Abstract

This paper studies the relation between firm managerial capacity in doing innovation and firm profitability. The approach taken is at the intersection of evolutionary/neo-Schumpeterian theory and the resource-based view of the firm. Utilizing a stochastic frontier analysis, we provide a direct measure of the innovation management capacity which is then plugged into a profit margin equation, augmented by the traditional Schumpeterian drivers of profitability. We run both ordinary least squares and quantile regressions.

Results show evidence of an average positive effect of the innovation managerial capacity on firm profitability, although quantile regressions show that this mean effect is mainly driven by the stronger magnitude of the effect for lower quantiles. This means that less profitable firms (i.e. the smaller ones in our sample) could gain more from increasing managerial efficiency for innovation in comparison to more profitable (larger) businesses.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

- Data Envelopment Analysis

- Ordinary Little Square

- Total Factor Productivity

- Innovation Performance

- Quantile Regression

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

1 Introduction

The evolutionary neo-Schumpeterian theory of the firm typically assumes that the competitive performance of businesses depends on a combination of market, innovation and firm-specific factors. Early investigations of relationships in this area took a structure-conduct-performance approach, focusing on traditional Schumpeterian determinants such as market structure, firm size, company R&D and innovation effort.

However, neo-Schumpeterian scholars recognized that firms’ idiosyncratic capacities to master innovation processes could have equally important weight in explaining potentials to achieve relatively better or lesser profit rates, in a given environment. This realization was in part influenced by the management field and by the resource-based theory of competitive advantage. However measuring firm capacity in managing innovation production is far harder than accounting for the role played by “traditional” factors, such as for example sectorial concentration, market power or scale.

The difficulties result from the immaterial and “fuzzy” nature of managerial capacities, which are approximated by variables that seem to give only a poor reckoning of the phenomenon. The problem becomes even trickier if we wish to separate the roles of “general” managerial abilities, concerning the overall management of firm divisions and activities, from the more entrepreneurial capacities specifically involved in managing innovation processes.

Papers such as those by Geroski et~al. (1993) and Cefis and Ciccarelli (2005) have tried to account for the role of managerial capacity when estimating a Schumpeterian profit function, by either incorporating fixed effects (Geroski et~al.), or firm-idiosyncratic elements through Bayesian random-coefficient regression (Cefis and Ceccarelli). Meanwhile, management studies have tried to capture roles in innovation by introducing proxies such as indicators of experience, education, researcher skills and firm managerial skills (Cosh et~al. 2005). As one example, Bughin and Jacques (1994) explored the Schumpeterian links between size, market structure and innovation by controlling for a series of managerial factors generally thought to affect efficiency and success rates in innovation.

The problems with this literature are twofold. First, it fails to explicitly examine the company capacities in managing innovation, and instead looks more at general capabilities. Second, the studies apply only partial and contingent measures of managerial capacity. On the other hand there have been a small number of recent econometric analyses of company innovation performance (Bos et~al. 2011; Gantumur and Stephan 2010) that have derived a direct measure of innovation capability by deconstructing the residual of a production function into a technological and an efficiency component. The residual term is in effect what Mairesse and Mohnen defined as “innovativeness”, in their well-known paper of 2002.Footnote 1

Continuing in this more recent line, in this work we identify a direct measure of innovation-related managerial capacities, to be plugged into a profit function along with traditional Schumpeterian determinants of profitability. The primary research goals for the study are to determine to what extent management’s capacity in mastering the generation of innovations could have a driving effect on profit rates, and if complementarities with traditional factors can be detected (Percival and Cozzarin 2008). We also wish to study the role of managerial capability given situations of different levels of company profitability and/or size.

The next section of the paper presents an in-depth review of the literature. Section 3 sets out a concise explanation of the econometric model used to measure the firm’s capacity in managing innovation. Section 4 presents the dataset, of over 2,000 “innovating” Italian companies, and the variables employed in the estimation stage. Section 5 shows the results of the analysis. First we present the results from a measure of innovation efficiency applying a stochastic frontier regression, which we call the “Innovation efficiency index” (IEI). Next we provide the results from a regression analysis of the operating profit margin (OPM) on IEI, while controlling for other variables. The intent of the analysis is to respond to the research question: “Is innovation management capacity significantly conducive to higher rates of profit, given other profit determinants?” We first use ordinary least squares (OLS) to examine to what extent the Innovation efficiency index is significantly related to the profit rate. Next we use a quantile regression (QR) to see whether the OLS results are sufficiently robust and to detect potential non-uniform patterns of the effect of IEI on OPM.

Section 6 offers a discussion of the results and of several implications for policy, management strategies and for the understanding of Schumpeterian models of competitive advantage.

2 Literature Review

The research concept stems from three strands of literature: (i) the evolutionary and resource-based approach, which offers theoretical and empirical approaches to the characterization of firms and competitive advantage (Nelson and Winter 1982; Dosi 1988); (ii) management literature, which provides empirical exploration of the role of managerial factors in firm innovation propensity and thus firm output; (iii) efficiency-frontier literature, which conceives of gauging managerial competencies in terms of the distance between the actual and the optimal innovation frontier.

2.1 Evolutionary and Resource-Based Literature

Evolutionary theory holds that the main function of the firm is the integration of resources and competencies in teams, for productive services that would not be accessible through market contracts. Following Penrose’s classic (1959) argument, value creation arises from business competencies in combining and using the available resources. The differences in firm behavior create particular traits of greater or lesser competitiveness, with selection advantages reflected in profitability. At the core of this firm capabilities theory are the key concepts of synergy and efficiency. Thus the character of links between the different parts of the firm, or the internal synergy, contributes to innovative capacity. At the same time, given the possibility of increasing returns, there are grounds for searching greater efficiency in the use of the firm’s assets. Nelson and Winter (1982), Winter (2003) and Teece (1984, 1986) are among the authors that explain inter-firm and intra-industry performance variability through an efficiency approach, rather than taking a market-positioning approach. Such studies stress the role and the understanding of firms’ internal features as sources of competitive advantages.Footnote 2

The relationship between market power (firm’s relative size) and efficiency (making the most of available resources) as drivers of business success is a further key issue in the evolutionary perspective. Here the actual concept of innovation is introduced as a cumulative and irreversible learning process regarding the technological path (Malerba and Orsenigo 1990; Pavitt et~al. 1987). This conception implies that the level of accumulated resources and capabilities plays a significant role in determining future innovation efficiency. According to Vossen (1998), large firm strengths are predominantly material, in economies of scale, scope, and financial and technological resources. It is often argued that larger firms permit greater innovation, since they enjoy greater economies of scale and scope than smaller firms (Cohen and Klepper 1996). Small firm strengths are in turn mostly behavioral, as smaller firms are generally more dynamic and flexible and can have closer proximity to the market. You (1995) suggests that efficient firm size is determined by the interaction between economies of scale, stemming from increasing returns to production technology, and diseconomies of scale, stemming from decreasing returns to organizational technology. Thus, although large firms can benefit from technological and learning economies, these may be outweighed by organizational diseconomies of scale (Zenger 1994).

