Abstract

Ever since the end of the Great Recession, the US economy has experienced a period of mild inflation, which contradicts with the output–inflation relationship depicted by a traditional Phillips curve. This paper examines how the permanent output loss during the Great Recession has affected the ability of the Phillips curve to explain US inflation dynamics. We find great similarity among several established trend–cycle decomposition methods: potential output declined substantially after the Great Recession. Due to the fact that a lower level of potential output implies a lesser deflationary pressure, we then show that the Phillips curve does predict a period of mild inflation. This finding is largely consistent with the observed data.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Other than the fact that it is the greatest economic downturn in post-WWII US history, the “Great Recession” associated with the onset of the sub-prime crisis in 2008 receives particular attention for the puzzling relationship between weak economic activities and moderate inflation afterward. In particular, Ball and Mazumder (2011) estimate a standard Phillips curve with the Congressional Budget Office’s (CBO) measures of output gaps and find that the predicted deflation was absent during the period from 2008 to 2010. This “missing deflation” puzzle has prompted an array of research on the changing dynamics of US inflation.

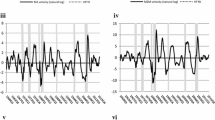

Given a steady level of inflation expectation, the Phillips curve describes a positive relationship between inflation and output gap, usually measured by the deviation of real output from its potential, or trend, level. However, output gap is not directly observable and can be measured using different estimation methods, which show great variations in their results. Figure 1 shows two widely used estimates of output gap, the CBO output gap and the Hodrick–Prescott (HP) filtered gap. The differences between them are striking: the HP-filtered estimates indicate a substantial degree of potential output loss during and after the Great Recession, while the CBO estimates imply the opposite. The notion that recessions can have permanent effects is not novel (e.g., Hamilton 1989; Kim et al. 2005); thus the possibly substantial declines in the potential output thus provide a plausible explanation for the absence of deflation in the post-2008 era.

The measures of the output gap and the potential output (2005:1–2013:3). These estimates were obtained using the sample from 1947:1

In this paper, our aim is to investigate the extent to which the missing deflation puzzle can be explained by the potential output loss during the Great Recession. Our empirical strategy is comprised of two steps. First, we will construct different potential output measures by several established methods. Second, we will study the inflation dynamics during the Great Recession through the lens of both backward- and forward-looking Phillips curves.

In order to measure the potential output variations, we consider a wide range of established and commonly used filtering methods, including the HP filter, unobserved-component models, the Beveridge–Nelson decomposition and neoclassical growth models. Except for the CBO estimates, all measures indicate that a substantial portion of the declines in the US real GDP after 2008 can be considered as permanent. That is, it is likely that the US economy suffered long-term damage to its potential output after the Great Recession (Bijapur 2012; Furceri and Mourougane 2012; Benati 2012; Reifschneider et al. 2013; Ball 2014; Fernald 2014). Our results also support the view that the USA has experienced a one-time, permanent shock to wealth (Bullard 2012).

Can the estimated potential output variations explain the missing deflation? Following Ball and Mazumder (2011), we conduct a dynamic simulation of inflation after 2008 with different output gap measures. We find that the traditional backward-looking Phillips curve with any of the measures considered except the CBO’s predicts near-zero or positive inflation. In order to account for the uncertainty associated with different measures of the output gap, we construct a weighted-averaged dynamic simulation based on the Bayesian information criterion. As a result, both the observed moderate inflation and the severe economic downturn after 2008 can be reconciled to a great extent within a backward-looking Phillips curve, if the potential output variations are considered.

Several studies have pointed out that these puzzling inflation dynamics can be explained by well-anchored inflation expectation (Ball and Mazumder 2011; Matheson and Stavrev 2013) or by higher inflation expectation due to oil price (Coibion and Gorodnichenko 2015). Accordingly, we extend our model by incorporating the forward-looking inflation expectation based on the Survey of Professional Forecasters (SPF) and also considering the core CPI as an alternative inflation measure to remove the effect of oil price fluctuations. Our empirical results are consistent with existing findings: in our extended exercise, the inflation prediction improves substantially with the CBO’s output gap. However, it still sits below the realized path. We then show that the model-averaged simulation accounting for possible lowered potential output does, in fact, capture the inflation dynamics more precisely, suggesting that the potential output variations play an important role in inflation dynamics after the Great Recession.

The outline for the remainder of the paper is as follows. In Sect. 2, we investigate the potential output variations using several trend–cycle decomposition methods. In Sect. 3, we re-assess the missing deflation puzzle using various measures of the potential output. Section 4 is our conclusion.

2 Potential output variations: a retrospective study

2.1 Methods for obtaining the potential output

In this section, we investigate how the potential output evolves, based on the following trend–cycle decomposition methods:

-

The Hodrick–Prescott (HP) filter. The smoothing parameter is set to be 1600 in accordance with quarterly data.

-

The unobserved-component (UC) models.

-

The Beveridge–Nelson (BN) decomposition.

-

The neoclassical growth models, including the one used by CBO.

The HP filter is a convenient mechanical detrending device applied for macroeconomic data, and the other methods hinge on some structural assumptions discussed in what follows.

2.1.1 UC model

The UC model has been a popular detrending method since it was developed in 1980s (Harvey 1985; Watson 1986; Clark 1987, etc). In general, the results obtained from the UC models vary with the assumptions for the econometric modeling of the trend, as well as with those for the cyclical components. In this paper, we adopt a version of the UC model used by Luo and Startz (2014), which nests a wide range of popular assumptions:

In the above model, \(y_t\) is the logarithm of the quarterly real GDP, which consists of a trend component, \(\tau _t\), and a cyclical component, \(c_t\). \(\tau _t\) follows a random walk with a drift \(\mu _t\), which is interpreted as the mean growth rate of the real output. The mean growth rate is assumed to be constant except for a possible one-time structural change.Footnote 1 We assume an unknown break date to be estimated with other model parameters. The cyclical component, \(c_t\), is assumed to follow a stationary AR(2) process. The two shocks, \(\eta _t\) and \(\epsilon _t\), are usually assumed to be jointly normally distributed. We denote this model simply as UC.

