Abstract

Many dynamic networks can be analyzed through the framework of equilibrium problems. While traditionally, the study of equilibrium problems is solely concerned with obtaining or approximating equilibrium solutions, the study of equilibrium problems not in equilibrium provides valuable information into dynamic network behavior. One approach to study such non-equilibrium solutions stems from a connection between equilibrium problems and a class of parametrized projected differential equations. However, there is a drawback of this approach: the requirement of observing distributions of demands and costs. To address this problem we develop a hybrid system framework to model non-equilibrium solutions of dynamic networks, which only requires point observations. We demonstrate stability properties of the hybrid system framework and illustrate the novelty of our approach with a dynamic traffic network example.

Access provided by CONRICYT-eBooks. Download chapter PDF

Similar content being viewed by others

Keywords

Introduction

Equilibrium problems are vastly applicable to many networks and their formulation has become fairly complex. To date, most studies of networks formulated as equilibrium problems are concerned with equilibrium solutions, where equilibrium is defined depending on the context of the problem (Wardrop [12–14], Nash/Cournot [10, 11, 16], market [3, 20], and physical/mathematical equilibrium [18, 19]). However, the study of equilibrium problems not in equilibrium provides information absent from the analysis of equilibrium solutions. For instance, in a classic dynamic traffic network equilibrium problem, non-equilibrium solutions describe the adjustment of flows on a network in response to disturbances (like lane closures, accidents, or road construction) in link costs or demand.

One approach to study non-equilibrium solutions is through a class of parametrized projected differential equations, called double layered dynamics (DLD), [5, 10, 11] which tracks the adjustment of demands over time. To do this, DLD requires observing distributions of network information at all times, which in reality may be difficult or impossible to obtain. To overcome this obstacle, we develop a hybrid system framework to model non-equilibrium solutions. Through the hybrid system framework we extend the association between dynamic networks and projected differential equations, through their common connection with variational inequalities (VI). The result is a hybrid system version of non-equilibrium solutions of dynamic networks, which advantageously require only an observed point of network information.

Preliminaries

To begin, we present the foundations for modeling non-equilibrium solutions. We define the frameworks of equilibrium problems for static networks, as described by VI and projected differential equations (PrDE). Next, we provide analogous definitions for the frameworks of equilibrium problems for dynamic networks, as defined by evolutionary variational inequalities (EVI) and DLD.

Equilibrium Problems: Variational Inequalities and Projected Differential Equations

Since their introduction in the 60s [18, 19], VI problems have been extensively used in the study of Wardrop, Nash, Walras, Cournot and mathematical physics equilibrium problems [2, 9, 12, 13]. As such, we consider a VI on a Euclidean space of arbitrary dimension X, with a non-empty, closed, and convex set K ⊂ X, and a mapping F: K → X is given by:

Definition 1

Variational inequality problem [22].

The set of points x ∗ ∈ K satisfying the inequality above is called the solution set of the VI, which we denote by SOLVI(F, K).

There is an important connection between VI and PrDE [1, 7, 21], where a PrDE on a non-empty, closed, and convex set K ⊂ X, with a Lipschitz continuous mapping F: K → X is defined as:

Definition 2

Projected differential equation [7].

where the set \(T_{K}(x) = \overline{\bigcup _{\delta >0}\frac{1} {\delta } \left (K - x\right )}\) represents the tangent cone at the point x to K and the mapping \(P_{T_{K}(x)}(\cdot )\) is the closest element mapping from X to the set T K (x) ∈ X.

The important connection between a VI defined by Definition 1 and a PrDE defined by Definition 2 is the correspondence between solutions x ∗ ∈ SOLVI(F, K) and the critical points \(P_{T_{K}(x^{{\ast}})}(-F(x^{{\ast}})) = 0\). As such, when some mild conditions are satisfied [5, 9], it follows that

Dynamic Equilibrium Problems: Evolutionary Variational Inequality and Double Layered Dynamics Problems

Akin to the relationship between VI and PrDEs, there is a similar connection between an EVI [3, 14, 15] and DLD. In essence, an EVI represents a dynamic network, or an equilibrium problem that evolves with time, and can be viewed as an infinite dimensional VI. A similar view can also be taken with the connection between PrDE and DLD.