Early research in this field initially focused on the role of the firm’s industrial market in performance variations (Schmalensee 1985), in keeping with the assumption that industry structure drives firm conduct and in turn firm performance (Scherer 1980, p. 4; Tirole 1988). Since then, other research streams have inquired into the role of corporate ownership, or emphasized analysis at the level of business units (Bowman and Helfat 2001; Brush and Bromiley 1997; James 1998; McGahan and Porter 1997, 2002; Rumelt 1991). By far the most consistent result across these studies is that, when estimated over time, the business unit class of analysis explains the most variance in performance (Brush and Bromiley 1997; James 1998; Roquebert et~al. 1996; Rumelt 1991).

A particularly interesting study in this area is by Bughin and Jacques (1994). These authors found that the positive correlation between firm market share and innovation success became significant and more robust across the various dimensions of innovation output, when controls for managerial (in)efficiency were explicitly introduced, and in this way concluded that the Schumpeterian conjecture is not rejected. However “without this normalization, the marginal effect of market share on innovation is biased downward” (Bughin and Jacques 1994, p. 658), meaning that in the specific area of managing their innovation, higher market-share firms are actually less effective, and that “systematic inefficiency is also related to firm size” (p. 658). Thus these scholars conclude that in keeping with Schumpeterian theory, increasing firm size and market share are conducive to innovation, but on the other hand smaller firms have relative “managerial” advantages in innovation activity.

There can also be a bi-directional causality between perfect/imperfect market structures and innovation efficiency. First, because in the presence of market structures showing perfect competition, inefficient firms would be driven out of the market, and second because empirical results have shown that competition has positive effects on innovation efficiency.Footnote 3 Since competition is positively associated with higher scores in management practice, endogeneity bias will lead to underestimation of the importance of competition, as better managed firms are in any case likely to have higher profit margins. It is therefore important to explicitly use indicators of market structure in examining performance functions such as innovation, production or profit.

Based on Penrose’s (1959) resource-based theory and Porter’s (1980, 1985) activity-based approach, the more recent strategic view of the firm investigates the influences on firm strategy both from market structures and from internal resources and capabilities. Such studies attempt to explain the effect of strategy-structure relationships on efficiency. The literature on strategic theory is the first to incorporate a “strategic efficiency” criterion to evaluate competitive advantage. Strategic efficiency refers to the realization of sustainable competitive advantages, as strategic rents of the firm. Depending on the origin of the competitive advantages, different strategic rents can be realized. If the competitive advantage results primarily from monopolistic advantages, as argued by Porter (1980, 1985), the strategic choice depends on the generation of monopolistic rents. If the competitive advantage is primarily based on knowledge advantages due to specific resources, capabilities and competencies, Ricardian and Schumpeterian rents can be realized (Peteraf 1993; Winter 1987).

Ultimately, findings from the empirical literature on the relationship between firm size and efficiency are ambiguous, but there are indications that firm size could be one of the primary sources of heterogeneities in technical efficiency. On the one hand, large firms could be more efficient in production because they use more specialized inputs and are better at coordinating their resources. On the other hand, small firms could be more efficient because they have more flexible, non-hierarchical structures and usually do not suffer from the so-called “agency problem” (Gantumur and Stephan 2010). Size may also have an indirect effect on productivity through other variables, such as resource and capability constraints (Geroski 1998).

2.2 Management Literature

The management literature includes an extensive body of studies on the impact of managerial practices on firm performance, measured in terms of productivity (Huselid 1995; Ichniowski et~al. 1997; Black and Lynch 2001; for a review see Bloom and Van Reenen 2010).

Bloom and Van Reenen (2007, 2010) found that measures of monitoring, target-setting and incentivizing, as assessed via surveys, are strongly associated with productivity and other measures of firm-level performance. The question of whether there is impact from management practices precisely in the area of innovation has received less attention, although several scholars have recently explored the effects from firm organization and employment conditions on propensity to innovate and on actual success in innovation (generally represented by sales of innovative products) (Arvanitis et~al. 2013).Footnote 4 Other scholars have attempted to examine managerial effects on innovation by examining mainly human resources management (HRM) practices, such as employee training, hiring criteria, teamwork, job design and employee hierarchies (Ichniowski and Shaw 2003).

There are many “partial” measures, assessing specific managerial capabilities, within the various studies of general management impact on innovation performance, although these provide very different results. Mookherjee (2006) observes that beyond such descriptive formulations, there is a general lack of theoretical models, and especially of formal models. Hempel and Zwick (2008) investigated the effects of two organizational practices, employee participation and outsourcing, on the likelihood of introduction of product and/or process innovations. They found that while employee participation is positively associated with product and process innovations, outsourcing favors innovations in the short-run, but then reduces performance in the long-run. Zoghi et~al. (2010) analyzed the relationships between innovation and certain organizational practices and incentive schemes in a large sample of Canadian firms with three cross-sections. They found correlation between innovation and the factors under examination, but in many cases this was weak. Many empirical studies find different innovation results according to the type of management practice under examination: Zhou et~al. (2011) for the Netherlands, Cosh et~al. (2012) for UK, Chang et~al. (2012) for Taiwanese firms, Jiang et~al. (2012) for Chinese firms, Koski et~al. (2012) for Finnish manufacturing firms, and Arvanitis et~al. (2013) for Swiss and Greek firms.

Certain management studies have advanced in the direction of applying specific measures of management capability through better use of surveys (Bloom and van Reenen 2010) and the analysis of “clustered” management practices. Laursen and Foss (2003), for instance, used a synthetic index considering a combination of human resources management practices, as revealed by principal component factor analysis, and find that this index is strongly significant in explaining innovation performance. These scholars interpreted this result as evidence of complementarities between HRM practices and innovation. Arvanitis et~al. (2013) find cumulative effects from the use of HRM practices on innovation. From a certain threshold on, the effect on innovation is larger with the firm’s introduction and intensive use of larger numbers of individual HRM practices. However, although both Laursen and Foss (2003) and Arvanitis et~al. (2013) control simultaneously for many different aspects of innovative HRM practices,Footnote 5 several problems still remain, as follows.

