Abstract

Investment decisions in power plants and other assets are typically made under evolving uncertainties. Power companies often have managerial discretion over the timing of the investment as well as flexibility regarding the type of technology. By abstracting from some real-world details, the real options approach provides an elegant mathematical framework in which to assess the value of such flexibilities to provide both managerial and policy insights. In this chapter, we introduce the real options approach and contrast it with the now-or-never net present value perspective. Besides dealing with the issue of optimal timing , the real options approach also enables a power company to value operational flexibility , e.g., in the form of faster ramping, as compound options . Other flexibilities, such as modularized investment and endogenous capacity choice , are also amenable to analysis via this approach. Finally, the impact of risk aversion is explored, and the chapter concludes with extensions and exercises for further analysis.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

- Real Options Approach

- Optical Analysis

- Power Company

- Elegant Mathematical Framework

- Optimal Investment Threshold

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

Investment decisions in power plants and other assets are typically made under evolving uncertainties. Power companies often have managerial discretion over the timing of the investment as well as flexibility regarding the type of technology. By abstracting from some real-world details, the real options approach provides an elegant mathematical framework in which to assess the value of such flexibilities to provide both managerial and policy insights. In this chapter, we introduce the real options approach and contrast it with the now-or-never net present value perspective. Besides dealing with the issue of optimal timing , the real options approach also enables a power company to value operational flexibility , e.g., in the form of faster ramping, as compound options . Other flexibilities, such as modularized investment and endogenous capacity choice , are also amenable to analysis via this approach. Finally, the impact of risk aversion is explored, and the chapter concludes with extensions and exercises for further analysis.

7.1 Assumptions and the Need for Dynamic Programming

In previous chapters, we observed that it may be beneficial to delay investment in new technologies when there is uncertainty concerning prices or performance. For example, consider a small power company that may invest in a new power plant from which it will earn revenues by selling the generated electricity at the prevailing spot price of power and incur costs associated with fuel purchases.Footnote 1 At the time of investment, the company must pay a one-time capital cost to cover the expenses associated with purchasing the equipment and installing it. Subsequently, there may be operating and maintenance (O&M) expenses not related directly to fuel costs. The basic question in engineering economics is, “Is it profitable to proceed with the investment now?” For this purpose, it is straightforward to calculate the expected now-or-never net present value (NPV) of investment and to determine whether it warrants immediate investment.

However, if the power company has exclusive rights to invest at a particular location, e.g., because of licensing agreements, then it also has the discretion to consider investing at a later date. Indeed, given the trajectory of electricity and fuel prices, it may be beneficial to delay the adoption decision by a year. In doing so, the power company must trade off the following three aspects in determining the correct timing:

-

1.

The marginal benefit from postponing the investment cost. Rather than paying the full investment cost now, delaying the project’s start by a year would mean incurring the discounted investment cost.

-

2.

The marginal benefit from starting the project with higher electricity prices or lower fuel prices. It may be profitable to invest immediately, but the trajectory of prices may be such that it is beneficial to delay adoption.

-

3.

The marginal cost from forgone cash flows in the waiting period. In effect, the cash flows that the power company could have been earning are an opportunity cost that must be figured into its decision.

In general, if the power company has the discretion to defer investment perpetually, then what should be the optimal time to invest? For example, in Fig. 7.1, the NPV of a hypothetical power plant is given as a function of the current electricity price. In addition to being able to invest immediately, the power company may undertake the same project in five or ten years’ time. Depending on the current electricity price and its growth rate, it may be optimal to invest immediately, wait five years, wait ten years, or never invest. Thus, the NPV of the overall investment opportunity is the upper envelope of the three NPV functions as well as zero. Furthermore, if underlying prices are uncertain, then how would the optimal investment decision be affected? How would characteristics of alternative technologies, e.g., operational flexibility or sizing , affect the investment decision? Would a modular investment strategy make sense in certain situations? Finally, how would the decisions change if the power company were risk averse? Tackling all of these features within an elegant mathematical framework would be desirable in order to elicit managerial insights.

NPV of power plant in different starting years

While the timing question may be addressed adequately via the now-or-never NPV approach , the analysis becomes cumbersome and leads us to propose a more suitable framework for decision making: real options. Essentially, real options is a dynamic programming approach to making optimal decisions in which investment and operational opportunities are thought of as options on real (rather than financial) assets. In finance, an “option” refers to an instrument that provides the holder with the right, but not the obligation, to obtain an asset in exchange for a so-called strike price [20]. Given suitable simplifying assumptions, real options can provide powerful insights into the value of managerial flexibility in appraising alternative investment proposals. For example, the now-or-never NPV approach would not be able to distinguish between investing in a single 100 MW power plant and investing in two 50 MW modules constructed sequentially when there is uncertainty about the electricity price. Yet intuitively, most managers would attribute more value to the modular approach, even though the now-or-never NPV approach would give the same expected value. Hence in this chapter, we abstract from some of the details of the previous chapters in order develop the intuition and methodology for applying real options analysis to investment and operational problems in the electricity industry.

Before proceeding to the exposition of the real options approach, we first state the assumptions and define the notation to be used for the rest of this chapter. Without loss of generality, we assume that the electricity price at time \(t \ge 0\), \(E_t\), follows a geometric Brownian motion (GBM). First, a Brownian motion (BM) may intuitively be thought of as a continuous-time analogue of a random walk with drift [35]. In other words, the absolute changes in the value of a random parameter following a BM are normally distributed. Second, in dealing with prices, it is convenient to limit the range of realizations to be nonnegative.Footnote 2 Thus, rather than considering absolute changes, it is expedient to deal with percentage changes, and a GBM is a stochastic process in which the percentage changes (rather than absolute changes) in the value are normally distributed. Consequently, if \(E_t\) follows a GBM, then:

where \(\mathrm {d}z_t\) is the increment to a BM at time t, \(\alpha \) is the annualized drift rate , \(\sigma \ge 0\) is the annualized percentage volatility , and \(E_0 \equiv E\).Footnote 3

Illustrative Example 7.1

GBM sample paths

If we ignore the stochastic \(\mathrm {d}z_t\) term, then we may derive the expected value of the GBM in year t conditional on E as \(\mathbb {E}_{E}[E_t]=E e^{\alpha t}\). In effect, the GBM, on average, exhibits exponential growth. Once the stochastic \(\mathrm {d}z_t\) term is considered, sample paths for the GBM may be generated that evolve with uncertainty around the conditional expectation. In Fig. 7.2, the forecast value, \(\mathbb {E}_{E}[E_t]=E e^{\alpha t}\), is plotted (solid series) along with five sample paths (dotted series) from a GBM with parameters \(\alpha =0.10\), \(\sigma =0.20\), and \(E=50\) over a period of ten years. Note that the forecast value after ten years is \(50 e^{0.10 \times 10}=135.91\).\(\Box \)

Forecast value and sample paths of a GBM

Taking the dynamic programming approach (see Appendix E for a summary) to solving real options problems [12], we assume that all cash flows are real and the exogenous discount rate is \(\rho > \alpha \) . Without loss of generality, we assume that the power company holds a perpetual option to invest in a power plant that will last forever once constructed. The latter assumption about infinite lifetime may be easily relaxed. However, the former is necessary to ensure analytical solutions that will facilitate insights. Furthermore, it may be justified by the fact that typically, an investor in the electricity industry will have monopoly rights to build a facility at a particular location, e.g., through either an agreement with the municipal authority or rights to the land. Finally, the impact of a finite option to build on the optimal investment threshold price is weak when the time to expiration is relatively large.

At the optimal time, the power company pays a deterministic capital cost, I (in $), to trigger the investment in the power plant. For now, we disregard the capacity size of the facility, i.e., we assume that it generates a notional 1 MWh of electricity per annum. Thus, I may be interpreted as a per-unit capacity cost. We assume that the power plant is constructed immediately once ordered by the power companyFootnote 4 and starts generating electricity at heat rate H (in MWh\(_{th}\)/MWh), which is sold at price \(E_t\) (in $/MWh). For now, we also assume that the fuel price at time t, \(F_t\) (in $/MWh\(_{th}\)), is constant, i.e., \(F_t=F\). In subsequent sections, we will explore the implications of relaxing some of these assumptions. However, in order to establish a benchmark and to gain intuition for how investment with a deferral option differs from a now-or-never NPV approach , we proceed to a stylized example in Sect. 7.2 with investment in a single power plant of given capacity. Next, in Sects. 7.3 and 7.4, we tackle flexibility in operations and modularity in investment, respectively. Sections 7.5 and 7.6 allow for the plant’s capacity to be a decision variable in either a continuous or discrete setting. In order to examine the effect of risk aversion on investment timing, we expand the framework in Sect. 7.7 to incorporate concave utility functions. In Sect. 7.8, we summarize the chapter and provide an overview of the recent literature. End-of-chapter exercises are included in Sect. 7.9. Section 7.10 provides MATLAB codes for solving numerical examples.

The nomenclature for the rest of the chapter is as follows:

Indices

- \(i,i^\prime \) :

-

Index for states.

- j :

-

Index for projects.

- s, t :

-

Index for time.

