Abstract

This paper develops an open-economy DSGE model with an optimizing banking sector to assess the role of capital flows, macro-financial linkages, and macroprudential policies. The key result is that macroprudential measures can usefully complement monetary policy. Countercyclical macroprudential polices can help reduce macroeconomic volatility and enhance welfare. The results also demonstrate the importance of capital flows and financial stability for business cycle fluctuations as well as the role of supply side financial accelerator effects in the amplification and propagation of shocks.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In the wake of the global financial crisis, it is increasingly recognized that central banks have a dual role in maintaining both price and financial stability. A key missing ingredient was an overarching policy framework responsible for systemic financial stability. Neither macroeconomic policymakers nor prudential regulators were in charge of ensuring the stability of the financial system as a whole.Footnote 1 One of the discerning features of this crisis has been that shocks originating in credit markets have resulted in a ”great recession” and large-scale unemployment. Against this backdrop, there have been increased calls for better understanding macro-financial linkages and the development of a policy that can explicitly focus on system wide risks and macroprudential framework (IMF 2011a).

Managing the macroeconomic stability implications of large capital inflows and build-up of systemic risks is of importance for Emerging Asia.Footnote 2 Policymakers face two sets of interrelated challenges: (i) to prevent capital flows from exacerbating macroeconomic overheating pressures and consequent inflation, and (ii) to minimize the risk that prolonged periods of easy financing conditions will undermine financial stability. Given Asia’s past experience with credit and/or asset valuation boom-bust cycles, macroprudential measures could be particularly useful in reducing the procyclicality of financial systems and, therefore, the amplitude of business cycles.Footnote 3 While debate continues on the appropriate tools and structures for successful mitigation of systemic risk,Footnote 4 we consider the policy implications of implementing a macroprudential overlay that could accompany the traditional microprudential and macroeconomic policy. Monetary policy and macroprudential policy are only some aspects of the needed macroeconomic adjustment that a country facing large capital inflows could undertake. The full range of policies in the toolkit for managing capital flows include foreign exchange market intervention, currency appreciation, fiscal adjustment, and structural reforms (see IMF 2011b for a comprehensive discussion).

This paper develops an open economy DSGE model with an optimizing banking sector to assess the role of capital flows, macro-financial linkages, and macroprudential policies in a stylized Emerging Market Economy (EME). It specifically looks at (1) the impact of capital inflows on the economy and credit-asset price cycles; (2) the monetary transmission mechanism in the presence of a banking sector and financial frictions; and (3) the potential role for macroprudential policies in maintaining macro-financial stability including their interactions with monetary policy.

We introduce a banking sector modeled after Gertler and Karadi (2011) and Gertler and Kiyotaki (2011) augmented with macroprudential policy in the form of capital requirements. Such a set up creates a financial accelerator effect on the supply side of funding where the lending constraint is relaxed when banks’ net worth increases. Financial accelerator mechanisms can foster inefficient economic fluctuations (such as excess volatility in lending, investment and output) which can be mitigated by macroprudential policy tools that increase (reduce) the cost to banks of extending (shrinking) credit in good (bad) times.

In such scenario, macroprudential measures can usefully complement monetary policy. Countercyclical macroprudential polices can help reduce macroeconomic volatility and enhance welfare in combination with a modified Taylor rule. The results also demonstrate the importance of capital flows and financial stability for business cycle fluctuations as well as the role of supply-side financial accelerator effects in the amplification and propagation of shocks.

2 Background

Over the past decades capital flows to Emerging Asia have been highly volatile (Asia Pacific Regional Economic Outlook (APD-REO henceforth) of April 2011). After a significant surge in the early 1990s, they saw a massive reversal with the Asian financial crisis. Since the mid-2000s, capital flows resumed, but remained volatile, recording a boom from 2006Q4 to 2007Q3, followed by a sharp decline during the Global Financial Crisis (GFC), and another upswing from 2009Q3 to 2011Q3 (Fig. 1).

Non-Resident Non-FDI Inflows to Asia (Four-quarter moving average)

After May 2013, in the wake of Fed tapering announcement, portfolio flows saw a sharp reversal. While the pattern of capital flow movements is similar for both industrial Asia (including Australia, Japan, and New Zealand) and the rest of Asia, the latter experienced larger shifts in flows, especially in the 1990s and in 2012-13.

Net capital flows were also volatile, particularly in Asian economies excluding China, also due to their composition. Flows to non-China Asia have been dominated by portfolio and other investment—mainly bank loans (Fig. 2). Both are volatile sources of funding: portfolio investment is considered more mobile than other flows, and bank loans are typically short-term. Large portfolio outflows occurred in the aftermath of the GFC, which is a reminiscent of massive outflows in ‘other investment category’ during the Asian crisis. Both types of flows are also highly sensitive to external financial conditions (see IMF 2011b) particularly in advanced economies: similarly to the most recent ‘surge’ in inflows, flows to Asia in the run-up to the Asia crisis was related to a declining trend in interest rates in the advanced countries and a search for yield. As global interest rates are expected to remain low for longer and Emerging Asia will remain a global growth leader, it will very likely continue to receive large capital flows. Nevertheless, a number of global and regional factors will affect interregional and intraregional flows, and most likely, will contribute to capital flow volatility. In the short to medium-term the US Fed exit from unconventional monetary policy and normalization of global interest rates will likely play a role. Bank of Japan’s (BoJ) program of quantitative and qualitative monetary easing (QQME) could also potentially have an impact on capital flows to and within the region. Beyond the medium term, capital flows to and within Asia will be largely shaped by capital account liberalization, most notably in China. Other factors, such as financial integration within and outside the region, financial development, and savings patterns—in turn driven by demographics—are also expected to contribute to shape capital flows movements, including within the region. Capital inflows present opportunities, but they can also pose macroeconomic and financial stability risks. The inflows, if channeled effectively, represent an opportunity to address long-standing investment needs, such as in infrastructure. However, capital inflows need to be managed carefully in order to avoid macroeconomic and financial risks. Inflows can increase liquidity and boost domestic demand and asset prices.