-

(i)

Other single managerial practices can impact on innovation performance, and various authors suggest additional ones as determinants of innovation performance. Indeed besides HRM practices, other traditional organizational design variables included in the theory of economics of organizations are sometimes neglected. Examples of overlooked variables include delegation, departmentalization, specialization, and others (Foss 2013). Hence a relevant problem recognized by many scholars working in this field is the possibility of “omitted variable bias”, which would imply inconsistent estimates of the effects. Solutions could lie in the use of fixed-effect regression, or in the indication of a broader set of observable variables.Footnote 6

-

(ii)

A single management capability measure has contingent effect: it can have a positive or a negative effect, depending on the circumstances in which the firm operates. Any coherent theory of management assumes that firms will choose different practices in different environments, so that some element of contingency always arises. As an example, Van Reenen and Bloom (2007) show that firms specialize more in people management (promotion, rewards, hiring and firing) when they are in a more skills-intensive industry. The interesting question is whether practices exist that would be unambiguously better for the majority of firms. The results of the study just cited, in which certain management practices are robustly associated with better firm performance, seem to suggest that this may be the case.

-

(iii)

There is a lack of benchmarks for understanding whether the management factors considered, and their measurement, are examples of good or bad practices. Van Reenen and Bloom (2007) developed a survey tool that in principle could be used to directly quantify management practices across firms, sectors and countries. The fundamental aim of this approach is to measure the firm’s overall managerial quality by benchmarking against a series of global best practices: “These practices are a mixture of things that would always be a good idea (e.g. taking effort and ability into consideration when promoting an employee) and some practices that are now efficient due to changes in the environment” (Bloom and Van Reenen 2010, p. 6). These scholars use an interview-based evaluation tool that defines and scores 18 basic management practices, from one (worst) to five (best practice). This evaluation tool was developed by an international consulting firm to target practices they believed were associated with better performance.Footnote 7 These management practice scores can then be related to firm performance (total factor productivity, profitability, growth rates, and Tobin’s Q and survival rates) as well as firm size. However, as the authors themselves suggest, these correlations should by no means be understood as causal (Bloom and Van Reenen 2010).

2.3 Efficiency-Frontier Literature

A third body of literature, efficiency-frontier studies, states that firm innovation performance is determined not only by hard factors such as R&D employees and investment, but also by factors like management practices and governance structures (Aghion and Tirole 1994; Black and Lynch 2001; Bertrand and Schoar 2003; Cosh et~al. 2005). Many management and organizational factors are found to be correlated with firm propensity to innovate. Bughin and Jacques (1994) found that in particular, synergy among firm departments, together with the effective protection of innovation, were the key factors for successful management of the innovation process. Translated into economic terms, their result means that: “innovation activity by firms may be subject to systematic inefficiencies, i.e. firms do not necessarily operate on their best practice frontier” (Bughin and Jacques 1994, p. 654).

Firm innovativeness can be defined as the ability to turn innovation inputs into innovation outputs. As such it naturally incorporates the concept of “efficiency”, which in turn can be explained by technological factors on the one hand, and firm-specific managerial capabilities on the other hand (Gantumur and Stephan 2010). There are difficulties in measuring firm capabilities because of their complex, structured and multidimensional nature. In typical econometric exercises examining determinants of innovation performance (Mairesse and Mohnen 2002, 2003), the firm’s innovation management efficiency is encompassed within an unobservable regression term. Mairesse and Mohnen (2002) refer to an innovation production function where, similar to the standard production function framework, differences across units (or time periods) are explained by differences (or changes) “in the inputs and in a residual that is known as total factor productivity or simply productivity” (Mairesse and Mohnen 2002, p. 226). This residual incorporates all the omitted determinants of performance, and grasps innovativeness in a loosely-defined sense. Starting from this assumption, a recent paper (Bos et~al. 2011) tested the weight of efficiency as determinant of an innovation production function, but in any case without identifying statistically significant and theoretically based components of such “efficiency”.Footnote 8 The relevance of managerial (in)efficiency implies that measure of innovation inputs in an innovation production function is biased, unless there is an indicator of firm (in)efficiency. If resources are not used effectively, additional investment may be of little support in stimulating the innovation process (Gantumur and Stephan 2010).

Bos et~al. (2011) studied the relationship between R&D inputs and innovative output in a sample of Dutch firms and found that over 63 % of inter-firm variation in the observed innovativeness could be attributed to inefficiency in the innovation process. “In productivity analysis it is quite common to separate (in)efficiency from technological change empirically, using stochastic frontier analysis (SFA)… In the empirical literature on the KPF (knowledge production frontier), however, researchers to date still assume, usually implicitly, that all innovation takes place at the frontier and no waste of R&D inputs occurs” (Bos et~al. 2011, p. 2) These scholars use a stochastic frontier analysis, and keeping the stock of knowledge constant, draw the innovation frontier of a knowledge production function.

In another paper, Bos et~al. (2007) analyzed the relation between innovation output growth and (in)efficiency by a stochastic frontier analysis (SFA) at macro level in 80 countries. The analysis relied on the usual practice adopted in cross-country growth studies, where differences in the efficient use of inputs are computed through a two-stage approach. Cross-country productivity is first retrieved as a residual from a production function estimation, and then regressed against a set of possible determinants of productivity growth. The authors comment that in the presence of inefficiency, total factor productivity indices are biased. SFA overcomes this problem, since it uses a benchmark approach for identifying the technically efficient use of inputs and production technology. Firm optimal behavior is represented by the production frontier, which is the maximum level of output the firm can achieve. The limit of this approach is the assumption of a common current technology for all firms, in all industries and countries, although the authors attempt to accommodate this assumption by accounting for cross-sectional heterogeneity.

Gantumur and Stephan (2010) also estimate an innovation frontier, but at micro level. The authors examine the innovation performance of firms as determined not only by innovation inputs, but also by productivity in innovation and factors affecting this productivity.Footnote 9 These authors noted that only a few papers in the preceding literature had studied innovative efficiency at the firm level by using quantitative approaches. Cosh et~al. (2005) examined the impact of management characteristics and patterns of collaboration on firm innovation efficiency by comparing both data envelopment analysis (DEA) and stochastic frontier analysis (SFA). Zhang et~al. (2003) applied the SFA approach to the R&D efforts of Chinese firms to examine the difference in efficiency among various types of ownership. Hashimoto and Haneda (2008) analyzed R&D efficiency change of Japanese pharmaceutical firms using DEA methodology. These examples are restricted to the estimation of the predicted inefficiency and use a two-stage approach when analyzing the inefficiency determinants.

