Abstract

The aim of this chapter is to investigate the impact of potential Systemic Bank Mergers and Acquisitions (M&As) in Greece on the competitiveness of the country’s banking system. The subject is highly topical nowadays given the various reports circulating in financial news sources regarding upcoming mergers between systemic banks in Greece. The period under investigation includes the decade 2008–2018, which covers the pre-crisis period and spans the crisis period in Greece, which started as a sovereign debt crisis, which affected also the banking sector. In our analysis, we apply the Lerner index to estimate the impact of each potential merger on the concentration of the Greek banking sector, and then we classify the M&As according to the Herfindahl-Hirschman and the Bank Z indices. We find that concentration has no significant impact on stability, while competition relates marginally significantly and positively to stability. Furthermore, according to the GMM estimators, there is no evidence of a significant correlation between the two indices. Finally, we apply a third model, in which a square term represents competition, to test the presence of non-linearity. The findings of our study contribute to the theory of effective structure demonstrating that an increase in concentration, because of M&As, does not affect market power and bank stability, whereas by focusing on effective management, operational costs and non-performing loans are very likely to increase ban stability.

Access provided by Autonomous University of Puebla. Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

The financial crisis, which originated in the USA (2007) and spread to other countries, also affected Greece. In 2010, Greece sought bailout funding and signed an M0U with the so-called Troika, that is, the EU the ECB and the IMF. However, although the Greek crisis started as a sovereign debt crisis, it soon turned into a banking crisis, as banks were the main holders of Greek bonds.

On the other hand, liberalization allowed banks to undertake excessive risks, which played a significant role in the global financial crisis of 2007 and, to some extent, in the Greek financial crisis of 2010 [1, 2]. As a result, regulators started to reconsider their decisions emphasizing on the stability of the banking system. This new environment led researchers to turn their interests to topics such as (i) Concentration-Competition, (ii) Concentration-Stability and (iii) Competition-Stability.

2 Literature Review

The existing literature does not lead to clear results in terms of the relationships among market concentration, market power and the financial stability of the banking system. In fact, even empirical studies fail to make safe conclusions as to what is ultimately valid. This ambiguity is evident in the available literature as we demonstrate in the following section.

2.1 Concentration-Competition

The existing literature mainly researches the relationship between competition and concentration. There are two prevalent views on the relationship between these two components.

The first view is based on the Structure-Conduct-Performance relationship [3, 4], according to which increasing concentration will have a positive impact on the increasing market power of large banks (and a negative impact on competition in the banking industry); taking advantage of the increase in their market share and/or the eradication of their competitors, banks can more easily impose higher prices and record (abnormally) higher profits. On the other hand, the second relation is based on the effective structure Hypothesis [5, 6], which suggests that most efficient banks can increase their profitability and size, simultaneously increasing their concentration. Therefore, an increase in this concentration does not imply market power, which means that there is, not necessarily, a causal relationship between concentration and competition in the banking sector.

However, other studies have concluded that there is no significant relationship between concentration and competition [7,8,9,10,11,12].

2.2 Concentration-Stability

The first view emerging in the existing literature is that increasing concentration under certain conditions has a positive impact on the sector’s stability. Such results can be found in cases of M&As occurring in the context of restructuring required of the sector (e.g., the acquisition of the ‘Agricultural Bank of Greece’ by ‘Piraeus Bank’ and the acquisition of the ‘Emporiki Bank of Greece’ by ‘Alpha Bank’). The increasing degree of concentration led to an improved stability within the sector [2, 13].

This view holds that stability in the industry improves when the degree of concentration within the industry increases, whether this is due to new M&As or comes because of an increase in the market share of the bigger banks.

Other studies conclude that it is easier to monitor a system with a few big banks rather than one where many small banks operate, and therefore, more detailed and systematic monitoring is required.

The proponents of this view support that in the most concentrated markets, individual banks can charge higher interest rates for loans, which increases the likelihood of moral hazard as borrowers make risky decisions, and, as a result, banking portfolios become riskier, too [14].

