Abstract

Prior studies indicate that perceived health is strongly associated with a sense of well-being. The effect of health insurance is much less clear: there has been little rigorous empirical research assessing whether health coverage has an independent impact on individual happiness. This topic is especially important in the US where recently an estimated 18 % of the non-elderly were uninsured and extension of coverage through means such as the Affordable Care Act has been controversial. The present study addresses this question. Drawing from a large survey that collected comprehensive health and personal information about the US adult population, controlling for a wide variety of factors known to influence well-being, and addressing the possible endogeneity of having health insurance, we find that individuals without health insurance coverage were less likely to be “very satisfied” or “satisfied” with life. This may be because health insurance reduces uncertainty. Regardless of other benefits it may bring, the expansion of health insurance coverage should increase the life satisfaction of American society.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

For readers of this journal, it would likely come as no surprise to encounter new evidence of a major link between health and individual life satisfaction. Prior research has demonstrated that perceived good health has a consistent, strong, positive impact on happiness, even controlling for a wide variety of other variables. Indeed, one broad survey of happiness findings labels health as one of the “big seven factors” regularly shown to influence life satisfaction (Layard 2005).

Nevertheless, it is one thing to know that having good health makes people happier; it is quite another to understand whether possessing health insurance does so. Commentators regularly remind us that having health insurance and even accessing health care are not the same things as being healthy, and the connections between using services and healthiness may be more tenuous than many imagine (Weintraub 2014). The scholarly literature in this area generally supports the conclusion that health insurance coverage and good health are positively related; however, findings are by no means universal and some of these studies have major methodological issues (Hadley 2003; Gruber 2008; Kaiser Family Foundation 2013; Institute of Medicine 2003). On the other hand, perhaps it is misleading to believe that health insurance only has a positive impact on life satisfaction because it makes one happier at present. Consider the billions of dollars Americans are willing to spend to purchase health insurance, even though a great many will use very few of the benefits for which they are eligible. Might there not be reason to think that any impact of health care coverage on happiness has much to do with something we might call “peace of mind?”

Interestingly, there has been relatively little rigorous analysis of the impact of health care coverage on happiness among Americans. This is the case despite: (1) the evidence that tens of millions lack health insurance; (2) the enormous attention paid to expansion of health insurance generally in recent years, both before and after the passage of the landmark Affordable Care Act; and (3) the burgeoning empirical social science literature on the causes of life satisfaction. While there is substantial literature indicating that perceived health is associated with life satisfaction, we could locate only one study to date that focuses on the effect of health care coverage per se on happiness (Graham 2008; Sirgy 2012; Earth Institute 2012; Salinas-Jimenez et al. 2010; Layard 2005; Blanchflower 2009).

The present research focuses directly on exploring the connection between well-being and health care coverage. Our study adds depth and relevance to the existing discussion on the evaluation of the desirability of recent health care reform in the US. We accomplish this by offering the necessary background information about the uninsured in this country, summarizing the important factors known to influence individual happiness, using a large data set, and analyzing the data in the manner appropriate for isolating the impact of having health insurance.

2 What We Know About Lack of Health Insurance in the United States and Its Consequences

Efforts to provide large groups of Americans with health care coverage have long been among the largest and most well supported social programs in the US. Many view them as a fundamental component of American efforts to mitigate the insecurities inherent in market economies. By all measures (budgetary size, number of recipients, growth over recent decades, etc.), Medicare (covering adults aged 65 and over) and Medicaid (covering low-income people of different ages and characteristics) are at the core of the American social welfare system. These programs also tend to be popular with the public and elected officials. (For overviews of the social welfare system and the place of medical programs within them, see Ben-Shalom et al. 2011; Howard 2007.)

Yet despite the reach of the above-mentioned programs, especially prior to the Affordable Care Act (ACA), a great many Americans have remained without health insurance. Some figures may help put this in perspective. As of 2011, 48 million non-elderly Americans lacked health care coverage, which means more than one in six, or 18 % of the non-elderly were uninsured (DeNavas-Walt et al. 2012). The Council of Economic Advisers’ projection suggests this number would have risen to about 72 million by 2040 in the absence of health care reform (Council of Economic Advisers 2009). This large uninsured population exists despite the fact that health care spending per capita in the US is higher than in any other industrialized nation.

Concern about the large uninsured population motivated recent reform efforts to institute systematic change to the American health care system, including the ACA. On March 23, 2010, President Obama signed that legislation, representing the most significant and comprehensive health care reform in the US since the passage of Medicare and Medicaid in 1965. The expectation is that the ACA reduces the uninsured rate by over 50 % by expanding Medicaid, providing subsidized private coverage for individuals with incomes up to 400 % of the federal poverty level, and reforming the health insurance marketplace (Congressional Budget Office 2012). The Congressional Budget Office estimated that by 2022, 38 million new individuals would have health coverage, specifically 12 million through Medicaid, and 26 million through the ACA’s health insurance exchanges (Congressional Budget Office 2013).

