Abstract

There were two major bureaucracy reduction programs in Hungary that aimed at the digitization of public administration. The expected benefits of digitization are operations that are more efficient and of a higher level of services. Results of these programs are limited, partly due to the simple support of the existing processes with information technology. The paper proposes a data-centric process design methodology that builds on artifacts as a modeling concept. It is argued and shown based on an example that starting from the expected final artifact of a process and applying a systematic approach, better results can be achieved than with the traditional process-based modelling approach.

Access provided by Autonomous University of Puebla. Download conference paper PDF

Similar content being viewed by others

Keywords

1 Introduction

Digital transformation (or digitization) is considered to be of prime importance for Hungarian society. Total digitization of public administration is amongst the long-term objectives [1], besides the implementation of the necessary infrastructural elements (e.g., a high-speed countrywide network) [2]. The expected general benefits of digitization are operations that are more efficient and of higher level of services. Digitization does not mean purely supporting an existing process with information technology but it might also change the process itself. In public administration, there has always been a temptation to simplify the digitization process to the mechanical transcription (imitation) of traditional paper processes. That was exactly the approach taken in Hungary. Today, a number of formerly paper-based applications can now be also submitted by electronic means (the general-purpose form filling program ÁNYKFootnote 1, and the “e-paper”Footnote 2) but this enhancement did not lead to significant changes in the way how our society operates. There are now about 8.3 million citizensFootnote 3 who are entitled to conduct business with the public administration authorities in Hungary. In order to contact the authorities, one needs a so-called Client Gate. The Client Gate is a free service provided by the state that authenticates its owner and provides storage for the owner’s electronic documents [3, 4]. A citizen should register by personal appearance to get his Client Gate. The number of registered persons peaked at 3.8 million in 2019 January, which is significantly less than the number of entitled citizens.

Hungarian enterprises are obliged by law to conduct their affairs with the public authorities almost exclusively by electronic means, that is, the person who acts on behalf of the enterprises is expected to use his Client Gate for that purpose [5]. The number of Hungarian enterprises fluctuated around 1.7 millionFootnote 4 in 2016–2018. If we compare this number to the number of individual Client Gate visitorsFootnote 5 (see Fig. 1), however, it becomes clear that the Client Gate is used much less than it could have been in principle. This indicates that the implementation of digital transformation is not a success story and we believe that one of the potential impediments is the formal digitization approach pursued in Hungary. We are going to support this statement with examples in the next section.

Number of individual Client Gate visits

There has been a permanent on-going reorganization within the Hungarian public administration since 2010, too [3, 4, 6]. The previously used guiding principle was sectorial affiliation, which was replaced by a county-based approach. The reorganization resulted in 20 Government Offices, one for each county [7, 8]. Due to this reorganization, financial data from different years of the public administration authorities is not comparable, and it not possible to measure the direct financial effect of digitization.

An increase in efficiency - which could be measured by the costs of operations - is often expected from digitization as well. Personnel costs is the largest item in the operational costs of Hungarian public administrationFootnote 6, and because of the fixed salary rules, the fluctuation in the total number of civil servants is a proper indicator for changes in efficiency as no major new public administration tasks were initiated in this period. The time line of the total number of civil servants until the end of 2018 shows a significant decrease at the end of 2017 (see Fig. 2). At that time, however, there was no significant digitization action, but a reorganization process took place. Central sectorial offices were dismissed, all the administrative procedures were integrated into the County Offices [8]. This led to considerable cuts in central and functional (finance, procurement etc.) staff.

Total number of Hungarian civil servants (http://www.ksh.hu/docs/hun/xstadat/xstadat_evkozi/e_qli006.html)

We conclude that the use of information technology (that was equated to digitization) plays a limited and formal role in the development of the Hungarian public administration and it did not significantly contribute to the improvement in efficiency. We need more profound actions for a quality change.

2 Problem Statement and Literature Overview

The fact, that public administration in its current form is an excessive burden on Hungarian society, which must be reduced for the sake of competitiveness, was already recognized a long time ago in the Hungarian government. In the course of the reform of Hungarian public administration, two major bureaucracy reduction programs have been implemented since 2010 [3, 4]. In these programs the ongoing administrative processes were reviewed and reorganized. A typical public administration process now looks as depicted in Fig. 3, which should be interpreted for each individual case type. Specific detailed rules are defined by the type of the case concerning the scope of the data to be provided in the application, the documents to be submitted and the required certificates. It is simpler, for instance, when no decision has to be made (e.g. handling of notices of data).