In addition, we extend the distributional assumption by specifying skew-normal distributions for the trend and cycle shocks. The skew-normal distribution has an extra shape parameter compared to the normal distribution. It collapses to normal distribution if the shape parameter is estimated to be zero.Footnote 2 We call this UC model with asymmetric shocks the UCSN model. Both models are estimated using Bayesian methods, as detailed in “Appendix A.”Footnote 3

2.1.2 BN decomposition

The BN (Beveridge and Nelson 1981) decomposition is another useful and general approach for trend–cycle decomposition. Given a reduced form ARIMA model, the BN trend is constructed according to the long-horizon conditional forecast of the time series minus any deterministic drift. Following Morley et al. (2003), we specify an ARIMA model for the quarterly growth rate of real GDP (\(\varDelta y_t\)) as follows:

where \(\varPhi (L)\) and \(\varPsi (L)\) denote lag polynomials with all roots outside the unit circle. The order of the lag polynomials is set to be 2. To account for the structural breaks in the mean growth rate, we allow \(\mu \) to break at 1973:1 and 2006:1 (Perron and Wada 2009; Luo and Startz 2014). The model is cast into a state space form and estimated using the maximum likelihood estimation, and the BN trend component can be constructed based on the parameter estimates.

2.1.3 Neoclassical growth model

As for the neoclassical growth model, we first adopt the estimates provided by the CBO, due to its popularity in the empirical literature. In addition, we estimate the potential output based on CBO’s method, but use the short-run unemployment rate instead of the total unemployment rate, to capture cyclicality of any variable.Footnote 4 We denote the latter as CBO-SR. Use of the short-run unemployment rate is motivated by dramatic changes in the composition of the total unemployed since the onset of the Great Recession: the long-term unemployment rate had been stable at approximately 1% for six decades but skyrocketed to 4% in 2010.Footnote 5 As the long-term unemployment can possibly be transformed into structural unemployment (Weidner and Williams 2011; Daly et al. 2012), the short-term unemployment rate may be a more representative indicator of business cycles.Footnote 6

2.1.4 Brief assessment of the different methods

Potential output conceptually exists but is unobserved. Hence a degree of subjective judgment is usually needed as to what is a legitimate detrending method.

The methods we include are notably different in terms of prior views and assumptions. The HP filter is easy to apply but lacks consistency with some economic notions, in that it assumes the output gap is simply white noise. Also, the choice of the smoothing parameter is hard to justify in a transparent way. The BN approach allows the trend component to be nonlinear. However, without parameter instability, it usually implies small and noisy cycle components (Morley et al. 2003) that are inconsistent with economic intuitions.Footnote 7 By contrast, the UC approaches and production function methods can be flexible in adapting a wide range of econometric assumptions and economic relationships. Nonetheless, detrending results are somewhat sensitive to specifications.

Furthermore, revisions between real-time and ex-post estimates affects results differently, depending on which of the various methods is used. It appears that the two-sided filters (HP and UC) give a higher weight to the end of sample observations, which are likely to be significantly revised (Cotis et al. 2004). Therefore, their estimates are likely to experience higher revisions than those produced by production function approaches at the last points of the estimation.

We would like to emphasize that we choose the set of methods we use because they are representative of the methods widely used in various literature. Cotis et al. (2004) summarizes properties of a wide range of detrending devices based on what they called “core requirements” or “user specific requirements,” corresponding to criteria that are universally in consideration or only relevant when estimates of potential outputs and output gaps are used for specific purposes. We refer interested readers to their paper for an extensive discussion.

2.2 Comparing different potential output estimates

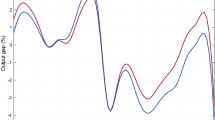

Figure 2 shows the six measures of the output gap considered in this paper for the financial crisis of 2008.Footnote 8 For the Great Recession, the CBO and the CBO-SR exhibit the first and second deepest troughs. In other words, they suggest the least potential output loss during this period. The CBO estimate still exhibits a large negative gap until the end of our samples, four years after the Great Recession ended, about 4% below trend. However, all the other measures suggest that the output gap has been closed despite slightly different historical estimates.

The measures of the output gap. Estimates were obtained using the US quarterly real GDP from 1947:3 to 2013:3

The retrospective analysis points out that the potential output may have declined after the Great Recession. That is, a substantial proportion of the output loss can be considered as permanent or long term. Nonetheless, uncertainty remains as to which measure fits the data best. In the next section, we will account for this issue through the model averaging. Existing literature has suggested that the prolonged recession and subsequent slow recovery could have damaged the long-term capacity of the economy, as well as lowered the potential output through, e.g., less investment (Reifschneider et al. 2013) and R&D activities (Ouyang 2011 and Haltmaier 2012). Bullard (2012) argues that the economy was disrupted by a permanent, one-time shock to wealth, which lowered consumption and output. In fact, the long-term damages to the potential output of the US economy after the Great Recession have been found in many studies, e.g., Bijapur (2012), Furceri and Mourougane (2012), Benati (2012), Reifschneider et al. (2013), Ball (2014) and Fernald (2014). Furthermore, the lack of a period of temporary high-speed growth following the end of a recession (Ng and Wright 2013) also implies there could be some extent of long-term declines in the real output, at least to some extent.

3 Inflation dynamics after the great recession

The financial crisis, which wiped out people’s wealth, forced households to reduce consumption and weakened corporations’ abilities to invest. This can account for a decrease in aggregate demand and also create deflationary pressure. On the other hand, the deflationary pressure will be mitigated if there are long-term damages to the potential output, which suppress the output gap and possibly lead to mild inflation, as observed after the Great Recession. The analysis in the previous section indicates that a great proportion of the real output fluctuations after the Great Recession is likely attributed to the potential output movements. In this section, we investigate its implication on US inflation dynamics in the post-crisis era, through the lens of the Phillips curve.

