Abstract

In this paper, the natural rate of interest in Denmark, Norway and Sweden is estimated. This is done by augmenting the Laubach and Williams (Rev Econ Stat 85:1063–1070, 2003) framework with a dynamic factor model linked to economic indicators––a modelling choice which allows us to better identify business cycle fluctuations. We estimate the model using Bayesian methods on data ranging from 1990Q1 to 2022Q4. The results indicate that the natural rate has declined substantially and in all countries is at a low level at the end of the sample.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

It is now a stylized fact that both nominal and real interest rates in OECD countries had been on a downward trend for several decades prior to the covid pandemic. The causes behind this development are disputed but lower global growth, increased income inequality, demographics, loose monetary policy, deleveraging, changes to government bond markets and shifts in saving and investment preferences are examples of factors put forward.Footnote 1 An additional explanation that is commonly suggested––and which clearly is related to some of the previously mentioned factors––is that the natural rate of interest has declined; see, for example, Holston et al. (2017), Rachel and Smith (2017) and Benati (2023).Footnote 2

From a monetary-policy perspective, a potential decline in the natural rate of interest is of particular relevance since it could indicate that the environment in which central banks are acting today is different to that of the 1990s when the inflation-targeting framework was adopted in many countries. For example, with a low natural rate, one can expect monetary policy to be constrained at the zero/effective lower bound more frequently and for longer periods of time. This means that central banks will have to rely on unconventional measures to a large extent if they want to be active in their conduct of monetary policy. Several aspects of unconventional measures can be considered problematic though. For example, Cecchetti and Schoenholtz (2020) pointed out that central banks’ purchases of corporate bonds should be considered fiscal policy and therefore undermines democratic accountability. Other aspects include that the central banks might induce excessive risk taking (IMF 2013; Altunbas et al. 2014; Beckmann et al. 2020; Adrian 2020; Riksbank 2021). In the light of the recent covid pandemic, these issues have only become more relevant as many central banks expanded their asset-purchase programs. The post-pandemic surge in inflation in many countries also highlights the importance of having an estimate of the natural rate, since it will provide an indication of where the future level of policy rates might be.

In this paper, we add to the discussion regarding the evolution of the natural rate of interest by providing new empirical evidence on this topic. More specifically, our purpose is to estimate the natural rate of interest in the Scandinavian countries––that is, Denmark, Norway and Sweden. This is done by augmenting the well-known Laubach and Williams (2003) framework with a small dynamic factor model that uses key economic indicators to help identify business-cycle fluctuations. We estimate the model using Bayesian methods on data ranging from 1990Q1 to 2022Q4.

In conducting our analysis, we make two specific contributions. First, we add empirical evidence on the evolution of the natural rate of interest. As pointed out above, falling interest rates have been an international phenomenon and it is accordingly relevant to study economies beyond those that typically receive the focus (such as the USA and the euro area). While being similar in several ways, the three Scandinavian countries studied here also come with some interesting variation; for example, while Sweden can be seen as a fairly traditional small open economy, Denmark has a fixed exchange rate vis-à-vis the Euro, and the Norwegian economy is highly influenced by the country’s oil production.

Second, we improve the popular Laubach and Williams (2003) framework, which has been used in a number of studies; see, for example, Garnier and Wilhelmsen (2009), Belke and Klose (2017), Holston et al. (2017) and Armelius et al. (2018). In Laubach and Williams’ model, the business cycle is described by an output gap, which in turn is a key determinant for price inflation. However, in most studies based on this framework, the information used to identify the output gap––and thereby also the natural rate of interest––has been quite limited; only a few variables and relationships have been employed. In this paper, we use a larger number of variables to identify the business cycle by linking a small dynamic factor model to Laubach and Williams’ model. In employing a larger information set to improve identification, we follow a line of research similar to that of Aastveit and Trovik (2014), Jarociński and Lenza (2018) and Barigozzi and Luciano (2019), who all used more variables in order to improve output-gap measures. Through our approach, we should produce better estimates of both the natural rate of interest and the output gap.

Concerning our results, we find a marked decline in the natural rate of interest in all three countries. Our estimates also indicate that most of this decline can be attributed to factors other than a decline in potential growth. During the Nordic banking crisis in the early 1990s, the natural rate seems to have been pushed up by exogenous factors. During the last couple of decades this has reversed, and these factors are now exerting a downward pressure on Scandinavian natural rates. Our results also point to a more active use of monetary policy in Sweden and Norway as compared to Denmark.

The covid pandemic introduces some difficulties in the estimation and the results for the post-pandemic years should be interpreted with some caution. The pandemic and related disruptions in global trade and value chains, as well as the war in Ukraine, are responsible for large swings in most of the variables included in our model near the end of the sample. Since these events are exogenous it is hard to interpret them within the model framework. However, we have still chosen to include all the available observations in the estimations since we think it is of interest to get an indication of where the natural rates are heading according to this framework. In the beginning of 2022, real interest rates dropped substantially in Denmark and Sweden (and somewhat in Norway) due to a rapid increase in inflation. Consequently, our natural rate estimates also drop. Our estimates of the real interest rate gap at the end of the sample are negative for Denmark and Sweden. While these as previously mentioned should be interpreted with caution, it can nevertheless be noted that this indicates that increasing policy interest rates should––at least in these two countries––contribute to a move towards a neutral monetary policy stance.

