firm (firm 1) always lack allowances and will spend more to purchase the allowances with the widening difference between the firms’ technological levels. This property reveals the low-carbon inducement mechanism from a specific operations perspective, which is consistent with the conceptual design of the cap-and-trade policy.

In addition, it is intuitive that the emission gap of each firm will increase with the weighting factor \(\delta \). Given the former analysis, we know that if a firm has a larger market share, it reduces its low-carbon investment, which leads to a widening emission gap. Inspired by the abovementioned results, it follows that a new entrant with a high level of carbon reduction technology in the industry (i.e., \(\lambda _i\) is low, \(\beta _i\) is high) will possess a distinct advantage and can profit from its allowances surplus.

6 Numerical examples

In this section, we provide several typical numerical examples to support and supplement the previous analysis. First, we show the relationship between the ex-post demand for emission allowances and the allocated emission allowances under the optimal emission allowance allocation mechanism. We then discuss how the optimal allocated emission allowances per product, the low-carbon investment, the emission gap and the production decision change with related factors.

For the parameters in the model, the numerical assignments are as follows: \(p = 100, c=40, {e_o} = 10\), \({p_e} = 3, {\beta _1} = 0.2, {\beta _2} = 0.5, \lambda = 0.6\) and \(\delta = 1\).

Example 1

We use this example to demonstrate our emission allowance allocation mechanism. We focus on the gap between the industry’s ex-post demand for emission allowances after low-carbon processing and the emission allowances allocated by the government. In this case, other related parameters: \({p_e} = 3\) and \(\delta = 1\). In Fig. 1a, the blue line represents the average actual carbon emissions of the industry with the low-carbon investment. The red line represents the emission allowances granted by the government. Obviously, the higher the low-carbon investment is, the lower the actual carbon emissions \(e(\theta )\). As shown in Fig. 1a, the carbon emission allowances will always be linearly insufficient to meet the ex-post demand at the industry level, where this gap depends on the effect of the carbon price \({p_e}\) and the weighting factor \(\delta \) stated in Corollary 1. The gap will be largest in the absence of low-carbon investment (i.e., \(e\left( \theta \right) = {e_o} = 10\)). The emission gap can be closed by making a higher low-carbon investment.

Optimal emission allowance allocation mechanism

Figure 1b, c exhibits the influence of the carbon price and the government’s environmental weighting factor on the optimal allocated emission allowances per product. This paper simulates the entire industry with two firms, where the optimal emission allowances are given in Eq. (20). Here, except for the independent variable in each case, we keep the initial values for other parameters (i.e., \({p_e} = 3,{\beta _1} = 0.2,{\beta _2} = 0.5,\lambda = 0.6,\delta = 1\)).

Figure 1b shows that as the carbon price increases, the emission allowances will first increase then decrease. Figure 1c illustrates that the obtained emission allowances of firms will decrease when the government puts more emphasis on carbon emissions. In reality, if the government sets out to more strictly control the carbon emissions, it may reduce the free emission allowances by adjusting the weighting factor for the particular industry.

Example 2

In this example, we refocus on the analysis of the two firms’ optimal low-carbon investment under the optimal emission allowance allocation mechanism. Similarly, except for the independent variable in each case, we keep the initial values for other parameters (i.e., \({e_o} = 10,{p_e} = 3,{\beta _1} = 0.2,{\beta _2} = 0.5,\lambda = 0.6,\delta = 1\)).

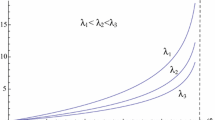

The influences of related factors on the optimal low-carbon investment

The piecewise impact of the technological level \({\beta _i}\) is depicted in Fig. 2a. According to Fig. 2a, we can see that the low-carbon investment of firm 1 is less than that of firm 2 when the two firms have the same level of carbon reduction technology. We can therefore deduce that a firm whose market share is larger than other firms in the same industry may make a lower low-carbon investment. Figure 2b, c, d clearly show that each firm’s low-carbon investment increases with the carbon price \({p_e}\) and the weighting factor \(\delta \) but is decreasing in its market share \({\lambda _i}\). Figure 2d shows that because the allocated emission allowances decrease with the government’s weighting factor, once the government implements a tight emission allowance allocation, the firms should make a higher low-carbon investment. Moreover, the related authority or the government can lead firms to take more low-carbon efforts by adjusting the carbon price. These results are the same as those from the analysis of Corollary 4.