Asia Capital Flows, Net (in Billions of US Dollars)

In Emerging Asia, the empirical relationship between non-FDI capital inflows and domestic demand is strong (see APD-REO of October 2010a). The impulse responses from an unrestricted VAR show that both consumption and investment respond strongly, particularly to equity flows (Fig. 3).Footnote 5 The effect of a 1 percentage point of GDP increase in equity flows persists for nearly four quarters. At its peak, the effect is equivalent to 0.4 percentage points of quarter-on-quarter annualized growth in the case of consumption, and more than three times that amount for investment. Both components of domestic demand also grow more rapidly following a shock to other investment flows. Finally, investment growth is associated positively with shocks to debt flows, although the effect wears off relatively quickly after two quarters. The main channel through which non-FDI capital inflows seems to work in EM Asia is by reducing the cost of equity finance and expanding private credit. The real cost of equity declines following a positive shock to equity inflows (Fig. 4).Footnote 6 The effect persists even six quarters after the initial shock and helps explain why investment growth increases in response to a large inflow of equity capital. Easier external financial conditions enhance the borrowing capacity of corporates and expand the volume of bank resources available to them. Bank credit to the private sector also responds favorably to other investment flows (Fig. 5), suggesting that a link between wholesale bank funding from overseas and credit supply.

EM Asia: Response to Increase in Net Capital Inflows

EM Asia: Response of Real Cost of Equity to a 1 percentage Increase in Net Portfolio Equity Flows

EM Asia: Response of Credit to Private Sector to a 1 percentage point of GDP Increase in Other Investment Flows

As banks also rely on wholesale external funding and benefit from lower cost of equity capital, there may also be a tendency to relax lending standards with the easing of external financial conditions. Rapid credit growth raises risks for asset quality and bank capital, particularly once the credit cycle matures. Asia’s past history also suggests that high liquidity growth at a time of large capital inflows increases the risk of asset price boom and bust cycles (see the APD-REO of April 2010b), which could lead to potential feed-back loops between the corporate/household sector and banks. The APD-REO of October (2011) confirms that episodes of rapid credit growth in Asia have been characterized by a higher incidence of crises relative to other emerging economies.

3 Literature Review

The importance of financial shocks in terms of how they affect the real economy has long been realized but until the 2007 financial crisis most of the general equilibrium models developed to study macro-financial linkages have focused only on the demand side of credit markets. In particular, Kiyotaki and Moore (1997), Bernanke, Gertler and Gilchrist (1999), Iacoviello (2005) and Gertler, Gilchrist, and Natalucci (2007) have introduced credit and collateral requirements to analyze the transmission and amplification of financial shocks. These models have abstracted from modeling the banking sector explicitly, and assume that credit transactions take place through the market (thereby not assigning any role to financial intermediaries such as banks). The credit spread that arises in equilibrium (the external finance premium) is a function of the riskiness of the entrepreneurs’ investment projects and/or his net wealth. Banks, operating under perfect competition, simply accommodate the changing conditions from the demand side. The growing importance of banks in the modern financial system and the global crisis has demonstrated that the role of financial intermediation cannot be overlooked, and we need to model the supply of credit to understand business cycle fluctuations better. Also, modeling credit supply is essential to study the transmission of shocks originating in the credit markets or financial stability risks. To this extent, after the 2007 financial crisis several models have been developed to study the impact and the transmission of financial shocks and how real shocks are amplified through banking frictions. Gertler and Karadi (2011) and Gertler and Kiyotaki (2011) introduce a financial accelerator on the supply side of credit. In their framework banks are subject to an incentive constraint that limits the amount of funds that can raise from depositors. Curdia and Woodford (2010 and 2011) use a heterogeneous agent framework to study how monetary policy (both conventional and unconventional) should respond to a variety of real and financial disturbances. Gerali, Neri, Sessa and Signoretti (2010) study the importance of credit supply factors and monetary policy in a framework in which banks issue a collateralized loans with loans margins depend on the bank’s capital-to-asset ratio and on the degree of price stickiness.

Alongside the role of credit supply frictions and shocks, the macro-financial literature considers the benefits of introducing financial and macroprudential regulation. Two main strands of literature can be identified. The first one considers how excessive borrowing can distort agents’ decisions. In this case negative externalities arises because the outcome of individual decisions is not internalized by agents and regulation can force agents to internalize the negative externalities associated with their decisions. Some examples on how over-borrowing can create negative externalities and how financial regulation can mitigate them can be found in Bianchi and Mendoza (2011), Jeanne and Korinek (2010) and Bianchi (2011). The second strand focuses on how macroprudential policy can mitigate the impact of shocks and the interactions with monetary policy. Some examples of this literature are: Angeloni and Faia (2009) Kannan, Rabanal, and Scott (2009), N’Diaye (2009) and Unsal (2013). These papers find an important role for macroprudential policies and non-trivial interactions between financial regulation and monetary policy. However, these papers have a demand-side ”financial accelerator” framework but lack a full-specific banking sector to gauge financial stability and credit supply shocks.

