Abstract

Green credit provides capital source to business investments that directs firms to make effective use of natural resources along with other environmental agendas such as waste management, controlling pollution, restore eco-system and conserve bio-diversity. These efforts altogether help in achieving economic and environmental sustainability and social equity. Thus, the present study aspires to combine the economic and environmental aspect of green credit on the basis of green growth and sustainability criteria. The study uses the data set over the period from 2013 to 2022 and employs DID model (difference-in-difference) to investigate the influence of green credit policy on the financing decisions of firms that heavily pollute the environment. The study finds the green credit policy has significantly reduced bank loans and non-bank loans for enterprises that heavily pollute the environment. Green credit sends policy regulation signals in capital markets and this signaling effect restrains the debt and equity financing of enterprises that heavily pollute the environment because the investors in capital markets are getting aware of risks associated with polluting enterprises under the green credit policy. Green credit policy also transmits the regulating signals to supply chain financing of firms i.e., downstream and upstream trade credit, hence, restricting the commercial trade credit of polluting firms. Finally, it is observed that green-credit policies act as efficient boosters for sustainable climate quality regulation in areas where heavily polluting enterprises operate.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Due to high emissions, various environmental problems have been emerged which is causing harm to environment and nature. Vietnam is counted in one of those nations which are affected due to climate change. Moreover, it is now in the series of economies who consumes high energy and emit higher emissions. Green development is an essential contributor as it helps in prioritizing sustainable development. Since, Vietnam has been facing pressure to reduce emissions, thereby, the country has developed carbon reduction plans (Jermsittiparsert, 2021; Ojogiwa, 2021). Among these plans, green credit is an effective one as it overcomes the shock wave of environmental issues and enhances firms’ conscientiousness in order to safeguard the environment. Through green credit policy, ecological protection is ruled and monitored by economic leverage which further can be utilized by firms to internalize pollution cost so that ex ante treatment can be attained. It is argued that commercial banks are capable of practicing capital flow via differentiated pricing that is meant to be helpful for ecological protection firms to utilize funds more effectively and promote sustainability at bigger level (Shibli et al., 2021; Wirsbinna & Grega, 2021).

Green finance via green credit is a crucial element used by financial institutions to mitigate pollution and environmental deterioration. The financial institutions are supporting the green revolution and restraining the volume of credit extended to corporations that are heavily contributing to pollution. The industrial consumption of fossil fuels has triggered ecological deterioration (Islam et al., 2022; Liang et al., 2022). Currently, damaging countries' social and economic security (Cui et al., 2022; Hao et al., 2021). Green financing as a tool to control environmental deterioration is getting the attention of policymakers, and this tool enhances climate protection and economic growth (Li & Chen, 2022). The “green credit guidelines issued in 2012” direct conventional banks to increase the cost of financing and decrease the financing scale for corporations that severely pollute the environment. The guidelines of green credit policy are beneficial in augmenting resource allocation and encouraging enterprises to take their own initiatives for environmental protection and social responsibility (Liu et al., 2017). The heavily polluting enterprises are extensively relying on external sources of financing i.e., bank loans, therefore, these enterprises can effectively adapt to green transformation via green credit policy (Li & Chen, 2022; Liu et al., 2019; Xing et al., 2021).

Recent researchers have documented the influence of green credit on enterprises that heavily pollute the environment. And these scholars infer that green credit improves the financial levels, and stock prices (Zhang et al., 2022a), while reducing the information disclosure quality (Shao et al., 2022). The other researchers infer that the two economic channels of green credit: information efficiency and information transparency help in reducing the risk of future stock price crashes (Ge & Zhu, 2022). Researchers also find that green credit helps in reducing the intensive emission of industrial carbon from extensively polluting industries (Lin & Zhang, 2023; Zhang et al., 2022b). Many other studies find that green credit overwhelming the financial ecosystem (Jiang et al., 2022), which is not beneficial for enterprises in terms of R&D-related investments (Zhang & Kong, 2022), however, green credit enhances the diversification trends (Li & Chen, 2022). Governments can adopt green transformation via the implementation of green credit guidelines to advance the climate issues initiated by high-polluting industries. It is important to inspect the influence of green-credit policy on financing alternatives of extensively polluting firms to access the efficiency and allocation of green credit policies for greener firms. The prevailing studies on financing choices are primarily focused on the debt financing of corporations. The debt-financing cost has increased due to green credit which lessens the ability of highly contaminating enterprises in the maturity of the debt financing used by these enterprises (Xu & Li, 2020). However, green credit enhances green innovations (Hu et al., 2021; Li et al., 2023).

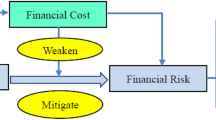

Green credit constrains the scale of bank loans, which further affects the operations and production of enterprises. To overcome such restrictions, can businesses avail alternative channels like supply chain financing or capital markets to fill this gap? Moreover, would these restraints fade the implementation impacts of green-credit? The prevailing research studies fail to exhibit the financing choices of firms under the umbrella of green-credit policy because the literature provides evidence on green credit via cash holdings and debt financing and also elaborates on the risks and financing constraints (Chai et al., 2022; Gao, 2022; Yu et al., 2023; Yuan & Gao, 2022); however, lacks a wide-ranging investigation on financing choices of enterprises. The enterprises that highly pollute the environment and pursue to adopt the green credit policy usually face difficulties to seek alternative financing modes. Firms try to expand their financing via bonds, equity, and bank loans; however, the capital markets limited the issuing threshold of (bonds and stock) enterprises. When enterprises use alternative sources of financing, it increases the intermediate and transaction costs. Moreover, the adoption of a “green credit policy” transmits a green signal to capital markets which reduce the confidence of investors to invest in enterprises that highly pollute the environment. But the green credit policies influence the commercial credit policy of enterprises, and this will lead to deficient working capital which hinders the supply of goods and the production process. This shortage of finances affects the production chain, supply chain, and capital chain of enterprises. Moreover, the account receivable and payable ratios are also affected.

