Abstract

We study gross domestic product (GDP) model utilizing Atangana–Baleanu, Caputo–Fabrizio and Caputo fractional derivatives under the light of real data of the United Kingdom given by World Bank (World development indicators, 2018) between years 1972–2007. We obtain analytical solutions of fractional models by using Laplace transform. We compare the GDP results obtained for different fractional derivatives with real data by simulations and tables with statistical analysis showing the efficiency of fractional models to the integer-order counterpart employing error sum of squares and residual sum of squares.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

Fractional analysis has led up to born a new ground in applied mathematics, physics, engineering and economy. That case has caused to be a popular subject in recent years. We can observe it in real-world modeling problems. Nevertheless, it has a few disadvantages. One of them is that fractional derivative of a constant is different from zero in Riemann–Liouville definition, and in this case, initial conditions are of fractional order in initial value problems IVPs. It was defined to overcome that problem with the help of Liouville–Caputo definition. Liouville–Caputo fractional derivative of a constant is zero, and so it has initial conditions of integer-order in IVPs. Riemann–Liouville and Liouville–Caputo fractional derivative definitions have singularity in its kernels, so this case sometimes causes important drawbacks in modeling problems. As a solution to that, Caputo and Fabrizio (2015) defined a new fractional derivative definition having non-singularity, by means of exponential function in its kernel. As a generalization of this new definition, Atangana and Baleanu (2016) gave a new fractional definition including Mittag–Leffler kernel.

Some modeling problems with Caputo–Fabrizio fractional derivative are studied by Gómez-Aguilar et al. (2016), Atangana and Baleanu (2017), Alsaedi et al. (2016), Jarad et al. (2017), Uğurlu et al. (2018), Owolabi and Atangana (2017), Atangana and Alqahtani (2016), Al-Refai and Abdeljawad (2017). Also, many scientists study modeling problems with Atangana–Baleanu fractional derivative Sun et al. (2017), Abdeljawad and Baleanu (2017b), Abdeljawad and Baleanu (2017a), Abdeljawad (2017), Gómez-Aguilar et al. (2017), Gómez-Aguilar and Atangana (2017), Yavuz et al. (2018). Various fractional modeling problems are studied by Atangana and Koca (2016), Kanth and Garg (2018), Almeida et al. (2016), Varalta et al. (2014), Kuroda et al. (2017), Chen (2008), Ozarslan et al. (2019), Bas (2015), Bas and Ozarslan (2019), Bas et al. (2019).

GDP shows the economic growth and production of a nation. It is used to determine the economic standard of living of a country. GDP enables to be evaluated increase or decrease in the percentage of economic output in various periods.

GDP model is used to specify the growth rate of a country’s economy and defined in two ways as linear and exponential,

In this study, we consider the GDP model by Atangana–Baleanu, Caputo–Fabrizio and Caputo fractional derivatives with real data of the United Kingdom given by World Bank (2018) between years 1972–2007, and we compare the results obtained with those fractional derivatives with real data by simulations and tables with statistical evaluations. Analytical solutions are obtained by Laplace transform, and results are simulated by figures and tables for showing the efficiency of fractional models relative to the integer model.

2 Preliminaries

Definition 1

(Caputo and Fabrizio 2015) Caputo–Fabrizio fractional derivatives are defined as follows;

left and right derivatives in Caputo sense,

left and right derivatives in Riemann–Liouville sense

where \(f\in \) \(H^{1}\left( a,b\right) ,\) \(a<b,\) \(\alpha \in \left[ 0,1\right] \).

where \(B\left( \alpha \right) >0\) is a normalization function with \( B(0)=B(1)=1\).

