Abstract

This paper evaluates the ability of various indicators related to macroeconomic fundamentals, credit conditions, and housing supply to predict house price growth in the United States during the post-financial crisis period. We find that the inclusion of different measures of housing supply indicators significantly improves the forecasting performance for the period of 2010-2022. Specifically, incorporating the monthly supply of new homes into a VAR model with house price growth reduces the RMSE by over 30 percent compared to a univariate benchmark. Moreover, forecasting accuracy improves further at a longer forecast horizon (greater than three months) when the mortgage rate spread is also used as a predictor. Further improvements are made if "Direct" forecasts are used instead of iterative forecasts. The shrinkage method like LASSO shows that the monthly supply of new homes is an important predictor at all forecasting horizons, while the mortgage spread is most relevant for longer forecast horizons.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

The housing market attracts significant attention from policymakers and financial markets globally, with increased focus on housing price fluctuations since the 2008-09 financial crisis due to their impact on the macroeconomyFootnote 1. Housing, as an asset, has a more widespread economic impact than stock market wealth due to its larger size and broader reach, with nearly two-thirds of US households being homeowners. It is not surprising that policymakers and financial markets pay close attention to forecasts of housing prices.

The housing market holds significant sway over the macroeconomy, but it garners less research attention in forecasting compared to the stock market. Most housing market research focuses on its impact on the macroeconomy and financial markets. The academic research on relationship between macroeconomic fundamentals and housing prices has a rich history. The underlying premise is that housing prices should, in the long term, mirror a nation’s macroeconomic fundamentalsFootnote 2. While debates persist about what constitutes these fundamentals, research typically focuses on factors like the price-rent ratio, price-income ratio, labor market dynamics, and interest rates. For instance, Poterba et al. (1991) delved into the role of user costs and real interest rates in shaping housing prices during the 1970s and 1980s. They uncovered some predictability within the housing market, with implications for households’ expectations about future housing prices. Likewise, Rapach and Strauss (2009) demonstrated that models incorporating information about both national and local economic conditions provide valuable insights into future housing prices across different states. Meanwhile, Kishor and Marfatia (2018) found that bivariate models, encompassing crucial domestic macroeconomic variables, particularly interest rates, outperform univariate models when forecasting real housing price growth in a set of OECD countries.

The collapse of the housing market in 2008-09 also sparked a surge in research interest in the relationship between credit and housing prices. Mian and Sufi (2011) showed that credit played a critical role in the rise and subsequent fall of housing prices in the US during the financial crisis of 2007-09. On the other hand, some studies have argued that credit conditions play a smaller role in explaining housing price fluctuationsFootnote 3. Glaeser and Sinai (2013) argue that housing price movements are too volatile to be attributed to changes in credit conditions, while Case and Shiller (2003) have demonstrated that housing price movements are more related to people’s perceptions of anticipated changes in housing markets than credit conditions. Bhatt and Kishor (2022) found that excessive credit buildup has a negative impact on housing price growth during housing busts, while low interest rates and expectations, as measured by past housing price growth, are associated with housing price boomsFootnote 4. Overall, the literature suggests that the relationship between housing prices and credit is complex and multi-faceted. Most of the work on this relationship focuses on examining the mechanism between these two variables.

The literature on the relationship between house prices and supply indicators primarily focuses on how house prices evolve in the long-run due to local and regional supply factors. Many studies examine the impact of supply constraints on housing price dynamics, considering that housing prices are relatively volatile compared to observable changes in fundamentals. For example, Glaeser et al. (2008) show that a more elastic housing supply leads to fewer and shorter price bubbles, with smaller price increases. Gyourko (2009) argues that differences in housing supply elasticity can account for variations in new construction volatility (but not price volatility) across markets over time. Some research has also focused on stock-flow models, where housing demand may differ from existing supply for several years, requiring short-term price adjustments to clear the market.Footnote 5 Caplin and Leahy (2011) use a housing liquidity model to show correlation between inventory and house prices. Inventories of housing stock, therefore, plays a crucial role in house price dynamics.

Recognizing that fundamentals, credit conditions, and supply play important roles in the evolution of house prices, this paper examines the predictive power of these variables in an out-of-sample framework. We extend the existing literature on forecasting by comparing the predictive performance of these different indicators, focusing on the post-financial crisis sample period. Our paper also contributes to the existing literature on machine learning in house price forecasting by using the Least Absolute Shrinkage and Selection Operator (LASSO) to shrink the predictor space. We include six measures of fundamentals, credit conditions, and supply indicators in our analysis.Footnote 6Using these indicators, we aim to answer the following questions in this paper: Is there evidence of predictability of house prices in the post-financial crisis period in the U.S.? Can the forecasting performance of a univariate AR model be improved by incorporating indicators of fundamentals, credit conditions, and supply? Is there a dominant predictor across different forecast horizons? Is there an improvement in forecasting performance if the "Direct Forecast" method is used instead of iterative forecasts for multi-step-ahead prediction?Footnote 7