Currently, Vietnam’s banking industry needs more restructuring so that the whole sector starts thinking having sustainable future rather than just snatching investments. This could be a stepping stone for Vietnamese banks because still some large banks are hesitant to break the barrier of environmental and social responsibility in credit activities (Chien et al., 2021; Hartani et al., 2021). Hence, stomping the addressed area, this paper provides evidence that green credit is crucial in signal and supply chain transmission and influences the financing of enterprises that extremely pollute the environment by utilizing bank loans. Therefore, the capital gap of the enterprises cannot be compensated by alternative financing methods. Commercial banks should restrict the financing for projects that pollute the environment and deal with enterprises with green credit policies (Sun et al., 2021, 2022). In order to respond to environmental quality, can green credit policy restrict the bank loan to enterprises that extremely pollute the environment? What is the influence of green financing on business loans from non-banking institutions? Do the guidelines of green credit have a diverse impact on different businesses? these questions are actually the inherent issues that the existing literature fails to address. Therefore, the study investigates (1) the influence of green-credit policies on loans taken from banks, (2) the influence of green credit policies on alternative financing tools like bond financing, equity financing, and commercial credit and, (3) the study explores the supply chain and signal transmission of policies regarding green finance. We contribute to the prevailing body of knowledge in the following ways, (1) the prevailing research work on enterprises’ green credit financing is based only on debt financing and ignores the overall capital mix decision of the firms (Chai et al., 2022), (2) this current research not only elaborate the influence of green credit policy on bank loans, but the study also explores the bonds, commercial credit, equity financing, and financing behavior and (3) the previous studies explore the correlation between the green-credit policies and non-bank loan, while current study explores the impact mechanism. As a non-direct association exists between green credit loans (non-bank loans), it is also essential to examine the influence of channels among them, (4) from the signal transmission and market efficiency perspectives of equity and bond financing, the current study explores the main cause of why the financing of extremely polluting firms is restrained in the capital markets, (5) from commercial credit perspective the study examines the supply chain transmission effect in two pillars operation/production and financing. We find that green credit policies confine the bank loans for extremely polluting firms as well as restrict non-bank loans, and alternative methods of financing are unable to fill the funding gaps of enterprises. We further infer that under the umbrella of green credit policy, green and low-carbon transformation becomes an unavoidable choice for enterprises that heavily pollute the environment. The paper recommends the proper adoption of green credit policy and governmental support in achieving net zero carbon economies for sustainable development of those businesses that extremely contaminate the environment. The research article is arranged as follows: the literature entails the previous pieces of evidence in the next section, while the theoretical model is constructed in the 3rd segment. Section fourth provides the empirical estimates while the conclusion, implications, and suggestions are addressed in the last section.

2 Literature review

2.1 Theoretical perspective

Embracing green and zero-carbon development mode is top priority of economies to address climate and environmental problems. Finding ways to consider to environmental issues while fixing economic growth is the most challenging situation of an era. Green credit policy is viewed as an “economic instrument”, backed up by firms’ information disclosure, to resolve environmental issues through adjusted credit structure. During the green lending process, financial institutions such as commercial banks when offer loans, show concerns about green credit policy. Currently, two contrary views regarding green credit policy implementations. The first view is related to non-executive theory which argues that “banks will not willingly follow the principles of the green credit policy because of a lack of economic incentives.” (Biswas 2011; Chien et al., 2022). This view supports the idea of profitability, hence, neglects the environmental goal because their ultimate goal is to maximize profits which can only be achieved when most of the energy-intensive firms are considered as the prime source of banks for the credit. In this case, green projects return ratio is lower as expected, hence, higher risks exist due to uncertainty. Scholars argue that when green credit guidelines are embraced consistently then there is a possibility to restrict credits to energy intensive and high polluting firms, however, it may damage financial performance of bank in the short run (Al Mamun et al., 2021; Sohail et al., 2022). Thus, financial institutions do not intend to follow green financing policies. Interestingly, there is another view that backs up executive theory. According to the view, green credit policy beholds promising opportunities for financial institutions in the longer run. Although the view agrees that in short run the outcome might be positive. However, in longer run, it has a capability to bring improvement in environmental risk management and enhance brand value. Besides, it also offers opportunities to tap into new areas which would maximize the efficiency of businesses. In addition to this, green credit policy is instrumental in nature, hence, has the power to give environmental protection and strengthen economic goals at the same time (Bouraima et al., 2021; Li et al., 2022).

2.2 Nexus of bank loans and green credit

Commercial banks use income and risk measures to estimate the value of an investment (He et al., 2019). However, pay less attention to climate disclosure for investment schemes, and consequential in the blind enlargement of enterprises that extremely pollute the climate (Cole & Elliott, 2005; Khoma & Vdovychyn, 2021). Corporate environmental performance is the first requirement of the green finance policy of 2012 for advancing loans, therefore green finance enhances the markup of loans and lessens the scale of loans for enterprises (Benfratello et al., 2008). The policy guidelines of the green finance ecosystem have changed the debt financing behavior of extremely polluting firms and transformed enterprises towards green and sustainable climate quality (Chai et al., 2022; Shi et al., 2022; Tian et al., 2022). It is further believed that the adoption of green credit policy has augmented debt-financing costs Xu and Li (2020), and equity financing costs Zhang et al. (2022b) due to information disclosure on climate financing. The previous research works focus on the adoption effects of green credit however, the literature lacks the impact of green credit policy on loans granted by banks to enterprises. The current research investigates the direct effects of green financing on bank loans and infers the following hypothesis:

Hypothesis 1

Bank loans to extremely polluting firms are restricted under the green credit policy.

2.3 Nexus of non-bank loans to green credit

Interestingly, when green credit policy restricts bank loans, enterprises can finance their business operation via commercial credit, equity financing, and other alternative methods of financing. Modigliani and Miller (1958) propose the financial sequence theory and Meltzer (1960) proposes the “Capital Rationing Theory”. These theories argue that commercial finance backs business operations when firms lack bank loans. Chai et al. (2022) investigate the “Capital Rationing Theory” and infer that reliance on commercial credit upsurges when polluting firms face restrictions on debt financing under green finance policy. When firms lack access to bank loans due to their inefficiency or due to governance issues Shahid et al. (2018), at that time equity financing is the best option to back the operations. But green credit policy imposes climate regulation restrictions on businesses and restrains them from using financing from external sources. Recently, An et al. (2021) argue firms have the option to finance through commercial credit besides equity and debt financing, but green credit policy also retrains commercial credit for firms that highly pollute the environment, however, the empirical evidence on such an argument is limited. Therefore, we propose the following hypothesis:

Hypothesis 2

Non-Bank loans to extremely polluting firms are restricted under the green credit policy.

