Abstract

Energy sources are of paramount significance in the contemporary landscape, categorically classified into two main types: (i) primary sources, encompassing a wide spectrum ranging from nuclear energy to fossil fuels like natural gas and oil; and (ii) renewable sources, including geothermal, hydropower, solar, and wind energies. Governments have taken proactive measures since 2010, culminating in the establishment of the Bureau of Energy Efficiency under the Energy Conservation Act, aimed at curtailing energy consumption across diverse economic sectors. The interconnectedness of energy consumption, environmental ramifications, and economic progress is undeniable. A noteworthy project originating in 2010 is rooted in the pioneering market-based mechanism known as the perform, achieve, and trade (PAT) framework, which predominantly targets industrial energy utilization. Given the substantial role of energy costs within the broader spectrum of total production expenses, it becomes imperative to gauge the profit margin intensity (PMI) within energy-intensive sectors and industries encompassed by the PAT initiative. This entails an exploration of the influence exerted by these sectors on PMI. Consequently, the identification of variables influencing industrial profitability with respect to energy employment becomes pivotal. This article introduces a methodology grounded in panel data analysis, applied to a specific case study involving Indian energy-intensive corporations. The investigation takes into account the impact of both the Energy Conservation Act (ECA) and PAT as dichotomous covariates. Notably, the ambit of PAT encompasses the eight most energy-intensive industries in India, spanning the years 2012 to 2015. India stands among the world’s foremost energy consumers, with its industrial sector notably emerging as the largest energy consumer in 2015. Evidently, energy serves as a driving force behind the country’s manufacturing costs. The findings of this study underscore a negative correlation between energy costs and profitability. While the overall impact of PAT on industry performance appears limited, the ECA emerges as a potent factor significantly affecting earnings. Moreover, a compelling indirect relationship between energy costs and profitability is discerned, wherein rising revenues correspondingly lead to amplified energy costs. Consequently, the implications drawn from our study are intricately linked to the efficacy of energy utilization regulations within energy-intensive industrial contexts. The statistical analyses integral to this study were diligently carried out using the R software.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Motivations, bibliography, and aims

This section provides the literature, motivations, and objectives of the study.

1.1 Introduction

The industrial sector stands as the driving force propelling economic advancement across various domains. The nexus between energy consumption, environmental impact, and economic progress is well-documented (Wang et al. 2010). In numerous nations, the industrial sector commands over fifty percent of total energy consumption (Mukherjee 2008; Carmona et al. 2017). A case in point is India, which holds a prominent position as a primary global energy consumer. Within India, specific industries such as cement, chlor-alkali, fertilizers, metals, paper, and power plants account for more than seventy percent of the nation’s industrial energy consumption.

Energy expenses constitute a significant segment of the overall production expenditure across diverse global industries. Studies have underscored a correlation between diminishing energy intensity and augmenting profitability. The World Steel Association (www.worldsteel.org) notes that enhanced energy consumption efficiency directly translates into reduced production costs, thereby bolstering competitiveness. Consequently, enterprises and manufacturing facilities are encouraged to channel investments into energy-efficient practices. These strategic practices serve a dual purpose: curbing energy intensity, thereby elevating industry profits, and concurrently enhancing both competitiveness and the trajectory towards sustainable development (de Andrade Guerra et al. 2021). This purpose is echoed in the Industrial Development Report 2011 (UNIDO 2012), which accentuates that energy efficiency emerges as a straightforward yet potent approach to simultaneously combat climate change, ameliorate air quality, heighten business competitiveness, and curtail energy expenditures.

In UNIDO (2012), the pivotal significance of energy efficiency is put into perspective for its potential to yield both tangible and intangible advantages. This perspective aligns with findings from various studies, indicating that energy efficiency has the potential to amplify firm profitability. The previous assertion is reinforced by insights from Dutta and Mukherjee (2010), which highlight how elevated energy expenses and substantial production volumes can serve as barriers to entry, exerting an impact on the competitive landscape of industries. A pertinent illustration can be observed in the Indian context, particularly within the aluminum industry. Furthermore, it is worth noting that energy-related expenditures within these industries have surged to encompass approximately 40 percent of the manufacturing sector. Consequently, energy costs stand as a relevant factor significantly shaping industrial performance and competitiveness.

1.2 State-of-the-art

Accurate quantification of energy consumption holds immense concern spanning a wide array of industries, garnering heightened attention from both countries and corporations alike. This mounting concern is indicative of the growing emphasis on sustainable energy practices. In Mukherjee (2008), a comprehensive analysis of energy efficiency within the manufacturing sector was conducted, with a specific focus on the Indian context. The analysis delved into the intricate fabric of interstate disparities in energy intensity, shedding light on pronounced variations that manifest across different geographical regions. Remarkably, the findings unveiled a discernible trend: industries characterized by elevated energy consumption exhibited diminished energy efficiency when gauged against manufacturing output metrics. Furthermore, an intriguing correlation emerged; regions boasting a highly skilled workforce were seen to align with superior levels of energy efficiency. This underscores the interplay between human capital and energy optimization, implying that a proficient workforce can contribute positively to achieving enhanced energy efficiency levels.

In Sahu and Narayanan (2014), the manufacturing performance and consumption of energy were studied, finding that energy intensity was directly associated with productivity/manufacturing performance. Other factors that may affect the energy intensity were studied in Kumar (2003) and Sahu and Narayanan (2009). To understand the critical factors affecting the dependent (response) variable related to energy intensity in industrial firms, multiple regression models were used in Kumar (2003) and Sahu and Narayanan (2009) to estimate the coefficients of other critical independent variables (covariates).

