Abstract

Ever since the “Wenchuan earthquake” in May 12, 2008, there are some other earthquakes every year in China. China seems at the stage with active earthquakes. However, there is nothing the government can do to prevent such natural disasters. Instead the government can only try to issue alert information and to build an efficient afterward recovering system. Earthquake insurance could be an effective way to provide additional recovering money besides government funds. But the question is whether consumers are willing to buy and pay for earthquake insurance if government is not paying. Therefore, this chapter is to investigate Chinese residents’ preferences for earthquake insurance, especially to analyze their willingness to accept and willingness to pay for earthquake insurance. Previous studies have shown that risk perception, social trust, and consumers’ characteristics have significant impact on consumers’ earthquake insurance. Thus the measure of association was used to analyze Chinese consumers’ preferences, followed by a short case for “Pearl River Delta” region in China. The data was collected though an online survey in Shenzhen, a core city in “Pearl River Delta” region. A total of 637 surveys were returned, and of those collected, 428 are valid. The results indicate that consumers are willing to buy and pay for earthquake insurance for higher-risk regions. However, for the lower-risk regions, government has to put more effort on increasing social trust for consumers. In addition, insurance companies need to provide earthquake property insurance product and earthquake life insurance product separately and together too according to consumers’ different preferences.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

1 Introduction

After the “Wenchuan earthquake” in May 12, 2008, residents in China started to pay much more attention to all information related to earthquakes. Specifically, they concern the possibility of having another huge earthquake in China, especially in their own region. From May 12, 2008, to May 24, 2014, there are 11 earthquakes in China with magnitude over 4.0 including the 2010 Yushu earthquake and the 2013 Ya’an earthquake. It seems China is at the stage with active earthquakes. However, there is nothing the government can do to prevent such kind of natural disaster. Instead the government can only try to issue alert information and to build an efficient afterward recovering system. Earthquake insurance could be an effective way to provide additional recovering money besides government funds. Therefore, it is important for China to design acceptable but indeed helpful earthquake insurance for Chinese residents. Thus, to study the earthquake insurance from consumers’ perspective becomes crucial today. China central government announced to design an earthquake insurance system in Shenzhen and Yunan province first before that for a whole country.

The percentage of homeowners who have purchased earthquake insurance has declined over the years, both in California and across the United States. The question is: could the earthquake insurance be successful in China? If so, what should China do? Therefore, the objective of this chapter is to investigate Chinese residents’ preference for earthquake insurance, especially to analyze their willingness to accept and willingness to pay for insurance from insurance consumers’ demographics and to provide Chinese government and insurance companies very important policy implications and managerial implications.

2 Conceptual Overview

Whether a consumer decides to buy earthquake insurance or not could be affected by many factors. Especially, if consumers have existing experience of buying other types of insurance before (pre_insurance), they might tend to buy earthquake insurance too when this type of insurance is available. Of course, risk and social trust can also affect consumers’ earthquake insurance buying decisions.

2.1 Risk Perception

Lichtenstein et al. (1978) observed systematic bias in the judged frequency of lethal events. This finding emphasized the important role of investigating social risk perception and determination of the source of the error. A study by Johnson et al. (1993) showed that deformation in people’s risk perception and framing effects existed in both the real world and in experimental researches and influenced consumers’ decisions about insurance purchasing. People tended to buy more insurance against moderately high probability, small-loss events than low-probability, high-loss events (Slovic et al. 1977). The experiments conducted by Schoemaker and Kunreuther (1979) showed that people’s limited abilities to deal with risk information and limited sensitivity to low-probability events and suggested future research on factors affecting insurance purchasing decisions. Understanding consumer characteristic affection on insurance decision and individuals’ behaviors in various types of insurance is important for public and private sectors (Showers and Shotick 1994).

In the process of decision making, a strong assumption provided in Smith’s (1968) standard insurance demand model argues that an individual can correctly predict the probability associated with all possible loss distribution. So far, the standard model cannot perfectly explain some specific behaviors on considering whether to buy insurance under uncertainty or about the probability or extent of catastrophe loss. In fact, the consideration on whether to adopt disaster loss mitigation measures can be attributed to what is called the “reflect effect” suggested by Kahneman and Tversky (1979). It indicates that the prediction of an individual’s choices in dealing with risk will reflect around the current situations and the attitude of the decision maker toward risk perception (Schwartz and Hasnain 2002). Similarly, risk perception and selection play a vital role for efficient risk sharing in natural-catastrophe insurance and then the purchasing of individual (Jametti and von Ungern-Sternberg 2010), and willingness to pay will be also affected by risk perception. Wang et al. (2012) investigated people’s risk perception into the analysis of people’s insurance choice in China after the Wenchuan earthquake. After that, Ye and Wang (2013) explored risk attitude through a comparative experimental method and its implication to catastrophe insurance practice in China and found that uncertainty about the risk perception and risk mitigation when people are faced up with purchasing choice results in a tendency of ignorance and rejection. Therefore, if individuals perceived an earthquake before (Per_risk), there is a higher chance that they will buy earthquake insurance.