Our data covers the period from April 2002 to August 2022, with forecasting starting in 2010. We assess both in-sample and out-of-sample forecasting accuracy for periods ranging from 1 to 12 months. The in-sample results indicate that some variables from the various indicators can predict future house price growth beyond their past values. Changes in the price-rent ratio and housing sentiment are significant predictors at 1- and 3-month horizons, while credit condition indicators are more effective at longer horizons. Supply indicators, particularly monthly new home supply and the ratio of unstarted to completed new homes for sale, have the in-sample ability to predict house prices at all horizons up to 12 months. To identify the best predictors, we use the LASSO method to reduce the number of predictors. LASSO selects monthly new home supply at all horizons, price-rent ratio and housing sentiment at short horizons, and mortgage spread, as well as lags of house price growth and monthly new home supply, at horizons longer than 3 months. These results are also supported by least angle regression (LARS). Using this information, we conduct out-of-sample forecasting using bivariate and trivariate VAR models with both iterative and direct forecasting methods. The results reveal that monthly new home supply is the most dominant predictor of house price growth. The bivariate VAR model that includes house price growth and monthly new home supply reduces the RMSE of house price growth by 30% over a 12-month period over a benchmark univariate model. The trivariate model that includes mortgage spread further improves the RMSE, particularly at longer horizons. In summary, monthly new home supply is the most important predictor of house price growth. The bivariate VAR model that includes house price growth and monthly new home supply as predictors outperforms a benchmark univariate model, and the trivariate model that includes mortgage spread further improves the RMSE.Footnote 8 . Direct forecasts are found to be more accurate than iterative forecasts, especially in the trivariate model that contains supply indicator and mortgage spread. We do not find evidence of any payoff in using nonlinear timeseries models in forecasting house pricesFootnote 9. Our findings highlight the significance of supply indicators in forecasting house price growth and recommend that professional forecasters and policymakers should take these indicators into account along with mortgage spread to obtain better forecasting results.

The rest of the paper is structured as follows: Section 2 discusses the literature, Section 3 provides a description of the data used in our empirical analysis, Section 4 reviews empirical models and results, Section 5 presents out-of-sample forecasting results, and Section 6 concludes.

Literature Review

Due to the significance of the housing market, considerable attention is presently focused on predicting house prices. The body of research in house price forecasting includes a wide variety of subjects, including economic indicators, statistical techniques, machine learning methods, and behavioral influences on housing markets.

The emergence of machine learning models has prompted the application of diverse machine learning tools for predicting house prices. For instance, Milunovich (2020) conducted an exhaustive analysis of 47 algorithms, spanning traditional time series models, machine learning procedures, and deep learning neural networks, to forecast Australian real house prices and growth rates. The results underscored variations in forecast accuracy across different time horizons and dependent variables, with the linear support vector regressor (SVR) algorithm consistently outperforming others. Kuvalekar et al. (2020) also utilized machine learning algorithms for the prediction of real estate property market values. They employ a Decision tree regressor to predict house prices in Mumbai city based on geographical variables, offering a valuable tool for prospective property investors. Their research demonstrates the Decision tree regressor’s high accuracy of 89%. Crawford and Fratantoni (2003) evaluated the forecasting efficacy of univariate time series models, like ARIMA, GARCH, and regime-switching models. Their findings indicated that while regime-switching models may excel in-sample, simpler ARIMA models generally perform better in out-of-sample predictions. Miles (2008) expanded the scope to non-linear forecasting models, investigating the effectiveness of the generalized autoregressive (GAR) model in projecting US home prices. Their study unveiled the GAR model’s superiority in various cases, particularly in volatile markets.

Spatial and temporal dependencies have proven instrumental in enhancing the precision of real estate price predictions. Liu (2013) introduced spatial and temporal dependencies into housing price forecasting through the spatiotemporal autoregressive model. By examining Dutch housing transaction data, Liu demonstrated notable enhancement in predictive power compared to traditional hedonic models. Oust et al. (2020) concentrated on merging repeat sales and hedonic regression techniques for property valuation, enhanced by spatial econometric models such as regression kriging and geographically weighted regression. Their application to Oslo’s real estate transactions displayed reduced prediction errors, highlighting the benefits of incorporating spatial and non-spatial insights from past sales.

The influence of macroeconomic uncertainty on predicting housing price movements has garnered attention, prompting studies into its effects on comovements and volatility. Gupta et al. (2022) investigated the relationship between macroeconomic uncertainty and housing price synchronization among US states. Using a Bayesian dynamic factor model and random forests, the study demonstrated macroeconomic uncertainties’ substantial predictive capability for forecasting national and regional housing price factors. Segnon et al. (2021) introduced a logistic smooth transition autoregressive fractionally integrated (STARFI) process for modeling and predicting housing price volatility. Their findings showcased the potential of frameworks like Markov-switching multifractal (MSM) and FIGARCH in refining forecast accuracy.

Additionally, Dotsis et al. (2023) assessed the predictability of housing market crashes in 18 countries over the years 1870-2020. They found that the rent-to-price ratio is a leading indicator and the most significant predictor of housing market crash episodes. The stance of monetary policy, as proxied by the short-term interest rate, is also an important determinant of the probability of housing market crashes in the post-WW2 period.

The interplay between market dynamics and comovements across distinct real estate markets has also been explored. Fan and Yavas (2020) employed wavelet technology to investigate price dynamics, cycles, and lead-lag relationships between private and public commercial real estate markets. Their discoveries highlighted discrepancies in trends and cycles between these markets, coupled with contagion effects during crises. This approach was similarly applied by Fan et al. (2019) to five major Chinese cities, revealing an average cycle of 3.25 years, notably shorter than housing cycles observed in the United States. Crawford and Rosenblatt (1995) extend options-based mortgage default theory to include transaction costs, providing insights into the behavior of rational borrowers in mortgage default situations. By considering transaction costs, they show that the rational borrower will default only when the value of the collateral falls below the mortgage value by an amount equal to the net transaction costs. Risse and Kern (2016) adopted a dynamic modeling and selection approach to predict house price growth across prominent European countries. Their study’s robust performance, especially post the 2008 financial crisis, underscored the necessity of accounting for model uncertainty and instability. In summary, this literature review highlights the research that has undertaken to study the role of fundamentals, credit conditions, and supply indicators. These studies enhance the intricate dynamics and predictive potential of diverse factors within real estate markets.