3 Methodology

Proceeding from the literature review, we adopt a methodological approach based on a stochastic frontier analysis (SFA). For the SFA, the innovation output is the firm “innovative turnover” and the inputs are the innovation effort (specifically the innovation expenditures) and various control variables. Adopting such a model allows us to compute an “Innovation efficiency index” (IEI), defined as the distance between the actual realized innovative output and the potential innovative output, given the inputs of the production function considered.

The assumption behind the approach is that the complement of this difference can be suitably interpreted as the managerial capacity of firms in promoting innovation. When for the same inputs this difference is high, we can conclude that the entrepreneurial ability in combining and exploiting innovation input potential has been poor; on the contrary, when this difference is low, business ability in combining and exploiting input potential has been substantial. Thus, the Innovation efficiency index, calculated as “minus the difference between the actual and the potential innovative output”, can be correctly used to approximate a direct measure of firm’s innovation management capacity.

Once we have this measure in hand, we wish to respond to at least two pertinent questions. First: is innovation managerial capacity significantly conducive to higher rates of profit, given other profit determinants? And then: is this effect uniform over the distribution of the profit rate or is it unevenly spread? The aim of this paper is to shed light on these issues.

In so doing, we assume that firms are subject to the same form of innovation function (Cobb-Douglas)Footnote 10 and share the same type of knowledge inputs, but can operate at different innovation output levels. Other things being equal, firms using the same level of input(s) can produce different innovation output (i.e., innovation turnover), because of the presence of inefficiency in the innovation process. Inefficiency in turn can depend “partly on adequacy of the strategic combinations […] and partly on idiosyncratic capabilities embodied in the various firms” (Dosi et~al. 2006, p. 1110; see also Teece 1986).

For the dataset, we use the third edition of the Eurostat Community Innovation Survey (CIS3) for Italy, merged with firm accounting data. CIS3 provides a broad set of data on firm innovation activity, both quantitative and qualitative, including information on “organizational innovation”. Furthermore both manufacturing and service companies are considered, and the survey reports on a substantial sample size of innovating firms (over 2,000). We use data on various innovative or new organizational practices from CIS3 as determinants of innovation-based managerial efficiency. When possible, inputs and outputs are taken with a delay to attenuate simultaneity.

Our experiment utilizes a two-step approach. In the first step, we estimate the direct measure of innovation-related managerial capacity (the Innovation efficiency index, IEI); in the second, a Schumpeterian profit function including IEI as predictor. To estimate IEI, we use a stochastic frontier analysis approach, starting from the equation:

where y i , x i , η i and ε i represent the innovative turnover, the innovation inputs, the innovation efficiency and an error term for the i-th firm, given an innovation technology f (\( \cdot \)). The term η i , varying between 1 and 0, captures the efficiency of the innovation, that is, the distance from the innovation production function. If η i = 1, the firm is achieving the optimal innovative output with the technology embodied in the production function f (\( \cdot \)). Vice versa, when η i < 1, the firm is not making the most of the inputs x i employed. Because the output is assumed to be strictly positive (i.e., y i > 0), the degree of technical efficiency is also assumed to be strictly positive (i.e., η i > 0).

Taking the natural log of both sides of Eq. (1) yields:

Assuming that there are k inputs and that the production function is linear in logs, and by defining u i = −ln(η i ) we have:

Because u i is subtracted from ln(y i), restricting u i > 0 implies that 0 < η i ≤ 1. Finally, we can assume u i to depend on a series of covariates z i , so that the final form of the model is:

By estimating this equation through maximum likelihood (assuming a normal truncated distribution for u i ) we can then recover the value of η i which represents the IEI, i.e. the firm idiosyncratic score accounting for firm capacity to suitably combine innovation inputs for achievement of innovation output, once all possible elements affecting innovation and efficiency in doing innovation are controlled for (x i and z i ). Thus, we can assume η i as a measure of the firm innovation managerial capacity, to be used as regressor in the second step of this methodology. Here, an operating profit function of the kind:

is estimated via ordinary least squares (OLS) and quantile regression(s) (QRs), to better examine the heterogeneous response of firms to innovation efficiency gains. The set of variables contained in the vector w i includes the determinants of the OPM different from η i (i.e., industrial organization determinants, financial factors, skills and R&D competence, etc.)

4 Dataset, Variables and Descriptive Statistics

As noted, the empirical application for our study draws on the Italian Community Innovation Survey, 3rd edition (1998–2000), containing information on innovation-related variables for 15,279 Italian companies. Information from this source is merged with firm accounting data obtained from the AIDA archives on Italian companiesFootnote 11 maintained by Bureau Van Dijk Electronic Publishing BV. The CIS provides information on the resources for firm innovation activity (inputs and outputs), sources of information and cooperation for innovation, and factors hampering innovation. The third edition of the survey has the advantage of providing, for the first time, a section on “organizational innovation”. We make use of all this information for the reliable construction of array x i , z i and w i , in order to obtain a reliable measure of η i for estimating Eq. (5).

Table 1 presents a brief description of the three sets of variables employed in the estimation of Eqs. (4) and (5). The rationale for the choice of these variables is as follows.

-

1.

The variables included in the array x i represent typical input factors characterizing an innovation production function, i.e. expenditures devoted to fostering innovation. The in-house R&D investment (R&D intra) traditionally represents the major innovation input, accounting for the firm’s direct effort devoted to knowledge production. Expenditures for purchasing R&D services provided by other companies (R&D extra) reflects in turn the amount of external knowledge sources needed for acquiring specific R&D capabilities not existing within the firm. Expenditure for machinery (Machinery) regards the need for fixed capital assets (tangibles), to set up, enlarge and maintain R&D productive capacity over time (i.e., labs, tools, etc.). Expenditure for acquiring technologies (Technology) concerns in turn investments in intangible assets, such as patents or technological licenses, and reflects the need to boost the size of the firm technological portfolio. The number of university-educated employees employed by the firm (Skills), represents a measure of human capital and thus of R&D skills available to the firm. Finally, some control variables are introduced to take into account the form of the company, as independent or part of a group (Group), its experience in doing business (Age), the presence of process innovation (Process), the sector of firm economic activity (Sector), its size (Size) and location (Geo). Note that the expenditures variables are expressed in logs, as a linearized Cobb-Douglas function is employed in the estimation phase.

