Abstract

This study investigates how information asymmetry affects the rent and vacancy rate adjust in response to external shocks using empirical data from the Hong Kong office market. We show that information asymmetry about the quality of real estate asset will lead to slower rent adjustments in response to external shocks. Information asymmetry makes it more difficult for the landlord and prospective tenant to agree on a new equilibrium rent, which also leads to temporary deviation of the vacancy rate form the natural vacancy rate. Compared to a low-end office unit, information asymmetry is less serious for a high-end office unit since a larger proportion of its rental value is derived from its location attributes which are easily observable by both the landlord and prospective tenant. One empirical implication is that high-end office rents adjust faster when there is a short-term disequilibrium. The other side of the coin is that the vacancy rates of high-end offices are less responsive to external shocks assuming that the natural vacancy rates are relatively stable over time. Empirical data from the Hong Kong office sub-markets are consistent with these implications.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

There is voluminous literature on the relationship between rents and vacancy rates in the real estate market ever since the work by Blank and Winnick (1953). They developed a theoretical model to explain vacancy rates and rents within some critical or normal zone of occupancy (i.e., above a certain level of vacancy rate since the rent-vacancy rate relationship will not hold as vacancy rate approaches zero) in the housing market. The main idea behind their model is frictional responses in the rental housing market, which can be extended to the non-residential real estate markets. Frictional responses arising from high trading and search costs, slow supply responses, credit market imperfections and the existence of long-term contracts may impede spontaneous adjustment of rents to clear the market (Rosen and Smith 1983). The real estate market is a heterogeneous goods market with high information cost. A transaction is the outcome of a search and matching process which is not purely dependent on the landlord’s asking rent but also on the time required to find a willing tenant. Therefore, it is often optimal for the landlord to ask a rent slightly higher than the rent that will minimize the time required for match and search (time on the market) during which the property is vacant (Wheaton and Torto 1988). When there is a positive external shock,Footnote 1 the search and match process is shortened and vacancy rate declines to a level lower than the optimal level, which also serves as a short run signal for landlords to increase their asking rents.

All these imply that rent may not adjust fully in the short run in response to external shock. There have been numerous empirical tests on the dynamics of vacancy and rent using residential (e.g., Eubank and Sirmans 1979; Rosen and Smith 1983) and non-residential market data (e.g., Shilling et al. 1987; Wheaton and Torto 1988; Hendershott 1996; Hendershott et al. 2002a, b and 2010; Englund et al. 2008; Brounen and Jennen 2009a; Ibanez and Pennington-Cross 2013; Adams and Füss 2012). However, very little attention has been paid to the causes of rent stickiness. Following previous analysis, rent stickiness is due to transaction costs. Transaction cost here is defined in the broadest sense that includes not just monetary costs paid to complete a transaction (trading cost) such as agent’s fee, legal charges and taxes, but also all costs of resources required to complete a transaction such as information cost, contract enforcement cost and the cost of measurement. This broad concept of transaction cost originated from Coase (1937), although did not use the term transaction cost but referred to them as the cost of using the price mechanism. Cheung (1998) defined transaction costs as “all the costs which do not exist in a Robinson Crusoe economy”. Thus in a world of zero transaction cost, rent will adjust to a new equilibrium level instantaneously and vacancy rate will always be close to zero (when transaction cost is zero, the natural vacancy rate can only be resulted from the time required for tenants to move in and out of a property). With positive transaction costs, rent adjustment becomes sticky. There have been very few studies on how different transaction costs affect the rent and vacancy dynamics.