A typical Hungarian public administration process

The quint-essential elements in Fig. 3 from the point of processing are

-

1.

what the client is expected to prove and

-

2.

whether the application requires a decision made by the authority (e.g. authorization or granting permission) or it is simply an official acknowledgment (acceptance of a notification).

In the above mentioned bureaucracy reduction programs, jurists reviewed public administration processes. Their review focused primarily on reducing the types and numbers of required authorizations, shifting towards acknowledgment. In addition, instead of an official proof for data submitted by the client, a mere declaration of proof became often enough in the revised process.

By doing so, the workload of the clients was reduced but the efficiency improvement on the social level is at least debatable. Even though the length of time since the introduction of the new system is still too short to draw conclusions, some problems can already be perceived in the absence of missed preparatory impact assessments. We would like to present the process of a construction permit for a family house [9] as an example.

Right now, there is essentially no need for a construction permit for a family house in Hungary. The administrative (legal) procedure – even for the occupancy permit - is a mere notification, which means that the former professional control of the state essentially ceased to exist. This is a significant relief for the construction authority. However, construction rules still do exist, so compliance checks and responsibility for potential problems related to the family house were devolved to the architect of the house: This responsibility is obviously reflected in the payment for the architect, which means that the financial burden on the client has significantly increased.

In addition, litigation (for example with neighbors) could have been dealt with during the permission phase of the original process. Now, disputes have been transferred to the judiciary system, resulting in greater costs for all parties. In order to avoid litigation, the proportion of informal consultations, for example, with local governments has increased significantly.

In summary, the reviewed and reorganized process of obtaining a construction permit resulted in more of an overload rather than a reduction in the tasks of construction authorities. Similar problems may occur due to lifting of the requirement of proof for the correctness of the submitted data. The costs incurred due to the control, abuse and the ex-post sanctioning procedures may even exceed the work saved in the filing.

The review did not take into consideration the possibilities of simplification and support provided by information technology, so it did not result in a substantial change in the administrative services provided. All these indicate the need for a more systematic, methodologically sound review that takes into consideration the existing and possible IT-support of sub-processes, instead of having ad-hoc reviews that are carried out from a purely legal point of view, so as to have a positive impact of digitization on public administration. Our research objective was to contrive an improved process design approach that might provide better results in terms of efficiency.

However, any approach should consider the specialties of public administration. The controversial result of the previous bureaucracy reduction programs shows that a process-focused review itself is not sufficient to optimize the complex system of public administration. The reason for the mistake is that the development of the public administration was “stuck” to the process-based approach (which dominated the Hungarian public administration from the beginning of the 20th century). The process-based approach starts with the established types of cases, which does not allow for revealing their broader connections and for reaching higher abstraction levels.

Different methods of reviewing (improving) processes in the literature have been discussed in detail for a long time [10,11,12,13]. Most methods start from an existing process and focus on their redesign, using simpler processes.

The process centricity of current public administration development approaches can be perceived not only in practice, but in the literature, too. A typical example is the work of Punia and Saxena who focus on advancing with the retention of the traditional administrative institutional structure [14].

The process-based approach makes it difficult not only to improve efficiency but also to implement a “one-stop-shop” service model that is now widely accepted in public administration as an improvement. The importance of the one-stop-shop is pointed out in the literature [15]; the EU has made it mandatory for cross-border services in the 2006/123/EC Directive (the Internal Market Directive).

It should be noted that there is a significant difference between the client-side and the core-public administration interpretation of the “one-stop shop” concept. In the practice of the profit-oriented sector (primarily in financial institutions) single-window administration is actually a “transactional” administrative action, such as cash withdrawal or depositing, or even opening an account with the agent (or electronic interface) immediately. On the other hand, the Hungarian public administration (and the one-stop administration) has stalled at the launching of the processing of a case. While the profit-oriented sector focuses on the one stop service, and the literature even deals with the conditions for a “no-stop shop” service [16], in the Hungarian public administration only the beginning of the process is to be integrated - due to its process-centered attitude. This also indicates that the review of the processes should be different in the future.