The remainder of this paper is organized as follows: In Sect. 2, we describe the model that we utilize. The data set is described in Sect. 3. In Sect. 4, we present the results from our empirical analysis. Section 5 concludes.

2 The model

Economic stabilization policies, as carried out by central banks and fiscal authorities, are based on the notion that economic variables can deviate from their “natural” levels, which gives rise to “gaps” such as the output gap. The task of economic policy is to implement the adequate economic measures to smooth the economic cycle and close the inflation and output gaps. This implies that it is an important task for economists to find reliable measures of the potential levels of key macroeconomic variables, so that gaps can be calculated. It is, however, a difficult task, and a lot of research has been produced refining the methods for estimating the cyclical position of the economy.

In the original Laubach and Williams’ (2003) model, the estimation of the output gap, the inflation gap and the gap of the natural rate of interest are calculated using a semi-structural model and classical (point- and stepwise) estimation methods. In essence, inflation works as a signal informing about the cyclical position of the economy. However, if the Phillips curve is flat, inflation will not necessarily be a good indicator of whether the economy is in a boom or a bust. Therefore, these methods can be problematic when the Phillips curve is flat, which many argue that it presently is; see, for example, Zhang et al. (2021) for a more detailed discussion.

We believe that an improvement over traditional Laubach-Williams types of models can be made by utilizing the fact that we have more data available for making correct estimations of the economic cycle. By better pinpointing the cyclical position of the economy, we should also be able to get a more reliable estimate of the natural rate of interest. We here therefore merge a dynamic factor model that uses key economic indicators to help identify business-cycle fluctuations into a Laubach and Williams-type model. The dynamic factor model builds on Jarociński and Lenza (2018), who use a similar model to estimate the output gap for the euro area. The model uses national accounts data, such as consumption and gross fixed capital formation, and survey data concerning consumer confidence and capacity utilization, which are known to be good indicators of the cyclical position of the economy.

As a practical concern, we have also found that we need to address large swings associated with the covid pandemic. For this purpose, we introduce twelve dummy variables (denoted\({ D}_{1}\), …, \({D}_{12}\)) individually indicating the quarters 2020Q1, 2020Q2, …, 2022Q4. (That is, the dummy variable takes on the value 1 for the quarter in question and 0 otherwise.) These are included in every equation relating to cycle indicators.

We assume that there exists an interest rate level that is compatible with a balanced resource utilization, and call this level the natural rate of interest, \({r}_{t}^{*}\). The ex-ante real rate (\({r}_{t}\)) will be a combination of the natural rate and an interest rate gap (\({r}_{t}^{G}\)) according to

That is, \({r}_{t}^{G}\) is the deviation from the natural level. As was pointed out already by Laubach and Williams (2003) in their original article, the interest rate gap can be seen as the stance of monetary policy; if the gap is positive (negative), monetary policy is contractionary (expansionary).

As in standard macroeconomic models, the natural interest rate is assumed to be related to potential growth, \({g}_{t}\).Footnote 3 However, as in Laubach and Williams (2003) there are also deviations from this relationship that are modelled with another non-observable and time-varying series \({z}_{t}\) according to

where \({z}_{t}\) follows a random walk,

The component \({z}_{t}\) captures all other factors that affect the interest rate, such as demographics, global saving, global demand for safe assets and structural changes in fiscal policy; see Armelius et al. (2014), Bean et al. (2015), and Rachel and Smith (2017) for more detailed discussions.

The real interest rate gap is assumed to follow a second-order autoregressive process [AR(2)] with a zero mean,

It can be noted that there is no explicit modelling of monetary policy in this setup. Our approach accordingly closely follows that of Laubach and Williams (2003) original work.Footnote 4 But while monetary policy is not explicitly modelled, it nevertheless affects the macro economy and is, accordingly, reflected in its behaviour. While this setting does not invite structural interpretations of monetary policy, it does allow us to estimate the monetary policy stance (which is given by the real interest rate gap). Given the cyclical nature of monetary policy, an AR (2) process seems like a reasonable choice for this process.

We assume that the cyclical position of the economy can be described by an unobserved common factor (\({f}_{t}\)) that is influencing a number of observed variables and economic indicators. Furthermore, we assume that (the log of) real GDP (\({y}_{t}\)) is given by

where \({y}_{t}^{*}\) is the trend component; the cyclical component of real GDP is accordingly given by the deviation \({y}_{t}-{y}_{t}^{*}\).