We propose that transaction costs resulting from information asymmetry is an important factor that affects the stickiness of office rents. Information asymmetry about the quality of real estate assets is a well-known characteristic of the real estate market. Wong et al. (2012) have shown that the volume of transaction is negatively associated with the degree of information asymmetry since information asymmetry makes it difficult for the buyers and sellers to agree on the transaction prices of a real estate asset. They have shown that information asymmetry mainly derive from the quality of the structure of the building and therefore the model that decompose property value into the land and structure components can be used to measure the degree of information asymmetry. Following the same logic, landlords and prospective tenants would have difficulty in agreeing on the rental prices of office units that have serious problems of information asymmetry. This is especially the case after an external shock since recent comparable transactions are of little use for discovering the new equilibrium price. Compared with low-end offices, high-end offices have lower degree of information asymmetry since the proportion of the value of high-end offices that is derived from land, such as location, accessibility and views, symmetrical much larger than that of low-end offices. When there is an external shock, it would be easier for the landlord and tenants of a high-end office unit to agree on a new rent and thus can restore to a new equilibrium level more quickly compared with the case of low-end office units. On the other hand, low-end offices are usually located in areas with lower land value and therefore the proportion of the value of the low-end office buildings is relatively lower compared with that of high-end offices. However, the quality of the building structure is more difficult for the prospective tenant (compared with the landlord) to observe. This is not the case for that of land component (i.e., location attributes) and thus low-end offices have a higher degree of information asymmetry compared to high-end offices. This is particularly true for high rise office buildings where the quality and conditions of units within the same building can affect each other. Information asymmetry deters the ability of low-end offices to adjust to a new equilibrium rent quickly when rent is in disequilibrium. Since rent cannot adjust quickly, vacancy rate will change (“adjust”) instead. Assuming that long term equilibrium vacancy rate (or natural vacancy rate) is relatively stable over time, the vacancy rate of low-end offices is more responsive to external shocks, ceteris paribus. This study tests the impact of information asymmetry on the adjustment of rent and vacancy rate dynamics using data from the office sub-markets in Hong Kong. We have chosen Hong Kong for our empirical tests for three reasons. First, Hong Kong is a small place where there is a little differences in the sensitively of economic viability in difference locations to the overall economic conditions. Second, there is a substantial difference in information asymmetry between low- and high-end offices. Third, most office rental leases in Hong Kong are very homogeneous, which is a typical 2-years leases and standard conditions. This paper is organized as follows: The second section review previous studies on rent and vacancy rate dynamics. The third section presents the theoretical analysis. The forth section describes the procedures for the empirical tests. The fifth section presents the data, the sixth section discusses the results and the seventh section concludes the study.

Literature Review

In the neoclassical demand and supply framework, the rent adjusts immediately to clear the market such that the vacancy rate always equals the natural vacancy rate. Any deviation from the natural vacancy rate means excess supply or demand in the market, which is characterized by short term disequilibrium rent. When vacancy is above the natural level, excess supply will force the rent to drop, thereby restoring the balance between the space demanded and supplied. The converse is true when vacancy falls below the natural level.

Market evidence, however, reveals huge variations in vacancy rates, suggesting that the either the natural vacancy rate is highly volatile or the observed vacancy rate indeed deviates from the natural rate from time to time. According to Rosen and Smith (1983) and Shilling et al. (1987), the natural vacancy rate varied greatly across U.S. cities, ranging from 1 % to over 20 %. Wheaton and Torto (1988) found large deviations between the actual and natural vacancy rates from 1968 through 1986, even after allowing for constant growth in natural vacancy. In theory, natural vacancy rate is the long term equilibrium vacancy rate which may vary across different types of real estate assets, but should be relatively stable over time unless there is a structural change that shifts the long term equilibrium vacancy rate. Most previous studies assume that the natural vacancy rate is constant over time but relax the instantaneous market clearing assumption and explicitly model the frictional rental adjustment process.

The rental price adjustment process literature generally describes the space market as a search market where landlords have an incentive to leave their space vacant and wait for a better offer. A positive demand shock to the space market would cause vacancy to fall below the natural level, which in turn drives the rent up. Shilling et al. (1987) and Wheaton and Torto (1988) find empirical support to this adjustment process using US office market rent and vacancy rate data. Similarly, Wheaton et al. (1997) found that lagged vacancy had a negative impact on current rents in the UK office market and attributed this relationship to the use of long-term leases.

Since most time series data are non-stationary, subsequent works model supply and demand factors together in a co-integration framework. The reduced-form Error Correction Model (ECM) proposed by Hendershott et al. (2002a, b) has been widely used in empirical studies worldwide (e.g., Brounen and Jennen (2009a) in the US; and Brounen and Jennen (2009b) in Europe; De Francesco (2008) in Australia). The ECM models the short-run relationship between rents and vacancy rates as well as how fast rents return to equilibrium in the short run. Englund et al. (2008) improved the ECM by employing Seemingly Unrelated Regression (SUR) to simultaneously estimate the adjustment of rents and vacancy rates.

