Abstract

This study assesses the impact of proximity to the Honolulu Rail Transit (HRT) on the single-family and condo values on Oahu, Hawaii. The data includes more than 32,000 single family homes and 47,000 condos between 2006 and 2015. In this paper, when semiparametric model using too large bandwidth, the results are not as rigorous as the fixed effects model with 130 controlled groups. The results indicate that after the ground-breaking event for HRT, the island-wide single family housing prices increase by 4%, but the condo values decrease by 4%; there are very slight positive distance spillover effects for single family housing market: houses located one mile closer to the HRT areas, the housing prices increase by 0.6%, however, this slight positive impact is at the costs of local housing values: for homes located within a 0.5 mile radius of the future HRT line, their values drop by 7.1%, for homes located between a 0.5 and 1 mile radius of the future HRT line, their values drop by 4.1%, and for homes located between a 1 and 2 mile radius of the future HRT line, their values drop by 2.1%. These negative local effects disappear after the 2 mile radius distance.

Access provided by CONRICYT-eBooks. Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

Oahu’s notorious traffic congestion, limited land mass, growing population and attempts to diversify the economy require innovative public transit solution to promote the state of Hawaii’s plans for sustainable growth. The America’s first fully driverless rail transit project is currently under construction in Oahu, Hawaii: Honolulu Rail Transit (HRT) project, also known as the Honolulu High-Capacity Transit Corridor Project. By 2030, nearly 70% of Oahu’s population and more than 80% of the island’s jobs will be located along the 20-mile rail corridor (HART 2015) with stops in downtown Honolulu, Waikiki beach, at three University of Hawaii system campuses, Aloha Stadium, the Honolulu International Airport and several shopping centers including Ala Moana. However, the project is controversial. Pro rail advocates argue that rail constitutes an essential component of Hawaii’s sustainable future initiatives and transit-oriented, high density, mixed use development plans since rail transit is expected to provide convenient access to the Central Business District (CBD), employment locations, commercial centers, schools, parks, and other recreational opportunities. Supporters note that rail will reduce traffic congestion along the 20-mile corridor; connect major residential areas with primary job centers; alleviate substantial traffic issues affecting the state’s most populous urban region; as well as provide a reliable transportation alternative for visitors and commuters in southern Oahu. For example, the rail could provide a convenient means to get to work, school or home as well as attend special events (including Aloha Stadium sporting events and concerts at the Blaisdell Center) without the hassles of parking and traffic. On the other hand, those against the HRT feel that an above-ground rail system is not cost-effective (the project already overbudget and behind schedule) and will exacerbate traffic congestion and pollution.

The controversy over the rail line was a key issue in local politics in the 2008 Honolulu elections and resulted in a city charter amendment which left the final decision to the citizens of Oahu. Construction on the HRT began on February 22, 2011 after the amendment passed with 53% of voters in favor. This paper examines whether homeowners are willing to pay a premium to be close to the future HRT line and whether or not the single family housing values and condo values change in proximity to the HRT. It is expected that any economic benefits which accrue from HRT should be capitalized into the price of nearby homes or condo values. Since the HRT is currently under construction—the initial section of the rail transit system, from Kapolei to Aloha Stadium, is slated to open in 2018; and the entire system, from Kapolei to Ala Moana Center, is set to be fully operational in 2019—the impact of the partially completed (and not yet operational) HRT on surrounding single-family housing prices and condo values are examined after the HRT ground breaking ceremony in 2011 and after the real start of the construction work in 2014.