In accordance with Laubach and Williams (2003), we let potential GDP follow a local trend:

The cyclical factor is assumed to drive inflation, emulating a Phillips curve, according to

where \({\pi }_{t}\) is core inflation (that is, excluding energy and food).Footnote 5

We link the cyclical factor to a small dynamic factor model, by adding the panel

where \({x}_{i,t}\) are additional economic indicators (\(i=\mathrm{1,2},\dots ,n\)) and \({w}_{i,t}\) are their trend components. Thus, because the unobserved common factor \({f}_{t}\) also enters Eq. (9), it is driving the cyclical position of each individual indicator, in addition to inflation. Some of the indicators are non-trending (and have a zero mean), in which case \({w}_{i,t}\) is set to zero. However, if \({x}_{i,t}\) is a variable with a trend, \({w}_{i,t}\)is modelled as a local trend according to

Finally, an important assumption is that the real rate gap has an influence on the factor driving the cyclical position of the economy. This is to say that if inflation expectations are anchored, then monetary policy can be used to smooth economic cycles. We therefore assume that

allowing for both contemporary and dynamic effects between the real interest rate gap, \({r}_{t}^{G}\), and the cyclical factor, \({f}_{t}\).

We estimate the model given by Eqs. (1–12) using a Bayesian filter that is outlined in Appendix A. For a given country, all equations are estimated simultaneously. This is an advantage of our approach, compared to standard Laubach-Williams-type approaches that typically use point- and stepwise estimation that tend to disregard parameter uncertainty. A necessity of Bayesian inference is to introduce prior distributions, making some subjective probabilistic statement of the parameters prior to conducting inference. In this paper, we have generally chosen very wide prior distributions. We therefore let the data “speak” more than what is typically found in similar studies that have used Bayesian methods to estimate the natural interest rate, such as Berger and Kempa (2014), Pedersen (2015) and Armelius et al. (2018). To our benefit, the inclusion of more data in the form of additional economic indicators enables us to produce reasonable estimates without resorting to more dogmatic prior beliefs.

3 Data

We use quarterly data from Denmark, Norway and Sweden as listed in Table 1. We define the (ex ante) real interest rate as the nominal rate minus expected inflation one year ahead. Following Laubach and Williams (2003), we estimate inflation expectations by making forecasts four quarters ahead from a simple regression on past CPI inflation.Footnote 6 As the nominal interest rate, we use the three-month interbank rate.

Our model utilizes ten observable time series for each country (the remaining time series in the model are non-observable). The observable time series include standard variables for natural rate estimation (core inflation, real interest rate and real GDP), and seven additional variables connected to the cyclical factor by the small dynamic factor model introduced in Sect. 2 (consumption, gross fixed capital formation, exports, imports, unemployment rate, capacity utilization and consumer confidence indicator). Of the latter (added) seven variables, the first five (consumption, gross capital formation, exports, imports and the unemployment rate) are treated as having a trend.Footnote 7 The last two variables (capacity utilization and consumer confidence indicator) should be mean reverting and have a zero mean by construction; they are hence modelled as not having a trend.

The sample for the estimation of the natural interest rate ranges from 1990Q1 to 2022Q4. As seen in Table 1, not all included variables have observations for the entire sample. The Bayesian filter handles missing values though; they are simply integrated out from the (conditional) likelihood in each sampling step.

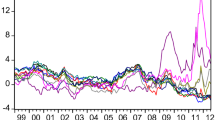

Figure 1 shows the first three variables––that is, core inflation, real interest rate and real GDP––per country, as well as the estimated inflation expectations. A few things are worth noticing. First, core inflation was substantially higher in Sweden than the other countries in the early 1990s. Second, inflation in Norway was higher (and closer to target) during the period of low inflation in the years around 2014–2018. Third, both Danmarks Nationalbank and Sveriges Riksbank had negative policy rates during much of this episode. Finally, the Norwegian real interest rate has also more or less consistently been higher than the Danish and Swedish counterparts; given the expected positive relationship between interest rates and growth, this would be expected since growth in Norway has been substantially higher than in the other countries.

Key variables. Note: For details regarding data, see Table 1

4 Results

In Figs 2, 3 and 4, the estimated natural rate of interest, output gap, real interest rate gap, as well as the contribution to the natural rate of interest from the processes \({g}_{t}\) and \({z}_{t}\) are shown for Denmark, Norway and Sweden, respectively.

Natural interest rate, output gap, real interest rate gap and contributions to the natural interest rate, Denmark. Note: Natural interest rate in per cent. Output gap in per cent of potential GDP. Real interest rate gap in percentage points. Contributions to natural interest rate in percentage points. Shaded areas denote the inclusion of dummy variables

Natural interest rate, output gap, real interest rate gap and contributions to the natural interest rate, Norway. Note: Natural interest rate in per cent. Output gap in per cent of potential GDP. Real interest rate gap in percentage points. Contributions to natural interest rate in percentage points. Shaded areas denote the inclusion of dummy variables

Natural interest rate, output gap, real interest rate gap and contributions to the natural interest rate, Sweden. Note: Natural interest rate in per cent. Output gap in per cent of potential GDP. Real interest rate gap in percentage points. Contributions to natural interest rate in percentage points. Shaded areas denote the inclusion of dummy variables

The natural rate has fallen from around 5–6% in the early 1990s to negative values by the end of 2022 in all three countries. The Norwegian natural rate has been slightly higher than the natural rates in Denmark and Sweden since the mid-1990s. This is mostly explained by a lower negative contribution from the additional factors represented by the process \({z}_{t}\). The general pattern of a downward trend in the natural rates is in line with previous findings; see, for example, Holston et al. (2017).

