Abstract

In any fire risk analysis or risk-based assessment, valid measurements of the severity of the fire hazard—the consequences of fire, if it occurs—are of paramount importance. Most analyses are limited to simple outcome measures, such as numbers of deaths or injuries or direct property damage, defined as direct harm to property requiring repair or replacement.

Access provided by Autonomous University of Puebla. Download chapter PDF

Similar content being viewed by others

Keywords

These keywords were added by machine and not by the authors. This process is experimental and the keywords may be updated as the learning algorithm improves.

Introduction

In any fire risk analysis or risk-based assessment, valid measurements of the severity of the fire hazard—the consequences of fire, if it occurs—are of paramount importance. Most analyses are limited to simple outcome measures, such as numbers of deaths or injuries or direct property damage, defined as direct harm to property requiring repair or replacement.

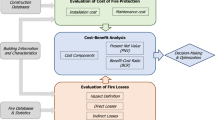

Consequences have to be expressed in monetary values if the purpose of the analysis is to permit a decision maker to express and compare all relevant costs and benefits of different choices in comparable terms that truly capture what is important to the decision maker or the group represented (such as the general public).

The rapidly growing use of performance-based fire protection design exemplifies the need for these advanced methods of consequence measurement at the level of an individual building or product, just as the growing number of countries demanding cost-benefit analysis of proposed new national regulations illustrates the need for these methods of measurement at the level of national policy.

This chapter describes some of the oft-neglected aspects of consequence measurement in support of economic decisions about fire protection engineering choices, specifically

-

An overview of the total cost of fire and of efforts to prevent or mitigate fire

-

A discussion of how the relevant costs and benefits for the same choices may vary, depending on whether they are analyzed from the point of view of an individual, an organization, or society as a whole

-

An overview of how costs and benefits are treated for insurance purposes

-

Methods for translating nonmonetary consequences—notably deaths and injuries—into monetary equivalents for purposes of analysis

-

Methods for estimating indirect losses—mainly business interruption costs—caused particularly by large fires

-

Utility theory and its role in capturing people’s preferences for certainty in outcomes

Principles of life-cycle costing are relevant but are covered at length in Chap. 81. Chapter 81 also provides additional material relevant to many of the subjects covered in this section. A more extensive treatment of these topics, with a range of examples, can be found in The Economics of Fire Protection by G. Ramachandran [1].

Components of Total National Fire Cost

For more than two decades, the World Fire Statistics Centre (WFSC) has issued periodic studies with comparative statistics from 15 to 20 countries on the total cost of fire [2]. Their methods are the starting point for most national analyses, including more detailed analyses from the United States and Canada [3]. The WFSC methodology tracks deaths and injuries, which are not converted to monetary equivalents, but focuses on four core economic components:

-

Damages due to fire, whether reported or unreported (for a fire service database), insured or uninsured (for an insurance database), direct or indirect (where indirect loss includes business interruption losses—also called consequential loss), temporary lodging, missed work, and other costs or lost income associated with recovery from a fire

-

Costs of fire-fighting organizations, typically dominated by or limited to the costs of municipal career fire service organizations

-

Incremental construction costs for buildings attributable to fire safety requirements or concerns

-

Administrative costs of fire insurance, including profits

Table 79.1 shows these costs from 1980 to 2011 for the United States [4]. The reports of the World Fire Statistics Centre show comparable figures for many other countries, primarily in Europe but including Japan and Canada. Comparisons are made easier because all loss figures are also shown as percentages of national gross domestic product (GDP). The total U.S. percentage for these core components typically runs about 1 % of the GDP. The United States tends to have one of the lower percentages for fire damage and fire insurance administration (although the latter is especially hard to calculate and has proven quite volatile from year to year). The United States tends to have one of the higher percentages for costs of fire-fighting organizations and for fire-related costs of building construction (although the latter is a subjective estimate, based on some special studies).

Table 79.2 shows the relative importance of the four core components of total cost and how that relative importance has changed over the 32 years studied. The costs of fire-fighting organizations and building construction for fire protection—where the U.S. figures tend to represent one of the higher GDP percentages—are by far the two dominant components of the total cost core, and their dominance has been growing. Not shown in Tables 79.1 and 79.2 are two other important points. First, in nearly every country providing indirect loss figures, indirect losses tend to be less than 25 % of direct damages (notably excepting Switzerland at roughly 40 %). Second, the U.S. fire death rate, relative to national population, consistently ranks among the highest rates in the countries studied by the World Fire Statistics Centre.

Indirect Loss Estimation: NFPA Approach to U.S. Losses

NFPA did a special study to provide a better basis for calculating indirect loss for properties other than homes. It found that indirect loss varied considerably as a fraction of direct damage from one type of property to another. Based on analysis of 109 fires from 1989, indirect losses (principally business interruption costs) add the following amounts to direct loss, based on property class:

-

65 % for manufacturing and industrial properties

-

25 % for public assembly, educational, institutional, retail, and office properties

-

10 % for residential, storage, and special-structure properties

-

0 % for vehicle and outdoor fires

These percentages may appear low to anyone whose sense of indirect loss is based primarily on a few well-publicized incidents where indirect losses were much larger than direct damages. From a statistical standpoint, however, such incidents are more than offset by the far more numerous incidents where indirect loss is either small or nonexistent.

There remains the problem of quantifying indirect loss associated with properties that never reopen. Here again, the overall pattern is much more modest than some figures that have circulated. Each year, an estimated 2 % of reported nonresidential structure fires, excluding fires in storage facilities and special structures (e.g., vacant properties, properties under construction, structures that are not buildings), result in business closings. For NFPA’s analysis of indirect losses in the United States, a closing is estimated to imply indirect losses equal to four times the reported direct loss in the fire.

These very rough calculations suffice to estimate indirect loss for purposes of a national analysis of total cost from society’s point of view. They clearly are not sufficient to produce estimates suitable for insurance purposes or any other decision making at the level of an individual firm. Also, detailed estimates of consequential losses to the national economy should reflect several economic factors, including level of employment or unemployment, level of capacity utilization, volume of exports and imports, exchange rates, and performance of national and international competitors. Due to the interactions of these factors, a detailed evaluation of consequential losses to the national economy is a complex problem requiring the application of econometric models, such as input-output analysis. These national factors do not apply to analysis at the level of an individual firm.

The effects of a fire on the earning capacity of a firm can be measured in terms of loss of profits during the period of interruption following the damage until the resumption of the activity in which the firm was engaged before the fire. Loss of profits is usually expressed as a percentage of loss of turnover. A cover against this loss can be obtained by purchasing a consequential loss insurance policy, the premium for which is a function of the period of indemnity. Loss of profits sustained by a supplier or customer of the firm that suffered the fire (called the “fire-hit firm” from here on) can be covered by a normal consequential loss policy based on reduction in turnover.