3.1 The missing deflation and permanent output loss

Ball and Mazumder (2011) examine US inflation dynamics, with particular emphasis on the Great Recession, using an accelerationist Phillips curve as follows:

where \(\pi _t\) is the annualized quarterly inflation of CPI, \(\pi ^e_t\) is the expected inflation, and \(y_t\) is the measure of economic slack, which is measured by the output gap in this paper. We start with following Ball and Mazumder (2011) and assuming purely backward-looking expectations, i.e., \(\pi ^e=0.25\sum _{j=1}^4\pi _{t-j}.\) Ball and Mazumder (2011)’s exercise, with the most recent data set, is as follows: we estimate Phillips curves (4) using the pre-crisis sample from 1981:3 to 2007:4 by ordinary least square and conduct dynamic simulations for the 2008–2013 period.Footnote 9 The output gap to capture inflationary pressure is measured by the CBO output gap as in their paper.

Figure 3 illustrates the updated missing deflation puzzle. The dashed line represents the predicted inflation, which falls to a negative level according to the Phillips curve. However, the actual inflation rate has been consistently positive since the recession ended. Current explanations for the missing deflation have been focusing on a higher expectation of inflation (e.g., Coibion and Gorodnichenko 2015), instability of the slope coefficient (e.g., Matheson and Stavrev 2013; Murphy 2014) and a well-anchored inflation expectation (e.g., Ball and Mazumder 2011).

The dynamic simulation of the CPI, based on the CBO output gap

We provide an alternative point of view as follows: instead of being a “problem” that needs to be solved, the missing deflation may, in point of fact, contain valuable information about the potential output in recent years. As shown in Fig. 3, the negative CBO output gap has persisted long after the end of the Great Recession. As the results, the Phillips curve predicts a continuously declining inflation. Since the output gap may not be as large as what the CBO reports, given the evidence provided in Sect. 2, this “missing deflation” may reflect an under-estimated permanent effect of the Great Recession.

To support our point of view, we re-estimate model (4) above with all output gap measures reported in Sect. 2. To reduce the effect of the supply side, we also apply our analysis to core CPI. The empirical results are presented in Table 1. All estimates based on different measures of the output gap are reasonable; however, their implications for the post-2008 inflation are heterogeneous. Figure 4 shows that, apart from the CBO gap which predicts deflation in the post-crisis period, the other five output gaps suggest a mild inflation rate, ranging from 0 to 4%, at the end of 2013.

The dynamic simulations on inflation with the backward-looking Phillips curve based on estimates reported in Table 1

To account for the uncertainty associated with the measures of the output gap, we take an average of the dynamic simulations weighted across different output gaps as the following:

The weight, \(w_j\), is constructed according to

where BIC is the Bayesian information criteria (BIC) defined as \(LLK-0.5k\ln (T)\), LLK is the log likelihood, k is the number of regressors, and T is the sample size.Footnote 10

Table 1 reports the weight for each model. The highest weight, 0.3017, is assigned to the HP gap for the CPI inflation, but the weights for other gap measures are not negligible. The CBO gap is assigned a weight of 0.1712, considerable but not dominating. As a result, the weighted average of the simulated inflation shown in Fig. 5 shifts toward the positive range. The model-averaged simulation indicates moderate and positive inflation for most of the simulation period, which is in sharp contrast to the simulation based on the CBO output gap. Results and point estimates in the Phillips curve are similar for the core CPI inflation. The model-averaged simulated inflation is brought upward to be mostly around zero, rather than being negative. Over 88% of the model weight, as reported in Table 1, is given to the HP gap, while the other gaps play relatively minor roles.

The model-averaged dynamic simulations on inflation with the backward-looking Phillips curve

3.2 Incorporating forward-looking inflation expectation

Despite the remarkable improvement in the Phillips curve prediction through considering permanent output loss, the performance of the pure backward-looking Phillip curve (4) is not fully satisfactory: it predicts near-zero inflation, which is not consistent with the mild inflation after 2011. One possible reason is that the simple backward-looking inflation expectation does not capture the expectations of producers well enough. We now examine the Phillips curve incorporating both forward- and backward-looking inflation expectation as follows.

where \(\pi ^F_t\) is the forward-looking expectation term and \(\pi ^L_t=\sum _{i=1}^4\pi _{t-i}/4\) is a backward-looking expectation. If \(\theta =0\), the model collapses to the simple model used by Ball and Mazumder (2011).

We use the SPF forecasts of the CPI inflation as a proxy for \(\pi ^F_t\) in both analyses with the CPI and the core CPI inflation.Footnote 11 Table 2 reports the estimates of the Phillips curve (5), and Fig. 6 reports the results from the dynamic simulations.

The dynamic simulations on inflation with forward-looking inflation expectation

Our results are consistent with the existing literature, in that the forward-looking inflation expectation plays an important role. The estimated \(\theta \) is around 0.9 for CPI inflation and around 0.7 for core CPI inflation. However, although greatly improved, the Phillips curve based on the CBO gaps still fails to capture the inflation dynamics for most of the post-Great Recession period: it predicts 0–0.5% inflation rates, which are mostly below the observed numbers (Fig. 7).

The model-averaged dynamic simulations on inflation with forward-looking inflation expectation

On the other hand, the Phillips curve based on other gap measures performs reasonably well in comparison. The predicted inflation rates lie mostly between 1 and 2%. As well, we observe notice that the differences among the predictions with different output gaps are not as dramatic as those with the backward-looking Phillips curve. This result is not surprising, considering the dominating role of the forward-looking component and the stable SPF inflation forecast after the Great Recession.