Example 3

Figure 3 summarizes the influences of the carbon reduction technological level of each firm, the market share of firm 1 and the government’s weighting factor on the emission gap of the two firms, respectively. Except for the independent variable in each case, we keep the initial values for other parameters.

The influences of related factors on the emission gap

Combining Fig. 3a, b, we notice that as the carbon reduction technological level of other firms increases, the emission gap of the firm will increase. However, every firm in the same industry can reduce its emission gap when their own carbon reduction technological level increases. Figure 3b illustrates that although the market share of firm 2 is slightly smaller than that of firm 1, firm 2 may earn some profits from selling its surplus emission allowances if its carbon reduction technological level is sufficiently high. As shown in Fig. 3c, firm 1 should buy more emission allowances in the carbon trading market as its market share increases, whereas the emission gap of firm 2 decreases with the market share of firm 1. In this case, we assume that the carbon reduction technological level of firm 2 is higher than that of firm 1. According to Fig. 3c, we deduce that a new entrant with a very small market share can obtain more of the remaining emission allowances by adopting a higher carbon reduction technological level. Figure 3d indicates that the emission gap of every firm increases with the environmental weighting factor. These results further corroborate the analysis of Corollary 6.

Example 4

This example aims to exhibit the effect of these carbon-related and market factors on the firms’ optimal output decisions. For simplicity, we assume that the market demand x is drawn from the uniform distribution on [0, 1]. Inheriting the other setting from the modeling part, we can derive explicit expressions for the firms’ optimal production quantities as follows:

In this example, we assume that each firm takes the same market share to avoid the impact of the market share (i.e., \({\lambda _i} = 0.5\)). Except for the independent variable in each case, we keep the initial values for other parameters. The results are shown in Fig. 4. Similar results can be derived when the market demand is drawn from the normal distribution or the exponential distribution.

The influences of related factors on the optimal production decision

From Fig. 4a, b, we can observe that the firm’s optimal production quantity \({{q_i} ^ * }(i=1,2)\) increases with its technological level of carbon emission reduction \({\beta _i}\), where \({{q_i} ^ * }\) decreases with the carbon reduction technological level of the other competitor. Given that the emission gap of each firm can be closed as its carbon reduction technological level increases, the higher the carbon reduction technological is, the less cost the firm should incur to make up the emission gap. Therefore, the firm can produce more products as its carbon reduction technological level improves. Conversely, each firm’s production could be negatively affected by an increase in the level of carbon reduction technology of the other firm. Thus, each firm should take measures to avoid an adverse impact when the other firm has improved its carbon reduction technological level. Figure 4c shows that firm 1 will expand its production as its market share increases, when firm 2’s market share decreases and firm 2 reduces its production. This is consistent with common sense. Figure 4d demonstrates that both firms reduce their production as the weighting factor \(\delta \) increases.

7 Concluding remarks and future research

In this paper, we focus on the design of emission allowance allocation mechanism and the impacts on operational decisions under the cap-and-trade regulation. We depict the target of a government with environmental and economic goals and develop a game-theoretical model to investigate this question. In contrast to the existing studies, we explore this issue from a low-carbon operations perspective. We construct a linear form of emission allowance allocation mechanism and verify its feasibility and effectiveness. A fundamental allocation mechanism is obtained and demonstrated in which the emission allowances per product is linear decreasing in the industry average carbon emission reduction rate.