Another previous finding in the literature is that foreign factors seem to have a large negative impact on natural rates in small open economies (Holston et al. 2017; Zhang et al. 2021). In our model this would be captured by the component \({z}_{t}\) (which can also contain other factors such as changes in fiscal policy rules and demographics). According to our estimates, there seem to exist some common patterns in the Scandinavian countries. All three countries have a positive contribution from \({z}_{t}\) in the early 1990s, but then have a negative contribution from \({z}_{t}\) after the global financial crisis in 2008–2009, although the magnitudes of the contributions differ somewhat between the countries. These patterns largely explain the decline in the natural rate. We do not know what is driving \({z}_{t}\), but given that all countries are small open economies it does not seem unlikely that foreign developments are important.

It should also be noted that in the two first quarters of 2022, our estimates of the natural rate of interest fell substantially in Denmark and Sweden––a fall which originated from a rapid increase in inflation, resulting in historically low real interest rates. The nature behind this development is too complicated to be well described by our model, and our estimates of both the natural rate of interest and the real interest rate gap at the end of the sample should hence be taken with a substantial pinch of salt. We nevertheless note that the negative real interest rate gaps in Denmark and Sweden at the end of the sample are consistent with increasing policy interest rates contributing to a move towards a neutral monetary policy stance.

Turning to some other results from the estimations, we find that the real interest rate gap has varied more in Norway and Sweden than in Denmark. This can be interpreted as monetary policy having been used more actively in Norway and Sweden. Since Denmark has a fixed exchange rate vis-à-vis the euro, this is not an unexpected finding. Overall, Norway has had the smallest fluctuations in the output gap over time––in particular in the aftermath of the global financial crisis.

In Table 2, the parameter posterior estimates are shown in terms of posterior means and 90% credible intervals for the parameters in the main equations. The posterior estimates for the parameters in the dynamic factor model and its trend components are provided in Appendix C. If a 90% credible interval does not encompass 0, then we can be relatively confident that the corresponding parameter is different from 0. This is the case for most of the parameters in Table 2. Looking at the estimated parameters for the Phillips curve (first panel of Table 2), we see no clear effect on inflation in Sweden from the cyclical factor \({f}_{t}\), judging by the posterior estimates of the parameters \({\gamma }_{\pi ,1}\) and \({\gamma }_{\pi ,2}\). We see an effect on inflation in Denmark and Norway. However, for both countries, the parameters \({\gamma }_{\pi ,1}\) and \({\gamma }_{\pi ,2}\) are of similar magnitude and have different signs, and the dynamic effect over time is moderate. Overall, our estimates are in line with a quite flat Phillips curve, motivating the use of additional indicators to estimate the output gap in these types of models.Footnote 8 Apart from inflation, we find that the economic cycle has a clear effect on the other economic indicators for each country, as shown by the posterior estimates provided in Appendix C.

5 Conclusions

We have estimated the natural rate of interest in the Scandinavian countries Denmark, Norway and Sweden from 1990Q1 to 2022Q4. In our approach, we have augmented the Laubach-Williams methodology with a dynamic factor model linked to conventional economic indicators to better identify business cycle fluctuations. This approach is particularly useful when the Philips curve is flat, since inflation is unlikely to provide a good signal of the cyclical position of the economy. Our results indicate that this is indeed the case in the economies we study.

The estimates of the natural rate differ somewhat between the three countries. However, a common feature is that they indicate that the natural rate has declined substantially during the sample. The last three years of the sample are turbulent, with both the covid pandemic and the period of high inflation (and rising interest rates) that followed. The results from this period should be interpreted with caution, but we note that the point estimates suggest that the natural rate of interest is still very low––in fact negative.

Our findings are hence in line with recent results for other economies; for example, Benati (2023) suggests that the natural rate in late 2019 in Canada, the euro area, the United Kingdom and the USA was negative in all four cases. Concerning implications for monetary policy, we note that there is an ongoing discussion regarding whether policy rates will stay high or return to lower levels––see, for example, Gopinath (2022) and International Monetary Fund (2023)––and recent evidence for the USA suggests that the short nominal rate will come down from its present (April 2023) level (Beechey et al. 2023). There is obviously a substantial amount of uncertainty regarding the future development of policy rates, but our results suggest that if inflation stabilizes at the target in a not too distant future, then a low natural rate of interest could contribute to low policy rates also in the future.