Parameters

- \(A^j\) :

-

Investment cost term for power plant j with endogenous sizing [$/(MWh)\(^2\)].

- \(B^j\) :

-

Investment cost superscript for power plant j with endogenous sizing (unitless).

- \(E_t\) :

-

Electricity price at time t [$/MWh].

- \(F_t\) :

-

Fuel price at time t [$/MWh\(_{th}\)].

- \(H^j\) :

-

Heat rate of power plant j [MWh\(_{th}\)/MWh].

- \(I^j\) :

-

Investment cost of power plant j [$].

- \(K^j\) :

-

Annual electricity output of power plant j [MWh].

- \(S^{i,i^\prime ,j}\) :

-

Switching cost between states i and \(i^\prime \) of power plant j [$].

Constants and Rates

- \(\alpha \) :

-

Percentage growth rate [1/year].

- \(\beta _1 (\beta _2)\) :

-

Positive (negative) root of the characteristic quadratic.

- \(\gamma \) :

-

Relative risk aversion parameter.

- \(\rho \) :

-

Discount rate [1/year] .

- \(\sigma \) :

-

Percentage volatility [1/year].

Functions

- \(\mathscr {I}(K^j)\) :

-

Investment cost for power plant j with endogenous capacity sizing [$].

- \(\mathscr {Q}(\beta )\) :

-

Characteristic quadratic function.

- \(\mathscr {U}(E)\) :

-

Utility function given electricity price E.

- \(\mathscr {V}^j(E)\) :

-

Expected now-or-never NPV of power plant j given electricity price E [$].

- \(\mathscr {W}^j_{i}(E)\) :

-

Value of power plant j in state i given electricity price E [$].

Variables

- \(a_{i,1} (a_{i,2})\) :

-

Coefficient for the positive (negative) branch of the option value function in state i.

- \(\kappa ^j(E)\) :

-

Optimal size for power plant j given current electricity price E [MWh].

- \(\xi ^j\) :

-

Optimal investment threshold price for power plant j [$/MWh].

- \(\xi ^{i,i^\prime ,j}\) :

-

Optimal switching threshold from state i to state \(i^\prime \) for power plant j [$/MWh].

- \(\xi ^j_{NPV}\) :

-

Now-or-never NPV investment threshold price for power plant j [$/MWh].

- \(\tau ^j\) :

-

Optimal stopping time for investment in plant j.

7.2 Optimal Timing Versus Now-or-Never Net Present Value Approaches

In the now-or-never NPV approach , the expected discounted revenues of a project are compared with its investment cost . The instantaneous cash flows of a power plant with heat rate H at time t are \(E_t-H F_t\). Assuming that the electricity price follows a GBM and that the fuel price is constant at F, the expected now-or-never NPV of such a power plant is:

In Eq. (7.2), we use the fact that the conditional expectation of a continuous random variable involves taking an integral. Thus, the first line is effectively a double integration, and without loss of generality, the order of integration may be reversed. We use this fact in the second line by moving the conditional expectation operator inside the integral with respect to time. Since \(\mathbb {E}_{E}[E_t]=E e^{\alpha t}\), we obtain the expression in the second line, and evaluating this integral yields the result in the final line. Intuitively, it states that the expected now-or-never NPV of such a power plant is the difference between the present value of the operating cash flows (stemming from electricity sales and fuel purchases) and the up-front investment cost. Consequently, if the option to defer investment is ignored, then investment occurs immediately as long as \(\mathscr {V}(E) \ge 0\). Otherwise, investment never occurs.

Rather than investing immediately, it may be desirable for the power company to postpone taking action. For example, the electricity price may be likely to increase in the next few years. The increase in expected revenues along with the delay in paying the investment cost could make deferral favorable. However, the forgone revenues from not having an active power plant in the intervening years are an opportunity cost of delaying that would have to be factored into the decision. Thus, the power company could consider waiting T years from now and then investing immediately in the power plant. The expected NPV of such a strategy is simply \(e^{-\rho T} \mathbb {E}_{E}[\mathscr {V}(E_T)]=\frac{E e^{-(\rho -\alpha )T}}{\rho -\alpha }-\frac{HF e^{-\rho T}}{\rho }-Ie^{-\rho T}\), i.e., it is the discounted expected NPV of a power plant that is constructed in T years when the electricity price is \(E_T\). To elaborate, the expected NPV of a power plant that is constructed in T years is \(\mathbb {E}_E \left[ \int _T^\infty \left( E_t-H F\right) e^{-\rho t} dt\right] -Ie^{-\rho T}\). Note that the conditional expectation may be written as \(\mathbb {E}_E \left[ \mathbb {E}_{E_T}\left[ \int _T^\infty \left( E_t-H F\right) e^{-\rho t} dt\right] \right] \) because of the law of iterated expectations, i.e., \(\mathbb {E}\left[ X\right] =\mathbb {E}\left[ \mathbb {E}\left[ X|Y\right] \right] \), where X and Y are random variables. Furthermore, since the GBM is a Markov process, i.e., the probabilistic structure of the future given the present is independent of the past, the inner conditional expectation may be rendered as \(\int _0^\infty \left( E_Te^{\alpha t^\prime }-H F\right) e^{-\rho (t^\prime +T)} dt^\prime \) after the change of variable \(t^\prime =t-T\). Thus, this integral becomes \(e^{-\rho T} \mathscr {V}(E_T)\) after including the discounted investment cost.

Illustrative Example 7.2

Investment timing at discrete points in time

Using parameter values of \(I=100\), \(\rho =0.10\), \(\alpha =0.05\), \(F=20\), and \(H=2.5\), we obtain the value functions for \(T=0\), \(T=5\), and \(T=10\) in Fig. 7.1. We first note that since the power plant is to generate a notional 1 MWh of electricity per annum, this results in an investment cost of $876/kW. Also, the heat rate implies a 40 % electrical conversion efficiency. These two parameters are in line with the characteristics of most gas-fired plants. Next, in terms of investment timing, if the power company can construct the plant at only these three points in time, then its optimal decision is dependent on the current electricity price. For example, if the current electricity price is $25/MWh, then it is optimal to invest in ten years. This is because the electricity price will need a decade to increase to a level that makes the plant profitable. Plus, the investment cost will be discounted. On the other hand, a relatively high current electricity price, e.g., greater than $60/MWh, warrants immediate investment. Intuitively, waiting is not worthwhile because the price is high enough to make the opportunity cost of not investing more than offset any benefit from deferral. An electricity price in the middle of the range makes it optimal to invest after five years, whereas a very low electricity price means that it is optimal never to invest. Therefore, the value of the entire investment opportunity to the power company is the upper envelope of the value functions as well as zero in Fig. 7.1.\(\Box \)

Suppose now that instead of having the option to invest in the power plant only at certain discrete points in time, i.e., \(T=0, 5, 10\), the power company may start the project at any point in time. In that case, the upper envelope in Fig. 7.1 reflecting the value of the investment opportunity should become a smooth curve and indicate the optimal investment threshold price . Using dynamic programming , we will derive this function and threshold rigorously. We assume that there are two states of the world: 0, in which the power company is waiting to invest, and 1, in which it has an active power plant. Working backward from state 1, we know that its value function is just the expected present value of an active power plant, i.e.:

Now, in state 0, we begin with the Bellman equation in order to value \(\mathscr {W}_0(E)\) and to determine the optimal investment threshold price, \(\xi \):

This states that the instantaneous return on the option to invest is equal to its expected appreciation. Intuitively, an external assessor’s required rate of return on the option to build the power plant, \(\rho \), must equal the expected value from owning the right to build the power plant outright. Expanding the right-hand side of Eq. (7.4) via Itô’s lemma and re-arranging, we obtain the following second-order ordinary differential equation (ODE) :

where we use the fact that \(\mathbb {E}_{E}\left[ \mathrm {d}E\right] =\alpha E \mathrm {d}t\) and \(\left( \mathrm {d}E\right) ^2=\sigma ^2 E^2 \mathrm {d}t\) in going from the first line to the second.

The general solution to the ODE in Eq. (7.5) is of the power form, i.e.:

which is subject to the following boundary conditions:

Intuitively, Eq. (7.7a) states that the option to invest in the power plant becomes worthless as the electricity price tends to zero. Since zero is an absorbing state for the GBM , it follows that there will be no value from either waiting to invest in such a plant or having an active one immediately. Next, Eq. (7.7b) is the value-matching condition , which requires the value of the investment opportunity to equal the expected NPV, \(\mathscr {W}_1(E)-I\), at the optimal investment threshold price, \(\xi \). Indeed, the value lost from killing the option must equal the value gained from an active power plant at this trigger price. Finally, Eq. (7.7c) is the smooth-pasting condition , which is actually a first-order condition for optimization that reflects the fact that the marginal benefit of waiting must equal the marginal cost of waiting at \(\xi \).