Theorem 1

(Caputo and Fabrizio 2015) The Laplace transform of fractional definitions with Caputo–Fabrizio fractional derivatives (1) and (3) is given as follows

Definition 2

(Caputo and Fabrizio 2015) Left and right integrals for Caputo–Fabrizio fractional derivatives are defined by, respectively

Definition 3

(Atangana and Baleanu 2016) Atangana–Baleanu fractional derivatives are defined as follows;

left and right derivatives in Caputo sense,

left and right derivatives in Riemann–Liouville sense

where \(f\in H^{1}\left( a,b\right) \), \(a<b\), \(\alpha \in \left[ 0,1\right] \).

where \(M\left( \alpha \right) >0\) is a normalization function with \( M(0)=M(1)=1.\)

Definition 4

(Abdeljawad and Baleanu 2017a) Left and right fractional integrals for Atangana–Baleanu fractional derivative are defined by, respectively

Theorem 2

(Atangana and Baleanu 2016) The Laplace transform of fractional definitions with Atangana–Baleanu fractional derivative (5) and (7) is given as follows

Definition 5

(Podlubny 1998) Mittag–Leffler functions with one and two parameters are defined by, respectively

and

Property 1

(Podlubny 1998) Inverse Laplace transform of some special functions has the following properties;

-

(i)

\(\mathbf {{\mathcal {L}} }^{-1}\left\{ \dfrac{a}{s\left( s^{\delta }+a\right) }\right\} =1-E_{\delta }\left( -at^{\delta }\right) \),

-

(ii)

\(\mathbf {{\mathcal {L}} }^{-1}\left\{ \dfrac{1}{s^{\delta }+a}\right\} =t^{\delta -1}E_{\delta ,\delta }\left( -at^{\delta }\right) \).

3 Main results

We find analytical solutions of fractional GDP models through direct and inverse Laplace transforms and solutions obtained are evaluated by least-squares error minimization technique with ParametricNDSolve and NMinimize methods in Wolfram Mathematica 11 (Wolfram Research, Inc.) for fitting real data of GDP taken by World Bank (2018).

3.1 Fractional gross domestic product model with Atangana–Baleanu fractional derivative

Let us consider the GDP model equations with Atangana–Baleanu fractional derivative in linear and exponential cases,

where \(S\left( t\right) \) is the GDP per capita at time t and k is a constant having dimension \(time^{-\alpha }\).

Applying Laplace transform to both side of Eq. (9) and by the help of Theorem 2, we have

Now, let us apply inverse Laplace transform to Eq. (11), then we can find the analytical solution of the problem (9),

Performing similar operations to both side of Eq. (10), we have

Finally, we can find the analytical solution of Eq. (10),

3.2 Fractional gross domestic product model with Caputo–Fabrizio fractional derivative

Let us consider the GDP model equations with Caputo–Fabrizio fractional derivative in linear and exponential cases,

here k is a constant having dimension \(time^{-1}\).

Applying Laplace transform to both side of Eq. (13) and by the help of Theorem 1, then we have

Performing similar operations, we can find the analytical solution of Eq. (13),

Similarly, for Eq. (14), we have

Finally, we can find the analytical solution of Eq. (14),

3.3 Fractional gross domestic product model with Caputo fractional derivative

Let us consider the GDP model equations with Caputo fractional derivative by linear and exponential cases,

here, k is a constant having dimension \(time^{-\alpha }\).

Comparison of fractional and integer models with real data

Comparison of fractional and integer models with each other and real data

Applying Laplace transform to both side of Eq. (17), then we have

Performing similar operations, we can find the analytical solution of Eq. (17),

Similarly for Eq. (18), we have

Finally, we have analytical solution

Remark 1

Mittag–Leffler function is taken as \(E_{\delta }\left( z\right) =\sum _{k=0}^{100}\frac{z^{k}}{\varGamma \left( \delta k+1\right) }\) in all figures to simulate approximate solutions and to find optimum parameter values, also we assume \(a=0.\)

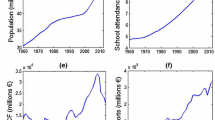

We show real data of GDP per capita of the United Kingdom in US$ in the following table and figures. We use the data from the World Bank (2018) between the years 1972–2007. We find the optimal parameter values the order \(\alpha \), normalization constants \(B(\alpha )\) and \(M(\alpha )\) and proportionality constant k in Table 1. Some data obtained from fractional and integer models are compared to the real data in Table 2, and the results in statistical way are given in Table 3 for showing the efficiency of fractional models. However, we evaluate the data obtained by fractional and integer-order models by using error sum of squares statistical analysis;

here, M is data number, \(a_i\) is each real data and \(b_i\) is estimated data obtained by models. We also evaluate the results with residual sum of squares for showing the efficiency with percentage value;

here, \(\epsilon _i\) is error margin between real and estimated data.