Non-elderly adults (individuals between 18 and 64 years old) make up a disproportionate share of the American uninsured population. They are not eligible for Medicare, which is available only to seniors, and are less likely than children to be eligible for Medicaid. Over the past several years, Medicaid coverage has partially offset declining employer-sponsored insurance, but not enough to prevent continued growth in the uninsured population. Currently, employer-sponsored health insurance is the predominant source of health care and is possible only with an annual $200 billion tax subsidy from the federal government to encourage employer-sponsored health insurance (Gruber 2008).

The uninsured population is comprised mainly of the “working poor.” Minorities are much more likely to be uninsured than whites, with about 32 % of Hispanics and 21 % of African Americans uninsured, compared to 13 % of non-Hispanic whites (Kaiser Family Foundation 2012). While the majority of the uninsured population is native or naturalized US citizens, undocumented immigrants account for nearly 20 % of the uninsured and will continue to remain uninsured, as they are not eligible for federally funded health coverage under the health care reform law (Kaiser Family Foundation 2012).

2.1 Consequences of Being Uninsured

There are many negative consequences related to the lack of health insurance. Uninsured adults are almost twice as likely to report having fair or poor health compared to those with insurance, with more than a third having a chronic condition. While it is possible that at least in part poor health leads to lack of health insurance rather than the other way around, the interrelationship between the two is cause for consideration. Lack of health insurance is also associated with a 25 % higher mortality risk and the Institute of Medicine (2003) estimates it to result in more than 18,000 deaths a year in the US. National data also suggest that the uninsured are much more likely to report not having a usual source of care, delaying, and forgoing needed care due to cost (Kaiser Family Foundation 2013). Undiagnosed health problems associated with lack of insurance could cost significantly more when treated later. Uninsured individuals also have greater risk of accumulating unpaid medical bills, as nearly half of uninsured individuals are not confident they can pay for needed health care services, compared to 21 % of those with health insurance (Kaiser Family Foundation 2012).

Furthermore, lack of health insurance may also result in negative physical and financial consequences for people other than the uninsured (i.e., negative externalities). Physical externalities include communicable diseases, as uninsured individuals are less likely to receive vaccinations and care for these diseases. Financial externalities are the substantial uncompensated care when the uninsured cannot pay their medical bills and these unreimbursed costs result in higher health insurance premiums for all. Furthermore, the uninsured are more likely to forgo regular medical visits and ultimately chose the more socially expensive option of visiting a hospital emergency room when a medical condition becomes too serious to ignore. Other financial externalities include lowered productivity due to the lock-in effect of staying in less productive jobs that offer health insurance benefit, as opposed to moving to different jobs without health insurance (Gruber 2008).

Given the ACA’s recent expansion of health care coverage, preliminary surveys are indicating that it is effective at reducing the uninsured rates and improving access to care (Collins et al. 2014). Unquestionably, health care coverage has a significant impact on access to health care and health status, but will having health insurance coverage make people more satisfied with life? We turn now to what the literature suggests in answer to that question.

3 What We Know About the Factors that Influence Subjective Well-being

Most studies interchange the terms happiness, well-being, subjective well-being (SWB), and life satisfaction to describe how happy people feel and how satisfied they are with their life. As Eid and Larsen (2008) indicate, an individual with high well-being “experiences life satisfaction and frequent joy, and only infrequently experiences unpleasant emotions such as sadness or anger.” On the contrary, Eid and Larson also note that a person with low well-being is “dissatisfied with life, experiences little joy and affection and frequently feels negative emotions such as anger or anxiety.” One must recognize that happiness data are subjective self-reported measures with no specific definition or value assigned to each happiness level, such as what it means to be very happy, pretty happy, and not too happy. The underlying notion is that people have their own idea of what “happiness” and “the good life” is, and it is reasonable to infer that people are the best judges of their overall quality of life. Therefore, it is best to ask individuals directly about their own happiness and life satisfaction. Prior research shows that these measures are highly reliable and valid measurements of well-being. According to Bottan and Truglia (2011), SWB measures correlate with measures of well-being that are more objective in construction. Consistency tests indicate that recorded happiness levels have been demonstrated to correlate with objective physiological, medical and social characteristics such as heart rate and blood pressure’s response to stress, assessments of the individual’s happiness by close friends and relatives, smile authenticity, and electroencephalogram measures of prefrontal brain activity (Blanchflower and Oswald 2002; Frey and Stutzer 2001; Bottan and Truglia 2011). Well-being research scientists generally agree that subjective measures of well-being seem to measure well-being appropriately (Frey and Stutzer 2001).

We have argued there are good reasons to think that lack of health care coverage has a major detrimental impact on happiness. Yet there is also some cause for doubt. The rapidly expanding literature on the causes of variance in individual well-being indicates that many other factors influence happiness. Some factors, such as basic personality traits, are largely beyond the influence of public policy. Accordingly, absent empirical evidence, it remains possible that the impact of having health insurance is minimal or even insignificant. In the paragraphs that follow, we briefly summarize factors known to affect happiness.