Review of previous empirical studies reveal that the how fast rent initially adjust to the long term equilibrium rent varies cross different type of properties. However, so far, there has been no attempt to explain the speed at which rents or vacancy rates return to the equilibrium, except for Ibanez and Pennington-Cross (2013). They found that adjustment was the slowest in office property, which takes a longer time to build and has longer-term leases than other property types in the U.S. We find that in their study, higher quality offices were also shown to adjust to equilibrium more quickly, though this was not mentioned in their paper and no explanation was provided. Our study extends their work by providing and testing an information-based explanation for the initial speed of rent adjustment, while holding the construction period and lease structure constant.

Development of Hypotheses

When there is an external shock, certain aspects of the space market will respond and adjust to a new equilibrium level. Adjustment in the form of new supply of space is generally sluggish because construction takes time. In the short run, rents – at least for newly signed leases – should, in principle, be responsible for all the adjustment. However the search and bargaining behavior of landlords and tenants gives rise to vacancy. This means both rent and vacancy rate are likely to respond to shocks simultaneously. If natural vacancy rate is relatively constant over time, faster adjustment in rent would imply that the observed vacancy rate be closer to the natural vacancy rate. With constant natural vacancy rate, the observed vacancy rate would appear to be less responsive to shocks when rent adjusts quickly. Therefore faster adjustment in rent would come along with a slower adjustment in vacancy rate, and vice versa. The question that motivates this study is: what determines the relative adjustment speed of rent and vacancy rates?

We posit that difference transaction costs are responsible variation in the speed of rent and vacancy rate adjustment. Transaction costs include typical search cost such as the cost of matching the landlords and tenants well as the broker’s fees. It also includes trading expenses such as legal fees and taxes. These search and trading costs normally do not differ considerably across real estate types. In our context, the relevant transaction cost that is responsible for the variation in the speed of rent and vacancy rate adjustment is asymmetric information about the quality of office buildings. Information asymmetry affects the process of discovery the rental price of office space. Variations in the degrees of information asymmetry across different offices lead to different speed of adjustment to a new level of equilibrium rent. The following analysis is analogues to Wong et al. (2012).

In the search and matching process, a necessary condition for a transaction to take place (a successful match) is that a tenant values the office space more than the landlord’s reservation rent. Assume that the probability of this occurring per unit time is:

where V B and V S are the private values of the product to the buyer and seller, respectively. In a world where both parties are equally informed about a product’s quality, valuation differences could still exist for such reasons as imperfect information and heterogeneous agents. These imperfections and heterogeneities make the probability of transaction greater than zero. A higher value of P means more successful matches per unit time, which implies faster adjustment of rent to a new equilibrium level (and therefore vacancy rate is always close to the natural vacancy rate) when there is an external shock.

The value of service flow from an office can be decomposed into two parts: 1) a symmetric part (i.e., land), the quality of which is observable by everybody since land value in an urban area is derived from its location, the attributes of which such accessibility, view, nearby facilities etc. are equally observable by both the landlord and prospective tenant and 2) an asymmetric part (i.e., building structure), the quality of which can be assessed more accurately by the landlord than the prospective tenant since the owner have more information about the any latent defects in the building structure. In addition, all offices in Hong Kong are multi-storey buildings. Therefore, latent defects of vertical and horizontal adjacent units, which might have a negative impact on the prospective tenant’s unit cannot be easily observed by the prospective tenant during inspection. It is also impossible to employ a professional building surveyor to carrying an inspection of the structure of the adjacent units as it is very unlikely that the tenants of the adjacent units would allow the surveyor to enter their units.

We measure the symmetric component of the office by the theoretical value land to the market value of the office (or land leverage), denoted by L% and the asymmetric component (value of building structure to the value of the office) by 1-L%. Since the building component has a higher degree of information asymmetry compared with the land component, higher land leverage, L%, implies less information asymmetry problem. But higher L% means that the office is more likely to be a high-end office located in a good location with higher land value. Therefore the probability of transactions in the high-end offices rental market is higher than that in the low-end office rental market, other thing being equal, which also implies faster adjustment in the high-end office market when rent is in disequilibrium.

Given the theoretical analysis above, we hypothesize that:

-

Hypothesis 1: Compared with low-end offices, rental levels of high-end offices are more responsive to external shocks, ceteris paribus.