This paper develops a model with a microfounded banking sector and following this second strand of the literature, takes banking capital requirements as the choice of macroprudential instrument for two main reasons. First, based on past experience systemic crises inevitably affect bank capital and the supply of credit, either directly or indirectly. And, not surprisingly, bank capital has taken centre stage in the ongoing debate on regulatory reform. Second, countercyclical risk weights and provisioning rates have been used frequently in Asia as a tool of macroprudential policy, which also predominantly works through a bank capital channel.

4 The Model

The core framework is an open economy model along the lines of Obstfeld and Rogoff (1995), Galí and Monacelli (2005) and Gertler, Gilchrist, and Natalucci (2007). The key modification is the inclusion of a microfounded banking sector as developed by Gertler and Karadi (2011) and Gertler and Kiyotaki (2011). The financial accelerator mechanism in the banking sector links the demand for loans (and therefore for capital) to the balance sheet of banks. As a consequence, a shock in the economy is amplified via the balance sheet of the bank.

In the model there are three players: households, banks and firms. Households work, deposit savings in the banks and consume a basket of home produced and foreign goods and they face financial frictions as in Benigno (2009). The banking sector collects deposits from households, make loans to firms and it faces an agency problem that limits the amount of deposits from households. Firms are divided in capital producers, goods producers and a retailers and their structure is fairly standard. Capital producers produced capital used by goods producers to produce final output. The role of the retail sector is to provide the source of nominal price stickiness.

4.1 Households

There is a continuum of identical households who consume, save and work. Each household deposit funds in a bank. Deposits take the form of riskless one period securities. Within the households, there is a fraction π of bankers and a fraction 1−π of workers. Bankers manages a financial intermediary and transfers non negative dividends to the households. Workers supply labour and return their wages to the households. Bankers remain engaged in their business activity next period with a probability σ which is independent of history. This finite survival scheme is needed to avoid that bankers accumulate enough wealth to remove the funding constraint. Upon exiting, a banker transfers retained earnings to the households and becomes a worker. As a consequence, in each period (1−σ) π workers become bankers, keeping the number in each group constant. Moreover, each new banker receives a transfer from the household since they cannot start the banking activity without funds.

Consumption Composites

Consumption index C t consists of home-produced C H and foreign C F goods:

The corresponding Dixit-Stiglitz price index is:

Standard intra-temporal optimizing decisions for home consumers lead to:

The real exchange rate can be defined as the relative aggregate consumption price \(RER_{C,t}\equiv \frac {P_{C,t}^{\ast } }{P_{C,t}}S_{t}\) where S t is the nominal exchange rate. As a consequence, foreign counterparts of the above defining demand for the export of the home goods are

where \(P_{H,t}^{\ast } \), \(P_{C,t}^{\ast } \) and \(P_{I,t}^{\ast } \) denote the price of home consumption, aggregate consumption and aggregate investment goods in foreign currency and we have used the law of one price, namely \( S_{t}P_{H,t}^{\ast } =P_{H,t}\). Again we define

and \(P_{I}^{\ast } \) similarly.

As in Benigno (2009) we assume that households face financial frictions when they purchase foreign bonds. There are two non-contingent one-period bonds denominated in the currencies of each block with payments in period t, B H, t and \(B_{F,t}^{\ast } \) respectively in (per capita) aggregate. The prices of these bonds are given by

where ϕ(⋅) captures the cost in the form of a risk premium for home households to hold foreign bonds, \(B_{F,t}^{\ast } \) is the aggregate foreign asset position of the economy denominated in home currency and P H, t Y t is nominal GDP. We assume ϕ(0)=0 and \(\phi ^{\prime } <0\). R n, t and \(R_{n,t}^{\ast } \) denote the nominal interest rate over the interval [t, t+1]. The term F B t represents a term that decreases the risk premium. Since this boosts foreign borrowing, we refer to this disturbance as a foreign borrowing shock that evolves according to the following process:

where 𝜖 F B, t is an independent and identically normal distributed process with zero mean and standard deviation σ F B .

The Household’s Decision Problem

The representative household maximizes:

where E t is the expectation operator indicating expectation formed at time t, β is the discount factor, χ is the degree of external habit on consumption and L t represents leisure. The parameters σ C and ρ refers to the elasticity of consumption and the household preferences respectively. The representative household is subject to the following budget constraint:

where h t represents hours worked P C, t is a Dixit-Stiglitz price, W t is the wage rate, T L t are lump-sum taxes net of transfers and Γ t are dividends from ownership of firms.

Consumption Allocation and Labour Supply

The intertemporal and labour supply decisions of the household are:

where

4.2 The Banking Sector

In the model, financial frictions affect real activity via the impact of funds available to banks and there is no friction in transferring funds between banks and nonfinancial firms (see Gertler and Karadi (2011) and Gertler and Kiyotaki. (2011)). Given a certain deposit level a bank can lend frictionlessly to nonfinancial firms against their future profits. In this regard, firms offer to banks a perfect state contingent security.

The level of the loans depends on the level of the deposits D t , the net worth of the intermediary N W t . This implies a banking sector’s balance sheet of the form:

where S B, t are claims on non-financial firms to finance capital acquired at the end of period t for use in period t+1 and Q t is the price of a unit of capital so that the assets of the bank. Consequently, Q t S B, t represents the level of the assets of the financial intermediary.

Net worth of the bank accumulates according to the following law of motion:

Banks exit with probability 1−σ per period and therefore survive for i−1 periods and exit in the ith period with probability (1−σ)σ i−1. Given the fact that bank pays dividends only when it exists, the banker’s objective is to maximize expected discounted terminal wealth:

subject to an incentive constraint for lenders (households) to be willing to supply funds to the banker.