Through the analysis, the government can adjust and control this industry’s low-carbon process by varying the weighting factor. Moreover, when the government places a larger weight on the environmental goal, the total carbon emissions declines, but it may also have a negative impact on production. Recalling that industries have different attributes and significance, the government should balance the economic goal against and environmental goal with an ordered plan for each industry. Under our allocation mechanism, the emission allowances are always insufficient for the actual carbon emission at the industry average level to induce a continuous low-carbon upgrade. The industry could narrow the gap between the actual demand of carbon emission and the allocated emission allowances with an industry-level low-carbon investment.

Furthermore, we simulate the industry with two firms to explore the effects of this emission allowance allocation mechanism on specific firms. The optimal strategies of these two firms are obtained, and we analyze the implementation effects of our allocation mechanism. Our analysis demonstrates that the firm’s optimal low-carbon investment would decrease with its own market share. In addition, as the firm’s carbon reduction technological level increases, this firm’s optimal low-carbon investment would exhibit a first-increase-then-decrease migration. If the firm adopts a higher carbon reduction technological level, it could narrow the emission gap and even earn surplus emission allowances in some cases, which would also incentivize the firm to produce more products. From the analysis of these two firms’ optimal strategies, we reveal the driving force and the running mechanism of our allocation policy: the firm with superior carbon reduction technological level is encouraged to take more low-carbon processing with a greater efficiency, whereas the firm with inferior carbon reduction technological level needs to spend more on purchasing emission allowances from the carbon trading market. This observation is in line with the conceptual design of cap-and-trade system from an operations perspective.

To summarize, our paper provides some suggestions and insights for both the government and firms. A brief and executable emission allowance allocation mechanism is proposed and analyzed, which might serve as a baseline and reference for further research. Of course, our paper has some limitations and could be extended in several directions. In this research, the demand for products follows an independent random distribution. In reality, it might be associated with market factors or carbon-related factors, such as the product price, consumers’ low-carbon preference, etc. In addition, all information is transparent to the government and the firms in our model. Obviously, it is difficult for the government to accurately informed about the low-carbon operational details at the industry level. Moreover, we only consider carbon emissions generated in the production process. In practice, each segment of the supply chain emits carbon pollutants, including procurement, logistics, inventory management and so on. Therefore, the question of how to allocate emission allowances to different firms that separately control a segment of the supply chain is an important one. We plan to consider these issues in our future research.

References

Ahn, J. (2014). Assessment of initial emission allowance allocation methods in the Korean electricity market. Energy Economics, 43(2), 244–255.

Benjaafar, S., Li, Y., & Daskin, M. (2013). Carbon footprint and the management of supply chains: Insights from simple models. IEEE Transactions on Automation Science and Engineering, 10(1), 99–116.

Brandenburg, M., & Rebs, T. (2015). Sustainable supply chain management: A modeling perspective. Annals of Operations Research, 229(1), 213–252.

Brauneis, A., Mestel, R., & Palan, S. (2013). Inducing low-carbon investment in the electric power industry through a price floor for emissions trading. Energy Policy, 53, 190–204.

Chang, X., Xia, H., Zhu, H., Fan, T., & Zhao, H. (2015). Production decisions in a hybrid manufacturing–remanufacturing system with carbon cap and trade mechanism. International Journal of Production Economics, 162, 160–173.

Chen, Y., & Lin, S. (2015). Decomposition and allocation of energy-related carbon dioxide emission allowance over provinces of China. Natural Hazards, 76(3), 1893–1909.

Chiu, Y.-H., Lin, J.-C., Su, W.-N., & Liu, J.-K. (2015). An efficiency evaluation of the EU’s allocation of carbon emission allowances. Energy Sources, Part B: Economics, Planning and Policy, 10(2), 192–200.

Cong, R.-G., & Wei, Y.-M. (2010). Potential impact of (CET) carbon emissions trading on China’s power sector: A perspective from different allowance allocation options. Energy, 35(9), 3921–3931.

Dong, C., Shen, B., Chow, P.-S., Yang, L., & Ng, C. T. (2016). Sustainability investment under cap-and-trade regulation. Annals of Operations Research, 240(2), 509–531.