Due to positive transaction cost, rent can never be fully adjusted to a new equilibrium level after an external shock. This partial or incomplete adjustment leaves a gap between supply and demand in the short run, which is reflected in changes in vacancy rate over time assuming that the long run equilibrium vacancy rate is relatively constant. Therefore in a market with relatively constant natural vacancy rate, faster (slower) adjustment in rent implies the observed vacancy rate is less (more) responsive to external shocks. Accordingly, the second hypothesis is:

-

Hypothesis 2: Compared with high-end offices, vacancy rates of low-end offices are more responsive to external shocks, ceteris paribus.

The test condition for the above two hypotheses is that high-end offices have higher land leverage than low-end offices.

Empirical Tests

The office market in Hong Kong can be divided into sub-markets, according to the grading scheme provided by Rating and Valuation Department (2012a, b): Grade A and C are correspondently high- and low- end offices. Grade A offices are usually located in CBD areas where land price is high while Grade C offices are mainly located in less prime non-CBD areas.Footnote 2 Therefore Grade A offices are likely to have higher land leverage (L%) compared with Grade C offices. Following Wong et al., the degree of information asymmetry can be measured by (1-L%), or building construction cost as a percentage property value. That is, higher land leverage implies lower degree of information asymmetry. Since Grade A offices are usually located in prime location, their land leverages are likely to be high. However, this may not be the case if the building construction costs of Grade A offices are also substantially higher those of Grade C offices. We have collected data from a building cost consultant to estimate the average land leverage of Grade A and Grade C offices over the observation period (see Table 11 in the Appendix). The degree of information asymmetry as measured by (1-L%) is consistently higher for Grade C offices. Therefore the test condition for the two hypotheses is satisfied.

The office lease usually has a short duration of 2 or 3 years at fixed rent in Hong Kong (Pretorius et al. 2003) because of the exemption of registration for lease term under 3 years (Building Ordinance Cap. 128). For some cities, e.g., London, the average office lease duration is longerFootnote 3 and can vary significantly across leases. The office lease duration in Hong Kong is much shorter and more homogeneous, compared with other cities in the world.

Clapp (1993) propose that there are three factors for the slow adjustment of office rental prices, namely long-term lease, slow supply of office space and high transaction costs. Difference in these factors will lead to different speed of rent adjustment. The first two factors are the same for all offices in Hong Kong. Therefore the main difference in the rent and vacancy dynamics between Grade A and Grade C offices in Hong Kong is mainly attributable to the difference in transaction costs, particularly those arising from different degree of information asymmetry.

Empirical Model

We adopt the approach in Englund et al. (2008) to perform the empirical test. This approach is an improved version of the empirical model by Hendershott et al. (2002a, b) which is a error correction model. In this approach, demand for office space is expressed as a Cobb-Douglas function:

where R is real effective rent for new contracts, E is office employment; λ R and λ E are the price and income elasticity respectively.

The long-run equilibrium condition is:

where S is total supply of office space, R * and v * are the long run equilibrium real effective rent and vacancy rate respectively. The latter is assumed to be constant over time.

Substituting R * for R in (2) and solving (2) and (3) for R * gives:

where γ E = − λ E /λ R , γ S = 1/λ R ,

Taking log on both sides gives the following long run equilibrium relationship:

Englund et al., propose to use empirical observations of R, E and S to estimate (5) with the error term representing the short term deviation of actual effective rent, R, from the long-run equilibrium rent, R *, i.e.,

where ε t is the error term which is the estimated short term disequilibrium rent (deviation of observed effective rent from long term equilibrium rent); \( {\overset{\frown }{\beta}}_0 \), \( {\widehat{\gamma}}_E \) and \( {\widehat{\gamma}}_S \) are the estimated values of γ S [ln(1 − v*) − λ 0], γ E , and γ E respectively.

Since (6) is a long term equilibrium relationship, the variables R, E, and S are expected to be co-integrated. The corresponding short run error correction model is a first difference equation of (6). As the observed vacancy rate also deviates from the natural vacancy rate or long run equilibrium vacancy rate, Englund et al. suggest in the short run, both rent and vacancy rates are likely to adjust to external shocks. Assuming that the long run equilibrium vacancy rate is constant, the lagged observed vacancy rate is a good proxy for disequilibrium vacancy rate (deviation of observed vacancy rate from constant long term equilibrium vacancy rate). Therefore the short run rent adjustment model should include the lagged vacancy rate as an explanatory variableFootnote 4:

where ε t-1 is the residual from co-integration model (6), The coefficient of ε t-1 is a measure of the initial response of rent adjustment to external shocks.Footnote 5 Hypothesis 1 implies that the magnitude of β R for Grade A offices is larger than that of Grade C offices.

