Abstract

Over the past 20 years there has been a large inflow of investment capital into commodity futures markets, a phenomenon known as the financialization of commodities. The purpose of this chapter is to analyse the behavior of commodity futures returns before and since financialization of the markets. In contrast with most of the literature that treats commodities as individual assets, this chapter models futures contracts as part of a balanced portfolio that includes other assets (equities and other commodities) and we control for weekly changes in speculative positions similar to Carter et al. (1983). In this study we allow for two factors giving rise to futures premiums: hedging pressure and systematic risk. We find that the recent poor returns to managed futures trading coincided with a suppressed risk premium.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

JEL Codes

“The genius of trend-following (in futures markets) is not how awesome it is, but its incredible mediocrity, which is far harder to engineer than people think. It’s like trying to cheat at the casino, if you’re too good then the casino throws you out. Trend following works right at the edge of randomness.”Footnote 1

1 Introduction

Over the past 20 years, there has been a large inflow of investment capital into commodity futures markets—the financialization of commodities. This chapter analyses the behavior of commodity futures contract returns before and since financialization of the markets. We believe that Professor Gordon Rausser’s research in the 1970s contributed to the dramatic inflow of speculative investment into commodity futures, because he showed there were possible profits to be made “right at the edge of randomness” with computerized trading rules. Using the methodology in Carter et al. (1983) we find that the financialization impacted the Keynesian risk premiums in the futures market, as the market became over-crowded with speculative money.

This chapter is dedicated to Gordon Rausser, who has been a significant and influential contributor to the literature on the economics of futures markets. He has also shaped the way in which hedge funds and other large investors such as pension funds view the commodity futures market. Some of Dr. Rausser’s publications in this area include Cargill and Rausser (1972, 1975); Carter et al. (1983); Just and Rausser (1981); Rausser and Just (1979); Rausser and Carter (1983), and Rausser and Walraven (1990).

Professor Rausser was one of the very first economists to use the latest in computer technology in the early 1970s to study futures price behavior and price patterns. This technique was subsequently picked up by many in the profession and importantly by hedge funds and professional money managers investing in the futures market. The business of hedge funds and other capital managers investing in commodity futures, using quantitative computer models, began after Gordon Rausser’s pioneering work with Cargill, see Cargill and Rausser (1972, 1975). Cargill and Rausser studied the stochastic behavior of futures prices, using a very sophisticated methodology for the time. Cargill and Rausser (1972) studied eight markets and their results raised doubts as to whether futures price behavior is consistent with the random walk model as a general explanation of how futures price behave over time. Then a few years later Cargill and Rausser (1975) studied seven commodity futures contracts in more detail: corn, oats, soybeans, wheat, copper, live beef cattle, and pork bellies. Based on a number of serial correlation tests, for these commodities Cargill and Rausser rejected the random walk model. The implication of this finding was that the application of certain mechanical filter trading rules could lead to substantial profits in commodity futures, due to their nonrandom behavior.

Subsequent to the publication of Cargill and Rausser (1975) the futures markets attracted more and more attention from investors from outside of the commodity business–non-commercial market participants. It then became commonplace for trend-following hedge funds and large money managers to begin to use computers for quantitative and statistical analysis of futures prices to inform trading decisions. They started what is now known as the financialization of the futures market and their techniques were no doubt informed by Professor Rausser’s work. In fact, the Chicago Mercantile Exchange (CME) held at least four managed futures symposia in the late 1980s and early 1990s, with an agenda that was largely based on Carter et al. (1983). These symposia covered institutional investors’ use of commodities and issues related to managed futures. The work of Carter et al. (1983) was presented at each symposia.

In an articleFootnote 2 entitled The hedge funds split over following market trends, the Financial Times reported on one of these successful firms that pioneered computer driven investing in commodity futures:

In 1982, Mike Adam, a scholarship student who had dropped out of Magdalen College, Oxford, took a backroom job in his father’s sugar broking firm in London. The new job entailed drawing commodity price charts by hand and tracking the brokerage’s trades. To save time, Mr. Adam programmed the first computer to arrive in the firm’s offices to do the job for him. Soon, overcome by curiosity, he began to test whether the computer could be coded in such a way that he could make money from trading patterns. Together with his close friend from university, Marty Lueck, who was a programmer, and David Harding, a Cambridge-educated scientist fascinated with finance, he designed a trading system. At its heart was a simple concept—financial markets exhibit trends, and computers can be programmed to spot those trends and profit from them. Amid much skepticism from a finance industry that largely believed using computers to predict market moves was little more than hocus-pocus, the trio in 1987 launched AHL—a name based on the first letters of their surnames. The firm, which now runs $30bn in assets, went on to help spawn a $300bn-dollar industry of similar hedge funds that follow market trends and which have minted vast fortunes.