2.2 Social Trust

Dating back to the 1970s, an earlier report has showed that when residents discuss with friends, neighbors, and family members, the likelihood of purchasing natural disaster insurance could increase (Kunreuther 1978). Based on other earlier research, Kunreuther and Michel-Kerjan (2009) showed that when respondents heard that other people have bought insurance against catastrophe risks, they become encouraged to follow the same behaviors even without changing their thoughts about the risks they faced or knowing about the price of coverage. Social trust can also lead to premature cancelation of insurance policies after some years of coverage without making any claim of insured damage. Respondents observe and tend to follow the behaviors of their neighbors and other people in social network when deciding whether to spend on mitigating the catastrophe risks they faced.

Focuses have been raised about the standard role of social trust and interdependencies. Kuran (1995) believes that social trusts are social artifacts that dissimulate individual true intentions and result in undesirable social outputs. In a similar way, Kunreuther and his colleagues (2009) argue that social interdependencies are likely to obstruct selection of effective risk mitigation choices and exacerbate the cognitive bias the individuals encounter.

Social trust is viewed in a more positive light in the study of adaptive institutions. Operating social networks can generate social assets and give impetus to collective action (Ostrom 2000). Networked relationships among members of community, media, and government, built on the rules of mutual trust and coactions, enable the sharing of knowledge, risk, and resources and can support recovery from natural disasters and the resulting economic shocks through mutual aids. Social trust and networks are generally deemed to be conducive to adapting communities to disaster risk and reducing their vulnerability (Pelling and High 2005; Nelson et al. 2007; Adger 2003), despite some counterevidence (Wolf et al. 2010). Affirmative empirical evidences exist in the literature of disaster risk management (Wong and Zhao 2001), but very few pertain to the purchase of catastrophe insurance specifically, let alone earthquake insurance. In this research, because of unpopularity and unfamiliarity among Chinese, we will not estimate the influence of neighbors’ choice. So we just put our focus on four aspects, government information trust, social media information trust, agreement of earthquake insurance program, and satisfaction of government current policy.

Therefore, social trust can also lead to premature cancelation of insurance policies after some years of coverage without making any claim of insured damage. Therefore, four aspects of social trust were concentrated in our study, including government information trust about earthquake peril (Gover_Inform), social media information trust about earthquake peril (Media_Inform), agreement of earthquake insurance program (G_Policy), and satisfaction of government current policy (Mitigation).

If an individual has more trust in government and media, she/he would be more easily influenced by the “reputational externalities effect” of risk information (Zeckhauser 1996; Swim et al. 2009; Norgaard 2011). This effect forms a sense for the respondents to believe that the catastrophic loss would more likely occur at some future time. It then has a positive influence on the attitude toward buying insurance. A positive relationship between G_Policy and insurance purchase and willingness to pay is also expected. Browne and Hoyt (2000) suggested that the government’s investment in earthquake protection is a substitute for insurance. If this is the case, the increased trust in government’s artificial disaster prevention measures would decrease the willingness to buy insurance. The effect of Mitigation on insurance purchase is thus hypothesized as negative (Fig. 7.1).

Conceptual framework

Therefore, for different consumers, to calculate the measure of association could provide government and insurance company more accurate information on reducing risk perception and increasing social trust to increase the probability for consumers to buy and their willingness to buy for earthquake insurance.

3 Why It Concerns Management?

To build an efficient earthquake insurance system, it’s very important how key stakeholders act within the system and outside the system. Among all stakeholders, the most important ones are government, insurance companies, and consumers. Therefore, to study from consumers’ perspectives, it can provide insights on managerial implication for both government and insurance companies.

4 Key Statistical Insights

An online questionnaire survey was undertaken in the online survey platform named Wenjuanxing which is a professional research institution. Questionnaire was launched by randomly selected respondents in China to understand the attitude of respondents in dealing with earthquake risk and toward earthquake insurance. Six hundred and thirty-seven questionnaires were collected after 2 weeks. Invalid data was rejected (questionnaires which are invalid because of the screening questions), and 428 valid questionnaires were analyzed for the measure of association.