Likewise, Englund et al., suggest the following short run vacancy rate adjustment model, which is analogous to (7):

where η R is a measure of the initial response of vacancy rate adjustment to external shocks. Hypothesis 2 implies that the magnitude of η R for Grade A offices is smaller than that of Grade C offices.

Following Englund et al., we model supply by lagged vacancy rate and disequilibrium rent with the lagged period determined empirically, i.e.,

where ϕ v and ϕ ε are coefficients to be estimated. The lagged period time τ represents the period between decision-making to realization of supply. The value of τ is determined empirically by maximizing the explanatory power of the model.

Since it takes a long time to plan, design and build offices, it is possible that changes in office stock are serially correlated, which justifies added a lagged dependent variable to (9). We have also estimated the results with this specification of the Supply Equation (see Alternative Model Specification).

The Eqs. (7), (8) and (9) are estimated as a system of equations using seemingly unrelated regressions (SUR) method. The expected signs of the estimated coefficients are summarized Table 1

Hypothesis 1 is confirmed if the magnitude of the coefficient of ε t ‐ 1 in (7) for Grade A office is larger than that of Grade C office.

Hypothesis 2 is confirmed if the magnitude of the coefficient of ε t ‐ 1 in (8) for Grade A office is smaller than that of Grade C office.

Data

All the data required for estimating the empirical model are publicly available in Hong Kong. We have collected yearly data over the period 1981–2013.Footnote 6 The data descriptions and source are summaries in Table 2.

Rental Indices (R)

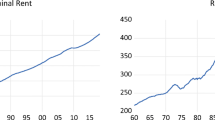

The Rating and Valuation Department of the Hong Kong SAR Government (RVD) started to publish rental indices for offices of different grades in the early 80s. According to the Technical Notes (Rating and Valuation Department 2012a, b), the rental indices “are designed to measure rental and price changes with quality kept at a constant”. The annual indices are the simple average of the monthly indices in respect of the relevant period.

The rental indices are not free of defects. The rental indices may tend to “understate market trends” (Rating and Valuation Department 2012a, b), since there will be some contractual terms unknown to the Department. “In a ‘tenants market’ for example, landlords are normally prepared to make concessions to tenants such as refurbishment or the granting of extended rent-free periods. If rents were adjusted to reflect standard terms of agreement, the rents as adjusted would tend to be lower than the quoted rents when the index is moving downwards and vice versa” (Rating and Valuation Department 2012a, b). However, considering that the impact of such terms contributes to only a small portion of the total consideration of the rental contract, the office rental indices are considered to be reliable indicators of office rental movements (Brown and Chau 1997).

Private Consumer Expenditure Deflator (PCED)

In order to remove the effect of inflation from the rental price indices, we need a measure of inflation. We use deflator for private consumer expenditure (PCE) as a measure of inflation. According to Census and Statistics Department (2015), PCE refers to “the value of final consumption expenditure on goods and services by households and private non-profit institutions serving households”. In addition, the PCE is “a comprehensive measure of a household’s overall spending on consumption goods (purchased from various channels including the conventional retail outlets) and services purchased locally or outside Hong Kong”. Real office rental indices are derived from deflating the office rental indices by the PCE deflator.

Stock (S)

Stock of offices is recorded at year end. In order to be consistent with other data, we use mid-year stock, which is estimated by the mean value of the current and the previous year end figures.

Vacancy Rate (v)

According to the Rating and Valuation Department (2012a, b), a vacant unit is “a unit not physically occupied at the time of the survey conducted at the end of the year”. In addition, “premises under decoration are classified as vacant”, and “some vacancies could be due to units not yet issued with the Certificate of Compliance or Consent to Assign, which therefore could not have been occupied”.

Similar to stock, vacancy rate are end year figures. We estimate the mid-year figures from the mean value of the current and previous year end figures.