A risk premium in futures prices is consistent with the Cargill and Rausser (1975) finding that futures prices may have deterministic trends, in violation of the random walk hypothesis. Such a risk premium could arise due to hedging pressure. It was Keynes (1923b) who suggested that futures prices may trend upward, because at any given time the futures price will be below the anticipated future spot price by the amount of the risk premium, paid by hedgers. The existence and size of a risk premium in futures markets has been controversial since the famous Telser-Cootner debate in the late 1950s and early 1960s (see Telser (1958) and Cootner (1960)). Based on the belief that trading profits on the long side could be earned from such a risk premium, about 40 years after the debate, the American International Group (AIG) established the AIG commodity index—an index of commodity futures prices—in the late 1990s.Footnote 3 The AIG index was established in order to attract outside investors to commodity futures. Investing in the AIG index was a relatively easy way for an investor to add commodities to a portfolio. The work by Gorton and Geert Rouwenhorst (2006) supported AIG’s aim to attract investors to futures markets as Gorton and Geert Rouwenhorst argued that commodity futures offer the same return and Sharpe ratio as U.S. equities. The underlying explanation was the existence of a risk premium in commodity futures. However this view was not without controversy, as Erb and Harvey (2006) concluded that average commodity futures returns are not equity-like, instead they are zero. Later, Erb and Harvey (2016) argued that portfolios of commodity futures do not have equity-like returns either.

Index speculation in commodities took off in the early 2000s, so much so that in 2008 the U.S. Senate held committee hearings on the role of index speculators influencing crude oil prices, because oil spiked above $130 a barrel in the summer of 2008. The impact of the increased trading of noncommercial players on commodity prices has been dubbed the financialization of commodity markets. Many of the “outside” investors hold commodities through commodity futures indexes such as the Goldman Sachs commodity index (GSCI), the Dow Jones index (DJ-UBS) and the S&P commodity index (SPCI). They also invest in over-the-counter (OTC) swaps and exchange-traded-funds (ETFs) linked to commodity indexes. Index speculators are thought to be the largest participants in the futures market today, and nearly all of them are based on passive, long-only, commodity futures positions (Stoll & Whaley, 2010). Pension and hedge funds joined this group of large speculators. For instance, the California Public Employees’ Retirement System (CalPERS) began allocating money to commodities in 2007.Footnote 4

Commodity index investments were profitable from around 2000 until 2008, according to the commodity trading adviser—CTA Benchmark Index. As shown in Fig. 1, the CTA Benchmark Index peaked around the same time as assets under management in commodity futures peaked (approximately 2012). Since then there has been a degradation in futures returns earned by this class of traders. Could this be due to increased competition for the same source of alphaFootnote 5–a case of more funds using the same approach in the same markets? The question we address is whether financialization of futures has impacted futures market risk premia. Previous studies by Hamilton and Wu (2015) and Main et al. (2018) have addressed a similar question but without controlling for changing speculative positions, the importance of which was recognized by Cootner (1960) and Carter et al. (1983)—hereafter CRS. We investigate the same futures markets as in CRS–wheat, corn, soybeans, cotton and live cattle.

Managed futures & returns index

Hamilton and Wu (2015) found that commodity index-fund investing had no measurable effect on commodity futures prices. Similarly, Main et al. (2018) showed that the average unconditional return to individual commodity futures markets was approximately equal to zero before and since financialization of the markets. Controlling for the importance of liquidity provision in the commodities market, Kang et al. (2020) find an empirical relationship between hedging pressure and expected futures risk premiums. However, these recent papers treat commodities as individual assets instead of being part of a balanced portfolio that includes equities and other commodities. In contrast to these studies, we control for weekly changes in speculative positions and model commodity returns in a portfolio context, similar to CRS. As in CRS, we allow for two factors giving rise to futures premiums, hedging pressure and systematic risk. We find that the recent poor returns to managed futures trading coincided with a suppressed risk premium.

The structure of our chapter is as follows: we start by providing a background on the financialization of commodity futures, which is followed by a literature review (Sect. 3) on normal backwardation since Keynes and its developments. The next section presents the methodology of the paper. Section 5 presents our empirical analysis and Sect. 6 concludes.

2 Background

The financialization of commodity futures refers to the fact that managed money (or institutional funds) investment in commodity futures has grown–i.e., the emergence of commodity futures as an asset class. Assets under management in commodity futures grew from less than $50 Billion in the early 2000s to over $300 Billion recently, see Fig. 1. In Fig. 1 assets under management are shown on the left-hand vertical axis and the Barclay CTA benchmark index showing trader’s performance is on the right-hand axis. A vertical line is drawn in Fig. 1 at the year 2007 to represent when financialization took hold, with over $200 Billion invested in the futures market by then. The Barclay CTA IndexFootnote 6 represents the performance of hundreds commodity trading advisersFootnote 7 and it has been declining since about 2012.

Figure 2 provides an annual breakdown of the average performance of managed futures funds, from 2000 to 2018. The funds earned positive returns on average from 2000 through 2008. From 2000 to 2006 the annual average return was 7.3%. Average returns then declined in the more recent years. From 2007 through 2018 the annual average return was only 2.8%, with negative annual returns as frequent as positive annual returns.

Managed Futures Performance

Further confirmation that futures have not been generating equity like excess returns is shown in Table 1, which reports 2008–2018 returns for the S&P equity index, Barclay’s bond index, and the Bloomberg Commodity Index (BCOM). Bloomberg’s BCOM is calculated as an excess return and it reflects commodity futures price movements. BCOM experienced an annual average returns of −2.74% from 2008–2018, while the S&P return averaged 6.74% over this same time period.

