Abstract

In this chapter, we aim to add to the literature that looks at the link between FDI, trade, and migration. In contrast to existing studies, we consider flows of capital, trade variables, and migrants across 16 destinations and 198 origin countries over 12 years (2000–2012). We distinguish between the flow of capital (FDI) and the flow of goods and services (trade). Our results show that migration is a main driver of FDI flows in our sample. We find that for a ten percent increase in migration this year, FDI flows next year will be roughly 5.7% higher. Further, the effect of migration on imports or exports is of similar magnitude. Overall, these findings support the results in the previous literature finding that migrant networks increase capital and trade flows. Further, once we deviate from a constant-elasticity model, we do not find evidence for non-constancy in the relationship between migration and FDI. The squared migration term that we include in our regression model is insignificant. This also holds for imports. However, for exports we find evidence for a non-constant elasticity. Overall, our results highlight the importance of immigration policies as a means to increase FDI and trade flows between countries.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

1 Introduction

Over the last couple of decades, the world has seen an increase in flows of capital (Foreign Direct Investment, FDI for short) and labour (migration). FDI flows in 2017 stand at $1.43 trillion according to the United Nations World Investment Report 2018, with the largest flows reported for developed economies ($712 billion) followed by developing countries ($671 billion). The United States experience the largest outflow ($342 billion) followed by Japan ($160 billion), and China ($125 billion). The average inward FDI return was 6.7%, where returns in developing countries, on average, were larger compared to developed countries (8 vs. 5.7%).

From the UN International Migration Report 2015 we can infer that 3.3% of the world’s population (roughly 250 million people) are migrants. Here, we use the UN Recommendations on Statistics of International Migration and define an international migrant as “[…] any person who changes his or her country of usual residence”. While the level is increasing, the report also documents that the rate of change is increasing. The UN report also documents that Europe and Asia are the two major areas of destination for international migrants. The top countries hosting migrants in 2015 were the United States, Germany, the Russian Federation, Saudi Arabia, and the United Kingdom. In some countries, the average annual rate of change was more than six percent. The average migrant in the world is male (52%), 39 years old, and comes from a middle-income country. Most migrants originate in Asia and Europe while Latin America and Africa are closing the gap.

In this chapter, we investigate the relationship between FDI flows, trade, and migration. There are various channels through which migration can, in theory, affect trade and FDI flows. First, immigrants moving to a country have specific tastes and demand a set of goods produced in their home countries. Hence, one can expect imports to the destination country to increase. Further, this effect should not change the volume of exports out of the destination country towards the origin country. Of course, there might be an offsetting substitution effect, where migrants in a given destination country start to produce these specific goods themselves (Girma and Yu 2002). Second, a key channel is that migrant (networks) reduce the trade costs between the destination and the origin country. Migrants, trivially, have better information of origin country markets, the language (esp. dialects), and business practices (incl. laws). Further, they form networks increasing the interconnectedness of countries. Along this line, we would expect the effect of reduced trade costs to be largest for very different destination–origin country pairs. This is due to the fact that the value of information is largest in this scenario.

We are, of course, not the first to look at these links. The early studies by Gould (1994), Rauch and Trindade (2002), and Rauch and Casella (2003) show how migrant networks can promote bilateral trade. Networks could increase the diffusion of knowledge (Jaffe et al. 1993), remove informational or cultural barriers (Kugler and Rapoport 2011), or better contract enforcement and taste similarities (Burchardi et al. 2018). Chaney (2014), for example, finds that French firms only export into markets where they have a contact. He then builds a network model of trade that fits the distribution of foreign markets accessed by firms in his sample. There are numerous further studies that establish a positive link between immigration and trade, as confirmed by Genc et al. (2012) in their meta-analysis of 48 empirical studies. For Sweden, Hatzigeorgiou (2010) find that immigration increase exports and imports, finding a stronger effect on exports. Interestingly, he provides evidence for the information channel by showing that the effect of migration is larger for differentiated goods than for homogeneous goods. Along this line, Fagiolo and Mastrorillo (2014) use a complex-network model of merchandise trade and find that the networks of migration and trade are strongly correlated. However, trade also depends on the relative embeddedness of a country in the complex web of corridors making up the networks.