2.4 The signaling effect of green financing

Green credit policy acts as a guiding tool and transmits the signal to investors about the environmental information of firms. So that investors can allocate their funds properly to the debt and equity of enterprises in capital markets (Chang et al., 2019; Moslehpour et al., 2023; Zhang & Qi, 2021). However, the prevailing literature lacks the impact of signal transmission about climate disclosure of green financing policy. He and Liu (2018) find that the influence of green credit policies automatically transmits to market participants but investors usually assume a public relief/welfare nature of green credit and may display a passerby attitude. But the study of the authors ignores the importance and discussion on enterprises that pollute the environment. Moreover, due to the inefficiency of Vietnam’s capital markets, the asymmetric information problem is very prominent. Green credit has changed the behavior of investors by influencing the credit decision of commercial banks by transmitting climate information into capital markets (Hussain et al., 2023; Yao et al., 2021). This transmitted signal makes the investors conscious of the risks of investing in enterprises that heavily pollute the environment (Ge & Zhu, 2022), thus these signals hinder the polluting firms to use bonds and equity financing (Eiler et al., 2015; Khattak et al., 2023). Hence, the following hypothesis is developed:

Hypothesis 3

Green credit policy transmits a signal about the environmental disclosure of firms in capital markets and hinders polluting firms to use equity and debt financing.

2.5 Supply chain transmission of green credit

Supply chain transmission of green credit infers whether green credit causes a risk to trade credit of firms and this risk transmits to the upstream (suppliers) and downstream (customers) supply chain of the enterprises that heavily pollute the environment (An et al., 2021; Huang et al., 2019). Commercial credit removes the financing constraints in the supply chain context (Chen, 2015; Chien, 2023). While it refers to advance payments and differed payments between the downstream manufacturers and upstream suppliers of the supply chain system (Chau et al., 2022; Zhou et al., 2017). Moreover, after banks, the trade commercial credit is the second largest source of financing (Wang et al., 2018). Chai et al. (2022) and Lin et al. (2022) argue that green credit hinders the commercial credit alternatives available to businesses. But the researchers fail to elaborate on how green credit replaces commercial credit to support the supply chain. When the supply chain restricts the bank loans in business operations with suppliers and buyers, the enterprises then extremely dependent on commercial credit hence, the credit risk is also transmitted to the supply chain of corporations (Bai et al., 2022; Cao et al., 2019). The suppliers and customers avoid investing in the supply chain of enterprises that heavily pollute the environment, therefore, the study postulates:

H4

Green credit policy transmits environmental disclosure and retrains the upstream and downstream supply chain commercial credit to enterprises that heavily pollute the environment.

3 Methodology and data description

In order to guide, implement and supervise the green loans, the commercial banks use the 2012 “Green Credit Guidance” which is a documented program that provides the policy implementations. The current study collects the data from listed enterprises of Vietnam over a longer period from 2013 to 2022 and constructs a DID model as guided by the “Green Credit Guidelines” of 2012 (Bertrand et al., 2004). First of all, the study inspects the effect of green credit on the choice of corporations to finance through bank-loans. The article adjusts the standard errors of OLS into different clusters i.e. time, enterprises, and industry levels.

where f indicates the industry, i exhibits the enterprises, t signifies the time, and the province is indicated by p. Bankit infers the scale of bank loan at year t for enterprise i. The intervention group (Pollution = 1) indicates the heavily polluting enterprises while (Pollution = 0) presents the control group for other enterprises. As the green credit guidelines were implemented in 2012, Post = {1, t ≥ 2012 & 0, t < 2012, Xit} is the dummy variable that represents the control variables that influence the corporate financing decisions, and these variables include the debt structure, return on assets, stock returns, equity concentration, a book to market ratio, net operating cash flows, Tobin Q and P/E ratio. The motivation to include these control variables is based on the previous studies (see Demirguc-Kunt, 1998); Lian, 2015; Su & Lian, 2018; Qi, 2019; Guo & Fang, 2022). In order to account for the influence of other climate directive strategies on provinces, an interaction is added between the provinces. Hence, province and time interaction are given by \(\delta_{{\text{p}}} \cdot \, \delta_{{\text{t}}}\), while the time and enterprise effects are represented by δt and δi respectively. Finally, the random error term is presented by εit. The variable measurement method is presented in Table 1.

The Non-credit loan tools such as pledges and mortgages are used by commercial banks in green credit products, hence the key explanatory variable in the current research work is bank loans. The study investigates how the scale of corporate external financing decisions is influenced by the inclusion of green credit policies. Based on the study of Guo and Fang (2022), we subtract the opening balance from the final balance to construct the financing method. The data is collected from the central bank of Vietnam and the ICAEW database. As for as core explanatory variables are concerned, the study includes the enterprises in the intervention group based on the previous studies which directly classify some enterprises as heavily polluting enterprises (see the studies of Shao et al., 2022; Jinliang et al., 2023; Zheng et al., 2023). However, other enterprises are affected by the green credit policy and included in the control group. The majority of enterprises lack complete information on pollution emission disclosure. Hence, the study uses industry-wise enterprise pollution emissions to obtain a large enough sample. The current study uses industrial waste gas, wastewater, dust (smoke), nitrogen gas, and sulfur dioxide emission as a single indicator of pollution. Hence, the paper utilizes the total industrial output value for emission and obtains each enterprise emission intensity. The study categorizes the heavily polluting enterprises (Intervention Group), whose average emission falls in the upper three quantiles of mean emissions. In addition to this, environmentally friendly enterprises take credit preferences from green credit policy. The control group contains the remaining enterprises and the data is collected from Vietnam Statistics Yearbook. Similar to the study of He and Liu (2018), the current research work investigates those enterprises which are involved in green business (Table 2).