Formally, we take an EVI to be defined on a Hilbert space of arbitrary dimension \(X:= L^{2}([0,T], \mathbb{R}^{q})\) to be given by:

Definition 3

Evolutionary Variational Inequality [4, 6].

where \(\ll \phi,x \gg:=\int _{ 0}^{T}\langle \phi (x)(t),x(t)\rangle dt\) is the Hilbert space inner-product, with ϕ and x ∈ X and \(F: \mathbb{K} \rightarrow X\) is a Lipschitz continuous mapping. The set of points \(x^{{\ast}}\in \mathbb{K}\) that satisfy the EVI is called the solution set of the inequality, which we denote as \(SOLEV I(F, \mathbb{K})\).

For simplicity, the constraint (feasible) set \(\mathbb{K} \subset X\) of an EVI is taken to be

where \(\lambda,\mu \in L^{2}([0,T], \mathbb{R}^{q})\), \(A \in L^{2}([0,T], \mathbb{R}^{l\times q})\) and \(\rho \in L^{2}([0,T], \mathbb{R}^{l})\). Such a set is typically assumed to be closed, convex, and bounded in \(L^{2}([0,T], \mathbb{R}^{q})\), and therefore appropriate convexity conditions on the functions λ, μ, and ρ are required.

Definition 4

Double layered dynamic [5, 9]. Let \(F: \mathbb{K} \rightarrow X\) be a Lipschitz continuous mapping, where \(\mathbb{K}\) is given by (3). Then a double layered dynamic is given by:

where \(x \in AC([0,\infty ), \mathbb{K})\).

Similar to a VI and PrDE, there is a connection between the solution set of an EVI defined by Definition 3 and the critical points of a DLD defined by Definition 4. That is [8, 9],

Hybrid Systems

A hybrid system is a dynamical system composed of continuous and discrete dynamics [23]. Often, hybrid systems combine multiple systems of differential equations (the continuous dynamic) through a series of jump rules (the discrete dynamic), which take place at time instances called event-times [23]. To construct the trajectory of a hybrid system from the continuous and discrete dynamics, one starts from an initial point and continuously evolves in accordance with a system of differential equations until an event-time occurs. At the first event-time the continuous evolution of the hybrid system temporarily pauses, and the model states and parameters are updated according to the specified jump rule. After updating the model states and parameters, the hybrid system starts to continuously evolve again according to the (potentially new) system of differential equations, and proceeds until the next event-time occurs. This process repeats itself until a desired time is reached.

Any differential equation can be used to describe the continuous dynamic of a hybrid system. For a hybrid system composed of states, (x 1, x 2, …, x n ): = x, parameters (θ 1, θ 2, …, θ m ): = θ, and a function \(F: \mathbb{R} \times \mathbb{R}^{n} \rightarrow \mathbb{R}^{n}\), the continuous dynamic can be stated as:

Definition 5

The continuous dynamic.

The discrete dynamic of a hybrid system is a jump rule [23] that updates the model’s states, and parameter values and functional structure upon the occurrence of an event-time. Consequently, at event-times t j , in accordance with the jump rules \(G_{j}: \mathbb{R} \times \mathbb{R}^{n} \times \mathbb{R}^{m} \rightarrow \mathbb{R}^{n}\) (for the model’s states), and \(H_{j}: \mathbb{R} \times \mathbb{R}^{n} \times \mathbb{R}^{m} \rightarrow \mathbb{R}^{m}\) (for the model’s parameter values), we determine new states and parameter values of the model. Thus the discrete dynamic can be stated as:

Definition 6

The discrete dynamic.

and

Note the − and + superscripts are used to distinguish between model states at pre and post event-times.