Employment (E)

Employment data by industry sub-sector are available from the Census and Statistics Department of the Hong Kong SAR Government. The classifications are “based on the Hong Kong Standard Industrial Classification Version 1.1 (HSIC V1.1), which is modeled on the United Nations’ International Standard Industrial Classification (Revision 2) (ISIC Rev. 2), with adaptation for the industrial structure of the local economy” before 2008. After 2008, a modified version, the Hong Kong Standard Industrial Classification Version 2.0 (HSIC V2.01), has been used.

We use employment in the financial sector as the demand driver for Grade A offices. For Grade C offices, demand drivers are much more diverse. We have therefore included employments in real estate, insurance, professional, social, personal and other services as demand drivers. We assume that a relatively constant fraction of employments in these sectors are tenants of Grade C offices.

As a robust check, we have also used the same demand driver (all service sector employment) for both Grade A and C offices. It is expected that using more demand drivers specific to for each sub-sector described above would produce more significant results.

Detailed information on office area per office employee is not available. We have assumed that office space per employee have not changed dramatically during the observation period. This is supported by the fact that in the long term growth rate of office space stock (1982–2013: 4.30 % p.a.) and the total number of persons engaged in the services sector (1982–2013: 4.25 % p.a.) are similar. The descriptive statistics of the all data used are shown in Table 3:

Results and Discussions

Table 4 shows that estimation of the long term equilibrium relationship (6) for Grade A and C offices.

All the coefficients have the expected sign. The Johansen trace test shows that the variables lnR, lnE and lnS are co-integrated with one or two co-integrating relationship for both Grade A and C office sub-markets.

The result of the estimating the system of Eqs. (7), (8), and (9) for Grade A and C offices using seemingly unrelated regression (SUR) method are presented in Table 5.

Rental Adjustment

Table 5 shows that the coefficient of disequilibrium rent in the rental adjustment equation, ε R, of Grade A office is −0.5372, meaning rental price adjusted approximately 54 % of the deviation from equilibrium rent in 1 year. This figure is higher than that of Grade C office (−0.2535). The result suggests that Grade A office rents adjust faster to external shocks. The difference between coefficients of disequilibrium rent in for Grade A and C office is significant at the 10 % level, which is consistent with Hypothesis 1.

It is interesting to note that the speed of Grade A office rent adjustment in Hong Kong is on the high side compared to those reported in studies using US data (Ibanez and Pennington-Cross 2013), UK (Hendershott et al. 2002a, b; 2010) and European data (Englund et al. 2008, Brounen and Jennen 2009b, Adams and Füss 2012). This is consistent with the relatively lower transaction cost in Hong Kong’s high-end office rental market due probably to the higher land prices in Hong Kong (which results in less information asymmetry problem), more homogeneous nature of the office leases and shorter lease terms of usually 2 years.

Grade A office rent do not respond to previous vacancy rate as shown by the insignificant coefficients of the lagged vacancy gap indicating that lagged vacancy gap has not played an important role in the rent dynamics for Grade A offices. This, however, is not the case for Grade C office. The negative and significant coefficient of lagged vacancy rate suggests that rent adjust to last year’s vacancy gap in the Grade C office sub-market.

Vacancy Rate Adjustment

The vacancy rate of Grade A offices is insensitive to external shock as shown by the insignificant coefficient of the disequilibrium rent ε t − 1. in the vacancy adjustment equation. In contrast, the vacancy rate of Grade C offices is significantly negatively correlated with ε t − 1 This suggests that in when there is an external shock, rent rather than vacancy rate will adjust to the shock in the Grade A office market. However, in the Grade C office market, both rent and vacancy rate will adjust to the external shock but the rent adjustment is slower compared with that of the Grade A office (approximately half of that of Grade A office). The slower rent adjustment process is partly “compensated for” by a vacancy rate adjustment process to restore to a new short run equilibrium point. This result is consistent with the hypothesis 2.

Supply Adjustment

The optimal time lagged is found by try and error. The lagged period that maximizes the adjusted R squared is chosen as the optimal lag. The optimal time lag is 3 years for both Grade A and Grade C offices (which is the same as that reported in Englund et al.). This means that it takes approximately 3 years for the supply decisions to be realized.