The link between immigration and trade has also been established at the firm level. For example, Cohen et al. (2017) find that firms are more likely to trade with countries that have a larger resident population close to their firm headquarters. They use the location of WWII Japanese internment camps as an instrumental variable to identify a population shock. Bastos and Silva (2012) match historically determined emigration stocks with detailed firm-level data from Portugal, and find that larger stocks of emigrants in a given destination increase export participation and intensity. In addition, they show that the former of these effects tends to be more pronounced among firms that are more likely to have close ties with the emigrants. Parratto et al. (2016) use employer–employee matched data for the whole Danish population of firms (and workers) between 1995 and 2007, and find that on average more ethnically diversified firms perform better on the international market along all measures of market reach.

The literature on the link between immigration and FDI is, however, more recent and is not that well established. Burchardi et al. (2018) have shown that the ancestry composition in U.S. counties has an effect on FDI sent and received by firms. They argue that this is mainly driven by a reduction in information asymmetries. Lücke and Stöhr (2018) use panel data for OECD countries and find a robust positive impact of bilateral immigrants on FDI only if residents of the two countries have few language skills in common. Parsons and Vezina (2018) use a natural experiment to address the causation versus correlation issue. They use the outflow of Vietnamese Boat People to the United States. They find that after trade restrictions were lifted, 20 years after the refugee inflow, U.S. exports to Vietnam grew the largest in U.S. states with larger Vietnamese populations. Along this line, Javorcik et al. (2011) show that US FDI abroad is positively correlated with migrants from the origin country in the US. Similarly, Buch et al. (2006) find that German states with a large foreign population have higher stocks of inward FDI. Tong (2005) shows that Chinese networks increase FDI flows between South-East Asian countries and countries beyond.

Kugler and Rapoport (2007) considered the skill component of migration. They find that manufacturing FDI is negatively correlated with low-skill migration. However, FDI flows in the service and the manufacturing sector are positively correlated with high-skill migration. Felbermayr and Jung (2009) find positive effects of migration on trade, but show that this effect does not depend on education levels. In contrast, Gheasi et al. (2013) show that education matters for this relationship in the UK. More educated migrants create a stronger positive effect on FDI. Tomohara (2017) uses FDI data for Japan and finds that with increasing skilled immigration, FDI inflows become more dominant than imports.

In contrast to this literature, we consider flows of capital and migrants across a larger set of destination and origin countries over 12 years. Further, we investigate whether the elasticity of FDI flows with respect to migration depends on the number of migrants. We hypothesize that the size of the migrant flow, as it affects the stock of migrants, and therefore the size of the migrant network, could have a non-constant effect on capital flows. We argue that the diffusion of knowledge is faster and informational or cultural barriers are reduced by more when the migrant network becomes larger. We test this hypothesis using flows of capital and migrants between 15 OECD countries and 126 origin countries from 2000 to 2012.

We then distinguish between the flow of capital (FDI) and the flow of goods and services (trade). As argued by Benassy-Quere et al. (2007) FDI flows, in contrast to trade flows, are more sensitive to any form of uncertainty. This is due to the high sunk cost component in investing capital abroad. Therefore, we are interested in investigating whether drivers are similar or different across these two components of international cooperation.

Several results stand out. We find that migration is a main driver of FDI flows in our sample. The direct effect of migration on FDI is highly significant. We find that for a ten percent increase in migration this year, FDI flows next year will be roughly 5.6% higher. This lends support to the previous literature finding that migrant networks increase capital (and trade) flows. If we control for various other covariates, we find that the partial effect of migration is reduced but still significant. Here, we find that a ten percent increase in migration flows this year will increase FDI flows next year by 4.3%. Further, we do not find evidence for the impact of migration to depend on the size of migration flows. The squared migration term that we include in our regression model is statistically insignificant.

