Abstract

In this paper, we consider the dynamic features of house price in metropolises that are characterised by a high degree of internationalisation. Using a generalised smooth transition (GSTAR) model we show that the dynamic symmetry in house price cycles is strongly rejected for the housing markets considered in this paper. Further, we conduct an out-of-sample forecast comparison of the GSTAR with a linear AR model for the metropolises under consideration. We find that the use of nonlinear models to forecast house prices, in most cases, generate improvements in forecast performance.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

During the last decade, housing markets have been characterised by a high degree of instability. This has particularly been the case in large metropolitan areas where real estate markets have experienced dramatic swings which resulted in one of the deepest recessions the world has experienced since the great depression in the 1930s. Partially motivated by these events, several authors have investigated the cyclical behaviour of real estate prices. Housing markets are known to be prone to boom and bust episodes. In a typical expansion phase, transaction volumes are high, average selling times are short, and prices tend to rise rapidly. In a bust period, transaction volumes are low, average selling times are long, and price growth is moderate or negative.

The empirical literature on housing markets recognises that the real economy is vulnerable to house price swings, but it is less assertive about the features of cyclical patterns. For example, Muellbauer and Murphy (1997) explore the behaviour of house prices in the UK. The authors suggest that transaction costs associated with the housing market cause important nonlinearity in house price dynamics. Further, Seslen (2004) argues that households exhibit rational responses to returns on the upside of the market, but do not respond symmetrically to downturns. On an upswing of the housing cycle, households exhibit forward-looking behaviour and are more likely to trade up, with equity constraint playing a minor role. On the other hand, households are less likely to trade when prices are on the decline causing stickiness on the downside of the housing market cycle.

While economic theory suggests that asymmetry may be a characteristic feature of real estate cycles, there have not been many attempts at modelling this phenomenon in an explicit fashion. Traditionally, in empirical literature house price dynamics have been analysed using error correction mechanisms to investigate short-run deviations from the fundamental value of housing. For example, Abrahm and Hendershott (1993) estimate a cointegrated model which includes lagged house price changes among other explanatory variables. They found evidence of slow adjustment toward the equilibrium which implies a cyclical adjustment path. Abelson et al. (2005) estimate an asymmetric threshold cointegrated model to investigate nonlinearity in house prices in Australia. Malpezzi (1999) analyses the impact of supply and demand factors on the path of house price adjustments. However, modelling asymmetry would require nonlinear time series models. Econometric models that work under the assumption of symmetry and linearity, in the presence of asymmetry would clearly be mis-specified and may lead to spurious inference (see for example Blatt 1980).

In this paper, we investigate the characteristics of housing market cycles in global cities. A global city (or world city) is defined as a city that is of primary importance for the global economic system (Sassen 2003). The term ‘global city’ has its origins from urban studies and relates to the idea that world globalization is facilitated by strategic cities which are instrumental in supporting the operation of the global system of finance and trade. According to Sassen (2003), the process of globalization gave rise to new geography in which global cities function as places that provide specific knowledge for multinational enterprises to manage the process of globalization. A characteristic feature of world cities is that their housing market dynamics is driven by local and global investment demand, rather than local household earnings. Given the peculiarity of world cities, it is most likely that housing markets in these metropolises have different dynamics than smaller urban settlements.

In this paper, we are interested in addressing three questions. First, what are the characteristics of house price cycles in global cities? Are housing market cycles asymmetric? Also, global cities are interconnected and have shared the experience of globalization. An obvious question is, therefore: Do world cities have similar housing market cycles? According to economic theory, housing markets in large metropolitan areas display significant momentum (Case and Shiller 1989), are mean reverting (Cutler et al. 1991), and experience high volatility with respect to the fundamentals (Glaeser and Nathanson 2015). While house prices dynamics at national and regional levels have been widely investigated, research at a more disaggregated level is rare. In this respect, notable exceptions are the work by Cook and Watson (2017) and Alqaralleh and Canepa (2019) who employed disaggregated data for world cities areas to investigate the dynamics of housing markets. Other related studies that investigate the turning points, such as by Cook (2006), Holly and Jones (1997) and Cook and Holly (2000), consider asymmetry in house prices aggregated at the regional or country level. However, to the best of our knowledge, a comprehensive investigation into the asymmetric adjustment at a disaggregated level is still missing in the literature. Simply assuming that the properties of the housing market at the national or regional level would also describe the features of the real estate markets in world cities is counterfactual. Strong demand pressure and inelastic supply leave these metropolises more exposed to bubbles in the housing market than the rest of the country. In this respect, a few recent studies support this conjecture. For example, Glaeser et al. (2008) show that during boom phases house prices in the US grow much more strongly in metro areas with inelastic supply. Saiz (2010) demonstrates that geographical restrictions constrain the elasticity of supply. The author shows that in cities that lack construction land, the process of urbanisation leads to price increases.

Frequent booms and busts in the housing market of world cities open the question of how the series of house prices should be modelled. Accordingly, the second issue we address in this paper is the following: How do we model asymmetric cycles of real estate prices in global cities? As Sichel (1993) points out, an asymmetric cycle is one in which a phase of the cycle is different from the mirror image of the opposite phase. A natural question is, therefore: What kind of econometric model would best be able to capture asymmetric adjustments in house prices? Once an econometric model has been specified, one may want to use it to make a forecast. The fact that we use a nonlinear model to handle asymmetry in the housing market has some practical implications. When real estate prices are being forecast using nonlinear models, the estimated forecast densities are asymmetric. On the other side in linear models, the forecast density is symmetric around each point forecast. Therefore, the third issue we tackle in this paper is: How does the out-of-sample performance of the adopted nonlinear model compare to a simple linear specification counterpart?

In order to answer the above questions, a three-step investigation has been conducted. In the first step, we focus on testing for potential asymmetric behaviour in the house price cycle. In particular, the non-parametric Triples test of Randles et al. (1980) is used to test for asymmetries in housing market cycles. The advantage with respect to available alternative inference procedures (see for example Sichel 1993) is that the test statistic has good finite sample properties and is robust to outliers (see Eubank et al. 1992). The application of the Triples test reveals evidence of asymmetric adjustment in all metropolises under consideration. In particular, the nature of the asymmetry observed indicates prolonged expansions phases in the market along with steeper contractionary periods.

The empirical results from the first step of our investigation can be a useful guide for the specification of the nonlinear model that would best be able to capture the observed features of housing market cycles. Accordingly, in the second step of our investigation, the generalised smooth transition model (GSTAR) suggested in Canepa and Zanetti Chini (2016) is used to estimate house price dynamics for the sample under consideration. The authors propose a STAR-type model where the logistic smooth transition function has two parameters governing the two tails of the sigmoid function in the nonlinear component of the model. The advantage of the proposed parameterisation with respect to the ordinary smooth transition models (STAR) is that the resulting specification is able to model the tails of the logistic function independently so that the rate of change in the left tail of the transition function can be different from the change in the right tail.