4 Empirical outcomes

The influence of green credit on bank loans is presented in Table 3 with an addition of control variables in different columns. To inspect the influence of green finance policy we eliminate the influence of other related policies from industries and provinces in column 3 to alleviate the endogenous problem. We observe that policy guidelines of green finance have considerably reduced the bank loan of enterprises that highly pollute the environment, such findings validate the first hypothesis and the findings are similar to earlier research (Sadiq et al., 2023; Xu & Li, 2020; Zhang et al., 2022b). It is clear from the table that up until 2022, the year-lagged effect of the green credit policy on pollution is inverse. It is clear that after the issuance of guidelines of “green credit policy in 2012”, these guidelines have a sustainable influence on reducing pollution as the coefficient is negative up to 10 lags.

Enterprises seek alternative financing approaches to support their operations and production because the green credit confines the bank loan for corporations that heavily pollute the environment. The stimulus effect of green credit on “non-bank loans” and external financing is exhibited in the first two columns of Table 4. The negative coefficients show that both the non-bank loans and external financing are significantly reduced for enterprises that heavily contribute to pollution. Hence, Hypothesis 2 is validated because green credit adversely influences the alternative methods of financing for highly contaminating firms. Moreover, the scale of both debt and equity financing also significantly decreases for highly polluting enterprises (see columns 3 & 4). Because these firms are unable to attract capital funding from capital markets under the presence of green financial policies and findings are similar to the research work by (Vu et al., 2023; Wang & Zhu, 2017).

The green credit signaling effect and capital market efficiency are also explained in this paper. The Vietnam markets are semi-strong form efficient as the transaction information is not fully reflected by these markets. There are also some corresponding thresholds for profitability and use of funds for corporations in Vietnam markets. Under such restraints, the increase in funds through securities (bond & stock) will result in an increase in financing costs and hinder the heavily polluting corporations from increasing the financing scale. Hence, the study investigates the cost of issuance of additional stock (addition), cost of allotment (allotment), and cost of convertible bonds (convertible) to examine whether these costs hinder the financing of enterprises that contribute to pollution. It is clear from Table 5 that terms are significant and negative for (Pollution × Post × c. Addition) and (pollution × Post × c. Convertible). Hence, a positive moderating effect is played by the issuance of bonds and stock. The effectiveness of the capital market in terms of issuance and allotment cost restricts the bond and equity financing in extremely polluting enterprises under the guidelines of green credit facilities. We incorporate the signaling effect of green credit policy which transmits a signal to market participants in financial markets and investors realize the higher environmental risks while investing in heavily polluting enterprises. This type of signal transmission reduces the confidence and activities of investors in the capital markets (Yao et al., 2020). We measure the investors’ confidence using the rate of stock turnover. Table 6 reveals a significant and negative coefficient in column 2, which shows that green credit efficiently sends a signal to investors to withdraw investments from heavily polluting enterprises to other firms or in other alternative investments (Shahid et al., 2023; Shahid, 2022) and imposes a barrier on high-polluting enterprises in accessing financing from capital markets. Hypothesis 3 is validated in Tables 5 and 6.

Vietnam has no particularly sound financial system as the high cost of commercial loans supports the economy of Vietnam. Apart from bank loans, and equity and debt financing, the corporation can raise funding from financial leasing and commercial credit. Table 7 via columns 1 and 2, reveals that the coefficient of financial leasing is inverse and insignificant, on the other hand, level of commercial credit considerably drops under the policy of green credit. This shows that highly polluting firms cannot use alternative financing via financial lease and commercial credit and under the guidelines of the green finance policy (Zhang et al., 2023a, 2023b).

The paper also explains the causes of decrease in commercial credit when the green credit policy transmits its effects in supply-chain of enterprises. The sales, purchases, and borrowing of goods and services form the commercial credit of enterprises are affected under green credit policy. However, business production and operations get blocked under the policy of green-credit which impacts the buying and selling of products. The restricted funding through commercial credit providers initiates the credit and environmental risks for extremely polluting corporations. Hence, the green credit shreds both the supply chain and signaling effects on the highly polluting firms by diminishing the supply of trade credit. The negative coefficients of Table 7 (see 2nd & 4th columns) reveal that both upstream (suppliers) and downstream (customers) trade credit have dimmish under the policy of green-credit. As the green finance guidelines restrict the commercial credit of businesses, therefore, the green finance policy rises the operational risk of enterprises because the supply chain is dependent on commercial credit (Bastos & Pindado, 2013). Based on the study of (Wang & Zhu, 2017), the current study computes the net operational risk of the corporation. The negative coefficients in column 5 indicate that the operational risk of extremely polluting firms is very high under the policy of green credit (see Table 7), this causes the corporations to act as a supplier of funds in the supply chain and results in lower commercial credit. Hence, the green credit policy puts a transmission effect on capital allocation, operations, and production in the supply chain, and this effect influences the upstream and downstream of trade credit and verifies hypothesis 4. The findings are similar to the outcomes of prevailing research, for example, the studies infer green credit affects equity financing (Zheng et al., 2023), and reduces commercial credit (An et al., 2021; Campello et al., 2011; Chetty et al., 2009; Ferrara et al., 2012).

5 Conclusions

The Vietnam economy is gradually sustaining its growth in the recent two years; however, this growth is constrained by decreasing environmental quality, resources, and energy. Moreover, the contradiction between sustainable socioeconomic development and environmental pollution is getting prominent. Promoting the quality of economic advancements and green transformation is urgently required by the highly polluting enterprises to cope with the 2020 dual carbon goal. Green credit simultaneously facilitates financial backing and climate quality by appropriately adjusting the credit resources and changing the financial mix of enterprises that extremely pollute the environment. The current study investigates the influence of green credit policy on financing options of corporate that heavily pollute the environment. Over the period from 2013 to 2022, we find a significant reduction in bank loans advanced by extremely polluting enterprises. It is further identified in the current study that the implementation of green credit policy has significantly decreased the financing of highly polluting firms because green credit effectively allocates the funds to enterprises that extremely pollute the environment.