As in Table 2, the major model weight shifts toward to the UC gap with CPI inflation and to the HP gap with core CPI inflation, while the weight assigned to the CBO’s gap is below 10% in both cases. Therefore, our model-averaged prediction follows the actual data quite closely.

3.3 Wage inflation dynamics

In this subsection, we investigate whether there is missing wage deflation and, if there is, how potential output variations explain wage inflation dynamics. A wage Phillips curve connects wage inflation to unemployment gap, and we adopt the same structure as (4). The measure of wages is based on earnings data for production and nonsupervisory workers from the Establishment Survey. We obtain measures of unemployment gap corresponding to our measures of the output gap through a gap version of Oknu’s law: \(u_t=-0.5y_t\), which comes from a general finding that for every 1% increase in the unemployment gap, the US GDP will be roughly an additional 2% lower than its potential GDP. The estimation sample spans from 1964:1 to 2013:3.

The dynamic simulations on wage inflation with backward-looking inflation expectation

First, we find that there is missing wage deflation. Figure 8 indicates that simulated wage inflation according to the CBO gaps is far below the actual observations. Consistent with our previous results, other gap measures do not imply deflation. Note that the CBO-SR gaps perform very well in explaining wage inflation. Second, we find that wage inflation dynamics are not puzzling if we account for permanent output variations properly. According to Table 3, more weights are put on the CBO gap, compared to estimation results from the price Phillips curve, but about 70% of the model weight is placed on other gap measures. Therefore, the model-averaged simulation shown in Table 3 closely captures the wage inflation dynamics.

4 Conclusion

Our empirical results suggest that the seemingly broken Phillips curve relationship after the Great Recession may be recovered to a great extent if we take permanent output losses into account. We have applied several popular detrending methods to estimate the output gap and found that a large portion of the declines in the real GDP during the Great Recession seems to be permanent. As a result, the Phillips curve with all measures of the output gap, except the CBO’s estimates, predicts mild inflation. A likelihood-based model averaging has been used to account for model uncertainty associated with the choice of detrending method. Finally, we have shown that the model-averaged prediction is largely in line with the observed data.

Given the complicated nature of the economy after the Great Recession, the puzzling post-crisis inflation dynamics may well result from more than one factor. We have shown that well-anchored inflation expectations truly do work to improve Phillips curve prediction substantially; nonetheless the potential output variations play an important role in explaining the post-crisis inflation dynamics.

Notes

Luo and Startz (2014) show that two breaks in the mean growth rate are not as likely as the one break assumption with quarterly real GDP data ended at 2013:3, and the detrending results are fairly similar to both assumptions if uncertainty in break dates is incorporated.

A random variable x follows a multivariate skew-normal distribution, \(SN({\bar{\varOmega }},\alpha )\), with density given by \( f_{SN}(x;{\bar{\varOmega }},\alpha )=2\phi (x;{\bar{\varOmega }})\varPhi (\alpha 'x)\), where \(\phi (x;{\bar{\varOmega }})\) is the pdf of the multivariate zero mean \(N(0,\varOmega )\) and \(\varPhi (.)\) is the cdf of the univariate N(0, 1) distribution.

Methodology and priors are mostly consistent with Luo and Startz (2014). Results are based on 20,000 effective samples after saving one of every 10 draws in 300,000 MCMC simulation and discarding the first 100,000 as burn-in samples.

The CBO’s method uses the unemployment gap—the difference between the total unemployment rate and the NAIRU—as the key variable for obtaining the cyclical components of any variable, as the unemployment gap usually moves up and down closely with the business cycle. See “Appendix B” for details.

The long-term unemployment is defined by the number of civilians unemployed for 27 weeks and longer.

Gordon (2013) also argues that the distinction between short-run and long-run unemployment may help to solve the “case of the missing deflation” after 2008 if the downward pressure on wages and the inflation rate comes mainly from the short-run unemployment.

It is not the case in our estimation as we consider structural breaks in trend growth rates.

Data are publicly available from FRED. Parameter estimates of all models are available by request.

There are two reasons for using data from 1981: first, we will incorporate the SPF inflation forecast, which is only available since 1981, as a proxy for forward-looking expectation. Secondly, the inflation dynamics in this sample period has been relatively stable than that in 1970s, so parameter instability is not a major concern. The empirical results are similar using sample starting from 1985.

The model averaging technique we adopt has been used in many studies. See, for example, Garratt et al. (2008) and Morley and Piger (2012). One can also follow Garratt et al. (2014) for a more sophisticated averaging technique where weights are based on the ability of each specification to provide accurate probabilistic forecasts of inflation.

The SPF forecasts of the core CPI inflation are not available until 2007.

We follow Koop (2003) for the definition of inverse gamma (IG) distribution. If \(x>0\) follows inverse gamma distribution \(IG(s^{-2},\nu )\), the probability density function of x is defined as:

$$\begin{aligned} f(x;s^{-2},\nu )=\left( \frac{2s^{-2}}{\nu }\right) ^{-\frac{\nu }{2}} \frac{1}{\varGamma \left( \frac{\nu }{2}\right) } x^{-\frac{\nu }{2}-1} exp\left( -\frac{\nu }{2s^{-2}x}\right) \end{aligned}$$where \(\varGamma (\cdot )\) is the gamma function.

Such truncation is assumed to avoid unreasonable draws for \(\mu \) and d. As noted in de Pooter et al. (2008), \(\mu \) and d are nearly unidentified when the samples of \(\phi _1\) and \(\phi _2\) get very close to the nonstationary region. In this case, arbitrary real values for \(\mu \) and d can be drawn and cause the Gibbs sampler to have difficulty in moving away from the nonstationary region.

As robustness check, setting the variance for the normal priors to be 10 and priors for \(\sigma _1^2\) and \(\sigma _2^2\) to be IG(100, 0.1) gives similar results.

Thus, there are as many break points as the number of recessions after 1950.