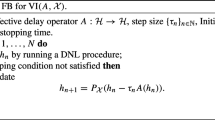

Given the continuous dynamic (5) and discrete dynamic (6)–(7) we now construct the hybrid system. To construct the hybrid system, as with a standard system of differential equations, we require an initial (observed) point of information x(0) as well as initial parameter values θ 1 and a time interval [0, T]. From the initial conditions, parameter values, and corresponding continuous dynamic, we proceed to compute the evolution of model states through

up until the first event-time t 1. At the first event-time we stop the continuous evolution of the model. The model, in accordance with the jump rule (6)–(7) undergoes a change in state and an update of parameters:

and

With the state, parameter values, and functional structure updated, the evolution of the continuous dynamic starts again. The continuous dynamic

is followed until the next event-time t 2, where we then once again undergo an update in model states G 2, parameters H 2, and functional structure F 3. This procedure is repeated until the end of the time interval [0, T] is reached. Formally, we have that a hybrid system is given by the following:

Definition 7

Hybrid systems. For a given uniform partition of [0, T] into segments [t j , t j+1], we have that for t ∈ [t j +, t j+1 −) we evolve according too

and when t = t j −,

and

where, once again the − and + superscripts are used to distinguish between model states at pre and post event-times.

Non-equilibrium Solutions of Dynamic Networks

The difference in approach between DLD and hybrid system non-equilibrium solutions of dynamic networks is evident under the context of a dynamic traffic network problem:

-

1.

A DLD non-equilibrium solution can be seen as an external view of the entire traffic network, where observed information on the evolution of the entire traffic flow across all links can be provided.

-

2.

A hybrid system non-equilibrium solution can be seen as an internal view of the traffic network, with knowledge of the network structure (links, nodes and equilibrium), but only current information about immediately viewable traffic (point observations) can be provided.

Definition 8

DLD non-equilibrium solutions. From the association between \(SOLEV I(F, \mathbb{K})\) and the critical points of a DLD, a DLD non-equilibrium solution is given by

where the mapping F and constraint set \(\mathbb{K}\) are taken as in Definition 3 and Eq. (3), respectively, and x(⋅ , τ) ≠ x ∗.

Definition 9

Hybrid system non-equilibrium solutions. To construct a non-equilibrium solution from a hybrid system, we define the continuous and discrete dynamic related to the dynamic equilibrium problem. We consider a hybrid system non-equilibrium solution to be composed of a series of jump rules that connect a series of projected differential equation. Each projected differential equation is defined on the set K j , where

Thus, the continuous dynamic for t ∈ [t j−1, t j −) of the hybrid system is

and the discrete dynamic is

To analyze the stability properties of hybrid system non-equilibrium solutions we define the following:

Definition 10

Hybrid system trajectory. For a uniform division Δ of [0, T], a hybrid system trajectory \(HS_{\delta }: [0,T] \rightarrow \mathbb{R}\) is defined as:

where \(N = \frac{T} {\delta }\).

Definition 11

The sequence of hybrid system trajectories. For all t ∈ [0, T] we denote \(\{HS_{\delta _{m}}\}_{m}\) as the sequence of hybrid trajectories with uniform division Δ m that consist of m divisions of length \(\frac{T} {\delta _{m}}\).

Definition 12

The feasible sets of hybrid system trajectories. For all t ∈ [0, T] and uniform divisions Δ, we denote the feasible set of hybrid trajectories as:

where \(N = \frac{T} {\delta }\).

From these definitions, for almost all t ∈ [0, T], it follows that

where

While there are many possible jump rules, imposing some physical properties on the jump rule will ensure that the discrete dynamic does not destabilize the system. As such, we consider jump rules that satisfy the following properties:

-

1.

Jump rules G j map equilibrium points to equilibrium points,

$$\displaystyle{ G_{j}(t_{j}^{-},x^{{\ast}}(t_{ j})) = x^{{\ast}}(t_{ j+1}), }$$(13)and

-

2.

jump rules do not increase the distance from equilibrium points,

$$\displaystyle{ \|x(t_{j}^{-}) - x^{{\ast}}(t_{ j})\| \geq \| G_{j}(t_{j}^{-},x(t_{ j}^{-})) - G_{ j}(t_{j}^{-},x^{{\ast}}(t_{ j}))\| =\| x(t_{j}^{+}) - x^{{\ast}}(t_{ j+1})\|. }$$(14)

From the definition of the feasible set of a hybrid trajectory, it follows that on any sub-interval [t j +, t j+1 −) that the critical point of the continuous dynamic x ∗ ∈ SOLVI(F, K j ). Thus, with the conditions (13)–(14), we can approximate the equilibrium curve with