5.1 Implications

The finding of the study has a few practical implications; 1) the government should encourage commercial banks to introduce green credit products, boost the green credit balance, and guide transformation to polluting firms, 2) as the capital markets of Vietnam are weak and semi-strong form efficient, therefore the investors can easily be motivated towards a green credit policy by moving their investments from extremely polluting firms to other firms.

The study also infers that the green credit policy spreads a signal of sustainable environmental quality, therefore, restricts the heavily polluting firms from financing through capital markets in the form of bonds and stocks. From the perspective of supply chain transmission, green credit can spread trade credit to downstream (customers) and upstream (suppliers) of enterprises, hence, restricting the heavily polluting firms from traditional commercial trade credit. Finally, it is observed that a green credit policy provides an efficient supplement for sustainable climate quality regulation in areas where heavily polluting enterprises operate.

The study also infers the idea that with the help of green credit policy, it would not become easier for heavily polluting firms to get further credit support and fine interest rates which eventually makes it more difficult to get funds for technology and innovation. Besides, green credit policy implementation comes up with more restrictions from commercial banks for enterprises which are heavily polluted. This stimulates firms to enhance their commercial credit in place of debt financing. It is also confirmed from findings that there is a need of improvement in green credit policy to eco-friendly firms. This could happen when there exists a refined green patent standardization and clear technical cope in order to guide the funds flow towards green transition of high polluting firms. Moreover, due to heterogenous aspects of countries and organizations, green credit policy shouldn’t be one size fits all. It is also advised that relevant areas of firms must be united to offer plausible support to green credit policies so that transparent and fair governance can be obtained. Lastly, government institutions must establish green social environment in order to show support toward policy system while shaping green credit policy. For that, there is a need to expand finance sources for green innovation and enhance investment resources so that high polluting and energy intensive firms can be transformed in to green enterprises without any financial constraint.

5.2 Limitations and future directions

The study has a few limitations: (1) the study investigates the impact of green credit guidelines on financing decisions of polluting firms while ignoring the other firms from those industries that partially adopted the green credit policy and still polluting the environment, (2) we conduct the analysis on an industry level pollution data due to non-availability of firm-level pollution data in Vietnam, which may lead towards the problem of selection biases. Furthermore, future research may conduct analyses before the implementation of the green credit policy 2012 and after its implementation. The Impact of the policy may be investigated under different sub-sample periods introduced by (Shahid et al., 2022; Shahid, 2019; Shahid & Sattar, 2017), but we rest the future researchers to address these issues.

Data availability

The data that support the findings of this study are available in the manuscript.

References

Al Mamun, A., Muniady, R., & Nasir, N. A. B. M. (2021). Effect of participation in development initiatives on competitive advantages, performance, and sustainability of micro-enterprises in Malaysia. Contemporary Economics, 15(2), 122–138.

An, S., Li, B., Song, D., & Chen, X. (2021). Green credit financing versus trade credit financing in a supply chain with carbon emission limits. European Journal of Operational Research, 292(1), 125–142. https://doi.org/10.1016/j.ejor.2020.10.025

Bai, X., Wang, K. T., Tran, T. K., Sadiq, M., Trung, L. M., & Khudoykulov, K. (2022). Measuring China’s green economic recovery and energy environment sustainability: Econometric analysis of sustainable development goals. Economic Analysis and Policy. https://doi.org/10.1016/j.eap.2022.07.005

Bastos, R., & Pindado, J. (2013). Trade credit during a financial crisis: A panel data analysis. Journal of Business Research, 66(5), 614–620. https://doi.org/10.1016/j.jbusres.2012.03.015

Benfratello, L., Schiantarelli, F., & Sembenelli, A. (2008). Banks and innovation: Microeconometric evidence on Italian firms. Journal of Financial Economics, 90(2), 197–217. https://doi.org/10.1016/j.jfineco.2008.01.001

Bertrand, M., Duflo, E., & Mullainathan, S. (2004). How much should we trust differences-in-differences estimates? The Quarterly Journal of Economics, 119(1), 249–275.

Bouraima, M. B., Stević, Ž, Tanackov, I., & Qiu, Y. (2021). Assessing the performance of Sub-Saharan African (SSA) railways based on an integrated Entropy-MARCOS approach. Operational Research in Engineering Sciences: Theory and Applications, 4(2), 13–35.

Campello, M., Giambona, E., Graham, J. R., & Harvey, C. R. (2011). Liquidity management and corporate investment during a financial crisis. The Review of Financial Studies, 24(6), 1944–1979. https://doi.org/10.1093/rfs/hhq131

Cao, E., Du, L., & Ruan, J. (2019). Lingxia Du and Junhu Ruan, “Financing preferences and performance for an emission-dependent supply chain: Supplier vs. bank.” International Journal of Production Economics, 208, 383–399. https://doi.org/10.1016/j.ijpe.2018.08.001

Chai, S., Zhang, K., Wei, W., Ma, W., & Abedin, M. Z. (2022). The impact of green credit policy on enterprises’ financing behavior: Evidence from Chinese heavily-polluting listed companies. Journal of Cleaner Production, 363, 132458. https://doi.org/10.1016/j.jclepro.2022.132458

Chang, K., Zeng, Y., Wang, W., & Wu, X. (2019). The effects of credit policy and financial constraints on tangible and research & development investment: Firm-level evidence from China’s renewable energy industry. Energy Policy, 130, 438–447. https://doi.org/10.1016/j.enpol.2019.04.005

Chau, K. Y., Lin, C. H., Tufail, B., Tran, T. K., Van, L., & Nguyen, T. T. H. (2022). Impact of eco-innovation and sustainable tourism growth on the environmental degradation: The case of China. Economic Research-Ekonomska Istraživanja. https://doi.org/10.1080/1331677X.2022.2150258

Chen, X. (2015). A model of trade credit in a capital-constrained distribution channel. International Journal of Production Economics, 159, 347–357. https://doi.org/10.1016/j.ijpe.2014.05.001

Chetty, R., Looney, A., & Kroft, K. (2009). Salience and taxation: Theory and evidence. American Economic Review, 99(4), 1145–1177. https://doi.org/10.1257/aer.99.4.1145

Chien, F. (2023). The impact of green investment, eco-innovation, and financial inclusion on sustainable development: Evidence from China. Engineering Economics, 34(1), 17–31.