Drake, D. F., Kleindorfer, P. R., & Van Wassenhove, L. N. (2016). Technology choice and capacity portfolios under emissions regulation. Production and Operations Management, 25(6), 1006–1025.

Du, S., Hu, L., & Song, M. (2016). Production optimization considering environmental performance and preference in the cap-and-trade system. Journal of Cleaner Production, 112, 1600–1607.

Du, S., Hu, L., & Wang, L. (2017a). Low-carbon supply policies and supply chain performance with carbon concerned demand. Annals of Operations Research, 255(1–2), 569–590.

Du, S., Ma, F., Fu, Z., Zhu, L., & Zhang, J. (2015). Game-theoretic analysis for an emission-dependent supply chain in a ‘cap-and-trade’ system. Annals of Operations Research, 228(1), 135–149.

Du, S., Zhu, Y., Zhu, Y., & Tang, W. (2017b). Allocation policy considering firm’s time-varying emission reduction in a cap-and-trade system. Annals of Operations Research,. https://doi.org/10.1007/s10479-017-2606-0.

Filar, J. A., & Gaertner, P. S. (1997). A regional allocation of world \(\text{ CO }_2\) emission reductions. Mathematics and Computers in Simulation, 43(3–6), 269–275.

Gallego, G., & Van Ryzin, G. (1994). Optimal dynamic pricing of inventories with stochastic demand over finite horizons. Management Science, 40(8), 999–1020.

Gomes, E., & Lins, M. E. (2008). Modelling undesirable outputs with zero sum gains data envelopment analysis models. Journal of the Operational Research Society, 59(5), 616–623.

Goulder, L. H., Hafstead, M. A., & Dworsky, M. (2010). Impacts of alternative emissions allowance allocation methods under a federal cap-and-trade program. Journal of Environmental Economics and management, 60(3), 161–181.

Han, R., Yu, B.-Y., Tang, B.-J., Liao, H., & Wei, Y.-M. (2017). Carbon emissions quotas in the Chinese road transport sector: A carbon trading perspective. Energy Policy, 106, 298–309.

He, P., Zhang, W., Xu, X., & Bian, Y. (2015). Production lot-sizing and carbon emissions under cap-and-trade and carbon tax regulations. Journal of Cleaner Production, 103, 241–248.

Hong, T., Koo, C., & Lee, S. (2014). Benchmarks as a tool for free allocation through comparison with similar projects: Focused on multi-family housing complex. Applied Energy, 114(2), 663–675.

Hong, Z., Chu, C., Zhang, L. L., & Yu, Y. (2017). Optimizing an emission trading scheme for local governments: A Stackelberg game model and hybrid algorithm. International Journal of Production Economics, 193, 172–182.

Jaber, M. Y., Glock, C. H., & El Saadany, A. M. (2013). Supply chain coordination with emissions reduction incentives. International Journal of Production Research, 51(1), 69–82.

Jeuland, A. P., & Shugan, S. M. (1988). Note-channel of distribution profits when channel members form conjectures. Marketing Science, 7(2), 202–210.

Ji, J., Zhang, Z., & Yang, L. (2017). Comparisons of initial carbon allowance allocation rules in an O2O retail supply chain with the cap-and-trade regulation. International Journal of Production Economics, 187, 68–84.

Jin, M., Granda-Marulanda, N. A., & Down, I. (2014). The impact of carbon policies on supply chain design and logistics of a major retailer. Journal of Cleaner Production, 85, 453–461.

Kaur, H., & Singh, S. P. (2016). Sustainable procurement and logistics for disaster resilient supply chain. Annals of Operations Research,. https://doi.org/10.1007/s10479-016-2374-2.

Kober, T., van der Zwaan, B., & Rösler, H. (2015). Schemes for the regional allocation of emission allowances under stringent global climate policy. In G. Giannakidis, M. Labriet, B. P. OGallachóir, & G. Tosato (Eds.), Informing energy and climate policies using energy systems models. Berlin: Springer.