As in Gertler and Karadi (2011), to motivate an endogenous constraint on the bank’s ability to obtain funds, we introduce the following simple agency problem. We assume that after a bank obtains funds, the bank’s manager may transfer a fraction of assets to her family. In the recognition of this possibility, households limit the funds they lend to banks. Moreover we assume that the fraction of funds that a banker can divert depends on the composition of the bank’s liabilities.

Divertable assets consists of total gross assets Q t S B, t . If a bank diverts assets for its personal gain, it faces defaults on its debt. The creditors may re-claim the remaining fraction 1−Θ of funds. Because its creditors recognize the bank’s incentive to divert funds, they will restrict the amount they lend. In this way a borrowing constraint may arise. In order to ensure that bankers do not divert funds the following incentive constraint must hold:

The incentive constraint states that in order for households to be willing to supply funds to a bank, the bank’s franchise value V t must be at least as large as the gain from diverting funds. As in Gertler and Karadi (2011) and Gertler and Kiyotaki (2011), to solve the problem we guess a linear solution of the form:

where ν s, t , and ν d, t , are time-varying parameters that are the marginal values of the asset at the end of period t. Let ϕ t be the leverage ratio of a bank that satisfy the incentive constraint, from the optimization problem we have that:

where ϕ t represents the leverage ratio. This is equal to:

and:

where \(DF_{t,t+k}=\beta ^{k}\left (\frac {{\Lambda }_{C,t+k}}{{\Lambda }_{C,t}}\right )\) is the real stochastic discount rate, Ω t is the shadow value of a unit of net worth and is equal to:

and the term R k, t+1 represents the return on capital defined in the following way:

where Z t+1 is the marginal product of capital.

Evolution of Aggregate Net Worth

At an aggregate level net worth is the sum of existing bankers and new bankers:

Net worth of existing bankers equals earnings on assets held in the previous period net cost of deposit finance, multiplied by a fraction σ, the probability that they survive until the current period:

Since new bankers cannot operate without any net worth, we assume that the family transfers to each one the fraction ξ B/(1−σ) of the total value assets of exiting bankers. This implies:

Given this the aggregate level of net worth is given by:

4.3 Non-financial Firms

4.3.1 Goods Producers

Competitive good producers operate a constant return to scale technology with capital an labour as inputs :

The term A t represents a technology shock that follows a process of the form:

where 𝜖 A, t is an independent and identically normal distributed process with zero mean and standard deviation σ A

The firm’s behavior is summarized by the following standard first order conditions:

4.3.2 Capital Producers

Capital producing firms at time t convert I t of output into (1−f(X t ))I t of new capital sold at a real price Q t , where f(X t ) is a investment adjustment cost function and \(X_{t}=\frac {I_{t}}{ I_{t-1}}.\) We assume that \(f^{\prime } ,f^{\prime \prime } \geq 0\). Their objective is to maximize the expected discounted profits:

This results in the first-order condition:

Up to a first order approximation this is the same as:

We complete this set-up with the following functional form:

Investment Composites

Gross investment consists of domestic and foreign final goods:

As for the consumption case, the corresponding Dixit-Stiglitz price index are:

This delivers the same form of intra-temporal first order conditions:

As before if, we define \(RER_{I,t}\equiv \frac {P_{I,t}^{\ast } S_{t}}{P_{I,t}} \) for investment, then foreign counterparts of the above defining demand for the export of the home goods are:

where \(P_{H,t}^{\ast } \), \(P_{C,t}^{\ast } \) and \(P_{I,t}^{\ast } \) denote the price of home consumption, aggregate consumption and aggregate investment goods in foreign currency and we have used the law of one price namely \( S_{t}P_{H,t}^{\ast } =P_{H,t}\). As before, we define:

4.3.3 The Retail Sector

The retail sector uses a homogeneous wholesale good to produce a basket of differentiated goods for consumption:

where ζ is the elasticity of substitution. This implies a set of demand equations for each intermediate good m with price P t (m) of the form:

where \(P_{t}=\left [{{\int }_{0}^{1}}P_{t}(m)^{1-\zeta } dm\right ]^{\frac {1}{1-\zeta }}P_{t}\) is the aggregate price index.

Now we assume that there is a probability of 1−ξ at each period that the price of each retail good m is set optimally to \({P_{t}^{0}}(m)\). If the price is not re-optimized, then it is held fixed.Footnote 7 For each retail producer m the objective is at time t to choose \(\{{P_{t}^{0}}(m)\}\) to maximize discounted profits:

subject to Eq. 45, where D F t, t + k is the nominal stochastic discount factor over the interval [t, t + k]. The solution to this is:

and by the law of large numbers the evolution of the price index is given by:

Defining the nominal discount factor by \(DF_{t,t+k}\equiv \beta \frac { {\Lambda }_{C,t+k}/P_{t+k}}{{\Lambda }_{C,t}/P_{t}}\), and M C t as the marginal costs, inflation dynamics are given by:

4.4 Central Bank

The central bank conducts monetary policy by adjusting the policy rate according to the following Taylor rule:

where 𝜖 r, t+1 is a monetary policy shock that is i.i.d. with zero mean and standard deviation σ M .

The real and the nominal interest rates are linked with the following Fisher equation:

4.5 Equilibrium, Foreign Asset Accumulation

Equilibrium and Foreign asset accumulation and the central bank behavior is given by the following equations.