Notes

The natural rate of interest as a concept was first introduced by Wicksell in 1896 as the equilibrium rate of interest that is consistent with stable prices. We follow Laubach and Williams (2003) – and others, including Holston et al. (2017) – and define the natural rate of interest as the real interest rate consistent with output equal to its natural rate and stable inflation. Seeing that we use an extended version of the Laubach and Williams (2003) model, it is also reasonable to use the same terminology. For a further discussion regarding terminology, see Platzer et al. (2022).

In contrast, Zhang et al. (2021) also estimate a monetary policy rule for the central bank.

The parameters for inflation lags sum to one, which is consistent with a vertical long-run Phillips curve; the same restriction was imposed by Laubach and Williams (2003) and Holston et al. (2017). We let the number of lags (\(p\)) in Eq. (8) for each country be chosen based on the Schwarz Information Criterion (Schwarz 1978) from a univariate autoregression for inflation; the maximum number of lags is set to eight.

The regression is an AR(3) process with a rolling estimation window of 40 quarters.

The unemployment rate obviously does not have a trend similar to that of the other four variables (seeing that those variables increase over time). However, the unemployment rate may have a unit root – at least within certain bounds – and hence a stochastic trend. This can be motivated, for example, by the work of Blanchard and Summers (1986) and the issue of a unit root in unemployment rates has been subject to much empirical research; see, for example, Papell et al. (2000).

References

Aastveit KA, Trovik T (2014) Estimating the output gap in real time: a factor model approach. Q Rev Econ Finan 54:180–193

Adrian T (2020) “‘Low for Long’ and Risk-Taking”, Departmental Paper Series No. 20/15, Monetary and Capital Markets Department, International Monetary Fund.

Altunbas Y, Gambacorta L, Marques-Ibanez D (2014) Does monetary policy affect bank risk? Int J Cent Bank 10:95–135

Armelius H, Solberger M, Spånberg E (2018) Is the Swedish neutral interest rate affected by international developments? Sveriges Riksbank Econ Rev 1:22–37

Armelius H, Bonomolo P, Lindskog M, Rådahl J, Strid I, Walentin K (2014) “Lower Neutral Interest in Sweden?”, Economic Commentary, No. 8, Sveriges Riksbank.

Auclert A, Malmberg H, Martinet F, Rognlie M (2021) “Demographics, Wealth, and Global Imbalances in the Twenty-First Century”, NBER Working Paper No. 29161.

Bai J, Wang P (2015) Identification and bayesian estimation of dynamic factor models. J Bus Econ Stat 33:221–240

Ball LM, Mazumder S (2019) A Phillips curve with anchored expectations and short-term unemployment. J Money Credit Bank 51:111–137

Barigozzi M, Luciani M (2019) “Measuring the output gap using large datasets”, Working Paper, https://doi.org/10.2139/ssrn.3217816.

Bean C, Broda C, Ito T, Kroszner R (2015) “Low for Long? Causes and Consequences of Persistently Low Interest Rates”, Geneva Reports on the World Economy 17, International Center for Monetary and Banking Studies.

Beckmann J, Fiedler S, Gern K-J, Kooths S, Quast J, Wolters M (2020) “The ECB Asset Purchase Programmes: Effectiveness, Risks, Alternatives”, Monetary Dialogue Papers, September 2020, European Parliament.

Beechey M, Österholm P, Poon A (2023) Estimating the US trend short-term interest rate. Financ Res Lett 55:103913

Belke A, Klose J (2017) Equilibrium real interest rates and secular stagnation: an empirical analysis for euro area member countries. J Common Market Stud 55:1221–1238

Benati L (2023) “A New Approach to Estimating the Natural Rate of Interest”, Forthcoming in Journal of Money, Credit and Banking

Berger T, Kempa B (2014) Time-varying equilibrium rates in small open economies: evidence for Canada. J Macroecon 39:203–214

Blanchard O, Cerutti E, Summers L (2015) “Inflation and Activity–Two Explorations and Their Monetary Policy Implications”, NBER Working Paper No. 21726.

Blanchard OJ, Summers LH (1986) Hysteresis and the European unemployment problem. NBER Macroecon Annu 1:15–78

Broadbent B (2014) “Monetary Policy, Asset Prices and Distribution”, Speech given at the Society of Business Economists Annual Conference, October 23.

Caballero RJ, Farhi E, Gourinchas P-O (2008) An equilibrium model of ‘global imbalances’ and low interest rates. Am Econ Rev 98:358–393

Cecchetti S, Schoenholtz KL (2020) “The Fed Goes to War: Part 2”, Blog post, March 25, http://www.moneyandbanking.com/commentary/2020/3/25/the-fed-goes-to-war-part-2

Durbin J, Koopman SJ (2002) A simple and efficient simulation smoother for state space time series analysis. Biometrika 89:603–615

Gaiotti E (2010) Has globalization changed the Phillips curve? firm-level evidence on the effect of activity on prices. Int J Cent Bank 6:51–84

Garnier J, Wilhelmsen BJ (2009) The natural rate of interest and the output gap in the euro area: a joint estimation. Empirical Economics 36:297–319

Gelman A, Carlin J, Stern H, Dunson D, Vehtari A, Rubin D (eds) (2013), Bayesian Data Analysis, 3 edn, Chapman and Hall/CRC

Geman S, Geman D (1984) Stochastic relaxation, Gibbs distributions and the Bayesian restoration of images. IEEE Trans Pattern Anal Mach Intell 6:721–741

Gopinath, G. (2022). “How Will the Pandemic and War Shape Future Monetary Policy?”, Presentation at the Jackson Hole Economic Symposium, August 26.