Prowess is an essential database of the Centre for Monitoring Indian Economy (CMIE), which is available at prowessiq.cmie.com. We are also using the data from Prowess for the present study. In the study presented in Kumar (2003), data of 1342 firms for eight years were collected from the CMIE-Prowess related to: capital intensity, firm age, firm size, integration degree, ownership pattern, profit margin, research and development (R&D) intensity, repair intensity, and technology import intensity as covariates. In that study, it was concluded that the firm size and energy intensity are negatively related, which can be accelerated to economies of scale. In the same study (Kumar 2003), it was also identified that energy intensity is positively related to repair intensity and technology import intensity, as opposed to what was expected. Furthermore, also in that study, it was investigated that the ownership pattern affects the energy intensity. Moreover, foreign and state ownership is associated with low and high energy intensity, respectively.

In Sahu and Narayanan (2009), data from 2350 firms in 2008 were extracted from the Prowess database. These data were analyzed, concluding that energy intensity and firm size have an inverted U-shaped relationship, whereas energy intensity is negatively associated with both export intensity and profit margin. Also, it was investigated that energy intensity is positively related to capital and repair intensities, as supported in Kumar (2003). Most of the results presented in Kumar (2003) and Sahu and Narayanan (2009) are similar, except for the relations between firm age and energy intensity. The covariates considered in Sahu and Narayanan (2009) included sales (in logarithmic scale), capital, labor, and repair intensities, and firm age. Other covariates are related to R&D and technology import intensities, foreign ownership (dummy variable), export intensity, and profit margin. Therefore, many of the covariates considered in Sahu and Narayanan (2009) are the same as those employed in Kumar (2003). In Sahu and Narayanan (2009), firm size and its square were used as covariates. The squared term was included to relate firm size and energy intensity as it does not need to be increased or decreased.

Another similarity between the studies of Kumar (2003) and Sahu and Narayanan (2009) was that both detected a direct relation between technology import and energy intensities, as opposed to what was expected. In Sahu and Narayanan (2009), a direct relationship was identified between firm age and energy intensity. This direct relationship is to be expected since older companies also have older plants and machinery. The results presented in Kumar (2003) are opposed to what was reported in Sahu and Narayanan (2009). In the investigation provided in Kumar (2003), a nonsignificant coefficient with negative sign of the age covariate was detected. In that investigation, a study of the energy intensity at an industry level was carried out, similar to what was established in Sahu and Narayanan (2009).

In Bertoldi et al. (2010), it was identified that instruments based on the market are one of relevant tools in the policy portfolio for calamite change mitigation and for further obtaining a tradable white certificate in the European Union. However, not only in the European Union, but it received importance in the United Kingdom (UK) as well (Hamrin et al. 2007; Clarkson et al. 2015). The UK searched for other methods to enhance energy efficiency and increase profitability. In 2002, the UK introduced a new method that enhances energy efficiency (Langniss and Praetorius 2006; Hamrin et al. 2007; Vine and Hamrin 2008). Furthermore, in 2003, Australia introduced the trading system of energy efficiency under the scheme of greenhouse gas abatement. This system permitted greenhouse abatement projects to reduce emissions generating national greenhouse certificates that are tradable (Zhang 1998; Christiansen and Wettestad 2003; Springer and Varilek 2004; Hamrin et al. 2007).

In the same line, France and Italy, in the year 2005, established their tradable systems with different energy-saving targets for the future (Hamrin et al. 2007; Franzò et al. 2019). Similarly, India was trying to decrease the energy intensity. In 2012, India presented a similar market-based measure to enhance energy efficiency under the Perform, Achieve, and Trade (PAT) mechanism (Hudedmani et al. 2019). This measure can permit for saving of between 6.5 and 10.0 Mtoe of consumption of energy during 2012–2015 (Kumar and Agarwala 2013; Bhandari and Shrimali 2018; de la Rue du Can et al. 2019), where Mtoe corresponds to millions of tonne of oil equivalent (1 toe = 10 millions of calories). The PAT is a method of several phases that covers the majority of economical sectors that consume high energy.

One of the principal users of primary energy in the globe is India, consuming coal, oil, and other fossil fuels (Liming 2009; Gaurav et al. 2017). In 2013, Indian total energy consumption was 527 Mtoe, with the industrial sector accounting for roughly 30% equivalent to 158 Mtoe (Sharma et al. 2019). In 2015, Indian total primary energy consumption was 107 Mtoe (Sharma et al. 2019). After China and the United States, the third emitter of greenhouse gases in the world is India (Saikawa et al. 2017). In 2016, Indian greenhouse gas emissions increased by 4.7 % over the previous year. Indian industries produce 25% of the greenhouse gas emissions generated in the country (Vig and Datta 2022).

In Oak (2017), the researchers studied firm-level data of Indian industries sourced from the Prowess repository. The objective of that study was to identify the variables that potentially influence the energy intensity in the Indian cement industry. To quantify the impact of the PAT mechanism, a fixed effect (FE) model based on panel data was employed, with the robustness of the model assessed using propensity score matching.

The Indian Ministry of Power (powermin.gov.in) utilized the PAT mechanism to identify the designated consumers (DCs) within the Indian cement industries. They highlighted that these industries exhibit inefficiency in terms of energy consumption. In Bhandari and Shrimali (2017), the efficacy of the PAT initiative was evaluated through semi-structured interviews conducted with DCs between May and July 2013. The impact of R&D on enhancing industrial energy utilization in China was examined in Teng (2012).

A secondary source of information was provided by the Indian Ministry of Power, concluding that: (i) the set targets are not rigorous and sufficient to make the industries more efficient in terms of energy; (ii) the long-term investment for efficiency in terms of energy is not possible; (iii) the PAT market cannot be constituted; (iv) several equity issues were not apparent or addressed; and (v) it is early to detect costs of transaction. Moreover, according to the report presented in Bhandari and Shrimali (2017), policy implications have as objectives: (a) to set new targets for rising energy costs; (b) to encourage long-term investments; (c) to introduce the PAT market platform for cost efficiency; (d) to reduce the equity concerns; and (e) to keep the costs of the low transition.

