Abstract

Fires can lead to costly building damage as well as loss of lives and injuries. Installed to protect buildings from fire, or to limit the damage from such outbreaks, fire protection measures are a common feature in buildings. However, these features come at a cost. Although quite ubiquitous in buildings, the value of these features to private individuals and to society is not fully understood. To understand their value, a cost benefit analysis detailing the costs and benefits of fire protection measures is needed. Carrying out such an analysis requires methods for computing both the cost of these fire protection measures, and losses from fires (including both direct and indirect losses). This study outlines methodologies for evaluating those costs and losses. An exhaustive collection of available data necessary for estimating both costs and losses is presented. Several limitations in current methodologies and data constraints were identified, with recommendations proposed to address these shortcomings. Relevant sections of a study by the authors that refines fire protection cost estimation at national and sub-national levels are emphasized, including updated building categories, guidance on computing multipliers, and detailed cost calculation methods for installation and maintenance costs. The calculation uses regularly updated U.S. Census Bureau construction data, ensuring timely multiplier updates. The insights and suggestions presented in this study will ultimately refine the process of selecting fire protection strategies that maximize the net benefit of fire protection measures for both private stakeholders and society at large.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

The expenditure on fire in the United States in 2014 was around $328.5 billion, making up about 1.9% of the total gross domestic product (GDP) [1]. Between 1980 and 2014, the total fire costs increased by 50.3% albeit the cost as a percentage of GDP dropped significantly from 7.6% to 1.9% [1]. These costs include the value of losses incurred due to fire and the cost expended to both protect against fires and mitigate their effects. Similarly, studies around the globe show significant annual costs of fire [2,3,4,5,6]. To optimize the benefits to society, it is crucial to allocate resources for fire protection efficiently, especially given the limitations on societal resources. To ensure optimal allocation of resources, the impact and cost of fire protection measures, both to private entities and to society, needs to be accurately measured. Fire protection measures are the strategies, systems, and practices designed to prevent the onset of fires, limit the spread and intensity of fires, and ensure the safety of people and assets in the event of a fire. These measures can be both passive and active in nature.

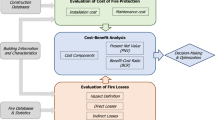

In selecting fire protection measures, efforts are geared towards reducing the risk of fire, with the understanding that it is not practicable to reduce fire risks to zero. In this regard, the criterion “As Low as Reasonably Practicable (ALARP)” denotes that a balance must be struck between the reduction of fire risk through the implementation of fire protection measures and their cost [7, 8]. To determine if a design meets the ALARP requirement, a cost benefit analysis (CBA) can be performed. CBA is a method for quantifying the costs and benefits of projects and can be an efficient means of determining the effectiveness of safety investments [8,9,10,11]. In fire protection applications, CBA is valuable to both policy makers who develop laws and guidelines prescribing fire safety measures, and private decision makers, offering a structured approach for comparing alternative fire protection strategies to decide on the preferred measures.

Carrying out a CBA for fire protection requires cost evaluation of both the expenditure on fire protection measures and the losses expected from fire incidences. When using CBA to assess a particular fire protection measure, the benefit derived from the presence of the measure is equated to the prevention of anticipated fire losses that would occur without this safety investment. Each of these cost categories has several sub-categories, encompassing the different costs associated with them [1,2,3]. For example, fire losses can be divided into direct losses (damage caused to a building, its contents and occupants during the course of a fire) and indirect losses (costs associated with a fire after it is extinguished) [12]. In addition, within each level of decision making (private or societal), the valuation of costs and benefits will generally be different. For instance, private businesses may be concerned with the immediate costs and attendant benefits of fire protection measures in their building, while local and national authorities may consider that this business loss in one enterprise is compensated by an uptake in commercial activity by its competitors. This myriad of components, each requiring specific methods of estimation, makes carrying out a CBA in fire protection a challenging exercise.

Over the last three decades, several attempts have been made to quantify the cost of fire protection and the losses due to fire incidents [1,2,3,4,5]. Also, CBAs of fire protection measures that can mitigate fire risk or reduce fire losses, have been the subject of some studies [12,13,14,15,16,17,18,19,20]. However, there is no established methodology for carrying out the CBA for fire protection measures. In an effort to address this gap, a recent project was undertaken to develop a methodology for the CBA of fire protection measures in buildings [21]. This methodology considers the costs associated with the systems, potential losses from fire outbreaks, and the benefits of having these systems in place. A critical aspect of this CBA is estimating the expenditure on fire protection and the potential losses resulting from fire outbreaks. This study, prompted by the lack of established methodologies to accurately determine these components of the CBA, presents the state of the art of the estimation of fire costs (cost of fire protection and fire losses) and also proposes reference methodologies for such cost estimations. This involves identifying the processes for each component, collecting data necessary for the cost estimation, as well as identifying shortcomings within the established methodologies and gaps in the data required for the cost estimation. Strategies aimed at overcoming the shortcomings and bridging the gaps in data are presented, and a holistic methodology for estimating national-level or subnational-level expenditures on fire protection is also delineated. The discussions in this paper are the outcome of the project entitled “Economic Impact of Fire: Cost and Impact of Fire Protection in Buildings” [21] which was carried out from October 2021 to July 2022 with the support of the Fire Protection Research Foundation (the research affiliate of the National Fire Protection Association).

2 Scope of Literature Review

In developing a methodology for the CBA of fire protection measures in buildings, a number of compositional elements need to be considered. These include the cost of installation and maintenance of the systems, the value derived from these systems, and the possible losses to individuals and society in the event of a fire outbreak if these systems are not in place. Each of these components requires a methodology for estimating a quantifiable value which can be used in the CBA.