We then turn our attention away from the flow in capital (FDI) and correlate migration and the trade in goods and services (imports and exports). We find that the effect of migration on trade is of similar magnitude as its effect on FDI flows. While in the FDI case, a ten percent increase in migration increased FDI flows by roughly 5.6%, the increase is 6.3% for exports and 6% for imports. Finally, for exports we find that the immigrant elasticity of exports depends on the size of migrant flows in the form of an inverted U-shaped relationship. Such a relationship is not present in the case of imports.

The chapter is structured as follows. In the next section, we present our data set. Section 21.3 has a preliminary view at our data. We present our empirical approach in Sect. 21.4. Section 21.5 presents our empirical results and Sect. 21.6 briefly concludes.

2 Data

2.1 Migration Flows

One of our key variables is the migration flow (migration) from origin to destination country. The data for migration are taken from the work by Aburn and Wesselbaum (2017). They have 16 OECD destination countries and 198 origin countries over the period from 1980 to 2015. The time period and choice of destination countries are dictated by data availability.

Migration flows are taken from the 2015 Revision of the United Nations’ Population Division and are combined with data from the OECD. As usual in the migration literature, this data set only covers regular, permanent migration. This implies that the data set excludes illegal immigration. This will likely lead to an underestimation of the true migration flows.

Although this data set has more than 80,000 observations, we can only use 35,062 of them in our analysis due to the data availability of other variables that need. This gives us a migration data set that only contains about 10% zero migration flows.

Our migration data are annual. Other papers in the literature use decennial time observations rather than annual migration flows (e.g. Kugler and Rapoport 2011). The advantage is that they can use a larger set of bilateral country pairs. However, the flip side is that these data sets contain a much larger number of zero flows. Further, the small number of time observations ignores year-to-year variations, especially important for the estimation of the effects of short-term fluctuations. This could be important given the large sensitivity of capital flows.

2.2 FDI Flows

Our FDI data come from Feng et al. (2018). They are one-way FDI outflows from 172 origin countries to 169 destination countries in millions of US$ that are available from the UNCTAD database. The data cover the years from 2001 to 2012. Of the FDI data, 33% are zeros, and about 18.6% are negative values.

2.3 Trade Data

Trade (exports and imports) data are obtained from UNSD’s COMTRADE database through World Integrated Trade Solution (WITS), and are in thousands of US$.

2.4 Covariates

All the covariates are standard gravity variables which are obtained from the Dynamic Gravity Dataset that has recently been developed (Gurevich and Herman 2018). This dataset is constructed in such a way that many standard gravity variables exhibit more variation in time and magnitude. The distance variable, for example, reflects the distance between pairs of cities by incorporating the proportion of the country’s population residing in each city, making distance a time-varying variable.

We use distance as a proxy for migration and trade costs. It is the population-weighted average of city-to-city bilateral distances in kilometres between each major city in the origin and destination countries. This definition of distance more accurately captures the distance economic activity must travel between two countries (Gurevich and Herman, The Dynamic Gravity Dataset: Technical Documentation Version 1.00). Further, we consider three dummy variables that proxy cultural closeness between countries. First, we use a border dummy (Contiguity), which is one if the country-pair shares a border. For various reasons (German reunification in 1990 and independence of Czech Republic, Slovakia, and Slovenia in the early 1990s) the border dummy is time-varying. Second, we use a common language dummy. The dummy for language is one, if a country-pair has the same official language. Finally, a dummy picking up post-1945 colonial ties (Colony). This dummy is one if the origin country was a colony of the destination OECD country for at least one year after 1945.