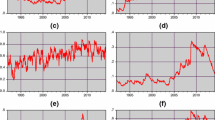

For 13 agricultural commodity futures markets, the Commodity Futures Trading Commission (CFTC) publishes weekly data on the relative importance of index trading in a supplemental commodity index report.Footnote 8 These data for 9 months in 2019 are provided in Figs. 3, 4, 5, 6, 7 for CBT SRW wheat, corn, soybeans, cotton and live cattle, respectively. The left-hand vertical axes in Figs. 3, 4, 5, 6, 7 report the net futures positions (long minus short) for four classes of traders: large speculators, large hedgers, small traders, and index traders. The large hedgers and large speculators are traders who hold outstanding futures positions that exceed CFTC defined thresholds.

Index traders large share of the market: Wheat

Index traders large share of the market: Corn

Index traders large share of the market: Soybeans

Index traders large share of the market: Cotton

Index traders large share of the market: Live Cattle

For reference, the commodity’s price is shown on the right-hand vertical axis in Figs. 3, 4, 5, 6, 7. Unlike other classes of traders, the overall number of contracts held by index traders from week to week does not seem to be correlated with the price at all. It is clear from these Figures that index traders are some of the largest participants in these markets, measured in terms of net positions. The Figures also show that the index traders in net terms were long for the entire time period, for all the commodity markets with information on index trader positions. In the case of CBT wheat in Fig. 3 index traders held on average over 105,000 (net long) contracts, compared to large speculators who held around 59,000 (net short) contracts on average. For corn in Fig. 4, index traders held over 252,000 (net long) contracts on average, while large speculators held around 89,000 (net short) contracts on average. See Table 2 for these summary statistics for the other markets. With the exception of live cattle, the index traders were the dominant group during the time periods shown in Figs. 3, 4, 5, 6, 7.

3 Literature Review

As mentioned above, an essay in the Manchester Guardian Commercial in 1923 by John M. Keynes (Keynes, 1923b) initiated the concept of the theory of normal backwardation.Footnote 9 In his view futures prices are unreliable estimates of the cash or spot price prevailing on the date of expiry of the futures contract. He believed it “normal” for the futures price to be a downward biased estimate of the forthcoming spot price. This theory in effect, argues that speculators sell “insurance” to hedgers and that the market is “normally” inefficient because the futures price is not an unbiased estimate of the subsequent spot price.Footnote 10

The three crucial assumptions of the theory of normal backwardation are: that speculators are net long, they are risk averse (i.e., they require positive profits), and they are unable to forecast prices (i.e., all of their profits can be viewed as a reward for risk bearing). Given these assumptions, two major implications can be assigned to the theory. The first is that over time speculators will earn profits by merely holding long positions in futures markets. The second implication is that there is an upward trend in futures prices, relative to spot prices, as the contract approaches maturity.Footnote 11

Cootner (1960) argued that Keynes’ hypothesis implies futures prices should not necessarily rise until after the peak of net short hedging has passed. That is, he interpreted the theory to mean seasonal trends in futures prices should be taken as an indication of a risk premium. Telser (1958) and Cootner (1960) both tested their interpretation of the theory of normal backwardation and obtained conflicting results, even though they used the same data. Cootner found evidence to support the theory of normal backwardation, whilst Telser’s conclusions were contrary. However, the problem was essentially assumed away to Telser. He assumed speculators require no remuneration to play the futures market and then went on to conclude they earn no remuneration in a competitive market.

Several other early writers have also tested the validity of the theory of normal backwardation. A succinct summary of their findings was given by Rockwell (1976) who concluded:

While the theory of normal backwardation may be valid for particular markets under special conditions, it is not adequate as a general explanation of the flow of profits in commodity markets. (p. 110)

Subsequently Dusak (1973) then tested for the existence of a risk premium within the context of the capital asset pricing model (CAPM). With this approach, she argued, the Keynesian notion of a risk premium takes on a new interpretation. Namely, the risk premium required on a futures contract should depend on the extent to which the variations in prices are systematically related to variations in the return on total wealth. If the CAPM applies, and if the risk of a futures contract is independent of the risk of changes in the value of all assets taken together, then investors will not have to be paid for that risk since they can diversify it away. The original Keynesian “insurance” interpretation, on the other hand, identifies the risk of a futures asset solely with its own price variability. Dusak tested for both types of risk in the futures market, and her results suggested that wheat, corn, and soybeans futures contracts are not risky assets whether they are held independently or as part of a larger portfolio of assets.

In Dusak’s analysis it is implicitly assumed that speculators are net long throughout the life of a futures contract. By relaxing this assumption it is believed that one could find at least some degree of specific risk associated with a futures contract. In empirically estimating the capital market line, Dusak uses the return on the value-weighted Standard and Poor (S&P) Index of 500 Common Stocks as a proxy variable for the return on total wealth. An alternative proxy (one which gives some weight to a commodity index, for example) may well yield some degree of systematic risk.