The form of insurance policy in more general use in the United States is known as business interruption insurance (BII). BII operates on lines similar to the U.K. contract of consequential loss insurance (CLI) with a turnover specification, though there are some differences. For private sector level insurance firms transacting BII or CLI, there are useful sources of data for estimating consequential losses due to fires in industrial and commercial premises. Organizations such as the Insurance Information Institute in the United States compile consequential loss data furnished by major insurance firms.

Indirect Loss Estimation: Unpublished U.K. Study

Returning to national- and society-level analyses of indirect or consequential loss, some now-old studies done in the United Kingdom illustrate how a more detailed analysis can be done. The U.K. government’s Home Office carried out two research studies between 1970 and 1980 on consequential losses to the national economy. The first study adopted an input-output-type model in which all losses were considered output losses [5]. Losses were either (1) losses in the type of output actually hit by fire or (2) losses in some other output, because production factors (e.g., fixed assets, entrepreneurial effort, or labor) have been less effectively employed as a result of the fire. The effects of a fire were assumed to have the most impact on the fire-hit firm, the supplying firm, the purchasing firm, the parallel firm, and the rest of the economy. A fire-hit firm was defined as a compartment of production covering just that type of output hit by a fire and no other output. A parallel firm was defined as the compartment of a firm that produced in parallel to the fire-hit compartment (which might be in the same firm or in another firm). Any effects in a parallel firm or somewhere else in the rest of the economy were assumed to be included in the calculation of the effects in a fire-hit firm, in a supplying firm, or in a purchasing firm.

In this Home Office study, consequential losses were measured by the net present values of streams of annual outputs lost by the fire-hit firm, supplying firms, and purchasing firms. In regard to the fire-hit firm, it was necessary to determine a length of time over which fixed assets destroyed by fire were assumed not to be replaced by extra investment in the economy. This time choice had to depend on a view of the future course of the economy, which depended on unknown events and influences. Hence, alternative calculations were produced based on the remaining lives of the assets and on a number of shorter periods. The net present values were corrected within the fire-hit firm, supplying firms, and purchasing firms for offsetting influences due to two factors. First, some production factors affected by fire might be used elsewhere in the economy. Second, production factors already employed elsewhere might be used more intensively. The extent of such offsetting influences would depend largely on the level of employment and the pressure of demand in the economy. Separate calculations were made for three alternative cases—slack, middle, and tight conditions in the economy. Results were given for each of 15 industries, including a factor by which a fixed assets valuation should be multiplied to give the sum of all the corrected output losses.

In order to verify the assumptions employed and results obtained in this study, the Home Office commissioned field research aimed at an in-depth investigation of a small sample of fires [6], which involved direct contact with fire-hit firms and concentrated on direct, consequential, and, hence, the total loss to the U.K. economy from industrial, distributive, and service sector fires. Consequential losses were considered to arise from loss of exports, extra imports, the diversion of resources from other productive activities, and reduction in the efficiency of resource use following the fire. The study assumed that there was full-capacity utilization of resources and that market values of the resources reflected their true worth. Insurance estimates of losses were used as measures of the assets destroyed in fires. Application of national capital output ratios translated these asset losses into losses of output from fire. Allowances were made for the secondary impact on suppliers and customers of fire-hit firms and for the impact of the level of capacity utilization. A correction factor was applied to account for the ability of the economy to “make good” the losses of the fire-hit firm by other firms.

The analysis produced estimates of the ratios of consequential to direct losses to the economy for “off-peak” and “peak” years and for each industry and service sector. The main conclusion was that most fires, except those in chemical and allied industries, produced no consequential losses to the national economy. Only in one sector (chemicals) was evidence found of a statistical link between consequential losses and direct losses. The study failed to estimate this link for other sectors and a number of other possible effects on consequential losses. Note the similarity of this conclusion to the results of the much smaller, rougher, and more recent NFPA study, leading to the indirect loss parameters still used in the United States.

Indirect Loss Estimation: Private Sector Level

A study by Hicks and Liebermann deals with costs and losses from the community and private perspective as they impact the fire victim [7]. The property class categories addressed in this study were commercial occupancies only, separated into four types: (1) mercantile, (2) nonmanufacturing, (3) manufacturing, and (4) warehouses. The authors considered first the following expression, based on a convenient formulation of the Cobb-Douglas production function [8]:

where

-

IL = Indirect loss

-

K = Constant

-

r, a = Regression coefficients

-

E = Expenditure for fire protection (–)

-

X = Number of fires (+)

-

T = Time (surrogate for technological advance) (–)

The signs in parentheses relate to the expected values of the coefficients for the independent variables. The term kerT is a scalar factor in which r measures increases in fire department efficiency due to technological advances in suppression equipment, training, or facilities as well as altered building codes, smoke alarms, and the like. Equation 79.1 can be converted to a multiple-regression model by taking logarithms of terms on both sides.

In principle, the parameters r and a can be estimated but, in practice, sufficiently detailed statistics typically are not available. The authors therefore adopted the following, much more simplified, form:

where DL is the direct loss and c and b are constants. Equation 79.2 is based on the assumption that very small fires typically generate small indirect losses while large fires produce larger indirect losses. If b = 1, this model reduces to the earlier-cited approach used by NFPA, wherein indirect losses are estimated as proportional to direct damages.

The results obtained by Hicks and Liebermann [7] are given in Table 79.3. Note that all values of the parameter b are near 1, which means the deviations from the even simpler model used by NFPA are modest. Statistical tests of significance showed that the regression model fitted well with the data in all the cases except warehouses. Since nationally aggregated data were utilized, it was recommended that the occupancy-specific models be used only at the national level and that any desired analysis of local impacts be accomplished using a local model. The value of parameter b has been estimated to be greater than unity for local and national levels and less than unity for the occupancy levels. For any increase in direct loss, the ratio of indirect to direct loss would increase if b > 1, and decrease if b < 1. The ratio would be a constant if b = 1. From the information given in the study, it was not possible to test whether the value of b was significantly different from unity for any of the six levels.

Indirect Loss: Illustrations from Some Major U.S. Fires

It is not difficult to identify large, well-publicized fires in which the cost of business interruption far exceeds direct property loss, such as a property that offers lodging or workspace and suffers so much damage that the slack capacity of the facility or even the community is not sufficient to absorb the displaced demand. An example is the MGM Grand Hotel fire, where the hotel claimed total direct damage and business interruption costs of $211 million, whereas NFPA’s best information placed direct damage at $30–50 million [9].