While many studies have investigated the economic impacts of rail station proximity on property values, this is the first to examine the impact of rail in the U.S.-affiliated Pacific Island Jurisdictions (USAPI) and the Pacific island region. Data from 2006 to 2015 is used to analyze the impact of the HRT on single-family house prices and condo values in the Oahu housing market. Hedonic pricing models are often utilized to analyze differentiated goods such as houses and cars (Rosen 1974). The differentiated products include distinct characteristics, which add or subtract from the property’s overall total price according to how buyers in the market value that amenity or disamenity. This paper incorporates residential value hedonics to determine the value of both access to HRT stations under construction and other neighborhood locations, such as schools, parks, wetlands, hospitals, bus stops, ocean, farmers’ markets, supermarkets, surf sites, and fire stations. To address the missing variables bias, this paper uses the dereference-in-difference (DID) fixed effects model to compare with the semiparametric models. The 32,053 single-family housing data includes 130 well-defined neighborhoods, and the 47,581 condo data includes 132 well-defined neighborhoods. Thus, the fixed effects model can help control for unobserved heterogeneities when these heterogeneities are constant over time. These constants can be removed from the data through differencing processes. The results indicate that after the ground-breaking event (in February, 2011) for HRT, the island-wide single family housing prices increase by 4% overall, but the island-wide condo values decrease by 4% overall; there are very slight positive distance spillover effects for single family housing market: houses located one mile closer to the HRT areas after the ground-breaking event, the housing prices increase by 0.6%, however, this slight positive island-wide impact is at the costs of local housing values: for homes located within a 0.5 mile radius of the future HRT line, their values drop by 7.1%, for homes located between a 0.5 and 1 mile radius of the future HRT line, their values drop by 4.1%, and for homes located between a 1 and 2 mile radius of the future HRT line, their values drop by 2.1%. These negative local effects disappear after the 2 mile radius distance. The real construction event (in March, 2014) has no significant island-wide as well as the local impact on the single-family housing market. For the condo market, there is no significant distance spillover effect after the ground-breaking event. However, condos located between a 1 and 1.5 mile radius enjoy a 9.2% value appreciation and condos located between a 1.5 and 2 mile radius enjoy a 5.4% value appreciation. After the construction began, it has slight negative distance spillover effect: for condos located one mile closer to the future HRT line, their values drop by 0.6%.

The contribution of this study to the literature is studying the first driverless rail transit system in an island economy and using both semiparametric and fixed effects model to see its impact on property values in the angles of both the periods of breaking-ground event and the real construction start.

2 Literature Review

Studies examining the relationship between the presence of the rail and house transaction have shown three very different results which can be categorized as follows: no measurable effects of rail on property values (category 1); mixed impacts of rail on property values (category 2), and positive impacts of rail on property values (category 3). In the first category, Mohammad et al. (2013) find that rail investments over time impact neither the location nor the values of property within the city. Moreover, it is shown that including property characteristics and neighborhood types in the estimation model does not change property values significantly.

In the second category, Duncan (2011) uses a hedonic price model with interaction terms and finds that the premium value associated with rail proximity is conditional upon permissive zoning arrangements and ordinances, which has a negative influence on home prices except in the area immediately surrounding rail stations. Cervero (2004) uses a simple hedonic pricing model to show that the values of multiple land parcels in different rail corridors of San Diego County appreciate, while commercial properties in some other areas accrued small or even negative capitalization benefits. Chen et al. (1998) find that the impact of light rail will negatively or ambiguously impact property values due to nuisance effects such as noise and vibrations. Chatman et al. (2012) find that the net impact of the rail on the owner occupied housing market in Southern New Jersey is neutral to slightly negative, while lower-income census tracts and small houses appear to appreciate near the rail station. Hess and Almeida (2007) find that rail impacts on residential property values in Buffalo, New York are experienced unevenly across the rail system: the proximity effects are positive in high-income station areas but negative in low-income station areas.

For the third category, a Difference-In-Differences (DID) model shows that light rail transit in Charlotte, North Carolina provides a neighborhood impact of 4% for single-family properties and 11.3% for condominiums sold within 1 mile of the rail stations (Billings 2011). And that the opening of a new rail on the Montreal (Canada) South Shore generates a location premium for houses located in the stations’ vicinity as opposed to houses that do not experience any improvement in accessibility to the line (Dubé et al. 2013). Mathur and Ferrell (2013) find that the average home sale price increases by 3.2% ($21,000) for every 50% reduction in the distance between the home and the rail transit in San Jose, California. They also find that housing prices within 1/8 mile of the rail were 18.5% higher than the prices more than 1/8 mile from the line during the post-construction period, 7.3% higher during the construction period and not statistically different in the pre-construction period.

3 Study Areas

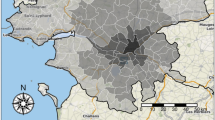

The study area is the island of Oahu in the US state of Hawaii. The study area, the HRT and the geocoded single family houses and condos are shown in Fig. 1, created by ArcMap.

Study area and Honolulu Rail Transit

This figure is created using ArcMap 10.3.1. It shows the study area of Oahu, HI. The circle dots are geocoded house addresses, the triangle dots are geocoded condo addresses, and the solid line is the Honolulu Transit Line.

