Abstract

Marginal rates of contribution (MRC), i.e., the rates at which additional revenues are skimmed via larger contributions or lower transfer receipts, quantify the incentives of a fiscal equalization scheme. This paper is the first to calculate marginal rates of contribution for the Laender (states) in the German fiscal equalization scheme for each of the 51 years since its establishment in 1970 and over five major reforms, taking into account all relevant revenues. Our results show that MRC have been at a consistently high level. Until 2019 the scheme induced an almost full skimming of additional tax revenues of recipient states. With the system’s latest reform in 2020, MRC increased further. Recipient states now face an over-skimming of additional tax revenues and, thus, massive fiscal disincentives to maintain their own tax base. While these findings have been widely expected, comprehensive evidence has been missing so far.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

A fiscal equalization scheme needs to balance two conflicting objectives. On the one hand, it has to level out financial resources across jurisdictions. On the other hand, it should not undermine the fiscal incentives for a jurisdiction to improve its own economic position. In Germany’s fiscal equalization scheme, the trade-off between these two objectives is particularly pronounced. First, the combination of comparable expenditure profiles and differing per capita revenues across the 16 federal states provides arguments for a system that levels out diverging revenues broadly. Second, the states have political means to influence and improve their economic and fiscal situation by their own efforts.

The existing literature shows that, in designing their fiscal equalization scheme, the German states solved this trade-off by opting for a highly redistributive system. As a consequence, under this system it becomes fiscally less attractive for a state to maintain and improve its tax base as large parts of the fiscal benefits of such an improvement are redistributed towards the other states and the federal level (see, e.g., Scherf 2007; Fuest and Thoene 2009; Feld et al. 2013; GCEE 2014; Hentze 2015; Buettner and Goerbert 2016; Scherf 2020a, b). Although a high degree of redistribution induces fiscal disincentives, it can still be welfare enhancing to use transfers to reduce disparities between regions, even if it comes at the cost of lower national output (Henkel et al. 2021). Therefore, finding the ideal degree of possibly welfare-enhancing redistribution that reduces disparities, while mainting the states’ incentives to cultivate their tax bases is a permanent challenge. As a consequence, the degree to which the states have chosen equality in revenues over favorable fiscal incentives has not been static over time. Instead, it varied over five major reforms that Germany’s fiscal equalization scheme underwent during the 51 years since its establishment in 1970. Therefore, the fiscal incentives for a state to maintain and improve its tax bases varied with each of the scheme’s reforms.

In this paper, we focus on the fiscal incentives of Germany’s state fiscal equalization scheme and quantify them by calculating each state’s marginal rate of contribution (MRC) to the equalization system in each year since 1970. The MRC reflect the share of a marginal increase in a state’s tax revenues that is skimmed and does not remain in the state, either due to increased contributions to or reduced transfer receipts out of the equalization scheme. To calculate the MRC for every state, we develop a simulation model of the German fiscal equalization scheme for every fiscal year between 1970 and 2021 that considers all relevant revenue sources, all stages of the system as well as each reform of the equalization scheme. To the best of our knowledge, this paper is the first in which MRC of the German state equalization scheme are calculated comprehensively for all years, reforms, equalization stages and revenue sources. This allows us to trace how the fiscal incentives exerted by the scheme developed over time and what effects the scheme’s reforms had on its incentives. The aim of this paper, which is an updated and extended version of a previous paper by Burret et al. (2018), is twofold. First, by including the latest reform of the equalization scheme into the calculations of each state’s MRC, we provide a comprehensive long-term quantification of the fiscal incentives that the scheme and each of its reforms exerted on each state in every year since 1970. Second, we make this comprehensive long-run quantification of the incentives of the German fiscal equalization system accessible for an international audience.

In contrast to our approach, other empirical studies that provide quantifications of the fiscal incentives of Germany’s state equalization scheme calculate MRC based on a selection of revenue sources only (Baretti et al. 2002; Hauptmeier 2007, 2009; Boenke et al. 2017), use single years (Scientific Advisory Board to the Federal Ministry of Finance 2015), ignore repercussion effects of increases in a state’s revenues on the average revenues of all states (Scherf 2020a) or only address the latest reform of the equalization system (Buettner and Goerbert 2016; Scherf 2020a). International evidence on MRC is scarce. Following Burret et al. (2018), Leisibach and Schaltegger (2019) calculate the MRC of the Swiss fiscal equalization system. They report MRC for cantons with high fiscal capacity of between 14 and 21% and for cantons with low fiscal capacity of between 9 and 92%, with an average of 51,4% for the latter in 2019. Canada has a zero percent MRC for provinces with high fiscal capacity and 100% for the provinces with low fiscal capacity (Feehan 2014).

Our results show that MRC have been at continuously high levels. Thus, the system consistently induced unfavorable fiscal incentives for a state to improve its economic position. This is especially the case for transfer receiving states that face an almost full skimming of additional revenues over almost all years. Only the reform of 2005 led to improvements in the system’s fiscal incentives. These improvements have been concealed by the reform of 2020 that pushed MRC to a historic high, inducing a skimming of up to 112% of additional state revenues for some states, meaning that the fiscal capacity of a state after equalization worsens if its revenues before equalization increase.

The remainder of the paper is organized as follows. Section 2 discusses previous findings on the effects of high MRC on the economic and fiscal policy of a jurisdiction. Section 3 reviews the different stages of Germany’s fiscal equalization scheme since 1970. In Sect. 4, we describe our simulation model to calculate the MRC of a state. In Sect. 5, we trace the development of the system’s MRC over the five major reforms which the system underwent. Section 6 concludes.

2 Incentive effects of MRC

The incentives that a fiscal equalization scheme exerts on a jurisdiction to improve its economic position can be quantified by the jurisdiction’s marginal rates of contribution (MRC) to the scheme. For a state that contributes funds to the system, the MRC indicate the share of additional revenue that does not remain in the state because of increased transfer payments due to its increased fiscal capacity. For a state that receives funds out of the equalization system, the MRC indicate the share of additional revenues that does not remain in the state due to a reduction of the payments the state receives out of the equalization system because of an increase in its fiscal capacity. Hence, from a theoretical point of view the fiscal incentives for a state to improve its own tax base decrease the higher its MRC are, and the fruits of a growth promoting policy do not remain within the state but are redistributed to other states or the federal level (Koethenbuerger 2002; Buettner 2006; Berthold and Fricke 2006; Bucovetsky and Smart 2006; Feld et al. 2012; Baskaran et al. 2017).