Substituting the function from Eq. (7.6) and its derivatives into Eq. (7.5), we obtain:

where \(\beta \) is taken as a generic parameter and \(\mathscr {Q}(\beta )\) is the fundamental characteristic quadratic function , which implicitly defines \(\beta _1\) and \(\beta _2\) as its two roots. Although both of these roots can be solved for explicitly, it becomes apparent from the geometry of the problem that \(\beta _1>1\) and \(\beta _2<0\) as in Fig. 7.3. To observe this, note that the expression in Eq. (7.8) is an upward-facing parabola with \(\mathscr {Q}(0)=-\rho <0\) and \(\mathscr {Q}(1)=\alpha -\rho <0\). The latter inequality implies that \(\beta _1>1\) because the parabola is still negative at \(\beta =1\). Likewise, the former inequality implies that \(\beta _2<0\) because the parabola is still negative at \(\beta =0\).

Characteristic quadratic function, \(\mathscr {Q}(\beta )\), for \(\alpha =0.05\), \(\rho =0.10\), and \(\sigma =0.20\)

Now, if \(a_{0,1} E^{\beta _1}\) is a solution to the ODE in Eq. (7.5), then so is \(a_{0,2} E^{\beta _2}\), where \(a_{0,1}\) and \(a_{0,2}\) are endogenous coefficients that depend on \(\xi \). Thus, we have:

Since the latter term in Eq. (7.9) goes to infinity as E goes to zero, it is inconsistent with the boundary condition in Eq. (7.7a). Therefore, it must be the case that \(a_{0,2}=0\), and, consequently, we obtain:

We now use the expression from Eq. (7.10) in Eqs. (7.7b) and (7.7c) to solve for \(\xi \) and \(a_{0,1}\):

Substituting the solution for \(a_{0,1}\) from Eq. (7.12) into Eq. (7.11), we obtain:

For comparison with the now-or-never NPV , we set the expression for \(\mathscr {W}_1(E)-I\) to zero in Eq. (7.3) and solve for E to obtain \(\xi _{NPV}=\left( \frac{\rho -\alpha }{\rho }\right) \left( HF+\rho I\right) \). This means that investment should occur only if the current price is high enough to cover the amortized operating and investment costs. By contrast, via the real options approach, \(\xi \) in Eq. (7.13) results in a higher threshold price for investment because \(\frac{\beta _1}{\beta _1-1}>1\).Footnote 5 This discretion to wait for a higher threshold vis-à-vis the now-or-never NPV approach stems from a combination of positive drift and volatility in the electricity price. Note that even if \(\sigma =0\), then the optimal investment threshold in Eq. (7.13) is greater than the now-or-never one. In particular, \(\lim _{\sigma \rightarrow 0} \beta _1 = \frac{\rho }{\alpha }\) from Eq. (7.8), which leads to \(\lim _{\sigma \rightarrow 0} \xi = HF+\rho I>\xi _{NPV}\). Indeed, even without uncertainty in the electricity price, as long as the power company has the discretion to wait for a higher price at which to launch the power plant’s operations, it will do so until the marginal benefit of waiting is just equal to the marginal cost of waiting , which results from the forgone cash flows in the waiting period. With greater uncertainty, the marginal benefit of waiting increases by more than the marginal cost because the latter depends only on the opportunity cost of lost cash flows in the immediate future. However, the marginal benefit of waiting is related to the possibility of a higher starting price for the power plant in the future, which is affected to a greater extent by uncertainty. Hence, with the deferral option, the value of the power plant project is higher, yet this also increases the opportunity cost of killing the option to wait, thereby leading to a higher investment threshold price.

Insights about investment under uncertainty may be facilitated via numerical examples. We first consider the investment decision in Illustrative Example 7.3. Next, we explore sensitivity analyses with respect to \(\sigma \), \(\alpha \), and \(\rho \) in Illustrative Examples 7.4–7.6.

Illustrative Example 7.3

Investment under uncertainty with continuous time

Here, we use \(\alpha =0.05\), \(\rho =0.10\), \(\sigma =0.20\), \(I=100\), \(H=2.5\), and \(F=20\) as base parameters. First, we plot the expected NPV and value of the investment opportunity with respect to the electricity price, E, in Fig. 7.4. The expected NPV function, \(\mathscr {W}_1(E)-I\), is the same as the immediate investment NPV in Fig. 7.1. Recall that when we allowed investment to occur only at discrete points in time, the value of the investment opportunity comprised the upper envelope of the NPV functions. By contrast, the real options approach enables such a comparison to be made at every infinitesimal point in time. Thus, as the time intervals between alternative investment opportunities go to zero, the kinked function in Fig. 7.1 becomes a smooth convex one, as indicated in Fig. 7.4. Note that the expected NPV of immediate investment, \(\mathscr {W}_1(E)-I\), equals zero for \(\xi _{NPV}=30\). However, the value of the investment opportunity stemming from the real options approach, \(\mathscr {W}_0(E)\), is strictly above the expected NPV, thereby revealing that there is positive value to waiting. In fact, it is optimal to wait until the electricity price hits the threshold \(\xi =79.30\). In the parlance of financial options, it is worthwhile retaining the option until it is deep “in the money.” Furthermore, as the initial electricity price goes to zero, the value of the option to invest also goes to zero because investment never occurs in that case.\(\Box \)

Expected NPV, \(\mathscr {W}_1(E)-I\), and value of the investment opportunity, \(\mathscr {W}_0(E)\), for \(\alpha =0.05\), \(\rho =0.10\), \(\sigma =0.20\), \(I=100\), \(H=2.5\), and \(F=20\)

Sensitivity of \(\xi \), \(\xi _{NPV}\), and \(\frac{\beta _1}{\beta _1-1}\) with respect to \(\sigma \) for \(\alpha =0.05\), \(\rho =0.10\), \(I=100\), \(H=2.5\), and \(F=20\)

Expected NPV, \(\mathscr {W}_1(E)-I\), and value of the investment opportunity, \(\mathscr {W}_0(E)\), for \(\alpha =0.05\), \(\rho =0.10\), \(\sigma =0\), \(I=100\), \(H=2.5\), and \(F=20\)

Illustrative Example 7.4

Sensitivity analysis of investment under uncertainty with respect to volatility

Here, we vary \(\sigma \) while holding all other parameters constant in order to examine the sensitivity of \(\xi \) to uncertainty. In Fig. 7.5, we note that the now-or-never investment threshold, \(\xi _{NPV}\), is not affected by uncertainty and remains constant at $30/MWh. However, the real options threshold, \(\xi \), increases from a value of $60/MWh (for \(\sigma =0\)) to nearly $90/MWh (for \(\sigma =0.25\)). Thus, greater uncertainty increases the investment threshold as the value of waiting becomes larger.Footnote 6 Consequently, the “wedge” between the now-or-never and real options thresholds, \(\frac{\beta _1}{\beta _1-1}\), increases with uncertainty as well.Footnote 7

An example of the value functions for \(\sigma =0\) is given in Fig. 7.6 to illustrate that there is a value in waiting since the electricity price is still going to increase. However, without the presence of uncertainty, its magnitude is reduced.

The effect of uncertainty on the value of the investment opportunity is summarized in Fig. 7.7, in which the relative value of \(\mathscr {W}_0(E)\) to \(\mathscr {W}_1(E)-I\) at \(E=50\) is plotted. Hence, higher uncertainty increases the discretion to wait, which leads to a higher investment threshold.\(\Box \)

Sensitivity of relative option value, \(\frac{\mathscr {W}_0(E)}{\mathscr {W}_1(E)-I}\), with respect to \(\sigma \) for \(\alpha =0.05\), \(\rho =0.10\), \(E=50\), \(I=100\), \(H=2.5\), and \(F=20\)

Illustrative Example 7.5

Sensitivity analysis of investment timing with respect to the drift rate

In Fig. 7.8, we vary \(\alpha \) while holding all other parameters constant. Intuitively, we would postulate that an increase in the drift rate would increase the investment threshold since it would be desirable to wait for a higher future electricity price at which to launch the power plant’s operations. Somewhat surprisingly, \(\xi \) actually decreases with \(\alpha \). In order to explain this seemingly counterintuitive outcome, we plot \(\xi _{NPV}\) and note that it is also decreasing but at a faster rate. Indeed, from Eq. (7.13), an increase in \(\alpha \) leads to a decrease in the now-or-never threshold, \(\xi _{NPV}\). But if we look at the expected NPV of the power plant upon investment at \(\xi \), we obtain \(\left( \frac{\beta _1}{\beta _1-1}\right) \left[ \frac{HF}{\rho }+I\right] -\frac{HF}{\rho }-I\). In other words, it is the “wedge” between \(\xi \) and \(\xi _{NPV}\) that is affected by \(\alpha \). Plotting the wedge, i.e., \(\frac{\beta _1}{\beta _1-1}\) in Fig. 7.8, we see that it is indeed increasing with respect to \(\alpha \), i.e., a higher drift rate increases the expected NPV of investment at the real options trigger.\(\Box \)

Sensitivity of \(\xi \), \(\xi _{NPV}\), and \(\frac{\beta _1}{\beta _1-1}\) with respect to \(\alpha \) for \(\sigma =0.20\), \(\rho =0.10\), \(I=100\), \(H=2.5\), and \(F=20\)

Illustrative Example 7.6

Sensitivity analysis of investment timing with respect to the discount rate

A similar breakdown of the behavior of \(\xi \) may be done with respect to \(\rho \) . Again, intuitively, we would imagine that an increase in the discount rate would make the future less important, thereby reducing the incentive to wait. Yet, Fig. 7.9 tells a story that seems to belief our understanding since \(\xi \) actually increases with \(\rho \). However, as with the analysis with respect to \(\alpha \), it is important to note that the wedge, \(\frac{\beta _1}{\beta _1-1}\), is the main driver of the result. Plotting it respect to \(\rho \), we are able to reconcile the finding with our intuition: a higher discount rate facilitates investment even as it lowers the expected NPV of an operational power plant.\(\Box \)

Sensitivity of \(\xi \), \(\xi _{NPV}\), and \(\frac{\beta _1}{\beta _1-1}\) with respect to \(\rho \) for \(\sigma =0.20\), \(\alpha =0.05\), \(I=100\), \(H=2.5\), and \(F=20\)

7.3 Operational Flexibility

In Sect. 7.2, we focus on the optimal timing of the investment decision, assuming that the power plant operates forever. In other words, the power company’s decision was completely irreversible. However, in many cases, there is at least partial reversibility in the form of subsequent managerial discretion to abandon, modify, or suspend temporarily the power plant. In this section, we focus on the latter aspect, i.e., treatment of the so-called compound option to turn the power plant on and off again after it has been constructed.