References

Ball LM (2014) Long-term damage from the great recession in OECD countries. Working Paper 20185, National Bureau of Economic Research

Ball L, Mazumder S (2011) Inflation dynamics and the great recession. Brook Pap Econ Acti 42(1):337–405

Benati L (2012) Estimating the financial crisis impact on potential output. Econ Lett 114(1):113–119

Beveridge S, Nelson CR (1981) A new approach to decomposition of economic time series into permanent and transitory components with particular attention to measurement of the business cycle. J Monet Econ 7(2):151–174

Bijapur M (2012) Do financial crises erode potential output? Evidence from OECD inflation responses. Econ Lett 117(3):700–703

Bullard J (2012) Inflation targeting in the USA. Delivered at the Union League Club of Chicago, Breakfast@65West, Chicago, Ill

Clark PK (1987) The cyclical component of U.S. economic activity. Q J Econ 102(4):797–814

Coibion O, Gorodnichenko Y (2015) Is the phillips curve alive and well after all? Inflation expectations and the missing disinflation. Am Econ J Macroecon 7(1):197–232

Cotis JP, Elmeskov J, Mourougane A (2004) Estimates of potential output: benefits and pitfalls from a policy perspective. In: Reichlin L (ed) The Euro area business cycle: stylized facts and measurement issues. Centre for Economic Policy Research, London, pp 35–60

Daly MC, Hobijn B, Şahin A, Valletta RG (2012) A search and matching approach to labor markets: did the natural rate of unemployment rise? J Econ Perspect 26:3–26

de Pooter M, Ravazzolo F, Segers R, van Dijk HK (2008) Bayesian near-boundary analysis in basic macroeconomic time-series models. In: Chib S, Griffiths W, Koop G, Terrell D (eds) Bayesian econometrics, advances in econometrics, vol 23. Emerald Group Publishing Limited, Bingley, pp 331–402

Durbin J, Koopman SJ (2002) A simple and efficient simulation smoother for state space time series analysis. Biometrika 89(3):603–616

Fernald J (2012) A quarterly, utilization-adjusted series on total factor productivity. Working Paper Series 2012-19, Federal Reserve Bank of San Francisco. http://ideas.repec.org/p/fip/fedfwp/2012-19.html

Fernald J (2014) Productivity and potential output before, during, and after the great recession. In: NBER Macroeconomics Annual 2014, vol 29. University of Chicago Press

Furceri D, Mourougane A (2012) The effect of financial crises on potential output: new empirical evidence from OECD countries. J Macroecon 34(3):822–832

Garratt A, Koop G, Vahey SP (2008) Forecasting substantial data revisions in the presence of model uncertainty. Econ J 118(530):1128–1144

Garratt A, Mitchell J, Vahey SP (2014) Measuring output gap nowcast uncertainty. Int J Forecast 30(2):268–279

Gordon RJ (2013) The phillips curve is alive and well: inflation and the nairu during the slow recovery. Tech. rep., NBER working paper

Haltmaier J (2012) Do recessions affect potential output? International Finance Discussion Papers 1066, Board of Governors of the Federal Reserve System

Hamilton JD (1989) A new approach to the economic analysis of nonstationary time series and the business cycle. Econom J Econom Soc 57:357–384

Harvey AC (1985) Trends and cycles in macroeconomic time series. J Bus Econ Stat 3(3):216–227

Kim CJ, Morley J, Piger J (2005) Nonlinearity and the permanent effects of recessions. J Appl Econom 20(2):291–309

Koop G (2003) Bayesian econometrics. Wiley, Hoboken

Luo S, Startz R (2014) Is it one break or ongoing permanent shocks that explains US real GDP? J Monet Econ 66:155–163

Matheson T, Stavrev E (2013) The great recession and the inflation puzzle. Econ Lett 120(3):468–472

Morley J, Piger J (2012) The asymmetric business cycle. Rev Econ Stat 94(1):208–221

Morley JC, Nelson CR, Zivot E (2003) Why are the Beveridge–Nelson and unobserved-components decompositions of GDP so different? Rev Econ Stat 85(2):235–243

Murphy RG (2014) Explaining inflation in the aftermath of the great recession. J Macroecon 40:228–244

Ng S, Wright JH (2013) Facts and challenges from the great recession for forecasting and macroeconomic modeling. J Econ Lit 51(4):1120–1154

Ouyang M (2011) On the cyclicality of R&D. Rev Econ Stat 93(2):542–553

Perron P, Wada T (2009) Let’s take a break: trends and cycles in us real GDP. J Monet Econ 56(6):749–765

Reifschneider D, Wascher W, Wilcox D (2013) Aggregate supply in the United States: recent developments and implications for the conduct of monetary policy. Finance and Economics Discussion Series 2013-77, Board of Governors of the Federal Reserve System (U.S.)

Wang J, Zivot E (2000) A Bayesian time series model of multiple structural changes in level, trend and variance. J Bus Econ Stat 18(3):374–386

Watson MW (1986) Univariate detrending methods with stochastic trends. J Monet Econ 18(1):49–75

Weidner J, Williams JC (2011) What is the new normal unemployment rate? FRBSF Econ Lett 5

Acknowledgements

Thanks to Robert M. Kunst and two anonymous referees for their general advice and Dick Startz for helpful comments.

Author information

Authors and Affiliations

Corresponding author

Additional information

Huang acknowledges support from National Natural Science Foundation of China under Grant 71601129.

Appendices

Appendices

Bayesian inference of the UC model

1.1 Normal innovations

The model containing (1)–(3) can be rewritten into state space form:

where \(x_t=[\tau _t,c_t,c_{t-1}]'\).

In order to ensure that the estimated covariance matrix is positive semi-definite, we decompose the covariance matrix in the following way:

and directly estimate \(\left\{ \sigma _1,\sigma _2,b\right\} \) instead of the covariance matrix parameters \(\left\{ \sigma _{\eta },\sigma _{\epsilon },\rho \right\} \). The posterior samples for the covariance parameters are obtained through transformation.