1.3 Motivations, objectives, and plan of the article

Our motivations for conducting the present study are described next. India is following relevant steps to control the energy intensity in its industries. First, India launched the Energy Conservation Act (ECA) in 2001. Second, the Bureau of Energy Efficiency (BEE) of India has been stated under the ECA to promote Indian energy efficiency. Moreover, third, India launched a plan of action for the climate change. The National Mission for Enhanced Energy Efficiency was formed to promote the energy efficiency using diverse mechanisms.

The PAT framework is related to the industries. The PAT tries to enhance the energy efficiency and it is ambitious in the Indian context since the country elaborated tools based on the market to solve problems related to environmental issues. The Indian Ministry of Power and the BEE identified the eight firms which are the most energy-intensive, as reported in Table 1. For these firms, the plants that were most energy-intensive have been stated as DCs. The SEC indicator (related to energy consumption in a specific order) is established as the proportion of input employing net energy for the DCs about output from the DCs, such that the sum of the targets for all DCs within a firm is equal to the firm target. These targets are associated with the heterogeneity in each industry concerning firm age, energy consumption trends, and energy saving potential, among others. The DC is needed to decrease its SEC by a fixed value, using this SEC indicator for the corresponding year, formulated as the SEC averaged starting in April 2007 until March 2010. Observe that the PAT phase I (PAT-1) started in the period between April 2012 and March 2015. When this period finished, a tradable energy saving certificate was obtained if the DC surpassed its target. The PAT-1 was stated to decrease the SEC in energy-intensive sectors from 478 DCs based on eight industries. The sub-sectors included were aluminum, cement, chlor-alkali, fertilizers, paper, steel, and thermal power plants. These DCs currently are 25% of the Indian gross domestic product, with about 45% of utilization of Indian industrial energy. In the PAT-1, about 8.67 Mtoe of energy saving was reached versus around 6.68 Mtoe of targeted saving energy, that is less than 30% on the target and similar to economic savings of approximately 9.5 billion rupees.

As the energy cost is the central part of the total production cost, estimating the profit margin intensity (PMI) of energy-intensive sectors/industries covered under PAT-1 is an aspect of interest. Also, another aspect of interest, it is needed to study the impact on PMI of these sectors due to the implementation of the ECA in 2001 and PAT in 2012, accounting for these covariates in dummy variable form. Based on the present extensive bibliographical review, no investigations exist about these aspects in Indian energy-intensive industries. Therefore, it is essential to state what variables affect the industries’ profitability in terms of their energy usage.

The principal objective of the present investigation is to propose and derive a methodology to determine the relationship between the profitability of energy-intensive industries considering the effect of PAT-1 and ECA together. We employ a panel data methodology to analyze a case study of Indian energy-intensive industries.

Panel data, by blending the inter-individual differences and intra-individual dynamics, have the following advantages over cross-sectional or time-series data: (i) more accurate inference of model parameters, as panel data often contain more degrees of freedom (DF) and more sample variability than cross-sectional data that may be viewed as a panel with \(T = 1\), or time series data which are a panel with \(N = 1\), hence improving the efficiency of econometric estimates (Hsiao et al. 1995); and (ii) greater capacity for capturing the complexity of human behavior than single cross-section or time series data.

When considering the influence of omitted variables, a common argument is that the true cause behind discovering (or not discovering) specific effects lies in the oversight of certain variables in the model specification. These variables are correlated with the included covariates. Panel data, as highlighted by Hsiao (2007), provide insights into both inter-temporal dynamics and individual entities, offering the potential to mitigate the impact of missing or unobserved variables.

After this introduction, the plan of our article is formed as follows. Section 2 presents the theoretical aspects of the proposed methodology. In Sect. 3, a case study of the Indian energy-intensive industries is developed. In Sect. 4, we report the findings found in this investigation. Some conclusions are stated in the final part (Sect. 5).

2 Methodology

This study employed a quantitative research design utilizing FE and random effect (RE) linear models to investigate the relationship between variables PMI and a sequence of covariates as detailed in Table 2, while accounting for individual-level and group-level variations.

In this section, we detail the theoretical background of the statistical methods applied in the present study.

2.1 Types of data

Definition 1

Time series data are time-dependent observations of a random variable X over t (time), denoted as \(x_{t}\), for \(t \in \{1,\dots ,T\}\).

Definition 2

Cross-sectional data are observations of a random variable X at a single point “i” of time denoted as \(x_{i}\), for \(i \in \{1,\dots ,N\}\). We refer to “i” as an individual. We are interested in modeling the heterogeneity across N individuals.

Definition 3

Panel data, sometimes named longitudinal data, correspond to a set with both cross-sectional unit and a time-series dimension. In panel data, all cross-section units \(i \in \{1,\dots ,N\}\) of a random variable X are observed during a time \(t \in \{1,\dots ,T\}\), denoted as \(x_{it}\). A panel data set is balanced if all individuals are observed a common number of times. Otherwise, it is unbalanced.

2.2 Types of models

Definition 4

Let N and T be a number of individuals and periods of time, respectively. A panel data model is formulated as

with:

-

\(Y_{it}\) being a response associated with individual i at time t.

-

\(\beta _0\) being the model intercept, which does not depend on i nor t.

-

\(\varvec{x}_{it}\) being a \(K\times 1\) vector corresponding to observed values of K covariates for individual i at t (time).

-

\(\varvec{\beta }\) being a vector of K regression parameters.

-

\(\varepsilon _{it}\) being the model error related to individual i at time t.