Finally, as a trade facilitation variable, we use a dummy variable (agree_pta) that equals one if the origin and destination countries are engaged in a preferential trade agreement of any type within a given year.

We had data on population and GDP as well, but these variables could not be included in the regression models due to collinearity in any of the models we estimated.

3 A Preliminary View at the Data

In this section, we want to have the first, preliminary view at our data set. Although our migration dataset contains 198 origin countries and 16 OECD destination countries, we end up with 126 origin countries and 15 OECD destination countries when we merge it with the FDI data.Footnote 1 Merging it with trade data gives us 97 origin countries for exports and 144 origin countries for imports.

Table 21.1 presents the descriptive statistics of our key variables. The average FDI flows are about 600 million US$ when negative flows are ignored. The average number of migrants is about one and half million. About 2% of the country pairs share a common border, and 14% have the same official language. About 22% of the country pairs are engaged in some type of a preferential trade agreement in a given year.

Figure 21.1 plots migration flows over time in our sample. We plot the total annual migrant inflows into all our destination countries coming from the 126 origin countries. There is a clear trend of increasing migration over the entire sample period. This includes a sharp peak in 2007, just before the Global Financial Crisis in 2008.

Migration flows over time

Figure 21.2 presents total FDI flows in our sample over time. We again observe a sharp peak in 2007 just before the Global Financial Crisis. The pattern the graph displays is very similar to the pattern displayed in the plot of migrant flows. However, the drop in FDI flows after the GFC is much sharper compared to the drop in migrant flows.

Total FDI flows in our sample

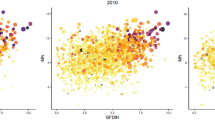

In Fig. 21.3, we show a scatter plot of migration versus FDI flows. In order to gain some intuition for out later analysis, we also plot a simple linear regression line (in red). We find a positive correlation between migration and FDI. This is as expected given the theoretical insights and the previous literature we discussed. It indicates that there is a relationship between migration and FDI. We also ran a quadratic regression to investigate the presence of non-linearity in the relationship, but the difference between the linear regression line and the obtained quadratic form was negligible.

Scatter plot of log migration versus log FDI

4 Empirical Approach

We construct a standard gravity model to investigate the relation between FDI and migrant flows, and also to investigate the relationship between trade and migrant flows. Gravity models have been used extensively in the literature for both trade flows and FDI flows. Although gravity models have traditionally been employed as linear models with log-transformed dependent variables, it is now widely recognized that more care needs to be taken due to the presence of many zeros in the observed values of the log-transformed variables. This is in fact the case in our analysis as 33% of the FDI flows are zeros in our sample.

Following the approach advocated by Silva and Tenreyro (2006) and recommended by Yotov et al. (2016), we estimate the gravity model in its multiplicative form by using a Poisson estimator known as the Poisson pseudo-maximum-likelihood (PPML) estimator. Thus, we estimate the simple gravity equation

where \(i,j,\) and \(t\) are indices for origin, destination, and time. The vector \(\varvec{X}\) contains migration flow, the main variable of interest, and the standard gravity variables as control variables. The terms \(\lambda_{it} ,\psi_{jt} ,\eta_{ij}\) represent the origin-time, destination-time, and origin–destination (pair) fixed effects, and \(\varepsilon_{ijt}\) is the standard error term. The dependent variable, \(y_{ijt}\), is either FDI flow or exports or imports, in levels.

This is a three-way fixed effects model with time-varying origin and destination fixed effects and time-invariant pair fixed effects. Computational issues with large samples such as ours have made it difficult to estimate such models for a long time, but Larch et al. (2019) have introduced an iterative PPML estimator that makes it possible to estimate these “high-dimensional fixed effects (HDFE)” models. We use their Stata command ppml_panel_sg to estimate the model (Zylkin 2017).