Sometimes, though, it can be difficult to determine what the true net loss due to business interruption is—what constitutes an “interruption.” Compare two large high-rise office building fires [10, 11]. Fire destroyed four floors of the 62-story First Interstate Bank building in Los Angeles in 1988 but also took the entire building out of service for 6 months—a true business interruption, because the property reopened after repairs.

By contrast, the 1991 One Meridian Plaza fire destroyed more floors in a shorter high-rise office building (38 stories) and the building never reopened. Dozens of firms, occupying nearly a million square feet of office space, had to seek new permanent homes, but the real estate community estimated, a year after the fire, that vacancy rates would still be 11–12 % after every displaced firm had been absorbed.

One Meridian Plaza represented an estimated 2.5 % of Philadelphia’s office space, whereas the MGM Grand represented a larger share of Las Vegas area hotel rooms. These are all factors in determining how easily a market can compensate for interruption of capacity from one provider. Similar concerns arise for fires in any type of large multiunit residential or health care occupancy.

The most clear-cut examples of widespread vulnerability involve critical elements of the nation’s infrastructure. Fears of great damage from a widely distributed computer virus have so far not materialized, and two major interruptions to the northeast electrical power grid in the last third of the twentieth century were not due to fire. However, there have been two fires involving telephone exchanges, the more recent in Hinsdale, Illinois, in 1988 [12].

A total of 38,000 customers were served by the Hinsdale office. The majority were still without service 5 days after the fire, and some did not regain service until 9 days after the fire. An estimated 9000 businesses were affected, including a nationwide hotel chain’s reservation service, a florist delivery service networked to 12,500 florists around the country, and communications between a Federal Aviation Administration control tower and both of Chicago’s major commercial airports. The most conservative estimate of the costs of the associated delays and lost business would exceed the estimated $40–$60 million in direct damage.

Economic Costs Not Usually Calculated Within the Core

Several cost components have been estimated by Meade but cannot be readily estimated each year [3]. They totaled $27.8 billion in 1991 and consist of the following:

-

Costs of meeting fire grade standards in the manufacture of equipment, particularly electrical systems equipment and “smart” equipment with its greater use of computer components ($18.0 billion)

-

Costs of fire maintenance, defined to include system maintenance, industrial fire brigades, and training programs for occupational fire protection and fire safety ($6.5 billion)

-

Costs of fire retardants and all product testing associated with design for fire safety ($2.5 billion)

-

Costs of disaster recovery plans and backups ($0.6 billion)

-

Costs of volunteer and paid activities involved in preparing and maintaining codes and standards ($0.2 billion)

The largest piece by far is the first one. Meade’s study developed estimates, by industry, firm, or individual making the estimate, that ranged over two orders of magnitude, from 20 % to 2000 % add-on cost. He settled on 30 %, which seems conservative. However, out of the fraction of equipment that could be affected by these costs, his estimate of the share that is built to these more demanding standards is not conservative. His estimate raises the concern that the fire safety spending habits of industry’s most fire-conscious companies have been treated as typical of all industry.

Based on the Consumer Price Index, the $27.8 billion estimated by Meade for 1991 would translate to $45.9 billion in 2011 in the United States. The NFPA now adds a figure for national and state fire agency costs, which was $3.0 billion in 2011.

Costs and Benefits Based on Level

The previous discussion noted that the calculation of indirect loss is done differently if the focus is on an individual firm or on the entire society. Any calculation of costs and benefits associated with fire, fire prevention, or mitigation activities and decisions will show differences based on level, because costs and benefits do not fall equally on all parties.

A fire that interrupts or destroys the ability of a single firm to offer its goods or services to the market results in devastating indirect loss to that firm. Society, however, may experience no discernable effect, provided that

-

1.

The firm represents a small part of its industry, so that neither price nor availability of its products or services is affected by the removal of the firm.

-

2.

The firm represents a small part of the employment opportunities in its community, so that its employees are able to find comparable work and income quickly and easily.

Conversely, a fire that results in little on-site damage but creates devastating environmental damage on the surrounding area, through air or water pollution, may represent a negligible cost to the firm, provided it is able to disown the off-site costs and pay minimal legal costs to do so. Meanwhile, the cost to society is enormous.

The second example cited above involves direct damage to property, and its central premise—that the firm could disavow off-site damages if they were sufficiently difficult to measure and to trace to an event on the firm’s site—is probably far-fetched in today’s world. The first example cited above involves a major type of indirect loss, sometimes called business interruption loss or consequential loss, and that example is not at all unusual.

Analysis can be done at many different levels—the individual person, the individual firm, the individual community, the individual industry, the individual state or province, the individual industry plus all industries strongly dependent on it, the individual nation, the entire world—but for purposes of analyzing business interruption or consequential loss, it may be useful to focus on two major levels of economic activity: (1) private sector and community level and (2) national and societal level. The first level includes the fire-hit firm and the firms supplying to or purchasing from the fire-hit firm’s materials, components, or services. Costs associated with moving, temporary accommodation, and lost profits are valid costs at the private sector level but not at the national level.

At the national level, the loss of a specific unit of productive capacity may be spread among the remaining capacity in the nation such that competitors may seize the opportunity to enter the market and maintain the national rate and volume of manufacture. In such cases, there may be little or no incremental loss to the national economy as a result of a fire in the premises of, for example, a manufacturing firm. Several studies by the now-defunct Insurance Technical Bureau (ITB) in the United Kingdom provide an indication of the various special factors one should consider in the evaluation of consequential losses due to fires and other hazards.

A small share of the total number of production lines in a plant manufacturing pharmaceutical products may generate a very large proportion of total gross profits [13]. Regulatory restrictions may limit possibilities for shifting manufacture to other plants or even to other lines in the same plant. Natural raw materials may be irreplaceable or out of season, creating another source of delay in recovery or another obstacle to meeting demand during the recovery process. Specialized plant equipment (e.g., tailor-made driers or centrifuges) may involve long delays for replacement. Loss of laboratory facilities may seriously interrupt testing and quality control programs.

The aerospace industry is another example where innovation driven by research creates a very short cycle time for the introduction of new products. In such cases there may be little redundancy in the supply of prototypes or other essential elements needed to keep the program on schedule [14]. Examples might include a new aircraft prototype assembly, untried or unproven research and development projects, or specimens for fatigue testing of aircraft structures. Loss of any of the above could result in a significant interruption to the program. In addition, the effect of delays in the development or supply of components or assemblies from specialist equipment manufacturers can be serious. The interactions of the many activities and firms involved in the manufacture of aerospace products makes for involved consequential loss considerations.