Due to the highly congested transportation corridor situated between Kapolei and UH Manoa and Waikiki, a 20-mile elevated rail line featuring 21 stations is under construction to provide high-capacity rapid transit to connect West Oahu with the Honolulu International Airport continuing through downtown Honolulu with a final stop at Ala Moana Center. The Honolulu Authority for Rapid Transportation (HART) unveiled its first rail column in East Kapolei in June 2012 and HART revealed that the funding of HRT comes from both local funding (0.5% surcharge on the General Excise and Use Tax paid by residents, businesses, and visitors on Oahu) and federal funding ($1.55 billion from the Federal Transit Administration). The 21 stations will pass through a 20-mile rail corridor that includes Waipahu, Pearl City, Waimalu, Aiea, and Halawa. Even though the ground-breaking event began on February 22, 2011, the real construction work started 3 years later in February, 2014. This paper investigates a number of key questions: does the ground-breaking event affect the housing market on Oahu? Does the real start of construction work affect the housing market on Oahu? And if the HRT indeed impacts property values, will the impacts occur locally or across the entire island?

4 Data and Methodology

There are 22 variables associated with housing characteristics (4 dummy variables of house qualities; 9 dummy variables of house views, and 4 dummy variables of car spaces) and 11 distance variables associated with amenities/disamenities. These distance variables are created using the ‘near’ function of ArcMap. The first step to assess the impact of the HRT on property values is to build a GIS database from the data collected from the Department of Planning and Permitting. Using sales data from the HBR (Honolulu Board of Realtors), more than 30,000 single family housing addresses and 47,000 condo addresses are geocoded. The housing data includes the major physical characteristics of the houses such as the number of bedrooms, bathrooms, square footage, age, etc. ESRI GIS shapefiles (including hospital, preschool, farmers’ market, bus stop, park, ocean, fire station, supermarket, surf sites and wetland shapefiles) were downloaded from the State of Hawaii’s Office of Planning website. The HRT shapefile is downloaded from the online ArcGIS website.

Hedonic analysis has been applied to data on heterogeneous goods in an attempt to estimate shadow prices of bundled characteristics such as housing attributes and public good amenities acquired through the housing market (Ohsfeldt and Smith 1985). Traditional hedonic estimation has been frequently used for the purpose of making inferences about non-observable values of different attributes like air quality, airport noise, and access to transportation (Espey and Lopez 2000). There have been many critical views about traditional hedonic models such as information asymmetry, measurement validity of explanatory variables, market limitations, multicollinearity and price changes. It is thus better to explore additional research designs or to use the hedonic price technique with application to other models. The hedonic pricing model is constructed based on three types of different house attributes: physical attributes, community attributes and attributes observed by the consumers but not econometricians (Bajari and Kahn 2005). These unobserved variables usually have some structural constraints associated with them and one can use these constraints to infer their values from the data (Chopra et al. 2007).

Assuming P is a vector of house prices associated with a vector of structure variables S and set of location variables N then it follows that their relationship can be represented by the following model:

where ln(Pi) = natural logarithm of house sale price of property i; Sip = physical attribute p of property i; Niq = location variable q of property i; β0, βp, βq = intercept and coefficients; εi = error. If the neighborhood feature affects house sale prices positively, the first-order relationship of house price with respect to the location variable is:

Nonparametric models offer significant advantages for hedonic price function estimation due to their functional form flexibility and spatially varying coefficients, which help to reduce spatial autocorrelation without imposing arbitrary contiguity matrices or distributional assumptions on the data (McMillen and Redfern 2010). The locally weighted regression (LWR), or loess, is a procedure for fitting a regression surface to data through multivariate smoothing: the dependent variable is smoothed as a function of the independent variables in a moving fashion analogous to how a moving average is computed for a time series (Cleveland and Devlin 1988). Detailed application of loess to the house price functions is in McMillen and Redfern (2010): let the target for the nonparametric estimator be a home with structural and locational characteristics given by the vector X. The LWR estimator is derived by minimizing the following equation with respect to α andβ:

The kernel function K (z) determines the weight that each house sold as an observation in estimating the house price at target point X with X i − X defined as the distance between the target point and the i th neighboring house and h is a smoothing parameter called the bandwidth. As z increases, the weights decline. Though there are various types of kernel functions such as rectangular, triangular, bi-square, tri-cube or Gaussian, the choice of kernel weight function usually has little effect on the results. This study uses tri-cube kernel weighting function but h is more important since it determines how many observations receive positive weight when constructing the estimate and how rapidly the weights decline with distance. By replacing more weight on more distant observations, high values of h imply local regressions that produce more smoothing than do smaller bandwidths (McMillen and Redfern 2010). This helps the nonparametric part of the semiparametric model, which takes the form as:

where m() is the unknown smooth function with the location variables and it is estimated by a least square procedure. By including location variable whose structure is not known a priori, one may study the existence of nonlinearities.