To this end, this study examined existing literature on estimating expenditures on fire protection in buildings and losses from building fires to present reference methodologies for the estimation of these costs. The collected studies focused principally on fire in buildings, its costs, frequency, and severity in various parts of the world. Data sources for estimating the components of CBA analysis (including cost of building construction, cost of installation and maintenance of fire protection measures, and fire loss statistics) were identified. In addition, research into methods for overcoming peculiar challenges, such as the effect of time on value, were also collected for the accurate calculation of costs and benefits.

The literature references were identified through references recommended by the project advisory committee as listed in [21], keyword searches in academic repositories (Google Scholar, Scopus, etc.), references known to the authors from previous studies, and secondary referencing from sources cited within other publications. The search was halted once it seemed that additional references consistently mirrored ideas in the already collected publications. Eventually, this led to the collection of a sizable number of reference materials. In total, approximately 100 independent reference sources were collected and used.

This study focuses on fire protection measures for buildings, and it analyses the main cost components related to fire (i.e., cost of fire protection and fire losses); some aspects of fire costs, for instance the cost of fire departments and the cost of insurance, are not discussed. In the subsequent sections, methods currently used for estimating the cost of fire protection and those used in estimating fire losses are presented and analysed. Limitations of the existing methods, possible methods for overcoming some of these limitations, and existing data sources needed for the presented methods are also delineated in separate sections.

3 Cost of Fire Protection

The cost of fire protection can be estimated at two distinct levels: the micro level and the macro level. The micro level cost (Sect. 3.1) consists of the costs of installation (Sect. 3.1.1) and maintenance (Sect. 3.1.2) of fire protection measures in a specific building. The macro level cost of fire protection is an aggregation of the cost of these measures for all the buildings at the national or sub-national levels of society. The most commonly used method for computing the macro level cost is the method of multipliers, as discussed in Sect. 3.2.1. An alternative method, involving extrapolating the expenditure on fire protection from sales data on the cost of fire protection materials and equipment sold within the time period under investigation, is laid out in Sect. 3.2.2.

3.1 Micro Level Cost Estimation

The overall methodology for estimating the installation and maintenance cost of fire protection measures at the micro level is illustrated in Figure 1. While the installation costs are relatively straightforward to estimate, the costs associated with maintenance requires more nuance and are dependent on the type of fire protection measure in question. Also, not all costs of fire protection can be readily related to the direct costs of installation and maintenance. For example, [12, 22] included in the cost of fire stairs, the revenue lost due to their presence, assuming that the stairs take up space that could alternatively be useable floor area.

Methodology for computing the cost of fire protection at the micro level

3.1.1 Installation Cost

Fire protection measures at the micro level are usually categorized into active and passive. Active fire protection measures refer to measures that are activated upon the outbreak of a fire such as fire sprinklers, ventilation systems, automatic detectors, fire extinguishers and emergency lighting systems. Passive fire protection measures include systems which act to forestall the spread and/or effect of fires without being activated. These include such systems as a means of egress, fire separation elements (walls, doors, and slabs), and structural elements’ fire protection.

Studies into the cost of fire protection at the micro level have focused primarily on calculating the cost of installing these systems. These installation costs vary among the different fire protection measures in use and are generally determined by estimating unit costs and multiplying the unit costs by quantities required. Most commonly, this simply involves identifying and obtaining costs for materials, labor and equipment needed for the systems [12, 14,15,16,17,18, 23,24,25,26,27,28,29,30,31]. Alternatively, some studies propose computing the cost of a fire protection measure as a function of another important variable. For example, Esposito computed the cost of fire-resistant elements (walls, doors, and slabs) as a function of their fire resistance rating (FRR) [32]. Also, regarding structural fire protection, some studies propose estimating the cost of the systems as the difference between the cost of the structural elements with fire protection, and alternative structural elements without the added fire protection [33].

In line with these previous studies, a procedure for computing the cost of fire protection measures at the micro level is presented below. This procedure encompasses the cost of installation of both active and passive fire protection measures in an individual building, and also forms the basis for determining the macro level cost of fire protection through multipliers.

-

(1)

Identify the fire protection measures to be used in the building. This could be a combination of passive and active fire protection measures.

-

(2)

Determine the components (e.g., fire sprinkler heads) and materials (e.g., sprayed fire-resistant materials) needed for the fire protection measures, along with their quantities.

-

(3)

Compute the cost of the identified materials, as well as the corresponding cost of labor and equipment needed for installation, using regularly updated data obtained from relevant construction cost manuals and databases. This is then taken as the initial cost of installing a fire protection measure. For passive fire protection measures which are a part of the building system, e.g., a fire-resistant wall which is also a structural wall, the cost of fire protection can be the difference in the costs of these systems and the cost of alternatives which are not fire resistant.

-

(4)

Evaluate the total initial installation cost of the fire protection measures as the sum of installation costs of the different fire protection measures in a building, using Equation 1. Any replacement of a fire protection measure’s components after the initial installation of the system will be considered as maintenance cost. If a building’s design life is used as the timeframe for cost calculation, any potential replacement of a whole fire protection measure after the initial installation but before the end of the building’s design life is also considered as maintenance cost.

$$C_{I} = \mathop \sum \limits_{j = 1}^{n} C_{Ij}$$(1)where CI is the total installation cost of fire protection in a building, n is the number of fire protection measures in the building, and CI,j is the initial cost of installing fire protection measure j.