-

2.

The variables included in the array z i represent factors explaining the company efficiency in doing innovation. The first main input is the total expenditure for innovation (Total innovation spending) and the second is Skills, since it is well recognized that efficiency is strictly linked to human capital. A series of dummies are then included, intended to account for a series of strategic behaviors adopted by companies to increase their capacity in suitably and effectively combining the heterogeneous set of innovation inputs.

-

3.

Finally, variables in z i should explain the main drivers (and controls) of company economic return (profitability). Apart from the auto-regressive components (the Operating profit margin at t-1 and t-2) and the Innovation efficiency, the other factors explaining profitability are: the size of the firm (Turnover), accounting for the potential existence of scale economies; Concentration, accounting for degree of competition and barriers to entry (Paretian rents); R&D per capita, surrogating the knowledge competence of the company; Skill intensity, representing the (relative quota) of human capital (and thus quality of the labor input); Export intensity, referring to the level of company external competition; Indebtedness, accounting for the financing structure of the company (the so-called capital structure); Labor costs, capturing the cost structure of the firm; a set of control dummies (Cooperation, Age, Group, Sector, Size and Geo), including also Patent dummy, signaling the presence of at least one patent application within the firm. This latter regressor should grasp the presence of potential Schumpeterian rents, i.e. rents due to company past innovative performance.

Tables 2 and 3 show some descriptive statistics of the variables noted above for the sample (2,094 units) used in the regression analysis (Sect. 5). Table 2 reports the continuous and binary variables and Table 3 the multi-value ones. From Table 2 it is immediately clear that some variables are very unevenly distributed: Turnover, for instance, has a mean of 39.01 million euros against a median of 9.59, demonstrating a very strong right-asymmetry for this variable, with few companies having a very large size. R&D per-capita and Export intensity are also asymmetrically distributed, while Operating profit margin and Innovation efficiency index are quite symmetric and bell-shaped. Looking at the binary factors (Table 2), we see that 40 % of companies have filed at least one patent, 39 % belong to a group, 20 % do innovation in cooperation, and 65 % have introduced new organizational changes for promoting innovation.

Table 3 sets out some structural characteristics of the sample. Concerning location (Macro regions) we see that the large majority of firms (72 %) are situated in northern Italy (the most developed region), while only around 20 % are situated in central Italy, and 8 % in the south and the islands. For Size, we note that the greatest share (around 45 %) are small companies (10–49 employees) with only a few very large firms (less than 3 %). Finally, the large part of the firms operate in medium-high technological sectors (28 %), and a small number in high-tech ones (13 %).

5 Model Specification and Results

Not every resource (financial, labor or capital assets) spent in R&D produces the same additional innovation. Therefore the final impact on economic performance can be different, as the same R&D inputs, ceteris paribus, can give different innovation output due to different innovativeness.

Firm innovativeness can be defined as the ability to turn innovation inputs into innovation outputs. As such, it incorporates the concept of efficiency, which in turn can be explained by technological factors on the one hand, and managerial capabilities (which are firm specific) on the other (Gantumur and Stephan 2010). Indeed, “The meaning of the term capabilities is ambiguous in the literature, often seeming synonymous with competence, but sometimes also seeming to refer to higher-level routines (Teece and Pisano 1994), that is, to the organization’s ability to apply its existing competences and create new ones” (Langlois 1997, p. 9). The organization’s ability can also be understood as a matter of fit between the environment and the organization as cognitive apparatus (Winter 2003).

As illustrated above, the current study aims at identifying a direct measure of innovation-related managerial capabilities (efficiency), to be inserted into a profit function along with traditional Schumpeterian determinants of profitability. We apply a stochastic frontier analysis (SFA) to innovation production, which permits separation of the technological factor effect on innovativeness, from that due to managerial capability.

Consider Eq. (4): in a world without inefficiency the i-th firm will produce, on average (as the error term has a zero conditional mean), an output equal to f(x i). In the study, this innovative output is explained by some of the typical innovation determinants, which are well established in the literature on economics of innovation [see among others Mairesse and Mohnen (2003)]. These are: R&D inputs, defined as intra-mural and extra-mural R&D expenditures connected to product or process innovations; acquisition of machinery and equipment; acquisition of external technology; human capital (skills); affiliation to a national or foreign group of firms; experience (age of firm); sector, size and localization dummies. We do not introduce the firm’s idiosyncratic stock of knowledge because of poor information on past R&D spending (see description of variables x in Table 1).

The stochastic frontier analysis assumes that firms can be inefficient and produce less than f(x i ) for an average amount equal to u i (z i ). According to Eq. (4), we estimate firm innovation inefficiency as function of: total innovation spending (including all innovation expenditures); organizational innovation, such as the introduction of new strategies, new management tools and new organization solutions; new marketing strategies; new competencies under international property rights protection (IPRs), together with employees’ skills, process innovation and cooperative innovation activity (see the description of variables z in Table 1).

According to Table 4, the estimation of the parameters of the innovation frontier, meaning the f(x i ) in Eq. (2), shows that almost all variables are statistically significant and that the most relevant positive effect is given by employee skills. This means that innovation turnover is highly sensitive to human capital upgrading. Table 4 also sets out the parameters’ estimate of the inefficiency function, i.e., the u i (z i ) in Eq. (2). We find that the elasticity of the inefficiency function in this specification is −0.52. This means that a 10 % increase of total innovation expenditures will on average produce an increase in efficiency (or decrease in inefficiency) of about 5.2 %. It is worth noting that the other variables, although not significant, generally take the expected sign. In particular, the management innovation dummies (except “new business strategies”) all take a negative sign, thus showing that they serve in the direction of reducing inefficiency. The same applies for the dummies of process innovation and IPRs protection capability, while higher labor skills and R&D cooperation present a positive (although again not significant) sign.

In short, it seems that our inefficiency function is not well explained by the organizational/managerial determinants, a finding that remains in keeping with other studies on the subject (e.g. Bos et~al. 2011). However, overall the regression is highly statistically significant (see the Chi-squared at the end of Table 4), thus we can trust the model’s predictions in obtaining firms’ efficiency scores (i.e, the η i ).

Figure 1 plots the distribution of the efficiency scores η i . It shows a higher frequency of firms for values higher than the sample mean (0.51), meaning a relatively larger presence of efficient firms. The distribution shows a fairly evident longer left tail with the median equal to 0.55.