We are mainly interested in the impact of migration on the dependent variable in the equations we estimate. We take the logarithm of migration flow, and, in order to reduce the problem of endogeneity, we use its lagged value in the regression. Thus, its coefficient can be interpreted as an elasticity.Footnote 2

The gravity control variables GDP, population, and distance enter our model after taking their logarithms. The remaining control variables described before enter as dummy variables.

5 Empirical Results

-

a.

FDI and Migration

Table 21.2 presents our estimation results. Model (1) presents the direct or total effect of migration on FDI flows in our sample. Here, we find a significant positive effect of migration on FDI. For a ten percent increase in migration flows, we would observe an increase of 5.7% in FDI flows. Notice that we are using lagged migration. Therefore, the interpretation slightly needs to be adjusted. For a ten percent increase in migration this year, FDI flows next year will be 5.7% higher. This also documents the persistence effect in the migration-trade relationship. This could be explained by network effects (Kugler and Rapoport 2011). Once migrants arrive, they need time to settle-in, where an existing migrant network would help. In general, such an existing migrant network would reduce the cost of migration. Related to trade, this implies that if migrants move from origin country i to designation country j, the network generated between the two countries ij will lead to a reduction in trade costs and, therefore, will create an incentive to do more business. We find this effect in our regression with an increase in FDI flows of about 5.7%.

Model (2) adds control variables that allow us to see whether the effect of migration also works through other channels and to address the unobserved variable bias. Of course, now our parameter estimate for migration will only indicate an indirect, or partial effect, of migration on FDI flows. Our regression shows that the effect of lagged migration on FDI is still significantly positive but smaller in magnitude compared to the direct (total) effect. Here, we find that a ten percent increase in migration flows this year will increase FDI flows next year by 4.3%. Distance, as expected, has a statistically significant impact on FDI flows. Colonial ties are found to have a negative impact. The remaining gravity variables have not been found to have a statistically significant effect.

Model (3) includes the square of logged lagged migration. Here, we test whether the migration elasticity of FDI flows would vary with the size of the migrant network, a hypothesis that a priori appears intuitive. However, we do not find evidence for this hypothesis in our data set. The squared migration term is statistically insignificant. The coefficient of lagged migration is significant again, and its magnitude is as high as it was with no other controls.

In conclusion, we find that migration does significantly affect FDI flows. For a ten percent increase in migration this year, FDI flows next year will increase by about 5.7%. Our findings support the results by others in the related literature that migrant networks can increase capital flows and business opportunities. The literature starting with Gould (1994), Rauch and Trindade (2002), and Rauch and Casella (2003) argue that migrant networks would increase bilateral trade. We find support for their results by showing that migration increases capital flows. Our results are in line with the findings by Javorcik et al. (2011) that show that US FDI abroad is positively correlated with migrants from the origin country in the US. They find that a 1% increase in the migrant stock increases the FDI stock by around 0.5%. Similarly, Buch et al. (2006) find that German states with a large foreign population have higher stocks of inward FDI. Tong (2005) shows that Chinese networks increase FDI flows between South-East Asian countries and countries beyond. We add to these papers by considering a larger cross-country panel.

When it comes to the mechanisms through which migration could affect FDI flows our results are silent. However, drawing from the work by Jaffe et al. (1993) and Kugler and Rapoport (2011), we could argue that migrant networks on the one hand increase knowledge diffusion and remove informational or cultural barriers.

At the end of this section, we want to emphasize some shortcomings of our study. The biggest concern is that our regression suffers from endogeneity bias. We tried to mitigate this problem by using lagged migration, but a better approach would be to use a proper instrumental variable approach. We were thinking about using natural disasters at an instrument. However, whether the exclusion restrictions hold is a difficult question.

-

b.

Is Trade Different?

In the previous section, we considered FDI flows. FDI flows, by definition, are different from trade as they measure financial capital rather than the trade of goods and services. In this section, we want to repeat our previous empirical approach, but use a trade variable.

Table 21.3 present our estimation results using imports at origin countries as dependent variable.