To what extent the concrete incentive effects of MRC influence local fiscal and economic policies in Germany’s fiscal federalism has been analyzed for the municipal and state levels. For the municipal level, Buettner (2006) shows that municipalities in the state of Baden-Wuerttemberg increased their business tax rate after an increase in the MRC of the municipal equalization scheme. Egger et al. (2010) exploit a natural experiment in the state of Lower-Saxony where the municipal equalization scheme was reformed in the year 1999 and confirm the results of Buettner (2006). Egger et al. (2010) argue that the equalization scheme compensates municipalities for the erosion of their tax base due to higher tax rates. Hence, fiscal equalization lowers jurisdictions’ incentives to attract mobile production factors through lowering tax rates. Buettner et al. (2011) find similar results, showing that attempts by the state level to extract fiscal resources from municipalities result in higher tax rates at the local level. Hauptmeier (2007) focuses on expenditure effects for municipalities in Baden-Wuerttemberg. He shows that higher MRC have negative effects on municipal investment spending, measured as a fraction of the overall municipal budget. He argues that it becomes less attractive for a municipality to maintain its tax base through public investment the more the revenues that a municipality can attain from this tax base are skimmed by the equalization scheme.

For the state level, three studies investigate the impact of the equalization scheme’s MRC on state fiscal policies. Hauptmeier (2009) focuses on public expenditures and shows for the period between 1980 and 2003 that increased MRC reduced state spending for infrastructure and education. Baretti et al. (2002) calculate the annual MRC in the German state equalization scheme for the period between 1970 and 1998 and provide evidence that MRC affected state revenues. They show that higher contribution rates to the equalization scheme had a negative effect on the tax revenues of the ten West German states. Following their results, an increase of the MRC of one percentage point reduces a state’s tax revenues relative to GDP by 0.0096 percentage points. Boenke et al. (2017) use a similar framework for the years 1998, 2001 and 2004. According to their results, the tax collection effort of a state is lower, the higher MRC are. That higher contributions to fiscal equalization affects the tax rate set by states is shown by Buettner and Krause (2021). Their results indicate that, in the case of full equalization, states set the rate of the real estate transfer tax 1.3 percentage points higher than without.

All of these studies confirm that high MRC incentivize a jurisdiction to reduce its efforts in improving its economic and fiscal situation and show that, although tax revenues are not a direct policy parameter, the expected changes in tax revenues impact direct policy parameters such as tax rates that are likely to affect a state’s tax base. However, for their empirical applications, the authors only calculate MRC for single years or for limited time periods and do not trace the system’s fiscal incentives over time. Moreover, most of them only consider an increase in the income tax for their calculation of a state’s MRC. Increases of other taxes that are relevant for a state’s contribution to the equalization scheme, such as the corporate tax or the VAT are not considered. Hence, the MRC which are calculated by them tend to be too low. Moreover, for state policymakers it is the overall burden of fiscal equalization which incentivizes their policies instead of focusing on the effects of equalization on single revenue sources only. Given these limitations, this paper, for the first time, quantifies the fiscal incentives of the German state equalization scheme for each federal state and every fiscal year since 1970, while taking into account all relevant revenues and distributive steps of the equalization system and calculating the overall burden that fiscal equalization exerts on a specific federal state.

3 Germany’s system of fiscal equalization

In Germany’s federalism, the Laender constitute an autonomous federal tier, while the municipalities are an integral part of the state level. To enable the states and their municipalities to fulfill their constitutional tasks, public revenues are distributed towards the different jurisdictions throughout a multi-layered fiscal equalization scheme. This scheme becomes necessary due to two obligations the German constitution (Grundgesetz or Basic Law) sets for the states and the federal government. The Basic Law entitles the states to receive a high enough share of overall public revenues that enables them to fulfill their constitutional tasks (Art. 107 of the Basic Law). Moreover, the Basic Law establishes homogeneous living conditions among all citizens in the federation as a constitutional obligation (Art. 72 of the Basic Law). Thus, the constitution establishes not only an allocative, but also a highly (re-)distributive goal of the equalization system.Footnote 1

3.1 The equalization system from 1970 until 2019

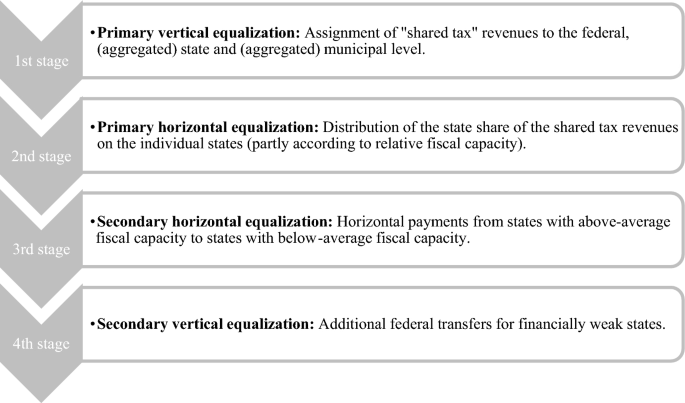

The state fiscal equalization scheme that was effective from 1970 until 2019 comprised four stages. In the first stage, revenues from the so-called “shared taxes” were assigned to the federal and (aggregated) state and municipal levels. These “shared taxes” are the income tax, the corporate tax, the capital (income) tax and the value-added tax (VAT).Footnote 2 Revenues from these shared taxes have been distributed to the (aggregate) state and municipal levels according to fixed shares (see Table 1).

In the second stage of the equalization scheme, the tax shares that had been assigned to the aggregated state level were distributed between the individual states. For the income and corporate tax, this redistribution was based on the tax’s occurrence. For the VAT, up to 25% of the overall aggregated state-share of VAT revenues were assigned to those states that had below-average per-capita tax revenues. The remaining 75% of the state share of VAT revenues were assigned to the states based on their population. Per-capita tax revenues comprised revenues from the income tax, the corporate tax and various state and municipal taxes. As states and municipalities can decide on the rates of some of their taxes autonomously, not actual tax revenues were considered. Instead, imputed tax revenues based on the average tax rates of all states entered the calculation of a state’s tax strength.

The distribution of VAT revenues based on the states’ tax revenues already induced a strong horizontal redistribution of state revenues. Contributing states were those states that were worse-off compared to a distribution of VAT revenues that would have been based on population figures only. This redistributive effect showed up in a change of the revenue ranking for some states. For instance, the state of North-Rhine-Westphalia which had an above-average tax strength before the distribution of VAT revenues arrived at a below-average tax strength after the redistribution of VAT revenues. Thus, it turned from a contributing state in the second stage of the scheme to a receiving state in the subsequent stages of the equalization scheme (Fig. 1).

Source: Own depiction

The stages of the federal fiscal equalization scheme before 2020.