If some individual characteristics (variables) \(\varvec{z}_i\), that do not vary over time, are available (observable), the model can be written as

where \(\varvec{z_{i}}\) is a time-invariant \(K\times 1\) vector of individual i, and \(\varvec{\beta }_1\) and \(\varvec{\beta }_2\) are \(K\times 1\) vectors of model coefficients.

If not all variables \(\varvec{z_{i}}\) are available, these unobserved individual characteristics can be modeled by a parameter \(\alpha _i\). In that case, \(\varepsilon _{it}\) can be decomposed as

where \(u_{it} \sim F(0,\sigma ^2_u)\), that is, \(u_{it}\) are independent identically distributed random variables according to F, with zero mean and variance \(\sigma ^2_u\). In fact, all individuals characteristics (time-invariant), observable or not, are captured by \(\alpha _i\).

Definition 5

An FE model is defined as

with \(\alpha _i\) (individual intercepts) being fixed for each \(i \in \{1,\dots ,N\}\).

When an FE model is used, it is assumed that there is something within individuals affecting the response variable Y, and therefore, it needs to be controlled. Because of this, it is not required that individual intercepts and the terms \(u_{it}\) are uncorrelated. However, \(\text {E}[\varvec{X}_{it},u_{it}]=0\) must hold. Since the time-invariant characteristics are related to each individual, they should not be associated with other characteristics of the individual. There are popular estimation techniques for the FE model that can be considered as: least square dummy variable and pooled ordinary least square (OLS).

Definition 6

An RE model is stated as

with \(u_{it} \sim F(0,\sigma ^2_u)\) and \(\alpha _i\sim G(0,\sigma ^2_{\alpha })\), that is, \(u_{it}\) and \(\alpha _i\) are independent identically distributed random variables according to F and G, with zero mean and variances \(\sigma ^2_u\) and \(\sigma ^2_\alpha\), respectively. Note that \(\alpha _i\) (individual intercepts) are fixed for each \(i \in \{1,\dots ,N\}\), where \(\alpha _i + u_{it}\) are considered as an error term based on two elements: (i) an individual specific one that does not vary in time t; and (ii) another one that is uncorrelated over time t.

2.3 Hypothesis testing

When an RE model is employed, we assume that the distribution of \(\alpha\) is nearly normal. Also, we assume independence between \(\alpha _i\) and \(u_{it}\), as well as independence of all components of \(\varvec{x}_{it}\). The RE model can be estimated with the OLS technique. To decide between an FE model and an RE model, we can apply the Hausman test, which uses the statistic \(\widehat{\varvec{\beta }}_{\text {FE}}-\widehat{\varvec{\beta }}_{\text {RE}}\) to contrast the hypotheses given by

with the test statistic stated as \((\widehat{\varvec{\beta }}_{\text {FE}}-\widehat{\varvec{\beta }}_{\text {RE}})^{\top } (\widehat{\varvec{V}}_{\widehat{\varvec{\beta }}_{\text {FE}}}-\widehat{\varvec{V}}_{\widehat{\varvec{\beta }}_{\text {RE}}}) (\widehat{\varvec{\beta }}_{\text {FE}}-\widehat{\varvec{\beta }}_{\text {RE}}) \sim \chi ^2(K),\)

where \(\widehat{\varvec{V}}\) is the estimated covariance matrix. Note that the Hausman statistic is chi-square distributed considering a number of DF equal to K, denoted as \(\chi ^2(K)\), with K being the number of model parameters, as mentioned.

To verify for homogeneity of slope coefficients, we can employ a poolability test. The null hypothesis is that \(\beta _i=\beta\), for \(i\in \{1,\dots ,N\}\), that is, no panel data are necessary. In this work, we utilize the Chow test (to the case of N linear regressions) given in Chow (1960). Furthermore, we use the Breusch–Pagan (BP) test to check heteroskedasticity of the error term in FE models. Additional information about estimates of the FE and RE models, unit-root (stationarity) test, poolability test and BP test, can be found in Verbeek (2008) and Baltagi (2021). For details about the Hausman test, see Hausman (1978) and Greene (2008).

3 Case study in India

This section describes the case study in three steps. Then, we formulate the econometric model and summarize the methodology in a pseudo algorithm by means of a flowchart.

3.1 Methodology: variables, industries, and time

Step 1: Identification of variables

The variables affecting profitability of firms (see Table 2) are:

-

X1

Energy intensity.

-

X2

Capital intensity.

-

X3

Labor intensity.

-

X4

Firm size.

-

X5

Firm age.

-

X6

Technology import intensity.

-

X7

Repair intensity.

Step 2: Identification of industries

The eight energy-intensive sectors used in the present study covered under PAT-1 mechanism (2012–2015) are:

-

I1

Aluminum.

-

I2

Cement.

-

I3

Chlor-alkali.

-

I4

Fertilizer.

-

I5

Steel.

-

I6

Paper.

-

I7

Textil.

-

I8

Thermal power plants.

Note that all the eight sectors have been included for analysis in this study. Since the seven variables and eight energy intensive sectors are included in the PAT-1, and the eight sectors utilize over 70% of the industrial consumption of energy in India and 25% in the Indian gross domestic product, we have selected the same variables and all eight sectors in our analysis.

As mentioned, the data were taken from CMIE-Prowess (prowessiq.cmie.com). Under PAT, plants of various companies have been considered, but as the data of the plant level are not available, we take data of the company level for our analysis.

Based on their energy consumption to be called a DC under the PAT, the sectors are divided into two datasets utilizing the PAT booklet of the Indian Ministry of Power, published in July 2012 (see Table 3). This division also needs to be done for solving the problem of availability of data only for few companies covered under the PAT on CMIE-Prowess. For each sector, the companies included in the study are presented in Tables 4 and 5, with these companies being covered under the PAT-1.

Step 3: Identification of time period

The following energy efficiency policies have been implemented by India:

2001: Energy Conversation Act.