Liao, Z., Zhu, X., & Shi, J. (2015). Case study on initial allocation of Shanghai carbon emission trading based on Shapley value. Journal of Cleaner Production, 103(15), 338–344.

Lippman, S. A., & McCardle, K. F. (1997). The competitive newsboy. Operations Research, 45(1), 54–65.

MacLeod, C., Eversley, M., (2014). U.S. China reach ‘historic’ deal to cut emissions. http://www.usatoday.com/story/news/world/2014/11/11/china-climate-change-deal/18895661/. Accessed November 20, 2014.

Meunier, G., Ponssard, J.-P., & Quirion, P. (2014). Carbon leakage and capacity-based allocations: Is the EU right? Journal of Environmental Economics and Management, 68(2), 262–279.

Pan, X., Teng, F., & Wang, G. (2014). Sharing emission space at an equitable basis: Allocation scheme based on the equal cumulative emission per capita principle. Applied Energy, 113, 1810–1818.

Qiu, R., Xu, J., & Zeng, Z. (2017). Carbon emission allowance allocation with a mixed mechanism in air passenger transport. Journal of Environmental Management, 200, 204–216.

Rezaee, A., Dehghanian, F., Fahimnia, B., & Beamon, B. (2017). Green supply chain network design with stochastic demand and carbon price. Annals of Operations Research, 250(2), 463–485.

Rosendahl, K. E., & Storrøsten, H. B. (2015). Allocation of emission allowances: Impacts on technology investments. Climate Change Economics, 6(03), 1550010.

Schmidt, R. C., & Heitzig, J. (2014). Carbon leakage: Grandfathering as an incentive device to avert firm relocation. Journal of Environmental Economics and Management, 67(2), 209–223.

Sheu, J.-B., & Li, F. (2013). Market competition and greening transportation of airlines under the emission trading scheme: A case of Duopoly market. Transportation Science, 48(4), 684–694.

Song, M.-L., Fisher, R., Wang, J.-L., & Cui, L.-B. (2016). Environmental performance evaluation with big data: Theories and methods. Annals of Operations Research,. https://doi.org/10.1007/s10479-016-2158-8.

Song, M.-L., Zhang, W., & Qiu, X.-M. (2015). Emissions trading system and supporting policies under an emissions reduction framework. Annals of Operations Research, 228(1), 125–134.

Tang, C. S., & Zhou, S. (2012). Research advances in environmentally and socially sustainable operations. European Journal of Operational Research, 223(3), 585–594.

Toptal, A., & Çetinkaya, B. (2017). How supply chain coordination affects the environment: A carbon footprint perspective. Annals of Operations Research, 250(2), 487–519.

Toptal, A., Özlü, H., & Konur, D. (2014). Joint decisions on inventory replenishment and emission reduction investment under different emission regulations. International Journal of Production Research, 52(1), 243–269.

Wang, K., Zhang, X., Wei, Y.-M., & Yu, S. (2013). Regional allocation of \(\text{ CO }_2\) emissions allowance over provinces in China by 2020. Energy Policy, 54, 214–229.

WHO. (2016). Ambient air pollution: A global assessment of exposure and burden of disease. http://who.int/phe/publications/air-pollution-global-assessment/en/. Accessed March 5, 2017.

Winkler, H., Spalding-Fecher, R., & Tyani, L. (2002). Comparing developing countries under potential carbon allocation schemes. Climate Policy, 2(4), 303–318.

Xia, L., Guo, T., Qin, J., Yue, X., & Zhu, N. (2017). Carbon emission reduction and pricing policies of a supply chain considering reciprocal preferences in cap-and-trade system. Annals of Operations Research,. https://doi.org/10.1007/s10479-017-2657-2.

Xiong, L., Shen, B., Qi, S., Price, L., & Ye, B. (2017). The allowance mechanism of China’s carbon trading pilots: A comparative analysis with schemes in EU and california. Applied Energy, 185, 1849–1859.