Regime switching models have been used in the literature to capture nonlinearity in the housing market. For example, Kim and Bhattacharya (2009) use a STAR model to investigate for nonlinearity in the regional housing market in the United States. The authors find that West and Northeast regions (and to some extent also the South) are characterized by high-speed transition between regimes. Nonlinear models are also used by Crawford and Fratantoni (2003) to forecast house price changes. Regime-switching models such as the STAR allow the dynamic of house price growth rates to evolve according to a smooth transition between regimes that depends on the signs and magnitude of past realisation of house price growth rates (see Chan and Tong 1986). The low speed of transition between different regimes in house price growth found in empirical studies validates the choice of smooth transition models. A possible shortcoming of these type of nonlinear models describing the features of housing markets is that in the model specification a symmetric transition function is used to capture oscillations from the conditional mean of the changes in house price series. Although STAR-type models efficiently describe nonlinearity in house price growth rates, the commonly used transition functions may not be suitable to capture dynamic asymmetries in real estate cycles.

In this paper, we argue that what in the related literature has been called ‘asymmetry’ can at most define a qualitative feature of the data, while the modelling issue is still neglected since the logistic transition function, which is commonly used to model house price series, is symmetric by construction. In other words, STAR-type models used in the related literature are at most able to tackle the question: Do house price series go back to their original regime after a shock and when? However, the primary interest of our investigation is to answer another, more challenging question: How do we model the fact that the speed of the transition between expansion and contraction phases is different? Also, how can we capture the fact that troughs and peaks are not symmetric? The model proposed by Canepa and Zanetti Chini (2016) is potentially promising since the type of parametrisation of the logistic transition function allows for the expansion and contraction phases to be modelled independently.

In the final stage of our investigation, we consider whether using the GSTAR model for forecasting leads to important improvements over forecasting with an incorrectly specified linear model. In the literature, the issue of the forecasting performance of the nonlinear model is still an open question. For example, Balcilar et al. (2015) use a STAR-type model to forecast house price distributions in the United States. They find that the use of nonlinear models to forecast house prices typically does not generate improvements in forecast performance. On the other side, Cabrera et al. (2011) compare the out-of-sample forecasting performance of international securitised real estate returns using linear and non-linear models. They compare the performance of several nonlinear models to the benchmark linear AR model and conclude that nonlinear models produce better out-of-sample forecasts. Similarly, Miles (2008) using the generalised autoregressive model concludes that the nonlinear specification has superior performance in out-of-sample forecasting, especially in housing markets traditionally associated with high home price volatility.

Against this background, we conduct an out-of-sample forecast comparison of the GSTAR with a linear AR model for the metropolises under consideration. We find that the use of nonlinear models to forecast house prices, in most cases, generate improvements in forecast performance. This is especially the case at short horizons.

The remainder of this paper is organised as follows. In Section “Housing Market Cycles in Large Metropolitan Areas”, some theoretical background on housing market cycle asymmetry is introduced. In Section “Data and Asymmetry Tests”, the characteristic of the housing market in large metropolitan areas are investigated. In Section “Testing for Asymmetries in the Housing Market Cycles”, the testing and modelling procedure are briefly discussed before presenting the empirical results. In Section “Modelling House Price Cycles”, the forecasting performance of the GSTAR model is investigated. In Section “Forecasting House Prices”, some robustness tests are performed. Finally, in Section “Robustness Checks”, some concluding remarks are given.

Housing Market Cycles in Large Metropolitan Areas

The behaviour of housing markets over phases of the business cycle has long been an object of interest in economic literature. From the theoretical point of view economists have explained asymmetric behaviour of the real estate cycle using demand and supply framework where the supply side is inelastic. For example, Abraham and Hendershott (1996) describe an equilibrium price level to which the housing market tends to adjust. The authors divide the determinant of house price appreciation in two groups: one that explains changes in the equilibrium price and another that accounts for the adjustment mechanism in the equilibrium process. Slow adjustment toward the equilibrium can be regarded as an indication of asymmetries in real estate cycles. Abelson et al. (2005) suggest that during periods when house prices increase, households exhibit forward-looking behaviour, while the equity constraint factor plays only a minor role. On the other hand, households are less willing to buy or sell properties during contraction phases due to loss aversion and more pronounced equity constraints causing stickiness on the downside of the housing market cycle.

The literature points to several of the factors that can explain the asymmetries of housing price cycles. First, housing prices are closely related to the business cycle. Asymmetry in housing cycles may result from asymmetry in the determinants of housing prices (see, for example, André 2010). Second, there is a close relationship between financial cycles and the housing market cycles. Theoretical research has argued that endogenous developments in financial markets can greatly amplify the effect of small income shocks through the economy. In a seminal paper, Bernanke et al. (1996) term this amplification mechanism the ‘financial accelerator’ or ‘credit multiplier’. The primary idea behind the financial accelerator is that under the assumption of a fixed leverage ratio, positive or negative shocks to income have a procyclical effect on the borrowing capacity of households and firms. This, subsequently, affects housing prices. Positive shocks to household income translate into higher house prices and an increase in economies where the prevailing leverage ratios are higher, and lower in countries where such leverage ratios are lower. Following a similar argument, Kiyotaki and Moore (1997) show that rising asset prices may ignite a lending boom by increasing the collateral values. A reversal in fundamentals further increases the loan default rate (see also Borio 2014). Third, cyclicality can be induced by the combination of extrapolative expectations and slow supply responses, which can generate hog-type cycles (André 2015). Bolt et al. (2014) argue that heterogeneous expectations and switching between optimistic and pessimistic expectations in the housing market generate cyclical behaviour and nonlinear aggregate price fluctuations with booms and busts triggered by stochastic shocks and significantly amplified by self-fulfilling expectations. Recent literature has used laboratory experiments to study the relationship between expectation and housing markets bubbles. For example, Bao et al. (2017) design an experimental housing market and find that expectations-driven bubbles and crashes in the housing markets are considerably similar to those observed in speculative asset markets (see also Glaeser and Nathanson 2015).

Coming to house price dynamics in large metropolitan areas, several authors have argued that in densely populated urban areas the rigidity of the supply side plays a major role in housing market cycles. This literature argues that high real construction costs and stricter regulations on new developments introduce unpriced supply restrictions. For example, Capozza et al. (2004) show that strict regulations on new development such as minimum lot size or regulatory-induced delays increase the cost of new housing (both in absolute terms and relative to existing housing) and they reduce the ability of builders to respond quickly to demand shocks. Similarly, Mayer and Somerville (2000) show that construction is less responsive to price shocks in markets with more local regulation. The fact that inelastic housing supply in large metropolitan areas induces high price volatility is broadly consistent with the literature on housing market bubbles. According to this literature, bubbles are seen as a temporary increase in optimism about future prices. Therefore, metropolitan areas where housing supply is more inelastic, demand shocks have a greater effect on price and less effect on new construction. In an influential paper, Glaeser et al. (2008) present a theoretical model of housing bubbles which postulates that housing markets with elastic supply have fewer and shorter bubbles and smaller price increases.