4 Discussion of GDP models

GDP model is evaluated by integer and fractional sense within ABC, Caputo and CFC under the light of real data. We use least-squares error minimization technique with ParametricNDSolve and NMinimize methods in Wolfram Mathematica 11 (Wolfram Research, Inc.) for finding optimal parameters of the models like fractional order \(\alpha \), \(M(\alpha ),\ B(\alpha )\) normalization constants and proportionality constant k. Optimal parameters are given in Table 1. Using these optimal parameters, comparative results between real data, integer and fractional results are given in Table 2 and the results are evaluated in statistical way in Table 3. We conclude from statistical evaluation that SSE and efficiency of ABC fractional model has the best estimated data and, respectively, estimated data of Caputo and CFC is better than estimated data of integer-order relative to the real data.

We can observe comparatively with fractional order results to the real data in Fig. 1. In Fig. 2, we can observe the results for fractional and integer-order models, also comparatively of all models in the last figure. We can conclude that ABC and Caputo behave similarly, but ABC model is more efficient than Caputo in Table 3. CFC result shows similarity to the integer-order, but it is more efficient for fitting last years’ data, and we can see that result also in Table 3.

We can deduce that estimated data of ABC are more efficient approximately \(\%63\) than the integer-order, Caputo is more efficient \(\tilde{\%}54\) and CFC is more efficient \(\tilde{\%}43\) in terms of SSE;

5 Conclusion

In this study, gross domestic product model is considered by Atangana–Baleanu, Caputo–Fabrizio and Caputo fractional and integer-order derivatives. Analytical solutions are obtained by Laplace transform, and results obtained are simulated by figures comparatively with real data of UK taken by World Bank (2018) between 1972 and 2007. Statistical evaluation is implemented of real and estimated data by using optimal parameter values.

Consequently, we can deduce that fractional models are more efficient in fitting real data than integer-order model. However, ABC is slightly more efficient than Caputo, Caputo and ABC are more efficient than CFC, but CFC model is more successful in capturing last data than integer-order counterpart. These fractional results show that fractional models will be more effective than integer-order ones in truly estimating the GDP results.

References

Abdeljawad T (2017) Fractional operators with exponential kernels and a Lyapunov type inequality. Adv Differ Equ 2017(1):313

Abdeljawad T, Baleanu D (2017a) Integration by parts and its applications of a new nonlocal fractional derivative with Mittag–Leffler nonsingular kernel. J Nonlinear Sci Appl 10(3):1098–1107

Abdeljawad T, Baleanu D (2017b) On fractional derivatives with exponential kernel and their discrete versions. Rep Math Phys 80(1):11–27

Al-Refai M, Abdeljawad T (2017) Analysis of the fractional diffusion equations with fractional derivative of non-singular kernel. Adv Differ Equ 2017(1):315

Almeida R, Bastos NR, Monteiro MTT (2016) Modeling some real phenomena by fractional differential equations. Math Methods Appl Sci 39(16):4846–4855

Alsaedi A, Baleanu D, Etemad S, Rezapour S (2016) On coupled systems of time-fractional differential problems by using a new fractional derivative. J Funct Sp 1:1–9

Atangana A, Alqahtani RT (2016) Numerical approximation of the space-time caputo-fabrizio fractional derivative and application to groundwater pollution equation. Adv Differ Equ 2016(1):1–13

Atangana A, Baleanu D (2016) New fractional derivatives with nonlocal and non-singular kernel: theory and application to heat transfer model. Therm Sci 20(2):763–769