Given the volatile nature of energy prices, such flexibility may be highly valuable. Indeed, [9] showed that by accounting for the option value of such flexibility, plants being sold in California after deregulation in the late 1990s were valued at higher than their book values as indicated by the NPV approach. In particular, gas-fired power plants have the flexibility to ramp up and down relatively quickly, although this occurs at a cost and may be constrained by minimum uptimes. For example, a gas-fired power plant with a maximum power capacity of 431 MW requires 1200 GJ of fuel (or approximately 333 MWh\(_{th}\)) for a “hot start” (immediately one hour after the plant is shut down), which leads to a startup cost of almost $7000, assuming a fuel price of $20/MWh\(_{th}\). These calculations are based on a combined-cycle gas turbine (CCGT) plant installed in 2010 in Aghada, Republic of Ireland [41]. Furthermore, according to the same source, CCGT plants have constraints on minimum uptimes and downtimes (typically four hours each).

Using the real options approach, we can analyze how the availability of such partial flexibility in the plant’s operations influences not only the value of the investment opportunity but also the initial investment decision. Intuitively, any power plant operator would value a flexible power plant more. However, the value of this flexibility is difficult to quantify via a now-or-never NPV approach. For example, at what threshold electricity price would it be optimal to suspend or to resume operations? If the value of operational flexibility increases with electricity price volatility, then how does it affect the investment threshold vis-à-vis that from Sect. 7.2?

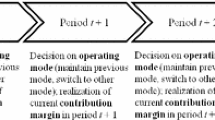

In order to focus on the implications of operational flexibility, we assume that after investment, the plant may be in one of two states: on (state 1) or off (state 2).Footnote 8 Transitioning between these two states incurs fixed resumption and suspension costs, \(S^{2,1}\) and \(S^{1,2}\), respectively, as indicated in Fig. 7.10. Associated with these transitions are threshold prices, \(\xi ^{2,1}\) and \(\xi ^{1,2}\), which will be determined endogenously.Footnote 9 Thus, we abstract from technical constraints of actual power plants such as finite ramping rates and minimum uptimes and downtimes. Instead, we assume that these features may be captured via fixed switching costs.

State-transition diagram for a power plant with operational flexibility

Although the sequence of decisions depicted in Fig. 7.10 begins in state 0 with the option to invest and progresses to state 1 with the valuation of an active power plant with the suspension option, we solve the problem using backward induction. Specifically, we start by considering the operational decisions of the power plant given that the investment decision with associated threshold, \(\xi \), has already been undertaken. We define \(\mathscr {W}_i(E)\) as the value of the power plant in state i and use dynamic programming to find not only the value functions but also the optimal switching thresholds. First, we consider state 1 and note that the value of the plant should comprise both the expected PV of cash flows from indefinite operations and the option value to shut down. Intuitively, the latter component should increase in value as the electricity price decreases. We now formally determine the value function in state 1 by setting up the Bellman equation while keeping in mind that it should be adjusted from that in Eq. (7.4) to reflect cash flows from ongoing operations:

The second term on the right-hand side of Eq. (7.14) is precisely the instantaneous cash flow from operations. Next, we expand \(\mathrm {d}\mathscr {W}_1\) via Itô’s lemma as in Sect. 7.2 and rearrange it to obtain a second-order ODE similar to that in Eq. (7.5):

The solution to the ODE in Eq. (7.15) is similar to that in Eq. (7.9) but with an extra term reflecting the expected PV of cash flows from a perpetually operating power plant:

where \(\beta _1\) and \(\beta _2\) are still the positive and negative roots, respectively, of the characteristic quadratic function from Eq. (7.8). Here, \(\frac{E}{\rho -\alpha }-\frac{\textit{HF}}{\rho }\) represents the expected PV of a power plant that operates forever, and \(a_{1,1} E^{\beta _1}+a_{1,2} E^{\beta _2}\) is the value of the option to suspend operations. Economically, we require \(\lim _{E \rightarrow \infty } \mathscr {W}_1(E)=\frac{E}{\rho -\alpha }-\frac{\textit{HF}}{\rho }\), i.e., the value of a power plant at very high electricity prices should be simply that of one that never shuts down. Indeed, it is only for relatively low electricity prices that the plant would ever shut down. Hence, we must have \(a_{1,1}=0\), thereby resulting in:

Second, we similarly tackle the value of a suspended power plant, i.e., one that is in state 2. Since there are no instantaneous cash flows, the Bellman equation becomes:

Again, by applying Itô’s lemma to the right-hand side and rearranging, we obtain a second-order ODE :

The solution is \(\mathscr {W}_2(E)=a_{2,1} E^{\beta _1}+a_{2,2} E^{\beta _2}\), which becomes the following after application of the boundary condition \(\lim _{E \rightarrow 0} \mathscr {W}_2(E)=0\):

Hence, the value of the power plant in state 2 is simply the value of the option to resume operations in the future, which is increasing with the electricity price.

From Eqs. (7.17) and (7.20), we have two endogenous variables, \(a_{1,2}\) and \(a_{2,1}\), as well as two thresholds, \(\xi ^{1,2}\) and \(\xi ^{2,1}\), to solve for. Thus, we need a total of four equations. We obtain these by writing a pair of value-matching and smooth-pasting conditions for each of the two operational transitions. First, in shutting down the power plant, i.e., going from state 1 to 2, we obtain:

Second, we have a pair of such equations for the transition from state 2 to 1:

Intuitively, Eqs. (7.21a)–(7.22b) state that the value gained must equal the value lost from switching operating modes and that the marginal benefit must equal the marginal cost from delaying any operational transitions. However, unlike Eqs. (7.11)–(7.12), the system of equations here with operational flexibility is highly nonlinear. Therefore, in general, it is not possible to obtain closed-form solutions for the four unknowns. Instead, we must resort to numerical methods to find solutions for specific parameter values. Most computational software packages like Mathematica , MATLAB , and Octave have functions, e.g., fsolve in MATLAB, that solve nonlinear systems if a guess for the solution is available.

We provide MATLAB code in Sect. 7.10 for solving the nonlinear system resulting from Illustrative Example 7.7. But, how should the guess for the solution be calculated? One way to proceed is to find analytical solutions to a simpler system, e.g., with a one-time abandonment option from state 1 or a one-time resumption option from state 2. Considering such a simplified model from state 1, we note that the resumption option from state 2 will not be available. Thus, the following system of two equations can be easily solved for guesses \(\tilde{a}_{1,2}\) and \(\tilde{\xi }^{1,2}\):