In the third stage of the equalization scheme, differences in per-capita tax revenues were levelled out through horizontal transfers from states with an above-average fiscal capacityFootnote 3 to those states with a below-average fiscal capacity. These transfers were calculated according to a schedule that changed several times since 1970 (see Fig. 2). There were three differences in the calculation of the fiscal capacity of a state in this stage, as compared to the stage before. First, in this stage, revenues from the VAT, from royalties and 64% of municipal tax revenues entered the calculation of a state’s per capita fiscal capacity. Again, not actual revenues from municipal taxes entered the calculation, but imputed revenues based on average tax rates. Second, to consider alleged additional financial needs, the population numbers of the city states Hamburg, Berlin and Bremen were weighted with the factor 1.35, while the population numbers of sparsely populated states were also multiplied by factors greater than oneFootnote 4 in order to increase the calculated fiscal needs of these states. Third, since 2005, increases in a state’s per capita tax revenues of up to 12% do not enter the calculation of a state’s fiscal capacity and thus remain within the state of occurrence. This so-called “premia-model” aims at reducing the skimming of additional tax revenues to improve the incentives of the equalization scheme.

Source: Own depiction

Schedule for the horizontal equalization over the five reform periods.

The fourth and last stage of the old equalization scheme comprised two sorts of vertical transfers from the federal level to specific states. “General federal transfers” (GFT; Allgemeine Bundesergänzungszuweisungen, ABEZ) were granted as non-earmarked grants to those states that still had a fiscal capacity below 99.5% of the average fiscal capacity of all states after the previous three stages of the equalization scheme. The remaining fiscal gap to 99.5% of the average fiscal capacity was then closed at a rate of 77.5%. In addition to the GFT, the federal government also granted “specific federal transfers” (SFT; Sonder-Bundesergänzungszuweisungen, SoBEZ), independently of the fiscal capacity of a state which aimed to compensate individual states for special fiscal needs.

3.2 The equalization system since 2020

In 2016, the federal government and the state governments agreed to rearrange the fiscal relations between the states as well as between the states and the federal government from 2020 onwards. The two horizontal stages of the equalization scheme described above have been fully replaced by an expanded distribution of VAT revenues that is now augmented by surcharges and deductions based on the per capita fiscal capacity of a state. States with a below average per capita fiscal capacity receive surcharges to their population-based VAT shares, while states with an above average per capita fiscal capacity face deductions from the VAT share that would be assigned to them purely based on their population numbers. Both, surcharges and deductions, follow a proportional schedule that closes 63% of the gap between a state’s per capita fiscal capacity and the average per capita fiscal capacity of all states. With two exceptions, the fiscal capacity of a state is calculated in the same way as in the third stage of the old system. First, municipal taxes are now included into the calculation of a state’s fiscal capacity with a discount factor of 75% instead of 64%. Second, state revenues from royalties are included with a discount factor of 33% only, instead of 100%. Other elements, for instance increased population weights for specific states or the premia model remained parts of the calculation of a state’s fiscal capacity. Vertical GFT from the federal government to specific states also remained part of the equalization system. Those states that still show a fiscal capacity of less than 99.75% of the average fiscal capacity of all states after the VAT distribution continue to receive GFT that close the fiscal gap to 99.75% at a rate of 80%. Note that both, the rate of the schedule and the schedule’s threshold have been increased from 77.5 to 80% and 99.5 to 99.75%, respectively.

As a new element, new SFT have been included into the new system. Those states with municipal tax revenues of less than 80% of the average municipal tax revenues of all states receive vertical transfers (SFT) that, at a rate of 53.5%, close the gap between a state’s municipal tax revenues and 80% of the average municipal tax revenues of all states. Scherf (2020b) argues that these SFT de facto replace former SFT that were granted to East German states to compensate them for politically defined special fiscal needs, independently of their actual fiscal capacity. This new instrument extends the skimming of additional tax revenues to the municipal level. Hence, the new SFT are expected to increase the system’s MRC significantly (Buttner and Goerbert 2016; Scherf 2020b). Besides the SFT for states with below-average municipal tax revenues, the federal level continues to grant additional SFT independently of a state’s fiscal position, e.g., for states with below-average research funding from the federal government.

Although the reform led to major formal changes, there have been hardly any changes that would be substantive to the system’s impacts or to its incentives (Scherf 2020b). Instead, the elements of the old scheme have been transformed into new redistributive instruments. Most of these new instruments are expected to even worsen the incentives the system exerts (Scherf 2020b; Buettner and Goerbert 2016; Feld et al. 2016). However, quantitative evidence on the fiscal incentives of the new scheme is missing so far.

4 Simulation model

To quantify and trace the fiscal incentives that the equalization system and its reforms exert on the states, we calculate the MRC for each state and year for the period between 1970 and 2021. For our calculation, we set up a simulation model of the German fiscal equalization scheme and use the ex-post data on actual tax revenues. In our model, we use the exact numbers that entered the calculation of the equalization transfers in the respective year for the respective state based on the annual accounts of the Federal Ministry of Finance. Thus, our simulations yield the exact ex-post MRC each state faced in every fiscal year. Note, that the calculated MRC could be endogenous if a state adapts its policy to yield a specific (expected) MRC in the course of the year. This should, however, not cause biased simulation results. The reason for this is that state policymakers can form their expectations on their state’s MRC in year t only on the MRC in year t-1. As the MRC for an individual state within the existing system should however be largely constant, we do not expect that policy changes of a state within a fiscal year are prone to substantially influence the actual ex-post MRC.

Our simulation model is based on a methodology of the German Council of Economic Experts (GCEE 2014) and the existing literature (Baretti et al. 2002; Buettner 2006; Boenke et al. 2017). After replicating the calculation of all equalization payments between the federal level and the states based on the actual revenues of each state in each year,Footnote 5 we apply the following two steps, which are applied separately for each state. First, we ficticiously increase those tax revenues in state A which accrue to the state level. Those are the state shares of the income and corporate tax, the genuine state taxes and municipal taxes. We assume an increase in state A’s tax revenues by a marginal rate of 0.1%, which can be regarded as an increase in a state’s tax base.Footnote 6 Thus, we calculate the average MRC across all state revenue sources. Second, we calculate the marginal retention rate of state A. The retention rate yields the share of the increased tax revenues that remains in state A. We calculate the retention rate as the ratio of the increased tax revenues from state A over the amount of the increase in tax revenues that remains in state A after applying all steps of the state fiscal equalization scheme in order to properly consider all skimming effects. Subtracting the marginal retention rate from one yields the marginal rate of contribution to the equalization scheme.Footnote 7

We set up separate simulation models of the entire equalization scheme for each year for two reasons. First, the absolute and relative contribution rate of a state depends on its relative position among the other 15 states and, thus, on the actual tax revenues of itself and of every other state in each year. Second, we need to recalculate every annual (major and minor) change in the legal framework of the equalization scheme so that our calculations exactly mirror the scheme that was effective each year in every detail. Note, however, that our replication of the fiscal equalization scheme deviates from the actual scheme in one respect. While municipal taxes entered the actual scheme discounted with a factor smaller than one, we include them without a discount factor in our baseline calculations for two reasons. First, in Germany’s fiscal federalism the states are responsible to endow the municipalities with sufficient funds. Thus, for state policymakers the municipalities’ fiscal capacity and their contribution to the equalization scheme is of similar importance as the state’s fiscal capacity itself. Second, the discount factor to which municipal tax revenues were included in the calculation of a state’s fiscal capacity changed several times since 1970. As the factor to which municipal taxes are considered in the calculation of a state’s fiscal capacity directly influences its MRC (the higher the discount factor, the higher the influence of a change in municipal tax revenues on transfer payments) we need to hold the discount factor constant to evaluate the ceteris paribus effects of the reforms of the equalization schemes as well as of each element on the development of a state’s MRC.