An example from the other end of the spectrum of industries would be resin, paint, and ink manufacture, which would not normally be expected to give rise to unduly high consequential loss [15]. Facilities are generally dispersed in small units throughout a given country, and there may be sufficient manufacturing capacity to absorb temporary loss at individual sites. Also few, if any, products are so special that they cannot be made elsewhere in the industry. Consequential loss, therefore, hinges primarily on the time for reinstatement of the plant and the ability of management to arrange for the supply of goods from other sources, pending a return to full production. Loss of raw materials or finished goods normally results in relatively short interruption periods. However, longer periods may be required for the replacement of tanks and pumps destroyed by fires, and for other hazards, such as explosion.

Due to high investment costs, specialized equipment (e.g., electronically or computer-controlled equipment) is generally used at full capacity in some industrial processes. Continuous operation of these processes may reduce the chance of a fire spreading but provides no scope for making up for lost production following a fire. Specialized equipment damaged by fire cannot be replaced easily or quickly, especially if the assemblies or spare parts for them have to be imported. Industries using such equipment are liable to sustain high consequential losses.

Measurement Approaches in the Insurance Industry

Statistical (actuarial) techniques are well developed for calculating the insurance premium for loss of profits due to fire (e.g., see Benckert) [16].

The risk premium is a function of the period of indemnity and is generally expressed as the product of the loss frequency and the mean amount of loss. The loss frequency is assumed to be independent of the period of indemnity. The frequency function of the period of interruption following a fire has a log-normal distribution [16, 17].

An insurance company generally adds two types of loading to the risk premium to calculate the premium payable by a policyholder. First, a safety loading is added toward chance fluctuations of loss beyond the expected loss. Second, another loading is imposed to cover the insurer’s operating costs, which include profits, taxes, and other administrative expenses. A number of texts have been published on different types of insurance and claims concerned with consequential losses (e.g., see Riley) [18].

Monetary Equivalents for Nonmonetary Costs and Consequences

Deaths and Injuries

Damage to life or health in terms of injuries and deaths is an important consequence in fire risk assessment and is usually the first priority consequence cited in national codes or regulations. Its importance is not in question. What is difficult is identifying a valid and acceptable method for estimating and comparing monetary equivalents of consequences of this type with costs and monetary equivalents of consequences of other types, such as property damage or indirect/consequential loss.

Insurance claims provide some data for the valuation of injury, though they are likely to be limited to costs mediated by the marketplace, such as treatment costs and the value of work time lost. Other costs, such as pain and suffering, are more difficult to evaluate.

The specification of a dollar equivalent for human losses, particularly for loss of life, remains an extremely controversial subject. It is important to emphasize that no one intends to suggest that there is an acceptable price for losing one’s life. Rather, these figures are intended to reflect a social consensus on the value of changes in the risk of death by fire. For example, if most people say they would be willing to pay $1500 to reduce their lifetime risk of dying in a fire from, say, one chance in 500 to one chance in 1000, then a simple way of restating that is that people value a life saved at $1500 for 1/1000 of a life, or $1.5 million per life.

Four approaches to valuing human life have been identified. The first method is concerned with gross output based on goods and services that a person can produce if not deprived, by death, of the opportunity to do so. Sometimes gross productivity is reduced by an amount representing consumption (net output). Discounted values are generally taken to allow for the lag with which the production or consumption occurs. The output approach usually gives a small value for life, especially if discounted consumption is deducted from discounted production. This must be so since the community as a whole consumes most of what it produces. It is argued that when a person dies, although the community loses that person’s future output, it also saves concurrent future consumption. The person’s own consumption or the utility that would be derived if the person were alive is not counted as a loss. This approach received considerable emphasis, say, 30 years ago, but not today. A variation of this approach is called the “livelihood approach” [19].

The second approach assumes that if an individual has a life insurance policy for $x, then he or she implicitly values his or her life at $x. Collection of necessary data from insurance companies is not a difficult task, and this is the major advantage in adopting the insurance method. There are, however, two drawbacks to this method. First, a decision whether or not to purchase insurance and the amount of insurance is not necessarily made in a manner consistent with one’s best judgment of the value of his or her life. This decision depends largely on the premium the insured can bear from his or her income, taking into account family expenditures. Second, purchasing an insurance policy does not affect the mortality risk to an individual. This purchase is not intended to compensate fully for death or to reduce the risk of accidental death. Hence insuring life is not exactly a value tradeoff that is considered between mortality risks and costs.

The third method for assessing value of life involves court awards to heirs of a deceased person as restitution from a party felt to be responsible for the fatality. Here again, collection of necessary data is not a problem. Assessment of values of life could also be expected to be reasonably accurate since lawyers and judges have a massive professional expertise in the ex post analysis of accidents. The object of such an analysis is to discover whether the risk could have been reasonably foreseen and whether the risk was justified or unreasonable.

There are, however, a few problems in using court awards for valuing human life. The court should ideally be concerned with the assessment of suitable sums as compensation for an objective loss (e.g., loss of earnings of the deceased) as well as for a subjective loss (e.g., damages to spouse and children for their bereavement and grief). In some countries damages can include a subjective component for pain and suffering of survivors, but certain courts are generally against such compensation for subjective losses to persons who are not themselves physically injured, believing that bereavement and grief are not losses which deserve substantial compensation. It is also difficult to value the quality of a life that has been lost. People who themselves suffer severe personal injury, of course, qualify for substantial damages for subjective losses. Resource costs such as medical and hospital expenses are significantly higher for obvious reasons in serious injury cases than in fatal cases; hence, awards for subjective losses tend to be much larger and more important in serious nonfatal cases than in fatal cases. Some courts have also limited to very low levels the damages that may be awarded for reductions of life expectancy. Last, in court awards risks to individuals are considered relative to the plaintiff and costs to the defendant. However, value judgments are likely to vary according to whether the individuals making these judgments are associated with the plaintiff, the defendant, or the court.

The fourth approach is the one most widely adopted for valuing life. The willingness to pay is based on the money people are willing to spend to increase their safety or reduce a particular mortality risk [20, 21]. It is difficult to differentiate between the benefit from increasing people’s feeling of safety and that from reducing the number of deaths. Anxiety is a disbenefit even if the risk is much smaller than believed. Likewise, a person who dies from something whose risk is not known to him or her still suffers a loss.