Given the definitions on hybrid system non-equilibrium solutions, we can now state the following stability result:

Theorem 1

Stability of the hybrid systems non-equilibrium solution. If the mapping F from a hybrid system non-equilibrium solution is strongly pseudomonotone of degree α < 2 with constant η (Appendix 1), and the jump rules are given by

then δ can be selected so that for some time t ∗ ∈ [0,T],

Furthermore, δ can be selected so that the hybrid system trajectory will converge to a curve arbitrarily close to the equilibrium curve after time t ∗ , where

For the proof see Appendix 3.

A Dynamic Traffic Network Example

To illustrate the DLD and hybrid system non-equilibrium solutions we consider a dynamic traffic network consisting of a single O/D pair of nodes with two direct links. The feasible set of the dynamic traffic network is taken to be

and the travel demand function,

The user cost function on the links is taken as

where the equilibrium flows are given by

and

DLD Non-equilibrium Solution

With initial distributions of travel demand across the links given by

user cost function F and constraint set \(\mathbb{K}\), the DLD non-equilibrium solutions gradually converge to the equilibrium (Fig. 1). Importantly, the convergence to the equilibrium is a result of the mapping F being strongly pseudomonotone of degree \(\alpha = \frac{3} {2}\) with constant η = 21∕4 (Appendix 2). This property of F ensures the stability of the dynamic traffic network, as it implies that any disturbance eventually dampens out by time [10],

Non-equilibrium solutions adjusting back to the traffic network equilibrium in a finite duration of time. For the demand on each link, the DLD non-equilibrium solutions consist of the red, green, blue, yellow and violet curves, the hybrid system non-equilibrium solution are the black dotted curves, and equilibrium solutions are the grey curves

HS Non-equilibrium Solution

For hybrid system non-equilibrium solutions we consider the initial conditions \(x_{1}(0) = \frac{4} {5}\rho (0) = 48.8,x_{2}(0) = \frac{1} {5}\rho (0) = 12.2\), together with a uniform partition of the interval [0, T] into segments [t j , t j+1) such that | t j+1 − t j | = δ. In addition, we require the definition of jump rules G j , which are taken as

where the constraint sets K j are defined by (12).

From this construction, an interpretation of hybrid system non-equilibrium solution is that of a non-equilibrium solution that crosses (or travels along) the DLD non-equilibrium solutions (Fig. 1). With this in mind, it is possible to show that both frameworks share desirable properties.

As such, the hybrid system non-equilibrium solution can converge to x δ ∗ by t ∗ ≈ 13. 9 due to the strongly pseudomonotone of degree \(\frac{3} {2}\) of F (Theorem 1). Consequently, it follows that one can select δ sufficiently small so that the hybrid system non-equilibrium solution converges arbitrarily close to the equilibrium of the dynamic traffic network on [t ∗, T] (Figs. 2 and 3). In other words, hybrid system non-equilibrium solutions, like their DLD non-equilibrium solution counterparts, will eventually dampen out any disturbance.

HS non-equilibrium solutions with 10 jumps (red), 20 jumps (blue), 40 jumps (green), 80 jumps (yellow), 160 jumps (violet), and 320 jumps (grey) for link 1 (left) and link 2 (right)

Euclidean distance of HS non-equilibrium solution from the equilibrium solution with 10 jumps (red), 20 jumps (blue), 40 jumps (green), 80 jumps (yellow), 160 jumps (violet), and 320 jumps (grey)

Discussion

We developed a hybrid system framework for modeling non-equilibrium solutions of dynamic networks. Our framework provides an alternative approach to model the adjustment of dynamic networks in response to disturbances. The primary advantage of hybrid system non-equilibrium solutions, in comparison to DLD non-equilibrium solutions, is the reduction of the requirement to track distributions of information across the entire network to that of point observations.

We illustrated the validity of our approach by comparing it to DLD non-equilibrium solutions of a dynamic traffic network. In particular, we show that if the cost function F is strongly pseudomonotone of degree α < 2, then there are similar stability behaviors in both the hybrid system framework and the DLD framework. More specifically, if F is strongly pseudomonotone of degree α < 2, then disturbances completely dampen out in a finite amount of time for both frameworks.