Holding the discount factor constant across years yields results that differ from actual MRCs realized by the states. To avoid misleading results of our replication model resulting from differences to the actual fiscal equalization scheme, we run an extension of the simulation model in which we include municipal taxes with the discount factor that was effective in the respective years, thus calculating real marginal effects in addition to the stylized ceteris paribus effects with a constant discount factor. The results of this extension show that actual MRC have been slightly smaller compared to the MRC calculated in our model (see Sect. 6). However, comparing the results of the model with a constant discount factor with those of the model with changing discount factors shows that the replication with constant discount factors is tracing the effects of the different reforms of the schemes on MRC more precisely. Thus, the advantages of holding the discount factor constant described above outweigh the potential drawbacks.

Apart from numerous minor changes, the German fiscal equalization scheme underwent five major reforms since its establishment in the year 1970:

-

Reform Period I (1970–1987): Fiscal Reform Act of 1969 and introduction of the horizontal redistribution scheme.

-

Reform Period II (1988–1994): Introduction of the GFT.

-

Reform Period III (1995–2004): “Solidarity Package I” (integration of the East German states and introduction of the SFT).

-

Reform Period IV (2005–2019): “Solidarity Package II” (conversion to a continuous schedule, introduction of a premia model into the calculation of a state’s fiscal capacity).

-

Reform Period V (since 2020): General revision of the equalization scheme (elimination of the explicit horizontal stage, expansion of the fiscal capacity based distribution of VAT revenues, introduction of SFT for states with relatively low municipal tax revenues).

Aside the introduction of the GFT in 1988, the periods differ in the applied equalization schedule and in the calculation of a state’s fiscal capacity. Between 1970 and 2004, a discrete schedule was applied. Between 2005 and 2019 this schedule was changed to a linear-progressive one. Since 2020, the horizontal redistribution follows a proportional schedule of the marginal transfer functions as depicted in Fig. 2.

Scherf (2020a) shows that unadjusted MRC can also be calculated without simulating the entire equalization system. Instead of running simulations, he sets up a system of equations to calculate a state’s marginal contributions across the different steps of the equalization scheme. The approach of Scherf (2020a) has the advantage that a complicated simulation of the whole system is no longer needed. Moreover, his system of equations allows the observation of the skimming effects for single tax sources of states and municipalities. There are, however, two downsides of this approach. First, the approach is easy to implement for the post 2019 system with a proportional schedule and without the complicated two-stage horizontal redistribution of revenues that was effective before 2020. Second, his approach ignores repercussion effects of a single state’s increased tax revenues on average tax revenues of all states. Thus, his approach overstates MRC compared to effective marginal contributions to the equalization system.Footnote 8

5 The development of the system’s fiscal incentives since 1970

The development of the system’s fiscal incentives measured as MRC since 1970 is depicted in Fig. 3. The MRC calculated in our simulations show that the German state fiscal equalization scheme constantly induced a high skimming of additional tax revenues and, thus, unfavorable fiscal incentives, especially for transfer receiving states. For some of them the equalization scheme induced an up-to complete skimming (for the post 2019 system even an over-skimming) of additional revenues. However, there were notable differences in MRC levels across different reform periods. These differences can be attributed to three elements of the equalization scheme: First, the schedule of the horizontal redistribution; second, vertical payments from the federal level that depend on a state’s fiscal capacity; third, the procedure to calculate a state’s fiscal capacity.

Source: Own depiction based on simulations

MRC of contributing and receiving states 1970–2021. *States that changed their status as contributor or receiver are classified according to the status which they hold for more years. Municipal revenues fully included.

5.1 Reform period I: financial reform act of 1969 and introduction of the horizontal redistribution scheme

During the first reform period (1970–1987), the core elements of the equalization scheme have been the horizontal, fiscal capacity based redistribution of VAT revenues and direct horizontal transfer payments between the states. The equalization schedule that was effective between 1970 and 1994 induced a complete skimming of additional tax revenues of a state at a relative per-capita fiscal capacity of ≥ 110% of the average per-capita fiscal capacity of all states. On the contrary, if a state had a relative per-capita fiscal capacity below 93% of the average per-capita fiscal capacity of all states, it received funds through the equalization scheme to completely fill the gap between its actual fiscal capacity and 93% of the average per-capita fiscal capacity of all states (see Fig. 2).

Moreover, the equalization payments followed a differential schedule according to which the skimming and the granting of funds was increased in brackets. The fiscal incentives of such a differential schedule are unfavorable, independently of its concrete design. These unfavorable effects originate in the situation of a state with a fiscal capacity that comes close to one of the schedule’s thresholds. If this state increased its fiscal capacity marginally, it ended up in the next schedule-bracket which led to a sharp increase in transfer payments or a sharp decrease in transfer receipts and thus particularly high MRC.Footnote 9

Our simulations confirm high MRC for the first reform period (see Figs. 3 and 4). For contributing states, our calculations yield MRC between 50% (North-Rhine-Westphalia in 1976) and 98% (Hamburg in 1973), though Hamburg is an outlier due to its high fiscal capacity, while the low level of MRC of North-Rhine-Westphalia is a forerunner of its status as a state changing sides from a contributing to a receiving state. The distribution of VAT revenues based on states’ tax revenues induced a strong horizontal redistribution of state revenues. Contributing states were those that were worse-off compared to a distribution of VAT revenues that would have been based on population figures. This redistributive effect showed up in a change of the revenue ranking for some states. For instance, North-Rhine-Westphalia which had an above-average tax strength before the distribution of VAT revenues arrived at a below-average tax strength after the redistribution of VAT revenues becoming a receiving state subsequently.

Source: Own depiction based on simulations. Municipal revenues fully included. – Abbreviations: BY: Bavaria; BW: Baden-Wuerttemberg; HE: Hesse; NW: Northrhine-Westphalia; HH: Hamburg; HB: Bremen; NI: Lower-Saxony; BE: Berlin; RP: Rhineland-Palatinate; SN: Saxony; SH: Schleswig–Holstein; BB: Brandenburg; TH: Thuringia; ST: Saxony-Anhalt; MV: Mecklenburg-Westpommerania; SL: Saarland

MRC and equalization schedule in reform periods I and II (1970–1994).