Conceptually, the equilibrium futures price in relation to the expected spot price at expiry can be characterized by examining the net positions of hedgers and speculators. Commercial hedgers are interested in entering into futures contracts in order to eliminate price risk. If commercial hedgers are typically net short, this means that at any given futures price, hedgers as a group want to sell more contracts than they want to buy as illustrated by the line WX in the left quadrant in Fig. 8.Footnote 12 The higher the futures price the more contracts they want to sell, and hence WX is downward sloping. Speculators have no interest in entering into futures contracts as a way to reduce risk, instead they enter into futures contracts with the goal of profiting from expected price movements. When the futures price is equal to the expected spot price at expiry, E, speculators as a group will be neither short nor long as there is no potential profit since the expected price change in the futures contract is zero. When the futures price is below the expected spot price at expiry, (the right-hand portion of the line YZ in Fig. 8) speculators will be net long as they anticipate earning a profit from the expected increase in the futures price. Similarly, when the futures price is above the spot price “expected” at expiry, speculators as a group will want to be net short. This is shown by the top portion of the line YZ in Fig. 8.

Theory of normal backwardation

The futures market will clear only when the total number of short contacts equals the number of long contracts. This market clearing condition along with the net short position of hedgers leads to the futures price equilibrium, B, at a price below the expected spot price (E) at expiry. In Fig. 8, we can see that the equilibrium futures price is at point B and the volume of contracts represented by the net hedgers position, A, equals the speculators net long position, C.

This is why, in the view of John Keynes, futures prices are unreliable estimates of the cash price prevailing on the date of expiration of the futures contract. He believed it “normal” for the futures price to be a downward-biased estimate of the forthcoming spot price. This theory, in effect, argues that speculators sell “insurance” to hedgers and that the market is “normally” informationally inefficient because the futures price is a biased estimate of the subsequent spot price.

CRS built on Houthakker (1957), Telser (1958), Cootner (1960), and Dusak (1973), and found a risk premium in the futures market. CRS measured returns in a portfolio context, as in the equity risk premium literature that focuses on the risk and return of an asset’s contribution to a portfolio instead of individualized risk and return. With this framework, futures returns depend on movement with the market—systematic risk and also idiosyncratic risk. CRS found commodities in which hedgers were net short had positive excess returns on average and commodities in which hedgers were net long had negative excess returns on average—supporting Cootner (1960) that speculative pressure matters. CRS estimated non-market and systematic risk as time-varying parameters to evaluate seasonal changes in investors’ positions and they modified Dusak’s choice of the investor’s portfolio. Marcus (1984) criticized CRS for over-weighting commodities in the well-diversified portfolio and showed that with a reduced weighting the hypothesis of zero systematic risk cannot be rejected. This is not surprising because it is essentially a restatement of the Dusak result, and it assumes that a portfolio comprised of only equities is optimal. The CRS finding of seasonality of non-market risk is independent from the debate over how much weight to give commodities in the investor’s portfolio.

CRS not only found evidence of systematic risk, but more importantly, they found evidence of non-systematic risk that varied seasonally. CRS’ finding of time-varying non-market risk encouraged subsequent work to apply more general non-static models of the pricing of futures contracts.

For example, Kang et al. (2020) provided a contrary perspective to the Keynesian theory. They find an empirical relationship between hedging pressure and expected futures risk premiums. Instead of hedgers paying speculators a risk premium, they suggest speculators must pay a premium to hedgers (i.e., commercial firms) in order to generate necessary market liquidity. However, their paper treats commodities as individual assets instead of being part of a balanced portfolio that includes equities and other commodities.

Fama and French (1987) also also tested for a time-varying risk premium in futures prices. Chang (1985), Bessembinder (1992) and De Roon et al. (2000) found that futures risk premia are related to market risk and hedging pressure, confirming the finding in CRS. Erb and Harvey (2006), and Gorton et al. (2012) further linked the commodity futures risk premium to backwardation in commodity futures and the theory of commodity storage.

Gorton and Geert Rouwenhorst (2006), and Bhardwaj et al. (2016) studied monthly returns to commodity futures as an asset class. Their data set went back as far as the 1950s. They conclude that commodity futures have offered the same return as publicly traded U.S. stocks, adjusted for the risk free return equities. Furthermore commodity futures returns are negatively correlated with stock returns and bond returns. The negative correlation arises from commodity futures different behavior over a business cycle because commodity futures are positively correlated with inflation. Implicit in this finding is the implication that speculators in commodity futures receive a return for providing price insurance to hedgers. In the presentations to large institutional money managers sponsored by the CME, mentioned above, Professor Rausser emphasized the portfolio diversification opportunities for risk reduction by including exposure to futures in combination with typical bond/stock portfolios.

Bhardwaj et al. (2019)-BJR found that futures prices have on average been trading at a discount to future spot prices by about 5% (1871–2018 data). Of the contracts that survived longer than 50 years, 91% earned a positive risk premium. BJR found that of the 230 contracts in their sample, 58% earn a positive lifetime “buy-and-hold” risk premium when they rolled expiring contracts forward over time, and the median geometric average premium across commodities was 1.5%.