This paper contributes to the existing research on housing markets by exploring the role of fundamentals, credit conditions, and supply indicators in forecasting house prices. Despite prior research into these indicators’ influence on house prices, a comprehensive joint consideration for out-of-sample forecasting has been lacking. This becomes particularly relevant in the current context where the housing market remains robust despite rapid increases in interest rates.

Data Description

Our data covers the period from April 2002 to August 2022. The start date is determined by the availability of supply indicators for the housing market. The sample primarily focuses on the housing market buildup before the crash and the subsequent slow recovery. Our main variable of interest is nominal house price growth where house price is the national house price index measured by S &P Case Shiller house price index. House price growth data are expressed as annualized percent changes. We focus on nominal house price growth mainly because nominal growth is usually the focus of attention of the financial markets and policymakers.

Our macro fundamental indicators are Kansas City Fed’s labor market activity indicator, changes in price-income ratio, housing sentiment index from National Association of Realtors, changes in price-rent ratio, changes in mortgage rate and change in real disposable income growth. Price-rent ratio and price-income ratio are widely cited as an indicators of the health of the housing market. Both these ratios are highly persistent and the null of unit root is not rejected at all conventional levels of significanceFootnote 10. Therefore, we use the first difference of these variables as predictors in our analysis. Labor market conditions also play an important role in the evolution of housing market. The natural measure of labor market is unemployment rate. However, big swings during the pandemic in unemployment rate makes it infeasible to include in the forecasting model. A good substitute of unemployment rate that does not suffer from huge swings in the pandemic period is labor market activity indicator of the Kansas City Fed. We also include housing sentiment index in the fundamental bucket of our analysis. Change in mortgage rate and growth rate of disposable income have been used to account for the problems associated with unit root in the level of these variables.

Our credit conditions indicators are Chicago Fed’s National Financial Conditions Index, Kansas City Fed’s Financial Stress Index, St. Louis Fed Financial Stress Index, spread of 30-year mortgage rate over yield on 1-year Treasury bond (mortgage spread), spread of BAA bond yield over 10-year Treasury Bond yield. Our final measure of credit condition is excess bond premium. This is the difference between the yield on an index of non-financial corporate bonds and a similar maturity government bond, where the latter is adjusted to eliminate default risk. The underlying idea is to have a pure measure of the excess return that is not confounded by expectations of default. This measure has been introduced by Gilchrist and Zakrajšek (2012); Gilchrist et al. (2009). They use secondary market prices of senior unsecured bonds issued by a large representative sample of U.S. non-financial firms to calculate this measure.Footnote 11

Our supply indicators include changes in housing starts, changes in building permits, the median number of months a newly completed home stays on the sales market, the ratio of housing starts to completed buildings, the ratio of new houses for sale that have not been started to new houses for sale that have been completed, and the monthly supply of new houses in the U.S. To the best of our knowledge, the last three measures have not been used in house price forecasting literature. However, using these variables in the context of a stock-flow model has been explored in the literature on housing completion and residential investment, such as Coulson (1999); Lunsford (2015). We chose to use these variables in our analysis because of the information they provide. Using multiple measures of supply helps us avoid overemphasizing one variable in our forecasting.

House Price Growth and Supply Indicators

House Price Growth and Credit Conditions

House Price Growth and Fundamentals

Forecast Comparison of Supply Indicators and Univariate Models

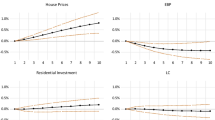

The starts-completion ratio is the ratio of housing starts to total completed housing units in the U.S. We use this as a measure of supply in our analysis because it provides a signal about the impending supply situation in the market. If builders anticipate a negative environment, then housing starts relative to the number of houses completed will fall. In fact, the correlation of this measure with house price growth is 0.57. Another measure that captures similar information is the ratio of new houses for sale that have not been started to the ratio of new houses for sale that have been completed. Our final measure of supply is the monthly supply of new houses in the U.S., which we refer to as inventory in our analysis. Unless noted otherwise, all data has been obtained from the FRED database of the Federal Reserve Bank of St. Louis. When available, we average weekly data to obtain monthly data (Figs. 1, 2, 3, and 4).Footnote 12

Tables 1, 2 and 3 present contemporaneous correlation between house price growth and 18 variables used in our analysis. It is evident that supply indicators on average have the highest correlation with house price growth. Changes in price-rent ratio is one exception where the contemporaneous correlation is 0.92. Although these correlations provide useful summary statistics for the sample period on average, it doesn’t provide any information on the predictive power after controlling for the effect of lag of house price growth.