5.2 Reform period II: differential schedule and introduction of general federal transfers

In the second reform period, horizontal equalization continued to follow a differential schedule. We illustrate the effects of this schedule on MRC of transfer receiving states on the basis of some examples based on our simulations. During the years in which Rhineland-Palatinate ended up in the lowest bracket of the schedule (e.g., 1974), its MRC have been much higher than in the years 1975–1978 and 1985–1986 when it fell into the bracket next to the average fiscal capacity of all states. The significant effects of the schedule’s thresholds also appear in the case of Schleswig–Holstein in the years 1990 and 1994. Because of full compensation of its gap in fiscal capacity within the lowest bracket of the schedule, changing its position from the lowest to the next higher bracket of the schedule made a significant difference in the amount of transfer payments the state received. Consequently, this led to high MRC for Schleswig–Holstein in those years. The same effect can be observed for Bremen in the midst of the 1970s. Switching from one schedule bracket to the other also had unfavorable effects for contributing states as can be observed for Hesse in 1993 and 1994. Hesse had an extraordinarily high fiscal capacity in these years and ended up in the highest bracket of the schedule, which led to a full skimming of additional tax revenues that exceeded 110% of the average fiscal capacity of all states.

While the differential schedule induced disincentives through an almost complete skimming of additional revenues for states with a particularly high or a particularly low fiscal capacity, it led to nearly no skimming of additional revenues for states with a fiscal capacity close to the average fiscal capacity of all states (see Fig. 4). This can exemplarily be observed for the state of North-Rhine-Westphalia. At the beginning of the 1980s the fiscal capacity of North-Rhine-Westphalia before and after the first stage of the equalization scheme was slightly above the average fiscal capacity of all states. With the differential schedule this meant that neither a skimming nor a compensation of additional revenues took place. Instead, the state entirely fell out of the horizontal stages of the equalization scheme, which explains the strikingly low MRC of North-Rhine-Westphalia in those years. The low skimming of additional revenues around the average fiscal capacity of all states can also be observed if a state changed its status from a receiving to a contributing state and vice versa. North-Rhine-Westphalia changed its status from a contributing to a transfer receiving state during the years 1991–1993 such that the state again fell out of the horizontal elements of the equalization scheme. The same effect can be observed for Bavaria that changed its status from a transfer-receiving to a contributing state in 1991. In this year, Bavaria also fell out of the horizontal elements of the equalization scheme. Subsequently, both states show no or only very low MRC during the respective transition periods.

With the introduction of the general federal transfers (GFT) in the year 1988, the scheme was amended by its first vertical redistributive element. However, the introduction of GFT only slightly changed the development of MRC (see Fig. 3) compared to the period before 1988. This can be attributed to the low volume of these vertical transfers compared to the dominating and unchanged horizontal elements of the scheme as well as to the unchanged equalization schedule. This does, however, not mean that the newly introduced vertical instrument would have been irrelevant for states’ MRC. The case of Lower-Saxony in the year 1993 shows how the GFT increased the MRC and, thus, fiscal disincentives for single states distinctly. In 1993, Lower-Saxony yielded a relative per-capita fiscal capacity that equalled the average per-capita fiscal capacity of all states. According to the equalization schedule, with a relative fiscal capacity that equalled the average fiscal capacity of all states, Lower-Saxony neither paid nor received transfers out of one of the horizontal components of the equalization scheme. Thus, the simulated MRC of 47% can be fully attributed to general federal transfers (Figs. 3 and 4).

The introduction of the GFT also shows how the scheme’s different thresholds lead to sharp increases and erratic jumps in a state’s MRC. This can be seen for the states of Bavaria and Northrhine-Westphalia during the first reform period, when these two states switched from a transfer receiving to a contributing status and vice versa. Identical effects can be observed for Schleswig–Holstein and Lower Saxony in the second reform period, when the fiscal capacity of those states fluctuated around the threshold that entitled them to receive GFT.Footnote 10

5.3 Reform period III: solidarity package I and integration of East German states

The transition from the second to the third reform period (1995–2004) shows a pronounced increase in the MRC for most of the states. The reason for this is the integration of the East German states into the equalization scheme and the associated deferrals of the relative per-capita fiscal capacities of the West German states. While in the previous periods only Saarland, Bremen and Schleswig–Holstein were confronted with MRC of above 90%, from 1995 onwards all East German states were additionally confronted with MRC of above 90%. The reason for this was the high volume of received transfers compared to the weak own tax base of the eastern states in the years after German reunification (see Figs. 3 and 5).

Source: Own depiction based on simulations. Municipal revenues fully included

MRC and equalization schedule in the reform period III (1995–2004).

The equalization schedule was slightly changed in 1995. Additional revenues that overshot 110% of the average fiscal capacity of all states were not skimmed completely anymore. However, the differential schedule and the full replenishment to a per-capita fiscal capacity of 93% of the average per-capita fiscal capacity of all states remained and so did most of the unfavorable fiscal incentives discussed above (see Figs. 3 and 5).

5.4 Reform period IV: “solidarity package II”

With the expiration of the transition period to include the East German states into the fiscal equalization scheme and the associated reform of the scheme in 2005, MRC have been reduced markedly. This becomes most obvious with regard to the transfer receiving states (see Fig. 3). While our simulations indicate an almost full skimming of additional tax revenues in the previous scheme for several states, the maximum MRC that we calculate for this reform period is 89% (Mecklenburg-Western-Pomerania in 2013) (see Fig. 6). The reason for the reduction of the MRC can be found in two changes of the equalization system.

Source: Own depiction based on simulations. Municipal revenues fully included

MRC and equalization schedule in the reform period IV (2005–2019).

First, the differential schedule that was effective since 1970 was replaced by a continuous linear-progressive formula-based schedule. Hence, the brackets of the differential schedule and the associated jumps in the skimming of additional revenues at their thresholds no longer existed (see Fig. 6). Subsequently, MRC that were high at these thresholds formerly were reduced through the change of the schedule. The continuous schedule also caused the zone without any skimming around the average fiscal capacity of all states to be ceased, which, ceteris paribus, should have increased MRC. However, the newly induced skimming of additional revenues around the average fiscal capacity of all states was overcompensated by the reduction of the skimming effects at the former thresholds of the differential schedule and in the tails of the distribution of fiscal capacities among the states.

Second, to reduce the skimming of additional revenues, a so-called “premia model” was included into the calculation of a state’s fiscal capacity. Since 2005, increases in a state’s per capita tax revenues of up to 12% above the average increase of the fiscal capacity of all states do not enter the calculation of a state’s fiscal capacity. Thus, an increase in a state’s tax revenues was no longer fully included into the calculation of the transfers a state had to pay to or was entitled to receive out of the equalization scheme. According to our simulations this reduced MRC for transfer receiving states markedly (see Fig. 3). The city state of Hamburg shows that the premia-model also exerted MRC reducing effects on contributing states (see Fig. 6). However, for the other contributing states, the MRC remained almost unchanged. This can be explained by the ceasing of the zone without any skimming around the average fiscal capacity of all states, which overcompensates the premia model for the other contributing states.