Tang and Xiong (2012) found price behavior of index commodities has become different from nonindex commodities—becoming more correlated with oil and equities—outside money from index investors has linked them together. The intuition for this rise is that institutions that entered these markets have linked them together, as well as with the stock market, through cross-holdings in their portfolios. In a study of 12 agricultural commodity futures, Hamilton and Wu (2015) found commodity index-fund investing had no measurable effect on commodity futures prices (using 1990–2014 data). Main et al. (2018) found the average unconditional return to 19 individual agricultural and energy futures markets was approximately equal to zero before and since financialization (using 1961–2014 data). Most of the literature addressing financialization has treated commodities as independent assets instead of being part of a portfolio. The latter has the advantages mentioned in CRS. Namely, the risk of an asset is properly measured by the volatility of the asset’s returns relative to that of a broad market portfolio, rather than viewing the asset’s risk separately from the overall market. Moreover the purpose of our analysis is to explore whether financialization affected the systematic and idiosyncratic risks associated with futures contracts.

4 Methodology

Building on Cootner (1960), CRS provided theoretical and empirical evidence to support the notion that the nonmarket rate of return is a stochastic variable that is a function of net hedging pressure. This generalizes the Keynesian theory of normal backwardation to allow for variable traders’ positions. Our methodology is based on CRS and the empirical model is shown in eq. (1).

Where: Rt is the asset return for futures contract j during period t,Footnote 13 xjt is the market index minus the risk-free interest rate, Zt is the (changing) speculative position (same for all contract months for a given commodity), α is the pooled non-market risk (averaged across all contracts for a specific commodity), β is the asset’s pooled systematic risk, and μjt is the error term. As in CRS, α* = α + δZt is the expected value of the non-market component of futures contracts’ excess return (CRS, p. 328), and β* = β + δZt is the expected value of the systematic component of futures contracts’ returns (CRS, p. 324). The total return to holding a futures contract is therefore made up of two components. The first is the systematic risk based on the asset’s covariance with the market index, and the second is the excess return. Hedging pressure can influence both of these components of return.

Our data set consists of weekly observations of five commodity futures contracts over the period from January 1986 to July 2019—corn, cotton, live cattle, soybeans and wheat. These are the same commodities studied by CRS. Each futures contract with a specific delivery month over this time period was included in our data. For instance, corn futures have five different delivery months (March, May, July, September and December). Our data set consists of each of the March corn contracts over the 1986 to 2019 time period, each of the May corn futures contracts, and so on.

We define Zt = (non-commercial longs)/(non-commercial longs + non-commercial shorts), sourced from Commodity Futures Trading Commission: Commitment of Traders (COT) weekly reports from January 1986–July 2019. When Zt = 0.5 speculators are neither long nor short on net; when Zt > 0.5 speculators are net long; and when Zt < 0.5 speculators are net short. Therefore, Zt represents the percentage of reporting speculators that were net long, and lies in the interval between zero and one. Figures 9 and 10 show the Zt index plotted against live cattle and wheat futures prices, respectively.Footnote 14 Interestingly the data reported in Figs. 9 and 10 show the Zt index for live cattle and wheat was more variable before financialization compared to after. The vertical lines drawn in Figs. 9 and 10 depict the cutoff point we are defining with regard to the period prior to financialization versus the period afterwards. The cutoff point is January 2007. In the case of crude oil the Zt index also trended upward with financialization. Finally, the xjt variable represent first differences of the natural logarithms of the market index (the Standard and Poor’s (S&P) and Dow Jones and Company (DJ&C) indices weighted equally) minus the 90-day Treasury Bill rate converted to a weekly interest rate.

CME cattle futures and Z index

CBOT wheat futures and Z index

As pointed out in CRS the error term of eq. (1) is a function of the errors from the nonmarket α* and systematic β* components of the futures contracts (i.e., they are heteroskedastic) and therefore the equation needs to be estimated using generalized least squares. We follow the same econometric methodology as CRS.

5 Analysis

Summary statistics for the weekly returns for all futures contracts, for each of the five commodities studied, are presented in Table 3. The descriptive statistics in Table 3 are calculated by pooling all the contracts for each commodity. The number of observations (N) is reported in the second column. Column three reports the average individual asset returns over the entire time period studied and column four reports the one period return autocorrelation (ρ). Columns five and six report the average Z values and average x (i.e., market index minus the riskless rate) return.

Table 3 reports that the unconditional mean weekly returns for live cattle and soybeans are positive and statistically significant from zero. Alternatively the average returns for corn and wheat are negative and statistically significant. Returns for cotton are not statistically different from zero.

The last two columns of Table 3 present the estimated slope coefficient of two simple regressions of weekly returns on the market index (the θ) and the Z values (the φ).Footnote 15 Live cattle and soybeans are the only commodities that have statistically significant θs. Overall, with this simple regression approach, the θs indicate varied results regarding statistically significant systematic risk across commodities. However, from Table 3 it is important to note that each commodity has a statistically significant φ. This suggests there is a relationship between futures returns and the net position of speculators, which is explored in more detail below.

Tables 4, 5, 6, 7, 8 present the results from the generalized least squares estimation of eq. (1), following the procedure in CRS. In each of these tables we report the regression results for the entire sample period and then separately for the before (1986–2006) and after (2007–2019) financialization sub-periods.