A closely related strand of the literature suggests that real estate prices in metropolitan areas exhibit short-run persistence and long-run mean reversion (see for example Abraham and Hendershott 1996; Capozza and Seguin 1996; Malpezzi1999; Meen 2002). In their seminal paper Case and Shiller (1989) find that house prices are correlated, which suggests that residential property markets are inefficient. In a more recent work Case and Shiller (2003) consider house prices in relation to the fundamentals. The authors make a compelling case that house prices exhibit statistically significant short-term momentum. Also, Shiller (1990) posits that asymmetries in real estate house price cycles are partially due to backward-looking expectations of market participants. In a similar vein, Capozza et al. (2004) (see also Dusansky and Koç 2007) finds that backward-looking expectations are likely to strengthen the momentum effect in booming housing markets.

High information costs can also result in asymmetric adjustments in the housing markets. In this respect, empirical research has found evidence of a negative correlation between population density and information costs. For example, Clapp et al. (1995) find that higher population density increases price transparency in the housing market. When transaction volume increases information costs are lower and, therefore, prices respond more rapidly to macroeconomic shocks. Empirical evidence also suggests that households show stronger behavioural biases when assets are harder to price (Hirshleifer et al. 2013; Kumar 2009; Capozza et al. 2004). Thus, we expect contraction phases to be shorter in large global cities than countrywide.

To summarise, consensus reached in the literature suggests that in densely populated urban areas the higher level of real construction costs and stricter regulations increase dynamic asymmetries in housing market cycles. On the other side, greater market transparency should have the opposite effect, so that in these cities the adjustment towards fundamental price level should be more rapid and the momentum effect is expected to be weaker. All in all, the dynamic behaviour of house prices is strongly dependent on the prevalent signs of these combined effects.

Data and Asymmetry Tests

The data used in this study consist of house prices in eleven global cities. The housing markets under consideration include a selection of metropolises in Europe, the United States, and the Asia-Pacific region. In the United States, the markets examined are New York, Los Angeles, San Francisco, and Chicago. For the Asia-Pacific region, the cities selected for analysis are Hong Kong, Singapore, Seoul, Tokyo, and Sydney. The cities of Europe chosen for the study are Vienna and Paris. Due to the availability of data, the period under consideration differs across the sample. For the cities in the United States, the data considered are the monthly Case-Shiller home price index from 1987: M1 to 2019: M1; for the Asian cities, the prices are monthly observations from 1996: M1 to 2015: M12. For Vienna and Sydney, the sample includes quarterly data from 1986: Q3 to 2018: Q4, and, finally, for Paris, the sample includes data from 1991: Q3 to 2018: Q4. The data were collected from several sources: house price series for the US cities were sourced from the Federal Reserve Bank of St. Louis data collection. The Asian cities’ data were provided by Bloomberg and the remaining house price series were collected from the Bank of International Settlement.

As far as the sample is concerned, global cities have been selected as a representative sample of metropolitan areas that rank among the top twenty in the Global Power City Index (GPCI) (2018) as world cities. The GPCI index ranks major cities of the world in the order of their ‘magnetism’ or their comprehensive power to attract creative people and business enterprises from around the world. More precisely, the GPCI index ranks a number of metropolises according to the degree of their economy, the level of research and development, the degree of cultural interaction, the degree of liveability, the quality of the environment, the degree of accessibility, and other individual indicators. Most of the cities considered in the sample have in common the fact that they are i) headquarters of several multinational corporations, ii) major financial or manufacturing centres, iii) important laboratories of new ideas and innovation hubs in business, economics, and culture, iv) host high-quality educational institutions, including renowned universities with international student attendance and world-class research facilities, v) feature a high degree of diversity in terms of language, culture, religion, and ideologies.

As Table 1 illustrates, seven of the cities selected are among the 2018 GPCI top-ten ranked global cities. In many cases, the choice of metropolises was dictated by the availability of data. However, the final sample does include most of the top-ten metropolises in the GPCI index.Footnote 1

Testing for Asymmetries in the Housing Market Cycles

Detecting asymmetry in the real estate time series is important since linear and Gaussian models are incapable of generating asymmetric fluctuations. Evidence of asymmetry may guide empirical investigators toward a particular class of nonlinear specifications able to model asymmetric cycles.

Therefore, prior to attempting any model estimation, in the following section, we investigate the characteristic features of housing market cycles for the cities under consideration.

In this paper, we focus on two types of asymmetries which may or not occur simultaneously in the housing market: steepness and deepness. As Sichel (1993) points out, steepness occurs when contractions are steeper than expansions, or vice-versa. The second type of asymmetry occurs when troughs are deeper than peaks are tall. Steep cycles in the housing markets may be generated by stiff housing supply. On the one hand, improving economic conditions tend to increase the incomes of households and, therefore, to boost the demand for housing. On the other hand, when property prices rise above the replacement costs, property developers initiate the construction process based on current property prices. However, creating a supply of new properties is, by definition, a slow process. By the time new properties are delivered, economic conditions may have changed for worse and prices begin to decline. This inertia of supply responsiveness causes asymmetries in the real estate cycles (Davis and Zhu 2005). Deepness could be generated by a model where endogenous developments in financial markets may amplify the effect of small income shocks through the economy.

To investigate possible asymmetries in the housing market cycles the Triples test suggested in Randles et al. (1980) has been used. Loosely speaking, the test is based on the principle that if a time series exhibits steepness, then its first differences should exhibit negative skewness. On the other hand, if a time series exhibits deepness, then it should exhibit negative skewness relative to mean or trend. Therefore, a test for steepness can be computed by using the series in first difference, whereas a test for deepness can be based on the coefficient of skewness of the house price series in levels. Intuitively, the Triples test counts all possible triples from a sample of size T of a univariate time series. When most of the triples are right-skewed the process is said to be asymmetric (see Randles et al. 1980 for more details).

Table 2 shows the calculated test statistics and relative p-values. In particular, the second column in Table 2 displays the calculated Triples test obtained using the logs of house price series for each city under consideration, the third column also contains the same test statistic but calculated using the logs of first differences of the house price series. In both cases, under the null hypothesis, the distribution of the house price series is symmetric around the unknown median against the alternative of asymmetry. Therefore, failure to reject the null hypothesis implies symmetry.

The asymptotic reference distribution of the test is a standard normal random variable. Note that prior to calculate the test statistics the Christiano and Fitzgerald (2003) filterFootnote 2 has been used to filter the series of house prices taken in natural logs.

From Table 2 it appears that all the cities under consideration feature asymmetric housing price cycles, but they have different characteristics. Most cities in the United States features deep and steep cycles, as in both cases the test statistics reject the null hypothesis. As for the Asian cities, Singapore and Seoul feature a deep cycle as the null hypothesis is rejected when the test statistic is calculated using house price changes. In these two cities troughs are deeper than peaks are high, as indicated by the calculated value of the statistic for the series in levels which have negative signs. The city of Tokyo features a deep but not steep cycle, whereas the city of Hong Kong presents a steep cycle with expansions that are longer than contraction phases.