The need for re-thinking the process of switching to digitized operations was discussed in the literature under the term of Business Process Reengineering (BPR). Stemberger and Jaklic review and propose methodological approaches to change processes in eGovernment development [12]. They examine business process change (BPC) methodological issues and build on the seven-stage phase-activity framework model proposed by Kettinger, Theng and Guha [17]. The stages of their framework are (1) Envision, (2) Initiate, (3) Diagnose – as-is model, (4) Redesign – to-be model, (5) Reconstruct and (6) Evaluate.

This approach is in line with the process-based approach of review and at the substantive step it relies on the use of “creative” methods, but the original process still limits the scope for action.

Process description techniques have also evolved meanwhile. The enhanced models typically use a more formalized technique (for example “hypergraphs”, [18, 19]). The new techniques can support automation better, but they are hardly suitable for understanding and modelling the complex legal, sociological, social policy, information technology and economic aspects. Still these techniques put the process into focus, and in public administration, the closeness of the concept of ‘case type’ delimits the opportunities for redesign. One must find such a design methodology that goes beyond the process review of the current case type (higher abstraction level) and, at the same time, is capable of accommodating the concepts of different fields of expertise.

3 The Reverse Data-Centric Process Design Approach

The limitations of the process-based approach and the related review methods were recognized in the literature and the so-called data-centric approach was proposed as an alternative. This methodological approach, suggested by IBM researchers, allows for the introduction of new concepts and looks at the process from another perspective [21, 22]. It builds on the concept of “business artifact”. An artifact corresponds to key (real or conceptual) business entities that should be managed. It can be an object or a set of information in the context. Cohn and Hull argued that “the artifact abstraction provides a vehicle for understanding the interplay between data and process in ways not supported by previous Computer Science abstractions”. ([20] pp. 7) Cohn and Hull also claim that the artifact-centric approach makes the separation of the logical and the physical design concerns possible.

Bhattacharya, Hull-and Su propose a four-step data-centered model design methodology that is based on two principles, as

-

1.

“data first”, which requires that at each step, data consideration, specification, and design should precede that of any other component; and

-

2.

“data centered”, which means that the specification and design of tasks and workflow should be formulated using the data design obtained at each step.

In the first step of this methodology, one should identify the artifacts, which means that it does not start with mapping activities. Having done that, the life cycles of the artifacts should be discovered. The second step is to develop a detailed logical specification of the data needed about the artifacts, the services that will operate on the artifacts and the linkages (associations) between the services and the artifacts. Services and associations should be described using pre-conditions and conditional effects for the services as well as Event-Condition-Action (ECA) rules for the associations. The third step is to map this description into a more procedural specification, and in the final fourth step the workflow may be realized [21]. The methodology is summarized in Table 1.

The data-centric design seems to be an applicable method for optimizing public administration processes, but the differences between the problems of profit-oriented activities and the problems of public administration have to be taken into account. In the profit-oriented world, both processes and related data have little hidden connections (buyer, vendor, contract, etc.). They are simpler, so they can be handled more individually from the point of digitization.

Both in the process-based and in the data-centric process design proceed in time order, which means, starting at the initial state. The forward-proceeding data centric methodology applied in the context of public administration would not mean a qualitative change. It would start at the initial artifact, that is, at the application and by the end of its processing, it would reach the final artifact, the decision. This approach cannot go beyond the limitations stemming from the logic of the existing case type.

We propose to start the design of a process at the final state, that is, to begin at the final state or the artifact of a case type. Grove also proposed starting from the output in a general sense, but he did not use the artifact concept [22]. We call this the “reverse data centric process design” approach and we shall show how to do it with help of an example in the next section. We are going to demonstrate that this approach may provide a higher abstraction level that can be interpreted by all actors involved in public administration.

Some examples of final artifacts are tax that has been collected; an inhabited family house or a family that was given social benefit. Having identified an artifact, you also need to determine whether it is of active or passive nature. An active artifact may be an actor to whom tasks can be assigned (for example, a client who submitted an application), whereas there are passive (purely data) artifacts where only processing bears meaning (for example, property records where we can add data or query and no further function is defined). We want to promote digitization; therefore we should also define the data characteristics of artifacts, including where they are handled (for example, already registered somewhere, customer data in the state personal records, etc.).

