Abstract

The Russian banking system is relatively young compared to other countries because the RF inherited the banking system of the Soviet Union. Michail Gorbatchev’s perestroika program, under which the first commercial banks were formed, marked the beginning of a modern banking system in Russia. Since then, the financial system has undergone several reforms structured in the following periods.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

The Russian banking system is relatively young compared to other countries because the RF inherited the banking system of the Soviet Union. Michail Gorbatchev’s perestroika program, under which the first commercial banks were formed, marked the beginning of a modern banking system in Russia. Since then, the financial system has undergone several reforms structured in the following periods.

1988–1996 Initial Privatization

This initial stage was characterized by an explosive increase in the number of commercial banks. Russia’s first commercial bank under the symbolic name Union was registered by the state Bank of the USSR on August 24, 1988, in Chimkent (Kazakh SSR). Just 2 days later in Leningrad (now St. Petersburg), the Patent bank was registered (now called Viking). By 1991, there were 869 banks in the banking system. At the end of 1992, more than 2000 credit institutions had already been registered in the country. The maximum number of banks in Russia was observed in 1994, with 2439 banking organizations.

1997–1998 Reformation and Maturity

The young Russian banking sector faced its first crisis in 1997, which pushed many newly established banks that lacked qualified specialists and basic experience in the banking sector out of business. A year later, the Russian economy was hit even harder by the global financial crisis of 1998. The Russian government and the Russian Central Bank devalued the ruble, set a 90-day memorandum on external commercial debt payments, and eventually defaulted on its debt. The crisis had severe impacts on the entire Russian economy and is remembered as a major turning point in the country’s recent history. Even though the crisis sparked further reforms, which in the following years led to rapid economic growth, the crisis had a negative impact on the still young banking system. Banks with weak management, insufficient assets, and large volumes of government bonds went bankrupt. Many of them were comparably large banks, such as Menatep, SBS-Agro, and Incombank. A bank restructuring strategy was implemented which eventually led to a more oligopolistic structure with less strong players in the market.

1999–2009 Formation of Monopolistic Structures

Russia bounced back quickly from the financial collapse and the economy grew fast in the following decade. The Russian banking system continued to form oligopolistic, if not even monopolistic, structures. During this period, dozens of the largest private monopoly banks were formed, in the hands of which a significant part of the country’s banking assets is concentrated.

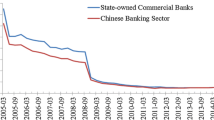

2009–2015 Strengthening of State Banks

This period saw the strengthening of state banks, primarily PAO Sberbank of Russia (Sberbank), Vneshtorg Bank (VTB), and Vnesheconombank. The growing importance of state-owned banks was due to the patronage of the state that became an important competitive advantage for them during the crisis. Clients preferred the reliability of state-owned banks to potentially volatile private commercial banks.

2016 Until Today: Further Consolidation

Recent years have seen a further consolidation of the banking sector through mergers, acquisitions, or liquidations of credit institutions. All these processes have has happened as the requirements from the Central Bank of the Russian Federation to banks have simultaneously toughened. The result of which has been a massive withdrawal of licenses from banks that do not comply with prudential requirements and standards from the regulator. Every year several dozen banks lose their licenses. As of March 2020, there are only 396 banks with valid licenses in Russia.

The Banking System Today

The banking system is not large enough in relation to the size of the Russian economy because the total assets of the banking system amounted to only 92% of GDP. From the structural point of view, the Russian banking system is two-tiered, as in most countries of the world. The first tier is a set of commercial banks and above them on the second tier is the Central Bank of the Russian Federation (CBR). The CBR is the main regulator of banking activity. The Central Bank enjoys powers beyond those typically found in other Western countries. In a way, a mega-regulator that performs a supervisory function over Russian credit institutions and in addition regulates foreign exchange markets, financial markets, and securities markets.

Another level of the banking system can be unofficially distinguished in Russia, which is formed by two state banks with a special status, namely Sberbank and VTB. In addition, another sub-level of banks can be considered as systemically important which means their stability ensures the stability of the entire banking system. These banks are Alfa-bank, Gazprombank, Credit Bank of Moscow, Russian Agricultural Bank, Promsvyazbank, Bank Otkritie, and the Russian subsidiaries of Unicredit, Rosbank (Societe Generale), and Raiffeisen bank. Among the above listed, five banks are under the direct control of the Russian state. These are namely: Sberbank, VTB, Russian Agricultural Bank, Otkritie Bank, and indirectly Gazprombank because it is controlled by the state-owned enterprise Gazprom . Only three banks (Alfa-bank, Credit Bank of Moscow, Promsvyazbank) are under private ownership while the three remaining banks are subsidiaries of large international financial groups (Unicredit, ROSBANK Societe Generale, and Raiffeisen). Banks that are considered as being of systemic importance are under greater control and need to fulfill higher mandatory standards than non-systemic institutions (Table 8.1).