Independent proper priors are specified for all parameters. \(\sigma _1^2\) and \(\sigma _2^2\) are assumed to have independent inverse gamma priors IG(100, 0.5)Footnote 12. These priors are diffuse and do not have finite moments. Therefore, a heavy weight will be put on sample information. We assume somewhat informative normal priors for \(\phi _1+\phi _2 \sim N(0.5, 1)\), \(\phi _2 \sim N(-0.5, 1)\) and \(b \sim N(0, 1)\). Imposing truncations for \(\mu \in [0, 2]\) and \(d \in [-1, 1]\),Footnote 13 the uniform priors for \(\mu \) and d are over the truncated areas giving truncated normal posteriors accordingly. While the above priors are broadly consistent with estimates from the literature, our estimation results are robust to more diffuse priors.Footnote 14 Lastly, a flat proper prior is assumed for Tb such that all dates from 1947:1 to 2013:2 have equal probability to be the break date in the mean growth rate. Therefore, the joint prior density is the product of all the above marginal prior densities.

Gibbs sampling approach is used to draw posterior samples for parameters including the break date. Sampling the joint posterior distribution of parameters can be conducted by sequential sampling from the conditional distributions. Details on the Gibbs sampling are summarized as follows:

Define \(\theta =[\mu , \phi _1, \phi _2, \sigma _{\eta }, \sigma _{\epsilon }, \rho , d]\). Let \((\cdot )^{(k)}\) denote the kth posterior draw of the latent variable \(x_t\) or the parameters. Y denotes all the observed quarterly log real GDP \(\left\{ y_1,y_2,{\ldots }y_T\right\} \). The kth step in our Gibbs sampler involves the following blocks:

-

Draw \(\left\{ x_t^{(k)}:t=1,{\ldots }T\right\} \sim f(x_1,{\ldots }x_T|Y, \theta ^{(k-1)}, Tb^{(k-1)})\) obtained from the simulation smoother developed by Durbin and Koopman (2002). We then obtain \(\tau _t^{(k)}\) and \(c_t^{(k)}\) as the first two elements in \(x_t^{(k)}\), as well as the residual terms \([\hat{\eta }_t,\hat{\epsilon }_t]'\).

-

Draw \(\left[ \phi _1^{(k)},\phi _2^{(k)}\right] \sim f(\phi _1,\phi _2|Y, x_t^{(k)}, \sigma _{\epsilon }^{(k-1)})\) given that the second row in (A.2) has the following regression form:

$$\begin{aligned} c_t= \left[ \begin{array}{c@{\quad }c} c_{t-1}&c_{t-2} \end{array} \right] \left[ \begin{array}{c} \phi _1 \\ \phi _2 \end{array} \right] + \epsilon _t \end{aligned}$$(A.4)Stack (A.4) by time, we have

$$\begin{aligned} Y_c=C \varPhi +\epsilon \end{aligned}$$where \(Y_c=\left\{ c_3^{(k)},{\ldots },c_T^{(k)}\right\} '\), \(\epsilon =\left\{ \epsilon _3,{\ldots },\epsilon _T\right\} '\mathop {\sim }\limits ^{i.i.d.} N(0,1/h_{\epsilon })\) with \(h_{\epsilon }=(\sigma _{\epsilon }^{(k-1)})^{-2}\), \(\varPhi =\left\{ \phi _1+\phi _2,\phi _2\right\} '\) and

$$\begin{aligned} C=\left[ \begin{array}{c@{\quad }c} c_2 &{} c_1-c_2\\ \vdots \\ c_{t-1} &{} c_{t-2}-c_{t-1}\\ \vdots \\ c_{T-1} &{} c_{T-2}-c_{T-1} \end{array}\right] \end{aligned}$$Given multivariate normal prior \(N(\varPhi _0,V_{\varPhi 0})\) for \(\varPhi \), the posterior distribution follows a multivariate normal distribution \(N(\tilde{\varPhi },\tilde{V}_{\varPhi })\), where

$$\begin{aligned} \tilde{V}_{\varPhi }&=\left( V_{\varPhi 0}^{-1}+h_{\epsilon }C'C\right) ^{-1}\end{aligned}$$(A.5)$$\begin{aligned} \tilde{\varPhi }&=\tilde{V}_{\varPhi }\left( V_{\varPhi 0}^{-1}\varPhi _0+h_{\epsilon }C'Y_c\right) \end{aligned}$$(A.6)The posterior samples for \(\left[ \phi _1^{(k)},\phi _2^{(k)}\right] \) must guarantee the stationarity of the process. Therefore, we discard nonstationary draws and regenerate new ones until they meet the stationary requirement.

-

Draw \(\left[ \mu ^{(k)},d^{(k)}\right] \sim f(\mu , d|Y, x_t^{(k)}, \sigma _{\eta }^{(k-1)})\) given the regression in the first row of (A.2):

$$\begin{aligned} \tau _t-\tau _{t-1}= \left[ \begin{array}{c@{\quad }c} 1&1(t>Tb) \end{array} \right] \left[ \begin{array}{c} \mu \\ d \end{array} \right] + \eta _t \end{aligned}$$(A.7)Stack (A.7) by time, we have

$$\begin{aligned} Y_{\tau }=D \left[ \begin{array}{c} \mu \\ d \end{array} \right] +\eta \end{aligned}$$where \(Y_{\tau }=\left\{ \tau _2^{(k)}-\tau _1^{(k)},{\ldots },\tau _T^{(k)}-\tau _{T-1}^{(k)}\right\} '\), \(\eta =\left\{ \eta _2,{\ldots },\eta _T\right\} '\mathop {\sim }\limits ^{i.i.d.} N(0,1/h_{\eta })\) with \(h_{\eta }=(\sigma _{\eta }^{(k-1)})^{-2}\) and

$$\begin{aligned} D=\left[ \begin{array}{c@{\quad }c} 1 &{} 0\\ \vdots &{} \vdots \\ 1 &{} 1(t>Tb)\\ \vdots &{} \vdots \\ 1 &{} 1 \end{array}\right] \end{aligned}$$Given uniform priors \(\mu \sim [0,2]\) and \(d\sim [-1,1]\), the posterior distribution follows a truncated multivariate normal distribution. It is equivalent to sampling the posterior from \(N(\tilde{M},\tilde{V}_M)\) and discard the samples out of the valid region, where

$$\begin{aligned} \tilde{V}_M&=(h_{\eta }D'D)^{-1}\end{aligned}$$(A.8)$$\begin{aligned} \tilde{M}&=h_{\eta }\tilde{V}_MD'Y_{\tau } \end{aligned}$$(A.9) -