We will examine the final (and the further) state with the question “what do we need to achieve it?”, and from the answer given, we will deduce what actors should be involved and what steps are needed. We shall repeat this process until we arrive at the initial artifact (state). Note that alternatives may arise during the reverse design. For example, in the case a construction permit the possibility of formal involvement of the local government can be raised (there are advantages and disadvantages).

In reverse data-centric process design, you need to determine how to handle the descriptive data of the artifacts. In this respect, the traditional systems analysis approach differs from the existing practice used in public administration. Though a design methodology may prescribe the unified management of an object (by describing its “attributes”), in practice, the descriptive data of an artifact may be stored in already existing separate registers due to regulatory requirements and in many cases, there is no way to change these registers.

In the course of reverse data-centric process design, the traditional systems analysis techniques can be used for description. Such technique is the artifact lifecycle description used by Bhattacharya, Hull and Su [21], the Business Process Modelling Notation description and the Unified Modelling Language figures. Even techniques, such as using hypergraphs that are on a higher level of abstraction, can be used.

Our practical experience shows that the acceptance and understanding of a technique by participants in the design process is more important than the actual descriptive power of that technique. It is often the case that a highly abstract technique is understandable only for its creator. When a system is implemented based on such abstract description its users might be shocked with the outcome.

4 An Example of Using the Proposed Methodology

We are going to look at the management of a local tax on real estate paid by natural persons. In Hungary, a local government may levy local tax on real estate and houses (within their territory). Tax liability is determined by a municipal decree; the affected clients (owners) should prepare their declaration and pay the tax. If we use the traditional process-based modeling approach on this taxation process, on the basis of the current “case type” we would model the following elements

-

1.

The client prepares and submits his tax declaration.

-

2.

The tax authorities levy the tax to be paid (in the traditional model this might require the participation of several clerks) and send (by mail) a check to the client.

-

3.

The client pays the check in the post office or sends the money via bank transfer.

Using the traditional process-based approach, this looks like a simple procedure as shown in the sequence diagram on Fig. 4.

The real estate tax collection process

In the traditional modelling approach, digitization of the real estate tax collection process would be limited to the automation of case management (automatic filing) and the direct registration of the declaration.

It is easy to see that certain foregoing activities, like the acceptance and publication of the actual rules of taxation by local government, are also part of the process but these are typically overlooked during traditional modelling. The taxation rules provide unequivocally procedures and could well change every year, but the procedure on Fig. 4 does not even indicate this as part of the case.

Activities that follow the payment are also part of the process, these are typically not included into the review either, as they are not described in the concerned local decree, but they are prescribed by other regulations. Such activities are:

-

1.

The concerned staff books the amount of the received money. It is simple in the case of the traditional check-based payments, when the tax authorities created the checks. If payment by bank transfer is also allowed, then a transfer could be made by a third party from a different bank account, therefore reconciling the payment with the identifier (registration number) of the specific case might be difficult or even impossible.

-

2.

The concerned staff (typically another organizational unit of the local government) checks the payment with the participation of several clerks and administrators. It differs for from organization to organization whether this is part of the previous process or it is an entirely separate process.

-

3.

There is another process for collecting unpaid taxes. In the previously described processing model, this is not an organic part of the case either, and the initiation of the collection can be delayed for years (typically, if there is a labor shortage and processing is done manually).

Leaving out actions before and after in time, the taxation process is not the only problem with the model on Fig. 4. This model assumes that the client knows the decrees on local taxation, but this is not a valid assumption. In practice, some clients do not follow these regulations, thus, even if they remember their obligation to submit tax declarations, these declarations are based on earlier information! Thus, additional activities, the correction of the tax declaration by the authorities and the client also belong to the process.