As before, we start with the direct effect of lagged migration on imports. We find that the effect is highly significant. For a ten percent increase in migration flows, we find an increase in the import value of 6%. This effect is similar in magnitude to the effect on FDI flows, which was about 5.7%. Next, model (5) controls for other covariates. Controlling for other variables reduces the impact of migration considerably. A ten percent increase in migration flows is now associated with a 1.5% increase in imports. As it was the case with FDI flows, the coefficient of the squared logged lagged migration is not statistically significant, implying that the constant-elasticity model is appropriate. Adding this squared term does not have any significant effect on the magnitude and statistical significance of the coefficients.

All the gravity variables have the expected signs, and all, apart from common language dummy, are statistically significant. Only the coefficients of logged distance and colony dummy variable were statistically significant in the estimation equation for FDI flows. Engaging in any type of a preferential trade agreement is found to have a positive effect on imports. (Such engagement is predicted to increase imports by about 23.5%, on average.) Having colonial ties has a very significant impact, increasing imports by about 52%, on average. A common border, on the other hand, increases imports by about 25%.

So far, we considered import value as a dependent variable, as a proxy variable of trade. We want to see whether the results are robust to using a different measure of trade: the export value. Table 21.4 presents our estimation results.

The results are similar to the ones obtained for import values. The main difference we find is that for exports, the coefficient on the squared logged migration flow is positive and statistically significant. This implies that the immigrant elasticity of exports is not constant and it varies with the size of migrant flows. The positive coefficient on this variable means that the marginal benefits from migration are larger for exports for higher levels of migration flows.

The magnitude of the effect of migrant flows on exports is of similar magnitude found for imports. The impact of being engaged in a preferential trade is found to have a very large impact on exports, about 79% increase on average. The impacts of having a common border and engaging in a preferential trade agreement are slightly larger for exports; 38% and 31%, respectively. The elasticity of exports with respect to distance is, however, much smaller compared to imports.

Overall, we can conclude that contiguity and free trade agreements are not associated with FDI flows, but they have an impact on trade. Speaking a common language, the way it is defined here, is not found to have an impact on FDI flows or trade. Most importantly, migration flows are found to be associated with both FDI flows and trade. The constant migration elasticity model is found to be valid for FDI flows and imports, but not for exports.

6 Summary and Conclusion

This chapter is motivated by the observed dynamic in flows of capital (Foreign Direct Investment, FDI for short) and labour (migration) over the last couple of decades that the world has seen. We investigate the relationship between FDI flows, trade, and migration.

We add to a growing literature that looks at the link between FDI, trade, and migration.

In contrast to the existing literature, we consider flows of capital, trade variables, and migrants across a larger set of destination and origin countries over 12 years (2000–2012). First, we investigate the relationship between migration flows and FDI flows as well as the relationship between migration and trade. We then investigate whether migration elasticity of FDI flows and trade is constant. Our idea is that the size of the migrant flows, as it affects the stock of migrants over time, can have a non-constant effect on capital flows and trade volumes. In line with the mechanisms discussed earlier, we argue that the diffusion of knowledge could be faster and informational or cultural barriers could be reduced by more, when the size of the migrant network increases. We test this hypothesis using flows of capital, trade, and migration between 16 OECD countries and 126 origin countries for FDI flows and 97 origin countries for trade flows from 2000 to 2012.

Our findings can be summarized as follows. We find that migration and previous colonial ties are important drivers of FDI flows in our sample. Contiguity and preferential trade agreements are also found to contribute to trade flows. The direct effect of migration on FDI is highly significant. We find that for a ten percent increase in migration this year, FDI flows next year will be roughly 5.7% higher. If we control for various other covariates, we find that the partial effect of migration is slightly reduced, but still significant. We find that a ten percent increase in migration flows this year will increase FDI flows next year by 4.3%. Further, the effect of migration on imports or exports is of similar magnitude when no other variable is controlled for. However, the impact is found to be much smaller when gravity variables are included in the regressions. Overall, these findings support the results in the previous literature finding that migrant networks increase capital and trade flows.