In a more recent study, Shim (2019) [15] shows that high concentration leads to a more stable financial environment compared with less concentrated markets, whereas Azmi et al. (2019) [16] also argue that concentration is beneficial for banking stability, focusing on dual banking economies.

2.3 Competition-Stability

Perhaps the more intensely studied relationship is the relationship between Competition and Stability. It all began in the 1990s, when there was a tendency to reduce restrictions on the banking sector to obtain the benefits an increased level of competition might offer. These tactics following deregulation are also the main reason leading to the 2007 crisis [17, 18]. Thus, the study of the Competition-Stability relationship was considered by experts as a major issue.

As in the relationships discussed above, opinions in the literature differ. The two main relationships under discussion are Competition-Stability and Competition-Fragility.

Big banks were considered ‘too big to fail’ having a ‘safety net’ provided by the state can engage in activities with greater risk. In more competitive markets, interest rates are lower and the ‘too big to fail’ and ‘safety net’ parameters are of lesser importance. Thus, the moral hazard problem is mitigated, and we are led to stability [14].

In addition to the aforementioned studies that focused on the impact of concepts like concentration and competition on the stability of the financial system, researchers also studied the aftermath of the unconventional monetary policies that central banks applied as remediation measures regarding the recent economic crises [19,20,21,22]. The effect of the unconventional monetary policies by Central Banks in general is positive for the real economy [23, 24].

According to Acharya et al. (2019) [25], the ECB’s Outright Monetary Transactions program indirectly recapitalized European banks through its positive impact on periphery sovereign bonds. Kenourgios, D., Christopoulos, A., and Dimitriou, D. (2013) [26] examined the returns on stocks, bonds, commodities, shipping, foreign exchange and real estate and found evidence of a correlated-information channel as a contagion mechanism between markets within different countries.

Yu (2017) [27] and Keddada and Schalckb (2020) [28] found that the correlation between sovereign and bank CDS spreads before the crisis remained small but had increased significantly until the end of the sample. Similarly, attempted to determine the extent to which European banks were vulnerable to sovereign credit risk from 2010 to 2013.

Thus, we conclude that for each case concerning a country, industry, system, or whether carried out for a different time-period, new research should be conducted to draw conclusions that are most likely to be valid for each case.

3 Data and Methodology

3.1 Data

The data in this research came from published consolidated financial statements, and specifically the balance sheets and profit and loss statements of the five largest banking groups in Greece for the period 2008–2018. Although only these five banks were included, our sample represents 97% of the industry’s total assets. Considering country-level data, these were collected from the databases of the World Bank and the European Central Bank.

The Herfindahl-Hirschman Index as a measure of concentration

The Herfindahl-Hirschman index (HHI) is one of the most widely used indicators in the theoretical literature. It can often be used as a benchmark to assess other concentration indicators. This indicator is the sum of the squares of bank shares as shown in the following formula:

where Si is the market share of the bank, and i and n are the number of enterprises in the sector. This indicator can take values from 1/n (HHI = n(1/n)2 = 1/n) where all banks are of equal size, and we have an indication of full competition up to10000 (HHI = 1002), when a bank has 100% of the shares and so we have an indication of a monopoly.

According to ECB ‘s instructions, market shares are calculated using the total assets.

The Lerner index as a measure of competition

This study uses the Lerner index, which has been commonly used in banking research, as a measure of competition (or market power). The Lerner index captures the capacity of price power by computing the disparity between price and marginal cost as a percentage of the price and ranges between 0 and 1. In case of perfect competition and monopoly, the index equals 0 and 1, respectively. The time-variant Lerner index at the bank-level is calculated as follows:

where the pit is the price of total assets proxied by the ratio of total revenues (interest and non-interest income) to total assets for bank i at time t. mcit is the marginal cost for bank s at time t.

The marginal costs are obtained by differentiating a translog cost function with respect to one output. We use a stochastic frontier model to estimate a translog cost function with one output (total assets) and three inputs (labour, funding and physical capital). The cost function for a given bank s at time t can be specified as follows:

where C is the total costs, Q is the output (total assets) and W is a vector of input prices (price of labour, price of funds and price of physical capital), v represents standard statistical noise and u captures inefficiency. Following Turk-Ariss (2010) [29], the total costs and prices of funds and labour are scaled by the price of physical capital to correct for heteroscedasticity and scale biases.