5 Results and Discussion

The natural logarithms of single family house prices and condo prices are the dependent variables and a combination of structural and locational characteristics are the independent variables in our models. Table 1 records the parametric and semiparametric regression results for single family property values. The parametric model includes both the benchmark OLS model and DID fixed effects model. Due to the singular matrix problem when using small bandwidth for semiparametric model, this paper uses a 0.9 bandwidth for the last model. Larger bandwidth tends to over-smooth the data and produces the results that are close to the linear OLS models.

Even though the linear OLS model generates larger R-squared values, it is prone to the missing variable biases. The fixed effects model on the other hand, can get rid of the constant unobserved heterogeneities within the 130 groups in the single family housing data. For example, the linear OLS model indicates that houses located within a 1.5 and 2 mile radius of the future HRT line, the property values increase by 4.2%; this positive local impact might be affected by the missing variable such as the quality of the schools. The fixed effects model indicates that houses located within 1 1.5 and 2 mile radius of the future HRT line, the property values decrease by 2.1%. The semiparametric model generates very similar results as the OLS model due to its large bandwidth selection. So, this paper uses the results from the more rigorous fixed effects model.

The fixed effects model shows that after the ground-breaking event took place in 2011, the single family housing market values appreciate by 4% overall. Even though the year dummies are added in the regression taking account the annual trend, this island-wide positive impact is prone to the general positive housing market after the recent Great Recession. The HRT line produces slight positive distance spillover effect: houses located one mile closer to the line, their values appreciate by 0.6% after the ground-breaking event. However, this small positive overall effect is at the costs of local housing values: houses located with a 0.5 mile radius of the line, property values drop by 7.1%; houses located between a 0.5 and 1 mile radius of the line, property values drop by 4.1%; houses located between 1 and 2 mile radius of the line, property values drop by 2.1%; and this negative local effects disappear after the 2 mile radius distance. There is no significant effect after the construction started. In other words, the positive distance spillover effect disappeared during the construction period as well as the negative local effect. When the construction really started 3 years after the ground-breaking event overcoming many hurdles, it became a credible policy effect. People believe that the HRT line will eventually be finished and operating. This might explain the disappearing negative local effects. Figures 2 and 3 show the surface plots of the graphical relationship between the main distance variables ‘DID_HRT’ and ‘DID_HRT1’ and single family housing prices across the study periods.

Surface Plot of single house price and distance variable across the years after ground-breaking event

Surface Plot of single house price and distance variable across the years after construction started

For the condo market, Table 2 shows that the fixed effects model results reveal that after the construction started in 2014, the condo market values drop by 4% overall. This implies that even though the single-family housing market is getting better, the condo market is still at hot waters. Before the ground-breaking event, the planned HRT line already produces positive distance spillover effect: condos located one mile closer to the planned line, the property values increase by 7.1%, however, after the event, this significant positive effect becomes insignificant. And after the construction started, the line produces negative distance spillover effect: condos located one mile closer to the line, their values decrease by 0.6%. All these negative impacts are companied by some positive local effects: condos located between 1 and 1.5 mile radius of the line, their values increase by 9.2% and condos located between a 1.5 and 2 mile radius of the line, their values increase by 5.4%. There are no significant local effects after the construction event. Figures 4 and 5 show the surface plots of the graphical relationship between the main distance variables ‘DID_HRT’ and ‘DID_HRT1’ and condo prices across the study periods.