-

(5)

Alternatively, an equivalent annual cost of fire protection can be computed, considering continuous discounting. An annualized calculation can be convenient when not all fire protection measures have the same design life. Equation 2 is used to compute the annual continuous discounted installation costs.

$$c_{I} = \mathop \sum \limits_{j = 1}^{n} \frac{{C_{Ij} \times \gamma }}{{\left( {1 - e^{ - \gamma L} } \right)}}$$(2)where cI is the annual continuous discounted installation cost of fire protection in a building, CIj is the initial cost of installing fire protection measure j, γ is the continuous discount rate, L is the timeframe considered, and n is the number of fire protection measures in the building.

Data for computing the micro level cost of fire protection can be obtained from cost reference manuals. These include the RSMeans datasets, particularly the Facilities Construction Cost Data manual [34] and the Residential Costs manual [35], both of which contain the cost of materials, labor and equipment necessary for installing fire protection measures in buildings in the United States. RSMeans data are also available as a searchable online database [36], providing a quick way to find reliable cost data on construction materials, equipment and labor. The RSMeans online database can also help a user to build complete estimates according to a building’s information. Data sources for other countries include the British Building Cost Information Service (BCIS) [37], SCI documents [38, 39], and the Rawlinson’s Australian handbook of construction [40]. In addition, commercial software is also available to estimate prices within the construction industry, for instance Xactimate developed by Xactware to support decision-making in the insurance market [41].

As can be seen from the range of available data sources, there is readily available data for the estimation of these micro level costs. However, these data sources have some shortcomings, especially in completeness. Although quite comprehensive on some commonly used fire protection measures such as sprinkler systems, the data sources do not provide explicit information on other systems such as passive fire protection measures of different fire ratings. Information on such systems requires extrapolation from the cost associated with their constituent components.

3.1.2 Maintenance Cost

The maintenance cost could either consist of a single cost for a whole system or be an aggregation of costs for the maintenance of components making up the system. These maintenance costs are usually accrued periodically over the design life of the system. Thus, in computing the maintenance costs, it becomes necessary to either annualize these maintenance costs, or calculate their present value (PV) over the design life, ensuring a common time frame of reference.

Most reviewed studies focus on computing the initial cost of fire protection measures and do not consider the recurrent cost of maintenance. A few studies do include the cost of maintenance of these systems, computing these costs as a percentage of the initial capital costs, e.g., [5, 12, 13, 16]. A step-by-step procedure for computing the maintenance costs is given below. As mentioned in Sect. 3.1.1, the replacement of any components within a fire protection measure after its initial installation will be categorized as maintenance costs. Additionally, if a building's design life serves as the timeframe for cost calculations, any potential full replacement of a fire protection measure after its first installation but before the building's design life concludes is also regarded as a maintenance expense.

-

(1)

Identify the components of a fire protection measure that will require maintenance over the design life of the system.

-

(2)

The maintenance period of the components and their corresponding costs can then be obtained from maintenance cost reference manuals and databases. This information is essential for determining the maintenance costs associated with each time point throughout the design life of the fire protection measure or the building’s design life.

-

(3)

The annual maintenance cost for a fire protection measure is then computed as shown in Equation 3.

$$c_{Mj} = \mathop \sum \limits_{k = 1}^{{u_{j} }} \frac{{C_{Mj,k} \times \gamma }}{{\left( {1 - e^{ - \gamma L} } \right)}}$$(3)where \({c}_{Mj}\) is the annual cost of maintenance for a fire protection measure j, \({u}_{j}\) is the number of components of the fire protection measure j that require maintenance, \({C}_{Mj,k}\) is the present maintenance cost of component k of the fire protection measure j, γ is the discount rate, and L is the timeframe considered.

-

(4)

The total annual cost of maintenance, can then be computed as:

$$c_{M} = \mathop \sum \limits_{j = 1}^{n} c_{Mj}$$(4)where cM is the annualized cost of maintenance for all fire protection measures for the building, n is the number of fire protection measures present in the building, and \({c}_{Mj}\) is the annual maintenance cost of fire protection measure j.

-

(5)

Alternatively, the PV cost can be used to determine the cost of the maintenance of the fire protection measure at a common reference time point as shown in Equation 5 and the total discounted cost of the maintenance of fire protection measures for the entire building can then be computed as shown in Equation 6.

$$C_{Mj} = \frac{{c_{Mj} }}{\gamma }\left( {1 - e^{ - \gamma L} } \right)$$(5)$$C_{M} = \mathop \sum \limits_{j = 1}^{n} C_{Mj}$$(6)where CMj is the discounted PV cost of maintenance for a single fire protection measure j, \({c}_{Mj}\) is the computed annual cost of maintenance for the fire protection measure j, γ is the continuous discount rate, L is the timeframe considered, CM is the total discounted PV cost of maintenance for fire protection for the building, and n is the number of fire protection measures in the building.

All the cost calculation in Equations 2, 3 and 5 should be conducted within the same time frame. If those costs are calculated for the purpose of comparing two different fire protection measures, the time frame can be the building design life. However, if only one specific fire protection measure is evaluated, the timeframe for the calculation in those equations can be the design life of this specific fire protection measure. In certain scenarios, shorter depreciation period may be used for financial purposes.

Data for computing the maintenance cost of fire protection measures can be found in the Whitestone Building Maintenance and Repair reference book [42], the RSMeans Facilities Maintenance and Repair costs manual [43], and also in the searchable RSMeans online database [36]. However, data on maintenance costs for fire protection measures is quite limited, especially for passive fire protection measures. Therefore, the maintenance costs of such systems need to either be assessed through expert judgement or extrapolated as a percentage of the installation costs.