To obtain the marginal cost, Eq. (1) is differentiated with respect to Q:

The Bank Z Score as a measure of bank stability

The Z-score is a widely used measure of bank stability in the related literature and can be interpreted as the number of standard deviations by which returns would have to fall from the mean to deplete the equity capital. Hence, it determines how many standard deviations in return on assets a bank is from insolvency. The score is computed as follows:

where ROA is the return on assets, E/TA represents the equity to total assets ratio and σ(ROA) denotes the standard deviation of return on assets. A higher Z-score implies a lower probability of insolvency (failure), providing a more direct measure of soundness compared to other measures of risk.

3.2 Control Variables

In our econometric models apart from the basic variables, we use a list of bank-specific and macroeconomic control variables.

In this section, we present each one of them with its definition and divided according to the relationship studied.

Table 3 reports the descriptive statistics of the variables used in the regression. Taking a glance at the basic variables (Lerner, HHI, LnBank Z score), we can make a first assumption of the results we might find for the three relationships of this study. The mean value, as well as the median of the Lerner index, is relatively low and quite close to zero, while, on the other hand, the ones of the HHI index and LnBank Z score have higher values. So, this could be a first sign that there might be a negative relationship between Market Power and Concentration, as well as Stability, while there might be a positive between Concentration and Stability.

3.3 Methodology

Before the econometric study, using the HHI index and its yearly change ΔΗΗΙ, an analysis on the level of Concentration of the Greek Banking industry is carried out and subsequently we estimate, using the same indices, the change in the sector’s Concentration the possible systemic banks merger scenarios might cause.

Then we proceed to the basic econometric study. Our first model has the form:

where COMPit is the dependent variable for competitiveness approached through the Lerner index for bank i and year t; COMPit−1 is the first lag of the Lerner index and is used to examine not only the importance of whether we should consider the previous values of the dependent variable but also the factor a1, which represents the rate at which competitiveness converges at a future level; and CONCit is the concentration variable that is approached through the HHI index. The rest are as described in Table 1 and εit is the error term.

In the second analysis, we calculate two models, where in the first, we consider a linear relationship between competition and stability. In the third model, based on the research of Berger et al. (2009) [31], we add the square term of competition to test for non-linear relationships between Competition and Stability [32].

where RISKit is the dependent variable for stability for Bank I and year t and is proxied by the Bank Z score index’s natural logarithm; RISKit−1 is the lag of the stability variable and, as previously, is used to examine not only the importance of whether we should consider the previous values of the dependent variable but also the factor a1, which represents the rate at which stability converges at a future level; and COMPit, as before, for competition with the Lerner index, but, in addition, here, based on Berger et al. (2009) [31] and Jimenez et al. (2013) [33], we also use a square term for the competition measure to capture a possible non-linear relationship between competition and risk with COMPit2 in Eq. (4). CONCt again is for concentration with the HHI index; the rest are as described in Table 2, and finally eit is the error term.

The two models used in this survey are calculated based on the generalized method of moments (GMM) to solve any endogenous problems that may arise. In the first case, the model used is based on the one used in the research by Carbo and Rodriguez-Fernandez (2007) [7], where we examine the relationship between Concentration and Competitiveness, and the second on models of Kasman and Kasman (2015) [34] and Fu et al. (2014) [35] to study the relationship between Concentration and Competitiveness with Stability. In both models, we used panel data from the five banks and the Greek Banking system for the period 2008–2018, which was also the most critical for the industry in Greece. Variables for stationarity reasons are at first difference. To address correlation and possible endogenous problems, Arellano and Bond (1991) [36] propose the use of the lags of the explanatory variables as instruments (Table 3).