While there are numerous benefits to using hybrid system non-equilibrium solutions, there is a cost in reducing the requirement of tracking entire distributions of information. Namely, a pre-defined jump rule is required. Fortunately, such a rule could be based on previously known information as supposed to the current information requirement of DLD non-equilibrium solutions.

A particularly interesting avenue for future investigation is combining DLD and HS frameworks to model non-equilibrium solutions of dynamic networks that have partial point information and partial distribution information. Such a merger of frameworks would provide an interesting way to maximize the use of all possible information in modeling non-equilibrium solutions of dynamic networks. In addition, incorporating network delays, or stochastic disturbances would also further strengthen the applicability of the HS framework to model non-equilibrium solutions of dynamic networks.

Overall, the hybrid system non-equilibrium solutions are directly applicable to many dynamic networks, including traffic networks, oligopolistic market problems and noncooperative Nash games. Advantageously, the hybrid system framework can be applied to any dynamic network modeled by DLD non-equilibrium solutions, starting from any point on a DLD non-equilibrium solution.

References

J.P. Aubin, A. Cellina, Differential Inclusions: Set-Valued Maps and Viability Theory, Springer (1984)

J.P. Aubin, A. Cellina, Differential inclusions. J. Appl. Math. Mech. 67 (2), 100 (1987)

A. Barbagallo, M.G. Cojocaru, Dynamic equilibrium formulation of the oligopolistic market problem. Math. Comput. Model. 49, 966–976 (2009)

B. Brogliato, A. Daniilidis, C. Lemaréchal, V. Acary, On the equivalence between complementarity systems, projected systems and differential inclusions. Syst. Control Lett. 55, 45–51 (2006)

M.-G. Cojocaru, Double-Layer Dynamics Theory and Human Migration After Catastrophic Events (Bergamo University Press, Bergamo, 2007)

M.G. Cojocaru, Piecewise solutions of evolutionary variational inequalities. Consequences for the doublelayer dynamics modelling of equilibrium problems. J. Inequal. Pure Appl. Math. 8 (2), 17 (2007)

M.-G. Cojocaru, L.B. Jonker, Existence of solutions to projected differential equations in Hilbert spaces. Proc. Am. Math. Soc. 132, 183–193 (2004)

M.G. Cojocaru, P. Daniele, A. Nagurney, Projected dynamical systems and evolutionary variational inequalities via Hilbert spaces with applications. J. Optim. Theory Appl. 127, 549–563 (2005)

M.G. Cojocaru, P. Daniele, A. Nagurney, Double-layered dynamics: a unified theory of projected dynamical systems and evolutionary variational inequalities. Eur. J. Oper. Res. 175, 494–507 (2006)

M.G. Cojocaru, C.T. Bauch, M.D. Johnston, Dynamics of vaccination strategies via projected dynamical systems. Bull. Math. Biol. 69, 1453–1476 (2007)

M. Cojocaru, P. Daniele, A. Nagurney, Projected dynamical systems, evolutionary variational inequalities, applications, and a computational procedure, in Pareto Optimality, Game Theory …, Springer (2008), pp. 387–406

S. Dafermos, Traffic equilibrium and variational inequalities. Transp. Sci. 14 (1), 42–54 (1980).

S. Dafermos, Congested transportation networks and variational inequalities, in Flow Control of Cogested Networks (Springer, Berlin, 1987)

P. Daniele, Dynamic Networks and Evolutionary Variational Inequalities (Edward Elgar, Cheltenham, Northampton, MA, 2006)

P. Daniele, A. Maugeri, W. Oettli, Time-dependent traffic equilibria. J. Optim. Theory Appl. 103 (3), 543–555 (1999)

P.T. Harker, A variational inequality approach for the determination of oligopolistic market equilibrium. Math. Program. 30, 105–111 (1984)