3.2 Macro Level Cost Estimation

The cost of fire protection at the macro level is an estimation of the total amount spent on fire protection in buildings at the national or sub-national level. Two methods for estimating such information are commonly used. These are: (i) cost multipliers as a fraction of the total cost of construction, and (ii) using sales data.

3.2.1 Cost Multipliers

This approach to computing the macro level cost of fire protection depends on knowledge of the micro level costs, and of the total cost of construction put in place at the macro level. When pre-established multipliers are available, estimating the macro level cost of fire protection reduces to obtaining an estimate for the total cost of construction and applying the multipliers.

To apply this approach, buildings are first divided into categories. Ideally, each category would contain buildings with similar fire protection requirements. Some previous studies into the total cost of fire have divided buildings into four categories namely private residential, private non-residential, public and other private building construction [2]. Other studies classified buildings into three categories, omitting the ‘other private building construction’ category [1, 3, 4]. However, one shortcoming in these classifications is the sheer variety of buildings lumped together in each category, with no consideration for the variation in the cost of fire protection. Schaenman et al. [5] attempted to address this, naming new sub-categories for residential buildings, and offering categories for other buildings with respect to their use in order to improve uniformity in the buildings grouped together. The categories considered were residential with sub-categories for single homes, semi-detached, low-rise apartments, high-rise apartments, and cottage & mobile homes; industrial buildings; commercial buildings; institutional buildings; and other buildings. Despite this improvement, the non-residential building categories still cover broad swathes of building types without any justification as to if the fire protection costs of the different buildings are similar enough to have them in a single category.

After categorization, prototype buildings are selected to represent each category, and the ratio of the micro-level fire protection cost and building construction cost of a prototype building in one category then define the multiplier of fire protection cost for that specific category, as shown in Equation 7. A prototype building is defined as a building with fire protection measures that represent the fire protection requirements of all buildings in a category. Table 1 summarizes the cost multipliers for the different building categories discussed in the studies listed. Some studies have computed cost multipliers for the aforementioned building categories, by utilizing industry professionals (i.e., experts) in determining the fraction of building costs that went into fire protection measures [44, 45]. Other studies developed multipliers using published cost data from prototype buildings [4, 5, 40, 46].

where CFPi is the cost of fire protection for a prototype building in category i, CBi is the cost of construction of the prototype building, and αi is the cost multiplier for fire protection for category i.

The construction cost of a prototype building as required in Equation 7, is commonly estimated based on construction statistics and databases. Another approach is based on the Real Market Value (RMV) of a building [47, 48]. The cost of installing fire protection measures as part of the initial construction can be estimated by the fire protection cost per square foot multiplied by the floor area. Alternatively, the micro level evaluation introduced in Sect. 3.1 can be applied. The building content and equipment are not included in these costs.

Once these multipliers are determined, the total cost of fire protection across all building categories can then be computed by summing up the costs obtained for each category, as presented in Equation 8.

where Cfp is the macro level annual expenditure on fire protection, αi is the cost multiplier for building category i, m is the number of building categories, and Ci is the annual construction expenditure on buildings in category i. The annual construction spending on buildings in each category can be collected from data sources such as the U.S. Census Bureau [49].

To determine a representative multiplier for a category, multiple prototype buildings need to be sampled in a statistical way and an overall multiplier calculated. However, this method may not be practical. Instead, a few prototype buildings from the same category can be simply selected and an average multiplier computed. The number of buildings used to represent a category should be carefully considered, as fewer buildings increase the importance of accurately selecting representative prototypes. At the extreme, only one building can represent each category, but it must be carefully selected to accurately represent the average building in a category.

The method of multipliers has some advantages in computing the macro-level cost of fire protection. Firstly, construction cost data for calculating multipliers is readily available and frequently updated. Secondly, national expenditure data for building construction required by the method is also readily accessible and updated, although the data are not always categorized in a way that allows accurate estimation of fire protection expenditure. Also, the process of computing macro cost is straightforward once the multipliers have been established. However, this method also has limitations. It is challenging to categorize buildings in a way that not only provide easily accessible data on construction expenditure but also groups buildings with very similar fire protection requirements in each category. Selecting representative prototype buildings for a category is challenging, limiting the accuracy of using multipliers for the whole category. Additionally, calculating fire protection and overall construction costs can be time-consuming, especially if details on materials, labor, and equipment are not readily available. These challenges with the method of multipliers have led to studies [1,2,3] continuing to use multipliers computed decades ago [44, 45] and also utilizing a very limited number of building categories when estimating the macro-level cost of fire protection. However, Researchers [53] urged caution in using the multipliers put forward by [45], deeming that the numbers proposed were not adequately substantiated.