3.1 Genetics and Personality

Although the present study does not focus on these factors, it is important to note that genetics and personality traits are among the most consistent and robust predictors of well-being. Lucas et al. (1996) estimated this effect to be approximately 50 % for immediate subjective well-being, and 80 % for longer-term SWB. Kahneman et al. (1999) found these traits explain approximately 20–50 % of the observed variance in long and short-term well-being among individuals. Furthermore, genes account for approximately 40 % of the variance in positive emotionality and 55 % of the variance in negative emotionality (Diener et al. 1999).

3.2 Income

Researchers have also found a significant positive correlation between income and happiness as wealthy people, on average, report higher SWB and wealthier countries are happier than poorer countries. However, Easterlin (1974) noted that while richer individuals are happier than poorer ones, over time US residents did not become happier as they became richer. Despite significant increases in real income, the average happiness level in the US had remained largely flat. Moreover, cross-country studies of happiness consistently demonstrate that after reaching a certain minimum level of per capita income, average happiness level does not increase as countries grow wealthier (Easterlin 1974). This also suggests that relative income, rather than absolute income, matters more to happiness.

3.3 Unemployment

Gross domestic product per person in a country may not be the best predictor of a nation’s well-being. Studies consistently found a substantial influence of non-financial variables on self-reported satisfaction and that non-income factors accounted for more variance in happiness than income factors (Headey and Wooden 2004; Frey and Stutzer 2001; Sharpe et al. 2010; Bottan and Truglia 2011). The unemployed were generally found to have 5–15 % lower self-reported happiness compared to those who were employed (Di Tella et al. 2002; Frey and Stutzer 2001, 2002; New Economics Foundation 2012). The effect of becoming unemployed was associated with highly significant lower levels of happiness as individuals typically required approximately two years to return to 72 % of their prior happiness levels (Bottan and Truglia 2011). More importantly, the effects of unemployment were associated with a significant rise in anxiety, depression, loss of confidence, and self-esteem occurring beyond the effects of lost income (Bok 2010; Blanchflower and Oswald 2002).

3.4 Marriage and Family

Marriage is highly correlated with increased happiness. According to Blanchflower and Oswald, the influence of marriage (as compared to being widowed or separated) on an individual’s happiness is worth the equivalent of around a $100,000 per year increase in household income (Blanchflower and Oswald 2002). In addition, Frey and Stutzer reported that the proportions of people reporting the highest happiness scores, who had no marriage partner (separated, widowed, or divorced) were respectively 15.9, 10.9 and 6.5 % points lower than compared to married individuals (Frey and Stutzer 2001). Similarly, Layard found that marriage is the second most important factor that affects individual happiness as married people are happier than those who are divorced, separated, widowed, or never have been married (Layard 2005). Overall, the positive relationship between marital status and happiness held constant in 16 of the 17 nations studied (Stack and Eshleman 1998).

3.5 Health Care Coverage and Health

Most important to this study, there is ample evidence to suggest that health has a major, independent effect on happiness. Through substantive studies across many countries, Graham found that health status correlates more strongly with happiness than any other single factor (Graham 2008). Similarly, Bok found chronic pain, sleep disorders, and depressions as the three severe and prolonged distress health conditions where public policy intervention could significantly improve happiness (Bok 2010). Most regression-based studies have found that self-reported health status strongly influences well-being. Although most researchers recognize that the causal link between health and SWB is controversial, they tend to view well-being mainly as an effect, rather than a cause in the relationship. Diener et al. (1999) and Dolan et al. (2008) found the effect of health on SWB remains substantial even after controlling for the reverse impact that SWB has on health. A meta-analysis of 104 studies concluded that objective and subjective measures of health accounted for 8–14 % of the variance in SWB (Sirgy 2012). Compared to individuals with poor health, the Earth Institute found excellent health increased an individual’s life satisfaction score by 3.45 points while good health improved the score by 2.82 points on a 10-point scale (Earth Institute 2012). Similarly, Salinas-Jimenez et al. (2010) detected the significant role of health on life satisfaction, with very good health, good health, and fair health increasing life satisfaction by 1.62, 1.09, and 0.64 points on a 10-point scale, respectively. Those with poor or fair self-rated health were 4.16 times more likely to fall in the lower quartile of happiness than those with better self-rated health (Salinas-Jimenez et al. 2010).