The national income identity is equal to:

where:

where ν are the share of the foreign economy. G t represents government purchases that evolves according to the following process:

where 𝜖 G, t is an independent and identically normal distributed process with zero mean and standard deviation σ G . Current account dynamics are given by:

where the term T B t represents the trade balance. This is defined as:

The nominal exchange rate:

With local currency pricing the real exchange rate and the terms of trade, defined as the domestic currency relative price of import to export \( \mathcal {T}_{t}=\frac {P_{F,t}}{P_{H,t}},\) are related by the relationships:

Inflation is given by a composite of home and foreign inflation given by the following CES function:

The nominal interest rate \(R_{n,t}^{\ast } \) and the real interest rate are linked with the following Fisher equation:

Where \(R_{n,t}^{\ast } \) and \({\Pi }_{t}^{\ast } \) are defined by the following processes:

where \(\epsilon _{Rn,t}^{\ast } \) and \(\epsilon _{\pi ,t}^{\ast } \) are independent and identically normal distributed processes with zero mean and standard deviation σ R n and σ π . We close the model with the following processes:

where \(\epsilon _{c,t}^{\ast } \) and \(\epsilon _{i,t}^{\ast } \) are an independent and identically normal distributed processes with zero mean and standard deviation σ c and σ i .

5 Macroprudential Policy

Macroprudential policy affects the net worth of existing bankers. As a proxy to financial regulation we assume the existence of a tax/subsidy scheme in the line of Gertler, Kiyotaki and Queralto (2012), De Paoli and Paustian (2013) and Levine and Lima (2015).Footnote 8 Given that the banking sector takes as given the tax/subsidy on net worth τ t , the net worth of banks in Eq. 16 can be expressed in period t as:

As in the previous case, the net worth of the bank equals the return on assets minus the cost of funding with the addition of the tax/subsidy carried over from the previous period.

At an aggregate level net worth is the sum of existing bankers and new bankers. We assume that only the net worth of existing bankers are affected by the macroprudential policy tax/subsidy, i.e.:

This implies that the aggregate net worth of the banking sector can be expressed as:

The optimization problem for the banking sector and the remaining equations are similar to the one described in the previous section. However, given the choice of macroprudential regulation, the optimization problem takes into account the changes introduced by the financial regulation in the structure of the balance sheet of the banking sector.

The macroprudential rule is given by the following equation:

where the parameter ρ τ measures the degree of persistence of of the macroprudential policy instrument and α F B denotes the degree of response of the macroprudential policy tool to deviations in foreign borrowing. This policy can be see as a time varying tax that depends on the level of foreign borrowing in the economy.

6 Calibration

Parameters are calibrated on quarterly data and they reflect broad characteristics of emerging Asian economies as in Anand, Peiris, and Saxegaard (2010) and Batini, Levine, and Pearlman (2007). In particular, following Anand, Peiris, and Saxegaard (2010) we calibrate the great ratios and the shares w C , w I , \(\mathrm {w}_{C}^{\ast }\), \(\mathrm {w}_{I}^{\ast } \) at 0.8 and, following Batini, Levine, and Pearlman (2007) we calibrate the substitution elasticities μ C , \( \mu _{C}^{\ast } \) at 1.5 and μ I , \(\mu _{I}^{\ast } \) at 0.25. The banking sector is calibrated as in Gertler and Kiyotaki (2011): σ is set at 0.975 implying a survival rate of 10 years. ξ and Θ are calibrated to hit an average credit spread of 100 basis points and a financial intermediaries leverage ratio of 4. Regarding the calibration of the foreign borrowing, technology and government spending we follow the values for the coefficients and the standard deviation based on the estimated model for an emerging Asian economy of Gabriel, Levine, Pearlman and Yang (2010). Their model is fairly similar to ours as they include a financial accelerator as in Bernanke, Gertler and Gilchrist (1999) and all the mentioned shocks. The estimated values of the coefficients and standard deviation for the technology shock and foreign borrowing are similar to the estimated ones of Elekdag, Justiniano and Tchakarov (2006). Table 1 provides the full list of the value of the parameters.

7 Optimal Policy Rules and Welfare Analysis

The interaction of monetary policy with macroprudential policies suggests scope to minimize macrofinancial instability by combining a modified Taylor rule with a macroprudential overlay. In this section we study how macroprudential policy interacts with monetary policy. In order to assess the importance of such interactions, we consider four different policy scenarios. In the first scenario we employ a standard Taylor rule as described in Eq. 52. In the second one we consider an augmented Taylor-rule that put some weight on credit growth. This allows us to study leaning-against-the-wind policy along the lines of Christiano et al. (2010), and Curdia and Woodford (2010) among others. The third scenario aims at showing the importance of macroprudential policy and, to this extent, we introduce the macroprudential framework in the analysis and we use the standard Taylor rule. In the fourth and last scenario we employ the augmented Taylor rule in the macroprudential policy framework.

Our analysis allows us to explore the two different mandates, or policy regimes. The first institutional regime is represented by the case in which the monetary authority and the macroprudential authority focus on their own policy objective. This implies a that the central bank reacts only to fluctuations in inflation and output without responding to changes in financial variables. An unified mandate characterize the second regime. In this case both the monetary and macroprudential authority react to fluctuations in financial variable. In our analysis this is represented by the fourth scenario, i.e. the central bank reacts to the augmented Taylor rule in the macroprudential policy framework.

To compute the welfare loss in terms of consumption equivalence we employ the methodology as in Schmitt-Grohé and Uribe (2007) and we calculate the welfare loss using a second order approximation of the utility function. This represents the fraction of consumption (in percentage terms) that is required to equate welfare under a given policy rule to the one given by the reference scenario in the face of a one percent given shock.Footnote 9 Following Faia and Monacelli (2007) and Gertler and Karadi (2011) we start by expressing the household utility function in a recursive form:

Then we take a second order approximation of this function at the steady state. Using the second order solution of the model we calculate the value of V t for each case. The comparison is made in terms of a consumption equivalent, given by the fraction of consumption required to equate welfare under a given policy to the welfare under the augmented Taylor rule in the macroprudential policy framework. The result is a measure of the welfare loss in units of steady state consumption. A higher value of welfare loss indicates that the policy is less desirable.