The authors have proposed an update to the existing multiplier methods, which is illustrated in Figure 2 [21]. This update includes new building categories and offers suggestions for calculating representative multipliers. The categorization, called Modified U.S. Census Bureau Categorization, is based on the U.S. Census Bureau’s 11 distinct building categories which provides regular data on construction expenditure [49]. The U.S. Census Bureau categorization classifies private residential buildings into subcategories for single family homes (including new houses and townhouses), and multi-family buildings. This study proposes further subdividing the multi-family buildings into low-rise and high-rise buildings. Multi-family dwellings up to 75 ft (22.86 m) above the lowest floor accessible to fire department vehicles are classified under low-rise multi-family buildings, while any residential building beyond this height is classified as high rise as defined by NFPA and IBC codes [50, 51].This division is necessitated by the fact that the fire protection requirements change significantly between low-rise buildings and high-rise buildings. The final categories are shown in Table 2, with 12 proposed categories. Comparatively, studies reviewed in Table 1 commonly used 3 or 4 categories, except for [5] which used 9. This proposed categorization anticipates achieving a favourable balance between estimation accuracy and data availability. Other publicly available building categorizations, such as those from the Federal Emergency Management Agency (FEMA) [52], the National Fire Protection Association (NFPA) [51], and the International Building Code (IBC) [50], have some similarities with that of the Census Bureau. Table 2 shows all four categorizations. An analysis of the categorizations reveals both similarities and notable distinctions across various categorizations. These discrepancies can be attributed to the distinct objectives that each categorization serves. For instance, the NFPA classification, which primarily focuses on fire protection requisites for buildings, exhibits certain parallels as well as deviations from the categorization employed by the U.S. Census Bureau. Also, certain building types that NFPA designates as residential are assigned to specific non-residential categories within the U.S. Census Bureau’s framework. In the present study, the U.S. Census Bureau's classification was selected as the foundational framework due to data availability. The U.S. Census Bureau provides regularly updated construction expenditure data for each category, including separate data for privately-owned single-family homes and multi-family buildings. Although it only presents aggregated data for all residential construction in the public domain, a reasonable inference can be drawn that residential buildings constructed by public entities would be multi-family dwellings. Consequently, incorporating this data into the private multi-family construction figures can yield a comprehensive value for expenditure on multi-family residential structures. However, the U.S. Census Bureau does not provide data for high-rise multi-family and low-rise multi-family buildings separately.

Methodology for estimation of fire protection cost at the macro level

3.2.2 Sales Data

This alternative method of computing the macro level cost of fire protection, involves collecting data from manufacturers and installers of fire protection measures on their sales over a defined period [5]. These data can then be used to estimate the total expenditure on fire protection measures at the macro level. In theory, this method might offer a comprehensive view of periodic cost for fire protection measures at a broad level, encompassing new construction and improvements (e.g., renovations, retrofits and repairs). However, it doesn’t differentiate building-specific data from overall construction data, and thus it may be difficult to extrapolate the expenditure on fire protection that specifically goes into buildings. It may be also difficult to obtain such data due to the large number and geographical spread of manufacturers of the components of fire protection measures. Also, this method does not consider costs of labor and equipment used for installation, which form an intrinsic part of the total cost of these systems. In addition, while accurate for active fire protection measures, this method may not capture the costs of passive fire protection materials, such as concrete, which may already be an intrinsic part of the building construction. To this end, the method of using multipliers computed as a fraction of the cost of construction remains the more popular method in use.

4 Cost of Fire Losses

Fires in buildings can endanger human life and properties, and cause indirect or consequential financial, social and environmental losses. In categorizing fire losses, the categories of those losses could vary based on country, specific context, priorities of a specific study, the sponsor of a specific study, and the quantity and quality of available data [53]. There are three important aspects in computing the losses resulting from a fire: definition of the hazard, estimation of direct losses from the fire, and estimation of indirect losses. Definition of the hazard level, examined in Sect. 4.2, consists of analysing both the fire frequency (Sect. 4.2.1) and the fire severity (Sect. 4.2.2). Direct losses (Sect. 4.3), refer to losses directly attributable to the fire. These include property losses and human losses. Indirect losses, explored in Sect. 4.4, refer to negative impacts on individuals and society, which can indirectly be traced back to the fire. These losses can be considered from the perspective of the individual or private entities, as well as from a societal perspective. It is imperative to consider these variables when estimating probable losses for a CBA of fire protection measures.

4.1 Methodology for Determination of Losses

The losses caused by a fire event are inherently “uncertain” and difficult to estimate in any a priori analysis. Furthermore, the costs associated to a fire need to consider the likelihood (probability) of fire occurrence as well as the probable damage due to fire. The probable damage is affected by a large number of parameters and requires a series of assumptions. In particular, the probable reduction in fire damage related to a specific fire safety measure is challenging to quantify. Methodologies for loss estimation as a result of natural hazards are usually in three domains [38]. The “hazard domain” typically defines the hazard characteristics, usually in terms of frequency of occurrence and intensity measure. The “damage domain” investigates the relationship between the defined hazard and the level of damage or consequences caused by the hazard. Finally, the “loss or cost domain” aims at translating the damage and consequences into a quantification of loss (both direct and indirect): this is commonly done on a monetary level because it is the common ground in which different consequences and losses can be easily associated with a cost. A flowchart illustrating the methodology recommended by this study and the main steps to estimate the losses caused by a fire event in buildings are shown in Figure 3. Note that the examples of indirect losses shown in the flow chart are some major examples for building fires and do not represent every type of loss that could be experienced in a fire.

Flowchart illustrating the prototype methodology for estimation of fire losses in buildings

4.2 Hazard Definition

The first step for the estimation of losses caused by any hazard typically concerns the definition of the hazard itself. Similar to approaches adopted for windstorms and earthquakes [54, 55], tsunamis [48], and tornadoes [47], fire is generally defined in terms of fire frequency (probability or return period) and fire severity (intensity measure). For instance, some studies [38, 56, 57] have proposed estimating fire losses by adopting the PEER framework that was originally developed to assess the performance of building systems and consequential damages due to earthquakes [58]. In those studies, the initial step of their analysis defines “hazard domain” in terms of fire frequency and fire severity.

4.2.1 Fire Frequency

Fires in buildings can be generally divided into two categories. “Fire ignitions” referring to any fire that is triggered in a building, irrespective of its size, and “structurally-significant fires” referring to any fire that may achieve flashover and challenge the structural integrity and stability of a load-bearing system. It is important to highlight that, in its definition, structurally-significant fires already include the failure of various fire protection measures aimed at preventing, controlling, or extinguishing the fire before reaching flashover.