This approach to value of life rests on the principle that living is a generally enjoyable activity for which people would be willing to sacrifice other activities, such as consumption. The implied value of life revealed by a willingness-to-pay criterion would depend on a number of factors. The acceptable expenditure per life saved for involuntary risks is likely to be higher than the acceptable expenditure for voluntary risks, as people are generally less willing to accept involuntarily the same level of risk they will accept voluntarily. The sum people are prepared to pay to reduce a given risk will also depend on the total level of risk, the amount already being spent on safety, and the earnings of the individuals.

The theoretical superiority of the willingness-to-pay method begins with its connection to the principle of consumer sovereignty, which says goods should be valued according to the value individuals put on them. Despite this individual-oriented underpinning, this approach can also be used to develop a general figure for a typical person, based on consensus patterns in the values individuals select. This, in turn, permits analysis of societal decisions using the willingness-to-pay principle.

Surveys have shown variability and inconsistencies in responses, because individuals have difficulty in answering questions involving very small changes in their mortality risks [22–24]. Due to insufficient knowledge about the risk, most people find it difficult to accurately quantify the magnitude of a risk. Also, the benefits are often intangible (e.g., enjoyment, peace of mind). It is difficult to put a monetary value on these factors.

Economists therefore use a variety of inferential methods to develop value of life and value of injury averted estimates for purposes of analysis. These include examination of patterns from the other three approaches—foregone future earnings, insurance policy amounts, and especially court judgments. It is also possible to develop an inferred value of life risk reduction from any action that has a cost and achieves such a reduction. Studies have been done of the implied value of life associated with hundreds of safety- and health-related regulatory actions. Studies could be done based on the price and demand curves for safety-oriented products, such as smoke alarms and child-resistant lighters.

It is useful to keep in mind the very wide variation in the estimates and valuations and the implied uncertainty as to what values are reasonable. For example, a landmark 1981 study cited sources for values of statistical life ranging from $50,000 to $8 million [25]. More recent valuations have been higher generally but still vary widely.

Economists at the U.S. Consumer Product Safety Commission (CPSC) have an ongoing program of studies of injury costs. Periodically, they review the literature, including their own studies, and select dollar values for use in policy analysis of fire safety and other product hazard analysis. The NFPA studies of the total cost of fire in the United States use values of $5 million per death and $166,000 per injury as 1993 values, then use the Consumer Price Index to calculate corresponding values for later years for injuries only, all in accordance with the practices of CPSC economists. Special studies have changed the NFPA methodology of estimating costs for injuries, adding a multiplier of 60% to civilian injuries, 30% to firefighter foreground injuries, and 10% to firefighter non-fireground injuries.

The total dollar equivalent for reported and unreported fire deaths and injuries in the United States, calculated in this way, was $31.7 billion in 2011 [4].

It is beyond the scope of this chapter or this handbook to review, even briefly, the many nuances, methods, and applications of value of life estimation. For those who wish to pursue the subject in more detail, several listed references are recommended [26–33].

Value of Donated Time

In the United States, the largest block of donated time for fire safety consists of that donated by the roughly 800,000 volunteer fire fighters who provide municipal fire protection to a sizeable fraction, mostly rural, of the U.S. population. One approach to valuing their donated time is to assume that costs are generated not so much by the workload of emergencies as by the need to provide coverage and readiness to respond for a certain area, that is, the ability to provide an effective response within a certain response time. If this approach is used, the primary factor in costs would not be workload, but geographical area. The low-density rural areas covered by volunteer fire departments would then require more personnel than would more compact areas of equal population covered by career fire departments.

Communities seeking to set such fire protection coverage at an appropriate level might begin with a response time objective. The part of response time that is most related to resource decisions is travel time, which may be treated as proportional to travel distance. If one thinks of a typical response area as a circle with the fire station in the middle, one can see that travel distance is proportional to the square root of area. For example, if the distance from the fire station to the edge of the response area doubles, that is equivalent to doubling the radius of a circle, whose area then is quadrupled. This also means that if the same population is spread out over an area four times as large, it will need twice as many fire stations to provide equivalent travel times, which means the needed number of fire fighters may be treated as inversely proportional to the square root of the population density.

In 2000, the metropolitan statistical areas of the United States had 80.3 % of the U.S. population in 20.0 % of the area. If one assigns all the remaining area and population to volunteers (which is a rough approximation), then the metropolitan population density (proportional to 80.3 % divided by 20.0 %) exceeds the nonmetropolitan population density (proportional to 19.7 % divided by 80.0 %) by a factor of 16. The square root is 4.0, which is somewhat higher than the actual ratio in fire fighters (2.8:1 in 2002).

Using the 4:1 ratio for personnel needed, assuming their costs would be the same as in career fire departments, and again adjusting for nonpersonnel costs included in reported local fire expenditures, the result is $139.8 billion in 2011 for the value of time donated by volunteer fire fighters.

If this estimate of the value of donated time by volunteer fire fighters is combined with the earlier estimates of the core components of total cost of fire, the other economic components estimated from data that is not updated yearly, and the estimated monetary equivalent of deaths and injuries associated with fire, the resulting total is $329 billion for the United States in 2011. This is 2.1 % of the total U.S. gross domestic product, a figure that fully justifies appeals from the fire protection engineering community for more support of research seeking to reduce the total, either through improved safety or through sustained safety at reduced cost.

Utility Theory

Even after all costs and benefits (e.g., risk reduction) have been converted to monetary equivalents, an important aspect of people’s preferences may be overlooked if expected-value techniques are used directly in a cost-benefit analysis of fire safety measures to include the certainty-equivalent of uncertain costs and benefits.

Suppose a person is offered a choice between $5 or a 50/50 coin toss wager between $10 and nothing. The expected values of the two choices are equal, assuming a fair coin. A person who prefers the sure thing is called risk averse. Most people are somewhat risk averse in some situations. Just how risk averse a person is can be measured by determining how low the sure-thing offer can be set before the person will choose the wager with the $5 expected value.

Fire loss is never a sure thing, and so people’s risk preferences are always relevant to assessing their preferences for choices involving fire risk.

People differ not only in their degree of risk aversion but also as a function of the type of choice being offered. Some people may prefer to take risks in most situations. It also is not unusual to find that a person is a risk preferer for ventures involving small losses but a risk avoider for those involving large values.

Any pattern of risk preferences can be quantified by the use of utility functions. Disutility, the negative counterpart of utility, is the appropriate term in an analysis involving negative outcomes such as fire loss, cost of fire protection, and insurance premiums.

Consider a few more examples based on participation in a game of chance. Suppose a person is offered the following bet on the toss of a coin—to win $100 if the coin comes up heads or lose $75 if the coin comes up tails. If the coin is a fair coin, the $probability of heads or tails coming up is one-half. The expected payoff is

if the person playing the game takes the bet and $0 if he or she does not take the bet. According to the expected value criterion, the bet should be accepted because its expected value is greater than the expected value of not taking the bet.