In our analysis we take into account three shocks, namely: (i) foreign borrowing shock, (ii) technology shock and (iii) government shock. This allows us to explore the implications of a shock that creates undesirable volatility (foreign borrowing shock), and shocks that creates desired volatility (technology and government shock). These last two shocks create interesting trade-offs. After a positive technology or government shock the macroprudential policy or a leaning against the wind policy act to mitigate the impact of innovations (in the case of a TFP shock) or the policy stance of another policy institution (in the case of a government shock). However, under a negative technology or government shock (e.g. fiscal retrenchment), those policy can successfully mitigate the adverse impact and be growth-enhancing.

Table 2 reports the optimized coefficients of the monetary policy rule and Table 3 indicates the optimized coefficients of the macroprudential policy rule in response to the financial shock.Footnote 10 We follow Levine and Lima (2015) and to compute the optimal value, we calculate the optimized parameters by searching numerically in the grid of the policy rules parameters that optimize welfare.

Tables 2 and 3 highlight two main findings. The first is related to the values of the optimized coefficients of the monetary policy rule. Introducing an additional policy target leads to a decrease in the response of the augmented Taylor Rule to output and inflation. This is more evident when macroprudential policy is nested in the model. A comparison with the respective case when macroprudential policy is not included shows that the value of coefficients of the Taylor rule is higher when macroprudential policy is absent. This implies that the need for the monetary authority to react aggressively to fluctuations in output and inflation is attenuated when a leaning against the wind policy and macroprudential policy is in place. Table 3 highlights the second result. The optimized coefficient of the macroprudential policy rule decreases when the central bank reacts according to a Taylor rule augmented with credit growth. This is because the central bank acts with the macroprudential policy authority to counteract the negative impact of the shock. Therefore, in the cooperative scenario, the policy space is higher and allows more room to prevent negative spillovers (see Angelini, Neri and Panetta 2014 and Levine and Lima 2015).

Table 4 shows the computed welfare losses. The first result that emerges is that the augmented Taylor rule in the macroprudential policy framework is the most effective since the welfare loss is positive in all the cases.

A second important result is that the welfare loss is higher when the financial shock hit the economy. The foreign borrowing shock produces the highest welfare loss followed by the technology shock and the government shock. In particular, for the foreign shock the difference between the standard Taylor rule scenario and the scenario with an augmented Taylor rule in the macroprudential policy framework is 0.0478 percent. Similarly, for the technology shock, the difference is 0.0301 percent. Finally, for the government shock the difference is 0.0253 percent. The results are in line with previous studies in the literature. For emerging markets, Unsal (2013) finds that the welfare gains with broad macroprudential policy under the optimal policy rule after a financial shock is about 0.05 percent of steady state consumption. For the United States, Bianchi and Mendoza (2011) and Bianchi (2011) find that the welfare gains of having macroprudential prudential policy are about 0.02 percent of steady state consumption.

Finally, the results suggest that macroprudential policy is more effective than the standard Taylor rule and the Taylor rule augmented with credit growth. This can be seen in the welfare loss difference when macroprudential policy is introduced in the model. As an example we consider the foreign borrowing shock. In terms of welfare the difference between the standard Taylor rule and the augmented Taylor rule is 0.0177 percent (difference between the first and the second line). However, when macroprudential policy is considered the difference becomes 0.0305 percent (difference between the first and the third line). The relatively small role of Taylor rules augmented with credit growth is recorded also when this policy option is included in a framework in which macroprudential policy is present. In this case the welfare loss difference is 0.0173 percent. This result applies to all the shocks considered. However, in the case of technology shock the gains in terms of welfare loss of a leaning against the wind policy are smaller if compared to the gains obtained in the case of the foreign borrowing shock and the government shock. This is because, after a technology shock a trade-off between output stabilization and inflation emerge. However, in line with the findings of Bernanke and Gertler (2000, 2001) and Gambacorta and Signoretti (2014), a central bank that reacts to a Taylor rule with credit growth produce a lower, even if limited, welfare loss. As in the previous case, macroprudential policy is effective in improving the welfare in the economy as it limits the expansion of credit caused by a positive technology shock.

Compared to the other shocks, when the central bank reacts to the standard Taylor rule, the government shock produces the lowest welfare loss. This is because this shock increases aggregate demand but results in a lower crowding in of private investment (see Fernández-Villaverde 2010). This also explains why the Taylor rule with credit growth does not produce significant welfare loss improvements. The limited spillovers to investment result in a lower demand for loans from firms which implies a relatively lower credit growth. As in the previous cases, macroprudential policy can act to mitigate the impact of the shock as it lowers the amount of credit. However, following a fiscal stimulus this policy might not be desirable as it produce a waste in government spending.

Overall, the results suggest that, if a central bank wants to mitigate the impact of negative financial and non financial shocks, macroprudential policy is more effective than targeting financial variables in the Taylor rule. Moreover, financial stabilization and in particular, macroprudential measures in the form of capital requirement, play a crucial role in the stabilization policy and especially in the stabilization of financial shocks.