Xu, X., He, P., Xu, H., & Zhang, Q. (2017). Supply chain coordination with green technology under cap-and-trade regulation. International Journal of Production Economics, 183, 433–442.

Yi, W.-J., Zou, L.-L., Guo, J., Wang, K., & Wei, Y.-M. (2011). How can China reach its \(\text{ CO }_2\) intensity reduction targets by 2020? A regional allocation based on equity and development. Energy Policy, 39(5), 2407–2415.

Yu, S., Wei, Y.-M., & Wang, K. (2014). Provincial allocation of carbon emission reduction targets in China: An approach based on improved fuzzy cluster and Shapley value decomposition. Energy Policy, 66, 630–644.

Zhang, B., & Xu, L. (2013). Multi-item production planning with carbon cap and trade mechanism. International Journal of Production Economics, 144(1), 118–127.

Zhang, J., Xiao, J., Chen, X., Liang, X., Fan, L., & Ye, D. (2017). Allowance and allocation of industrial volatile organic compounds emission in China for year 2020 and 2030. Journal of Environmental Sciences,. https://doi.org/10.1016/j.jes.2017.10.003.

Zhang, Y.-J., & Hao, J.-F. (2017). Carbon emission quota allocation among China’s industrial sectors based on the equity and efficiency principles. Annals of Operations Research, 255(1–2), 117–140.

Zhang, Y.-J., Wang, A.-D., & Da, Y.-B. (2014). Regional allocation of carbon emission quotas in China: Evidence from the Shapley value method. Energy Policy, 74, 454–464.

Zhang, Y.-J., Wang, A.-D., & Tan, W. (2015). The impact of China’s carbon allowance allocation rules on the product prices and emission reduction behaviors of ETS-covered enterprises. Energy Policy, 86, 176–185.

Zhao, J., Hobbs, B. F., & Pang, J.-S. (2010). Long-run equilibrium modeling of emissions allowance allocation systems in electric power markets. Operations Research, 58(3), 529–548.

Zhao, R., Min, N., Geng, Y., & He, Y. (2017). Allocation of carbon emissions among industries/sectors: An emissions intensity reduction constrained approach. Journal of Cleaner Production, 142, 3083–3094.

Zhou, P., & Wang, M. (2016). Carbon dioxide emissions allocation: A review. Ecological Economics, 125, 47–59.

Zhou, P., Zhang, L., Zhou, D., & Xia, W. (2013). Modeling economic performance of interprovincial \(\text{ CO }_2\) emission reduction quota trading in China. Applied Energy, 112, 1518–1528.

Acknowledgements

We are grateful for the editor’s and anonymous reviewers’ constructive comments and suggestions which have greatly improved the quality of this paper. We also thank Dr. Li Wang for her valuable suggestions on model analysis and acknowledge the USTC Modern Logistics Research Centre for its data-driven practical platform. This research was supported by the National Natural Science Foundation of China (Grant Nos. 71571171, 71631006, 71471168), the Foundation for International Cooperation and Exchange of the National Natural Science Foundation of China (No. 71520107002), the Youth Innovation Promotion Association, CAS (Grant No. 2015364) and the Fundamental Research Funds for the Central Universities (Grant No. WK2040160028).

Author information

Authors and Affiliations

Corresponding author

Appendices

Appendix A: The linear form of allocation mechanism

Proof

we firstly discuss the situation where the emission allowances per product is linear with carbon emission reduction rate.

1.1 Step 1: Solve the industry’s profit maximization problem

The profit function of the industry has been given in Eq. (6). The first-order conditions of \(\pi \) with respect to q and \(\theta \) respectively are:

Then, we get the equations of stationary point

Accordingly, we verify that the determinant of the Hessian matrix at the stationary point is negative definite:

So the \(\pi \) reaches the maximum at the stationary point.