4 Empirical Results

4.1 Merger Scenarios

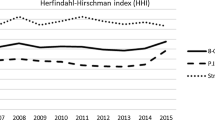

In this section, we present the level of Bank Concentration in Greece as well as its yearly change measured by the HHI and ΔΗΗΙ indices, respectively, for the period 2004–2018.

Table 4 shows that up to 2012 the HHI index in column 4 is below the limit of HHI > 2000 set by the ECB. However, in 2012, the change in the index as seen in column 5 comes quite close to the limit of ΔΗΗΙ > 150, due to the forced acquisitions that followed the debt crisis in that period. In 2013, however, we see that the index combined with its change (ΔΗΗΙ) far exceeds the limits. The fact that regulators allowed these acquisitions is because they were used as a measure to restore stability for the Greek banks, instead of injecting further capital coming from Greek taxpayers [2, 13]. So, we see that this index acts more as a guideline and is combined with other factors characterizing its situation, by regulators, to allow or not a M&A deal.

Over the next few years, mergers and acquisitions did not cause any significant change in the index, but the previous events had already raised the index to very high levels, causing the sector to be considered very concentrated, even though we cannot be certain at this time if this result is mostly negative. Next, based on the HHI index, we test the possible merger scenarios for the year 2019 for the four systemic banks in Greece representing more than 90% (EBF, 2020) of the sector’s market share.

As we can see from Table 5, the results for each merger go far beyond the limits set by the ECB, i.e., H > 2000 in conjunction with ΔΗΗI > 150. Thus, based on this indicator and the limits set, we can conclude that for reasons of creating a monopoly, or price cartel conditions, none of the above scenarios can be realized. However, as mentioned, this index and its yearly change act as guidelines. So, if the sector needs to be further consolidated (as recently stated by the ECB), due to the benefits of integration within EU banking, those other factors might play a much more important role than the index and foster M&As of systemic banks. If this is the case and the merger scenarios illustrated in Table 4 could be realized, based only on the above results, we can propose that the most preferable ones are those of Alpha Bank – Eurobank and Piraeus Bank – Eurobank, as they raise the overall sector’s Concentration index less, compared to the other scenarios. This is a sign that they are less probable to create a monopoly in the Greek sector, with whatever drawbacks this situation might cause.

5 Econometric Models

In our econometric study, we examine separately the relationships of Concentration-Competition (Market Power) and Concentration and Competition-Stability based on the models mentioned in Sect. 3.

5.1 Concentration-Competition

We estimating model (2) using the GMM, considering the HHI index as the basic variable. The results are summarized in Table 6:

As we see above the variable HHI is not significant to our model. This leads us to rule in favor of the theory of effective structure as it is more possible to explain the competitive conditions within the Greek banking industry. These results agree with the ones found by Claessens and Laeven (2004) [8], Casu and Girardone (2006) [9], Carbo and Rodriguez-Fernandez (2007) [7], Yeyati and Micco (2007) [10], Efthyvoulou and Yildirim (2014) [11], and Rakshit and Bardhan (2019) [12].

On the other hand, we have control variables that are significant to the model. Initially, we see the paradox that there is a positive relationship with the ‘Provisions for Losses’ from ‘Loans to Total Assets’, whereas we would expect there to be a negative relationship with market power.

Another variable is inefficient. As we see, it has a negative relationship, which seems perfectly reasonable. As banks do not enjoy market power, this negative element may affect the dependent variable this way.

The ‘Fee Based Activities’ variable is also negative. In this case, it makes sense as the more banks specialize in their primary activities, the more they will gain a competitive advantage, since they become more efficient and consequently gain more market power.

Finally, the only other important variable is the ‘lag of the dependent’. This states the importance of considering previous index values. But the fact that it is negative shows us that the previous results affect the index in reverse, which means that we will have constant ups and downs.