Due to the implementation of the continuous schedule and the premia model, the outliers that we found when a differential schedule was applied are no longer present (see Fig. 6). Note, however, that our simulation model yields reduced MRC after 2005 mainly because we assume a constant and full inclusion of municipal tax revenues when calculating the per-capita fiscal capacity of a state. In the actual equalization scheme, the MRC reducing effect of the reform of 2005 was partially compensated by an increase of the discount factor to which municipal taxes entered the calculation of a state’s fiscal capacity from 50 to 64% (see Appendix 2). This increase expanded the skimming effects of the scheme on municipal revenues and offset most of the reduction of MRC achieved through the reform elements discussed above (Scherf 2007).

5.5 Reform period V: general revision of the equalization scheme

With the expiration of the Solidarity Package II in 2020, the equalization system underwent significant changes. Formally, the most important change was the conversion of the horizontal stages of the equalization system into vertical surcharges and deductions on a state’s VAT share that follow a proportional schedule of 63% and have horizontal redistributive effects. Our simulations show that the newly introduced proportional schedule that replaced the former linear-progressive one reduced MRC. This can be seen at the MRC of the two contributing states Bavaria and Baden-Wuerttemberg. Both states show reduced MRC compared to the pre-2020 system (see Fig. 7 and Table 2). However, the introduction of the proportional schedule is the only element of the reform that improved the fiscal incentives to maintain their tax bases that the equalization system exerts on the states.

Source: Own depiction based on simulations. Abbreviations: BY: Bavaria; BW: Baden-Wuerttemberg; HE: Hesse; NW: Northrhine-Westphalia; HH: Hamburg; HB: Bremen; NI: Lower-Saxony; BE: Berlin; RP: Rhineland-Palatinate; SN: Saxony; SH: Schleswig–Holstein; BB: Brandenburg; TH: Thuringia; ST: Saxony-Anhalt; MV: Mecklenburg-Westpommerania; SL: Saarland

Change in MRC after the 2020 reform of the fiscal equalization scheme.

While the conversion of the horizontal stages into the VAT distribution has been the most important change formally, substantively the expansion of the GFT and the introduction of SFT for states with relatively low municipal tax revenues turned out to be equally important for the fiscal incentives created by the system’s latest reform. This becomes obvious regarding the transfer receiving states. For most of them our simulations yield sharp increases in MRC with an over-skimming of additional tax revenues, i.e., a reduction of transfers that is greater than the increase in a state’s tax revenues. While parts of the MRC increase and the over-skimming of additional revenues are caused by the expansion of the GFT, large parts of MRC increases as well as the over-skimming of additional revenues can also be attributed to the newly introduced SFT for under-proportional municipal tax revenues. Moreover, and in line with Scherf’s (2020a) findings, our simulations show that states that receive the new SFT surpass states that exhibited a higher fiscal position before equalization in the ranking of fiscal capacity.

Given both, the over-skimming of additional revenues and the change in the ranking of fiscal capacity, the new SFT render it fiscally unattractive for a state with relatively low municipal tax revenues to improve its own revenue situation.Footnote 11 The over-skimming could even lead to a situation where states are incentivized to impair the tax base of their municipalities as they would fiscally benefit from a deterioration of their municipal tax base post equalization.

The only state for which the MRC declined compared to the pre-2020 system is Rhineland-Palatinate. This can be attributed to the changing status from a receiving towards a contributing state in 2021, which is caused by windfall tax revenues from a single company, the vaccine manufacturer Biontech which resides in Rhineland-Palatinate. For Rhineland-Palatinate attaining the status of a contributor outweighed the disincentive effects of the reform itself.

As the increase in MRC for the remaining transfer receiving states is mainly driven by the relative fiscal position of the municipalities of a state, our assumption to include municipal tax strengths without any discount factor could bias our results upwards. To assure that we are not overestimating MRC because of not including a discount factor, we run our simulations applying the system’s actual discount factor of 75%. Furthermore, to ensure that results are neither driven by changes in tax revenues during the downturn of the COVID 19 pandemic, we additionaly run our simulations for the post 2020 system with tax data of 2019. Our results show that including the discount factor and using tax data of 2019 leaves MRC almost unchanged.

Our results regarding aggregated MRC in the post 2019 equalization system are in line with the results of Scherf (2020a). As expected, the MRC calculated in our simulation model are lower than those derived by Scherf (2020a). The reason for this are repercussion effects of an increased fiscal capacity of a state on the average fiscal capacity of all states that are reflected in our simulation model but not in Scherf’s (2020a) analysis.

6 Comparing full inclusion of municipal revenues with discouted municipal revenues

In order to be able to assess ceteris paribus effects of individual reform steps of the fiscal equalization scheme on MRC, we deviated in our calculations from the actual design of the scheme and fully included municipal tax revenues into the calculation of a state’s fiscal capacity. In order to avoid drawing false conclusions about the impact of individual reform steps on the MRC due to this deviation from the actual design of the scheme, we calculate the MRC for each state and each year additionally taking into account the actual rate at which the tax revenues of a state's municipalities have been included in the calculation of the state's fiscal capacity.

Results are reported in Fig. 8 and, for individual states and years, in the table in Appendix 2 and the graphs in Appendix 3. They show that when the actual discount factors are taken into account, a state's MRC follow the same pattern within the reform periods in which this discount factor was constant as when we include municipal tax revenues completely. Interestingly, for some states and years, the MRC is even higher if we use discounted municipal tax revenues, as compared to a full inclusion of municipal revenues. While this result seems counterintuitive at first glance, it can be explained by deviating changes in municipal tax revenues from the changes of state tax revenues. A notable difference in the pattern of MRC only occurs for Reform period IV, in which the discount factor was increased from 50 to 64%. Our results show that this increase in the discount factor outweighed the positive effect of the premia model on a state’s MRC. Thus, the positive ceteris paribus reform effect of the premia model can only be identified, if we hold the discount factor constant.

Source: Own depiction based on simulations. Municipal tax revenues fully included. States are classified as contributors and receivers according to their status in the respective year

Development of MRC for the federation 1970–2021.

7 Conclusions

In designing Germany’s state fiscal equalization scheme, the states and the federal government face the trade-off between redistributing diverging fiscal resources across states effectively without eliminating the fiscal incentives for a state to maintain and improve its tax base by own efforts. This paper is the first to provide a comprehensive quantification of the fiscal incentives that Germany’s state fiscal equalization scheme exerted on each state in every year since the establishment of the equalization scheme in 1970 to its latest reform in 2020. To quantify the fiscal incentives of the equalization scheme, we calculated each state’s marginal rates of contribution to the scheme over 50 years and the scheme’s five major reforms. To calculate the states’ MRC, we developed a simulation model of Germany’s equalization scheme based on all relevant revenues, all stages of the scheme and considering all of its reforms.