According to the previous model, the client has to provide the data of his/her real estate for completing the tax declaration, including the classification based on the type of use. It is assumed here that the client has at his disposal the evidence of property deed where the necessary data is available (and he knows where to look for them). In practice – especially in the case of less educated older persons who inherited the real estate from relatives – this is not always the case, and the client must visit the land registry and ask for the required data. Apparently, the “booking the payment received” part of the process seems to be simple, but with the introduction of the possibility of bank transfers very often linking a payment to the proper taxpayer causes significant extra work for the authorities (e.g., the payer might be a different person, the file number was not entered in the comment field). Thus, starting from a case type (“real estate tax collection”) we have not detected either the process as a whole or the actual problems. The recognition of the problem depends to a great extent on the “creativity” of the reviewer.

Let us now model according to the proposed reverse data-centric process design methodology. Starting from a higher abstraction level, we should identify the artifact that the authorities need in the course of the whole taxation process. It is the tax payment received (collectable). The next question is what the descriptive data of this artifact is, which is needed for the taxation authority; and the answer is the tax that was paid and is on the proper account of the local authority, more precisely of the local government. This is what must be achieved, this is the final state. Thus, we have two artifacts: the paid (individual) tax and the local government to which the money belongs. Since the base of the tax is real estate, the concerned property (real estate) itself can also be identified as an artifact already at this level.

The data of the real estate are available in the Real Estate RegisterFootnote 7, where the type of use, the owner (ownership share) and its extent can be found. The tax is to be paid by the owner, thus the owner (or client) is also an artifact. Address data of the owner is available in the Personal Data and Address of Citizens Register, including his official and electronic address (if the natural person voluntarily accepts being approached by electronic means and has registered for their client gateway).

We model (design) the taxation process starting from final artifact, “paid (individual) tax”, and we arrive at a completely different result from that of the process-based approach. Whereas traditional analysis starts from the “what happens?” question to explore the related elements, the data-centered approach starts from the problems and at each step poses the question “what do we need to achieve it?”

In the taxation example, the client who wants to pay the tax needs to know, that

-

he has the obligation to pay,

-

to whom he should pay and

-

how much he should pay.

The client must receive the necessary information to fulfil his obligation. To determine the tax liability of an individual, the rules of taxation must be laid down in regulations (local government decrees; this is a precondition outside the scope of this review). Thus, we have discovered another artifact, regulation. The regulation must (also) be published according to the law as an unstructured text in a Central Register, therefore it has an assigned data part. Note that this discovery perfectly illustrates the difference between the traditional process-based and the reverse data-centric approach. In time, the issue of the regulation precedes the payment of the individual tax; but the objective of taxation is to collect the payments and the regulation is required only to achieve this goal. The existence of the regulation is only a necessary condition.

Though our starting point is the paid (individual) tax, it is clearly necessary to handle the case when a tax is not paid. At this point we have arrived to the introduction of an intermediate artifact, namely to the concept of tax liability of the individual taxpayer. It is important to stress that this intermediate artifact can appear in different objectified (tangible) forms. One form is when the taxpayer himself formulates the declaration (tax return) and the authorities perform only a random check. Another form is when the tax authorities determine the tax liability and the taxpayer is notified on his obligation. Note here that previously in Hungary personal income tax was paid on the basis of tax returns submitted by the taxpayers, but with the advent of digital transformation now the tax authority computes the tax to be paid (based on all known personal income).

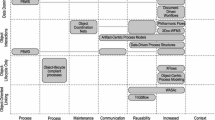

The initially discovered artifacts are shown on Fig. 5, where different symbols indicate the active elements (owner, local government) and the passive, data elements. During analysis, we have to categorize (group) the elements to separate those that would be included in the review and those that are external elements. In our example, we focus on the individual real estate tax liability artifact. At this level, mapping the data of individual tax liability is not determined yet, while for the other artifacts it is possible to identify the mapping of their data (e.g. Personal Data and Address of Citizens, Real Estate Register). Here we have arrived at alternative solutions. We can link “tax declaration” either to “tax statement” where the client is expected to declare his tax; or to “notice on tax liability” issued by the local tax authority. In the first case, the failure to establish tax liability should be also examined; in the second case there is no such activity. The only element that must be examined is the case of non-payment.

Initially discovered artifacts for real estate taxation

A local authority has all the necessary data to determine individual tax liability therefore (since the aim of digitization to achieve more efficient operations) here we have chosen sending a notice to the taxpayer. On this basis, the process of determining the individual tax liability is shown in Fig. 6.