Empirical Model and Results

In-Sample Predictability of Housing Prices at Different Horizons

While correlation results presented in the above section are informative, it does not provide any information on the marginal predictive power of these variables on future housing returns. To examine this question, we perform a simple in-sample estimation of predictive regression at different horizons. In particular, we seek to examine if the inclusion of one of the indicators leads to an improvement in the in-sample fit of housing return equation. We estimate the following regression specification:

where y is house price growth, and x is one of the predictors. This is a bivariate regression where the objective is to examine if a variable has in-sample predictive power at different forecast horizons. This is based on Marcellino et al. (2006) who argue that direct forecast obtained from the above regression is more robust to misspecification.

The results for this exercise are shown in Table 4. The predictive performance for different variables can be put into different buckets: in the first bucket, we find significant in-sample predictive power at all horizons. In the second category, there are variables where predictive power is concentrated at either very short-run or at longer horizons (m=12). In the final bucket, we have some variables that do not contain marginal predictive power for house price growth beyond what is already contained in its own past values. Most of the supply indicators belong to the first category, where it has marginal predictive power for house price growth. In particular, ratio of new houses for sales not started to new houses for sale completed, and monthly supply of new houses in the U.S. are significant at all conventional levels of significance at all forecast horizons. This is not the case for credit conditions indicators, where the strongest evidence of predictive power lies at longer horizons (h=9,12). In particular, financial stress index and mortgage spread are significant at h=9,12. For macro fundamentals, the results are mixed with housing sentiment exhibiting highest predictive power followed by changes in price-rent ratio at very short horizons. Overall, the results suggest that supply indicators and to some extent credit conditions do contain valuable information about future movements in house price growth than what is already contained in its past values.

Variable Selection Based on LASSO

In the previous section, we show that depending upon different forecasting horizons predictive power of different variables for house price growth vary. One of the issues that a practitioner may encounter in predicting house price growth in the present set up is that bivariate relationship between different indicators and house price growth suggest usefulness of many variables. The inclusion of all these variables in a forecasting exercise may lead to overfitting. Therefore we need a variable selection method to choose the most informative measures for predicting house price growth in our analysis. To do so, we rely on widely use the Least Absolute Shrinkage Operator (LASSO) method. For a detailed exposition describing the LASSO methodology, see the seminal contribution of Tibshirani (1996). Here, we lay out this framework keeping the technical details to the necessary minimum. LASSO solves the following optimization problem:

where y is house price growth , x are different predictors outlined above , K is the total number of independent variables indexed by k.Footnote 13 The parameter \(\lambda \) imposes a penalty factor on reducing the residual sum of squares through additional regressors k. Note that for \(\lambda =0\), the problem reduces to ordinary least squares. Increasing \(\lambda \) leads to dropping of the regressors that are least useful in explaining the variation in y. We perform this variable selection exercise for different forecast horizon where the regression specification is based on Eq. 2. The results for this exercise are presented in Table 5. The optimal value of the tuning parameter \(\lambda \) is based on K-fold cross-validation where K=10. For details on this method, see James et al. (2013). As can be seen, there is certainly a payoff in using the LASSO method. On one hand, the variables chosen by LASSO are also the variables that were consistently significant at different forecast horizons in in-sample forecasting analysis. At the same time, only a small subset of variables survive shrinkage based on the LASSO method. Inventory as measured by monthly supply of new houses is the most important predictor of house price growth according to LASSO. This predictive power holds at all forecast horizon in our analysis. For 1-, and 3-month ahead house price growth, housing market sentiment and changes in price-rent ratio are picked in addition to house price growth lag and inventory. However, they lose their predictive ability for \(h > 3\). This is also consistent with the results shown in the previous section. Interestingly, only mortgage spread is picked in addition to inventory and house price growth lag at h=6,9 and 12 months forecasting horizons. Mortgage spread is one of the six credit condition index and this is the only measure that survives shrinkage at longer horizons.

Variable Selection Based on the Least Angle Regression

In conjunction with LASSO, we employ an intuitive and straightforward variable selection method known as the least angle regression (LAR). LAR embodies a democratic approach to forward stepwise regression, admitting only the degree of predictor contribution it merits. During its initial step, it identifies the predictor most strongly correlated with the response variable. Rather than fully fitting this predictor, LAR incrementally adjusts its coefficient toward its least-squares value, leading to a reduction in its absolute correlation with the evolving residual. Once another predictor reaches a comparable correlation with the residual, the process pauses, and this second predictor is included. This sequence continues until all predictors are integrated into the model, culminating in a complete least-squares fit. We employ this approach to select the most informative predictors from a pool of 18 predictors utilized in our analysis. The findings of this procedure are presented in Table 6. Each column of the table corresponds to predictors chosen for various forecast horizons based on Mallow’s Cp criterion. The outcomes remain largely consistent across diverse horizons. Irrespective of the forecast horizon, LAR consistently identifies inventory as a significant predictor. lagged house price growth appears at most horizons except h=3 and 6. Mortgage spread is an important predictor at longer horizons. These outcomes also align with the variable selection outcomes obtained through the use of LASSO. Overall, the results from the variables selection approach either LASSO or LARS show the important role played by inventory in predicting house prices.