House price cycle in Sydney presents deep and steep cycles with cyclical peaks that are higher than troughs are deep and peaks that are approached more slowly than troughs. Finally, both Paris and Vienna present house prices with asymmetric cycles. For Paris, however, the null hypothesis of steepness is rejected, and the opposite is the case for Vienna.

Modelling House Price Cycles

The Econometric Model

Let yt be a realization of a the house price changes (i.e. yt = Δyt) observed at t = 1 − p,1 − (p − 1),..,− 1,0,1, T − 1, T. Then, the univariate process \(\{y_{t}\}_{t}^{T}\) can be specified using the following model

In Eqs. 1–2 the vectors \(z_{t}=(1,y_{t-1},\dots ,y_{t-p})^{\prime }, \phi =(\phi _{0},\phi _{1} ,\dots ,\phi _{p})^{\prime }, \theta =(\theta _{0},\theta _{1},\dots ,\theta _{p})^{\prime }\) are parameter vectors. The process \(\{\epsilon _{t}\}_{t}^{T} \) in \(\left (1\right ) \) is assumed to be a martingale difference sequence with respect to the history of the time series up to time t − 1, denoted as Ωt− 1 = [y1−(p−a), yt−p], with E[𝜖t|Ωt− 1] = 0 and \(E[{\epsilon _{t}^{2}}|{\Omega }_{t-1}]=\sigma ^{2} \).The expression \(G(\tilde {\gamma },h(c_{k},s_{t}))\) defines the transition function, which is assumed to be continuously differentiable with respect to the scale parameters \(\tilde {\gamma }\in \left (\gamma _{1} ,\gamma _{2}\right ) \) and bounded between 0 and 1. Also, \(G(\tilde {\gamma },h(c_{k},s_{t}))\) is continuous in the function h(ck, st) and h(ck, st) is strictly increasing in the transition variable st. The transition variable st is assumed to be a lagged endogenous variable, that is, st = yt−d for a certain integer d > 0. The parameters ck ∈{1,2} are the location parameters. Defining \(\eta _{t}=\left (s_{t}-c\right ) \) in Eq. 2 we have

for ηt ≥ 0 (μ > 1/2) and

for ηt < 0 (μ < 1/2).

Asymmetric behavior in house price dynamics is introduced in the model by Eqs. 3-4. In particular, Eq. 3 models the higher tail of the probability function, whereas Eq. 4 models the lower tail of the probability function. The speed of the transition between the expansion and contraction regimes in the housing markets is controlled by the slope parameters \(\tilde {\gamma }\). If the vector \(\tilde {\gamma }>0,\) the function h(ηk, t) is an exponential rescaling that increases more quickly than a standard logistic function. On the other hand, if \(\tilde {\gamma }<0\), the function h(ηk, t) is a logarithmic rescaling that increases more slowly than a standard logistic function.

Different choices of the transition function \(G(\tilde {\gamma },h(c_{k} ,s_{t}))\) give rise to different types of regime-switching behaviour. If k = 1 in Eq. 2 the parameters on the right hand side of Eq. 1 change monotonically as a function of st from ϕ to ϕ + 𝜃 and the corresponding transition function is given by

with h(η1, t) given in Eqs. 3–4 and \(I\left (\cdot \right ) \) is an indicator function.

The GSTAR nests several well known linear and non-linear models. Before considering the estimation procedure of the GSTAR it is of interest at this point to relate the proposed model to other models available in the literature.

First, the model in \(\left (1\right ) \) with γ1 = γ2 = γ in the transition function in Eqs. 3–4 implies that the GSTAR model reduces to a one-parameter symmetric logistic STAR model (see Teräsvirta 1994). However, with respect to the STAR model a clear advantage of the indicator functions in Eqs. 3–4 is that slope parameters are not constrained. Positiveness of the slope parameter is an identifying condition which was a crucial assumption in Teräsvirta (1994). Second, the transition function in the GSTAR nests an indicator function \(I_{(s_{t}>c)}\) when \(\tilde {\gamma }\rightarrow +\infty \). Therefore, the GSTAR reduces to the model in Tong (1983) when \(\tilde {\gamma }\rightarrow +\infty \) and it becomes a straight line around 1/2 for each st when \(\tilde {\gamma }\rightarrow -\infty \). Finally, the GSTAR model nests a linear AR model when \(\tilde {\gamma }\) is a null vector.

As far as the estimation of the GSTAR model is concerned, estimation is performed by concentrating the sum of square residuals function with respect to the vectors 𝜃 and ϕ, that is minimizing:

where

and

As noticed in Zanetti Chini (2018), if all the nonlinear parameters are known and fixed, the GSTAR model is linear in 𝜃 and ϕ. Therefore, the estimation reduces to a minimization problem on three parameters, and it is solved via a grid search over γ1, γ2 and c. Without this simplification, one should adopt a nonlinear least square minimization of a likelihood function, that is computationally more demanding and often leading to an inappropriate corner solution.

In our illustrations, both γ1 and γ2 are chosen between a minimum value of \(\gamma _{\min \limits }=-10\) and a maximum of \(\gamma _{\max \limits }=10\) with rate 0.25. The grid for the parameter c is the set the values computed for the range of the 10th and 90th percentile of st with the increase rate computed as the difference of the two percentiles at the boundary divided by an arbitrarily high number (in our estimation 400). The initial values were set according to the following rule: \(\lambda _{0}=\left (\frac {\left \vert x^{\max \limits }-x^{\min \limits }\right \vert }{med\left [ grid\left (\lambda \right ) \right ] }\right ) \), were the denominator is the median of the set of values constituting the grid for parameter \(\lambda =\left [ \gamma _{1},\gamma _{2},c\right ] \). The software used to estimate the model was MATLAB R2012b.

Before the estimated GSTAR model can be accepted as adequate, it should be subjected to misspefication tests. Some important hypotheses which should be tested are: i) the hypothesis that there is no residual correlation, ii) the hypothesis that there is no remaining nonlinearity and iii) the hypothesis of parameter constancy (See Canepa and Zanetti Chini 2016 for more details).

Estimation Results

The adopted modelling procedure, firstly, involves determining the dynamic structure of the series of house price growth. In our case, for each house price series, the maximal lag order of the AR(p) model has been chosen by using the Bayesian information criterion and the Portmanteau test for serial correlation. Then, the second step prior to beginning the estimation procedure is to test if the data support the hypothesis of nonlinearity. A natural way of doing it is to perform a test of linearity and check if the model in Eq. 5 reduces to a linear autoregressive model. This can be done by using LM principle. However, the distribution of such test would not be identified under the null hypothesis since the parameters \(\tilde {\gamma }\) and c in Eq. 5 are not identified under the null hypothesis. The identification problem can be solved by using a Taylor series approximation to reparametrise the transition function in Eq. 5.