S. Karamardian, S. Schaible, Seven kinds of monotone maps. J. Optim. Theory Appl. 66, 37–46 (1990)

D. Kinderlehrer, G. Stampacchia, An Introduction to Variational Inequalities (SIAM, Philadelphia, 2000)

J. Lions, G. Stampacchia, Variational inequalities. Commun. Pure Appl. Math. 20 (3), 493–519 (1967)

A. Nagurney, Network Economics: A Variational Inequality Approach (Springer, Berlin, 1993)

A. Nagurney, D. Zhang, Projected Dynamical Systems and Variational Inequalities with Applications (Kluwer Academic, Dordrecht, 1996)

G. Stampacchia, Variational inequalities, in Theory and Applications of Monotone Operators Proceedings of a Nato Advance Study Inst. Vienice, Italy (1969), pp. 101–192

A. van der Schaft, H. Schumacher, An Introduction to Hybrid Dynamical Systems (Springer, Berlin, 2000)

Acknowledgements

Scott Greenhalgh and Monica-Gabriela Cojocaru would like to thank the referees comments which led to a clearer presentation of this work. Monica-Gabriela Cojocaru graciously acknowledges the support received from the Natural Sciences and Engineering Research Council (NSERC) of Canada.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Appendices

Appendix 1: Common Definitions and Theorems for VI, EVI, and PrDE

Definition 13

Some classifications of the mapping F [17]. Given that X is a Hilbert space of arbitrary dimension, \(\mathbb{K} \subset X\) is a non-empty, closed, and convex set, then a mapping \(F: \mathbb{K} \rightarrow X\) is said to be

-

1.

Pseudomonotone on \(\mathbb{K}\) if

$$\displaystyle{\begin{array}{ll} \langle F(x),y - x\rangle \geq 0 \Rightarrow \langle F(y),y - x\rangle \geq 0&\forall x,y \in \mathbb{K}\end{array} }$$ -

2.

Strictly pseudomonotone on \(\mathbb{K}\) if

$$\displaystyle{\begin{array}{ll} \langle F(x),y - x\rangle \geq 0 \Rightarrow \langle F(y),y - x\rangle > 0&\forall x\neq y \in \mathbb{K}\end{array} }$$ -

3.

Strongly pseudomonotone of degree α on \(\mathbb{K}\) if for some η > 0,

$$\displaystyle{\begin{array}{ll} \langle F(x),y - x\rangle \geq 0 \Rightarrow \langle F(y),y - x\rangle \geq \eta \| x - y\|^{\alpha }&\forall x,y \in \mathbb{K}\end{array} }$$

Definition 14

Monotone attractor. Let X be a Hilbert space of arbitrary dimension, \(\mathbb{K} \subset X\) be a non-empty, closed, and convex set, and \(F: \mathbb{K} \rightarrow X\) a Lipschitz continuous mapping. Then

-

1.

A point \(x^{{\ast}}\in \mathbb{K}\) is a local monotone attractor for a PrDE if there exists a neighborhood V of x ∗ such that the function ϕ(τ): = ∥ x(τ) − x ∗ ∥ X is non-increasing with respect to τ for any solution x(τ) of a PrDE starting in V.

-

2.

A point \(x^{{\ast}}\in \mathbb{K}\) is a global monotone attractor for a PrDE if condition X is satisfied for any \(x(\tau ) \in \mathbb{K}\).

Definition 15

Stability of equilibria. Let X be a Hilbert space of arbitrary dimension, \(\mathbb{K} \subset X\) be a non-empty, closed, and convex set, and \(F: \mathbb{K} \rightarrow X\) a Lipschitz continuous mapping. If \(x^{{\ast}}\subset \mathbb{K}\) is an equilibrium of a PrDE, B(x, r) is a ball of radius r centered on \(x: \mathbb{R}^{+} \rightarrow \mathbb{K}\) (a non-equilibrium solution to a PrDE), then

-

1.

The point x ∗ is exponentially stable if there exists ε > 0 and μ > 0 such that \(\forall x \in B(x^{{\ast}},\epsilon )\) and \(\forall \tau \geq 0\), we have that ∥ x(τ) − x ∗ ∥ X ≤ ∥ x(0) − x ∗ ∥ X exp(−μ τ).

-

2.

The point x ∗ is a finite-time attractor if there exists ε > 0 such that \(\forall x \in B(x^{{\ast}},\epsilon )\) and \(\forall \tau \geq 0\), there exists T: = T(x) < ∞, where x(τ) = x ∗ for all τ ≥ T.