Out-of-Sample Forecasting

Our empirical analysis so far has focused on the in-sample predictive relationship between house price growth and different predictors. In our case, we focus on three set of broad indicators: macro fundamentals, credit conditions and supply. While informative, the results presented so far does not provide us information on the usefulness of these predictors in an out-of-sample context. In particular, how do these predictors perform when information from the full sample is not included. For this purpose we perform a recursive out-of-sample forecasting exercise for house price growth in this sampleFootnote 14. Our sample begins in 2002:M4 and runs through 2022:M8. Our first forecasts cover the period 2010:M4-2011:M3 and uses sample information until 2010:M3. The estimation sample for the first forecasts is 2002:M4-2010M3. We then move ahead one month, re-estimate the model and forecast 2010:M5-2011:M4, etc. Our final set of forecasts, for 2021:M9-2022:M8. We consider different monthly horizon forecasts until M=12. In addition to these monthly forecasts, we also examine the average over next 12 months. These averages are used in the analysis to get around the noise associated with monthly projections. In the subsections below, we first present the results for conventional VAR models and then discuss the results from direct forecast method.

Forecasts from VAR Models

We utilize simple vector auto regression (VAR) models originally proposed by Sims (1980) to undertake our out-of-sample forecasting exercise. Our VAR model includes house price growth and different predictors that include fundamentals, credit conditions and supply indicators. The lags in the VAR model are selected based on Bayesian information criterion (BIC).Footnote 15 From the VAR(p) model, we obtain h-step ahead out-of-sample recursive forecasts of house price growth at time t for each predictor. For parsimony, we consider an AR(1) model as our univariate benchmark model. We perform our analysis in two steps: first, we consider whether inclusion of credit indicators or real house price growth leads to an improvement in forecasting performance of a univariate model. Secondly, we consider trivariate model where we include real house price growth in a bivariate model of real activity and house price growth and examine the inclusion of real house price growth improves the forecasting performance as compared to the bivariate model.

The forecast results from VAR model are shown in Tables 7, 8 and 9. We first compare the results for univariate forecasting models. Although AR(1) is our benchmark model for forecast comparison, it is instructive to compare its forecasting performance relative to a random walk (RW) model. This comparison will provide us preliminary information about predictability of housing markets in an out-of-sample framework. Our findings provide convincing evidence that the information contained in the housing markets’ own past price movements can successfully outperform the random walk model forecasts. These results are presented in the last two column. RMSEs for AR model is lower than that of a RW model for all forecasting horizons. Our results confirm the earlier findings by Case and Shiller (1988, 1990) about the rejection of the efficient market hypothesis in the housing market. In particular, they found that housing markets in Atlanta, Chicago, Dallas, and San Francisco are not efficiently priced and the house price movements in these markets can be predicted with a number of forecasting variables.

Bivariate VAR Models

The results for the bivariate VAR model forecasts are mixed. If one is interested in forecasting house price growth out-of-sample using fundamentals as predictors, the results from bivariate models do not portray a very convincing picture. There is no variable for which the VAR model consistently dominates a univariate AR(1) model. For \(h > 3\) and average over 12 months, changes in disposable income improves the forecast of house price growth over a univariate model. When credit condition measures are used as predictors, the evidence is also mixed. If one is interested in forecasting over 12-months, the results suggest that EBP, BAA10Y and STLFSI have lower RMSE than AR(1) model, although the improvement is modest at best. At very short horizons, h=1,2, NFCI and KCFSI perform the best. Some of these results are consistent with the in-sample prediction results obtained in the earlier section. The results are most encouraging for the supply indicators. All 6 supply indicators improve upon the forecasting performance of the univariate AR model at all forecasting horizons. The degree of improvement is different for different measures. Inventory as measured by months of supply of new homes has the highest predictive power with an improvement of almost 30 percent for h=1-12 months horizon. The second best measure is EPNSS where the reduction in RMSE is around 22 percent. These results indicate that including different measures of supply indicator in a VAR model leads to significant improvement in forecasting performance of house price growth in the post-financial crisis period. The superiority of supply indicators in forecasting house price growth in an out-of-sample framework that past values of house price already encapsulate the information present in the past values of fundamentals and credit conditions, whereas this is not the case for supply indicators.

Trivariate VAR Models

The results from bivariate model suggest that a model of house price growth with supply indicators lead to superior forecasting performance. The question then arises is if we can include more variables to the bivariate system so that we can gain additional benefit in terms of lower RMSEs. The natural question is what combinations to use for the trivariate model. We seek guidance on this from our LASSO framework. LASSO results pick inventory for all forecasting horizons. In addition to inventory, housing sentiments and changes in price-rent ratio were chosen for short horizons and mortgage spread were picked for \(h > 3\). We incorporate these findings into our analysis by generating forecasts from three trivariate models: one that includes house price growth, inventory, and housing sentiment; another with house price growth, inventory, and changes in the price-rent ratio; and a third incorporating house price growth, inventory, and mortgage spread.

The forecasting results from trivariate VAR models are shown in Table 10 . + in the columns refers to the inclusion of the variable to house price growth and inventory. Out-of-sample forecasting results are consistent with the LASSO results. Housing sentiment and changes in price-rent ratio lead to improvement in forecasting of house price growth at 1-month and 2-months ahead. At longer forecasting horizons, only inclusion of mortgage spread leads to improvement in forecasting performance in terms of lower RMSE. The improvement in forecasting performance is around 4-5% in terms of lower RMSEs. The degree of improvement is not as significant as the bivariate inventory model over univariate AR model.