Kernel estimation of the distribution of innovation efficiency scores

Before presenting results on the operating profit margin (OPM) function, we look at its distribution and quantiles plots (see Fig. 2). These illustrate that about 90 % of firms have a positive OPM (in 2000), and that the margins are mainly concentrated between values 0 and 10; finally, 40 % of the sample is located above the OPM mean value, which is around 4.2 %.

Kernel estimation of the distribution and quantiles for operating profit margin (OPM) in 2000

We now turn to examining whether the innovation efficiency, which impacts on innovation output, also has an effect on firm economic performance, by introducing the values of the efficiency scores η i within the operating profit margin (OPM in 2000) regression [in short we estimate Eq. (5)]. We assume that the relation between R&D activities and profit margin, ceteris paribus, is influenced by firms’ managerial capability in innovating (as defined above), and we also introduce various explanatory/control variables for the OPM in order to get an unbiased estimate of the Innovation efficiency coefficient.

First, we estimate Eq. (5) by ordinary least squares (OLS) according to three model specifications: one not including lagged OPM realizations (i.e., the autoregressive component); one including a one-time lag (t-1); and finally, one specifying a two-time lag structure (t-1 and t-2). The other explanatory variables are: industrial structure variables, such as the level of turnover (approximating firm size and demand); industry concentration (at 2-digit sectoral level), to capture market power effects; export intensity, to grasp the type of market in which the firm operates and the level of competitive pressure; firm knowledge production capacity indicators, such as the R&D per-capita expenditures and employee skills; cost variables, such as labor cost and financial capital cost (degree of indebtedness); organizational variables, such as new forms of organization, new marketing methods, presence of cooperation in innovation; patenting activity, leading to potential commercialized innovation and property rights rent. Finally, as usual, we consider some control variables, such as firm age, affiliation to a group, sector, and spatial location in which the firm operates.

The OLS estimations are presented in Table 5. These show that in all three specifications, firm innovation efficiency has a positive effect on firm economic performance, although its marginal contribution to the OPM growth is slightly lower when the autoregressive components are included. The other factors which have a statistically significant impact on OPM in all three model specifications are, in addition to the expected past OPM levels: employee skills; the patent dummy; and, with a negative impact, the cost of financial capital, which has a less relevant marginal impact when firm profit margins at t-1 and t-2 are included.

Thus, at least at this stage, we can conclude that the managerial capacity in producing innovation has a positive effect on company profit rate. Nevertheless, it seems worthwhile to look beyond this average effect, to study the heterogeneous structure of the impact that innovation managerial efficiency has on firm profit margins. To this purpose, we perform a quantile regression (QR) analysis, using the OPM model specification including the profit margin at t-1 (that with the better F-test under OLS).

We run a number of quantile regressions at different quantiles of OPM in 2000 (see Table 6). These reveal that the marginal effect of innovation managerial efficiency is stronger and significant in the first two quantiles considered (10 % and 25 %) compared with higher quantiles (50 %, 75 % and 90 %), where in any case it remains positive and increases in the last quantile, although with no appreciable significance.

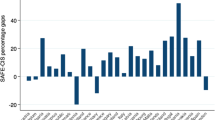

The QR analysis allows graphic inspection of the pattern of marginal effects from the Innovation efficiency index on OPM along all the OPM quantiles. Figure 3 presents the graph. Firstly, we can observe that the innovation efficiency coefficient equals the OLS coefficientFootnote 12 (represented by the horizontal dotted line) around the 20th quantile of the OPM distribution, where the effect is around 1.70. To the left of this point the effect of the innovation efficiency is stronger, even though the observation is with large confidence intervals for very low quantiles. Around the 60th quantile the effect approaches zero, and then again starts increasing for higher quantiles, although with no statistical significance.

Graph of the innovation efficiency index coefficient in quantile regressions: the grey area represents confidence intervals; the horizontal dotted lines refer to the OLS coefficient and its confidence interval (colour figure online)

This graph deepens our understanding regarding the impact of the innovation managerial efficiency on firm profitability. In fact while a positive effect seems to emerge on average, the QR analysis clearly shows that this finding is mainly driven by the relatively higher effect of those firms positioned in the first quantiles (more or less from first to the 30th) of the OPM distribution. Here the effect is remarkably stronger and significant than in larger quantiles. As a consequence, since firms located in lower OPM quantiles are those with a negative or very small OPM, this finding states that the sensitivity of the OPM to a unit increase of innovation efficiency is stronger for firms economically more fragile (i.e., less competitive). This means that firms with relatively lower operating profit margins could experience larger benefits from implementing higher innovation efficiency than more profitable firms would.

Finally, Fig. 4 provides similar graphs for the other covariates. Three of these are interesting for brief comment. First, the profit margin at (t-1) shows an increasing pattern. This means that in the analysis, as firms become more profitable instead of less profitable, the effect of the profit margin at (t-1) increases accordingly. More profitable firms thus are more positively sensitive to past (positive) profits. Second, indebtedness shows a clear decreasing pattern, from positive to negative values. This means that the negative effect of indebtedness is basically driven by the behavior of more profitable firms, which get stronger negative values. The OPM of these firms is very sensitive to increasing debt. Third, OPM is positively sensitive to export intensity, especially for firms located in higher quantiles, meaning firms with a higher OPM. Finally, the other covariates do not seem to show any appreciably clear pattern.

Graphs of different regressors’ quantile regressions coefficients: grey area represents the confidence interval; horizontal dotted lines refer to the OLS coefficient and its confidence interval (colour figure online)

Before concluding this section, it would be interesting to see whether any differences emerge at different company sizes. In this regard, Table 7 displays the effect of innovation efficiency on OPM at different quantiles, by three ranges of firm size. We immediately see that the positive effect found in the pooled regression is significantly driven by the behavior of smaller companies, and especially those characterized by low OPM quantiles. This means that firms that are smaller, and at the same time have poorer OPM performance, are those that could potentially achieve higher benefits from an increase in innovation efficiency. This result fits with the significant negative sign of larger firms at higher quantiles. All in all it seems that as size increases, the role played by innovation efficiency in increasing profitability becomes weaker. This suggests the advisability of policies incorporating specific measures aimed at helping small companies to increase their innovative efficiency, and through this their profitability and potential growth.

6 Conclusions

The paper proves that managerial efficiency in mastering innovation is, on average, an important driver of firm innovative performance and market success, and that it complements traditional Schumpeterian determinants, such as market concentration. We have moved further along the theoretical-empirical trajectory laid out by Nelson and Winter (1982), and the resource-based view of the firm developed by strategic management literature, in proposing a direct measure of firm managerial capacity in implementing innovative products and activities.