Solving Eqs. (7.23a)–(7.23b), we obtain \(\tilde{\xi }^{1,2}=\left( \frac{\beta _2}{\beta _2-1}\right) \left( \rho -\alpha \right) \left[ \frac{\textit{HF}}{\rho }-S^{1,2}\right] \) and \(\tilde{a}_{1,2}=-\frac{\left( \tilde{\xi }^{1,2}\right) ^{1-\beta _2}}{\beta _2\left( \rho -\alpha \right) }\) as the guesses for \(\xi ^{1,2}\) and \(a_{1,2}\), respectively. By similarly simplifying Eqs. (7.22a) and (7.22b) to remove the \(\left( \xi ^{2,1}\right) ^{\beta _2}\) terms, we obtain \(\tilde{\xi }^{2,1}=\left( \frac{\beta _1}{\beta _1-1}\right) \left( \rho -\alpha \right) \left[ \frac{\textit{HF}}{\rho }+S^{2,1}\right] \) and \(\tilde{a}_{2,1}=-\frac{\left( \tilde{\xi }^{2,1}\right) ^{1-\beta _1}}{\beta _1\left( \rho -\alpha \right) }\) as the guesses for \(\xi ^{2,1}\) and \(a_{2,1}\), respectively. Indeed, even without solving the nonlinear system numerically, we obtain the insight that with uncertainty and the option to make operational changes, the switching thresholds lead the decision-maker to be more cautious than the now-or-never NPV rule in which the plant would be shut down when the electricity price dropped below \(\left( \textit{HF}-\rho S^{1,2}\right) >\tilde{\xi }^{1,2}\) and restarted when the electricity price increased above \(\left( \textit{HF}+\rho S^{2,1}\right) <\tilde{\xi }^{2,1}\). These results follow because \(\left( \frac{\beta _1}{\beta _1-1}\right) \left( \frac{\rho -\alpha }{\rho }\right) >1\) and \(\left( \frac{\beta _2}{\beta _2-1}\right) \left( \frac{\rho -\alpha }{\rho }\right) <1\) for \(\sigma >0\). To see this, note that \(\left( \frac{\beta _2}{\beta _2-1}\right) <1\) and \(\left( \frac{\rho -\alpha }{\rho }\right) <1\). Thus, \(\left( \frac{\beta _2}{\beta _2-1}\right) \left( \frac{\rho -\alpha }{\rho }\right) <1\). On the other hand, \(\left( \frac{\beta _1}{\beta _1-1}\right) >1\) but \(\left( \frac{\rho -\alpha }{\rho }\right) <1\). Since \(\left( \frac{\beta _1}{\beta _1-1}\right) \) is the lowest when \(\sigma =0\), we can show that even in this case, we have \(\lim _{\sigma \rightarrow 0} \left( \frac{\beta _1}{\beta _1-1}\right) = \frac{\rho }{\rho -\alpha }\). Hence the product \(\left( \frac{\beta _1}{\beta _1-1}\right) \left( \frac{\rho -\alpha }{\rho }\right) \) must be greater than 1 for all \(\sigma >0\).

As in Sect. 7.2, the optimal investment threshold, \(\xi ^{0,1}\), may be found via value-matching and smooth-pasting conditions between \(\mathscr {W}_0(E)\) and \(\mathscr {W}_1(E)-I\). We remark that the optimization must occur in going from state 0 to state 1 rather than state 2 because it would not make sense for the power company to invest I only to have an idle power plant. For this reason, the thresholds should have the ordering \(\xi ^{1,2}< \xi ^{2,1} < \xi ^{0,1}\). In order to obtain \(\mathscr {W}_0(E)\), we follow the same procedure as in Eq. (7.5) to obtain:

Next, value-matching and smooth-pasting conditions yield the following system of equations:

In contrast to Eqs. (7.11)–(7.12), here an analytical solution is impossible. However, it is possible to reduce Eqs. (7.25a)–(7.25b) to one nonlinear equation for \(\xi ^{0,1}\):

Using \(\xi \) from Eq. (7.13) as a guess, we can solve numerically for \(\xi ^{0,1}\) and consequently for \(a_{0,1}\). Yet even without an analytical solution, it is possible to prove that \(\xi ^{0,1}<\xi \) by comparing the implicit definition of \(\xi ^{0,1}\) in Eq. (7.26) with the following for \(\xi \):

The two equations are identical except for the presence of the \(\left( \beta _1-\beta _2\right) a_{1,2}\left( \xi ^{0,1}\right) ^{\beta _2}\) term in Eq. (7.26), which is strictly positive. This adds to the linear term \(\left( \beta _1-1\right) \frac{\xi ^{0,1}}{\rho -\alpha }\), thereby ensuring that its intersection with the constant \(\beta _1\left( \frac{\textit{HF}}{\rho }+I\right) \) is for a lower threshold price. In Illustrative Examples 7.7 and 7.8, we demonstrate the shapes of the value functions, perform sensitivity analyses on the thresholds with respect to the volatility, and provide MATLAB code in Sect. 7.10 for solving the nonlinear system of equations.

Illustrative Example 7.7

Investment timing with operational flexibility

Using \(\alpha =0.05\), \(\rho =0.10\), \(\sigma =0.20\), \(I=100\), \(S^{1,2}=S^{2,1}=10\), \(H=2.5\), and \(F=20\) as base parameters, we plot the value functions as in Fig. 7.11. Note that the functions \(\mathscr {W}_1(E)\) and \(\mathscr {W}_2(E)\) are defined over the ranges \((\xi ^{1,2}, \infty )\) and \((0, \xi ^{2,1})\), respectively. Thus, \(\mathscr {W}_2(E)\) is a convex function that has the same gradient as \(\mathscr {W}_1(E)\) at \(\xi ^{2,1}\) and differs from it by exactly \(S^{2,1}\) at that point. Meanwhile, \(\mathscr {W}_1(E)\) has a pronounced convex shape only for relatively low values of E, whereas it becomes asymptotically linear as \(E \rightarrow \infty \). Indeed, for extremely high electricity prices, the value of the option to shut down the plant is nearly zero. Consequently, an active power plant’s value converges to that of a plant that operates forever. However, for low electricity prices, it becomes optimal to suspend operations and switch to state 2. Therefore, at \(\xi ^{1,2}\), \(\mathscr {W}_1(E)\) has the same gradient as \(\mathscr {W}_2(E)\) and differs from it by \(S^{1,2}\) at that point. Moreover, the suspension and resumption thresholds at $37.99/MWh and $61.38/MWh, respectively, are lower and higher, respectively, than the now-or-never NPV thresholds of $49/MWh and $51/MWh, respectively. Finally, the value function in state 0 satisfies the value-matching and smooth-pasting conditions with \(\mathscr {W}_1(E)-I\) at \(\xi ^{0,1}\), which at $76.23/MWh is lower than that of $79.30/MWh for \(\xi \).\(\Box \)

Value functions with operational flexibility for \(\alpha = 0.05\), \(\rho = 0.10\), \(\sigma = 0.20\), \(I = 100\), \(S^{1,2}=10\), \(S^{2,1}=10\), \(H = 2.5\), and \(F = 20\)

Sensitivity of \(\xi ^{0,1}\), \(\xi ^{1,2}\), and \(\xi ^{2,1}\) with respect to \(\sigma \) with operational flexibility for \(\alpha = 0.05\), \(\rho = 0.10\), \(I = 100\), \(S^{1,2}=10\), \(S^{2,1}=10\), \(H = 2.5\), and \(F = 20\)

Sensitivity of relative value of flexibility with respect to \(\sigma \) with operational flexibility for \(\alpha = 0.05\), \(\rho = 0.10\), \(I = 100\), \(S^{1,2}=10\), \(S^{2,1}=10\), \(H = 2.5\), and \(F = 20\)

Illustrative Example 7.8

Sensitivity analysis of operational flexibility with respect to volatility

By varying the volatility parameter, e.g., between 0.15 and 0.35, we investigate the sensitivity of the thresholds and the relative value of flexibility. In Fig. 7.12, we show that higher volatility causes the thresholds to spread wider apart. Indeed, greater uncertainty induces more hesitancy as the value of suspension from an active state increases, but this value stems from the option value of keeping the discretion to suspend alive. Likewise, from state 2, higher volatility increases the value of the option to resume operations by moving to state 1. However, this also increases the opportunity cost of exercising the option to resume operations, and, as a result, the power company is more cautious in making the operational change. As for the relative value of flexibility , we plot in Fig. 7.13 the ratio of \(a_{0,1}\) from Eq. (7.24) to that from Eq. (7.10) with respect to \(\sigma \). It increases with volatility because, intuitively, more uncertainty gives more value to the flexibility option. Here, the power company would be willing to pay about 3 % more for a power plant with such flexibility. A similar analysis for a California-based distributed generation unit may be found in [39].\(\Box \)

7.4 Modularity and Capacity Expansion

Rather than investing in a power plant all at once, it may be desirable to make incremental capacity additions. One motivation for modularizing adoption of the power plant is that the power company may prefer to observe how the electricity price is unfolding and to match capacity to the needs to the market. For example, technological advances have made it possible for small-scale modules, i.e., less than 300 MW, to be developed even for nuclear power plants [44]. By proceeding to add capacity in an incremental manner, the power company may benefit from starting cash flows sooner while adding larger modules later on [16]. Hence, although the total investment costs of modular units may be higher than that of a single large unit, these diseconomies of scale may be outweighed by the benefit from optimizing capacity additions.

In order to explore such modular capacity expansion, we assume that the power company may invest in a power plant of total capacity \(K = K^1 + K^2\) either directly or sequentially. Without loss of generality, we assume that the capital cost from “lumpy” investment, I, will be the same as the total capital cost from the modular approach, i.e., \(I^1+I^2\), where \(I^j\) is the capital cost of module j. This may be extended to treat an arbitrary number of modules as well as operational flexibility. Thus, although we ignore total economies of scale, we nevertheless have \(\frac{I^1}{K^1}<\frac{I^2}{K^2}\), i.e., relative diseconomies of scale in integrating the second module, which reflect difficulties associated with modifying fixed infrastructure. This is similar to the assumption made by [25, 40].