As mentioned, the errors in eq. (1) are heteroskedastic and the results of the estimation by GLS are reported in Tables 4, 5, 6, 7, 8. The dependent variables (Rjt) used in the regression were the first differences of the natural logarithms of weekly average futures prices minus the riskless rate. As regards the independent variables, the Zt were obtained from the Commodity Futures Trading Commission (CFTC) weekly Commitment of Trader (CoT) reports. The xjt variables represent the first differences of the natural logarithms of the market index (the S&P and DJ&C indices weighted equally) minus the 90-day Treasury Bill rate converted to a weekly interest rate. In addition, the Davidson and McKinnon (1993) test was carried out to explore the potential indogeneity of the regressors with respect to the error term. All the tests did not reject the null hypothesis of exogeneity.Footnote 16

Looking down Tables 4, 5, 6, 7, 8, for both the before and after periods, we find that corn and cotton are the only two commodities with estimated systematic risk coefficients (βs) that are generally significantly different from zero. These results are consistent with CRS and other literature, which has found mixed results regarding systematic risk. Furthermore, across contract months, for cotton, live cattle, and soybeans there are fewer β values statistically significant in the after period compared to the before period. This means that updating the CRS results we find that the prevalence of systematic risk is lower after financialization of the commodity markets. If a commodity has no systematic risk then any returns above zero will be due to idiosyncratic (or nonsystematic) risk only (i.e., excess returns).

The γ estimates in Tables 4, 5, 6, 7, 8 suggest that for those contracts displaying systematic risk, the degree of systematic risk is impacted by the Z value. Across all commodities studied the β and γ coefficients have opposite signs. Since the net long position of speculators increases with Z, this finding suggests that an increase in speculative buying will tend to reduce the systematic risk, ceteris paribus. In other words, increased financialization has tended to reduce the systematic risk component of futures returns.Footnote 17

The nonmarket rate of returns measure (α) and its systematic change associated with net speculative positions (δ), go directly to the question of whether or not there is a Keynesian risk premium. As in CRS, we find the estimated α and δ values are almost all significantly different from zero and the δ values tend to be roughly twice as large as the α values and they tend to have the opposite sign. This is the case across Tables 4, 5, 6, 7, 8. It is also noteworthy that the estimated α and δ values are different in the before/after time periods.

As in CRS, these results provide an interesting interpretation of the Cootner hypothesis. Recall that the value of α∗ = α + δZt, represents the expected value of the nonmarket component of a futures contract’s return, i.e., the risk premium. When Zt is equal to 0.5, the net position of speculators is neither long nor short; and the results in Tables 4, 5, 6, 7, 8 suggest that the nonmarket returns are near zero. When Zt > 0.5, speculators are net long and the rate of return is greater than the amount predicted by the market model. Similarly, when Zt < 0.5, speculators are net short, and there are negative returns in excess of the market return. Therefore our findings provide support for the Cootner hypothesis of the existence of a degree of normal backwardation in the commodity futures market, given an appropriate interpretation of the net position of speculators.

Figures 11, 12, 13 present different graphical views of the estimated α and δ coefficients estimated from eq. (1).Footnote 18 As shown in Tables 4, 5, 6, 7, 8, the estimated α and δ coefficients in all cases are statistically different from zero, with the exception of corn in the after period. All of the contracts have values of α that are negative and positive for δ (except for corn in the after period), which matches the results by contract presented in CRS. Figure 11 shows the before and after α coefficients, and Fig. 12 shows the before and after δ coefficients. The 45-degree line in these two figures indicates no change in the parameters across the two time periods. Figure 11 shows that all the commodities are characterized by negative values of α in both periods. Most of the commodities (except for corn) show a decrease in the value of α (i.e., the coefficient became more negative). In the case of corn, the value α increased after financialization, although it remained negative. It is important to note that this change in the value of α happened in all the corn contracts when the regressions were run contract by contract.

Before and after alpha-alpha relationship

Before and after delta-delta relationship

Alpha-delta before/since relationship

The values of δ in Figure 12 mimic what is observed in the case of α but in a reverse way. All of the commodities show an increase in the value of δ, except for corn.

Figure 13 presents α and δ pairs for the two sub periods. The Figure shows a clear change in the distribution of the coefficients. However it is important to note that the α and δ relationship is preserved in the after period, it is just shifted. After 2007 the pairs of coefficients moved in the north-west direction, indicating that they all became larger in absolute value, with the exception of corn. The net effect of the shift is that the values of α∗ = α + δZt were reduced.

This impact is shown in Table 9 which reports estimates of the annualized excess futures returns before and since 2007. The table shows a significant decrease in the average non-market returns to speculators after 2006. For instance, cotton returns declined from 2.4% to −5.6%. At the same time, soybean returns declined from 12.5% to 3.3%. Live cattle was the only commodity to experience an increase in returns, from 6.2% to 9.4%. On average, the annualized returns declined from 4.2% to −3.6%. Overall, these result provides evidence supporting the view that the scale of financialization was large enough to reduce the historical risk premiums in the commodity futures markets evaluated by CRS.

6 Conclusion

The popularization of commodities as an investment is commonly referred to as the financialization of commodity futures markets. In the early 2000s, investors were attracted to commodity futures as a new asset class. The investors were informed that commodities provided stock like returns, with the added advantage of a low correlation with stocks and bonds. Hundreds of billions of dollars then flowed into the commodities market. Large institutional investors generally gained long exposure to commodities through direct holdings of futures contracts as well as the use of over-the-counter derivatives and swaps. The returns to this asset class initially performed well, but then peaked in about 2012. Since then, the investment benefits have not turned out as promised. For instance, $10,000 invested in one of the larger commodity index funds in the United States–the United States Commodity Index Fund (USCI)–was worth around $5,000 in June 2020.