A common source for quantifying the probability of fire occurrence is fire statistics databases collected and reported by different authorities, at the regional or national level [59,60,61,62,63]. Given the varied characteristics of fire hazards and the diverse regulations around the world, the fire frequency in these databases is typically highly dependent on examined geographical area or country, and reported by local authorities. Nominal probabilities of fire occurrence for structurally-significant fires can also be found in national and international standards such as Eurocode 1 [64, 65]. The effects of certain fire protection measures on the fire-induced losses can be only estimated by understanding how different systems affect the probability of occurrence of fire ignition or a structurally-significant fire. In the Eurocode, this is taken into consideration by defining different conditional probabilities of a structurally-significant fire, depending on the installed fire protection measures (e.g., automatic sprinklers systems, automatic alarm system, time to fire service intervention) [64, 65]. Reduction factors or conditional probabilities for different fire protection measures can be found in several studies, depending on their focus (e.g., automatic sprinklers systems) [12, 63, 66]. In other studies, fire statistics have been used to characterize various analytical or more complex models to estimate the fire frequency in a specific building [67,68,69,70]. Generally, in these models, the probability of fire occurrence is expressed as a function of the building occupancy and size (total area or volume) [12, 71].

These fire statistics data collected in the databases [59,60,61,62,63] are also used to help policy makers decide on ways to improve fire safety according to the most likely cause of fire and the most likely place where a building’s occupants may suffer injuries or fatalities. However, these databases only contain data on relevant fires attended by public fire departments, fires where fatalities or significant injuries may have occurred, or fires causing extensive damage, excluding small or quickly extinguished fires. Consequently, they cannot be considered as fully reliable sources to estimate the probability of fire ignition [12, 72]. Greene and Andres [73] used surveys to assess the ratio of unreported to reported fires, noting that reported fires are commonly used in the calculation of those fire statistics, as those data are more readily available. In general, for any assessment involving fire statistics, it is very important to keep in mind the number of fires on which the data is based. In some cases, a great deal of confidence can be placed on certain analyses related to fire due to the very large number of fires used in the analyses, while in other cases using databases with relatively few fires, caution must be exercised in drawing conclusions.

4.2.2 Fire Severity

While the frequency of occurrence of a fire plays a key role in any probabilistic analysis aimed at loss estimation, the definition of the fire scenario-referred to here as fire severity-is fundamental for estimating the damage to property and people, and subsequently, the overall fire losses. The definition of fire severity depends highly on which type of damage or loss is the objective of the analysis, and the fire scenario is defined accordingly. For instance, in a life safety analysis in which the fire growth phase is key, a typical pre-flashover fire (heat release rate curve) can be the suitable option to investigate the fire dynamics and smoke movement and ensure safe evacuation of a building’s occupants [74]. On the contrary, a post-flashover fire (or structurally-significant fire) is a more relevant scenario in analyses focused on ensuring structural integrity and stability during and after a fire, as well as safe operation of fire and rescue services. In either of these cases, various approaches or models can be adopted to specify fire curves, generally defined in terms of a time-history of adiabatic surface temperature of fire-exposed structural elements. For post-flashover fires, the most used approaches are the standard temperature–time fire curve, typically for regulatory purposes, and the Eurocode parametric fire curves to reproduce natural fire exposures for performance-based design [64]. In addition to the fire exposure definition, the mentioned models can also be detailed at probabilistic level. Examples are offered by [38, 57], in which the main input parameters of the Eurocode parametric fire curves (i.e., fire load density, fire growth rate, compartment opening factor and thermal inertia of the enclosure boundaries) were defined with specific probability distributions. This enabled a probabilistic definition of the fire exposure, hence a probabilistic estimation of the fire-induced damages and losses.

4.3 Direct Losses

Direct losses are losses which can be directly attributed to the fires [12]. These are generally divided into property losses and human losses. Property losses are estimated as the sum of damage to buildings and their components during the fire. Human losses on the other hand are related to human deaths and injuries from fire incidents, quantified by the monetary value needed for reducing the likelihood of such losses.

4.3.1 Property Losses

Buildings are composed of both structural and non-structural systems, and contain items of varying valuation. In general, to estimate direct property losses due to fires, it is important to consider all these components, both within and outside the immediately affected fire compartment(s). The structural system itself typically represents only about 25% of the building’s worth [75]. In fact, for certain building occupancies, the damage to non-structural systems and contents tend to dominate economic loss [75]. In determining direct losses to property, two approaches are commonly used: a statistical approach and a modelling approach.

In applying a statistical approach, fire statistics are employed to assess fire-induced damage in buildings [76]. Fire statistics databases such as the National Fire Incident Reporting System (NFIRS) [60] and the British Fire Protection Association (FPA) Large Loss Database [62] can be used to estimate the average fire damaged area. This value can in turn be used to quantify the fire loss as a product of the fire-damaged area and the construction cost per unit area (specified according to the building characteristics, and computed from construction cost databases, handbooks or software) [68, 69]. In some instances, fire statistics can also offer direct cost estimates for fire incidences. For instance, the NFIRS database provided by the U.S. Fire Administration reports loss estimates made by fire response personnel. However, while this estimation of fire loss includes contents damaged by fire, smoke, water and overhaul, it does not include indirect loss, such as business interruption [77].