The process resulted by using the reverse data-centric design methodology

It was necessary to introduce a parametrization step to correlate the “regulation” artifact to the “individual tax liability” artifact because a regulation text is not suitable for direct automation. Furthermore, as the chosen alternative was sending a tax notice, it became necessary to ensure the possibility of querying the electronic accessibility of the client. This makes the use of electronic communication as much as possible. Data required for this can be retrieved from the Personal Data and Address of Citizens. For the purpose of simplicity, Fig. 6 does not show the steps involved in the acceptance of the payment but a deeper analysis should include these steps, too in order to ensure that all the steps of the process fit, all the necessary data are created and can be transferred/received.

The activities of the actors of the process (including a possible non-payment) is shown on Fig. 7. The digitized process is substantially automated; supervision by clerks is essentially required only at the problematic branch. The problems caused by erroneous returns and mistaken payments will also decrease.

The digitized process of real estate tax collection

The actual IT support for the above process should be built on such document for-mats that can be processed by both man and machine (for instance the notice should be this kind of electronic document), because at the connections of the process (collection, controversies) this will support electronic, and if possible automated processing. Kiss and Klimkó [23] discussed this issue in detail.

5 Conclusions

Due to the complexity of public administration processes and the alignment of the “case types” with the paper-based operation, the traditional process design that starts from the existing processes a priori limits the possible outcomes of any development that aims at the implementation of one-stop-shop, automated administration or “life-situation” based services. In order to eliminate these barriers, we have proposed a modelling approach in which the review or analysis should be carried out in reverse order, starting from the final state (or the required artifact). During the design process one should scrutinize the artifact step by step by posing the question “what do we need to achieve it?” with consistent follow-ups. The reverse data-centric process design approach enables the communication with the other professionals involved in the review and makes it possible to design a process by revealing its abstraction levels, and therefore it reduces the implementation risks of the supporting information systems for the review process.

Taking into account the compromise in the level of abstraction, our proposed approach also eases the communication with those who are involved in this area of the administration, reducing the risks of implementing the systems redesigned backed by information technology.

Notes

- 1.

- 2.

- 3.

- 4.

- 5.

- 6.

Act L. of 2018 on the 2019 Central Budget of Hungary, Chap. XI. Prime Ministry, Title 12.

- 7.

Act CXLI of 1997 on Real Estate Registration.

References

National Infocommunication Strategy 2014–2020. https://joinup.ec.europa.eu/sites/default/files/document/2016-11/nis_en_clear.pdf. Accessed 12 Mar 2019

Digital Single Market, Policy: Country information – Hungary. https://ec.europa.eu/digital-single-market/en/orszaginformaciok-magyarorszag. Accessed 12 Mar 2019

European Commission: eGovernment in Hungary, Edition 16.0 (2014). https://joinup.ec.europa.eu/elibrary/factsheet/egovernment-hungary-april-2014-v160. Accessed 12 Mar 2019

OECD: Public Governance Reviews. Hungary: Towards a Strategic State Approach (2015). http://www.oecd.org/publications/hungary-towards-a-strategic-state-approach-9789264213555-en.htm. Accessed 12 Mar 2019

Act CCXXII of 2015 on the General Rules for Electronic Administration and Trust Ser-vices (in Hungarian). http://njt.hu/cgi_bin/njt_doc.cgi?docid=193173.338642. Accessed 12 Mar 2019

Act CIV of 2016 on Amending Certain Acts Relating to the Revision Of Central Offices and the Strengthening Of District (Capital District) Offices and the Transfer of Tasks of Certain Budgetary Bodies (in Hungarian). http://njt.hu/cgi_bin/njt_doc.cgi?docid=197962.338820. Accessed 11 Mar 2019

Magyary Zoltán Public Administration Development Programme (in Hungarian). https://magyaryprogram.kormany.hu/admin/download/a/15/50000/Magyary_kozig_fejlesztesi_program_2012_A4_eng_%283%29.pdf. Accessed 11 Mar 2019

Act CXXVI of 2010 on Metropolitan and County-level Government Offices and Legislative Amendments Pertaining to the Establishment of Metropolitan and County-level Government Offices and to Territorial Integration (in Hungarian). http://njt.hu/cgi_bin/njt_doc.cgi?docid=132734.362760. Accessed 11 Mar 2019