Gourinchas P-O, Portes R, Rabanal P (2016) Secular stagnation, growth, and real interest rates. IMF Econ Rev 64:575–580

Holston K, Laubach T, Williams JC (2017) Measuring the natural rate of interest: international trends and determinants. J Int Econ 108:59–75

IMF (2013), Global Financial Stability Report, April 2013. International Monetary Fund.

Jarociński M, Lenza M (2018) An inflation-predicting measure of the output gap in the euro area. J Money, Credit, Bank 50:1189–1224

Karlsson S, Österholm P (2020) A note on the stability of the Swedish Phillips curve. Empirical Economics 59:2573–2612

Kuttner K, Robinson T (2010) Understanding the flattening Phillips curve. North Am J Econ Financ 21:110–125

Laubach T, Williams JC (2003) Measuring the natural rate of interest. Rev Econ Stat 85:1063–1070

Marx M, Mojon B, Velde F (2019) Why have interest rates fallen far below the return on capital? J Monet Econ 124:S57–S76

Milan A, Straub L, Sufi A (2021), “What Explains the Decline in r*? Rising Income Inequality Versus Demographic Shifts”, Becker Friedman Institute for Economics Working Paper No. 2021–104, University of Chicago. Prepared for the 2021 Jackson Hole Symposium.

Papell DH, Murray CJ, Ghiblawi H (2000) The structure of unemployment. Rev Econ Stat 82:309–315

Pedersen, J. (2015), “The Danish Natural Real Rate of Interest and Secular Stagnation”, Danmarks Nationalbank Working Papers No. 94.

Platzer J, Tietz R, Lindé J (2022) Natural versus neutral rate of interest: parsing disagreement about future short-term interest rates. VoxEU.org

Rachel L, Smith TD (2017) Are low real interest rates here to stay? Int J Cent Bank 13:1–42

Sveriges Riksbank (2021), Monetary Policy Report, February 2021.

Schwarz GE (1978) Estimating the dimension of a model. Ann Stat 6:461–464

Summers LH (2014) U.S. economic prospects: secular stagnation, hysteresis, and the zero lower bound. Bus Econ 49:65–73

Teulings C, Baldwin R (eds) (2014) Secular Stagnation: Facts, Causes, and Cures. CEPR Press, London

Zhang R, Martínez-García E, Wynne MA, Grossman V (2021) Ties that bind: estimating the natural rate of interest for small open economies. J Int Money Financ 113:102315

Funding

Open access funding provided by Örebro University.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing interests

Armelius is employed at Sveriges Riksbank. None of the other authors have any competing interests to declare that are relevant to the content of this article.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

We are grateful to an anonymous referee for valuable comments. The views expressed in this article are the sole responsibility of the authors and should not be interpreted as reflecting the views of Sveriges Riksbank.

Appendices

Appendix A: Estimation method

Equations (1–12) can be written as a Gaussian state space model,

where \({{\varvec{y}}}_{t}={\left({r}_{t}, {y}_{t}, {\pi }_{t}, {x}_{1,t},\dots {,x}_{7,t}\right)}{\prime}\) is a vector \((10\times 1)\) of the observed variables, and \({\boldsymbol{\alpha }}_{t}\) is a latent state vector \((18\times 1)\),

\({\varvec{\alpha}}_{t} = \left( {r_{t}^{*} ,z_{t + 1} ,r_{t + 1}^{G} ,r_{t}^{G} ,y_{t}^{*} ,g_{t + 1} ,f_{t} ,f_{t - 1} ,w_{1,t} , \ldots ,w_{5,t} ,u_{1,t} , \ldots ,u_{5,t} } \right){\prime}\).

Note the leading index on \({r}_{t+1}^{G}\), which is due to that we allow for a contemporary effect between \({f}_{t}\) and \({r}_{t}^{G}\) in Eq. (12). Likewise, the leading indices on \({g}_{t+1}\) and \({z}_{t+1}\) allow for a contemporary effect between \({r}_{t}\) and \({g}_{t}\) and \({z}_{t}\) in Eq. (2). Also note that only five (and not seven) of each of the latent trend variables \({w}_{i,t}\) and \({u}_{i,t}\) from Eqs. (10) and (11) are elements of \({\boldsymbol{\alpha }}_{t}\), since only the first five of the economic indicators in the panel \({x}_{i,t}\) of Eq. (9) have trends; see Sect. 3 and Appendix B.