Surface Plot of condo price and distance variable across the years after ground-breaking event

Surface Plot of condo price and distance variable across the years after construction started

6 Conclusion

South Oahu’s notorious traffic congestion, limited land mass, growing population and attempts to diversify Oahu’s economy provide numerous opportunities for public transit. In this paper, we study the impact of the HRT on property values in Oahu from 2006 to 2015. Due to the big bandwidth (0.9) chosen for the semiparametric model, it produces almost similar results as the OLS model. This proves that the correct bandwidth selection is very important. Too large bandwidth tends to over-smooth the data, but too small bandwidth tends to produce more noises. This paper uses the fixed effects model controlling for about 130 groups to get rid of many unobserved heterogeneities within those groups that are constant across the study periods. This study finds that the two different segments of the housing market produce different reactions towards the ground-breaking event of the HRT and its construction event. There are many controversies and hurdles before the completion of the HRT. But for the single-family housing market, the homeowners’ negative reaction towards the HRT after the ground-breaking event seems to disappear after the construction started. On the other hand, some condo owners’ positive reaction towards the HRT after the ground-breaking event seems to disappear after the construction started. For future study, we need to do a survey to see the mentality changes between the single-family house owners and condo owners towards the two events.

References

Bajari, P., & Kahn, M. (2005). Estimating housing demand with application to explaining racial segregation in cities. Journal of Business and Economics Statistics, 23(1), 20–33.

Billings, S. (2011). Estimating the value of a new transit option. Regional Science and Urban Economics, 41(6), 525–536.

Cervero, R. (2004). Effects of light and commuter rail transit on land prices: Experiences in San Diego county. Journal of the Transportation Research Forum, 43(1), 121–138.

Chatman, D., Tulach, N., & Kim, K. (2012). Evaluating the economic impacts of light rail by measuring home appreciation: A first look at New Jersey’s river line. Urban Studies, 49(3), 467–487.

Chen, H., Rufolo, A., & Dueker, K. J. (1998). Measuring the Impact of Light Rail Systems on Single-Family Home Values – a Hedonic Approach with Geographic Information System Application. Land Use and Transportation Planning and Programming Applications, 1617, 38–43.

Chopra, S., Trampy, T., Leahy, J., Caplin, A., & Lecun, Y. (2007). Discovering the hidden structure of house prices with a nonparametric latent manifold model. In Proceedings of the 13th ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (pp. 173–182). New York: ACM.

Cleveland, W., & Devlin, S. (1988). Locally weighted regression: An approach to regression analysis by local fitting. Journal of the American Statistical Association, 83(403), 596–610.

Dubé, J., Thériault, M., & Des Rosiers, F. (2013). Commuter rail accessibility and house values: The case of the Montreal South Shore, Canada, 1992–2009. Transportation Research Part A: Policy and Practice, 54, 49–66.

Duncan, M. (2011). The synergistic influence of light rail stations and zoning on home prices. Environment and Planning A, 43(9), 2125–2142.

Espey, M., & Lopez, H. (2000). The impact of airport noise and proximity on residential property values. Growth and Change, 31(3), 408–419.

HART. (2015). The rail facts—Honolulu Rail Transit. [online] Accessed November 19, 2015, from http://www.honolulutransit.org/rail-facts.aspx

Hess, D., & Almeida, T. (2007). Impact of the proximity to light rail rapid transit on station-area property values in Buffalo, New York. Urban Studies, 44(5/6), 1041–1068.

Mathur, S., & Ferrell, C. (2013). Measuring the impact of sub-urban transit-oriented developments on single-family home values. Transportation Research Part A: Policy and Practice, 47, 42–55.

McMillen, D., & Redfern, C. (2010). Estimation and hypothesis testing for nonparametric hedonic house price functions. Journal of Regional Science, 50(3), 712–733.

Mohammad, S., Graham, D., Melo, P., & Anderson, R. (2013). A meta-analysis of the impact of rail projects on land and property values. Transportation Research Part A: Policy and Practice, 50, 158–170.

Ohsfeldt, L., & Smith, A. (1985). Estimating demand for heterogeneous goods. The Review of Economics and Statistics, 67(1), 165–171.

Rosen, S. (1974). Hedonic prices and implicit markets: Product differentiation in pure competition. Journal of Political Economy, 82(1), 34–55.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2017 Springer International Publishing AG

About this paper

Cite this paper

Yu, P., Levy, J. (2017). Estimating the Value of the Honolulu Rail Transit Project: A Semiparametric Analysis of Property Values on Oahu, HI. In: Bilgin, M., Danis, H., Demir, E., Can, U. (eds) Empirical Studies on Economics of Innovation, Public Economics and Management . Eurasian Studies in Business and Economics, vol 6. Springer, Cham. https://doi.org/10.1007/978-3-319-50164-2_16

Download citation

DOI: https://doi.org/10.1007/978-3-319-50164-2_16

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-50163-5

Online ISBN: 978-3-319-50164-2

eBook Packages: Business and ManagementBusiness and Management (R0)