2012–2015: Perform, Achieve and Trade in phase I.

Therefore, the time period selected for the present investigation is since 1995 to 2015, because it helps us to study the influence of policies for energy efficiency on energy intensity, profitability, and emission intensity of industries.

3.2 Statistical model

As mentioned, a model of panel data is employed to estimate PMI of the selected Indian industries. To get the most robust/appropriate results in all scenarios, an econometric model is applied to both datasets 1 and 2 considering OLS estimation, as well as FE and RE structures. To estimate PMI, the model is defined as \(\text {PMI} = f(\text {EI, A, LI, CI, RI, SI, TMI, PAT, ECA}),\) where the covariates EI, A, LI, CI, RI, SI, TMI, PAT, and ECA are defined in Table 2. The data set is balanced and indexed by \(i \in \{1, \dots , N\}\), where N is the number of companies, and \(t \in \{1, \dots , 21\}\). The variables are defined in Table 6.

All the variables, except firm age, are measured in Ruppies million (as extracted from CMIE-Prowess: prowessiq.cmie.com). Therefore, to correct it for inflation, we employ the index of industrial production (IIP) data (secured from indiastat.com) expressed as

3.3 Summary of the methodology

Figure 1 summarizes the methodology in a pseudo algorithm by means of a flowchart to help with the understanding of our methodology.

Flowchart of the methodology

4 Results

The section reports the findings obtained from our analysis for the case study in three subsections. The first two ones introduce exploratory data analyses of the two datasets considered in this investigation. The third one presents the models described in Sect. 3.2.

4.1 Stationarity test

The unit-root test is initially employed in the panel data methodology to assess the stationarity characteristics of the relevant variables. Various approaches can be utilized for conducting panel unit-root testing. To enhance result robustness, we utilize two unit-root tests: the Levin–Lin–Chu (LLC) test and the Im–Pesaran–Shin (IPS) test.

The LLC test considers variability, although its power diminishes in small sample sizes due to potential serial correlation, which is challenging to completely mitigate. These unit-root methods evaluate hypotheses regarding the stationarity of the variables. The outcomes of the unit-root tests for each variable are presented in Tables 7 and 8. The results reported in these tables indicate that each variable demonstrates stationarity in certain tests, while not meeting the stationarity criteria in others.

4.2 Heterogeneity analysis

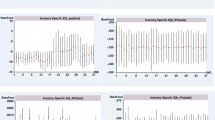

Figures 2 and 3 depict the heterogeneity across years for dataset 1. Both figures distinctly illustrate noticeable differences between the groups. Given this heterogeneity, the application of pooled OLS is not suitable, thus warranting the utilization of FE or RE models. The blue lines within the figures represent the 95% confidence intervals surrounding the mean within each group.

Plot of heterogeneity for the indicated company according to its ID as in Table 4 for dataset 1, where the blue lines are 95% confidence intervals around the mean within each group

Plot of heterogeneity for the indicated year with dataset 1, where the blue lines are 95% confidence intervals around the mean within each group

Similarly, in dataset 2, Figs. 4 and 5 also reveal evident heterogeneity across companies and years. This heterogeneity further reinforces the need to avoid pooled OLS and consider the FE or RE models. Table 9 shows the results of the poolability test (Chow test) for datasets 1 and 2 by years. The test supports the application of a different approach than choosing a pooling model, as it can be detected from near-zero p-values.

Plot of heterogeneity for the indicated company according to its ID as in Table 5 for dataset 2, where the blue lines are 95% confidence intervals around the mean within each group

Plot of heterogeneity for the indicated year with dataset 2, where the blue lines are 95% confidence intervals around the mean within each group

4.3 Regression results

To ensure the robustness of our findings across various scenarios, we have employed three distinct models: OLS, FE, and RE. In Table 10 and Fig. 6, we present the comprehensive impact of all covariates on the PMI, considering both the dummy variables PAT and ECA together.

Plot of estimated coefficients for dataset 1 with the indicated method and variable

As evident from the results in Table 10, the energy intensity exhibits statistical significance across the majority of the models, displaying an inverse relationship with PMI. This suggests that an increase in energy intensity is associated with a decrease in profits. In other words, a rise in the energy intensity of the production process within industries is likely to lead to a reduction in PMI.

In accordance with the pooled OLS model, a 1% increase in energy intensity corresponds to a 0.266% decrease in PMI. Compared to the FE model, a 1% growth in energy intensity results in a 0.344% reduction in PMI. Similarly, based on the RE model, a 1% increase in energy intensity is associated with a 0.323% decrease in PMI.

Firm age exhibits an indirect correlation with PMI, where an increase in the age of the company leads to a decrease in PMI. This trend might be attributed to the aging of equipment and production methods over time, potentially resulting in increased energy intensity and reduced profits.

According to the pooled OLS model, a 1% increase in age leads to a 0.072% decrease in PMI. In line with the RE model, a 1% age increase is linked to a 0.06% decrease in PMI.

The coefficient of labor intensity lacks statistical significance across all models and appears to be positively or negatively related to PMI. Similarly, the coefficient of capital intensity is also statistically nonsignificant in all models and appears to have a positive or negative relation to PMI.

All models consistently indicate a direct relationship between PMI and repair intensity. This signifies that as industries allocate more resources to operational repairs, their PMI tends to rise. However, it is important to note that the significance of the PMI coefficient is observed in only a subset of these models. The relationship between firm size and PMI remains uncertain due to varying outcomes. In some instances, the correlation is negative, while in others, it is positive. Additionally, the coefficient demonstrates significance with both signs across different models. In addition, the coefficient for technological import intensity lacks significance in all models, indicating that this variable has minimal impact on PMI.