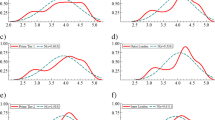

Table 3 reports the result of the linearity test, the estimated parameters and the misspecification tests. On the basis of the empirical p -values reported in the top panel of Table 3 the null hypothesis of nonlinearity can be rejected for all cities at 5% or 10% significance level, thus confirming our conjecture that a nonlinear specification needs to be used to model the house price series at hand.

With respect to the transition function from Eqs. 3–Eq. 4 it is clear that the choice of the number of location parameters k affects the type of asymmetric behavior characterized by the model. The nature of the asymmetry observed in Section “Data and Asymmetry Tests” indicates prolonged upswings in the housing markets to pronounced cyclical peaks along with sharper contractionary periods. Evidence of asymmetry in Table 2 therefore points toward the GSTAR model which can be estimated using the expression in Eq. 5 with k = 1. On the other hand, choosing k = 2 in Eq. 5, would result in an exponential form of the transition function suitable to model a symmetric cycle where contraction and recovery phases have similar dynamics.

In the middle panel of Table 3 the estimated parameters and the relative standard errors are reported. From Table 3 it appears that house price changes are persistent since most of the estimated coefficients, ϕi and 𝜃i (for i = 1,...,3), are significantly different from zero. This result is consistent with the findings in Capozza et al. (2004) where evidence of backward-looking expectations in the housing market is found (see also Dusansky and Koc 2007).

The estimated parameters γ1 and γ2 indicate the speed of the transition between expansion and contraction regimes, respectively. These coefficients are also significantly different from zero. With regard to the signs of these coefficients it is observed that the parameter γ1 is negative in most cases, whereas γ2 is in most cases positive. This indicates that the speed of the transition from one regime to the other regime increases during periods of house price busts at a rate that is greater than one which would be consistent with a standard logistic curve, but increases during the periods of house price expansions at a rate which is slower than one that would be consistent with a standard logistic function. From Table 3 it appears that the estimated parameters \(\left \vert \gamma _{1}\right \vert >\left \vert \gamma _{2}\right \vert \) in the case of San Francisco, Los Angeles, Sydney, Singapore, Seoul, Tokyo, and Paris, whereas the opposite is true for New York and Chicago. Therefore, the former group of metropolises features a strong deep and mildly steep cycle. On the other hand, the housing markets in New York City and Chicago present more the feature of a cycle which is strongly steep and moderately deep. Finally, considering Hong Kong and Vienna the estimated coefficients γ2 and γ1, respectively, are not statistically significant, thus indicating that steepness is a predominant feature of the housing market cycle in these metropolises. Note that the relatively small estimates of γ1 and γ2 indicate that other types of nonlinear models in the class of regime switching, such as the Markov switching or the TAR models, are no suitable to capture housing market dynamics since these models assume a sudden transition between one regime and the other (i.e. in these models \(\gamma _{1}=\gamma _{2}\longrightarrow \infty \) by assumption). Coming now to the parameter c, this indicates the halfway point between the expansion and contraction phases of the housing markets. In all cases, the estimated parameters c are statistically significant at the 5% level. Another significant finding is that the estimated location parameters c show the different level of sensitivity to the magnitude of exogenous shocks. Singapore, Hong Kong, San Francisco, Los Angeles, and Chicago are more sensitive to market shocks than other metropolises.

Once that the model has been estimated, the goodness of fit can be evaluated using the misspecification tests. The diagnostic statistics considered here are: i) the LM test and the F-test for the hypotheses that there is no serial correlation against the forth order autoregression (for q = 4), ii) the LM test the hypothesis that there is no remaining asymmetry, iii) the LM test for parameter constancy. The p-values of the tests are reported in the bottom panel of Table 3. Looking at the results of the misspecification tests it emerges that both tests do not reject the null hypotheses of no autocorrelation against q-order autoregression for all estimated models. There is also no evidence of remaining asymmetry given that the LM test does not reject the null hypothesis for the estimated models. Similarly, the LM test of parameter constancy also does not reject the null hypothesis at the 5% significant level for all the estimated models. Overall, the results in Table 3 suggest that the estimated models do not suffer from misspecification problems.

Forecasting House Prices

Consider the case where yt is described by the model in Eq. 1, that is,

where is given by \(F\left (z_{t};{\Omega }_{t}\right ) =\phi ^{\prime } z_{t}+\theta ^{\prime }z_{t}G(\gamma ,h(c_{k},s_{t}))\).

Let \(y_{t+h|t}^{f}=E[y_{t+h}|\mathcal {I}_{t}]\) the optimal point forecast of y|t+h made a t on the base of the past information \(\mathcal {I}_{t}\) up until that time. Based on Eq. 7, the one step-ahead forecast for yt+ 1 is given by

where \(z_{t+1}^{f}=(1,y_{t}+\epsilon _{t},y_{t-1,}\dots ,y_{t-(p-1)})^{\prime }\). Similarly, for the two step-ahead forecast period we have

where \(z_{t+2}^{f}=(1,y_{t+1}+\epsilon _{t+1},y_{t,}{\dots } ,y_{t-(p-2)})^{\prime }\). The exact expression for Eq. 8 is

where \({\Phi }\left (\omega \right ) \) is the cumulate density function of 𝜖t+ 1. Note that if in Eqs. 3–4 the vector \(\tilde {\gamma }\) is a null vector, then the h-step-ahead forecast can be obtained recursively in a manner similar to Eq. 8. This the so called “skeleton extrapolation” approach, that in the case of nonlinear models would yield biased forecasts (see for example Granger and Terasvirta 1993). For the GSTAR model when the forecast horizon increases, the multi-step ahead forecast is not available in closed form, but it could be computed by numerical integration. If Eq. 9 is solved by numerical integration for the model in Eq. 1 with p = 1 and d = 1 the two-steps ahead forecast is given by

where

for h(c, ω) > 1/2 and

for h(c1, ω) < 1/2. Solving the integral in Eq. 10 is relatively easy, however an exact expression for \(E[y_{t+h}|\mathcal {I}_{t}]\) would involve solving an h − 1 dimensional integral which is rather time consuming. A less cumbersome approach to obtain a multi-step ahead house price forecast is by using the bootstrap method to find an numerical approximation of \(y_{t+h|t}^{f}\). Non parametric bootstrap procedures to forecast time series in non-linear models were successfully used in Lundbergh and Terasvirta (2004). Given that the STAR-type models considered in Lundbergh and Terasvirta (2004) are nested in the GSTAR model considered in this work below we follow these authors and generate the h-steps ahead forecast of house price change series by using a block bootstrap procedure to generate the empirical analogue of \(y_{t+h|t}^{f},\) say \(\widetilde {y}_{t+h|t}^{f}\).

Below we use the parameters obtained estimating the GSTAR model to calculate the out-of-sample density forecasts and consider whether the forecasts generated by the GSTAR outperform those obtained estimating a simple linear AR(p) model. To avoid cluttering, the estimation results for the AR(p) model are reported in Appendix. The out-of-sample forecast comparisons do not rely on a single criterion, for robustness we compare the results of four density forecast performance measure. Namely, we use the logarithmic score (LogS), the quadratic score (QSR), the continuous-ranked probability score (CRPS), and the quantile score (qS).