Alternative Model Specification

Since both disequilibrium rent and vacancy gap in the model are results of the same external shock, it may be argued that only one disequilibrium variable is needed to represent the external shock in the estimation of (7) an (8). Since vacancy gap does not feature in the long run equilibrium model, we re-estimate the empirical model by excluding vacancy gap as an additional disequilibrium factor in (7) and (8). We have also included lagged dependent variable in the stock adjustment equation to reflect the stickiness of changes in the stock level of office buildings. The results for Grade A and C office are shown in Tables 6 and 7 respectively. The results are qualitatively similar across different model specifications. In particular, the rent adjustment coefficient for Grade A office is significantly larger than that of the corresponding model for Grade C office (p < 10 % at least) for all model specifications, which is consistent with hypothesis 1. The coefficients of the disequilibrium rent in the vacancy adjustment equations are insignificant in all models for Grade A while those for Grade C office are all significant the 1 % level, which is consistent with hypothesis 2.

As a robust test, we have also used the office sector-wide demand driver for both Grade A and Grade C offices. The results long run model and error correction models are shown in Tables 8 and 9 respectively. Even using the a common demand indicator for both Grade A and Grade C offices, the results are similar to those using sector specific demand indicators (Tables 4 and 5). The results are less significant for Grade A offices but more significant for Grade C offices. This suggests that Grade C office employment could be a relatively fixed percentage of total service sector employment. If this were the case, Grade C office results in Table 9 and Grade A office results in Table 5 should be adopted. However, this will only reinforce the results of confirming hypothesis 1 (hypothesis 2 will not be materially affected) since the rent adjustment coefficient is −0.1998, which is even smaller than that in Table 5.

Conclusion

In a world of zero transaction cost, rental price will adjust to a new equilibrium level immediately after external shocks and the observed vacancy rate will always be equal the natural vacancy rate. In reality, transaction cost is high in the office rental market, causing rent and vacancy rate to deviate from their long term equilibrium level in the short run, which trigger the rental and vacancy rate adjustment process. One of the major transaction costs that hinders rent and vacancy rate to fully and instantaneously adjust to a new equilibrium position after an external shock is asymmetric information about the quality of office spaces.

Compared with low-end office buildings (Grade C offices), the quality of the high-end office buildings (Grade A offices) can be more easily observed by the prospective tenants. That is, information asymmetry is less serious for high-end offices since the quality of Grade A offices are mainly derived from its location which is easily observable by the prospective tenant. The probability of a successful transaction in the high-end office market is higher compared to that in the low-end office market. We therefore hypothesize that rent adjustment is faster in the high-end office market after an external shock. On the other hand, since rent adjust more slowly in the low-end office market due to more serious information asymmetry problem, vacancy rate will also response to external shock to compensate the slower rent adjustment, which leads to our second hypothesis. These hypotheses are supported by empirical results from Hong Kong. The results are robust across different specifications of the empirical models. Similar results can be found in Ibanez & Pennington-Cross using US data, which provides further support to our hypotheses.

Notes

Due to high information cost, some land lords may not be able to adjust their asking rent immediately

Table 10 in the Appendix shows that on average, close to 70 % of the Grade A offices are located in CBD areas while 70 % of the Grade C offices are in non-CBD areas of the traditional commercial areas in Hong Kong. This Patten has been rather stable over the observation period although there is tendency for more Grade A offices located in non-CBD areas.

The average duration of the office lease in London was 10.8 years for year 2007/08 on a rent weighted basis, according to British Property Federation and Investment Property Databank (2008)

Disequilibrium rent and vacancy rates are two sides of the same coin, including both disequilibrium rent and vacancy variables in the rent or vacancy rate the short run adjustment model may lead to double counting since the effect of the same external shock appeared twice (but in different form) in both the rent and vacancy rate adjustment equations. Another possible specification is to represent external shock by disequilibrium rent only so that (7) and (8) do not include lagged vacancy rate as an additional disequilibrium factor. We have also estimated empirical models with this specification in our robustness tests (see Alternative Model Specification).

Unlike Englund at el and some of the similar studies, we have not included the lagged dependent variable in our empirical estimation since our rental indices are constructed based on actual rental transactions rather than appraised values. The inclusion of a lagged dependent variable in (10) is also not consistent with the long term equilibrium model (9) which does not included a lagged dependent variable as a regressor.

The data may not be as long as one would wish to get in order to have more robust and reliable results. However, we can only work with what is available and that our data series is longer than those in most pervious similar studies.

References

Adams, Z., & Füss, R. (2012). Disentangling the short and long-run effects of occupied stock in the rental adjustment process. Journal of Real Estate Finance and Economics, 44(4), 570–590.