Chien, F., Ajaz, T., Andlib, Z., Chau, K. Y., Ahmad, P., & Sharif, A. (2021). The role of technology innovation, renewable energy and globalization in reducing environmental degradation in Pakistan: A step towards sustainable environment. Renewable Energy, 177, 308–317.

Chien, F., Hsu, C. C., Andlib, Z., Shah, M. I., Ajaz, T., & Genie, M. G. (2022). The role of solar energy and eco-innovation in reducing environmental degradation in China: Evidence from QARDL approach. Integrated Environmental Assessment and Management, 18(2), 555–571.

Cole, M. A., & Elliott, R. J. (2005). FDI and the capital intensity of “dirty” sectors: a missing piece of the pollution haven puzzle. Review of Development Economics, 9(4), 530–548. https://doi.org/10.1111/j.1467-9361.2005.00292.x

Cui, X., Wang, P., Sensoy, A., Nguyen, D. K., & Pan, Y. (2022). Green credit policy and corporate productivity: Evidence from a quasi-natural experiment in China. Technological Forecasting and Social Change, 177, 121516. https://doi.org/10.1016/j.techfore.2022.121516

Demirguc-Kunt, A., & Maksimovic, V. (1998). Law, finance, and firm growth. The Journal of Finance, 53(6), 2107–2137. https://doi.org/10.1111/0022-1082.00084

Eiler, L. A., Miranda-Lopez, J., & Tama-Sweet, I. (2015). The impact of accounting disclosures and the regulatory environment on the information content of earnings announcements. The International Journal of Accounting, 50(2), 142–169.

Ferrara, E. L., Chong, A., & Duryea, S. (2012). Soap operas and fertility: Evidence from Brazil. American Economic Journal: Applied Economics, 4(4), 1–31. https://doi.org/10.1257/app.4.4.1

Gao, Y. (2022). Green credit policy and trade credit: Evidence from a quasi-natural experiment. Finance Research Letters, 50, 103301. https://doi.org/10.1016/j.frl.2022.103301

Ge, Y., & Zhu, Y. (2022). Boosting green recovery: Green credit policy in heavily polluted industries and stock price crash risk. Resources Policy, 79, 103058. https://doi.org/10.1016/j.resourpol.2022.103058

Guo, J., & Fang, Y. (2022). Green credit, financing structure and enterprise environmental investment. The Journal of World Economy., 45(8), 57–80. https://doi.org/10.19985/j.cnki.cassjwe.2022.08.008

Hao, Y., Ba, N., Ren, S., & Wu, H. (2021). How does international technology spillover affect China’s carbon emissions? A new perspective through intellectual property protection. Sustainable Production and Consumption, 25, 577–590. https://doi.org/10.1016/j.spc.2020.12.008

Hartani, N. H., Haron, N., & Tajuddin, N. I. I. (2021). The impact of strategic alignment on the sustainable competitive advantages: Mediating role of it implementation success and it managerial resource. International Journal of eBusiness and eGovernment Studies, 13(1), 78–96.

He, L. Y., & Liu, L. (2018). Stand by or follow? Responsibility diffusion effects and green credit. Emerging Markets Finance and Trade, 54(8), 1740–1760. https://doi.org/10.1080/1540496X.2018.1430566

He, L., Zhang, L., Zhong, Z., Wang, D., & Wang, F. (2019). Green credit, renewable energy investment and green economy development: Empirical analysis based on 150 listed companies of China. Journal of Cleaner Production, 208, 363–372. https://doi.org/10.1016/j.jclepro.2018.10.119

Hu, G., Wang, X., & Wang, Y. (2021). Can the green credit policy stimulate green innovation in heavily polluting enterprises? Evidence from a quasi-natural experiment in China. Energy Economics, 98, 105134. https://doi.org/10.1016/j.eneco.2021.105134

Huang, L., Ying, Q., Yang, S., & Hassan, H. (2019). Trade credit financing and sustainable growth of firms: Empirical evidence from China. Sustainability, 11(4), 1032. https://doi.org/10.3390/su11041032.Article1032

Hussain, H. I., Kamarudin, F., Anwar, N. A. M., Ali, M., Turner, J. J., & Somasundram, S. A. (2023). Does income inequality influence the role of a sharing economy in promoting sustainable economic growth? Fresh evidence from emerging markets. Journal of Innovation & Knowledge, 8(2), 100348.

Islam, M. M., Irfan, M., Shahbaz, M., & Vo, X. V. (2022). Renewable and non-renewable energy consumption in Bangladesh: The relative influencing profiles of economic factors, urbanization, physical infrastructure and institutional quality. Renewable Energy, 184, 1130–1149. https://doi.org/10.1016/j.renene.2021.12.020

Jermsittiparsert, K. (2021). Linkage between energy consumption, natural environment pollution, and public health dynamics in ASEAN. International Journal of Economics and Finance Studies, 13(2), 1–21.

Jiang, P., Jiang, H., & Wu, J. (2022). Is inhibition of financialization the sub-effect of the green credit policy? Evidence from China. Finance Research Letters, 47, 102737. https://doi.org/10.1016/j.frl.2022.102737

Jinliang, W., Chau, K. Y., Baei, F., Moslehpour, M., Nguyen, K. L., & Nguyen, T. T. H. (2023). Integrated perspective of eco-innovation, green branding, and sustainable product: a case of an emerging economy. Economic Research-Ekonomska Istraživanja, 36(3), 2196690.

Khattak, M. A., Ali, M., Azmi, W., & Rizvi, S. A. R. (2023). Digital transformation, diversification and stability: What do we know about banks? Economic Analysis and Policy, 78, 122–132.

Khoma, N., & Vdovychyn, I. (2021). Universal basic income as a form of social contract: Assessment of the prospects of institutionalisation. Przestrzeń Społeczna, 1(1/2021 (21)).