5.2 Concentration-Competition-Stability

In the second analysis, we consider the effect of two variables on stability. For the first, we consider the relationship between competition and stability, and for the second, the effect of concentration. Using again a GMM estimation on model (3) and having as basic explanatory variables, the Lerner and HHI indices, we gain the following results (Table 7):

For the first basic variable, the Lerner index, we see that it has a marginal significance to our model. Nonetheless, in our investigation, we accept it to extract conclusions. Thus, we see that it has a positive relationship with the stability index. This makes us lean toward the Competition-Fragility view (consistent with, among others: Yeyati & Micco, 2007 [10], Turk-Ariss, 2010 [29], Leroy & Lucotte, 2017 [37]). This means that the increase in the market power of banks (within reasonable limits) is expected to bring greater stability.

The second variable is HHI. For this variable, we see that it is not significant to the model. Therefore, we find no relation with Stability. As a result, we cannot rule in favor of any of the views Concentration-Stability, or fragility, for which we have not found similar results in the literature.

Of the control variables that are important, initially, GDP’s annual growth rate is positively related to the stability variable. The next expected result is the negative relationship of the ‘Provisions for Loan Losses’ to ‘Total Assets’ with Stability. However, the unexpected result for which we have not been able to provide a satisfactory explanation is the positive relationship between the indicative variable ‘CRISIS’ and Stability.

The last significant variable positively affecting stability is the amount of capital requirements.

For a robustness test following Jimenez et al. (2013) [33] and Fu et al. (2014) [35], we also use a quadratic term of the measure of competition, to capture a possible non-linear relationship between competition and risk, as illustrated in model (4). The results are as follows (Table 8):

Because both the Lerner index and its square are not important to the model, we can deduct that the Competition-Stability relationship is linear, which is in line with previous studies including the quadratic term but supporting the linearity.

6 Conclusions

This chapter examined the impact of Systemic Greek Bank M&A on the financial sector’s major concepts: Concentration, Competition and Stability, as the subject is highly topical these days given the various reports circulating in financial news sources regarding upcoming systemic bank mergers in Greece.

For this purpose, we tested the relationships of Concentration-Competition, Concentration-Stability and Competition-Stability.

Thus, as a final view, based on our results, it could be said that while a merger between two Greek systemic banks seems, at first sight, dissuasive, on the contrary, it can have positive effects on the stability of the system.

For the Greek economy, these results mean that measures such as forced mergers and acquisitions to save the banks, and consequently the system, constitute a positive development. As we have observed from our results, the increase in concentration following mergers and acquisitions did not have any major negative impact on the stability and did not lead to the sector becoming a monopoly; on the contrary, the results of these moves by the banks helped reverse the situation and save the banking system. Opposite results would have resulted in bankruptcy for the banks, and consequently the collapse of the economy, as the system’s overall money flow relies on the banks. Also, our results cannot explain extreme situations of concentration and competition, but the conclusions are made based on values given to the variables not far exceeding our sample.

Our last limitation concerned our models. The variables within our models were based on previous ones presented in similar studies dependent on a previously developed theoretical framework. Even though the variables used in our model emerged from a thorough study of the existing literature and might not be the optimal ones to test the pertinent relationships without the shadow of a doubt, testing every possible variable for suitability is rather impractical. As a result, we relied on those variables that are most probable and most appropriate for the research conducted.

Closing this chapter, we shall refer to possible expansions of this research. One relevant expansion might be the inclusion of the Covid-19 crisis in the sample, testing dynamically by modeling and simulating the sample [38,39,40,41,42]. Whether M&A are moves that banks or other kind of businesses might use to gain positive results and cover their losses. Finally, another future research development might be to examine other advantages that mergers and acquisitions might bring considering where most synergies are coming from.

References

Ozturk, S., Sozdemir, A.: Effects of global financial crisis on Greece economy. Proc. Econ. Financ. 23, 568–575 (2015)

Provopoulos, G.: The Greek economy and banking system: recent developments and the way forward. J. Macroecon. 39, 240–249 (2014)

Mason, E.S.: Price and production policies of large-scale enterprise. Am. Econ. Rev. 29, 61–74 (1939)

Bain, J.S.: Relation of profit rate to industry concentration. Q. J. Econ. 65, 293–324 (1951)

Demsetz, H.: Industry structure, market rivalry, and public policy. J. Law Econ. 16(1), 1–9 (1973)