Figure 7.14 illustrates the sequence of decisions that are possible under the direct and modular investment strategies. In the former, the only possible transition is between states 0 and 2. Proceeding backward, state 2 is one in which both modules are active, i.e., the power company has a perpetually operating plant that outputs K MWh of electricity per year and costs I to install. Thus, the value in state 2, assuming that the electricity price follows a GBM as in Eq. (7.1), a heat rate of H , a fuel price of F , and an exogenous discount rate of \(\rho \) , is:

In state 0, the value function reflects simply the option to invest directly in such a power plant. Consequently, by following the same argument as in Eqs. (7.4)–(7.5), we have:

We let the \(^d\) denote a “direct” investment strategy with the corresponding endogenous \(a^d_{0,1}\). Via value-matching and smooth-pasting conditions between the functions in Eqs. (7.28) and (7.29), we obtain the optimal investment threshold price by following the direct investment strategy:

Analogously, we have:

State-transition diagram for a power plant with two modules

By contrast, with a modular investment strategy, the power company first invests in a module of annual output \(K^1\), i.e., going from state 0 to state 1. In state 1, its value function includes not only the expected PV of cash flows from a module that operates forever but also the option to upgrade to the second module. Thus, the value function in state 1 is:

Finally, the value function in state 0 reflects the option value to invest in the first module with the subsequent option to acquire the second one:

Under the modular strategy, we need to solve for two investment thresholds, \(\xi ^{1,2}\) and \(\xi ^{0,1}\), as well as \(a_{1,1}\) and \(a_{0,1}\). We obtain these via four value-matching and smooth-pasting conditions :

The analytical solutions are:

In comparing the solutions, we note that \(\xi ^{0,1}\) is independent of \(\xi ^{1,2}\). Indeed, although the value in state 0 is affected by that of state 1 (since \(a_{0,1}\) depends on \(a_{1,1}\)), the timing of the investment in the first module is myopic, i.e., it is as if the second module did not exist. This is due to the structure of the sequential decision-making problem. Recall that the investment is delayed up to the point that the marginal benefit of waiting equals the marginal cost of waiting. From Sect. 7.2, we know that the former quantity is related to starting the plant at a higher price and reducing the discounted investment cost. Meanwhile, the marginal cost of waiting is the opportunity cost of not earning cash flows from an active power plant. Now with a subsequent module, the marginal benefit of waiting additionally includes the discounted expected marginal benefit (from having to wait less until the second module is installed after the first one is adopted) and the discounted expected marginal cost (from having to wait longer from the initial point until the option to install the second module is available). These two extra marginal values cancel out, thereby rendering the effect of the second module on the timing inconsequential. In order to examine the properties of modularity, we next perform Illustrative Examples 7.9 and 7.10.

Illustrative Example 7.9

Investment timing with modularity

Let \(\alpha = 0.05\), \(\rho = 0.10\), \(I^{1}=40\), \(I^{2}=60\), \(K^1=0.5\), \(K^2=0.5\), \(H = 2.5\), and \(F = 20\). Thus, \(I=100\) and \(K=1.0\), and \(\sigma \) is allowed to vary between 0 and 0.35. First, Fig. 7.15 indicates the value functions with a direct investment strategy. Here, investment occurs when the electricity price reaches a threshold of $79.30/MWh. Second, in Fig. 7.16, we have the modular investment strategy. As expected, the first module is adopted at a lower threshold, i.e., $78.31/MWh, than in the direct investment strategy. A subsequent price increase to $81.95/MWh is required to trigger adoption of the second module.\(\Box \)

Value functions with direct investment strategy for \(\alpha = 0.05\), \(\rho = 0.10\), \(\sigma = 0.20\), \(I = 100\), \(K=1\), \(H = 2.5\), and \(F = 20\)

Value functions with modular investment strategy for \(\alpha = 0.05\), \(\rho = 0.10\), \(\sigma = 0.20\), \(I^{1}=40\), \(I^{2}=60\), \(K^1=0.5\), \(K^2=0.5\), \(H = 2.5\), and \(F = 20\)

Optimal thresholds under direct and modular investment strategies for \(\alpha = 0.05\), \(\rho = 0.10\), \(I^{1}=40\), \(I^{2}=60\), \(K^1=0.5\), \(K^2=0.5\), \(H = 2.5\), and \(F = 20\)

Illustrative Example 7.10

Sensitivity analysis of modularity with respect to volatility

In performing sensitivity analysis, we examine how the thresholds change with uncertainty in Fig. 7.17. As anticipated, all thresholds increase with uncertainty, with those related to the modular investment strategy sandwiching the one for the direct investment strategy. The relative value of flexibility from following a modular approach is sketched out in Fig. 7.18. For the base case of \(\alpha =0.05\), this relative value is barely 0.1 %. However, with a lower annualized percentage growth rate, it can comprise nearly 5 % of the project’s value. The reason is that a modular strategy enables the power company to take advantage of revenues from the more economic module even at relatively low prices before waiting for the right time to complete the project. Finally, this relative value of modularity decreases with uncertainty since an increase in \(\sigma \) warrants delaying investment of any type. Hence, there is less discrepancy between the direct and modular investment strategies. See [31, 38] for applications of the modular investment approach to gas-fired power plants and distributed generation facilities, respectively.\(\Box \)

Relative value of modular investment strategy for \(\rho = 0.10\), \(I^{1}=40\), \(I^{2}=60\), \(K^1=0.5\), \(K^2=0.5\), \(H = 2.5\), and \(F = 20\)

7.5 Continuous Capacity Sizing

Up to now, we have examined managerial discretion with respect to investment timing, operations, and modularity while assuming that the size of the completed power plant is simply a constant parameter, K. In reality, the size of the power plant itself may be a decision variable. Subject to land, permitting, and resource constraints, the power company may scale the plant’s capacity in order to maximize profit. Depending on the type of plant, the sizing decision may be considered continuous or discrete. For example, in an analysis of distributed generation investment, [29] models gas-fired units as having discrete capacity sizes with batteries and solar photovoltaic panels having capacities that are continuous decision variables. Likewise, [2] examines the optimal investment timing and capacity sizing problem of a run-of-river hydropower plant in Norway by assuming that the scaling decision variable is continuous. By contrast, [14] treats the capacity sizing decision of a wind farm as a discrete one. Thus, either assumption may be valid depending on the characteristics of the technology and siting constraints. In this section, we assume that the endogenous sizing decision is continuous and follow in the spirit of [6]. A discrete treatment of the sizing decision is implemented in the next section.

As in previous sections, we assume that the power company has the discretion to invest in a power plant at a time of its choosing after which it will earn a profit flow that equals the stochastic revenue from electricity sales and a deterministic operating cost. Now, in addition, the power company may also determine the size of the plant, \(\kappa (E)\), which depends on the electricity price and is the solution to the following now-or-never expected NPV maximization problem:

We assume increasing marginal construction costs because of land and material restrictions, for example. Thus, the investment cost is:

where \(A>0\) and \(B>1\) are deterministic parameters. Consequently, with this convex investment cost, the optimal capacity size is obtained by differentiating the right-hand side of equation (7.39) with respect to K and setting it equal to zero:

Hence, the maximized expected now-or-never NPV is obtained via substitution of Eq. (7.41) into the right-hand side of Eq. (7.39):

\(\mathscr {W}_1(E; \kappa (E))-\mathscr {I}(\kappa (E))\) indicates the maximized expected NPV of the power plant given that it is optimal to construct immediately. However, besides this sizing flexibility, the power company also has discretion over the investment timing. As in previous sections, it is possible to show that the value of the option to invest is:

We next determine the optimal investment threshold via value-matching and smooth-pasting conditions between the functions in Eqs. (7.42) and (7.43):

Although Eqs. (7.44a) and (7.44b) are highly nonlinear, it is possible to solve them analytically for \(\xi \):

Finally, by substituting \(\xi \) from Eq. (7.45) into Eq. (7.41), we obtain the optimal capacity size at the investment threshold price:

where we must ensure that \(\beta _1(B-1)-B>0\).