Atangana A, Baleanu D (2017) Caputo–Fabrizio derivative applied to groundwater flow within confined aquifer. J Eng Mech 143(5):D4016005

Atangana A, Koca I (2016) Chaos in a simple nonlinear system with Atangana–Baleanu derivatives with fractional order. Chaos Solitons Fractals 89:447–454

Bas E (2015) The inverse nodal problem for the fractional diffusion equation. Acta Sci. Technol. 37(2):251–257

Bas E, Ozarslan R (2019) Theory of discrete fractional Sturm–Liouville equations and visual results. AIMS Math. 4(3):593–612

Bas E, Acay B, Ozarslan R (2019) The price adjustment equation with different types of conformable derivatives in market equilibrium. AIMS Math. 4(3):593–612

Caputo M, Fabrizio M (2015) A new definition of fractional derivative without singular kernel. Progr. Fract. Differ. Appl 1(2):1–13

Chen W-C (2008) Nonlinear dynamics and chaos in a fractional-order financial system. Chaos Solitons Fractals 36(5):1305–1314

Gómez-Aguilar J, Atangana A (2017) New insight in fractional differentiation: power, exponential decay and Mittag–Leffler laws and applications. Eur Phys J Plus 132(1):13

Gómez-Aguilar JF, Morales-Delgado VF, Taneco-Hernández MA, Baleanu D, Escobar-Jiménez RF, Al Qurashi MM (2016) Analytical solutions of the electrical RLC circuit via Liouville–Caputo operators with local and non-local kernels. Entropy 18(8):402

Gómez-Aguilar JF, Atangana A, Morales-Delgado VF (2017) Electrical circuits RC, LC, and RL described by Atangana–Baleanu fractional derivatives. Int J Circuit Theory Appl 45(11):1514–1533

Jarad F, Uğurlu E, Abdeljawad T, Baleanu D (2017) On a new class of fractional operators. Adv Differ Equ 2017(1):247

Kanth AR, Garg N (2018) Computational simulations for solving a class of fractional models via Caputo–Fabrizio fractional derivative. Procedia Comput Sci 125:476–482

Kuroda LKB, Gomes AV, Tavoni R, de Arruda Mancera PF, Varalta N, de Figueiredo Camargo R (2017) Unexpected behavior of Caputo fractional derivative. Comput Appl Math 36(3):1173–1183

Owolabi KM, Atangana A (2017) Numerical approximation of nonlinear fractional parabolic differential equations with Caputo–Fabrizio derivative in Riemann–Liouville sense. Chaos Solitons Fractals 99:171–179

Ozarslan R, Ercan A, Bas E (2019) \(\beta \)-Type fractional Sturm–Liouville coulomb operator and applied results. Math Methods Appl Sci 42(18):6648–6659

Podlubny I (1998) Fractional differential equations: an introduction to fractional derivatives, fractional differential equations, to methods of their solution and some of their applications. Elsevier, New York

Sun H, Hao X, Zhang Y, Baleanu D (2017) Relaxation and diffusion models with non-singular kernels. Phys A Stat Mech Appl 468:590–596

Uğurlu E, Baleanu D, TAŞ K (2018) On the solutions of a fractional boundary value problem. Turk J Math 42(3):1307–1311

Varalta N, Gomes AV, Camargo RdF (2014) A prelude to the fractional calculus applied to tumor dynamic. TEMA (São Carlos) 15(2):211–221

World Bank (2018) World Development Indicators. Accessed 25 July 25 2018

Yavuz M, Ozdemir N, Baskonus HM (2018) Solutions of partial differential equations using the fractional operator involving Mittag–Leffler kernel. Eur Phys J Plus 133(6):215

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare that they have no conflict of interest.

Ethical approval

This article does not contain any studies with human participants or animals performed by any of the authors.

Additional information

Communicated by V. Loia.

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Ozarslan, R., Bas, E. Reassessments of gross domestic product model for fractional derivatives with non-singular and singular kernels. Soft Comput 25, 1535–1541 (2021). https://doi.org/10.1007/s00500-020-05237-4

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00500-020-05237-4