Table 4 reports the results of the h-step-ahead forecasts for the forecast period h = {1,3,6,12}. In columns 2 and 3 the forecasting horizon and the forecast error measures are reported, respectively, whereas in columns 4-7 the forecasting results for each housing market are reported. From Table 4 it is clear that according to the QSR and the CRPS performance measures the GSTAR model performs better than it’s linear counterpart for most cities, especially for medium and long run horizons. However, the results according to the LogS and the qS performance measures are mixed.

Robustness Checks

In Section “Testing for Asymmetries in the Housing Market Cycles”, the GSTAR model has detected widespread evidence of asymmetric adjustment in the cities under consideration. The nature of the asymmetry observed indicated prolonged upswings in the market rising to pronounced cyclical peaks along with sharper recessionary or contractionary periods. This result is in accordance with economic theory, where it is shown that the inertia of supply resulting from construction lags in combination with backward-looking expectations generate asymmetric cycles (see, for example, Glaeser and Gyourko 2018; Case and Shiller1989). In metropolises, high real construction costs such as land cost and stricter regulations on new developments introduce unpriced supply restrictions. In this respect, our results support the model proposed by Capozza et al. (2004), wherein it is postulated that a higher real income, a higher level of real construction costs and strict regulation increase asymmetries in the housing market cycles. In an influential paper, Gyourko et al. (2013) provide evidence that house prices and income growth are related. The author labels as ‘superstar cities’ those metropolitan areas where: i) demand exceeds supply and ii) supply growth is limited. A crucial characteristic for a city to be classified as a superstar is that residents are willing to pay a premium to live there and in which the proportion of high-income households is relatively high. In places that are desirable, but have low construction rates, households with high incomes or strong preferences for that location outbid lower income families for scarce housing and drive up the price of the underlying land. By contrast, in locations where housing supply is not constrained, households can buy at construction costs so that instead of growth in house prices, the areas exhibit growth in house supply. According to the theoretical framework suggested by Gyourko et al. (2013), the clearing process continues as long as the growth in the income-weighted demand for a location exceeds the addition in supply, either in the original location or in a close substitute. In addition to attracting highly skilled workers, global cities also attract inflows of foreign capital due to increasing financial market liberalisation that the world has witnessed in recent years. According to Favilukis et al. (2013) (see also Badarinza and Ramadorai 2018) many countries that saw large housing booms and busts attracted foreign capital and much of this capital was invested in the property market thank to mortgage credit extension.

Against this background, a natural question is, are the characteristic features of house prices cycles in global cities different from less dynamic urban centres? As a robustness check, we consider house prices in metropolitan areas in the United States which have lower price-to-income as compared to the global cities considered in this paper and investigate the characteristic features of house price cycles in these metropolitan areas. If the hypotheses in Gyourko et al. (2013) and Favilukis et al. (2013) hold true, we should expect house prices in these metropolitan areas to be linear and feature more symmetric cycles.

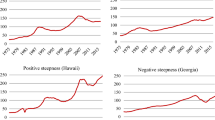

With this target in mind, quarterly data at the metropolitan statistical area (MSA) level from 1975: Q1 to 2019: Q1 were collected from the Federal Housing Finance Agency. The data collected included the 100 largest MSAs in the United States.Footnote 3 Of these MSAs, those with the lowest house prices growth were selected. To classify the MSAs according to their level of house price inflation during the period under consideration, the average price growth in each MSA was calculated and the MSAs were ranked from the least to the most expensive locations by considering the quantile distribution of the average price growth. The final subsample included the 10 MSAs that were classified in the lowest 10st percentile of the house price inflation distribution.

To investigate the characteristic features of the housing market in these metropolitan areas nonlinearity and asymmetry tests were calculated. Table 5 reports the two test statistics for each MSA. In Table 5 the MSAs are ordered according to the lowest percentile, so that in the MSA of Dayton-Kettering in Ohio was ranked in the 1st percentile.

Looking at the results in Table 5, it appears that for most of the MSAs considered the linearity test does not reject the null hypothesis of linearity, which suggests that the house price series are not suitable to be modelled using highly nonlinear models such as the GSTAR. Only for three out of ten MSAs, the test suggests that housing market series are nonlinear at 10% significance level. This is in sharp contrast with the results in Table 3 where the linearity test rejects the null hypothesis for all global cities in the same country. Similarly, the Triples test suggests that there is no asymmetry in the housing market cycles in all but three MSAs in which some steepness is detected. Overall, the results in Table 5 suggest that less dynamic metropolitan areas have different house price dynamics than the global cities.

Discussion

Before concluding this section a question is in order: What do we learn from the GSTAR model about housing market dynamics in world cities? Looking at the results shown in Table 3, it is clear that the type of logistic transition function commonly adopted in STAR models may be suitable to estimate house price dynamic at higher level of aggregation (e.g. country or regional level), but may not be the best specification to capture asymmetric oscillations from the conditional mean of house price in global cities. This is because house prices in these metropolises are subject to strong exogenous shocks that make the stochastic processes highly nonlinear. Being the sigmoid in the transition equation a logistic function the LSTAR is model reflexively symmetric. Hence, the resulting model may be able to reproduce steepness but not deepness which we found to be an important feature of the data at hand. In this respect, using a class of models indexed by two shape parameters that influence the symmetry and heaviness of the tails of the fitted transition equation may be more suitable to fit the non-central regions of the probability function and therefore better capture the asymmetries found in the previous section.

In the business cycle literature, which is closely related to the application in this paper, asymmetric behaviour over the business cycle has long been an object of interest in applied and theoretical works. Asymmetric behaviour has been observed in many macroeconomic series. Therefore, it is not surprising that several variations of the STAR model have been suggested in the literature. For example, Sollis et al. (1999) suggest raising the transition function of the STAR to an exponential. Alternatively, Sollis et al. (2002) propose to add a parameter inside the transition function in order to control the asymmetry of both tails of the transition function. The suggested procedures successfully address the issue of dynamic asymmetry in several classical macroeconomic series. However, Zanetti Chini (2018) shows that neither of these solutions is free from challenges: in the Sollis et al. (2002) model, the transition function can be non-smooth; whereas the Sollis et al. (1999) parametrisation conveys a smooth transition, but the ensuing increase in the asymmetry parameter often translates to no more than a shift effect in the same transition function if it is not properly restricted. This shift could translate into an almost symmetric predictive density. On the other hand, the logarithmic (exponential) rescaling of the GSTAR model preserves the smoothness of the transition function by construction. No restrictions are required for model identification and estimation. Therefore, the specification allows us to model the two states (or possibly more, if multiple transition functions are required) in the density function of the process.

The results in Table 4 show that the GSTAR model has good forecasting properties. This is an important result since the financial stability policy requires action before the market overheating goes too far and requires financial authorities’ intervention to stabilise the market. It is well known that house price adjustments can signal impending adjustments in macroeconomic fundamentals (see Iacoviello and Neri 2010). World cities are more exposed to business cycle movements and may pick up early signals of economic turmoil. In this respect, reliable forecasting of house price movements plays a crucial role in informing financial authorities responsible for maintaining stable markets.