Yet to date and to our knowledge, only one paper has focused on the relationship between happiness and health care coverage. In this paper, Blanchflower studied the impact on happiness on not being able to see a doctor due to cost and found that the effect was extremely substantial, leading to an estimated 21 % point decrease in happiness. The magnitude of this effect was the same as the difference in happiness variance between having <$10,000 annual income and having annual income of >$75,000—or alternatively between being employed and having been unemployed for at least one year (Blanchflower 2009). Blanchflower’s study shows that not being able to see a doctor due to cost has a robust effect on happiness. However, Blanchflower did not account for the impact of perceived health itself in assessing the impact of health care coverage on happiness. Failing to include health measures leads to omitted variable bias that incorrectly leaves out health factors found to be significant in other well-being studies. This bias could compensate for the missing factors by overestimating or underestimating the effect of other factors in the regression model. Furthermore, Blanchflower did not account for the likely endogeneity of health care access to other explanatory variables included in his regression that explained differences in individual levels of happiness. This introduced another possible bias into the reported effect of being able to see a doctor on happiness.

4 Methods

The data for the present study come from the Centers for Disease Control and Prevention (CDC)’s Behavioral Risk Factor Surveillance System (BRFSS) 2010 survey (Center for Disease Control and Prevention 2010). Established in 1984, the BRFSS is the world’s largest telephone data collection program that measures behavioral risk factors in the adult population (18 years of age or older) living in households in the US. Data collected includes information pertaining to health risk behaviors, preventive health practices, and health care access. The identification and interviewing of survey participants occurred through telephone-based methods. In 2010, the BRFSS survey conducted over 425,000 phone interviews throughout the US, with a median 14 % refusal rate and a 55 % response rate.

Our initial data set consists of 451,075 observations. Of the respondents, 46 % were very satisfied with their life, 49 % were satisfied, 4 % were dissatisfied, and 1 % were very dissatisfied. This is consistent with other findings in the well-being literature as most people report being satisfied or very satisfied with their life (Frey and Stutzer 2001).

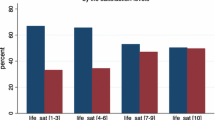

Figure 1 shows the percentage of life satisfaction for individuals aged 18–64 with and without health insurance coverage in the 2010 BRFSS survey. Relative to the survey population without health insurance, the portion of the population in the “very satisfied with life” category was 16 % points higher for those with health coverage (i.e., 48 vs. 32 %). Meantime, the percentage of those reporting being “dissatisfied” or “very dissatisfied” with life was seven points higher among those without health insurance (i.e., 9 vs. 4 %). Without controlling for the other individual factors expected to influence one’s self-reported life satisfaction, there appears to be a noticeable correlation between possessing health insurance and life satisfaction.

Health insurance coverage and life satisfaction of respondents aged 18–64, 2010

Figure 1 supports our hypothesis that health insurance coverage leads to greater life satisfaction. However, the previous literature on determinants of individual happiness suggests that there are other important drivers of self-reported differences. Thus, a more rigorous, multivariate assessment of the influence of possessing health insurance on life satisfaction must control for differences in demographics, family situation, education, economics, and health to minimize the danger of omitted variable bias when declaring that health insurance matters. Unfortunately, we must exclude genetic and personality factors from our empirical investigation because they are unavailable in the BRFSS data set. Information on a survey respondent’s possession of health insurance came from the question “Do you have any kind of health care coverage, including health insurance, prepaid plans such as HMOs, or government plans such as Medicare?” (BRFSS 2010). After dropping missing observations, the sample used for the regression analysis contained just over 360,000 observations.

The dependent variable used in our regression estimation is a dichotomous measure of the survey respondent’s self-reported life satisfaction based upon the question (Center for Disease Control and Prevention 2010): “In general, how satisfied are you with your life — very satisfied, satisfied, dissatisfied, or very dissatisfied?” Those reporting being very satisfied or satisfied with life were coded with a one (94.6 % of all survey respondents), while those dissatisfied or very dissatisfied with life were coded with a zero (5.4 % of the entire sample). Our decision to focus on this dichotomous dependent variable requires explanation, and discussion of other approaches tried. We chose this dichotomization of life satisfaction after first running an ordered probit regression (using all four possible responses) in the STATA regression package. We then assessed the validity of the latter analytical approach using the omodel command to perform a likelihood ratio test, allowing us to determine whether the explanatory variables exert a consistent influence on moving from one point to the next on the given four-point BRFSS life satisfaction scale. With high confidence (p < 0.01), this was found not to be the case. Technically this is a violation of the “parallel regression assumption” necessary to trust the results of ordered probit. Thus, we needed to instead use multinomial probit and all four of the BRFSS life-satisfaction categories (very satisfied, satisfied, dissatisfied, or very dissatisfied). Some of the findings from this analysis are discussed below. However, ultimately we opted not to fully report the multinomial probit results in the present article due to our desire to account for the simultaneous nature of the key explanatory variable No Health Insurance, and the other necessary explanatory variables included in the model as controls. Such accounting is only possible in a dichotomous probit estimation, and not a multinomial probit estimation. Thus, we felt it reasonable to dichotomize the BRFSS four-point scale between those reporting some level of satisfaction with their life set to one (very satisfied or satisfied; consisting of 94.6 % of respondents) and some level of dissatisfaction set to zero (dissatisfied or very dissatisfied; consisting of 5.4 % of respondents).