-

3.

The point x ∗ is globally exponentially stable, or a global finite-time attractor if X, or respectively Y hold for any \(x \in \mathbb{K}\).

Theorem 2

Let \(\mathbb{K} \subset X\) be a non-empty, closed, and convex set, \(F: \mathbb{K} \rightarrow X\) a Lipschitz continuous mapping, and x ∗ an equilibrium of a PrDE.

-

1.

If F is locally (strictly) pseudomonotone around x ∗ , then x ∗ is a local (strictly) monotone attractor.

-

2.

If F is (strictly) pseudomonotone on \(\mathbb{K}\) , then x ∗ is a global (strictly) monotone attractor.

Theorem 3

Let \(\mathbb{K} \subset X\) be a non-empty, closed, and convex set, \(F: \mathbb{K} \rightarrow X\) a Lipschitz continuous mapping, and x ∗ an equilibrium of a PrDE.

-

1.

If F is strongly pseudomonotone around x ∗ , then x ∗ is a locally exponentially stable.

-

2.

If F is strongly pseudomonotone with degree α < 2 around x ∗ , then x ∗ is a local finite-time attractor.

-

3.

If F is strongly pseudomonotone on \(\mathbb{K}\) , then x ∗ is a globally exponentially stable.

-

4.

If F is strongly pseudomonotone with degree α < 2 on \(\mathbb{K}\) ,around x ∗ , then x ∗ is a global finite-time attractor.

Appendix 2: Strongly Pseudomonotone of Degree α < 2

Here we show that the mapping F from the example in section “A Dynamic Traffic Network Example” is strongly pseudomonotone of degree \(\frac{3} {2}\).

Proof

To begin, recall that

with the constraint set,

To show F is strongly pseudomonotone of degree \(\frac{3} {2}\), we use the following identity:

It follows that

Equivalently, replacing x 2 − y 2 through the identity above, we have that

and

Because the square root function is subadditive, it follows that

Finally, the proof is complete upon noting that

Thus, we have that F is strongly pseudomonotone of degree \(\alpha = \frac{3} {2}\) with \(\eta = \sqrt{2}^{2-\alpha }\).

Appendix 3: Stability of a Hybrid System Non-equilibrium Solution

To demonstrate the stability properties of a hybrid system non-equilibrium solution, consider a mapping F that is strongly pseudomonotone of degree α < 2 with constant η, and the jump rules:

and

It follows that δ can be selected sufficiently small so that for some t ∗ ∈ [0, T],

Proof

The proof here follows the same approach for showing finite time attraction to an equilibrium of a projected differential equation [9, 21]. To begin, let Δ: = Δ m be a uniform division of [0, T] for some fixed m, with division points t j , so that | t j+1 − t j | = δ. Taking t > t j we have that

From the jump rule defined by (15), we have that

Since 2 −α > 0 and the power function is increasing we get

Continuing in this fashion, we finally arrive at

Thus t ∗ is taken such that:

Thus on the subinterval [t k , t k+1] that contains t ∗, we have necessarily that

Furthermore, since the jump rule maps x ∗(t j ) → x ∗(t j+1) for all j,

for all t ≥ t ∗ on each interval \([t_{i},t_{i+1}]\;\;\forall i > k\). Thus by Lebesgue’s dominated convergence theorem, we have that δ can be selected so that

for any ε > 0.

Rights and permissions

Copyright information

© 2017 Springer International Publishing AG

About this chapter

Cite this chapter

Greenhalgh, S., Cojocaru, MG. (2017). Non-equilibrium Solutions of Dynamic Networks: A Hybrid System Approach. In: Daras, N., Rassias, T. (eds) Operations Research, Engineering, and Cyber Security. Springer Optimization and Its Applications, vol 113. Springer, Cham. https://doi.org/10.1007/978-3-319-51500-7_13

Download citation

DOI: https://doi.org/10.1007/978-3-319-51500-7_13

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-51498-7

Online ISBN: 978-3-319-51500-7

eBook Packages: Mathematics and StatisticsMathematics and Statistics (R0)