These fire statistics can be also processed for general analyses. For example, by plotting the fire loss against the damaged area, trend lines can be included to provide predictive models for estimating an average fire cost given an average damage area [12]. Such relationships usually vary depending on the building occupancy and fire risk category, and can be updated regularly according to the latest fire statistics and financial trends (e.g., inflation) [72].

However, there are some drawbacks with using fire statistics data in estimating losses. First, by nature, this data is highly subjective and hard to verify because it is based on loss adjusters’ experience and judgement. Also, these databases only contain data on relevant fires attended by public fire departments with serious injuries and/or fatalities, or extensive damage. Therefore, the data excludes small fires or fires extinguished by suppression systems. Thus, the use of said data to inform generalized fire loss models could lead to an over-estimation of costs as all fires within the dataset will be the larger, more expensive fires [12, 72]. Alternatively, other types of data sources can be used to estimate fire-related losses. For example, building fire losses can be assessed from the insured value, a method used in [71] which employed three different sources of Swiss fire insurance data (1995–2009), or from the Real Market Value (RMV) of the building determined from the U.S. Census [47,48,49]. Using data sources of various natures (e.g., insurance-focus vs. fire-service-based) can result in significantly different estimates, particularly for certain building occupancies [72].

It is quite challenging to associate the effect of different fire protection measures with the damage and the loss due to fire using fully statistical approaches. In the available fire statistics, the level of detail required is rarely present. As a consequence, there has been a recent push for collecting fire statistics of higher quality, with additional and more structured information [70]. However, even without such information, the effect of different fire protection measures can be explicitly included in other ways, for example by suggesting reduction factors for the probability of fire occurrence and fire severity.

Unlike statistical approaches, modelling-based approaches mainly rely on detailed models and simulations to quantify the resulting damages and losses. Advanced examples are computational fluid dynamics models or finite element models [38, 57, 78]. Such numerical models can be used in quantifying damage to the buildings (structural and non-structural systems), as well as to the contents of the buildings.

Depending on defined hazard scenarios, the modelling approach can be used in quantifying damage to structural and non-structural elements of buildings, either with or without a probabilistic distribution. The damage definitions are usually not on a continuous scale, but categorized into a number of classes, each representing a different level of damage, with respect to the building’s physical condition [38, 55, 57, 75].

After damage assessment and consequent categorization of damage, the replacement or repair cost of a building’s elements are usually estimated according to damage classes and building occupancy [38, 55, 57]. This is determined either as a percentage of the replacement value [55], or based on loss ratios corresponding to damage states [75]. For instance, Hazus defines default values of direct economic loss based on loss ratios corresponding to each state of damage with a loss of 2%, 10%, 50%, or 100% of the building’s replacement cost, corresponding to slight, moderate, extensive and complete damage levels respectively [75]. More explicit replacement and repair costs of structural elements can also be obtained via a detailed evaluation of different repair actions and adopting construction cost databases. Alternatively, in case of complete damage of a structural system, the replacement cost can be estimated using Table 3, with the replacement cost of the structural system approximated as a fraction of the total cost of the building depending on building occupancy and structural system type. The damage and losses of the non-structural system of a building can also be estimated using the same approaches defined for structural elements.

If information on the damage level is unavailable, a common assumption is to consider the structural and non-structural systems within a compartment affected by a post-flashover fire fully damaged (requiring complete replacement), and no damage outside the compartment of fire origin (if no breach of compartmentation is verified). However, this assumption is quite conservative and could lead to over-estimations of the losses. Alternatively, [79] proposed a general theoretical model for failure cost evaluation in buildings, which normalizes all the losses due to structural failure by the initial construction cost. In particular, they estimated that the damage cost due to structural failure is generally in the ranges 15–40% and 10–30% of the initial construction cost for structural and non-structural systems, respectively (depending on the building occupation type).

Apart from the structural and non-structural building systems, a fire event can seriously damage the content and equipment within and outside the compartment of fire origin. Although often smaller than the losses to the building, in some cases, the content loss may be higher than the building fire loss [71]. Consequently, the extent of the loss related to content and equipment typically depends on the building content and occupancy: it could be negligible or significant compared to the building construction cost. Particularly, in manufacturing and commercial facilities, the inventory losses can vary considerably according to the business type. Similar to the building components, Hazus offers factors to estimate the content replacement cost as a fraction of the total construction cost depending on building occupancy, as shown in Table 4.

Similar to structural and non-structural systems, in absence of more detailed information, common assumptions are to consider homogenously-distributed content over building volume, fully-damaged content within the fire compartment and no damage outside it (if no breach of compartmentation is observed). Like with the assumptions made for the damage to building components, this assumption of complete damage within the fire compartment is considered conservative.

4.3.2 Human Losses

Quantifying fire losses due to human fatalities and injuries is fraught with challenges, including the ethical complexity of placing monetary value on human life and health, the difficulty in measuring emotional and psychological trauma, the variability of long-term health consequences, legal and insurance complications, and inconsistent data collection [80, 81]. These issues highlight the multifaceted and deeply personal nature of such losses, extending beyond simple financial metrics to encompass broader ethical and methodological considerations. However, it is crucial to always keep in mind that the valuation of risk to life when comparing fire safety investments does not imply placing a value on the life of individual humans, but implies quantifying the value of risk reduction.