Our simulations yield MRC at constantly high levels (see Fig. 8). For transfer receiving states, the system skimmed additional revenues almost fully and, since 2020, more than completely. Thus, in designing the fiscal equalization scheme the German states and the federal government decided to achieve horizontal and vertical redistributive goals. This comes at the cost of favorable fiscal incentives for the states to maintain and improve their own tax bases, especially if a state’s fiscal position lies way below the average per capita tax revenues of all states. Thus, the scheme tends to cement the economic and fiscal gaps between states with above and below average tax revenues (Henkel et al. 2021). The only two exceptions in which a state improved its fiscal position and switched its status from a receiving to a contributing state have been Bavaria and Rhineland-Palatinate, the latter only due to the single case windfall tax revenues of the vaccine manufacturer Biontech. Although these results have been expected, comprehensive evidence was missing so far.

Since 1970, the equalization scheme was reformed five times. Our results show that, from all five reforms, only the reform of 2005 induced a reduction of the states’ MRC and thus, an improvement in the fiscal incentives that the scheme had on the states to maintain and improve their tax base. However, a comparison of Panel A and B of Fig. 8 indicates, that this effect only unveils if we disregard the simultaneous increase of the discount rate to which municipal revenues enter the calculation of a state’s fiscal capacity. All other reforms caused increases in MRC and worsened the fiscal incentives the equalization scheme had on the federal states. Notably, most of the reforms followed the same pattern. While the skimming effects of the horizontal schedule have been gradually reduced in each of the reforms since 1995, extended and additional vertical transfer elements and an increased inclusion of municipal revenues into the calculation of a state’s fiscal capacity caused an additional skimming of state revenues.

These newly caused vertical skimming effects did mostly exceed the reduction in the horizontal skimming of state revenues. This is especially the case for the system’s latest reform in the year 2020 that pushed MRC to a historic height. Focusing on MRC and fiscal results of the German equalization scheme may disregard additional effects of fiscal equalization.

Studying the effects of the high MRC in the German fiscal equalization scheme on policy measures of the states based on the comprehensive data of this paper provides scope for future research. Note, however, that our simulations yield the states’ ex-post MRC. For the incentive effects of the equalization scheme, anticipated (ex-ante) MRC should however be more relevant. Although anticipated MRC are not observable, they are likely to be approximated based on the realized ex-post MRC of the previous year. Thus, expected and realized MRC should be highly correlated. The only exception to this might occur when a state changes its status from a contributing to a transfer receiving state (and vice versa). In 2022, it has become known that the high profits of Biontech as the licence holder of the Pfizer/Biontech vaccine against the COVID 19-virus lead to such an increase in tax revenue that the state of Rhineland-Palatinate has become a net contributor to the new fiscal equalization system for the first time in the history of that state which is sharply reducing its MRC. It remains open how sustainable this outcome is. Still, it will be a very interesting case for future research. Finally, we focused on a quantification of the fiscal incentives of the German state fiscal equalization scheme. Fiscal incentives, however, are just one of several dimensions for fully assessing the efficiency and overall welfare effects of a fiscal equalization system.

Data availability

Data will be made available after publication.

Notes

Although this distributive goal is sometimes interpreted as a constitutional call on solving the trade-off between redistribution and favorable fiscal incentives for the states by entirely opting for the former, the German Constitutional Court explicitly made clear that “…the fiscal equalization scheme (…) is not an instrument to replace the (…) distribution of tax revenues by a system which is shaped by the sentiment of fiscal equivalence between the states, but does not consider the sovereignty and (fiscal) autonomy of the states anymore.” (GCC 1987).

While tax shares for the income, corporate and capital income tax are determined in the constitution, this is not the case for the VAT. VAT shares are set by simple law from the two chambers of parliament according to the fiscal needs of the different federal levels and changed over time accordingly.

In the first and second stage of the system only tax revenues have been regarded for the fiscal position of a state. Therefore, the tax capacity of a state was the relevant measure for redistribution in these stages. In the subsequent stages, also other revenues enter the calculation of a state’s fiscal position. Therefore, from stage 3 onwards, the fiscal capacity of a state is the relevant measure for a state’s fiscal position. Still, some revenues are not or not fully considered in the fiscal equalization system, e.g., revenues from economic activities.

Mecklenburg-West-Pomerania (with a factor of 1.05), Brandenburg (with a factor of 1.03) and Saxony-Anhalt (with a factor of 1.02) received this additional kind of population weighting.

We consider all stages of the equalization scheme. The calculated transfer payments are compared with the actual transfer payments in the respective year to ensure that our calculations yield the exact transfer payments in the respective year, considering all revenue sources, redistributive instruments and (minor and major) legal changes in the equalization scheme correctly.

The revenue increases that provide the basis for a skimming can only be assured by this marginal increase which must be considered as an increase of the tax base. Otherwise, a revenue increase that is due to a tax rate effect (instead of a base effect) would be endogenous and would induce interaction effects.

For further details of the simulation model see Appendix 4.

Being aware of this issue, Scherf (2020a) denotes the MRC calculated by him “unadjusted”.

Both, the marginal transfer/contribution and the transfer/contribution volume, increase. Whether the increase shows a kink or is continuous depends on the volatility of the tax base: the more volatile it is, the more probable is a kink..

If, e.g., Lower-Saxony increased its fiscal capacity marginally, it would no longer have been entitled for GFT, which induces a high MRC.

Also, from a theoretical point of view, these new SFT are highly problematic as they privilege the fiscal capacity of municipalities over that of the states (Scherf 2020b).

References

Baretti C, Huber B, Lichtblau K (2002) A tax on tax revenue. The incentive effects of equalizing transfers. Evidence from Germany. Int Tax Public Financ 9:631–649

Baskaran T, Feld LP, Necker S (2017) Depressing dependence. Transfers and economic growth in the German states. 1975–2005. Reg Stud 51:1815–1825

Berthold N, Fricke H (2006) Föderalismus und Wachstum. Eine vernachlässigte Beziehung. In: Empter S, Vehrkamp RB (Hrsg) Wirtschaftsstandort Deutschland. Wiesbaden, VS, pp 279–316

Boenke T, Jochimsen B, Schroeder C (2017) Fiscal equalization and tax enforcement. Ger Econ Rev 18:377–409

Bucovetsky S, Smart M (2006) The efficiency consequences of local revenue equalization. Tax competition and tax distortions. J Public Econ Theory 8:119–144

Buettner T (2006) The incentive effects of fiscal equalization transfers on tax policy. J Public Econ 90:477–497

Buettner T, Goerbert T (2016) Neuregelung des bundesstaatlichen Finanzausgleichs: Umverteilungs- und Verbleibeffekte. Wirtschaftsdienst 96:818–824

Buettner T, Schwager R, Hauptmeier S (2011) Efficient revenue sharing and upper-level governments. Theory and application to Germany. J Inst Theor Econ 167:647–667

Burret HT, Bury Y, Feld LP (2018) Grenzabschöpfungsraten im deutschen Finanzausgleich. List Forum Für Wirtschafts- und Finanzpolitik 44:1–22