Illustrative Example 7.11

Investment with continuous capacity sizing

In order to gain more intuition about having flexibility over capacity sizing, we perform numerical examples with the following parameter values: \(\alpha = 0.01\), \(\rho = 0.10\), \(A=2.65 \times 10^{-5}\), \(B=2\), \(H = 2.5\), and \(F = 20\). We allow the volatility, \(\sigma \), to vary between 0.01 and 0.10. The parameter A corresponds approximately to the investment cost of a typical gas-fired power plant. For example, the 430 MW CCGT plant built in Aghada [41] cost $371 million. Since this is close to the capacity cost of $876/kW assumed in Sect. 7.2, we use it to calculate a total investment cost for this plant to be $377 million. By inserting this value into Eq. (7.40), we obtain \(A=\frac{377 \times 10^6}{\left( 430 \times 8760\right) ^2}=2.65 \times 10^{-5}\). Using these parameters, we obtain the value functions given in Fig. 7.19. Here, the function \(\mathscr {W}_1(E; \kappa (E))-\mathscr {I}(\kappa (E))\) represents the maximized expected NPV of the power plant from Eq. (7.42). In other words, this nonlinear function assumes that there is no discretion over the timing of the investment, but the capacity of the plant may be determined optimally as a function of the current electricity price, E. This now-or-never capacity size, \(\frac{\kappa (E)}{8760}\), is illustrated in Fig. 7.23 for different values of E and is linearly increasing as long as the electricity price is high enough to cover the discounted operating costs. A doubling of A simply reduces the optimal now-or-never capacity level. For this reason, the maximized expected NPV in Fig. 7.19 is bounded by zero. Taking the value of waiting into account means that it is optimal to invest in the plant only when the price of electricity hits the threshold \(\xi \), which is $90/MWh in this case. Thus, the difference between the functions \(\mathscr {W}_0(E)\) and \(\mathscr {W}_1(E; \kappa (E))-\mathscr {I}(\kappa (E))\) reflects the value of this deferral option. Finally, the linear function \(\mathscr {W}_1(E; \kappa (\xi ))-\mathscr {I}(\kappa (\xi ))\) is one in which there is no discretion over either investment timing or capacity sizing. As such, it reflects the now-or-never expected NPV of investing in a power plant of optimal capacity \(\frac{\kappa (\xi )}{8760}=1075\) MW immediately. Consequently, since the firm has no subsequent flexibility over its decision-making, it is exposed to losses if the electricity price decreases. Figure 7.20 repeats this figure for a doubled marginal cost of investment, i.e., \(A=5.31 \times 10^{-5}\).\(\Box \)

Value functions with capacity sizing, \(\sigma =0.10\), and \(A=2.65 \times 10^{-5}\)

Value functions with capacity sizing, \(\sigma =0.10\), and \(A=5.31 \times 10^{-5}\)

Optimal investment threshold price with endogenous capacity sizing as a function of volatility, \(\sigma \)

Illustrative Example 7.12

Sensitivity analysis of investment with continuous capacity sizing with respect to volatility

We next conduct sensitivity analysis with respect to the volatility, \(\sigma \). In Fig. 7.21, we plot the optimal investment threshold price, \(\xi \), and note that it increases monotonically. Interestingly, it is independent of the A parameter, i.e., a higher marginal cost of capacity will not affect the optimal timing of investment. This is also evident analytically from Eq. (7.45). The explanation for this result is provided by what happens to the optimal capacity size. In Fig. 7.22, we plot both the optimal capacity size, \(\frac{\kappa (\xi )}{8760}\), and the now-or-never capacity size, \(\frac{\kappa (E)}{8760}\), at the current electricity price of $50/MWh as given in Eqs. (7.46) and (7.41), respectively, for two levels of A. Since the now-or-never decision is independent of the volatility, it is constant for all values of \(\sigma \) at 119.45 MW (and 59.72 MW for the higher value of A). By contrast, optimal capacity sizing is based on waiting until the electricity price hits \(\xi \) and building a power plant of the appropriate size. For \(\sigma =0.10\), this is 1075 MW (and 537.50 MW for the higher value of A). Hence, as uncertainty increases, it is optimal to wait longer and to build a larger plant, but the impact of a higher marginal cost of capacity expansion is absorbed into the sizing decision only and leaves the optimal investment threshold unchanged. Finally, Fig. 7.23 plots the now-or-never capacity size, \(\frac{\kappa (E)}{8760}\), from Eq. (7.41) as a function of the current electricity price to indicate the linear dependence as long as the price is high enough to cover operating costs.\(\Box \)

Optimal capacity size as a function of volatility, \(\sigma \)

Now-or-never capacity size as a function of initial electricity price, E

Independent real options analyses of two discrete-sized projects, 1 and 2, for \(\sigma =0.30\)

7.6 Mutually Exclusive Technologies

In the previous section, we assumed that it is possible to determine the size of the power plant endogenously as a continuous variable. While this supposition may be valid for certain types of facilities, it does not hold for those that are available only in discrete capacity sizes. For example, wind turbines and nuclear reactors cannot be scaled continuously. Likewise, even smaller gas-fired generators are typically optimized for performance and are available in discrete sizes [29]. Thus, in choosing capacities [14] or between different technologies [37, 43], it is also desirable to consider mutually exclusive discrete alternatives from the viewpoint of real options.

In this context, [11] proposes a simple adjustment to the standard real options treatment of investment under uncertainty when considering any finite number of discrete investment opportunities under uncertainty. For example, with two projects, \(j=1,2\), of discrete size as given in Fig. 7.24, [11] would proceed as follows:

-

1.

Find the optimal investment thresholds, \(\xi ^j\), along with the endogenous coefficients, \(a^j_{0,1}\), from independent real options analysis of each alternative.

-

2.

Let \(j^*\equiv \underset{j}{\arg \max } \left\{ a^j_{0,1}\right\} \) be the project with the higher option value coefficient.

-

3.

If the current price, E, is less than project \(j^*\)’s threshold, \(\xi ^{j^*}\), then wait for the threshold \(\xi ^{j^*}\) to be hit and invest in project \(j^*\); otherwise, if \(E>\xi ^{j^*}\), then invest immediately in the project with the highest expected NPV, \(\mathscr {W}_j(E)-I^j\).

This procedure seems sensible, but it can break down when the option value coefficient for the smaller project is higher than that for the larger project, i.e., \(a^1_{0,1} > a^2_{0,1}\), and the initial electricity price is equal to the indifference level between the two NPVs. In such a situation, [11] would suggest tossing a coin to break the tie. However, given the uncertainty in the electricity price, it seems intuitive that waiting for more information would be optimal in such a situation.

Following this line of reasoning, [7] allows for the value of the option to invest to be discontinuous, i.e., dichotomous with an upper branch that straddles the indifference point, \(\tilde{E}\), at which the two projects’ expected NPVs are equal. Specifically, if we let the now-or-never expected NPV of project \(j=1,2\) be defined as:

In order to have a tradeoff between the two projects, we assume that \(K^2>K^1\) and \(I^2>I^1\) such that \(I^1/K^1<I^2/K^2\). Without loss of generality, we set \(H^1=H^2\). Thus, the power company has a mutually exclusive choice between a smaller but relatively less costly (plant 1) or a large but relatively more costly (plant 2) option along with the right to determine the timing of the investment decision. By setting the expected NPVs of the two projects equal to each other, we find the indifference point:

If we do a real options analysis of each project j independently, i.e., assuming that the other project does not exist, then we obtain the usual optimal investment threshold prices and endogenous coefficients via value-matching and smooth-pasting conditions:

Hence, the independent value of the option to invest in project j is simply

The procedure in [7] for dealing with such mutually exclusive investment opportunities is as follows:

-

1.

Order the projects by their capacities.

-

2.

Find \(a^j_{0,1}\) for each project j.

-

3.

If \(a^1_{0,1} \le a^2_{0,1}\), then the value of the option to invest will not be dichotomous because the larger project dominates the smaller one. In this case, the value of the investment opportunity is simply \(\mathscr {W}_0(E)=\mathscr {W}^2_0(E)\), i.e., project 1 can effectively be ignored.

-

4.

If \(a^1_{0,1} > a^2_{0,1}\), then the value of the option to invest will have two waiting regions:

-

a.

\(E \in [0,\xi ^1)\), which involves waiting for the price to increase until it is optimal to invest in project 1.

-

b.

\(E \in (\xi ^L,\xi ^R)\), which involves waiting for the price to decrease (increase) until it is optimal to invest in project 1 (2).

The value of the investment opportunity is thus:

$$\begin{aligned} \mathscr {W}_0(E)=\left\{ \begin{array}{lr} a^1_{0,1} E^{\beta _1},&{} \text {if } E \in [0,\xi ^1)\\ a^R E^{\beta _1}+a^L E^{\beta _2},&{} \text {if } E \in (\xi ^L,\xi ^R). \end{array} \right. \end{aligned}$$(7.52) -

a.

Thus, the dichotomous value function in Eq. (7.52) is defined over two ranges. Although \(\xi ^1\) and \(a^1_{0,1}\) are known, the thresholds, \(\xi ^L\) and \(\xi ^R\), as well as the coefficients, \(a^L\) and \(a^R\), must be found endogenously via value-matching and smooth-pasting conditions between the second branch of \(\mathscr {W}_0(E)\) in Eq. (7.52) and \(\mathscr {W}^j_1(E)-I^j\) as follows:

The system in Eqs. (7.53a)–(7.53d) is highly nonlinear and must be solved numerically. As in Sect. 7.3, guesses for the four unknowns are required. Reasonable guesses for \(\xi ^L\) and \(\xi ^R\) are \(\frac{\xi ^1+\tilde{E}}{2}\) and \(\xi ^2\), respectively. Likewise, a guess for \(a^R\) may be obtained by dropping the \(\beta _2 a^L \left( \xi ^R\right) ^{\beta _2-1}\) term in smooth-pasting Eq. (7.53d) to solve explicitly for the remaining option value coefficient. This may be substituted into the remaining smooth-pasting Eq. (7.53b) to obtain a guess for \(a^L\).