The dummy variable representing PAT has demonstrated weak significance in only a few models, displaying a negative correlation with energy intensity. This suggests that during years when PAT is in effect, there has been an increase in the PMI of companies. Conversely, the coefficient for the dummy variable ECA exhibits significance or weak significance across the majority of models. It appears to elevate PMI during years when ECA is in effect for companies. This indicates that the implementation of ECA seems to be yielding the intended impact on the energy intensity of companies and consequently influencing PMI.

In the pooled OLS model, the presence of an ECA year is associated with a 0.03% increase in PMI. In comparison to the FE model, the presence of an ECA year corresponds to a PMI increase of 0.02%. In relation to the RE model, the presence of an ECA year results in a PMI increase of 0.33%.

As shown in Table 11 and Fig. 7, energy intensity holds statistical significance in the majority of the models, revealing an inverse relationship with PMI. This suggests that as energy intensity increases, profits tend to decrease. In other words, if the production process within industries witnesses a rise in this intensity, it is likely to correspond with a reduction in profit intensity.

Plot of estimated coefficients for dataset 2 with the indicated method and variable

Comparing to the pooled OLS model, a 1% increase in energy intensity is associated with a 0.464% decrease in PMI. In alignment with the FE model, a 1% growth in energy intensity corresponds to a PMI reduction of 0.411%. As per the RE model, a 1% rise in energy intensity is linked to a PMI decrease of 0.421%. Furthermore, there exists a negative correlation between the variable age and PMI. This suggests that as a company’s age increases, its PMI experiences a decline. This phenomenon could potentially be attributed to the progression of time leading to the obsolescence of equipment and production methods within the company. This aging process might render them less efficient, culminating in heightened energy intensity and consequently reduced profitability.

Based on the FE model, a 1% increase in age is associated with a PMI reduction of 0.079%. In comparison to the RE model, a 1% growth in age corresponds to a PMI decrease of 0.041%. The coefficient of labor intensity holds significance in certain models and appears to demonstrate a negative correlation with PMI. This suggests that as labor intensity increases, PMI decreases, possibly due to the presence of surplus or redundant labor.

As per the pooled OLS model, a 1% increase in labor intensity corresponds to a PMI reduction of 0.318%. In comparison to the FE model, a 1% growth in labor intensity leads to a more substantial PMI reduction of 1.109. Similarly, when applying the RE model, a 1% rise in labor intensity is linked to a PMI decrease of 0.880%.

The coefficient associated with capital intensity exhibits statistical significance in the models and showcases a negative relationship with PMI. This indicates that as capital intensity increases, PMI decreases, potentially due to the higher energy consumption of machinery and equipment, resulting in reduced profits.

Utilizing the pooled OLS model, a 1% increase in capital intensity is linked to a PMI decrease of 0.074. Correspondingly, with the FE model, a 1% growth in capital intensity leads to a PMI reduction of 0.233%. In alignment with the RE model, a 1% rise in capital intensity results in a PMI decrease of 0.192%.

All models consistently highlight a direct relationship between PMI and repair intensity. This implies that as industries allocate more resources to operational repairs, their PMI tends to increase.

Comparing to the pooled OLS model, a 1% increase in repair intensity is associated with a PMI increase of 1.378%. In alignment with the FE model, a 1% growth in repair intensity corresponds to a PMI increase of 1.531%. Similarly, based on the RE model, a 1% rise in repair intensity results in a PMI increase of 1.642%.

Regarding the relationship between technology import intensity and PMI, its exact nature remains unclear as it exhibits varying signs across different scenarios.

The dummy variable representing PAT years holds significance in the models and demonstrates a negative correlation with PMI. This implies that during years when PAT is in effect, there is a reduction in companies’ PMI. In addition, for the ECA dummy variable, its coefficient is significant across most models and indicates an increase in PMI during ECA years for companies. This suggests that the ECA has the intended impact on companies’ energy intensity and subsequently on PMI.

Comparatively, utilizing the pooled OLS model, the presence of an ECA year is associated with a PMI increase of 0.024%. In line with the FE model, the presence of an ECA year leads to a PMI increase of 0.050%. Similarly, with the RE model, the presence of an ECA year results in a PMI increase of 0.037%.

The p-values of the Hausman test for datasets 1 and 2 are 0.00469 and less than 0.0001, respectively, under the null hypothesis \(\text {H}_0\text{:}\)the RE model is appropriate. Consequently, with a significance level of 5%, the null hypotheses are rejected, indicating that the FE model is the preferred choice for describing PMI. These results are summarized in Table 12.

We deduce that the within-group intercepts \(\alpha _i\) depend on the covariates denoted as \(X_{it}\), implying that variations across entities are not randomly distributed. We assume that these inter-entity differences do not exert an influence on our dependent variable PMI. Moreover, since the intercept in the FE model accounts for the unobserved, non-time-dependent variables, there is no necessity to incorporate these variables explicitly.

Figure 8 displays a visualization of the residuals. The BP test outcomes presented in Table 13 and Fig. 9 affirm a common occurrence in panel data analysis: heteroskedasticity. This occurrence is addressed by adopting a heteroskedasticity-consistent estimation approach for the covariance matrix of the estimated coefficients, as presented in Table 14. The revised t-test outcomes reveal a fresh array of significant variables, with the standard errors adapted to account for the presence of heteroskedasticity, as detailed in Baltagi (2021, ch. 2) for more comprehensive insights.

Plots of residuals versus their year for FE models with the indicated dataset

Plots of fitted-values versus their residual for FE models with the indicated dataset

5 Discussion, conclusion and visions

This section encompasses a comprehensive analysis and interpretation of the study’s findings, followed by our derived conclusions. Moreover, we acknowledge certain limitations inherent to our research and propose potential avenues for future research.