In this chapter we posit that Professor Rausser’s research on futures markets published in the 1970s was influential in leading to the financialization of commodity futures and the rise of commodity hedge funds and their computer aided trend-following investment strategies. There has been discussion in the literature whether the scale of financialization was large enough to reduce the historical risk premiums in commodity futures markets. Our results from an analysis of 5 commodities (updating the findings in Carter et al. (1983)) provides evidence supporting the view that risk premia have declined after 2007.

Notes

- 1.

This quote is from a Financial Times interview with Mike Adam, one of the founders of the successful hedge fund AHL. Mr. Adam started by drawing price charts by hand in his father’s sugar broking firm. https://www.ft.com/content/916ed2e0-d63f-11e9-a0bd-ab8ec6435630. September 16, 2019.

- 2.

https://www.ft.com/content/916ed2e0-d63f-11e9-a0bd-ab8ec6435630. September 16, 2019

- 3.

The Goldman Sachs Commodity Index was developed in 1991, and the Bloomberg Commodity Index was developed around the same time as the AIG index.

- 4.

In September 2014 CalPERS announced that it was eliminating its hedge fund program. However at the same time CalPERS announced that it was maintaining a portfolio of commodity futures tied to the S&P GSCI.

- 5.

The excess return of an asset relative to the return associated with the asset’s beta is the asset’s alpha.

- 6.

The Barclay CTA Index is designed to broadly represent the performance of all CTA programs in the BarclayHedge database. The programs included in the index must have a performance history. Only CTAs with 4 years of performance history are included in the index and the performance history begins with year 5. At the beginning of the year a hypothetical portfolio is formed with each constituent program given an equal allocation. The index monthly return is simply the monthly return of this hypothetical portfolio. In 1999 319 CTA programs were included in the index.

- 7.

- 8.

The CFTC explains that: “Index Traders are drawn from the noncommercial and commercial categories. The noncommercial category includes positions of managed funds, pension funds, and other investors that are generally seeking exposure to a broad index of commodity prices as an asset class in an unleveraged and passively-managed manner. The commercial category includes positions for entities whose trading predominantly reflects hedging of over-the-counter transactions involving commodity indices–for example, a swap dealer holding long futures positions to hedge a short commodity index exposure opposite institutional traders, such as pension funds.” see https://www.cftc.gov/MarketReports/CommitmentsofTraders/ExplanatoryNotes/index.htm. The 13 markets included in the CFTC supplemental index report include: CBOT SRW wheat, CBOT HRW wheat, CBOT corn, CBOT soybeans, CBOT soybean oil, CBOT soybean meal, ICE cotton, CME lean hogs, CME live cattle, CME feeder cattle, ICE cocoa, ICE sugar No. 11, and ICE coffee.

- 9.

See Cristiano and Naldi (2014) for an interesting analysis of Keynes’s own personal speculation in the cotton market as it relates to the theory of normal backwardation.

- 10.

As an aside note, it is not surprising that the insurance explanation behind backwardation appealed to Keynes as he was a director of the Provincial Insurance Company from 1923 until his death. It is also interesting that although he was well aware of the operations of different commodity markets as evidenced by (Keynes, 1923a), the only empirical information presented in (Keynes, 1923b) is a calculation based on cotton futures markets.

- 11.

- 12.

Not all hedgers are not short since there are commercial buyers of product in the market that have an incentive for hedging as well.

- 13.

As in Dusak (1973), Rjt is interpreted as net of the risk-free rate. In other words, it is interpreted as the risk premium on the spot commodity, i.e., Rjt - Rf, where Rf is the risk-free interest rate.

- 14.

- 15.

The t-values in Table 3 are based on heteroskedasticity-consistent standard errors.

- 16.

We tested the robustness of the results to different combinations of weights for the S&P and DJ&C indices, by computing the correlation of different weights. If we consider the series used for the estimation (50/50) the correlations with (90/10) is 0.9924 and with (75/25) is 0.9960. We therefore conclude that the results are robust to the choice of weights.

- 17.

The increased financialization did not occur just with commodity futures but as well with the introduction of tradable ETFs on commodities. However the ETF managers typically enter into the futures markets to offset their risk exposure to the ETF purchasers

- 18.

Since the graphs by contract show very similar patterns as the estimates of the pooled sample, we only present the parameters from the pooled sample. The disaggregated graphs are available from the authors upon request.

References

Bessembinder, H. (1992). Systematic risk, hedging pressure, and risk premiums in futures markets. The Review of Financial Studies, 5(4), 637–667.

Bhardwaj, G., Gorton, G. B., & Geert Rouwenhorst, K. (2016). Investor interest and the returns to commodity investing. The Journal of Portfolio Management, 42(3), 44–55.

Bhardwaj, Geetesh, Rajkumar Janardanan, and K Geert Rouwenhorst. 2019. The Commodity Futures Risk Premium: 1871–2018. Available at SSRN 3452255.