Illustrative Example 7.13

Mutually exclusive investment with high volatility

In order to illustrate how the waiting region may be dichotomous, we perform a numerical example with \(\rho =0.04\), \(\alpha =0\), \(K^1=1\), \(K^2=2.9\), \(I^1=100\), and \(I^2=900\). Without loss of generality, we set \(F=0\) and allow \(\sigma \) to range from 0.05 to 0.30. In other words, plant 2 is almost three times as large but has an investment cost that is nine times as high as that of plant 1. Note that these parameter values are different from those in Sect. 7.2 in order to obtain a nontrivial result with \(a^1_{0,1}>a^2_{0,1}\) for low values of volatility. Figure 7.24 illustrates that the two projects may be analyzed separately for a relatively high value of \(\sigma \), i.e., 0.30. Here, it is clear that \(a^1_{0,1}<a^2_{0,1}\), because \(\mathscr {W}^2_0(E)>\mathscr {W}^1_0(E)\). Thus, the optimal strategy is simple: the power company should disregard plant 1 and wait for the electricity price to hit the threshold \(\xi ^2=34.30\). The corresponding value functions are indicated in Fig. 7.25.\(\Box \)

Mutually exclusive investment opportunity in two discrete-sized projects, 1 and 2, for \(\sigma =0.30\)

Mutually exclusive investment opportunity in two discrete-sized projects, 1 and 2, for \(\sigma =0.15\)

Illustrative Example 7.14

Mutually exclusive investment with low volatility

With a relatively low level of volatility, e.g., \(\sigma =0.15\), we have \(a^1_{0,1}>a^2_{0,1}\). Consequently, the waiting region becomes dichotomous with an upper region around the indifference price, \(\tilde{E}=16.84\). This upper waiting region, reflected by \(a^R E^{\beta _1}+a^L E^{\beta _2}\), extends from \(\xi ^L=11.89\) to \(\xi ^R=21.71\). For comparison, we have \(\xi ^1=6.76\) and \(\xi ^2=20.97\). Figure 7.26 shows that the lower portion of the \(\mathscr {W}_0(E)\) function is precisely \(\mathscr {W}^1_0(E)\).\(\Box \)

Illustrative Example 7.15

Sensitivity analysis of mutually exclusive investment with respect to volatility

As \(\sigma \) is varied, we obtain waiting and immediate investment regions for the two plants considered together in Fig. 7.27. For \(\sigma \le 0.21\), it is impossible to disregard plant 1, and the dichotomous value of waiting must be considered. For example, with \(\sigma =0.15\), there are lower and upper waiting regions. In the former, the power company should wait until the electricity price increases to \(\xi ^1\) before investing immediately in plant 1. By contrast, in the latter, the power company may end up investing in either plant 1 (if the price drops to \(\xi ^L\)) or plant 2 (if the price increases to \(\xi ^R\)). However, if the current electricity price is in the range \([\xi ^1, \xi ^L]\) or \([\xi ^R, \infty )\), then it is optimal to invest immediately in plant 1 or 2, respectively. The MATLAB code in Sect. 7.10 solves the nonlinear system in Eqs. (7.53a)–(7.53d) and generates Fig. 7.27. As [7] illustrates using a similar numerical example, the percentage gain from optimally delaying investment at the indifference price relative to investing immediately as suggested by [11] may be substantial. In our example, it will be 18.31 % for \(\sigma =0.15\). Finally, this mutually exclusive analysis may be extended to allow for switching options as in Sect. 7.4, i.e., having the right to switch from plant 1 to 2 [14], or allowing for subsequent improvement in the performance of one of the two plants [37].\(\Box \)

Investment and waiting regions for a mutually exclusive investment opportunity in plants 1 and 2

7.7 Risk Aversion

In previous sections of this chapter, we assumed that the decision maker, i.e., typically a power company, is risk neutral because its objective is to maximize expected profit. While this may be justified if the standard assumptions of finance, viz., complete markets, hold and risk may be diversified by holding a portfolio of freely traded assets, such a supposition may not hold in practice. For example, besides market risk, power companies in the electric power industry may be exposed to heterogenous risk stemming from technological uncertainty associated with R&D in renewable energy technologies or the possibility of a change in policy support. Moreover, some municipally owned power companies may be inherently risk averse since they are answerable to a more conservative class of investor. Either way, it would be desirable to expand the framework for analysis to permit the decision maker to be risk averse when solving optimal timing or technology choice problems.

Taking the perspective of [19], we embed a utility function into the real options framework in order to examine how a risk-averse investor may make decisions under uncertainty with the deferral option. In the economics literature, constant relative risk aversion (CRRA) is a standard workhorse for both its analytical tractability and its desirable property that the fraction of wealth placed in a risky (as opposed to risk-free) asset by a decision-maker is independent of the initial level of wealth [33].Footnote 10 In particular, the CRRA utility function with relative risk aversion parameter \(0\le \gamma \le 1\) has the form:

Hence, as a concave function, \(\mathscr {U}(E)\) captures the risk aversion of a conservative investor.

One difficulty with incorporating the CRRA utility function is the treatment of the operating costs. This is because the function is not separable in E and \(\textit{HF}\), i.e., \(\mathscr {U}(E-HF) \ne \mathscr {U}(E)-\mathscr {U}(HF)\). Since we would like to avoid working with a function of the form \(\frac{\left( E-HF\right) ^{1-\gamma }}{1-\gamma }\), we decompose the cash flows using the approach of [4], in which operating costs are also included in a risk-averse analysis of real options decision making. Suppose that at the current time, i.e., \(t=0\), the power company has set aside all of the cash that it will need to pay for a power plant of nominal annual output 1 MWh that will cost I to build and will incur operational costs of \(\textit{HF}\) per MWh of electricity generated. If the power plant operates forever after construction, then its discounted investment and operational costs are \(I+\frac{HF}{\rho }\) (assuming a subjective discount rate \(\rho \)). This lump sum is assumed to be sitting in an interest-bearing account earning the same discount rate until the plant is constructed at optimal time \(\tau \), which implies an instantaneous cash flow of \(\rho \left( I+\frac{HF}{\rho }\right) \). Consequently, the discounted (to time 0) utility of the cash flows from this lump sum is \(\int _0^{\tau } e^{-\rho t} \mathscr {U}\left( HF + \rho I\right) dt\). Given that the power plant starts to earn revenues, \(E_t\), at time \(\tau \) that follow a GBM, the time-zero discounted expected utility of the cash flows is:

where E is the electricity price at \(t=0\). Now, since the first term in Eq. (7.55) may be reexpressed as \(\int _0^{\infty } e^{-\rho t} \mathscr {U}\left( HF + \rho I\right) dt-\int _{\tau }^{\infty } e^{-\rho t} \mathscr {U}\left( HF + \rho I\right) dt\), we can de facto decompose the cash flows as follows:

From the law of iterated expectations and the strong Markov property of the GBM ,Footnote 11 the conditional expectation in Eq. (7.56) may be rewritten as follows:

Since the first term in Eq. (7.56) is a constant, it may be ignored in determining the optimal time to invest. Thus, Eq. (7.57) is the discounted (to time \(t=0\)) expected utility of cash flows from a power plant that becomes active at \(\tau \) and operates forever. Intuitively, the inner conditional expectation’s independence from E means that the two expectations may be separated as follows:

In moving from the second to the third line of Eq. (7.58), we use Theorem 9.18 from [24], which finds a closed-form expression for the conditional expectation of an integral of a function of a Brownian motion. Here, \(\beta _1>1\) and \(\beta _2<0\) are again the positive and negative roots, respectively, of the characteristic quadratic function in Eq. (7.8). Hence, the value of the investment opportunity for a risk-averse decision-maker may be formulated as the solution to the following optimal stopping-time problem :

Using the fact that the conditional expectation of the stochastic discount factor is of power form, i.e., \(\mathbb {E}_{E} \left[ e^{-\rho \tau } \right] = \left( \frac{E}{E_{\tau }}\right) ^{\beta _1}\), as shown on page 315 of [12], and letting \(\xi \) denote the optimal threshold price, we can recast the optimal stopping-time problem in Eq. (7.59) as the following unconstrained nonlinear maximization problem:

Taking the first-order necessary condition with respect to \(\xi \), we obtain the following:

Solving Eq. (7.61), we obtain the following optimal investment threshold price:

Note that although investment thresholds are typically expressed in terms of \(\beta _1\), e.g., as in Sect. 7.2, here it is more expedient to use \(\beta _2\). Using the fact that \(\beta _1 \beta _2 = -\frac{2 \rho }{\sigma ^2}\), it can also be verified that \(\xi \) is the same as the investment threshold under risk neutrality from Eq. (7.13) for \(\gamma =0\). Although we have a closed-form expression for the optimal investment threshold under risk aversion, it is possible to prove analytically that the threshold increases with both volatility and risk aversion as one would expect. However, the proofs are tedious and are carried out in full in [4]. Intuitively, it is important to stress that both volatility and risk aversion increase the optimal investment threshold price but for vastly different reasons: greater uncertainty delays investment because the value of waiting for more information increases, thereby also increasing the opportunity cost of exercising the option to invest. By contrast, since greater risk aversion lowers the inherent payoff of an active power plant, it also reduces the marginal cost of delaying investment , which consists exclusively of stochastic cash flows, by more than the marginal benefit (see [4] for a rigorous proof).

Illustrative Example 7.16

Investment under uncertainty with risk aversion