The results in Table 7.1 indicate that there is no association between consumers’ WTP and consumers’ pre-experience of buying any insurance; however, consumers’ perceived risks are associated with their WTP. But consumers’ decision on whether to buy earthquake insurance is statistically associated with both pre-insurance-buying experience and perceived risks. Thus, if consumers perceived the existence of earthquake risk, they are willing to buy and pay earthquake insurance. All demographic variables have been tested to see whether there exists measure of association between consumers’ decision to buy insurance and WTP. The results indicate that all demographics are not statistically significant for a very small probability event, like earthquake.

However, the results in Tables 7.2 and 7.3 show that there exiting measure of association between consumers’ decision on buying earthquake insurance, and consumer’s social trust in all four different aspects, including the level of trust in government’s information about earthquake risk, the level of the satisfaction with government’s earthquake prevention constructions, the level of trust in social media’s information about earthquake risk, and the level of agreement with government’s implementation of the earthquake insurance program. The same significant measure of association goes to WTP and consumer's social trust. Therefore, to encourage consumers to buy earthquake insurance and increase their williness to pay (WTP) for earthquake insurance, the government should try to publish updated earthquake information through trustful social medias, to update infra structures which are more earthquake prevented, and to design more easy to land earthquake insurance policies.

5 Illustrative Examples, Cases, and Mapping

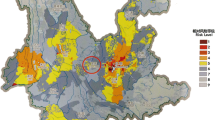

The Southeast China Coastal fold belt seismic zone poses great seismic hazards to the Hong Kong-Shenzhen-Guangzhou metropolitan area, the so-called “Pearl River Delta” region. These coastal regions are the economic backbone of China and Southeastern Asia. Although the seismicity is low, the study of earthquake and its prevention and control is very important in this area because of its highest population density, economic development, and contribution in the overall GDP of China. A moderate earthquake may cause high casualties and economic losses in this region as compared to other less developed and low-population Western parts of China (Lanbo 2001).

The Pearl River Delta is a densely populated metropolitan area that is home to more than 42 million inhabitants. Covering a territory of some 20,600 km2, it comprises the urban districts of Hong Kong, Shenzhen, Dongguan, Macau, and Guangzhou. Situated in one of the world’s most disaster-prone regions, floods and typhoons put more people at risk than in any other metropolitan areas in the world. This region is one of China’s main economic centers. However this region has been evaluated with low risk with earthquakes (Swiss Re 2014) (Fig. 7.2).

Population density and earthquake risk of Pearl River Delta, China (Source: Eastview LandScan2011TM and GSHAP)

Thus, does it mean that there is no need for this region to have earthquake insurance? On August 26, 2014, the 6.0 magnitude earthquake that struck the San Francisco Bay area early Sunday is estimated to have caused $1 billion in economic losses, according to the US Geological Survey. Only about 12 % of California homeowners have earthquake insurance coverage (Lu 2014). In areas hardest hit by this Sunday’s quake, such as Napa, fewer than 6 % of homeowners have earthquake coverage, according to the most recent data from the California Earthquake Authority.

Therefore, for a region with higher population intensity and lower risk for earthquakes, it’s very important to have more consumers to buy earthquake insurance. Because if an earthquake happens, it can cause severe loss in billions and requires huge amount of money for afterward recovering. Earthquake insurance can help to provide some earthquake funds in case of emergency.

6 Concluding Remarks

Earthquake is active in China these days. It is urgent to build an effective insurance system for all regions inside China. From the analysis of both consumers’ perspective and current conditions, it shows that is necessary to build an efficient earthquake insurance system in China. For the region with higher risk of earthquakes in China, the only thing that government needs to do is to support insurance companies to have earthquake insurance products, and then consumers will buy.

However, for the region with lower risk of earthquakes in China, the government has to put more effort on increasing social trust for consumers, such as more accurate information about earthquake prediction and more information on social networks about the earthquakes, especially to have some program to encourage consumers to buy earthquake insurance. In addition, insurance companies need to provide earthquake property insurance product and earthquake life insurance product separately and together too according to consumers’ different preferences. Therefore, further study about consumers’ willingness to pay for earthquake insurance product under uncertainty should be investigated.