Blank, D., & Winnick, L. (1953). The structure of the housing market. Quarterly Journal of Economics, 67, 181–208.

Brounen, D., & Jennen, M. (2009a). Asymmetric properties of office rent adjustment. Journal of Real Estate Finance and Economics, 39(3), 336–358.

Brounen, D., & Jennen, M. (2009b). Local office rent dynamics. Journal of Real Estate Finance and Economics, 39(4), 385–402.

Brown, G., & Chau, K. W. (1997). Excess returns in the Hong Kong commercial real estate market. Journal of Real Estate Research, 14, 91–105.

Census, and Statistics Department. (2015). 2014 Gross Domestic Product. Hong Kong: Census and Statistics Department.

Cheung, S. N. (1998). The transaction costs paradigm 1998 presidential address western economic association. Economic Inquiry, 36(4), 514–521.

Clapp, J. (1993). Dynamics of office markets: Empirical findings and research issues. Washington: Urban Institute Press.

Coase, R. (1937). The nature of the firm. Economica, 4, 386–405.

de Francesco, A. J. (2008). Time-series characteristics and long-run equilibrium for major Australian office markets. Real Estate Economics, 36(2), 371–402.

Englund, P., Gunnelin, Å., Hendershott, P. H., & Söderberg, B. (2008). Adjustment in property space markets: taking long-term leases and transaction costs seriously. Real Estate Economics, 36, 81–109.

Eubank, A., & Sirmans, C. (1979). The price adjustment mechanism for rental housing in the United States. Quarterly Journal of Economics, 93, 163–183.

Hendershott, P. (1996). Rental adjustment and valuation in overbuilt markets: evidence from the Sydney office market. Journal of Urban Economics, 39, 51–67.

Hendershott, P. H., Macgregor, B. D., & Tse, R. Y. C. (2002a). Estimation of the rental adjustment process. Real Estate Economics, 30, 165–183.

Hendershott, P. H., Macgregor, B. D., & White, M. J. (2002b). Explaining real commercial rents using an error correction model with panel data. Journal of Real Estate Finance and Economics, 24(1–2), 59–87.

Hendershott, P. H., Lizieri, C. M., & Macgregor, B. D. (2010). Asymmetric adjustment in the city of London office market. Journal of Real Estate Finance and Economics, 41(1), 80–101.

Ibanez, M. R., & Pennington-Cross, A. (2013). Commercial property rent dynamics in U.S. metropolitan areas: an examination of office, Industrial, flex and retail space. Journal of Real Estate Finance and Economics, 46(2), 232–259.

Pretorius, F., Walker, A., & Chau, K. W. (2003). Exploitation, expropriation and capital assets: the economics of commercial real estate leases. Journal of Real Estate Literature, 11(1), 1–34.

Rating and Valuation Department (2012). Hong Kong property Review 2008. Hong Kong Property Review. Hong Kong.

Rating and Valuation Department (2012). Technical notes. Property market statistics. Hong Kong, Rating and Valuation Department.

Rosen, K. T., & Smith, L. B. (1983). The price-adjustment process for rental housing and the natural vacancy rate. The American Economic Review, 73(4), 779–786.

Shilling, J. D., Sirmans, C. F., & Corgel, J. B. (1987). Price adjustment process for rental office space. Journal of Urban Economics, 22(1), 90–100.

Wheaton, W., & Torto, R. (1988). Vacancy rates and the future of office rents. Real Estate Economics, 16, 430–436.

Wheaton, W., Torto, R., & Evans, P. (1997). The cyclic behavior of the greater London office market. Journal of Real Estate Finance and Economics, 15, 77–92.

Wong, S. K., Yiu, C. Y., & Chau, K. W. (2012). Liquidity and information asymmetry in the real estate market. Journal of Real Estate Finance and Economics, 45(1), 49–62.

Acknowledgments

This project is financially supported by General Research Fund (RGC Reference Number: 710810) of the Research Grants Council of the Hong Kong SAR.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Chau, K.W., Wong, S.K. Information Asymmetry and the Rent and Vacancy Rate Dynamics in the Office Market. J Real Estate Finan Econ 53, 162–183 (2016). https://doi.org/10.1007/s11146-015-9510-7

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11146-015-9510-7