A Strongly Nationalized System

Since 2004, Russia has installed a deposit insurance system that guarantees depositors a license from a commercial bank, the return of the deposit up to 1,400,000 rubles, in the event of revocation. This insurance is carried out through a specially created institute—Deposit Insurance Agency (DIA), which accumulates the insurance premiums of banks and makes payments to depositors of affected banks. For individuals, one cannot be afraid to open deposits within the insurance amount. For business, it is better to focus on banks with state participation, which seem more reliable in comparison with private banks.

In the Russian banking system, there is another feature that distinguishes local banks from foreign credit institutions. This is the lack of the practice of irrevocability of deposits in Russia. The Civil code of the Russian Federation allows citizens at any time to cancel the contract on bank deposits and withdraw money from the bank. It is important to note that the lack of irrevocability of deposits creates a competitive advantage for state banks and branches of foreign banks, as well as banks whose owners own large raw material assets.

The banking system in Russia is clearly nationalized. This is confirmed by the dominance of state and quasi-state banks as they account for up to 75% of all banking assets. Such a large share of state-owned banks corresponds to the ownership structure and the degree of concentration in the real sector of the Russian economy, in which state-owned enterprises occupy leading positions (Ivanter, 2017). When comparing Russian banks with firms in the real sector of the economy in terms of production, it turns out that these banks are too small in relation to enterprises in financial capabilities, and therefore cannot provide them with credit resources in the required amounts. The share of bank loans in total investments of Russian organizations in fixed assets for the period 2011–2015 varied between 8.4 and 10%. Currently, this share has remained practically unchanged (Mandron & Gutorova, 2016).

Recent Reforms and Trends

In 2018, the CBR introduced changes to the banking system that divided banks into two levels. The first level includes banks whose capital will be above 1 billion rubles. These banks operate under a universal license, i.e., they are allowed all types of banking operations. The second level comprises those banks whose owners are not able to produce 1 billion rubles of capital. Such banks are required to have a minimum capital of 300 mill. rubles and need to operate under a basic license, which implies restrictions on certain banking operations.

Currently, there is a change in the model of the banking business, which is moving to the so-called new reality. The latter term implies a stable, low inflation and further reduction of the key rate by the CBR. As a result, relatively low interest rates on loans and deposits will become the norm with the prospect of further reduction of the spread, i.e., the difference between the rates on deposits and loans (Dolzhenkov, 2017).

Tough measures on the part of the CBR are imposed on most banks that do not meet modern standards. Most commercial banks in Russia are captive banks, which were established by large corporations to lend to their own business. Accordingly, these banks have a narrow focus and are dealing only with a limited number of private or corporate clients. Under today’s conditions with increasing regulation by the CBR, many owners prefer to get rid of bank assets.

Outlook

What is troubling about the Russian banking system is the fact that it was established in a non-market economy. As a result, all banks in Russia are universal and can only be organized as joint-stock companies. The banking act does not authorize the creation of specialized, co-operative, or regional banks. That restriction deeply impoverishes the Russian banking system and limits its capability to structurally reflect the real sectors of the economy.

To sum up, the Russian banking system is still in a transitional phase. The main challenge is that it needs to resolve the double role of the Central Bank and the inherit problems that come with it. The Central Bank is the majority owner and supervisor of the largest Russian banks. It is difficult to imagine that it can fulfill both tasks without avoiding potential conflict of interests. In addition, further fundamental structural reforms are necessary with the objective to make the system more efficient and to have a more significant impact on stimulating the growth of the Russian economy.

References

Ivanter, A. (2017). The abolition of the syndrome. Expert, 40, 19. [Ivanter А. Sindrom otmeny. // EHkspert. 2017. №40. S.19.].

Dolzhenkov, A. (2017). Survive the “new normality”. Expert, 51, 44. [Dolzhenkov А. Perezhit' «novuyu normal'nost'» // EHkspert 2017. №51. S.44.].

Mandron, V. V., & Gutorova, A. A. (2016). Investment activity of Russian banks and problems of its implementation. The Young Scientist, 28, 486–491. Retrieved September 4, 2018, from https://moluch.ru/archive/132/37020/ [Mandron V. V., Gutorova А. А. Investitsionnaya deyatel'nost' rossijskikh bankov i problemy ee osushhestvleniya // Molodoj uchenyj. — 2016. — №28. — S. 486-491. — URL https://moluch.ru/archive/132/37020/ (data obrashheniya: 04.09.2018).]

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2021 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this chapter

Cite this chapter

Dubianskii, A.N. (2021). Russian Banking System. In: Medinskaya, O., Randau, H.R., Altmann, C. (eds) Russia Business. Springer, Cham. https://doi.org/10.1007/978-3-030-64613-4_8

Download citation

DOI: https://doi.org/10.1007/978-3-030-64613-4_8

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-64612-7

Online ISBN: 978-3-030-64613-4

eBook Packages: Business and ManagementBusiness and Management (R0)