Li, R., & Chen, Y. (2022). The influence of a green credit policy on the transformation and upgrading of heavily polluting enterprises: A diversification perspective. Economic Analysis and Policy, 74, 539–552. https://doi.org/10.1016/j.eap.2022.03.009

Li, X., Ozturk, I., Ullah, S., Andlib, Z., & Hafeez, M. (2022). Can top-pollutant economies shift some burden through insurance sector development for sustainable development? Economic Analysis and Policy, 74, 326–336.

Li, L., Qiu, L., Xu, F., & Zheng, X. (2023). The impact of green credit on firms’ green investment efficiency: Evidence from China. Pacific-Basin Finance Journal, 79, 101995. https://doi.org/10.1016/j.pacfin.2023.101995

Lian, L. (2015). Does green credit affect the cost of debt financing—Comparative study on green enterprises and “two high” enterprises. Res. Financ. Econ, 30, 83–93.

Liang, J., Irfan, M., Ikram, M., & Zimon, D. (2022). Evaluating natural resources volatility in an emerging economy: The influence of solar energy development barriers. Resources Policy, 78, 102858. https://doi.org/10.1016/j.resourpol.2022.102858.Article102858

Lin, B., & Zhang, A. (2023). Can government environmental regulation promote low-carbon development in heavy polluting industries? Evidence from China’s new environmental protection law. Environmental Impact Assessment Review, 99, 106991. https://doi.org/10.1016/j.eiar.2022.106991

Lin, C. Y., Chau, K. Y., Tran, T. K., Sadiq, M., Van, L., & Phan, T. T. H. (2022). Development of renewable energy resources by green finance, volatility and risk: Empirical evidence from China. Renewable Energy. https://doi.org/10.1016/j.renene.2022.10.086

Liu, J. Y., Xia, Y., Fan, Y., Lin, S. M., & Wu, J. (2017). Assessment of a green credit policy aimed at energy-intensive industries in China based on a financial CGE model. Journal of Cleaner Production, 163, 293–302. https://doi.org/10.1016/j.jclepro.2015.10.111

Liu, X., Wang, E., & Cai, D. (2019). Green credit policy, property rights and debt financing: Quasi-natural experimental evidence from China. Finance Research Letters, 29, 129–135. https://doi.org/10.1016/j.frl.2019.03.014

Meltzer, A. H. (1960). Mercantile credit, monetary policy, and size of firms. The Review of Economics and Statistics, 42(4), 429–437.

Modigliani, F., & Miller, M. H. (1958). The cost of capital, corporation finance and the theory of investment. The American Economic Review, 48(3), 261–297.

Moslehpour, M., Aldeehani, T. M., Sibghatullah, A., Tai, T. D., Phan, T. T. H., & Ngo, T. Q. (2023). Dynamic association between technological advancement, green finance, energy efficiency and sustainable development: evidence from Vietnam. Economic Research-Ekonomska Istraživanja, 36(3), 2190796.

Ojogiwa, O. T. (2021). The crux of strategic leadership for a transformed public sector management in Nigeria. International Journal of Business and Management Studies, 13(1), 83–96.

Qi, C. (2019). Has China’s green credit policy been implemented? An analysis of loan scale and costs based on “Two Highs and One Surplus” enterprises. Contemporary Finance & Economics, 03, 1.

Sadiq, M., Moslehpour, M., Qiu, R., Hieu, V. M., Duong, K. D., & Ngo, T. Q. (2023). Sharing economy benefits and sustainable development goals: Empirical evidence from the transportation industry of Vietnam. Journal of Innovation & Knowledge. https://doi.org/10.1016/j.jik.2022.100290

Shahid, M. N. (2022). COVID-19 and adaptive behavior of returns: evidence from commodity markets. Humanities and Social Sciences Communications, 9(1), 1–15.

Shahid, M. N., & Sattar, A. (2017). Behavior of calendar anomalies, market conditions and adaptive market hypothesis: Evidence from Pakistan stock exchange. Pakistan Journal of Commerce and Social Sciences (PJCSS), 11(2), 471–504.

Shahid, M. N., Siddiqui, M. A., Qureshi, M. H., & Ahmad, F. (2018). Corporate governance and its impact on firm’s performance: Evidence from cement industry of Pakistan. Journal of Applied Environmental and Biological Sciences, 8(1), 35–41.

Shahid, M. N., Islam, M. U., Alam, N., & Ali, M. (2022). Time-Varying Return Predictability and Adaptive Behavior in The US Commodity Markets During COVID-19. International Journal of Economics & Management, 16, 59–80.

Shahid, M. N., Azmi, W., Ali, M., Islam, M. U., & Rizvi, S. A. R. (2023). Uncovering risk transmission between socially responsible investments, alternative energy investments and the implied volatility of major commodities. Energy Economics, 120, 106634.

Shahid, M. N. (2019). Behavior of Stock Return, Calendar Effects and Adaptive Market Hypothesis (AHM): Evidence from Pakistan by Using Historic data with Special Focus on Gregorian and Islamic Calendar. Ph.D. Thesis

Shao, H., Wang, Y., Wang, Y., & Li, Y. (2022). Green credit policy and stock price crash risk of heavily polluting enterprises: Evidence from China. Economic Analysis and Policy, 75, 271–287. https://doi.org/10.1016/j.eap.2022.05.007

Shi, J., Yu, C., Li, Y., & Wang, T. (2022). Does green financial policy affect debt-financing cost of heavy-polluting enterprises? An empirical evidence based on Chinese pilot zones for green finance reform and innovations. Technological Forecasting and Social Change, 179, 121678. https://doi.org/10.1016/j.techfore.2022.121678

Shibli, R., Saifan, S., Ab Yajid, M. S., & Khatibi, A. (2021). Mediating Role of Entrepreneurial Marketing Between Green Marketing and Green Management in Predicting Sustainable Performance in Malaysia’s Organic Agriculture Sector. AgBioforum, 23(2), 37–49.