4.1 Regression Model

In simple functional form, our dichotomous regression model is:

where,

Supplemental tables A and B offer a more detailed explanation of each of the variables included in our regression model.

We strongly note that a binary outcome model designed to account for differences in self-assessments of life satisfaction (which must include measures of marital situation, education, income, employment status, and health assessment as additional explanatory variables) should account for the possibility that an individual’s health insurance status is not independent of other explanatory variables. That is, some of the same factors that determine a person’s life satisfaction may endogenously determine a person’s health insurance status. Following Cameron and Trivedi, such unaccounted for endogeneity in a regression analysis yields an inconsistent estimate of the regression coefficient calculated for the endogenous variable No Health Care Coverage (Cameron and Trivedi 2010). The estimated influence of No Health Care Coverage on Life Satisfaction from the regression analysis would therefore not be an unbiased estimator of the true effect.

As suggested in Cameron and Trivedi (2010), we account for this endogeneity through the identification of instrumental variables in the BRHSS Survey that we expect to influence the endogenous explanatory variable No Health Care Coverage, but not the dependent variable measuring Life Satisfaction. These instrumental variables are No Smoke and No Drink. No Smoke is a dummy variable that takes on a value of one if the survey respondent has smoked <100 cigarettes in her entire life. No Drink is also a dummy variable that takes on a value of one if in the last 30 days a person has consumed absolutely no form of alcoholic beverage. The respective means of these instrumental variables (No Smoke and No Drink) are 0.537 and 0.525. We include them as appropriate instruments because they represent differences in opinion among individuals as to choices regarding risk, pleasure, and health outcomes. These insights should help in the explanation of why two people with the same demographic and socio-economic characteristics would make different choices regarding the possession of health insurance. Most likely that those who choose to not smoke, or to not drink, are more likely to make the choice to purchase health insurance not provided by their employer. Importantly, we believe (as required of valid instruments) that No Smoke and No Drink exert no expected influence on one’s assessment of Life Satisfaction.

5 Results

Given the likelihood of the explanatory variable No Health Care Coverage being endogenous to the regression model described above, we choose to use probit estimation. Probit estimation, unlike logit estimation, allows for the correction of this endogeneity through an instrumental variable estimation approach (Cameron and Trivedi 2010) designated as ivregress in STATA. Thus, the results recorded here are for both the standard probit regression estimation (with no account for the expected endogeneity of No Health Care Coverage) and what we believe the more appropriate instrumental variable probit regression (which explicitly accounts for this endogeneity). Reporting both results allows the reader to see the possible regression coefficient bias that results from not accounting for the endogeneity of the health care insurance variable. As shown at the bottom of Table 1, a Wald Test of Exogeneity did indeed indicate that No Health Care Coverage is endogenous and the instrumental variable probit results are the ones to consider more valid. Furthermore, as described by Cameron and Trivedi (2010), we employ STATA’s estat command that yields a test statistic indicating that a null hypothesis of No Smoke and No Drink being weak instruments in the prediction of No Health Care Coverage can be rejected with high certainty (p < 0.01).

For our study, the critical question is the marginal impact of health care coverage on self-reported life satisfaction. As shown below, our research indicates that not having health care coverage decreases a person’s likelihood of life satisfaction by <5 % in the standard probit regression, and just >80 % in the instrumental variable probit regression (both at a highly statistically significant CI). That is, having health care coverage has an important impact on the probability that an individual will report being satisfied with life. Table 1 presents our results in terms of the percentage change in the likelihood of someone being in the very satisfied or satisfied category of self-assessed life satisfaction for all the causal factors included in the regression model (holding other causal factors constant). Note that we choose to report these marginal influence in two different ways because given the non-linear, instrumental-variable, probit estimation technique, there is no one consistent estimated influence. That is, the expected influence varies by values taken on by all of the explanatory variables in the probit regression. As noted by Cameron and Trivedi (2010), it is best to report possible multiple levels of influence depending on the values assigned to the explanatory variables. The first marginal effect, reported in bold in Table 1, is the average marginal effect (AME). It is derived by finding the marginal effects, given the specific relevant characteristics for all 300,000 plus individuals in the regression sample, and taking an average of these. The second marginal effect is diagnosed for one representative individual (MER). For this individual, we choose an age 38, high-school educated, employed, white, single, female, with children, who has no health insurance, and considers herself in fair health. Cameron and Trivedi (2010) note that such calculated marginal effects “…can differ appreciably in nonlinear models.” However, they stress that for policy analysis it is best to rely on the AME or MER specified for a relevant type of individual, which is why we report both.

What happens if we use multinomial regression? The key relationship remains. That is, the results suggest an influence on where a BRFSS survey respondent falls on the four-point life satifaction scale. The one representative individual marginal effect (MER) of No Health Insurance of reporting very satisfied with life is −2.4 %; of reporting satisfied with life is −2.0 %; of reporting dissatisfied with life is 3.1 %; and of reporting very disssatisfied with life is 1.3 %. For reasons specified previously, we only fully report the results of our analysis using the dichotomous dependent variable; more complete mutlinomial results are available from the authors upon request.