Peltzman, S.: The gains and losses from industrial concentration. J. Law Econ. 20, 229–263 (1977)

Carbó, V.C., Rodríguez, Fernández, F.: The determinants of bank margins in European banking. J. Bank. Financ. 31, 2043–2063 (2007)

Claessens, S., Laeven, L.: What drives bank competition? some international evidence. J. Money Credit Bank. 36(3), June part 2, 563–June part 2, 583 (2004)

Casu, B., Girardone, C.: Bank competition, concentration and efficiency in the single European market. Manchester School. 74(4), 441–468 (2006)

Yeyati, E.L., Micco, A.: Concentration and foreign penetration in Latin American banking sectors: impact on competition and risk. J. Bank. Financ. 31, 1633–1647 (2007)

Efthyvoulou, G., Yildirim, C.: Market power in CEE banking sectors and the impact of the global financial crisis. J. Bank. Financ. 40, 11–27 (2014)

Rakshit, B., Bardhan, S.: Bank competition and its determinants: evidence from Indian banking. Int. J. Econ. Bus. 26(2), 283–313 (2019)

Sompolos, Z., Mavri, M.: Estimating the efficiency of Greek Banking System during the last decade of world economic crisis: an econometric approach. Benchmark. Int. J. 25(6), 1762–1794 (2018)

Boyd, J.H., De Nicolo, G.: The theory of bank risk-taking and competition revisited. J. Financ. 60, 1329–1343 (2005)

Shim, J.: Loan portfolio diversification, market structure and bank stability. J. Bank. Financ. 104, 103–115 (2019)

Azmi, W., Ali, M., Arshad, S., Rizvi, S.A.: Intricacies of competition, stability, and diversification: evidence from dual banking economies. Econ. Model. 83, 111–126 (2019)

Beck, T., De Jonghe, O., Schepens, G.: Bank competition and stability: cross-country heterogeneity. J. Financ. Intermediat. 22(2), 218–244 (2013)

González, L.O., Razia, A., Búa, M.V., Sestayo, R.L.: Competition, concentration, and risk taking in Banking sector of MENA countries. Res. Int. Bus. Financ. 42, 591–560 (2017)

Lenza, M., Pill, H., Reichlin, L.: Monetary policy in exceptional times. Econ. Policy. 25, 295–339 (2010)

Eser, F., Schwaab, B.: Evaluating the impact of unconventional monetary policy measures: empirical evidence from the ECB's securities markets programme. J. Financ. Econ. 119(1), 147–167 (2016)

Steeley, J., Matyushkin, A.: The effects of quantitative easing on the volatility of the gilt-edged market. Int. Rev. Financ. Anal. 37, 113–128 (2015)

Beetsma, R., de Jong, F., Giuliodori, W.D.: Realized (co) variances of eurozone sovereign yields during the crisis: the impact of news and the securities markets programme. J. Int. Money Financ. 75, 14–31 (2017)

Fratzscher, M., Duca, M.L., Straub, R.: ECB unconventional monetary policy: market impact and international spillovers. IMF Econ. Rev. 64(1), 36–74 (2016)

Kenourgios, D., Papadamou, S., Dimitriou, D.: Intraday exchange rate volatility transmissions across QE announcements. Financ. Res. Lett. 14, 128–134 (2015)

Acharya, V.V., Eisert, T., Eufinger, C., Hirsch, C.: Whatever it takes: the real effects of unconventional monetary policy. Rev. Financ. Stud. 32(9), 3366–3411 (2019). https://doi.org/10.1093/rfs/hhz005

Kenourgios, D., Christopoulos, A., Dimitriou, D.: Asset markets contagion during the global financial crisis. Multinatl. Financ. J. 17(1/2), 49–76 (2013)

Yu, S.: Sovereign and bank interdependencies – evidence from the CDS market. Res. Int. Bus. Financ. 39, 68–84 (2017)

Keddada, B., Schalckb, C.: Evaluating sovereign risk spillovers on domestic banks during the European debt crisis. Econ. Model. 88, 356–375 (2020)