Now suppose the amounts involved are $1,000,000 and $750,000 rather than $100 and $75. The expected payoff is now $125,000 if the bet is taken and $0 if the bet is not taken. Every value has been multiplied by 10,000. According to the expected value criterion, the bet should still be taken and is even more attractive. But would you take this bet? Probably not, unless you are wealthy enough that you could afford to lose $750,000. The possible gain of $1,000,000 is tempting, but losing could be devastating or even intolerable.

As another example, consider a choice between two bets. In the first bet, the person playing the game wins $2 million if a coin comes up heads and wins $1 million if the coin comes up tails. In the second bet $8 million can be won if the coin comes up heads, but nothing will be won if the coin comes up tails. The expected payoffs of the two bets are $1.5 and $4 million, respectively. The second bet has a much larger expected payoff than the first, and hence should be chosen on the basis of the expected value criterion. However, many would choose the first bet because they focus on the larger minimum gain—the closest thing to the “sure thing” in a choice between two bets. With the first bet, you are assured of at least $1 million. With the second bet, there is a 50 % chance of winning nothing.

Consider a third example, defined more directly in terms of fire safety. Suppose the owner of a home or other building faces a probability, p, of fire occurring in the coming year and a loss, L, in the event of a fire. (In this simplified example, only one kind and severity of fire is possible.) The expected annual loss due to fire in that building is pL, and it is a two-outcome bet, like a coin toss.

The sure-thing alternative, from the owner’s point of view, can be achieved through insurance. The property owner has two options—to insure or not insure the building. The expected loss (cost) is equal to the insurance premium (call it I) if insured, and pL if not insured.

On the basis of the expected value principle, the owner should choose the insurance option only if I is less than pL. This condition will never be satisfied since an insurance firm would determine the premium, I, for a risk category by adding to the risk premium, pL, two loadings—a safety loading and another loading to cover the operating costs of the firm which include profits, taxes, and other administrative expenses. From the insurance company’s point of view, it should offer the insurance only if I is greater than pL. How is it that insurance even exists under these conditions?

The risk aversion of most people provides the foundation for breaking this dilemma. Based on risk aversion, the building owner will accept a sure-thing loss of I even if I is greater than pL. The difference is typically large enough not only to make a mutually acceptable deal possible, but to allow I to be large enough to cover the two loadings mentioned above.

In practice, many different sizes and severities of fire are possible. For the smallest fires, the building owner’s risk aversion will probably be much less pronounced, and insurance may seem unattractive. The creation of a deductible threshold solves that problem by allowing the insurance to be limited to losses large enough for the owner’s risk aversion to be strong. If a very large fire occurs, the insurance company may be unable to cover the loss. This leads to reinsurance markets, particularly for properties with the potential for more than one very large loss in a short period of time. For smaller losses, the safety loadings on the risk premium would provide a safety margin for the insurance company, depending on its calculations of the probability distribution for the fire loss. There may also be an upper bound set on the maximum loss the insurance company can cover.

The preference for a small fixed loss over a risk of large loss originates primarily from an aversion to the psychological state of uncertainty. For the reasons mentioned previously, the expected monetary value is not a satisfactory criterion for decisions involving potential losses in ranges where risk aversion is an issue for many people. Note that the ranges of risk aversion can depend on the size of the decision maker’s resource base—how large a loss can be sustained at all, and how large a loss can be absorbed without serious inconvenience or harm—and on the number of “bets” undertaken. An insurance purchaser has one bet (at least one per year) going, so he or she is exposed to the full uncertainty of the risk. An insurance company with many customers has many bets going, so the company’s annual loss experience will fit a much narrower range around the expected value, except in certain circumstances. If many customers are exposed to a common risk, such as will happen if many customers live in the same hurricane-prone region, the range of probable outcomes for the insurance company will be much wider. If the insurance company’s evaluation of the probabilities and consequences is seriously deficient or simply outdated, then its exposure may be quite different than it believes.

Utility and Disutility

For positive outcomes (gains), utility means a measurement scale for desirability [34]. It is a number measuring the attractiveness of a consequence—the higher the utility, the more desirable the consequence. A utility function translates monetary consequences into a scale for which expected-value calculations accurately reflect the preferences of an individual, a firm, or a decision maker. For negative outcomes (losses and costs), disutility is a measurement scale for undesirability—the higher the disutility, the less desirable the consequence.

The examples given earlier illustrate the fact that, for a specific person, firm, or decision-making entity, the value of gaining x dollars (or consequence of losing x dollars) is not necessarily x multiplied by the value of gaining a single dollar (or consequence of losing a single dollar). Issues of certainty and of the ability to accept loss can cause substantial deviations from the simple multiplicative relationship.

If it were possible to measure the true relative values to the decision maker of the various possible payoffs in a problem of decision making under uncertainty, expected values could be calculated in terms of these true values instead of the monetary values. The theory of utility seeks to develop such values, permitting choices to be analyzed using the decision-making rule—the maximization of expected utility or minimization of expected disutility. Utility theory provides a means of encoding risk preferences in such a way that the risky venture with the highest expected utility or lowest expected disutility is preferred. Symbolically, if the monetary value of the ith outcome is X i the utility corresponding to a gain X i is U(X i ) the disutility corresponding to a loss X i may be denoted by D(X i ).

Utility Functions

The mathematical structure of the function U(X) is central to the application of utility theory. Figure 79.1 graphically shows three typical utility functions that are usually encountered in this analysis [35]. The utility function represented by the straight line A is appropriate for a decision maker operating on an expected monetary value (EMV) basis. This line satisfies the equation U(X) = X and represents risk neutrality. The concave curve B corresponds to a risk-averse (or risk-avoiding) decision maker, and the convex curve C to a risk-prone (or risk-taking) decision maker. For a decision maker who is more risk prone than the EMV individual or who prefers a risk, the utility of a fair game exceeds the utility of not gambling and hence a fair game will always be played. On the other hand a decision maker who is more risk averse than the EMV person does not like or cannot afford risks and is a risk avoider.

Typical utility functions

Some individuals could have a sigmoid form of utility function as illustrated by Fig. 79.2. Such a person is a risk preferer for small values of X but a risk avoider for larger values.