5.1 Discussion and conclusions

In this article, we have introduced a novel methodology for assessing profitability in energy-intensive industries through the lens of panel data analysis. Our approach has been applied to a case study involving Indian energy-intensive enterprises, incorporating the dynamic influences of the PAT in phase I and the ECA as dummy covariates.

A crucial finding of our study underscores the adverse impact of energy costs on the profitability of energy-intensive industries. Our results reveal a robust and negative relationship between energy costs and profits, indicating that as energy expenditures rise, profits correspondingly decline. Additionally, our analysis indicates a negative correlation between a firm’s age and its profitability. This highlights the significance for mature companies to invest in energy-efficient measures, thereby curbing energy intensity, elevating industry profits, and enhancing competitiveness. The imperative for industries to curtail energy consumption as a means of boosting profitability is also evident.

An integral strength of our analysis lies in its incorporation of the influence of the PAT in phase I and ECA while elucidating the intricate relationship between energy intensity and profitability. In contrast, existing literature, such as Kumar and Agarwala (2013), Bhandari and Shrimali (2017, 2018), and Sharma et al. (2019), tends to focus on generalized relationships between energy intensity and profitability.

While the impact of the PAT appears relatively muted on overall industry performance, our findings highlight the positive influence of the ECA. The legislation has been shown to effectively lower energy intensity, leading to increased profits—a trend that can potentially be attributed to technological advancements fostering greater energy efficiency.

As highlighted by Bhandari and Shrimali (2017), the initial phase of the PAT demonstrated easily attainable targets, resulting in energy savings surpassing expectations and leading to an abundance of energy savings certificates. However, it is evident that such achievements may not suffice to drive enduring energy efficiency improvements within industries in the long term (Dasgupta and Roy 2017). Therefore, it becomes apparent that a comprehensive evaluation of the policy’s effectiveness necessitates adjustments and enhancements across subsequent phases of the PAT. Furthermore, considering the relatively recent conclusion of its first phase (2012–2015), it is essential to refrain from prematurely forming a final judgment on the policy’s overall impact and effectiveness within the Indian context.

5.2 Limitations of the study

A notable limitation of our study lies in its focus on a specific subset of companies within the timeframe of the PAT in phase I (2012–2015), drawing data primarily from the CMIE-Prowess database. Additionally, our investigation exclusively examines the impact of the PAT in phase I and ECA on the performance of Indian energy-intensive industries. Other limitations of our study are as follows:

-

(1)

The study’s temporal scope encompasses 21 years (1995–2015), primarily due to our concentrated interest in investigating the effects of the PAT during its phase I (2012–2015).

-

(2)

The utilization of firm-level data stems from the unavailability of plant-level data within the CMIE-Prowess database.

-

(3)

The study is confined to companies falling under the purview of the PAT, aligning with our objective of assessing the influence of the PAT’s first phase on industrial energy consumption.

The unavailability of data significantly limits the scope of our study. Notwithstanding this limitation, upon reviewing the broader literature, it is reasonable to suggest that even with expanded data availability, the fundamental relationship between the profitability and energy costs of energy-intensive industries would likely persist. However, the inclusion of additional data could potentially provide a more comprehensive understanding of the effects of the PAT in phase I and ECA on industrial energy intensity. Furthermore, the acquisition of data would allow us to explore the interplay between profitability and other independent variables within individual industries, thereby enhancing the depth of our analysis.

5.3 Scope for future research and policy implications

Possible extensions of this study encompass an exploration of subsequent phases of the PAT, either in combination or individually. Similarly, an avenue for research involves dissecting various sectors under the PAT phases I and II separately. The study’s scope can be broadened by introducing additional independent variables, thereby yielding more nuanced outcomes. Moreover, a comprehensive analysis of the impact of various policy measures on industrial performance could yield valuable insights. We anticipate sharing the results of these potential analyses through future publications.

In terms of policy implications, our study underscores the importance for all eight energy-intensive industries—namely aluminum, cement, chlor-alkali, fertilizer, steel, paper, and textil—to make substantial investments in energy efficiency measures. Such initiatives are poised to significantly enhance industry profitability, aligning with the overarching objective of any industrial endeavor. Government bodies, including India, may consider taking proactive measures to facilitate the adoption of these initiatives by energy-intensive industries, and even potentially mandate their implementation.

An imminent future endeavor on our agenda is the development of an R software package, thereby facilitating the accessibility and applicability of our proposed methodology for other researchers in the field. This step could contribute to a more standardized and streamlined approach to analyzing profitability and energy intensity dynamics within energy-intensive industries.

References

Baltagi BH (2021) Econometric analysis of panel data. Edition 6. Springer, New York, NY, USA

Bertoldi P, Rezessy S, Lees E, Baudry P, Jeandel A, Labanca N (2010) Energy supplier obligations and white certificate schemes: comparative analysis of experiences in the European Union. Energy Policy 38:1455–1469

Bhandari D, Shrimali G (2017) The perform, achieve and trade scheme in India: an effectiveness analysis. Renew Sustain Energy Rev 81:1286–1295

Bhandari D, Shrimali G (2018) The perform, achieve and trade scheme in India: An effectiveness analysis. Renew Sustain Energy Rev 81:1286–1295

Carmona M, Feria J, Golpe AA, Iglesias J (2017) Energy consumption in the US reconsidered. Evidence across sources and economic sectors. Renew Sustain Energy Rev 77:1055–1068

Chow GC (1960) Tests of equality between sets of coefficients in two linear regressions. Econometrica 28:591–605

Christiansen AC, Wettestad J (2003) The EU as a frontrunner on greenhouse gas emissions trading: how did it happen and will the EU succeed? Clim Policy 3:3–18

Clarkson PM, Li Y, Pinnuck M, Richardson GD (2015) The valuation relevance of greenhouse gas emissions under the European Union carbon emissions trading scheme. Eur Account Rev 24:551–580