Further, once we deviate from a constant-elasticity model, we do not find evidence for non-constancy in the relationship between migration and FDI. The squared migration term that we include in our regression model is insignificant. This also holds for imports. However, for exports we find evidence for a non-constant elasticity.

When we look at the other covariates in our regression, we find that both colonial ties and distance reduce FDI flows. For a ten percent increase in population-weighted distance between the pairs of countries, FDI flows will be reduced by roughly 3.6%. The reduction in trade flows is much larger for trade, 9.3% for imports and 5.7% for exports. Colonial ties are found to have a positive impact on trade flows. Preferential trade agreements and contiguity are also found to be positively associated with trade volumes.

Overall, our results highlight the importance of immigration policies as a means to increase FDI and trade flows between countries. There are benefits to be received from encouraging immigration and engaging in preferential trade agreements.

Notes

- 1.

These OECD countries are Australia, Austria, Belgium, Canada, Denmark, Finland, Germany, Italy, Netherlands, New Zealand, Norway, Spain, Sweden, Switzerland, UK, and USA. Belgium is not included in the FDI dataset.

- 2.

Some of the values for migration flows are zeros, 2.42% in analysing FDI flows and 10.4% in analysing trade flows. We considered using the inverse hyperbolic sine (IHS) transformation, which retains zeros, as suggested by Burbidge et al. (1988). This transformation assigns zeros to observed values of zeros. We instead assigned zeros to the logarithm of zero migration flows just as HIS transformation would, equivalent to changing zeros to ones before taking the logarithm. We compared our results to the results obtained with HIS transformation. They were almost identical.

References

Aburn, A., & Wesselbaum, D. (2017). Gone with the wind: International migration. Otago Discussion Paper.

Bastos, P., & Silva, J. (2012). Networks, firms, and trade. Journal of International Economics, 87(2), 352–364.

Benassy-Quere, A., Coupet, M., & Mayer, T. (2007). Institutional determinants of foreign direct investment. The World Economy, 30(5), 764–782.

Buch, C. M., Kleinert, J., & Toubal, F. (2006). Where enterprises lead, people follow? Links between migration and FDI in Germany. European Economic Review, 50, 2017–2036.

Burbidge, J. B., Magee, L., & Robb, A. L. (1988). Alternative transformations to handle extreme values of the dependent variable. Journal of the American Statistical Association, 83(401), 123–127.

Burchardi, K., Chaney, T., & Hassan, T. (2018). Migrants, ancestors, and foreign investments. Review of Economic Studies, 0, 1–39. https://doi.org/10.1093/restud/rdy044.

Chaney, T. (2014). The network structure of international trade. American Economic Review, 104(11), 3600–3634.

Cohen, L., Gurun, U. G., & Malloy, C. (2017). Resident networks and corporate connections: Evidence from World War II Internment Camps. Journal of Finance, 72(1), 207–248.

Fagiolo, G., & Mastrorillo, M. (2014). Does human migration affect international trade? A complex-network perspective. PLos ONE, 9(5).

Felbermayr, G. J., & Jung, B. (2009). The pro-trade effect of the brain drain: Sorting out confounding factors. Economics Letters, 104(2), 72–75.

Feng, X., Lin, F., & Sim, N. C. S. (2018). The effect of language on foreign direct investment. Oxford Economic Papers, 1–23.

Genc, M., Gheasi, M., Nijkamp, P., & Poot, J. (2012). The impact of immigration on international trade: a meta‐analysis. In P. Nijkamp, J. Poot, & M. Sahin (Eds.), Migration impact assessment (pp. 301–337). Cheltenham: Edward Elgar.

Gheasi, M., Nijkamp, P., & Rietveld, P. (2013). Migration and foreign direct investment: Education matters. The Annals of Regional Science, 51, 73–87.