Sigmoid utility function

Consider now a game with a 50 % chance of winning $100 and a 50 % chance of winning nothing, which has the expected value $50. The expected value line A in Fig. 79.1 connects the points [0, u(0)] and [100, u(100)]. To find the utility of the game for the risk avoider (curve B), find the utility value corresponding to the point on the straight line above the expected $50 value of the game. By reading to the left, cutting curve B, this value is equal to U($20) so that the decision maker’s cash equivalent (CE) for the game is $20. He or she would be willing to pay up to $20 to be able to participate in the game. This is still below the EMV of $50 since the utility function B is that of a risk avoider.

The difference between the EMV and CE is the risk premium, which is $30 in this example. The decision maker would be willing to pay $30 to avoid the risk involved in participating in the game.

In the case of the risk taker denoted by curve C, the utility of the game is equal to U($70), so $70 is the cash equivalent for the game. Although the expected value is only $50, the risk taker is willing to pay up to $70 to be able to participate in the game. Hence the risk premium is –$20. It is negative because the decision maker, instead of being willing to pay a premium to avoid the risk in the game, is willing to pay a premium (above and beyond the expected value) to be able to participate in the game.

The risk premium, RP, discussed above is the amount that a decision maker, on the basis of his or her utility function, is willing to pay to avoid or participate in a risky activity. For increasing utility functions such as those shown in Fig. 79.1, the risk premium for any risky venture is defined as

where EMV is the expected monetary value and CE the cash equivalent. The parameter CE is also referred to as certainty monetary equivalent, CME, in the literature on utility theory [36].

For a risk avoider whose increasing utility function is concave, the risk premium RP given by Equation 79.3, for any situation in which the outcome is uncertain, is positive (EMV is greater than CE). For a risk taker whose increasing utility function is convex, RP is negative. For a risk neutral person whose utility function is linear, RP is always zero (EMV = CE).

The CE is defined mathematically as

where the right-hand side is the expected value of the utility over the range of values taken by x. If x 1, x 2, . . ., x n are the values (consequences) with probabilities p 1, p 2, . . ., p n

If x is a continuous variable with probability density function h(x), the expected utility is given by

The CE or CME of a risky venture, V, is an amount, \( \widehat{x} \), such that the decision maker is indifferent between the risky venture, V, and the certain amount, \( \widehat{x} \). Put another way, \( \widehat{x} \) is the value for which U(\( \widehat{x} \)), the utility function on \( \widehat{x} \), is equal to the expected value of the utility function on the full range of possible outcomes.

The expected value of a random variable, x, is given by

or by

in the continuous case.

To illustrate the procedure for calculating a CE or CME, consider, as an example, the specific utility function

Suppose the decision maker is faced with a venture with two possible outcomes: x 1 with probability ½ and x 2 with probability ½. The expected value of the venture is

The certainty equivalent (CE) is therefore the solution to this equation:

It may be verified that for c = 1, x 1 = 10, and x 2 = 20, the certainty equivalent is

The expected value is

Consider a second example in which the risky venture has a continuous range of outcomes, ranging from 0 to 20, with an exponential probability density function

The expected value is

Suppose we further assume a utility function as

The certainty equivalent is given by \( \widehat{x} \) such that

Specific Probability Distributions for Utility Analysis of Fire Safety Choices

Based on the formulations just discussed, a utility analysis requires a probability distribution function for the outcomes of a risky choice and a utility function on those same outcomes. For a risky choice where fire loss is the source of risk, the key variable in differentiating the outcomes is the size of the fire loss (in monetary terms). Let that be defined as x.

Consider a property owner with an asset value of W. If a loss of x is incurred in a fire, the asset value would be reduced to

The property owner’s utility function will be defined in terms of the reduced asset value, rather than the fire loss, because the reduced asset value reflects the owner’s wealth and ability to absorb a loss. An appropriate utility function in terms of positive X would be

which is an increasing risk averse utility function [36].

Although the extent of risk aversion quantified by θ is constant for all X, this exponential utility function is widely used in view of its computational simplicity.

Next, in order to match the form of the utility function to the form of a distribution on probabilities of fire loss size, Equation 79.11 should be rewritten as

where W′ = e -θW and is a constant. As discussed earlier, the certainty equivalent \( \widehat{x} \) is given by solving the following equation for \( \widehat{x} \):

where v(x) is the probability density function of fire loss, x.

As x increases from zero, U(x) decreases from a value of –W′ A larger loss means a lower adjusted asset value and hence lower utility.

According to statistical studies carried out by Ramachandran [37–39], Shpilberg [40], and other authors, loss in a fire has a skewed (nonnormal) probability distribution. Ramachandran has concluded that a good fit is obtained from an exponential-type distribution applied to the logarithm, z, of fire loss size, x (i.e., z = log x follows an exponential distribution). Among distributions of this type, a normal distribution for z or a log-normal distribution for x is commonly used. An exponential distribution for z or a Pareto distribution for x has also been considered by some actuaries.

If the probability distribution function for fire loss is expressed in terms of z (= log x) instead of x, it will be computationally necessary to have a utility function expressed in terms of z as well. Ramachandran [41] has argued that z (= log x) may be used in Equation 79.12 instead of x so that the utility function is

which is equivalent to

The utility function in Equation 79.15 is a decreasing function with θ = 1 representing risk neutrality. The value of θ should be greater than unity to express a risk averse attitude. The degree of risk aversion increases with θ.

Consider a property worth total financial value V belonging to a risk category with fire loss x having a log-normal distribution. If μ and σ are the mean and standard deviation of z (= log x), following the method described by Ramachandran [1], the certainty equivalent for the range (0, V) is given by

where

and G(t) is the standard normal distribution. The expected monetary value of the loss is given by θ = 1 in Equation 79.16, because risk neutrality means utility is linearly related to loss. For a decreasing utility function (or increasing disutility function) such as Equation 79.15, the certainty equivalent, CE, is greater than the EMV.

For a property with a given level of fire protection, the CE corresponding to a given degree (θ) of risk averse attitude of the owner is the maximum insurance premium the owner will be willing to pay to meet the uncertain consequences of a fire. The CE will increase with θ; an owner more risk averse than another will be prepared to spend more money on insurance.

Both EMV and CE will decrease with increasing levels of fire protection. Hence, by adopting efficient fire protection measures, a property owner with a given degree of risk aversion can reduce the cost of the insurance premium. He or she can also obtain a further reduction in the premium by taking self-insurance for small losses.

References

G. Ramachandran, The Economics of Fire Protection, E & FN Spon, London (1998).

R.T.D. Wilmot (ed.), World Fire Statistics Centre Bulletin, Geneva Association, Geneva, Switzerland (1995).

W.P. Meade, “A First Pass at Computing the Cost of Fire Safety in a Modern Society,” NIST-GCR-91-592, National Institute of Standards and Technology, Building and Fire Research Laboratory, Gaithersburg, MD (1991).