155/2016. (VI. 13.) Government Decree on the simple announcement of the construction of a residential building. http://njt.hu/cgi_bin/njt_doc.cgi?docid=195876.364610. Accessed 11 Mar 2019

Radnor, Z.J.: Review of Business Process Improvement Methodologies in Public Services, pp. 1–94. Aim Research, London (2010)

Zellner, G.: A structured evaluation of business process improvement approaches. Bus. Process Manag. J. 17(2), 203–237 (2011)

Stemberger, M.I., Jaklic, J.: Towards E-government by business process change—a methodology for public sector. Int. J. Inf. Manag. 27(4), 221–232 (2007)

Weerakkody, V., Janssen, M., Dwivedi, Y.K.: Transformational change and business process reengineering (BPR): lessons from the British and Dutch public sector. Gov. Inf. Q. 28(3), 320–328 (2011)

Punia, D.K., Saxena, K.B.C.: Managing inter-organisational workflows in eGovernment services. In: Proceedings of the 6th International Conference on Electronic Commerce, pp. 500–505. ACM, March 2004

Wimmer, M.A., Tambouris, E.: Online one-stop government. In: Traunmüller, R. (ed.) Information Systems. ITIFIP, vol. 95, pp. 117–130. Springer, Boston, MA (2002). https://doi.org/10.1007/978-0-387-35604-4_9

Scholta, H., Mertens, W., Reeve, A., Kowalkiewicz, M.: From one-stop-shop to no-stopshop: an e-government stage model. In: Proceedings of the 25th European Conference on Information Systems (ECIS), Guimarães, Portugal, 5–10 June 2017, pp. 918–934 (2017)

Kettinger, W.J., Teng, T.C., Guha, S.: Business process change: a study of methodologies, techniques, and tools. MIS Q. 21(1), 55–81 (1997)

Polyvyanyy, A., Weske, M.: Hypergraph-based modeling of ad-hoc business processes. In: Ardagna, D., Mecella, M., Yang, J. (eds.) BPM 2008. LNBIP, vol. 17, pp. 278–289. Springer, Heidelberg (2009). https://doi.org/10.1007/978-3-642-00328-8_27

Molnár, B., Őri, D.: Towards a hypergraph-based formalism for enterprise architecture representation to lead digital transformation. In: Benczúr, A., et al. (eds.) ADBIS 2018. CCIS, vol. 909, pp. 364–376. Springer, Cham (2018). https://doi.org/10.1007/978-3-030-00063-9_34

Cohn, D., Hull, R.: Business artifacts: a data-centric approach to modeling business operations and processes. Bull. IEEE Comput. Soc. Tech. Comm. Data Eng. 32(3), 3–9 (2009)

Bhattacharya, K., Hull, R., Su, J.: A data-centric design methodology for business processes. In: Handbook of Research on Business Process Modeling. IGI Global (2009)

Grove, A.S.: High output management. Vintage (2015)

Kiss, P.J., Klimkó, G.: Electronic forms-based model of public administration operations. In: Kő, A., Francesconi, E. (eds.) EGOVIS 2017. LNCS, vol. 10441, pp. 19–31. Springer, Cham (2017). https://doi.org/10.1007/978-3-319-64248-2_3

Author information

Authors and Affiliations

Corresponding author

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2019 Springer Nature Switzerland AG

About this paper

Cite this paper

Kiss, P.J., Klimkó, G. (2019). A Reverse Data-Centric Process Design Methodology for Public Administration Processes. In: Kő, A., Francesconi, E., Anderst-Kotsis, G., Tjoa, A., Khalil, I. (eds) Electronic Government and the Information Systems Perspective. EGOVIS 2019. Lecture Notes in Computer Science(), vol 11709. Springer, Cham. https://doi.org/10.1007/978-3-030-27523-5_7

Download citation

DOI: https://doi.org/10.1007/978-3-030-27523-5_7

Published:

Publisher Name: Springer, Cham

Print ISBN: 978-3-030-27522-8

Online ISBN: 978-3-030-27523-5

eBook Packages: Computer ScienceComputer Science (R0)