8 Conclusion

This paper develops an open economy DSGE model with an optimizing banking sector to assess the role of capital flows, macrofinancial linkages, and macroprudential policies. The key result is that macroprudential measures can usefully complement monetary policy in response to most types of exogenous shocks. Macroprudential polices can help reduce macroeconomic volatility and enhance welfare in combination with a modified Taylor rule that also places a weight on credit developments. However, the gains from countercyclical macroprudential policies are lower with technology shocks and generally result in lower medium term output. Thus, there is a potential trade-off of using countercyclical capital requirement as proposed in Basel III for emerging markets, requiring a judicial use of macroprudential policies tailored to country circumstances. The results also demonstrate the importance of capital flows and financial stability for business cycle fluctuations as well as supply-side financial accelerator effects in the amplification and propagation of shocks in an emerging Asian economy.

Asset prices and banking lending are the key channels of transmission of capital flows in emerging Asia. The large capital inflows received by emerging Asian countries can result in macroeconomic overheating pressures such as higher inflation and real exchange rate appreciation as well as financial stability risks as capital inflows fuel rapid asset price inflation and credit growth. Our analysis suggests that the best response to financial and foreign shocks would be to implement countercyclical macroprudential polices as they help reducing macroeconomic volatility and procyclicality of the financial system in combination with a modified Taylor rule that places some weight on credit growth. Indeed, as the welfare analysis showed, among the policy options considered the welfare loss in minimized when countercyclical regulation is taken into account together with an augmented Taylor rule. This seems a more attractive option than contemplating direct measures to control capital inflows and large-scale foreign exchange interventions that have been shown to be suboptimal even in models without optimizing banking sectors (see Unsal 2013 and Berg et Bergal. 2011 among others), although this paper does not consider those policies and leaves that for future research.

Financial instability has a pervasive and significant impact on the real economy through macrofinancial linkages. The model sheds light on the key transmission mechanism of a financial crisis by showing how bank leverage amplifies the initial shock to capital and tightens the banks’ borrowing constraint inducing effectively a fire sale of assets. The crisis then feeds into real activity as the decline in asset values is responsible for the magnified drop in investment and output. In this way the model captures how the deleveraging process can slow down a recovery as observed in the global financial crisis and Asian financial crisis. This transmission mechanism also highlights the importance of maintaining an adequate bank capital buffer, avoiding a rapid growth in credit that often leads to rash of non-performing loans, and role of asset prices in amplifying business cycles. Here again, macroprudential policies could help minimize macrofinancial instability by combining a modified Taylor rule with a countercyclical capital requirement.

Notes

See Viñals (2010).

See Craig, Davis, and Pascual (2006) for evidence on the procyclicality of Asian financial markets.

Figure 3 shows the response of quarter-on-quarter annualized growth to 1 percentage point of GDP increase in net inflows (see APD-REO of October 2010 for a detailed discussion of net capital inflows to Asia).

Conceptually, the real cost of equity (i.e., the implied rate of return required by investors) is equal to the sum of the risk-free interest rate and the equity risk premium. At a time of capital inflows, the relative appeal of capital investment increases, making it easier for firms to borrow from banks based on their greater net worth.

Thus we can interpret \(\frac {1}{1-\xi }\) as the average duration for which prices are left unchanged.

We assume that the tax ∖subsidy scheme is provided by the government.

References

Anand R, Peiris SJ, Saxegaard M (2010) An Estimated Model with Macrofianncial Linkages for India, IMF Working Paper No. 10/21, International Monetary Fund

Angelini P, Neri S, Panetta F (2014) Monetary and macroprudential policies. J Money, Credit Bank, Blackwell Publ 46(6):1073–1112, 09

Angeloni I, Faia E (2009) A Tale of Two Policies: Prudential Regulation and Monetary Policy with Fragile Banks, Kiel Working Papers 1569, Kiel Institute for the World Economy

Asia Pacific Regional Economic Outlook (2010a). International Monetary Fund

Asia Pacific Regional Economic Outlook (2010b). International Monetary Fund

Asia Pacific Regional Economic Outlook (2011). International Monetary Fund

Batini N, Levine P, Pearlman J (2007) Monetary Rules in Emerging Economies with Financial Market Imperfections, NBER Chapters. In: International Dimensions of Monetary Policy, pages 251-311 National Bureau of Economic Research, Inc.

Benigno P (2009) Price stability with imperfect financial integration. J Money, Credit Bank, Blackwell Publ 41(s1):121–149, 02

Bank of International Settlements (2010) Financial system and macroeconomic resilience: revisited. BIS papers N. 53

Berg A, Schindler M, Papageorgiou C, Weisfeld H, Pattillo CA, Spatafora N (2011) Global Shocks and their Impact on Low-Income Countries: Lessons from theGlobal Financial Crisis, IMF Working Papers 11/27, International Monetary Fund

Bernanke BS, Gertler M (2000) Monetary policy and asset price volatility. NBER Working Papers 7559

Bernanke BS, Gertler M (2001) Should central banks respond to movements in asset prices? Am Econ Rev Am Econ Assoc 91(2)

Bernanke B, Gertler M, Gilchrist S (1999) The Financial Accelerator in a Quantitative Business Cycle Framework, Handbook of Macroeconomics, Vol. 1C, Chapter 21, ed. By J.B. Taylor and M. Woodford (Amsterdam: North-Holland)

Bianchi J (2011) Overborrowing and systemic externalities in the business cycle. Am Econ Rev, Am Econ Assoc 101(7):3400–3426

Bianchi J, Mendoza EG (2011) Overborrowing, Financial Crises and Macro-Prudential Policy IMF Working Papers 11/24, International Monetary Fund

Christiano L, Motto R, Rostagno M (2010) Financial factors in economic fluctuations, Working Paper Series 1192, European Central Bank