Girma, S., & Yu, Z. (2002). The link between immigration and trade: Evidence from the UK. Weltwirtschaftliches Archiv, 138, 115–130.

Gould, D. (1994). Immigrants links to the home countries: Empirical implication for U.S. bilateral trade flows. Review of Economics and Statistics, 76(2), 302–316.

Gurevich, T., & Herman, P. (2018). The dynamic gravity dataset: 1948–2016. USITC Working Paper 2018-02-A.

Hatzigeorgiou, A. (2010). Does immigration stimulate foreign trade? Evidence from Sweden. Journal of Economic Integration, 25(2), 376–402.

Jaffe, A. B., Trajtenberg, M., & Henderson, R. (1993). Geographic localization of knowledge spillovers as evidenced by patent citations. The Quarterly Journal of Economics, 108(3), 577–598.

Javorcik, B. S., Özden, C., Spatareanu, M., & Neagu, I. C. (2011). Migrant networks and foreign direct investment. Journal of Development Economics, 94(2), 151–190.

Kugler, M., & Rapoport, H. (2011). Migration, FDI, and the margins of trade. CID Working Paper, No. 222.

Kugler, M., & Rapoport, H. (2007). International labor and capital flows: Complements or substitutes? Economics Letters, 94(2), 155–162.

Larch, M., Wanner, J., Votov, Y. V., & Zylkin, T. (2019). Currency unions and trade: A PPML re-assessment with high-dimensional fixed effects. Oxford Bulletin of Economics and Statistics, 81(3), 487–510.

Lücke, M., & Stöhr, T. (2018). Heterogeneous immigrants, exports and foreign direct investment: The role of language skills. World Economics, 41, 1529–1548.

Parrota, P., Pozzoli, D., & Sala, D. (2016). Ethnic diversity and firms. European Economic Review, 89, 248–263.

Parsons, C., & Vezina, P.-L. (2018). Migrant networks and trade: The Vietnamese boat people as a natural experiment. Economic Journal, 128(612), F210–F234.

Rauch, J. E., & Casella, A. (2003). Overcoming informational barriers to international resource allocation: Prices and ties. Economic Journal, 113(484), 21–42.

Rauch, J. E., & Trindade, V. (2002). Ethnic Chinese networks in international trade. Review of Economics and Statistics, 84(1), 116–130.

Silva, S. J., & Tenreyro, S. (2006). The log of gravity. Review of Economics and Statistics, 88(4), 641–658.

Tomohara, A. (2017). How does immigration affect modes of foreign market access: Trade and FDI? Applied Economics Letters, 24(18), 1280–1284.

Tong, S. Y. (2005). Ethnic networks in FDI and the impact of institutional development. Review of Development Economics, 9(4), 563–580.

Yotov, Y. V., Piermartini, R., Monteiro, J.-A., & Larch, M. (2016). An advanced guide to trade policy analysis: The Structural gravity model. Geneva: WTO.

Zylkin, T. (2017). PPML_PANEL_SG: Stata module to estimate “Structural Gravity” models via Poisson PML. https://ideas.repec.org/c/boc/bocode/s458249.html.

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2021 The Author(s), under exclusive license to Springer Nature Switzerland AG

About this chapter

Cite this chapter

Genç, M., Wesselbaum, D. (2021). The Impact of Immigration on Foreign Market Access: A Panel Analysis. In: Kourtit, K., Newbold, B., Nijkamp, P., Partridge, M. (eds) The Economic Geography of Cross-Border Migration. Footprints of Regional Science(). Springer, Cham. https://doi.org/10.1007/978-3-030-48291-6_21

Download citation

DOI: https://doi.org/10.1007/978-3-030-48291-6_21

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-48290-9

Online ISBN: 978-3-030-48291-6

eBook Packages: Economics and FinanceEconomics and Finance (R0)