1.2 Step 2: Solve the optimization problem faced by the government

The government anticipates the behaviors of the industry and makes own decisions. Now, the objective function of the government has been given in Eq. (8). To find the optimal results, we firstly take the derivative of Eq. (A.2) with respect to a and \({K_o}\) respectively. Then, we have

Reducing the above equations, we get

By taking the derivative of Eq. (A.3) with respect to a and \({K_o}\) respectively, we have

Reducing the above equations, we get

Finally, the first-order conditions of W regarding a and \({K_o}\) can be derived as:

Reducing the above equations, we get

We verify that the determinant of the Hessian matrix is negative definite:

So the solution to the first order conditions gives the unique solution.

1.3 Step 3: To find the equilibrium solutions

Combining Eqs. (A.2), (A.3) and (A.9), we can derive the optimal solutions. The optimum decisions for the industry and government are shown as follows.

The form of the carbon emission allowances allocation mechanism is given as:

\(\square \)

Appendix B: The quadratic form of allocation mechanism

In this paper, we attempt to explore the other form of emission allowance allocation mechanism preliminarily. Here, we suppose that the carbon emission allowances per product may be a concave or convex function with regard to the industry-level carbon emission reduction rate. Then we adopt the quadratic form to represent the allocation mechanism, this form is formulated as follows:

Additionally, we suppose that this allocation mechanism is a quadratic function with mathematical characteristics including \(K'\left( {\rho \left( \theta \right) } \right) < 0\) or \(K'\left( {\rho \left( \theta \right) } \right) > 0\), \(K\left( 0 \right) ={K_o}\), \(\mathop {\lim }\nolimits _{\rho \left( \theta \right) \rightarrow 1} K\left( {\rho \left( \theta \right) } \right) = 0\). And the second-order condition of the carbon emission allowances per product regarding the carbon emission reduction rate is constant. It can be described as:

Based on the above characteristics of this quadratic function, the quadratic form of allocation mechanism is equivalent to:

In this section, we try to examine the rationality and feasibility of this form. First of all, we discuss how this mechanism affects the production and carbon reduction decisions of the industry. Substituting Eq. (B.3) into Eq. (1), we have:

When the mechanism is declared by the government, the industry is to make decisions to realize its own interests. We can get the optimal production quantity and investment of the industry by taking the derivative of the profit function. The two decision variables are determined by:

where \({q^*}\left( {{K_o},a} \right) \) and \({\theta ^*}\left( {{K_o},a} \right) \) are the optimal reaction functions of the industry given \({K_o}\) and a. Here, the objective function of the government can be written as:

The first-order conditions of W regarding a and \({K_o}\) respectively are:

By reducing the above equations, we get \(\rho \left( {{\theta ^*}\left( {{K_o},a} \right) } \right) = 1\). When the carbon emission reduction rate is 1, the government doesn’t need to allocate any allowance to the industry. However, the operations with no emission would not happen in real life and it is so hard for the industry to achieve 100% carbon emission reduction. Based on the actual practice, this paper assumes the carbon emission reduction rate is less than 1. So it doesn’t make sense to discuss the solution, i.e. \(\rho \left( {{\theta ^*}\left( {{K_o},a} \right) } \right) = 1\). This solution is infeasible and discarded since it doesn’t satisfy the assumption. Thus, there is no equilibrium solution under the strict quadratic form. Finally, the quadratic form will turn into the linear form.

where \(a=0\).

Proof

We explore whether the quadratic form of allocation mechanism is executable. In the same manner which has been adopted in “Appendix A”, we address this problem by using the backward induction.

1.1 Step 1: Solve the industry’s profit maximization problem

The quadratic form of allocation mechanism and the profit function of the industry have been shown in Eqs. (B.3) and (B.4). The first-order conditions of \(\pi \) can be derived as:

Then, the production quantity and low-carbon investment are given as follows:

1.2 Step 2: Solve the optimization problem faced by the government

Likewise, the government makes decisions according to anticipated behaviors of the industry. The objective function of the government has been shown in Eq. (B.6). To get the first-order conditions of W, we firstly take the derivative of Eq. (B.12) with respect to a, we obtain

Reducing the above equation, we get

Then, we take the derivative of Eq. (B.12) with respect to \({K_o}\), we obtain