J.R. Hall, Jr., The Total Cost of Fire in the United States, NFPA Fire Analysis & Research Division, Quincy, MA (2014).

“The Economic Cost of Fire,” Economist Intelligence Unit Ltd., unpublished report, London (1971).

“Investigation of Consequential Losses to the Economy from Fires,” PA Management Consultants Ltd., unpublished report, London (1977).

H.L. Hicks and R.R. Liebermann, “A Study of Indirect Fire Losses in Non-Residential Properties,” Fou-brand, 1, pp. 8–15 (1979).

J.M. Henderson and R.E. Quandt, Microeconomic Theory, Chapter 3, McGraw-Hill, New York (1971).

“MGM Fire Litigation,” Business Insurance, p. 10 (January 2, 1984); and “Fire at the MGM Grand,” Fire Journal, pp. 19 f. (January 1982).

T.J. Klem, “Los Angeles High-Rise Bank Fire,” Fire Journal, p. 85 (May/June 1989).

D.M. Halbfiner, “Incalculable Cost of One Meridian Fire,” Philadelphia Business Journal, February 24, 1992, pp. 1, 30.

M.S. Isner, “Telephone Central Office, Hinsdale, Illinois, May 8, 1988,” NFPA Fire Investigation Report, Quincy, MA (1989).

Fire and Explosion Hazards in the UK Pharmaceutical Industry, The Insurance Technical Bureau, London (1977).

Fire and Explosion Hazards in the UK Aerospace Industry, The Insurance Technical Bureau, London (1976).

Fire and Explosion Hazards in the UK Paint and Ink Manufacturing Industries, The Insurance Technical Bureau, London (1978).

L.-G. Benckert, “The Premium for Insurance Against Loss of Profit Due to Fire as a Function of the Period of Indemnity,” in Transactions of the 15th International Congress of Actuaries, New York, pp. 297–305 (1957).

D. Flach, J. Schlunz, and J. Straub, “An Analysis of German Fire Loss of Profits Statistics,” Blatter der Deutschen Gesellschaft fur Vesicherungsmathematik, Vol. X, Part 2 (1971).

D. Riley, Consequential Loss Insurance and Claims, Sweet and Maxwell Ltd., London (1967).

R.F.F. Dawson, “Current Costs of Road Accidents in Great Britain,” Report No. RRLLR 396, Road Research Laboratory, Crowthorne, UK (1971).

J. Linnerooth, “The Evaluation of Life Saving,” Research Report RR-75-21, International Institute of Applied Systems Analysis, Laxenbury, Austria (1975).

S.J. Melinek, “A Method of Evaluating Human Life for Economic Purposes,” Accident Analysis and Prevention, 6, p. 103 (1974).

J.P. Acton, “Measuring the Social Impact of Heart and Circulatory Disease Programs: Preliminary Framework and Estimates,” Rand R-1697/NHLI, Rand Corporation, Santa Monica, CA (1975).

G.W. Fischer and J.W. Vaupel, “A Lifespan Utility Model; Assessing Preferences for Consumption and Longevity,” working paper, Durham, NC (1976).

E. Keeler, “Models of Disease Costs and Their Use in Medical Research Resource Allocations,” P-4537, Rand Corporation, Santa Monica, CA (1970).

J.D. Graham and J.W. Vaupel, “Value of a Life: What Difference Does It Make?” Risk Analysis, 1, p. 89 (1981).

M.W. Jones-Lee (ed.), The Value of Life and Safety, Elsevier, North Holland, New York (1982).

G. Blomquist, Estimating the Value of Life and Safety: Recent Developments in the Value of Life and Safety, Elsevier, North Holland, New York (1982).

T.C. Schelling, “The Life You Save May Be Your Own,” in Problems in Public Expenditure Analysis, Brookings Institution, Washington, DC (1968).

G. Maycock, “Accident Modelling and Economic Evaluation,” Accident Analysis and Prevention, 18, p. 169 (1986).

S.G. Helzer, B. Buchbinder, and F.L. Offensend, “Decision Analysis of Strategies for Reducing Upholstered Furniture Fire Losses,” Technical Note 1101, National Bureau of Standards, Washington, DC (1979).

S.E. Chandler and R. Baldwin, “Furniture and Furnishings in the Home—Some Fire Statistics,” Fire and Materials, 7, p. 76 (1976).

I.C. Appleton, “A Cost-Benefit Analysis Applied to Foamed Plastics Ceilings,” Current Paper CP 50/77, Fire Research Station, Borehamwood, UK (1977).

M.W. Jones-Lee, The Value of Life: An Economic Analysis, Martin Robertson, London (1976).

J. von Neumann and O. Morgenstern, Theory of Games and Economic Behavior, Princeton University Press, Princeton (1947).

P.G. Moore, Risk in Business Decision, Longman Group, London (1972).

R.L. Keeney and H. Raiffa, Decisions with Multiple Objectives: Preferences and Value Trade-Offs, John Wiley and Sons, New York (1976).

G. Ramachandran, “Extreme Value Theory and Fire Losses—Further Results,” Fire Research Note No. 910, Fire Research Station, Borehamwood, UK (1972).

G. Ramachandran, “Extreme Value Theory and Large Fire Losses,” ASTIN Bulletin, 7, p. 293 (1974).

G. Ramachandran, “Extreme Order Statistics in Large Samples from Exponential Type Distributions and Their Application to Fire Loss,” in Statistical Distributions in Scientific Work, 355, D. Reidel, Dordrecht, Netherlands (1975).

D.C. Shpilberg, “Risk Insurance and Fire Protection; A Systems Approach. Part 1: Modelling the Probability Distribution of Fire Loss Amount,” Technical Report No. 22431, Factory Mutual Research Corp., Norwood, MA (1974).

G. Ramachandran, The Interaction Between Fire Protection and Insurance, Seminar, Zurich, Switzerland (1984).

Author information

Authors and Affiliations

Editor information

Editors and Affiliations

Rights and permissions

Copyright information

© 2016 Society of Fire Protection Engineers

About this chapter

Cite this chapter

Ramachandran, G., Hall, J.R. (2016). Measuring Consequences in Economic Terms. In: Hurley, M.J., et al. SFPE Handbook of Fire Protection Engineering. Springer, New York, NY. https://doi.org/10.1007/978-1-4939-2565-0_79

Download citation

DOI: https://doi.org/10.1007/978-1-4939-2565-0_79

Publisher Name: Springer, New York, NY

Print ISBN: 978-1-4939-2564-3

Online ISBN: 978-1-4939-2565-0

eBook Packages: EngineeringEngineering (R0)