Forecasts from Nonlinear Models

We also generate forecasts using three widely popular nonlinear autoregressive models: Smooth Transition Autoregressive (STAR), Self-Exciting Threshold Autoregressive (SETAR), and Generalized Additive Model (GAM). STAR and SETAR are classes of threshold models in which the relationship between the dependent variable and its lagged values varies depending on a threshold variable. The threshold variable represents a point at which the relationship between the dependent variable and its lagged values changes abruptly. These models are useful when analyzing time series data that exhibit nonlinearity. For details on STAR and SETAR models, see Teräsvirta (1994); Teräsvirta and Anderson (1992); Dijk et al. (2002) et al., among others. GAMs extend the concept of linear regression by incorporating nonlinear smoothing functions, such as cubic splines or loess smoothers, to model the relationship between the predictor variables and the response variable. The advantage of GAMs is that they can model complex nonlinear relationships without researchers needing to specify a particular functional form. This makes GAMs particularly useful when the relationship between the response variable and the predictor variables is unknown or difficult to specify.Footnote 16

We utilize these three models to generate iterative forecasts for house price growth, and the results are presented in Table 11. We compare these results with our benchmark AR and Random Walk models. The results show that the AR(1) model consistently outperforms the forecasts obtained from all these nonlinear models. Forecasts from GAM come closest to the AR model, whereas forecasts from STAR and SETAR perform poorly, especially at longer horizons. Overall, the results seem to indicate that there is not much payoff in using nonlinear models in forecasting house price growth in the U.S.

Comparison with Direct Forecast Method

One concern with the forecasts generated from VAR model is that those forecasts may be prone to misspecification. This may be especially relevant for long horizon forecast as pointed out by Marcellino et al. (2006). To address this issue, we perform direct estimation of the model instead of iterative forecasting as done in the previous sectionFootnote 17. Direct forecasts are made using a horizon-specific estimated model, where the dependent variable is the multiperiod ahead value being forecasted. The results for bivariate models are shown in Tables 12, 13, 14 and 15. We find slight improvement in forecasts for most of the models as compared to the iterative models in previous sections. The overall pattern in terms of the superiority of the supply indicators in forecasting house price growth stands.

The results for trivariate models show some improvements over iterative forecasts in Table 15 except for the model with mortgage spread where the improvement is substantial. Most of the improvements is obtained at forecast horizon \(h > 1\). We find that the improvement of direct forecast over iterative forecast is more than 20 percent on average over 1-12 months horizon. As a result, the reduction in RMSE compared to a univariate AR model is more than 40 percent. To summarize, we do obtain slight improvement in forecasting performance if direct method of forecasting is used. The improvement is substantial for the trivariate model with house price growth, inventory and mortgage spread.

Conclusion

Do the fundamentals, credit conditions, and supply indicators predict the growth of house prices in the US in the post-financial crisis sample? And how does the forecasting performance vary among these three indicators? This paper attempts to answer these questions by using monthly data from April 2002 through August 2022. The results confirm that the housing market shows predictable behavior in the post-financial crisis period. Although a lot of variables show strong predictive ability in the in-sample prediction, a variable selection method like LASSO and an out-of-sample forecasting exercise reduce the predictor space to a few variables. Among these variables, supply indicators have the strongest predictive power for future movements of house price growth. The bivariate model of house price growth and inventory-months of supply of newly built homes has the lowest mean squared error (RMSE) among 18 different predictors, and the RMSE from this model is 33% lower than the forecasts from a univariate model. Models incorporating housing sentiment and changes in price-ratio significantly improve the forecasting performance at 1- and 3-month forecast horizons. The LASSO approach is used to further shrink the predictor space. Besides house price growth’s own lag, LASSO selects housing sentiment and changes in price-rent ratio at short horizons and mortgage spread over treasury yields for horizons greater than 3 months. Inventory level is selected for all forecasting horizons. The results show that adding mortgage spread to a VAR model with house price growth and inventory improves the forecasting performance of house price growth. Additionally, there is some improvement in the forecasting performance if a "direct" forecast approach is used, where the forecasts are made using a horizon-specific estimated model and the dependent variable is forecasted over an iterative forecasting model. Overall, there is strong evidence that housing inventory combined with mortgage spread provides valuable information about future movements in house price that cannot be obtained from its past values and other predictors.

Notes

Leamer (2007) argued that housing is the business cycle and he suggested replacing output gap measure in Taylor’s rule with housing starts and the changes in housing starts.

See Smith et al. (1988) for an excellent review of the housing market models.

The six measures of fundamentals are changes in price-income ratio, changes in price-rent ratio, labor market activity indicator, housing sentiment index, changes in mortgage rate and change in real disposable income growth. Different measures of credit conditions include a measure of financial conditions, two measures of financial stress, mortgage rate spread over treasury bond, BAA bond spread and excess bond spread. The six measures of supply indicators are changes in housing starts, changes in building permits, median number of months on sales market for newly completed homes, ratio of housing starts to completed buildings, ratio of new houses for sales not started to new houses for sale completed, and monthly supply of new houses in the U.S.

Direct forecasts are made using a horizon-specific estimated model, where the dependent variable is the multiperiod ahead value being forecasted. For details, see Marcellino et al. (2006).

Some papers have compared the forecasting performance of different timeseries models in forecasting house price growth. For example, Das et al. (2011) find that the Dynamic Factor Model statistically outperforms the vector autoregressive models in forecasting regional house price growth. Plakandaras et al. (2015) found some payoff in using hybrid machine models.

We use three nonlinear time series models for our analysis: Smooth Transition Autoregressive (STAR), Self-Exciting Threshold Autoregressive (SETAR), and Generalized Additive Model (GAM).

These tests are performed using Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP). The results are also similar for other unit root tests. The results are not reported here, but are available upon request.