Cargill, T. F., & Rausser, G. C. (1972). Time and Frequency Domain Representations of Futures Prices as a Stochastic Process. Journal of the American Statistical Association, 67(337), 23–30.

Cargill, T. F., & Rausser, G. C. (1975). Temporal price behavior in commodity futures markets. The Journal of Finance, 30(4), 1043–1053.

Carter, C. A., Rausser, G. C., & Schmitz, A. (1983). Efficient asset portfolios and the theory of normal backwardation. Journal of Political Economy, 91(2), 319–331.

Chang, E. C. (1985). Returns to speculators and the theory of normal backwardation. The Journal of Finance, 40(1), 193–208.

Cootner, P. H. (1960). Returns to speculators: Telser versus Keynes. Journal of political Economy, 68(4), 396–404.

Cristiano, C., & Naldi, N. (2014). Keynes’s activity on the cotton market and the theory of normal backwardation: 1921-1929. The European Journal of the History of Economic Thought, 21(6), 1039–1059.

De Roon, F. A., Nijman, T. E., & Veld, C. (2000). Hedging pressure effects in futures markets. The Journal of Finance, 55(3), 1437–1456.

Dusak, K. (1973). Futures trading and investor returns: An investigation of commodity market risk premiums. Journal of Political economy, 81(6), 1387–1406.

Erb, C. B., & Harvey, C. R. (2006). The strategic and tactical value of commodity futures. Financial Analysts Journal, 62(2), 69–97.

Erb, C. B., & Harvey, C. R. (2016). Conquering misperceptions about commodity futures investing. Financial Analysts Journal, 72(4), 26–35.

Fama, E., & French, K. (1987). Commodity futures prices: some evidence on forecast power, premiums, and the theory of storage. Journal of Business, 60(1), 55–73.

Gorton, G., & Geert Rouwenhorst, K. (2006). Facts and fantasies about commodity futures. Financial Analysts Journal, 62(2), 47–68.

Gorton, G. B., Hayashi, F., & Geert Rouwenhorst, K. (2012). The fundamentals of commodity futures returns. Review of Finance, 17(1), 35–105.

Hamilton, J. D., & Wu, J. C. (2015). Effects of index-fund investing on commodity futures prices. International economic review, 56(1), 187–205.

Houthakker, H. S. (1957). “Can speculators forecast prices?” The Review of Economics and Statistics (pp. 143–151).

Just, R. E., & Rausser, G. C. (1981). Commodity price forecasting with large-scale econometric models and the futures market. American Journal of Agricultural Economics, 63(2), 197–208.

Kang, W., Geert Rouwenhorst, K., & Tang, K. (2020). A tale of two premiums: The role of hedgers and speculators in commodity futures markets. The Journal of Finance, 75(1), 377–417.

Keynes, J. M. (1923a). Special Memoranda on Stocks of Staple Commodities. London and Cambridge Economic Service, in CWK, 12, 267–647.

Keynes, J. M. (1923b). Some aspects of commodity markets. Manchester Guardian Commercial: European Reconstruction Series, 13, 784–786.

Main, S., Irwin, S. H., Sanders, D. R., & Smith, A. (2018). Financialization and the returns to commodity investments. Journal of Commodity Markets, 10, 22–28.

Marcus, A. J. (1984). Efficient asset portfolios and the theory of normal backwardation: A comment. Journal of Political Economy, 92(1), 162–164.

Rausser, G.C., and R. E. Just. 1979. “Agricultural Commodity Price Forecasting Accuracy: Futures Markets Versus Commercial Econometric Models.”

Rausser, G. C., & Carter, C. (1983). Futures market efficiency in the soybean complex. The Review of Economics and Statistics, 469–478.

Rausser, G. C., & Walraven, N. A. (1990). Linkages among commodity futures markets and dynamic welfare analysis. The Review of Economics and Statistics, 631–639.

Rockwell, C. S. (1976). Normal backwardation, forecasting, and the returns to commodity futures traders. In The Economics of Futures Trading (pp. 153–167). Springer.

Stoll, H. R., & Whaley, R. E. (2010). Commodity index investing and commodity futures prices. Journal of Applied Finance (Formerly Financial Practice and Education), 20(1).

Tang, K., & Xiong, W. (2012). Index investment and the financialization of commodities. Financial Analysts Journal, 68(6), 54–74.

Telser, L. G. (1958). Futures trading and the storage of cotton and wheat. Journal of Political Economy, 66(3), 233–255.

Author information

Authors and Affiliations

Corresponding authors

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2022 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this chapter

Cite this chapter

Carter, C.A., Revoredo-Giha, C. (2022). The Theory of Normal Backwardation and Financialization of the Futures Markets. In: de Gorter, H., McCluskey, J., Swinnen, J., Zilberman, D. (eds) Modern Agricultural and Resource Economics and Policy. Natural Resource Management and Policy, vol 55. Springer, Cham. https://doi.org/10.1007/978-3-030-77760-9_16

Download citation

DOI: https://doi.org/10.1007/978-3-030-77760-9_16

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-77759-3

Online ISBN: 978-3-030-77760-9

eBook Packages: Economics and FinanceEconomics and Finance (R0)