Conclusion

This paper investigates potential asymmetrical adjustment of house prices in cities which rank high on the Global Power City Index (2018). The index evaluates major cities in the world according to their comprehensive power to attract people, capital, and enterprises from around the world. Global cities play a crucial role in supporting global finance, trade and enhancing knowledge transfer. A peculiarity of world cities’ real estate markets is that house price dynamics are driven by local and global investment demand, which often makes homes rather unaffordable for the average local income earners. Strong pressure on the demand side and inelastic supply make these cities vulnerable to housing market bubbles. It is probably not a coincidence that most of the metropolises under consideration in this paper also score highly in the UBS Global Real Estate Bubble Index (see UBS Global Real Estate 2018), which estimates the probability of a bubble bursting in a given metropolis at a given point in time.

To model house price dynamics we use a generalized logistic function which is able to parametrize the asymmetry in the transition equation of house price series, thus capturing the dynamic asymmetry in the conditional mean of house price series. Our findings reveal several insights into the patterns of the housing markets under consideration. In particular, the results obtained show extensive evidence of asymmetry to exist with deep and steep housing cycles frequently detected. This asymmetry has important implications. First, observing a deep cycle implies that the housing market may overheat during expansion phases with high peaks in house prices being observed or may struggle with severe housing market busts which would trigger financial instability in the economic system. Therefore, the knowledge of the characteristic features of the cycle may forewarn the economic policymakers to formulate policy to stabilise the housing market to preserve the economic stability in the country. Second, given that dynamic asymmetry prevails in the housing markets in all the cities under consideration, econometric models that tend to be symmetrical in nature fail to capture fundamental features of the data with important consequences for the reliability of the estimated parameters. Third, literature has extensively reported on the ripple effect that the house price dynamics in major metropolitan areas causes in the neighbouring areas (see, for example, Cook and Holly 2000 and the references therein). Therefore, the ability to forecast the movements in the housing markets of large cities may prove crucial for the policymakers and their willingness to ‘lean against the wind’. Finally, empirical evidence that suggests that housing markets feature deep and steep cycles may support the construction of theoretical models capable of explaining why this empirical evidence is so persistent.

Notes

Note the city of London was at the top of the GPCI index in 2018. However, an extensive investigation on housing market cycles in London is considered in Canepa and Zanetti Chini (2019). Note also that the GPCI index is published yearly, therefore the ranking of the cities changes over time. However, the cities under consideration have been ranking in the top twenty for at least the last five years.

Note that in their original work Randles et al. (1980) use the filter suggested in Hodrick and Prescott (1997) to filter the series prior to testing for asymmetry. However, Hamilton (2018) shows that this filter has several limitations and introduces spurious dynamic relations that have no basis in the underlying data-generating process. For this reason the filter in Christiano and Fitzgerald (2003) has been used in this work.

Note that according to the United States Office of Management and Budget an MSA has an urbanized core of minimally 50,000 population and includes outlying areas determined by commuting measures.

References

Abelson, P., Joyeux, R., Milunovich, G., Chung, D. (2005). Explaining house prices in Australia: 1970 to 2003. Economic Record, 81, 96–103.

Alqaralleh, H., & Canepa, A. (2019). Dynamic asymmetries of housing market cycles in large urban areas EST Working Papers 03/19. Italy: University of Turin.

Abrahm, J.M., & Hendershott, P.M. (1993). Patterns and Determinants of Metropolitan House Prices, 1977-91. In Browne, & Rosengren (Eds.) Proceedings of the 25th Annual Boston Fed Conference. Real Estate and the Credit Crunch, (Vol. 18 p. 56). Boston.

Abraham, J., & Hendershott, P. (1996). Bubbles in metropolitan housing markets. Journal of Housing Research, 7, 191–207.

André, C. (2010). A bird’s eye view of OECD housing markets. OECD Economics Department Working Paper No. 746.

André, C. (2015). Housing cycles: stylised facts and policy challenges. In: Proceedings of OENB Workshops No 19. Oesterreichische Nationalbank, Vienna.

Balcilar, M, Gupta, R., Miller, S.M. (2015). The out-of-sample forecasting performance of non-linear models of regional housing prices in the U.S. Applied Economics, 47, 2259–2277.

Bao, T., Hommes, C.H., Makarewicz, T.A. (2017). Bubble formation and (In)efficient markets in learning-to-forecast and optimize experiments. Economic Journal, 127, 581–609.

Badarinza, C., & Ramadorai, T. (2018). Home away from home? Foreign demand and London house prices. Journal of Financial Economics, 130, 532–555.

Bernanke, B., Gertler, M., Gilchrist, S. (1996). The financial accelerator and the flight to quality. Review of Economics and Statistics, 78, 1–15.

Blatt, J.M. (1980). On the Frisch model of business cycles. Oxford Economic Papers, 32, 467–79.

Bolt, W., Demertzis, D., Diks, C.G.H., Van der Leij, M.J. (2014). Identifying booms and busts in house prices under heterogeneous expectations CeNDEF Working Papers 14-13. Universiteit van Amsterdam: Center for Nonlinear Dynamics in Economics and Finance.

Borio, C. (2014). The financial cycle and macroeconomics: what have we learnt?. Journal of Banking and Finance, 45, 182–98.

Cabrera, J.F., Wang, T., Yang, J. (2011). Linear and nonlinear predictability of international securitized real estate returns: a reality check. Journal of Real Estate Research, 33, 565–594.

Canepa, A., & Zanetti Chini, E. (2016). Dynamic asymmetries in house price cycles: a generalized smooth transition model. Journal of Empirical Finance, 37, 91–103.

Canepa, A., & Zanetti Chini, E. (2019). Housing market cycles in London. ESTWorking Papers, University of Turin.

Chan, K., & Tong, H. (1986). On estimating thresholds in autoregressive models. Journal of Time Series Analysis, 7, 178–190.

Capozza, D.R., & Seguin, P.J. (1996). Expectations, efficiency, and euphoria in the housing market. Regional Science and Urban Economics, 26, 369–386.

Capozza, D.R., Hendershott, P.H., Mack, C. (2004). An anatomy of price dynamics in illiquid markets: analysis and evidence from local housing markets. Real Estate Economics, 32, 1–32.

Christiano, L.J., & Fitzgerald, T.J. (2003). The band pass filter. International Economic Review, 44, 435–465.

Clapp, J.M., Dolde, W., Tirtiroglu, D. (1995). Imperfect information and investor inferences from housing price dynamics. Real Estate Economics, 23, 239–270.

Case, K.E., & Shiller, R.J. (1989). The efficiency of the market for single-family homes. American Economic Review, 79, 125–37.

Case, K.E., & Shiller, R.J. (2003). Is there a bubble in the housing market? Brookings Papers on Economic Activity, 2, 299–362.