Craig RS, Davis E, Pascual AG (2006) Sources of Procyclicality in East Asian Financial Systems. In: Gerlach S, Gruenwald P (eds) Procyclicality of Financial Systems in Asia, International Monetary Fund

Curdia V, Woodford M (2010) Credit spreads and monetary policy. J Money, Credit Bank, Blackwell Publ 42(s1):3–35, 09

Cúrdia V, Woodford M (2011) The central-bank balance sheet as an instrument of monetarypolicy. J Monet Econ, Elsevier 58(1):54–79

De Paoli B, Paustian M (2013) Coordinating monetary and macroprudential policies, Staff Reports 653, Federal Reserve Bank of New York

Eichengreen B (1998) Exchange Rate Stability and Financial Stability. Open Econ Rev, Springer 9(1):569–608

Elekdag S (2006) An estimated small open economy model of the financial accelerator. IMF Staff Papers, Palgrave Macmillan 53(2):2

Faia E, Monacelli T (2007) Optimal interest rate rules, asset prices, and credit frictions. J Econ Dyn Control, Elsevier 31(10):3228–3254

Fernández-Villaverde J (2010) Fiscal policy in a model with financial frictions. Am Econ Rev, Am Econ Assoc 100(2):35–40

Gabriel V, Levine P, Pearlman J, Yang B (2010) An Estimated DSGE Model of the Indian Economy, School of Economics Discussion Papers 1210, School of Economics, University of Surrey

Galí J, Monacelli T (2005) Monetary policy and exchange rate volatility in a small open economy. Rev Econ Stud, Oxford University Press 72(3):707–734

Gerali A, Neri S, Sessa L, Signoretti FM (2010) Credit and banking in a DSGE model of the euro area. J Money, Credit Bank, Blackwell Publ 42(s1):107–141, 09

Gertler M, Gilchrist S, Natalucci F (2007) External constraints on monetary policy and the financial accelerator, journal of money. Credit Bank 39:295–330

Gertler M, Karadi P (2011) A model of unconventional monetary policy. J Monet Econ, Elsevier 58(1):17–34

Gertler M, Kiyotaki N (2011) Financial Intermediation and Credit Policy in Business Cycle Analysis in Handbook of Monetary Economics by Benjamin M. Friedman & Michael Woodford

Gertler M, Kiyotaki N, Queralto A (2012) Financial crises, bank risk exposure and government financial policy. J Monet Econ, Elsevier 59(S):S17–S34

Gambacorta L, Signoretti FM (2014) Should monetary policy lean against the wind?. J Econ Dyn Control, Elsevier 43(C):146–174

Iacoviello M (2005) House prices, borrowing constraints, and monetary policy in the business cycle. Am Econ Rev, Am Econ Assoc 95(3):739–764

International Monetary Fund (2011a) Macroprudential Policy, An Organizing Framework (SM/11/54, March), International Monetary Fund

International Monetary Fund (2011b) Recent Experiences in Managing Capital Inflows, Cross-Cutting Themes and Possible Guidelines (February)

Jeanne O, Korinek A (2010) Managing Credit Booms and Busts: A Pigouvian Taxation Approach, NBER Working Papers 16377, National Bureau of Economic Research, Inc

Kannan P, Rabanal P, Scott A (2009) Monetary and Macroprudential Policy Rules in a Model with House Price Booms, IMF Working Papers 09/251, International Monetary Fund

Kiyotaki N, Moore J (1997) Credit cycles, journal of political economy. Univ Chic Press 105(2):211–48

Levine P, Lima D (2015) Policy mandates for macro-prudential and monetary policies in a new Keynesian framework, Working Paper Series 1784, European Central Bank

Maino R, Barnett S (2013) Macroprudential Framework in Asia, I.M.F.

Montiel P (2014) Capital Flows: Issues and Policies. Open Econ Rev, Springer 25(3):595–633

N’Diaye P (2009) Countercyclical Macro Prudential Policies in a Supporting Role to Monetary Policy. IMF Working Paper WP/09/257

Obstfeld M, Rogoff K (1995) Exchange rate dynamics redux, vol 103

Schmitt-Grohe S, Uribe M (2007) Optimal simple and implementable monetary and fiscal rules. J Monet Econ, Elsevier 54(6):1702–1725

Summer M (2003) Banking regulation and systemic risk. Open Econ Rev, Springer 14(1):43–70

Unsal DF (2013) capital flows and financial stability: monetary policy and macroprudential responses. Int J Central Bank, Int J Central Bank 9(1):233–285

Viñals J (2010) Towards a Safer Global Financial System, speech delivered at the Center For Financial Studies at the Goethe Universität, Frankfurt, November

Author information

Authors and Affiliations

Corresponding author

Additional information

This paper has benefited from insightful comments by an anonymous referee. Furthermore, we are thankful to Rahul Anand, Vivek Arora, Chikako Baba, Paul Levine, Ola Melander, Raffaele Rossi, Sarah Sanya and the seminar participants at the Asia-Pacific Department of the International Monetary Fund and at the Central Bank of Philippines for useful comments. The views expressed herein are those of the authors and should not be attributed to the IMF, its Executive Board, or its management.

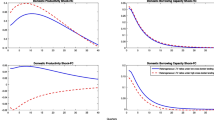

Appendix I - Optimal Coefficients of the Policy Rules Following a Technology and Government Shock

Appendix I - Optimal Coefficients of the Policy Rules Following a Technology and Government Shock

Rights and permissions

About this article

Cite this article

Ghilardi, M.F., Peiris, S.J. Capital Flows, Financial Intermediation and Macroprudential Policies. Open Econ Rev 27, 721–746 (2016). https://doi.org/10.1007/s11079-016-9389-9

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11079-016-9389-9