In short, the absence of health insurance is associated with greater likelihood of being dissatisfied with life regardless of how we examine the data. The relationship is evident from simple bivariate analysis. It is increasingly more apparent when using probit analysis with a wide variety of control variables. It emerges again when we attempt to remove endogneneity by substituting intrumental variables for our health insurance measure. And it is evident in multinomial regression. No matter which approach we take, health insurance matters. The exact magnitude of the influence is less certain, and varies in our research based on the method used. We readily acknowledge the need for further study of the magnitude of the relationship between health insurance and life satisfaction; however, our study underscores the conclusion that there is a statistically and substantively significant connection.

What about the impact of other explanatory variables? The standard (instrumental) variable probit regression results in Table 1 with an MER interpretation demonstrate that self-reported health status is also an important factor in individual life satisfaction, as individuals with very good to excellent health are about 15 (seven) percent more likely to be satisfied with life than those with poor health. Similarly, individuals with good health are about 13 (six) percent more likely to be satisfied with life compared to those with poor health. Along with the prominent impacts of health status, the additional predictors of income, marital status, work status, and ethnicity also influence happiness at a statistically significant level.

Using the standard probit MER interpretation (given as the second entry in the calculated marginal effects for all explanatory variables in the standard probit results in Table 2), Fig. 2 offers an illustration of the percentage change in the likelihood of being in the very satisfied or satisfied category of life satisfaction after a one-unit change in the respective causal factor.

Percentage change in likelihood of stating “Very Satisfied” or “Satisfied” as life satisfaction from a one unit change in explanatory variables using standard probit MER interpretation

While the majority of the variables found to exert a statistically significant influence returned expected results, some of the findings recorded in Table 1 were unexpected. For instance, the education and race/ethnicity variables in the standard probit regression produced unexpected signs. The regression indicates that compared to individuals who did not graduate from high school, those with higher education are less satisfied with life. Furthermore, the standard probit regression indicates that some non-whites are more satisfied with life as compared to their white counterparts. To understand better these results, we ran two additional standard probit regression results where the only explanatory variables in one accounted for differences in education, while in the other only differences in race/ethnicity were included. The results of these regressions are in the “Appendix’s Table 2” and show that in a regression with only the education variables or the race/ethnicity variables, the coefficients show the signs expected, consistent with previous studies on happiness. Table 2, column one, indicates that individuals with higher level of education are more likely to be satisfied with life. Table 2, column two, also indicates that individuals of other races/ethnicities are less satisfied with life compared to their white counterparts. However, as shown in the “Appendix’s Table 2”, column 3, when combining education and race variables with income variables, the regression produced the opposite effect (similar to those observed in this study’s regression results). This suggests that the results only appear irregularly after controlling for income. However, failing to include race and education variables found to be significant in other well-being studies would lead to omitted variable bias.

Furthermore, we explored other regression models by substituting the health insurance coverage variable with other related measures of access to health care, such as whether the participants had a personal doctor and whether they can afford a doctor. Our analysis showed these measures also had a major substantive and statistically significant impact on life satisfaction, using the same set of control variables, including perceived health. This further validates our findings that having health insurance coverage increases life satisfaction. Detailed results are available from the authors.

5.1 Limitations and Future Research

The complexity of health insurance coverage on well-being is extensive and multifaceted. Many possibilities exist for future research to explore further this aspect of well-being. Additionally, we acknowledge some limitations to our analysis. To keep the focus of the present study manageable we used one year of data from the BRFSS survey; expanding this study to include multiple years would allow for a comparison of results across time. Moreover, because we relied solely on secondary data sources for our study we were limited to the variables the survey contained. As a result, we were not able to study the effect of various types of health insurance coverage on life satisfaction. Future studies could use a different data source that includes this health insurance variable to study whether individuals having public health insurance are less satisfied with life than those receiving private health insurance. Given the known impact of genetics and personality on happiness, finding a data source that contains these measures could significantly increase the overall model fit and regression estimates. Future research should attempt to include such variables. The dichotomous grouping of survey respondents into the vast majority who reported being very satisfied and satisfied with life, as compared to the 6 % who reported being dissatisfied or very dissatisfied with life, may also help explain the large endogenous effect of an 80 % decrease in the likelihood of being in the upper-end category when individuals shift from having insurance (Not Having Health Care Coverage equal to zero) to not possessing it.

6 Discussion and Policy Implications

Our findings underscore the detrimental effect of the lack of health care coverage on life satisfaction. It is especially notable that this impact is substantial after not only controlling for factors such as income, marital status, and employment, but also after controlling for individuals’ own assessments of their overall health. That is, health insurance per se appears to increase life satisfaction. This may be because health insurance coverage reduces uncertainty. Specifically, the lack of clarity about the ability to afford needed health care can bring other psychological and financial worries as individuals can quickly exhaust their savings and incur debt in the event of required major medical procedures, given such high out of pocket costs for those without health insurance.