The study has tested the significance of this direct measure of managerial capacity in a profit margin equation, augmented by the traditional competitive structural factors (demand, market concentration) and other control variables. It analyzes the role played by “innovation management efficiency” in fostering profitability, by means of an ordinary least squares and a series of quantile regressions. The model thus better clarifies the role played by companies’ heterogeneous response to innovation management capacity, at different points of the distribution of the operating profit margin.

We have found evidence of an average positive effect from management efficiency, although quantiles regressions have shown that this average effect is mainly driven by a stronger magnitude of the effect for lower quantiles (i.e., for firms having negative or low-positive profitability). This means that weaker firms (in our sample those of smaller size) could profit more from an increase of managerial efficiency in doing innovation than more profitable businesses (in our sample, the larger ones).

Finally, our findings seem to suggest that the three main pillars explaining Schumpeterian comparative advantages, specifically efficiency, market concentration and skills, have different strength over the various profit margin quantiles, that is over different firm size. Higher efficiency is more relevant for small firms, market concentration is more relevant for medium firms, and human resources competencies are more relevant for larger companies.

Notes

- 1.

“Innovativeness is to innovation what TFP (Total Factor Productivity) is to production. […] Both correspond to omitted factors of performance such as technological, organizational, cultural, or environmental factors (and to other sources of misspecification errors), although TFP is commonly interpreted as being mainly an indicator of technology” (Mairesse and Mohnen 2002, p. 226).

- 2.

An important evolution of the firm capability theory deals with dynamic capabilities. Teece (1987, p. 516) define firm dynamic capabilities as the ability to integrate and reconfigure internal and external competences/resources. These capabilities are what matters also in the case of R&D collaboration and joint ventures.

- 3.

Over time, low productivity firms are selected out and the better ones survive and prosper. But in the steady state there will always be some dispersion of productivity, as cost factors limit the number of new firms that enter the market (Bloom and van Reenen 2010).

- 4.

These scholars reported that, overall, variables representing workplace organization show highly significant positive associations with innovation propensity, and that some of them seem to be more important than other “standard” determinants of innovation, such as demand development, competition conditions or human capital assets.

- 5.

They control the impact on: (a) the firm’s innovation propensity (whether or not a firm has introduced innovations in a certain period), and (b) innovation success as measured by the firm’s innovative product sales in relation to total turnover.

- 6.

Another problem indicated by Arvanitis et~al. (2013) is reverse causality: innovative firms could in turn be more likely to adopt innovative organizational practices.

- 7.

One way to summarize firm-specific quality is to z-score each individual question and take an average across all 18 questions. Another is to take the principal factor component. This in fact provides extremely similar results to the average z-score, since they are correlated (see Van Reenen and Bloom 2007).

- 8.

Other scholars have used data envelopment analysis (DEA) to estimate the innovation frontier. Zhang et~al. (2003) and Coelli and Rao (2005) provide a discussion of the differences between DEA and stochastic frontier analysis (SFA). Kumbhakar and Lovell (2000) give an elaborate discussion of the development and application of SFA to efficiency measurement.

- 9.

The general aim of their paper is to examine at micro level the impact of external technology acquisition on the achievement of innovative efficiency and productivity, i.e. on a firm’s innovation performance.

- 10.

For the sake of simplicity we do not assume other forms of the production function (e.g., the translog), or that the Cobb-Douglas regression coefficients vary across sectors.

- 11.

AIDA: Information Analysis of Italian Companies.

- 12.

References

Aghion P, Tirole J (1994) The management of innovation. Q J Econ 109(4):1185–1209

Arvanitis S, Seliger F, Stucki T (2013) The relative importance of human resource management practices for a firm’s innovation performance, KOF Working Papers, N. 341, September

Bertrand M, Schoar A (2003) Managing with style: the effect of managers on firm policies. Q J Econ 118(4):1169–1208

Black SE, Lynch LM (2001) How to compete: the impact of workplace practices and information technology on productivity. Rev Econ Stat 83(3):434–445

Bloom N, Van Reenen J (2010) Why do management practices differ across firms and countries? J Econ Perspect 24(1):203–224

Bos J, Economidou C, Keotter M, Kolari J (2007) Do technology and efficiency differences determine productivity. Discussion paper series 07–14, Utrecht School of Economics, Utrecht University

Bos JWB, van Lamoen RCR, Sanders MWJL (2011) Producing innovations: determinants of innovativity and efficiency, preprint submitted to J Econ Growth

Bowman EH, Helfat CE (2001) Does corporate strategy matter? Strateg Manag J 22(1):1–23

Brush TH, Bromiley P (1997) What does a small corporate effect mean? A variance components simulation of corporate and business effects. Strateg Manag J 18(10):825–835

Bughin J, Jacques JM (1994) Managerial efficiency and the Schumpeterian link between size, market structure and innovation revisited. Res Policy 23(6):653–659

Cefis E, Ciccarelli M (2005) Profit differentials and innovation. Econ Innov New Technol 14(1–2):43–61

Chang YC, Chang HT, Chi HR, Chen MH, Deng LL (2012) How do established firms improve radical innovation performance? The organizational capabilities view. Technovation 32: 441–451

Coelli TJ, Rao DS (2005) Total factor productivity growth in agriculture: a Malmquist index analysis of 93 countries, 1980–2000. Agric Econ 32:115–134

Cohen W, Klepper S (1996) Firm size and the nature of innovation within industries: the case of process and product R&D. Rev Econ Stat 78:232–243

Cosh A, Fu X, Hughes A (2005) Management characteristics, collaboration and innovative efficiency: evidence from UK survey. Data Centre for Business Research, University of Cambridge Working Paper No. 311

Cosh A, Fu X, Hughes A (2012) Organization structure and innovation performance in different environments. Small Bus Econ 39:301–317

Dosi G (1988) Sources, procedures, and microeconomic effects of innovation. J Econ Lit 26(3):1120–1171

Dosi G, Marengo L, Pasquali C (2006) How much should society fuel the greed of innovators? On the relations between appropriability, opportunities and rates of innovation. Res Policy 35:1110–1121

Foss N (2013) Reflections on the explanation of heterogeneous firm capabilities. http://www.organizationsandmarkets.com/category/theory-of-the-firm/, last consulted 02/05/2014

Gantumur T, Stephan A (2010) Do external technology acquisitions matter for innovative efficiency and productivity? DIW Berlin Discussion Papers, 1035

Geroski PA (1998) An applied econometrician’s view of large company performance. Rev Ind Organ 13:271–293