To avoid duration mismatch issues, which can contaminate the information content of credit-risk indicators, yield spreads for each underlying corporate security are derived from a synthetic risk-free security that exactly mimics the cash flows of that bond.

We do not include monthly supply of existing homes because the timeseries data is unavailable for our sample period.

All variables are standardized for LASSO, so that selection is not driven by differences in relative variances.

Because of data unavailability, we do not include real-time data in our analysis.

For comparison, we also fix the number of lags in VAR to 1, and the results are qualitatively similar.

See James et al. (2013) for details on GAM.

For iterative VAR forecasts, in addition to forecasting the variable of interest, in this case, house price growth, we also forecast the other variables to obtain multi-period ahead forecasts (for example, fundamentals).

References

Annett, A. (2005). House prices and monetary policy in the euro area. Chapter III in Euro area policies: selected issues, IMF Country Report, 5, 266.

Balcilar, M., Gupta, R., & Miller, S. M. (2015). The out-of-sample forecasting performance of nonlinear models of regional housing prices in the US. Applied Economics, 47(22), 2259–2277.

Bhatt, V., & Kishor, N. K. (2022). Role of credit and expectations in house price dynamics. Finance Research Letters, 50, 103203.

Caplin, A., & Leahy, J. (2011). Trading frictions and house price dynamics. Journal of Money, Credit and Banking, 43, 283–303.

Carroll, C. D., Otsuka, M., & Salacalek, J. (2011). How Large Are Housing and Financial Wealth Effects? A New Approach. Journal of Money, Credit and Banking, 43(1), 55–79.

Case, K., & Shiller, R. J. (1988). The behavior of home buyers in boom and post-boom markets. New England Economic Review, 29–46

Case, K. E., & Shiller, R. J. (1990). Forecasting prices and excess returns in the housing market. Real Estate Economics, 18(3), 253–273.

Case, K. E., & Shiller, R. J. (2003). Is there a bubble in the housing market? Brookings papers on economic activity, 2, 299–362.

Case, K. E., Shiller, R. J., & Quigley, J. M. (2005). Comparing Wealth Effects: The Stock Market vs. the Housing Market. Advances in Macroeconomics, 5(1), 1–34.

Coulson, N. E. (1999). Housing inventory and completion. The Journal of Real Estate Finance and Economics, 18, 89–105.

Crawford, G. W., & Fratantoni, M. C. (2003). Assessing the forecasting performance of regime-switching, ARIMA and GARCH models of house prices. Real Estate Economics, 31(2), 223–243.

Crawford, G., & Rosenblatt, E. (1995). Efficient mortgage default option exercise: Evidence from loss severity. Journal of Real Estate Research, 10(5), 543–555.

Das, S., Gupta, R., & Kabundi, A. (2011). Forecasting regional house price inflation: a comparison between dynamic factor models and vector autoregressive models. Journal of Forecasting, 30(2), 288–302.

Dotsis, G., Petris, P., & Psychoyios, D. (2023). Assessing Housing Market Crashes over the Past 150 years. The Journal of Real Estate Finance and Economics, 1–19.

Fan, Y., Yang, Z., & Yavas, A. (2019). Understanding real estate price dynamics: The case of housing prices in five major cities of China. Journal of Housing Economics, 43, 37–55.

Fan, Y., & Yavas, A. (2020). Price dynamics in public and private commercial real estate markets. The Journal of Real Estate Finance and Economics, 1-41

Favara, G., & Imbs, J. (2015). Credit Supply and the Price of Housing. American Economic Review, 105(3), 958–992.

Gilchrist, S., & Zakrajšek, E. (2012). Credit spreads and business cycle fluctuations. American Economic Review, 102(4), 1692–1720.

Gilchrist, S., Yankov, V., & Zakrajšek, E. (2009). Credit market shocks and economic fluctuations: Evidence from corporate bond and stock markets. Journal of Monetary Economics, 56(4), 471–493.

Glaeser, E. L., Gyourko, J., & Saiz, A. (2008). Housing supply and housing bubbles. Journal of Urban Economics, 64(2), 198–217.

Glaeser, E. L., & Sinai, T. (2013). Postmortem for a housing crash. Hous Financ Crisis, 1(2), 117–128.

Gupta, R., & Das, S. (2010). Predicting downturns in the US housing market: a Bayesian approach. The Journal of Real Estate Finance and Economics, 41, 294–319.

Gupta, R., Marfatia, H. A., Pierdzioch, C., & Salisu, A. A. (2022). Machine learning predictions of housing market synchronization across US states: the role of uncertainty. The Journal of Real Estate Finance and Economics, 1–23

Gyourko, J. (2009). Housing supply. Annual Review of Economics, 1(1), 295–318.

Himmelberg, C., Mayer, C., & Sinai, T. (2005). Assessing high house prices: Bubbles, fundamentals and misperceptions. Journal of Economic Perspectives, 19(4), 67–92.

Holly, S., & Jones, N. (1997). House prices since the 1940s: cointegration, demography and asymmetries. Economic Modelling, 14(4), 549–565.

Hort, K. (1998). The determinants of urban house price fluctuations in Sweden 1968–1994. Journal of Housing Economics, 7(2), 93–120.

Iacoviello, M., et al. (2002). House prices and business cycles in Europe: A VAR analysis. Technical Report, Boston College Working Papers in Economics

James, G., Witten, D., Hastie, T., & Tibshirani, R. (2013). An introduction to statistical learning (Vol. 112, p. 18). New York: Springer

Justiniano, A., Primiceri, G. E., & Tambalotti, A. (2019). Credit supply and the housing boom. Journal of Political Economy, 127(3), 1317–1350.