Our findings reinforce a principal conclusion of Graham’s (2011) studies of happiness in many countries. She concludes that despite the fact that people commonly adapt to even negative circumstances, they “seem to have trouble adapting to uncertainty… Indeed, most people seem to prefer negative certainty to uncertainty.” In the health area, this was evident in findings that “conditions such as problems with mobility had no significant or lasting well-being effects, while those associated with uncertainty—such as anxiety, pain, and epilepsy—had significant and notable effects.” Even if individuals do not get sick, the psychological and financial stress from worrying what would happen if they do can be detrimental. That is precisely what lack of health insurance threatens: the possibility that financial ruin or worse may be just around the corner.

The consequences of the lack of health insurance extend beyond the health and productivity impact on the individual since lack of health insurance directly affects their families, communities, and society. Thus, everyone shares the risks of lacking health insurance. To promote stability and avert unnecessary risks of working families living in constant fear, individuals need to be able to purchase affordable health insurance for themselves and their families. Having a venue to obtain cost-effective routine and preventive care and screenings could protect individuals from potentially detrimental but preventable health consequences that often incur costs borne largely by the public.

Consistent with findings from other well-being research, this study finds that health status is by far the most influential predictor of well-being. Having “good” to “excellent” health increases an individual’s chances of life satisfaction approximately about one and a half times greater than moving from <$10k household income to >$75k (based on results from standard probit MER interpretation). This finding emphasizes the serious need to improve health care access to advance public policy for the well-being of all Americans, which is arguably more pressing than raising the nation’s GDP. Lack of health insurance significantly decreases an individual’s access to screenings and routine preventive and acute care, which could increase the severity of illness and lead to premature death. Increased access to health care, improved health care quality and delivery are among the most effective ways to improve individuals’ health conditions and decrease disparities and inequity in access to health care. This study provides evidence that the most effective strategy to improve well-being is through improving health outcomes, thus making health a high priority policy agenda.

Most significantly, our research provides further support for the importance of expanding health insurance coverage in the US. It is beyond the scope of this paper to assess the specific approach enacted in the ACA, let alone to draw inferences for the sometimes-troubled real world implementation of the legislation. However, our research suggests that meeting the goal of the ACA—extending health insurance to millions of Americans who were previously uninsured—will most likely to increase the proportion of the population that classifies itself as being satisfied with life, regardless of any other benefits such expansion of coverage may provide. An America in which people seldom lack health insurance should be an America where many fewer are dissatisfied with life.

References

Ben-Shalom, Y., Moffitt, R. A., & Scholz, J. K. (2011). An assessment of the effectiveness of anti-poverty programs in the United States. NBER Working Paper Series. Working Paper 17042.

Blanchflower, D. (2009). Happiness and health care coverage. Institute for the Study of Labor, Discussion Paper No. 4450. http://iza.org/dp4450.pdf

Blanchflower, D., & Oswald, A. (2002). Well-being over time in Britain and the USA. Journal of Public Economics, 88(7–8), 1359–1386.

Bok, D. (2010). The politics of happiness: What government can learn from the new research on well-being. New Jersey: Princeton University Press.

Bottan, N., & Truglia, R. (2011). Deconstructing the hedonic treadmill: Is happiness autoregressive? The Journal of Socio-Economics, 40, 224–236.

Cameron, A. C., & Trivedi, P. K. (2010). Microeconomics using Stata. College Station: Stata Press.

Center for Disease Control and Prevention. (2010). Behavioral Risk Factor Surveillance System Survey Data. U.S. Department of Health and Human Services. Atlanta: Georgia. http://www.cdc.gov/brfss/annual_data/annual_2010.htm

Collins, S., Rasmussen, P., & Doty, M. (2014). Gaining ground: Americans’ health insurance coverage and access to care after the Affordable care Act’s first open enrollment period. http://www.commonwealthfund.org/~/media/files/publications/issue-brief/2014/jul/1760_collins_gaining_ground_tracking_survey.pdf

Congressional Budget Office. (2012). Estimates for the insurance coverage provisions of the Affordable Care Act updated for the recent supreme court decision. http://www.cbo.gov/sites/default/files/cbofiles/attachments/43472-07-24-2012-CoverageEstimates.pdf

Congressional Budget Office. (2013). The budget and economic outlook: fiscal years 2013 to 2023. http://www.cbo.gov/sites/default/files/cbofiles/attachments/43907_Outlook_2012-2-5_Corrected.pdf

Council of Economic Advisers. (2009). The economic case for health care reform. Executive Office of the President of the United States. http://www.whitehouse.gov/assets/documents/CEA_Health_Care_Report.pdf

DeNavas-Walt, C., Proctor, B., & Smith, J. (2012). Income, poverty, and health insurance coverage in the United States: 2011. United States Census Bureau and U.S. Department of Commerce. http://www.census.gov/prod/2012pubs/p60-243.pdf

Di Tella, R., MacCulloch, R., & Oswald, A. (2002). The macroeconomics of happiness. Journal Review of Economics and Statistics, 85(4), 809–827.