References

Adger WN (2003) Social capital, collective action, and adaptation to climate change. Econ Geogr 79(4):387–404

Browne MJ, Hoyt RE (2000) The demand for flood insurance: empirical evidence. J Risk Uncertain 20(3):291–306

Jametti M, von Ungern-Sternberg T (2010) Risk selection in natural-disaster insurance. J Inst Theor Econ 166(2):344–364

Lu J (2014). Washingtonpost. http://www.washingtonpost.com/news/business/wp/2014/08/26/fewer-americanhomeowners-are-buying-earthquake-insurance-and-the-risk-is-growing/. Retrieved 09 Oct 2014

Johnson EJ, Hershey J, Meszaros J, Kunreuther HC (1993) Framing, probability distortions, and insurance decisions. J Risk Uncertain 7:35–51

Kahneman D, Tversky A (1979) Prospect theory: an analysis of decision under risk. Econometrica: J Econom Soc 47(2):263–291

Kunreuther HC (1978) Disaster insurance protection: public policy lessons. Wiley, New York

Kunreuther H, Michel-Kerjan E (2009) At war with the weather: managing large-scale risks in a new era of catastrophes. MIT Press, Cambridge, MA

Kuran T (1995) Private truths, public lies: the social consequences of preference falsification. Harvard University Press, Cambridge, MA

Lanbo L (2001) Stable continental region earthquakes in South China. Pure Appl Geophys 158(2001):1583–1611

Lichtenstein S, Slovic P, Fischhoff B, Layman M, Combs B (1978) Judged frequency of lethal events. J Exp Psychol Hum Learn Mem 4(6):551–578

Nelson DR, Adger WN, Brown K (2007) Adaptation to environmental change: contributions of a framework. Annu Rev Environ Resour 32(1):395–419

Norgaard KM (2011) Living in Denial: climate change, emotions, and everyday life. MIT Press, Cambridge, MA

Ostrom E (2000) Collective action and the evolution of social norms. J Econ Perspect 14(1):137–158

Pelling M, High C (2005) Understanding adaptation: what can social capital offer assessments of adaptive capacity? Glob Environ Chang 15(4):308–319

Schoemaker PJ, Kunreuther H (1979) An experimental study of insurance decisions. J Risk Insur 46(4):603–618

Schwartz A, Hasnain M (2002) Risk perception and risk attitude in informed consent. Risk Decis Policy 7(2):121–130

Showers VE, Shotick JA (1994) The effects of household characteristics on demand for insurance: a Tobit analysis. J Risk Insur 61(3):492–502

Slovic P, Fischhoff B, Lichtenstein S, Corrigan B, Combs B (1977) Preference for insuring against probable small losses: insurance implications. J Risk Insur 44(2):237–258

Smith VL (1968) Optimal insurance coverage. J Polit Econ 76(1):68–77

Swim J, Clayton S, Doherty T, Gifford R, Howard G, Reser J, Stern P, Weber E (2009) Psychology and global climate change: addressing a multifaceted phenomenon and set of challenges. American Psychological Association, Washington, DC

Swiss Re (2014) Mind the risk: a global ranking of cities under threat from natural disasters. www.swissre.com by Swiss Reinsurance Company Ltd

Wang M, Liao C, Yang S, Zhao W, Liu M, Shi P (2012) Are people willing to buy natural disaster insurance in China? Risk awareness, insurance acceptance, and willingness to pay. Risk Anal 32(10):1717–1740

Wolf J, Adger WN, Lorenzoni I, Abrahamson V, Raine R (2010) Social capital, individual responses to heat waves and climate change adaptation: an empirical study of two UK cities. Glob Environ Chang 20(1):44–52

Wong KK, Zhao X (2001) Living with floods: victims’ perceptions in Beijing, Guangdong, China. Area 33(2):190–201

Ye T, Wang M (2013) Exploring risk attitude by a comparative experimental approach and its implication to disaster insurance practice in China. J Risk Res 16(7):861–878

Zeckhauser R (1996) The economics of catastrophes. J Risk Uncertain 12(2–3):113–140

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2016 Springer Science+Business Media Singapore

About this chapter

Cite this chapter

Ge, J., Zhao, J., Nisar, S. (2016). New Consumers’ Perspective in Insuring Earthquakes. In: Foo, C. (eds) Diversity of Managerial Perspectives from Inside China. Managing the Asian Century. Springer, Singapore. https://doi.org/10.1007/978-981-287-555-6_7

Download citation

DOI: https://doi.org/10.1007/978-981-287-555-6_7

Publisher Name: Springer, Singapore

Print ISBN: 978-981-287-554-9

Online ISBN: 978-981-287-555-6

eBook Packages: Economics and FinanceEconomics and Finance (R0)