Draw \(\left[ \sigma _1^{(k)},\sigma _2^{(k)}\right] \sim f(\sigma _1,\sigma _2|Y, x_t^{(k)}, \mu ^{(k)}, d^{(k)}, \phi _1^{(k)}, \phi _2^{(k)}, b^{(k-1)})\). Define \(\eta _t^*=\eta _t\sim N(0,\sigma _1^2)\) and \(\epsilon ^*_t=-b{\eta }_t+{\epsilon }_t \sim N(0,\sigma _2^2)\), and we have the following:

$$\begin{aligned} B^{-1} \left[ \begin{array}{c} \hat{\eta }_t\\ \hat{\epsilon }_t \end{array} \right] = \left[ \begin{array}{c} \hat{\eta }_t\\ -b\hat{\eta }_t+\hat{\epsilon }_t \end{array} \right] = \left[ \begin{array}{c} \hat{\eta _t^*}\\ \hat{\epsilon _t^*} \end{array} \right] \sim N\left( \left[ \begin{array}{c} 0 \\ 0 \end{array} \right] ,\left[ \begin{array}{c@{\quad }c} \sigma _1^2 &{} 0 \\ 0 &{} \sigma _2^2 \end{array} \right] \right) \end{aligned}$$(A.10)where

$$\begin{aligned} B= \left[ \begin{array}{c@{\quad }c} 1 &{}0\\ b &{}1 \end{array} \right] \end{aligned}$$According to (A.10),

$$\begin{aligned} \left[ \begin{array}{c} \eta _t^*\\ \epsilon _t^* \end{array} \right] \sim N\left( \left[ \begin{array}{c} 0 \\ 0 \end{array} \right] ,\left[ \begin{array}{c@{\quad }c} \sigma _1^2 &{} 0 \\ 0 &{} \sigma _2^2 \end{array} \right] \right) \end{aligned}$$(A.11)We assume independent priors for \(h_i^{-1}=\sigma _i^{2}\sim IG(s_{i0}^{-2}, \nu _{i0})\) with \(i=1,2\). It is equivalent to assume a Gamma prior \(G(s_{i0}^{-2}, \nu _{i0})\) for \(h_i\). The posterior of \(h_i\), in this case, is \(G(\tilde{s}_i^{-2}, \tilde{\nu }_i)\), where for \(i=1,2\)

$$\begin{aligned} \tilde{\nu }_i&=T+\nu _{i0}\end{aligned}$$(A.12)$$\begin{aligned} \tilde{s}_1^{2}&=\frac{\eta ^{*'}\eta ^*+\nu _{10}s_{10}^{2}}{\tilde{\nu }_1}\end{aligned}$$(A.13)$$\begin{aligned} \tilde{s}_2^{2}&=\frac{\epsilon ^{*'}\epsilon ^*+\nu _{20}s_{20}^{2}}{\tilde{\nu }_2}\end{aligned}$$(A.14)$$\begin{aligned} \eta ^{*}&=\left[ \eta ^{*(k)}_1,{\ldots },\eta ^{*(k)}_T\right] '\end{aligned}$$(A.15)$$\begin{aligned} \epsilon ^{*}&=\left[ \epsilon ^{*(k)}_1,{\ldots },\epsilon ^{*(k)}_T\right] ' \end{aligned}$$(A.16) -

Draw \(b^{(k)} \sim f(b|Y, x_t^{(k)}, \mu ^{(k)}, d^{(k)}, \phi _1^{(k)}, \phi _2^{(k)}, \sigma _2^{(k)})\). Given the second row in (A.10), we have a standard regression to sample b:

$$\begin{aligned} \hat{\epsilon }_t=\hat{\eta }_t b+\epsilon _t^* \end{aligned}$$(A.17)where \(\epsilon _t^* \sim N(0, \sigma _2^2)\).

Stack (A.17) by time, we have

$$\begin{aligned} \hat{\epsilon }=E b + e^* \end{aligned}$$where \(\hat{\epsilon }=\left\{ \hat{\epsilon }_1^{(k)},{\ldots },\hat{\epsilon }_T^{(k)}\right\} '\), \(E=\left\{ \hat{\eta }_1^{(k)},{\ldots },\hat{\eta }_T^{(k)}\right\} '\) and \(e^*=\left\{ \epsilon ^*_1,{\ldots },\epsilon ^*_T\right\} '\mathop {\sim }\limits ^{i.i.d.} N(0,1/h_{s2})\) with \(h_{s2}=(\sigma _{2}^{(k)})^{-2}\). \(\hat{\eta }_t^{(k)}\) and \(\hat{\epsilon }_t^{(k)}\) are residuals in the first two rows in (A.2).