Geroski P, Machin S, Van Reenen J (1993) The profitability of innovating firms. RAND J Econ 24(2):198–211

Hashimoto A, Haneda S (2008) Measuring the change in R&D efficiency of the Japanese pharmaceutical industry. Res Policy 37:1829–1836

Hempel T, Zwick T (2008) New technology, work organization, and innovation. Econ Innov New Technol 17(4):331–354

Huselid MA (1995) The impact of human resource management practices on turnover, productivity, and corporate financial performance. Acad Manag J 38(3):635–872

Ichniowski C, Shaw K (2003) Beyond incentive pay: insiders’ estimates of the value of complementary human resource management practices. J Econ Perspect 17(1):155–180

Ichniowski C, Shaw K, Prennushi G (1997) The effects of human resource management practices on productivity: a study of steel finishing lines. Am Econ Rev 87(3):291–313

James CR (1998) In search of firm effects: are managerial choice and organizational learning sources of competitive advantage? Paper presented at the strategic management society meetings, Fall 1997

Jiang J, Wang S, Zhao S (2012) Does HRM facilitate employee creativity and organizational innovation? A study of Chinese firms. Int J Hum Resour Manag 23(19):4025–4047

Koski H, Marengo L, Mäkinen I (2012) Firm size, managerial practices and innovativeness: some evidence from Finnish manufacturing. Int J Technol Manag 59(1/2):92–115

Kumbhakar SC, Lovell CAK (2000) Stochastic frontier analysis. Cambridge University Press, UK

Langlois R (1997) Cognition and capabilities: opportunities seized and missed in the history of the computer industry. In: Garud R, Nayyar P, Shapira Z (eds) Technological entrepreneurship: oversights and foresights. Cambridge University Press, New York, NY

Laursen K, Foss NF (2003) New human resource management practices, complementarities and the impact on innovation performance. Camb J Econ 27:243–263

Mairesse J, Mohnen P (2002) Accounting for innovation and measuring innovativeness: an illustrative framework and an application. Am Econ Rev Pap Proc 92(2):26–230

Mairesse J, Mohnen P (2003) R&D and productivity: a reexamination in light of the innovation surveys. Paper presented at the DRUID summer conference 2003 on creating, sharing and transferring knowledge, Copenhagen, 12–14 June

Malerba F, Orsenigo L (1990) Technological regimes and patterns of innovation: a theoretical and empirical investigation of the Italian case. In: Heertje A, Perlman M (eds) Evolving technology and market structure. Michigan University Press, Ann Arbor, MI, pp 283–306

McGahan AM, Porter ME (1997) How much does industry matter, really? Strateg Manag J 18(Summer Special Issue):15

McGahan AM, Porter ME (2002) What do we know about variance in accounting profitability? Manag Sci 48:834–851

Mookherjee D (2006) Decentralization, hierarchies, and incentives: a mechanism design perspective. J Econ Lit 44(2):367–390

Nelson RR, Winter S (1982) An evolutionary theory of economic change. Harvard University Press, Cambridge, MA

Pavitt K, Robson M, Townsend J (1987) The size distribution of innovating firms in the UK: 1945–1983. J Ind Econ 35(3):297–316

Penrose ET (1959) Theory of the growth of the firm. Wiley, New York, NY

Percival JC, Cozzarin BP (2008) Complementarities affecting the returns to innovation. Ind Innov 15(4):371–392

Peteraf M (1993) The cornerstones of competitive advantage: a resource-based view. Strateg Manag J 14:179–191

Porter ME (1980) Competitive strategy: techniques for analyzing industries and competitors. Free Press, New York, NY

Porter ME (1985) Competitive advantage: creating and sustaining superior performance. Free Press, New York, NY

Roquebert JA, Phillips RL, Westfall PA (1996) Markets vs. management: what ‘drives’ profitability? Strateg Manag J 17(8):633–664

Rumelt RP (1991) How much does industry matter? Strateg Manag J 12(3):167–185

Scherer FM (1980) Industrial market structure and economic performance. Houghton Mifflin, Boston, MA

Schmalensee R (1985) Do markets differ much? Am Econ Rev 75:341–351

Teece DJ (1984) Economic analysis and strategic management. Calif Manag Rev 26(3):87–110

Teece D (1986) Profiting from technological innovation: implications for integration, collaboration, licensing and public policy. Res Policy 15:285–305

Teece DJ (ed) (1987) The competitive challenge: strategies for industrial innovation and renewal. Harvard University Press, Cambridge, MA

Teece DJ, Pisano G (1994) The dynamic capabilities of firms: an introduction. Ind Corp Chang 3(3):537–556

Tirole J (1988) The theory of industrial organization. MIT, Cambridge, MA

Van Reenen J, Bloom N (2007) Measuring and explaining management practices across firms and countries. Q J Econ 122(4):1351–1408

Vossen RW (1998) Relative strengths and weaknesses of small firms in innovation. Int Small Bus J 16(3):88–95

Winter S (1987) Knowledge and competence as strategic assets. In: Teece DJ (ed) The competitive challenge: strategies for industrial innovation and renewal. Harvard University Press, Cambridge, MA, pp 159–184

Winter SG (2003) Understanding dynamic capabilities. Strateg Manag J 24(10):991–995

You JI (1995) Critical survey: small firms in economic theory. Camb J Econ 19:441–462

Zenger T (1994) Explaining organizational diseconomies of scale in R&D: agency problems and the allocation of engineering talent, ideas, and effort by firm size. Manag Sci 40:708–729

Zhang A, Zhang Y, Zhao R (2003) A study on the R&D efficiency and productivity of Chinese firms. J Comp Econ 31:444–464

Zhou H, Dekker R, Kleinknecht A (2011) Flexible labor and innovation performance: evidence from longitudinal firm-level data. Ind Corp Chang 20(3):941–968

Zoghi C, Mohr RD, Meyer PB (2010) Workplace organization and innovation. Can J Econ 43(2):622–639

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2015 Springer International Publishing Switzerland

About this chapter

Cite this chapter

Cerulli, G., Potì, B. (2015). The Role of Management Capacity in the Innovation Process for Firm Profitability. In: Pyka, A., Foster, J. (eds) The Evolution of Economic and Innovation Systems. Economic Complexity and Evolution. Springer, Cham. https://doi.org/10.1007/978-3-319-13299-0_19

Download citation

DOI: https://doi.org/10.1007/978-3-319-13299-0_19

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-319-13298-3

Online ISBN: 978-3-319-13299-0

eBook Packages: Business and EconomicsEconomics and Finance (R0)