Buttner T, Krause M (2021) Fiscal equalization as a driver of tax increases. Empirical evidence from Germany. Int Tax Public Financ 28:90–112

Egger P, Koethenbuerger M, Smart M (2010) Do fiscal transfers alleviate business tax competition? Evidence from Germany. J Public Econ 94:235–246

Feehan JP (2014) Canada’s equalization formula: peering inside the black box and beyond. SPP Res Paper. https://doi.org/10.2139/ssrn.2510557

Feld LP, Schnellenbach J, Baskaran T (2012) Creative destruction and fiscal institutions. A long-run case study of three regions. J Evol Econ 22:563–583

Feld LP, Kube H, Schnellenbach J (2013) Optionen für eine Reform des bundesdeutschen Finanzausgleichs. Gutachten im Auftrag der FDP-Landtagsfraktionen der Länder Baden-Württemberg, Bayern

Feld LP, Fuest C, Haucap J, Schweitzer H, Wieland V, Wigger BU (Kronberger Kreis) (2016) Für eine echte Reform der Bund-Länder-Finanzbeziehungen. Stiftung Marktwirtschaft. Study No. Berlin, 62

Fuest C, Thoene M (2009) Reform des Finanzföderalismus in Deutschland. Stiftung Marktwirtschaft, Berlin

GCC (German Constitutional Court) (1987) Verdict of the German Constitutional Court: Finanzausgleich I. Entscheidungen des Bundesverfassungsgerichts, 72, Tübingen

GCEE (German Council of Economic Experts) (2014) Mehr Vertrauen in Marktprozesse. Jahresgutachten 2014/15. Wiesbaden: Destatis

Hauptmeier S (2007) The impact of fiscal equalisation on local expenditure policies. Evidence from German municipalities. Mannheim: Zentrum für Europäische Wirtschaftsforschung. Discussion Paper 07-081

Hauptmeier S (2009) Fiscal competition and the impact of fiscal equalisation. Theory and evidence from Germany. Dissertation. München: Volkswirtschaftliche Fakultät der LMU München

Henkel M, Seidel T, Suedekum J (2021) Fiscal transfers in the spatial economy. Am Econ J Econ Policy 13:433–468

Hentze T (2015) Länderfinanzausgleich. Eine Bewertung aktueller Vorschläge zur Neuordnung der Bund-Länder-Finanzbeziehungen. Köln: Institut der Deutschen Wirtschaft. Policy Paper 29/2015

Koethenbuerger M (2002) Tax competition and fiscal equalization. Int Tax Public Financ 9:391–408

Leisibach P, Schaltegger CA (2019) Zielkonflikte und Fehlanreize: Eine Analyse der Anreizwirkungen im Schweizer Finanzausgleich. Perspekt Wirtsch 20:254–280

Scherf W (2007) Grenzbelastungen im Länderfinanzausgleich. Justus-Liebig-Universität. Finanzwissenschaftliche Arbeitspapiere, Gießen, pp 79–2007

Scherf W (2020a) Grenzbelastungen im Länderfinanzausgleich. Justus-Liebig-Universität. Finanzwissenschaftliche Arbeitspapiere, Gießen, pp 103–2020

Scherf W (2020b) Länderfinanzausgleich 2020: neue form—alte probleme. Wirtschaftsdienst 100:601–607

Scientific Advisory Board to the Federal Ministry of Finance (2015). Reform des bundesstaatlichen Finanzausgleichs. Berlin: BMF. Gutachten 01/2015

Acknowledgements

This paper extends and updates an earlier analysis by Burret et al. (2018) by particularly including the most recent reform of Germany’s fiscal equalization system in force since 2020. We thank Thiess Buettner, Clemens Fuest, Justus Haucap, Heike Schweitzer, Volker Wieland and Berthold Wigger for the discussion about the reform of the fiscal equalization system in Germany. We thank Heidrun Ganz, Christopher Hoegen, Amanda März, Johanna Schworm and Steffen Zetzmann for excellent research support.

Funding

Open Access funding enabled and organized by Projekt DEAL.

Author information

Authors and Affiliations

Contributions

Yannick Bury, Heiko T. Burret and Lars P. Feld developed the idea for and the design of the study. Yannick Bury and Heiko T. Burret collected the data and set up the simulation model. Yannick Bury conducted the simulations and wrote the first draft of the paper. Yannick Bury and Lars P. Feld revised the paper in its several stages of revision and edited the manuscript. Lars P. Feld ensured the financing of the study. All authors read and approved the content of the manuscript.

Corresponding author

Ethics declarations

Conflict of interest

The authors declare no competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendices

Appendix 1

See Table 3.

Appendix 2

See Table 4.

Appendix 3

See Fig. 9.

Source: Own depiction based on simulations

Graphs of MRC with discounted municipal revenues. *States that changed their status as contributor or receiver are classified according to the status which they hold for more years. Municipal revenues fully included.

Appendix 4: Simulation model

Our simulation model is based on a methodology of the German Council of Economic Experts and the existing literature (Baretti et al. 2002; Buettner 2006; GCEE 2014; Boenke et al. 2017). We focus on the level of the state and the horizontal redistribution of the scheme. Thus, we do not regard increased federal tax revenues due to the vertical distribution of shared taxes as component of a state’s MRC. In our model, we apply the following four steps. Note, that steps two to four are applied separately for each state.

-

1.

Replication of the calculation of all equalization payments between the federal level and the states based on the actual tax revenues of each state in each year. We consider all stages of the equalization scheme. The calculated transfer payments are compared with the actual transfer payments in the respective year to ensure that our calculations yield the exact transfer payments in the respective year, correctly considering all revenue sources, redistributive instruments and (minor and major) legal changes in the equalization scheme.

-

2.

Increasing all actually collected state-tax revenues in state A (stemming from the state shares of the income and corporate taxes, state taxes and municipal taxes) by a marginal rate of 0.1%.

-

3.

Calculation of the marginal retention rate of state A. The retention rate yields the share of the increased tax revenues that remains in state A. We calculate the retention rate as the ratio of the increased tax revenues from state A over the amount of the increase in tax revenues that remains in state A after applying all steps of the state fiscal equalization scheme.

-

4.

Calculation of the average marginal rate of contribution of state A across all revenues sources (1-marginal retention rate)

We set up separate simulation models of the entire equalization scheme for each year for two reasons. First, the absolute and relative contribution rate of a state depends on its relative position among the other 15 states and thus, on the actual tax revenues of itself and of every other state in each year. Second, we need to recalculate every annual (major and minor) change in the legal framework of the equalization scheme so that our calculations exactly mirror the scheme that was effective each year in every detail.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Bury, Y., Feld, L.P. & Burret, H.T. Skimming the achieved? Quantifying the fiscal incentives of the German fiscal equalization scheme and its reforms since 1970. Econ Gov 25, 291–334 (2024). https://doi.org/10.1007/s10101-024-00316-w

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10101-024-00316-w