Diener, E., Suh, E., Lucas, R., & Smith, H. (1999). Subjective well-being: Three decades of progress. Psychological Bulletin, 125(2), 276–302.

Dolan, P., Peasgood, T., & White, M. (2008). Do we really know what makes us happy? A review of the economic literature on the factors associated with subjective well-being. Journal of Economic Psychology, 29, 94–122.

Earth Institute. (2012). World happiness report. Columbia University. http://www.earth.columbia.edu/sitefiles/file/Sachs%20Writing/2012/World%20Happiness%20Report.pdf

Easterlin, R. A. (1974). Does economic growth improve the human lot? Some empirical evidence. In P. A. David & M. W. Reder (Eds.), Nations and households in economic growth: essays in honor of Moses Abramowitz (pp. 89–125). New York: Academic Press.

Eid, M., & Larsen, R. (2008). The science of subjective well-being. New York: The Guillford Press.

Frey, B., & Stutzer, A. (2001). What can economists learn from happiness research? Journal of Economic Literature, 40, 402–435.

Frey, B., & Stutzer, A. (2002). Happiness & economics: How the economy and institutions affect human well-being. New Jersey: Princeton University Press.

Graham, C. (2008). Happiness and health: Lessons—And questions—For public policy. Health Affairs, 27(1), 72–87.

Graham, C. (2011). The pursuit of happiness: An economy of well-being. Washington, DC: Brookings Institution Press.

Gruber, J. (2008). Covering the Uninsured in the United States. Journal of Economic Literature, 46(3), 571–606.

Hadley, J. (2003). Sicker and poorer—The consequences of being uninsured: A review of the research on the relationship between health insurance, medical care use, health, work, and income. Medical Care Research and Review, 60(2), 3S–75S.

Headey, B., & Wooden, M. (2004). The effects of wealth and income on subjective well-being and ill-being. Institute for the Study of Labor, 1–23. http://papers.ssrn.com/sol3/papers.cfm?abstract_id=516883

Howard, C. (2007). The welfare state nobody knows: debunking myths about U.S. social policy. Princeton: Princeton University Press.

Institute of Medicine. (2003). Hidden costs, value lost: Uninsurance in America. Washington, DC: The National Academies Press.

Kahneman, D., Diener, E., & Schwarz, N. (1999). Well-being: The foundations of hedonic psychology. New York: Russell Sage Foundation.

Kaiser Family Foundation. (2012). The uninsured: A primer—Key facts about Americans without health insurance. http://www.kff.org/uninsured/upload/7451-08.pdf

Kaiser Family Foundation. (2013). The uninsured: A primer—Key facts about health insurance on the eve of health reform. http://kaiserfamilyfoundation.files.wordpress.com/2013/10/7451-09-the-uninsured-a-primer-e28093-key-facts-about-health-insurance2.pdf

Layard, R. (2005). Happiness: Lessons from a new science. New York: Penguin Books.

Lucas, R., Diener, E., & Suh, E. (1996). Discriminant validity of well-being measures. Journal of Personality and Social Psychology, 71(3), 616–628.

New Economics Foundation. (2012). Well-being evidence for policy: A review. http://www.neweconomics.org/sites/neweconomics.org/files/Well-being_Evidence_for_Policy_final.pdf

Salinas-Jimenez, M., Artes, J., & Salinas-Jimenez, J. (2010). Income, motivation, and satisfaction with life: An empirical analysis. Journal of Happiness Studies, 11(6), 779–793.

Sharpe, A., Ghanghro, A., & Johnson, E. (2010). Does money matter? Determining the happiness of Canadians. Center for the Study of Living Standards, Report No. 2010-09. http://www.csls.ca/reports/csls2010-09.pdf

Sirgy, J. (2012). The psychology of quality of life: Hedonic well-being, life satisfaction and eudaimonia. New York: Springer.

Stack, S., & Eshleman, R. (1998). Marital status and happiness: A 17-nation study. Journal of Marriage and the Family, 60(2), 527–536.

Weintraub, D. (2014). The conversation: It takes a lot more than care to keep us healthy. Sacramento Bee, April 6. http://www.sacbee.com/2014/04/06/6297168/it-takes-a-lot-more-than-care.html

Author information

Authors and Affiliations

Corresponding author

Electronic supplementary material

Below is the link to the electronic supplementary material.

Appendix

Appendix

See Table 2.

Rights and permissions

About this article

Cite this article

Tran, N.L.T., Wassmer, R.W. & Lascher, E.L. The Health Insurance and Life Satisfaction Connection. J Happiness Stud 18, 409–426 (2017). https://doi.org/10.1007/s10902-016-9729-x

Published:

Issue Date:

DOI: https://doi.org/10.1007/s10902-016-9729-x