Sohail, M. T., Majeed, M. T., Shaikh, P. A., & Andlib, Z. (2022). Environmental costs of political instability in Pakistan: policy options for clean energy consumption and environment. Environmental Science and Pollution Research, 29, 25184–25193.

Su, D. W., & Lian, L. L. (2018). Does green credit affect the investment and financing behavior of heavily polluting enterprises. J. Financial Research, 12, 123–137.

Sun, Y., Yesilada, F., Andlib, Z., & Ajaz, T. (2021). The role of eco-innovation and globalization towards carbon neutrality in the USA. Journal of Environmental Management, 299, 113568.

Sun, Y., Li, H., Andlib, Z., & Genie, M. G. (2022). How do renewable energy and urbanization cause carbon emissions? Evidence from advanced panel estimation techniques. Renewable Energy, 185, 996–1005.

Tian, C., Li, X., Xiao, L., & Zhu, B. (2022). Exploring the impact of green credit policy on green transformation of heavy polluting industries. Journal of Cleaner Production, 335, 130257. https://doi.org/10.1016/j.jclepro.2021.130257

Vu, T. L., Paramaiah, C., Tufail, B., Nawaz, M. A., Xuyen, N. T. M., & Huy, P. Q. (2023). Effect of financial inclusion, eco-innovation, globalization, and sustainable economic growth on ecological footprint. Engineering Economics, 34(1), 46–60.

Wang, K., Zhao, R., & Peng, J. (2018). Trade credit contracting under asymmetric credit default risk: Screening, checking or insurance. European Journal of Operational Research, 266(2), 554–568. https://doi.org/10.1016/j.ejor.2017.10.004

Wang, L., & Zhu, Y. (2017). Green credit policy and the maturity of corporate debt. In Proceedings of the Tenth International Conference on Management Science and Engineering Management (pp. 1709–1717). Springer Singapore.

Wirsbinna, A., & Grega, L. (2021). Assessment of economic benefits of smart city initiatives. Cuadernos De Economía, 44(126), 45–56.

Xing, C., Zhang, Y., & Tripe, D. (2021). Green credit policy and corporate access to bank loans in China: The role of environmental disclosure and green innovation. International Review of Financial Analysis, 77, 101838. https://doi.org/10.1016/j.irfa.2021.101838

Xu, X., & Li, J. (2020). Asymmetric impacts of the policy and development of green credit on the debt financing cost and maturity of different types of enterprises in China. Journal of Cleaner Production, 264, 121574. https://doi.org/10.1016/j.jclepro.2020.121574

Yao, W., Zhang, L., & Hu, J. (2020). Does having a semimandatory dividend policy enhance investor confidence? Research on Dividend-Financing Behavior. Economic Systems, 44(4), 100812.

Yao, S., Pan, Y., Sensoy, A., Uddin, G. S., & Cheng, F. (2021). Green credit policy and firm performance: What we learn from China. Energy Economics, 101, 105415.

Yu, C., Moslehpour, M., Tran, T. K., Trung, L. M., Ou, J. P., & Tien, N. H. (2023). Impact of non-renewable energy and natural resources on economic recovery: Empirical evidence from selected developing economies. Resources Policy, 80, 103221.

Yuan, N., & Gao, Y. (2022). Does green credit policy impact corporate cash holdings? Pacific-Basin Finance Journal, 75, 101850. https://doi.org/10.1016/j.pacfin.2022.101850

Zhang, D., & Kong, Q. (2022). Credit policy, uncertainty, and firm R&D investment: A quasi-natural experiment based on the Green Credit Guidelines. Pacific-Basin Finance Journal, 73, 101751. https://doi.org/10.1016/j.pacfin.2022.101751

Zhang, B., & Qi, R. (2021). Transportation infrastructure, innovation capability, and urban economic development. Transformations in Business & Economics, 20, 526–545.

Zhang, A., Deng, R., & Wu, Y. (2022a). Does the green credit policy reduce the carbon emission intensity of heavily polluting industries?Evidence from China’s industrial sectors. Journal of Environmental Management, 311, 114815. https://doi.org/10.1016/j.jenvman.2022.114815

Zhang, M., Zhang, X., Song, Y., & Zhu, J. (2022b). Exploring the impact of green credit policies on corporate financing costs based on the data of Chinese A-share listed companies from 2008 to 2019. Journal of Cleaner Production, 375, 134012. https://doi.org/10.1016/j.jclepro.2022.134012

Zhang, M., Wang, A., & Zhou, S. (2023a). Effect of analysts’ earnings pressure on environmental information disclosure of firms: Can corporate governance alleviate the earnings obsession? Borsa Istanbul Review, 23(2), 495–515. https://doi.org/10.1016/j.bir.2022.12.001

Zhang, Y., Li, L., Sadiq, M., & Chien, F. (2023b). The impact of non-renewable energy production and energy usage on carbon emissions: Evidence from China. Energy & Environment. https://doi.org/10.1177/0958305X221150432

Zhang, Y., Li, L., Sadiq, M., & Chien, F. S. (2023c). Impact of a sharing economy on sustainable development and energy efficiency: Evidence from the top ten Asian economies. Journal of Innovation & Knowledge. https://doi.org/10.1016/j.jik.2023.100320

Zheng, S., Zhang, X., & Wang, H. (2023). Green credit policy and the stock price synchronicity of heavily polluting enterprises. Economic Analysis and Policy, 77, 251–264. https://doi.org/10.1016/j.eap.2022.11.011

Zhou, Y. W., Cao, B., Zhong, Y., & Wu, Y. (2017). Optimal advertising/ordering policy and finance mode selection for a capital-constrained retailer with stochastic demand. Journal of the Operational Research Society, 68, 1620–1632. https://doi.org/10.1057/s41274-016-0161-8

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

It is declared that there is no conflict of interest.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Chen, CW., Zheng, J., Chang, TC. et al. Green finance policy and heavy pollution enterprises: a supply-chain and signal transmission of green credit policy for the environment—Vietnam perspective. Environ Dev Sustain (2023). https://doi.org/10.1007/s10668-023-03967-7

Received:

Accepted:

Published:

DOI: https://doi.org/10.1007/s10668-023-03967-7