Kishor, N. K. (2007). Does consumption respond more to housing wealth than to financial market wealth? If so, why?. Journal of Real Estate Finance & Economics, 35(4)

Kishor, N. K., & Koenig, E. F. (2014). Credit Indicators as Predictors of Economic Activity: A Real-Time VAR Analysis. Journal of Money, Credit and Banking, 46, 545–564.

Kishor, N. K., & Marfatia, H. A. (2017). The dynamic relationship between housing prices and the macroeconomy: Evidence from OECD countries. The Journal of Real Estate Finance and Economics, 54, 237–268.

Kishor, N. K., & Marfatia, H. A. (2018). Forecasting house prices in OECD economies. Journal of Forecasting, 37(2), 170–190.

Kuvalekar, A., Manchewar, S., Mahadik, S., & Jawale, S. (2020). House price forecasting using machine learning. In Proceedings of the 3rd International Conference on Advances in Science & Technology (ICAST)

Leamer, E. E. (2007). Housing is the business cycle. NBER Working Paper

Liu, X. (2013). Spatial and temporal dependence in house price prediction. The Journal of Real Estate Finance and Economics, 47, 341–369.

Lunsford, K. G. (2015). Forecasting residential investment in the United States. International Journal of Forecasting, 31(2), 276–285.

Marcellino, M., Stock, J. H., & Watson, M. W. (2006). A comparison of direct and iterated multistep AR methods for forecasting macroeconomic time series. Journal of Econometrics, 135(1–2), 499–526.

McCarthy, J., & Peach, R. W. (2004). Are home prices the next bubble? FRBNY Economic Policy Review, 10(3), 1–17.

Meen, G. (2002). The time-series behavior of house prices: a transatlantic divide? Journal of Housing Economics, 11(1), 1–23.

Mian, A., & Sufi, A. (2011). House prices, home equity-based borrowing, and the US household leverage crisis. American Economic Review, 101(5), 2132–56.

Mian, A., Rao, K., & Sufi, A. (2013). Household balance sheets, consumption, and the economic slump. The Quarterly Journal of Economics, 128(4), 1687–1726.

Mian, A., & Sufi, A. (2014). What explains the 2007–2009 drop in employment? Econometrica, 82(6), 2197–2223.

Miles, W. (2008). Boom-bust cycles and the forecasting performance of linear and non-linear models of house prices. The Journal of Real Estate Finance and Economics, 36, 249–264.

Milunovich, G. (2020). Forecasting Australia’s real house price index: A comparison of time series and machine learning methods. Journal of Forecasting, 39(7), 1098–1118.

Oust, A., Hansen, S. N., & Pettrem, T. R. (2020). Combining property price predictions from repeat sales and spatially enhanced hedonic regressions. The Journal of Real Estate Finance and Economics, 61, 183–207.

Plakandaras, V., Gupta, R., Gogas, P., & Papadimitriou, T. (2015). Forecasting the US real house price index. Economic Modelling, 45, 259–267.

Poterba, J. M., Weil, D. N., & Shiller, R. (1991). House price dynamics: the role of tax policy and demography. Brookings Papers on Economic Activity, 1991(2), 143–203.

Rapach, D. E., & Strauss, J. K. (2009). Differences in housing price forecastability across US states. International Journal of Forecasting, 25(2), 351–372.

Risse, M., & Kern, M. (2016). Forecasting house-price growth in the Euro area with dynamic model averaging. The North American Journal of Economics and Finance, 38, 70–85.

Segnon, M., Gupta, R., Lesame, K., & Wohar, M. E. (2021). High-frequency volatility forecasting of US housing markets. The Journal of Real Estate Finance and Economics, 62, 283–317.

Sims, C. A. (1980). Macroeconomics and reality. Econometrica: Journal of the Econometric Society, 1–48

Smith, L. B., Rosen, K. T., & Fallis, G. (1988). Recent developments in economic models of housing markets. Journal of Economic Literature, 26(1), 29–64.

Teräsvirta, T. (1994). Specification, estimation, and evaluation of smooth transition autoregressive models. Journal of the American Statistical association, 89(425), 208–218.

Teräsvirta, T., & Anderson, H. M. (1992). Characterizing nonlinearities in business cycles using smooth transition autoregressive models. Journal of Applied Econometrics, 7(S1), S119–S136.

Dijk, D. V., Teräsvirta, T., & Franses, P. H. (2002). Smooth transition autoregressive models–a survey of recent developments. Econometric Reviews, 21(1), 1–47.

Tibshirani, R. (1996). Regression shrinkage and selection via the lasso. Journal of the Royal Statistical Society: Series B (Methodological), 58(1), 267–288.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

The author acknowledges financial support from the Niho Faculty Excellence Fund at the University of Wisconsin-Milwaukee.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Kishor, N.K. Forecasting House Prices: The Role of Fundamentals, Credit Conditions, and Supply Indicators. J Real Estate Finan Econ (2023). https://doi.org/10.1007/s11146-023-09971-y

Accepted:

Published:

DOI: https://doi.org/10.1007/s11146-023-09971-y

Keywords

- House price forecasting

- Fundamentals

- Credit conditions

- Supply indicators

- Variable selection

- Direct forecasts