Turk-Ariss, R.: On the implications of market power in banking: evidence from developing countries. J. Bank. Financ. 34(4), 765–775 (2010)

Boyd, J.H., Gertler, M.: Are banks dead? or are the reports greatly exaggerated? Federal Reserve Bank of Minneapolis. Q. Rev. 18, 2–23 (1994)

Berger, A.N., Klapper, L.F., Turk-Ariss, R.: Bank competition and financial stability. J. Financ. Serv. Res. 35(2), 99–118 (2009)

Angbanzo, L.: Commercial bank net interest margins, default risk, interest-rate risk and off-balance sheet banking. J. Bank. Financ. 21, 55–87 (1997)

Jimenez, G., Lopez, J., Saurina, J.: How does competition affect bank risk-taking? J. Financ. Stabil. 9, 185–195 (2013)

Kasman, S., Kasman, A.: Bank competition, concentration, and financial stability in the Turkish banking industry. Econ. Syst. 39, 502–517 (2015)

Fu, X., Lin, Y.: Molyneux P Bank competition and financial stability in Asia Pacific. J. Bank. Financ. 38, 64–77 (2014)

Arellano, M., Bond, S.: Some tests of specification for panel data: Monte Carlo evidence and an application to employment equations. Rev. Econ. Stud. 58, 277–297 (1991)

Leroy, A., Lucotte, Y.: Is there a competition-stability trade-off in European banking? J. Int. Finan. Markets. Inst. Money. 46, 199–215 (2017)

Kanellos, N., Sakas, D.P., Kamperos, I.D.G., Reklitis, D.P., Giannakopoulos, N.T., Nasiopoulos, D.K., Terzi, M.C.: The effectiveness of centralized payment network advertisements on digital branding during the COVID-19 crisis. Sustainability. 14(6), 3616 (2022)

Alexandros, N.K., Damianos, S.P., Dimitrios, N.K., Dimitrios, V.S.: Modelling the Process of a Web-Based Collaboration Tool Development. In: Kavoura, A., Sakas, D., Tomaras, P. (eds) Strategic Innovative Marketing. Springer Proceedings in Business and Economics. Springer, Cham (2017). https://doi.org/10.1007/978-3-319-56288-9_51

Sakas, D.P., Nasiopoulos, D.K., Reklitis, P.: Modeling and Simulation of the Strategic Use of Marketing in Search Engines for the Business Success of High Technology Companies. In: Sakas, D., Nasiopoulos, D. (eds) Strategic Innovative Marketing. IC-SIM 2017. Springer Proceedings in Business and Economics. Springer, Cham (2019). https://doi.org/10.1007/978-3-030-16099-9_27

Sakas, D.P., Nasiopoulos, D.K., Reklitis, P.: Modeling and Simulation of the Strategic Use of the Internet Forum Aiming at Business Success of High-Technology Companies. In: Sakas, D., Nasiopoulos, D. (eds) Strategic Innovative Marketing. IC-SIM 2017. Springer Proceedings in Business and Economics. Springer, Cham (2019). https://doi.org/10.1007/978-3-030-16099-9_22

Sakas, D., Vlachos, D., Nasiopoulos, D.: Modelling strategic management for the development of competitive advantage, based on technology. J. Syst. Inf. Technol. 16, 187 (2014)

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2024 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this paper

Cite this paper

Christopoulos, A., Katsampoxakis, I., Thanos, I., Toudas, K. (2024). Mergers and Acquisitions Between Systemic Banks in Greece and Their Impact on Concentration and Control. In: Sakas, D.P., Nasiopoulos, D.K., Taratuhina, Y. (eds) Computational and Strategic Business Modelling. IC-BIM 2021. Springer Proceedings in Business and Economics. Springer, Cham. https://doi.org/10.1007/978-3-031-41371-1_37

Download citation

DOI: https://doi.org/10.1007/978-3-031-41371-1_37

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-031-41370-4

Online ISBN: 978-3-031-41371-1

eBook Packages: Business and ManagementBusiness and Management (R0)