Cook, S. (2006). A non-parametric examination of asymmetrical behaviour in the UK housing market. Urban Studies, 11, 2067–2074.

Cook, S., & Watson, D. (2017). Asymmetric price adjustment in the London housing market: a disaggregated analysis. Research Journal of Economics, 1, 1–7.

Cook, S., & Holly, S. (2000). Statistical properties of UK house prices: an analysis of disaggregated vintages. Urban Studies, 37, 2045–2055.

Crawford, G., & Fratantoni, M. (2003). Assessing the forecasting performance of regime-switching, ARIMA and GARCH models of house prices. Real Estate Economics, 31, 223–243.

Cutler, D.M., Poterba, J.M., Summers, L.H. (1991). Speculative dynamics. Review of Economic Studies, 58, 529–546.

Davis, P.E., & Zhu, A. (2005). Commercial Property Prices and Bank Performance. BIS Working Paper n. 175.

Dusansky, R., & Koç, .̧C. (2007). The capital gains effect in the demand for housing. Journal of Urban Economics, 61, 287–298.

Eubank, R.L., LaRiccia, V.N., Rosenstein, R.B. (1992). Testing symmetry about an unknown median via linear rank procedures. Nonparametric Statistics, 1, 301–311.

Favilukis, J., Kohn, D., Ludvigson, S.C., Van Nieuwerburgh, S. (2013). International capital flows and house prices: theory and evidence, chapter in NBER book: housing and the financial crisis. In Glaeser, E.L., & Sinai, T. (Eds.)

Glaeser, E.L., Gyourko, J., Saiz, A. (2008). Housing supply and housing bubbles. Journal of Urban Economics, 64, 198–217.

Glaeser, E.L., & Nathanson, C.G. (2015). Housing bubbles. Handbook of Regional and Urban Economics, 5, 701–751.

Glaeser, E.L., & Gyourko, J. (2018). The economic implications of housing supply. The Journal of Economic Perspectives, 32, 3–30.

Global Power City Index Yearbook 2018. (2018). MMF institutes for urban strategies. The Mori Memorial Foundation.

Granger, C.W.J., & Terasvirta, T. (1993). Modelling Nonlinear Economic Relationships. Oxford: Oxford University Press.

Gyourko, J., Mayer, C., Sinai, T. (2013). Superstar cities. American Economic Journal, 5, 167–99.

Hamilton, J.D. (2018). Why you should never use the Hodrick-Prescott filter? Review of Economics and Statistics, 100, 831–843.

Hirshleifer, D.A., Hsu, P.H., Li, D. (2013). Innovative efficiency and stock returns. Journal of Financial Economics, 107, 632–54.

Hodrick, R.J., & Prescott, E.C. (1997). Postwar U.S. business cycles: an empirical investigation. Journal of Money, Credit, and Banking, 29, 1–16.

Holly, S., & Jones, N. (1997). House prices since the 1940s: cointegration, demography and asymmetries. Economic Modelling, 14, 549–565.

Kim, S., & Bhattacharya, R. (2009). Regional housing prices in the USA: an empirical investigation of nonlinearity. Journal of Real Estate Finance and Economics, 38, 443–460.

Kiyotaki, N., & Moore, J. (1997). Credit cycles. Journal of Political Economy, 105, 211–248.

Kumar, A. (2009). Hard-to-value stocks, behavioral biases, and informed trading. Journal of Financial and Quantitative Analysis, 44, 1375–1401.

Iacoviello, M., & Neri, S. (2010). Housing market spillovers: evidence from an estimated DSGE model. American Economic Journal: Macroeconomics, 2, 25–64.

Lundbergh, S., & Terasvirta, T. (2004). Forecasting with smooth transition autoregressive models. In Clements, M.P., & Hendry, D.F. (Eds.) A companion to economic forecasting: Blackwell Publishing.

Mayer, C.J., & Somerville, C.T. (2000). Residential construction: using the urban growth model to estimate housing supply. Journal of Urban Economics, 48, 85–109.

Malpezzi, S. (1999). A simple error correction model of housing prices. Journal of Housing Economics, 8, 27–62.

Meen, G. (2002). The time-series behavior of house prices: a transatlantic divide? Journal of Housing Economics, 11, 1–23.

Miles, W. (2008). Boom-bust cycles and the forecasting performance of linear and nonlinear models of house prices. Journal of Real Estate Finance and Economics, 36, 249–264.

Muellbauer, J., & Murphy, A. (1997). Booms and busts in the U.K. housing market. Economic Journal, 107, 1701–1727.

Randles, R.H., Fligner, M.A., Policello, G.E., Wolfe, D.A. (1980). An asymptotically distribution-free test for symmetry versus asymmetry. Journal of the American Statistical Association, 75, 168–172.

Saiz, A. (2010). The geographic determinants of housing supply. Quarterly Journal of Economics, 125, 1253–96.

Sassen, S. (2003) In Borsdorf, A, & Parnreiter, C (Eds.), The global city: strategic site/new frontier. Wien: Verlag der Österreichischen Akademie der Wissenschaften.

Seslen, T.N. (2004). Housing Price dynamics and household mobility decisions. USC LUSK/FBE Real Estate Seminar, 9, 1–42.

Sichel, D. (1993). Business cycle asymmetry: a deeper look. Economic Inquiry, 31, 224–236.

Sollis, R., Leybourne, S., Newbold, P. (1999). Unit roots and asymmetric smooth transitions. Journal of Time Series Analysis, 20, 671–677.

Sollis, R., Leybourne, S., Newbold, P. (2002). Tests for symmetric and asymmetric nonlinear mean reversion in real exchange rates. Journal of Money, Credit and Banking, 34, 686–700.

Teräsvirta, T. (1994). Specification, estimation and evaluation of smooth transition autoregressive models. Journal of the American Statistical Association, 89, 208–218.

Tong, H. (1983). Threshold Models in Non-Linear Time Series Analysis. No 21 in Lecture Notes in Statistics. New York: Springer.

Shiller, R. (1990). Market volatility and investor behavior. The American Economic Review, 80, 58–62.

UBS UBS Global Real Estate Bubble Index. (2018). UBS Group AG, Zuric.

Zanetti Chini, E. (2018). Forecasting dynamically asymmetric fluctuations of the U.S. business cycle. International Journal of Forecasting, 34, 711–732.

Acknowledgements

The authors appreciate comments and suggestions from two anonymous referees. We also thank Rickard Sandberg, Jan G. de Gooijer, Yongmiao Hong, Takashi Yamagata for their useful comments. Thorough and insightful remarks from the participants of the 10th Nordic Econometrics Meeting (May 2019, Stockholm, Sweden) and the Asian Meeting of the Econometric Society (June 2019, Xiamen, China) are also gratefully acknowledged.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher’s Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Appendix

Appendix

Rights and permissions

About this article

Cite this article

Canepa, A., Chini, E.Z. & Alqaralleh, H. Global Cities and Local Housing Market Cycles. J Real Estate Finan Econ 61, 671–697 (2020). https://doi.org/10.1007/s11146-019-09734-8

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-019-09734-8