The vector \({\varvec{c}}\) \((10\times 1)\) relates to the observable right-hand time series of the equations, including the dummy variables,

\({\varvec{c}}=\Big(0, {\sum }_{d=1}^{12}{\delta }_{y,d}{D}_{d}, \left(1-{\sum }_{{l}=2}^{p}{\phi }_{\pi ,{l}}\right) {\pi }_{t-1}+{\sum }_{{l}=2}^{p}{\phi }_{\pi ,{l}}{\pi }_{t-{l}}+{\sum }_{d=1}^{12} {\delta }_{\pi ,d} {D}_{d}, {\sum }_{d=1}^{12}{\delta }_{1,d}{D}_{d},\dots , {\sum }_{d=1}^{12}{\delta }_{7,d} {D}_{d}\Big)^{\mathrm{^{\prime}}}\).

The matrices \({\varvec{A}}\) \((10\times 18)\) and \({\varvec{F}}\) \(\left(18\times 18\right)\) collect the parameters associated with the latent state vector,

\({\varvec{A}} = \left( {\begin{array}{*{20}c} 1 & 0 & 0 & 1 & 0 & 0 & 0 & 0 & 0 & 0 & \cdots & 0 \\ 0 & 0 & 0 & 0 & 1 & 0 & 1 & 0 & 0 & 0 & \cdots & 0 \\ 0 & 0 & 0 & 0 & 0 & 0 & {\gamma_{\pi ,1} } & {\gamma_{\pi ,2} } & 0 & 0 & \cdots & 0 \\ 0 & 0 & 0 & 0 & 0 & 0 & {\gamma_{1,1} } & {\gamma_{2,1} } & 1 & 0 & \cdots & 0 \\ 0 & 0 & 0 & 0 & 0 & 0 & {\gamma_{1,2} } & {\gamma_{2,2} } & 0 & 1 & \cdots & 0 \\ \vdots & \vdots & \vdots & \vdots & \vdots & \vdots & \vdots & \vdots & \vdots & \vdots & \ddots & 0 \\ 0 & 0 & 0 & 0 & 0 & 0 & {\gamma_{1,7} } & {\gamma_{2,7} } & 0 & 0 & \cdots & 1 \\ \end{array} } \right)\),

\(\varvec{F} = \left( {\begin{array}{*{20}c} 0 & 1 & 0 & 0 & 0 & 4 & 0 & 0 & \varvec{0} & \varvec{0}\\ 0 & 1 & 0 & 0 & 0 & 0 & 0 & 0 & \varvec{0}& \varvec{0}\\ 0 & 0 & {\phi _{1} } & {\varphi _{2} } & 0 & 0 & 0 & 0 & \varvec{0}& \varvec{0}\\ 0 & 0 & 1 & 0 & 0 & 0 & 0 & 0 & \varvec{0}& \varvec{0}\\ 0 & 0 & 0 & 0 & 1 & 1 & 0 & 0 & \varvec{0}& \varvec{0}\\ 0 & 0 & 0 & 0 & 0 & 1 & 0 & 0 & \varvec{0}& \varvec{0}\\ 0 & 0 & {\rho _{{r,0}} } & {\rho _{{r,1}} } & 0 & 0 & {\rho _{{f,1}} } & {\rho _{{f,2}} } & \varvec{0}& \varvec{0}\\ 0 & 0 & 0 & 0 & 0 & 0 & 1 & 0 & \varvec{0} & \varvec{0} \\ \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& {\varvec{I}_{5} } & {\varvec{I}_{5} } \\ \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& \varvec{0}& {\varvec{I}_{5} } \\ \end{array} } \right),\) where \({{\varvec{I}}}_{5}\) denotes the \(5\times 5\) identity matrix, and \(\varvec{0}\) denotes a zero matrix of appropriate size.

The matrices \({\varvec{B}}\) \((10\times 9)\) and \({\varvec{G}}\) \((18\times 15)\) are selection matrices consisting of subsets of the columns of the identity matrix, loading onto the errors \({{\varvec{\epsilon}}}_{t}\) \((9\times 1)\) and \({{\varvec{u}}}_{t}\) \((15\times 1)\),

The matrices \({{\varvec{\Sigma}}}\) and \({\varvec{H}}\) contain the error variances on their main diagonals; the off-diagonal elements are zero.