Dasgupta S, Roy J (2017) Analysing energy intensity trends and decoupling of growth from energy use in Indian manufacturing industries during 1973–1974 to 2011–2012. Energ Effic 10:925–943

de Andrade Guerra JBSO, Berchin II, Garcia J et al (2021) A literature-based study on the water-energy-food nexus for sustainable development. Stoch Env Res Risk Assess 35:95–116

de la Rue du Can S, Khandekar A, Abhyankar N, Phadke A, Khanna NZ, Fridley D, Zhou N (2019) Modeling India’s energy future using a bottom-up approach. Appl Energy 238:1108–1125

Dutta M, Mukherjee S (2010) An outlook into energy consumption in large scale industries in India: the cases of steel, aluminium and cement. Energy Policy 38:7286–7298

Franzò S, Frattini F, Cagno E, Trianni A (2019) A multi-stakeholder analysis of the economic efficiency of industrial energy efficiency policies: empirical evidence from ten years of the Italian white certificate scheme. Appl Energy 240:424–435

Gaurav N, Sivasankari S, Kiran GS, Ninawe A, Selvin J (2017) Utilization of bioresources for sustainable biofuels: a review. Renew Sustain Energy Rev 73:205–214

Greene WH (2008) Econometric analysis. Prentice Hall, Saddle River, USA

Hamrin J, Vine E, Sharick A (2007). The potential for energy savings certificates as a major tool in greenhouse gas reduction programs. Report of the Center for Resource Solutions, Henry P. Kendall Foundation, Boston, MA, USA. Available at: http://resource-solutions.org/wp-content/uploads/2015/08/Draft_Report_ESC_V12_cleanFINAL_5-24-07.pdf

Hausman JA (1978) Specification tests in econometrics. Econometrica 46:1251–1271

Hsiao C (2007) Panel data analysis-advantages and challenges. TEST 16:1–22

Hsiao C, Mountain DC, HO-Illman K (1995) Bayesian Integration of end use metering and conditional deman analysis. J Econom 109:107–150

Hudedmani MG, Soppimath VM, Hubballi SV, Kundur Z (2019) Perform achieve and trade (PAT) a revolutionary measure in energy efficiency and conservation-review. Int J Adv Sci Eng 6:1206–1212

Kumar A (2003) Energy intensity: a quantitative exploration for Indian manufacturing. IGIDR Working Paper, 152. Available at http://papers.ssrn.com/sol3/papers.cfm?abstract_id=468440

Kumar R, Agarwala AK (2013) Renewable energy certificate and perform, achieve, trade mechanisms to enhance the energy security for India. Energy Policy 55:669–676

Langniss O, Praetorius B (2006) How much market do market-based instruments create? An analysis for the case of white certificates. Energy Policy 34:200–211

Liming H (2009) Financing rural renewable energy: a comparison between China and India. Renew Sustain Energy Rev 13:1096–1103

Mukherjee K (2008) Energy use efficiency in US manufacturing: a nonparametric analysis. Energy Econ 30:76–96

Oak H (2017) Factors influencing energy intensity of Indian cement industry. Int J Environ Sci Dev 8:331–336

Sahu SK, Narayanan K (2014) Energy use patterns and firm performance: evidence from Indian industries. J Energy Dev 40:111–133

Sahu S, Narayanan K (2009) Determinants of energy intensity: a preliminary investigation of Indian manufacturing industries. In: Proceedings of the 44th conference of The Indian Econometrics Society, 16606. https://mpra.ub.uni-muenchen.de/16606/1/MPRA_paper_16606.pdf

Saikawa E, Trail M, Zhong M et al (2017) Uncertainties in emissions estimates of greenhouse gases and air pollutants in India and their impacts on regional air quality. Environ Res Lett 12:065002

Sharma A, Roy H, Dalei NN (2019) Estimation of energy intensity in Indian iron and steel sector: a panel data analysis. Stat Trans New Ser 20:107–121

Springer U, Varilek M (2004) Estimating the price of tradable permits for greenhouse gas emissions in 2008–12. Energy Policy 32:611–621

Teng Y (2012) Indigenous R &D, technology imports and energy consumption intensity: evidence from industrial sectors in China. Energy Procedia 16:2019–2026

UNIDO (2012) Industrial energy efficiency for sustainable wealth creation: capturing environmental, economic and social dividends. Industrial Development Report 2011, United Nations Industrial Development Organization (UNIDO), Vienna, Austria.

Vasudevan R, Cherail K, Bhatia R, Jayaram N (2011) Energy efficiency in India: history and overview. Alliance for an Energy Efficient Economy, New Delhi, India

Verbeek M (2008) A guide to modern econometrics. Wiley, Chichester, UK

Vig S, Datta M (2023) The impact of corporate governance on sustainable value creation: a case of selected Indian firms. J Sustain Finance Invest. https://doi.org/10.1080/20430795.2021.1923337

Vine E, Hamrin J (2008) Energy savings certificates: a market-based tool for reducing greenhouse gas emissions. Energy Policy 36:467–476

Wang Q, Yuan X, Ren L, Ma C, Zhang K (2010) Is there a concrete relationship between energy consumption, economic development and environmental load in developing economies? A case study in Shandong Province, China. Stoch Env Res Risk Assess 24:1225–1231

Zhang ZX (1998) Greenhouse gas emission trading and the world trading system. J World Trade 32:219–239

Funding

None.

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Competing interests

The authors have not disclosed any competing interests.

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Sharma, P., Sharma, A., Leiva, V. et al. Assessment of profitability and efficiency of regulatory acts on energy-intensive industries: a panel data methodology and case study in India. Stoch Environ Res Risk Assess 37, 5009–5027 (2023). https://doi.org/10.1007/s00477-023-02536-8

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00477-023-02536-8