Given normal prior \(N(b_0,V_{b0})\) for b, the posterior distribution follows a normal distribution \(N(\tilde{b},\tilde{V}_b)\), where

$$\begin{aligned} \tilde{V}_b&=\left( V_{b0}^{-1}+h_{s2}E'E\right) ^{-1}\end{aligned}$$(A.18)$$\begin{aligned} \tilde{b}&=\tilde{V}_b\left( V_{b0}^{-1}b_0+h_{s2}E'\hat{\epsilon }\right) \end{aligned}$$(A.19) -

Draw \(Tb^{(k)} \sim f(Tb|Y, \theta ^{(k)})\). According to Wang and Zivot (2000), given the flat proper prior assumed for Tb,

$$\begin{aligned} f(Tb|Y,\theta )&=\frac{f(Y|Tb,\theta )f(Tb|\theta )}{f(Y|\theta )} \nonumber \\&\propto f(Y|Tb,\theta )f(Tb) \nonumber \\&\propto f(Y|Tb,\theta ) \end{aligned}$$(A.20)According to (A.20), we can draw Tb from a multinomial distribution where \(f(Tb|Y,\theta )=\frac{f(Y|Tb,\theta )}{\sum _{t=1}^{T-1}{f(Y|Tb=t,\theta )}}\)

1.2 Skew-normal innovations

A linear Gaussian state space model:

where \(\varvec{\omega }=\hbox {diag}(\omega _1,\ldots ,\omega _d)\) and \(\varvec{\sigma }=\hbox {diag}(\sigma _1,\ldots ,\sigma _r)\). In what follows, matrix with upper bar represents a correlation matrix. A linear skew-normal state space model deviates the Gaussian one by assuming that

Note that a random variable x follows a multivariate skew-normal distribution, \(SN({\bar{\varOmega }},\alpha )\), with density given by

where \(\phi (x;{\bar{\varOmega }})\) is the pdf of the multivariate zero mean \(N(0,\varOmega )\) abd \(\varPhi (.)\) is the cdf of the univariate N(0, 1) distribution.

In our Bayesian analysis, we use the following stochastic representation of the multivariate skew-normal distribution.

where \(\delta =[\delta _1,\delta _2,\ldots ]'\) and \(D(\delta )=\sqrt{I-\hbox {diag}(\delta )^2}\). The random variable Z follows a half normal \(N^+(0,1)\) and U a normal \(N(0,{\bar{\varPsi }})\). Note that there is a 1-to-1 relation between \(({\bar{\varOmega }},\alpha )\) and \((\delta ,{\bar{\varPsi }})\):

where \(\lambda =D(\delta )^{-1}\delta \).

The scaled error terms thus have the following distributions:

The corresponding stochastic representation is as follows:

The only difficulty comes from the non-Gaussian term \(Z=[Z_m,Z_s]\). Conditional on Z, however, the model reduced to the following standard linear Gaussian state space model:

The FFBS can be used to draw samples from conditional distribution of \(\beta ^T\). Therefore, the Gibbs sampler will be completed by drawing sample from conditional distribution of Z given \(\epsilon ^T\) and \(\eta ^T\). Note that \(y_t-H\beta _t=\epsilon _t\) and \(\beta _t-F\beta _{t-1}=\eta _t\).

Take \(Z_m\) as example. Conditional on \(\epsilon ^T\) and other parameters,

Therefore, completing the square leads to the conditional distribution as follows:

Conditional on Z and other blocks, we have the following regression system:

Drawing \(\theta _m\) and \(\varSigma _m\) can be done easily.

Estimates of the output gap using CBO’s method

The CBO estimates the potential output based on a neoclassical growth model, in which the output is determined by the production function as follows:

where L represents hours worked, K is capital input, TFP is total factor productivity, and C is a constant. The potential output, denoted by \(Y^*\), is then computed by

where \(L^*\) and \(\hbox {TFP}^*\) are potential level of hour worked and total factor productivity.

The key device used by the CBO to obtain the potential level of a variable X is a cyclical adjustment equation as follows:

\(f_t(\beta )\) is a linear function of time which breaks at the peak in the business cycle.Footnote 15 U is the unemployment rate, and \(U^*\) is the CBO’s estimates of the natural rate of unemployment. Equation (B.3) can be estimated consistently using the ordinary least squares for all variables needed to construct CBO’s potential output estimates.

The new potential output can be written as

where \(y_\mathrm{nf}\) is the potential output in the nonfarm business sector, and \(y_\mathrm{other}\) is the real output in other sector. CBO estimates \(y_\mathrm{nf}\) using a neoclassical growth model, but using the cyclical adjustment Eq. (B.3) to obtain \(y_\mathrm{other}\) due to data availability. We take an approximation of the above equation around the CBO’s estimate, denoted by superscript \(*\), as follows:

Thus, we only need to compute the two term on the right-hand side; then, we can obtain the potential output \(\ln ({\hat{y}})\). Note that

The variables with \(\hat{\quad }\) are obtained using cyclical adjustment Eq. (B.3) with the short-run unemployment rate, while those with \(*\) are using Eq. (B.3) with total unemployment rate. The total factor productivity of the nonfarm business sector is obtained from Fernald (2012). For the other sector, we obtain the real output in other sector by subtracting real output in the nonfarm business sector from the total real output. The potential output in the other sector is thus constructed using cyclical adjustment Eq. (B.3).

We are confronted with a minor difficulty while using cyclical adjustment Eq. (B.3) with the short-run unemployment rate. The natural rate of the short-run unemployment is not available and needed to be estimated. Let \(p_s\) be the sample mean of the proportion of the short-run unemployment in the total unemployment, which is 0.8331 in our sample. We obtain the estimates of the natural rate of the short-run unemployment by \(p_s\times U^*\), where \(U^*\) is the CBO’s estimates of the natural rate of unemployment.

Measures of the output gaps from 1947:3 to 2013:3

Figure 9 shows the estimated output gap from 1947:3 to 2013:3.

Measures of the output gap

Rights and permissions

About this article

Cite this article

Huang, YF., Luo, S. Potential output and inflation dynamics after the Great Recession. Empir Econ 55, 495–517 (2018). https://doi.org/10.1007/s00181-017-1293-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s00181-017-1293-7