Let \({\varvec{\theta}}\) denote the set of all parameters and let \({\varvec{\alpha}}_{1:T} = \left\{ {{\varvec{a}}_{t} } \right\}_{t = 1}^{T}\) and \({\varvec{y}}_{1:T} = \left\{ {{\varvec{y}}_{t} } \right\}_{t = 1}^{T}\) denote the sets of latent variables and observable data, respectively. We apply a Bayesian filter with the goal to find the joint posterior distribution, \(p{(}{\varvec{\theta}},{\varvec{\alpha}}_{1:T} {|}{\varvec{y}}_{1:T} )\). We use Gibbs sampling – see, for example, Geman and Geman (1984) and Gelman et al. (2013) – to draw iteratively from the full conditional posteriors, \({\varvec{\theta}}^{\left( d \right)} \sim p{(}{\varvec{\theta}}{|}{\varvec{\alpha}}_{1:T}^{{\left( {d - 1} \right)}} ,{\varvec{y}}_{1:T} )\), \({\varvec{\alpha}}_{1:T}^{\left( d \right)} \sim p{(}{\varvec{\alpha}}_{1:T} {|}{\varvec{\theta}}^{\left( d \right)} ,\user2{ y}_{1:T} )\), over \(d = 1, \ldots , D.\) We set \(D = 100,\!\!000\), where the first \(10,\!\!000\) draws are left out. Gibbs sampling is a Markov chain Monte Carlo method for posterior simulation and is often used for joint estimation of parameters and latent states in linear Gaussian state space systems; see, for example, Bai and Wang (2015) and Jarociński and Lenza (2018).

Note that, given \({\varvec{\alpha}}_{1:T}\), equations (A1) and (A2) can be seen as a multivariate linear regression system with Gaussian errors. Furthermore, due to the diagonal properties of \({{\varvec{\Sigma}}}\) and \({\varvec{H}}\), the system is just a collection of standard simple linear regressions. By using conjugate priors, we can find \(p{(}{\varvec{\theta}}{|}{\varvec{\alpha}}_{1:T}^{{\left( {d - 1} \right)}} ,{\varvec{y}}_{1:T} )\) by standard Bayesian linear regressions. Here, we use the Gaussian-scaled-inverse-chi-square prior; see, for example, Gelman et al. (2013). Let \({\varvec{\beta}}\) be a vector of non-variance parameters in any of these single linear regressions, with corresponding residual variance \(\sigma^{2}\). The prior become \({\varvec{\beta}}|\sigma^{2} \sim {\mathcal{N}}\left( {\varvec{0},\frac{{{\upsigma }^{2} }}{\omega }{\varvec{I}}} \right),\) \(\sigma^{2} \sim {\text{Scale - inverse - }}\chi^{2} \left( {\nu ,\tau^{2} } \right).\) We choose \(\omega = 1/100\) for all equations, creating a reasonably wide prior for each non-variance parameter. For all variance parameters (with exceptions for \(\sigma_{{r^{G} }}^{2}\) and \(\sigma_{f}^{2}\), see below) we choose \(\nu = 0.01\) and \(\tau^{2} = 0.25\), placing around 5% prior probability for variances less than 1, and an almost uniform prior for variances from 1 going up the positive real line in many orders of magnitude––that is, a very wide prior, with just a little extra emphasis on small numbers. For \(\sigma_{{r^{G} }}^{2}\) and \(\sigma_{f}^{2}\), we choose \(\nu = 1\), and \(\tau^{2} = \frac{{s_{r}^{2} }}{9}\) and \(\tau^{2} = \frac{{s_{y}^{2} }}{9}\), respectively, where \(s_{r}^{2}\) and \(s_{y}^{2}\) are the respective sample variances of \(\left( {r_{t} - r_{t - 1} } \right)\) and \(\left( {y_{t} - y_{t - 1} } \right)\); that is, a large part of the prior density is placed such that the residual variances \(\sigma_{{r^{G} }}^{2}\) and \(\sigma_{f}^{2}\) are smaller than the sample variances of the underlying variables.

Lastly, the other conditional posterior, \(p{(}{\varvec{\alpha}}_{1:T} {|}{\varvec{\theta}}^{\left( d \right)} ,\user2{ y}_{1:T} )\), is found using the Simulation smoother of Durbin and Koopman (2002).

Appendix B: Additional data

Figure

Additional economic indicators

5 shows time series of the additional seven economic indicators: consumption, gross fixed capital formation, exports, imports, unemployment rate, capacity utilization and consumer confidence indicator. The last two series have a zero mean by construction. Thus, for these series the trend components \(w_{i,t}\) and \(u_{i,t}\) are set to zero.

Appendix C: Additional results

Additional results, see Tables

3,

4,

5 and

6.

Rights and permissions

Open Access This article is licensed under a Creative Commons Attribution 4.0 International License, which permits use, sharing, adaptation, distribution and reproduction in any medium or format, as long as you give appropriate credit to the original author(s) and the source, provide a link to the Creative Commons licence, and indicate if changes were made. The images or other third party material in this article are included in the article's Creative Commons licence, unless indicated otherwise in a credit line to the material. If material is not included in the article's Creative Commons licence and your intended use is not permitted by statutory regulation or exceeds the permitted use, you will need to obtain permission directly from the copyright holder. To view a copy of this licence, visit http://creativecommons.org/licenses/by/4.0/.

About this article

Cite this article

Armelius, H., Solberger, M., Spånberg, E. et al. The evolution of the natural rate of interest: evidence from the Scandinavian countries. Empir Econ 66, 1633–1659 (2024). https://doi.org/10.1007/s00181-023-02503-w

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-023-02503-w