The concept of Value of Statistical Life (VSL) is usually applied to estimate the monetary value of human fatalities. Widely studied and adopted in welfare economics and in transportation risk analysis, this concept attempts to quantify the monetary value of increased safety and reducing the risk of mortality [1, 82,83,84]. It is important to emphasize that the VSL corresponds to a valuation of risk reduction, and not to a valuation of identifiable human beings. To avoid this (common) misunderstanding, the term Societal Capacity to Commit Resources (SCCR) [8] or Societal Willingness To Pay (SWTP) [85] is also sometimes used. A prevalent method for the valuation of the VSL is the Willingness To Pay (WTP) approach [86]. A more objective basis, however, is to derive the VSL from the Life Quality Index proposed by Nathwani et al. [87]. The Life Quality Index valuation has been incorporated into the ISO 2394:2015 standard.

A formula to calculate VSL has been suggested by the U.S. Department of Transportation [1, 88], and using this formula, VSL estimate is equal to 11.6 million USD for 2020. There is however significant variation in the values across studies due to their diverse objectives and contexts [89]. ISO 2394:2015 [85] suggests a VSL of 5.7 million USD, which is in line with a 2021 Canadian study on the cost of fire, where a statistical value of a human life equal to 4.4 million CAN was suggested [84].

Similar to VSL, the concept of Value of a Statistical Injury (VSI) attempts to quantify the value of preventing injuries. VSI is estimated as a fraction of VSL and grouped according to the Maximum Abbreviated Injury Scale (MAIS). The MAIS levels (minor, moderate, serious, severe, critical, and unsurvivable) aim to define coefficients that can be applied to VSL and assign each injury class a value corresponding to a fraction of a fatality [1, 88]. In the most recent NFPA study on total cost of fire in the United States, the corresponding fraction values of VSL were defined as 0.003, 0.047, 0.105, 0.266, 0.593, and 1.0 [1]. On the contrary, in a similar study in Canada, only “serious” and “light” injuries were calculated and associated to 15% and 2% of VSL, respectively [84]. It is important to highlight that the cost of an injury may also exceed the cost of human life, for example because of extensive medical costs, significantly reduced life expectancy, and a general loss of life quality.

Once both the VSL and VSI parameters have been defined, an estimate can be made of the expected rate of fatalities and injuries in a specific fire event. Generally, the number of fatalities and injuries are separated and treated differently between civilians and fire service [90]. In the absence of a building specific evaluation, the rate of fatalities and injuries of civilians and fire fighters can be estimated from fire statistics and databases. The latest statistics (period 2015–2019) report numbers in the range 0.7–2.2 injuries per 100 fires and 1.3–6.9 deaths per 100,000 building fires for fire fighters and 0.4–3.1 injuries per 100 fires and 0.15–7.3 deaths per 1000 fires for civilians [91,92,93]. These numbers are average values, and they depend on many factors such as populations protected by specific fire departments [92]. Also, since residential fires are the most common, many more fatalities and injuries occur in this type of building. However, fires in some non-residential structures, such as storage and mercantile properties, are just as hazardous, if not more so, to firefighters. It is also important to highlight that these numbers collected by fire statistics refer to all the fire incidences, while this study focuses on fires in buildings. For example, in 2020, only 50% of fireground deaths were related to building fires, while the other 50% were related to wildland fires.

Apart from the VSL and VSI approach, other methods can be also found in the literature to estimate the human loss. For instance, a theoretical model in [79] estimated the cost of injuries and fatalities due to structural failure as a normalized value of the initial construction cost for different occupation types. These values were found to vary within a wide range, from about 10–20% for residential and commercial buildings up to 100–2000 times the initial building costs for nuclear power plant catastrophes.

4.4 Indirect Losses

4.4.1 Concept

Different types of losses and associated costs can be the consequence of a fire event after it has been extinguished [94]. These indirect or consequential losses are a constitutive part of the economic and societal impact caused by fires, but they are arguably the most difficult cost component to estimate [1]. The lack of research in this area is usually associated with the paucity of usable data and well-developed techniques [12, 95]. In addition, even in cases where data is available and analyses performed, a wide variation of values and parameters related to indirect loss estimation is found. Ramachandran and Hall have indicated that indirect losses are typically small for most fires, except in a few exceptional cases [82]. On the contrary, a case study by Ashe et al. stated that indirect losses are not negligible [4]. This study determined that in Australia, about 15% of the total annual cost of fire can be attributed to losses with direct losses accounting for 11% and indirect losses accounting for 4%; the remaining 85% of the cost pertains to expenses associated with installation, maintenance, fire services, and other related aspects.

The nature and extent of indirect losses caused by a fire depends greatly on the building occupancy and activity. For instance, large fires occurring in industrial and commercial properties can cause substantial consequential losses arising from loss of production, profits, employment, and exports, and thus destroy a significant percentage of the economic wealth of a private entity, a society, or even a country. In such cases, the need for appropriate fire safety strategies and fire prevention measures reaches its maximum level of importance because of the risk of high consequential losses [12]. A small business that suffers a fire might also go out of business, a major setback for the owners and, in some instances, a significant loss to their community as well. The different types of consequential losses which can be linked to fire are identified and explained in Table 5.

4.4.2 Estimation of Indirect Losses

Unlike direct losses to property where a monetary value can be directly computed for the losses, the monetary value attributable to indirect losses are more nuanced. This is especially so, as the indirect cost of the fire go beyond the severity and frequency of fires and can also be due to other factors such as the type of business it affects, the location of the fire and the aspect of the economy affected by the fire.

General research studies have been carried out to understand and quantify the indirect losses due to fire in different sectors [82, 101]. In a study based on 109 fires from 1989 onwards, it was estimated that the indirect losses due to fire in the private sector (principally business interruption costs) were 65% for manufacturing and industrial properties, 25% for public assembly, educational, institutional, retail, and office properties, 10% for residential, storage, and special structure properties, and 0% percent for vehicle and outdoor fires [82]. However, the authors highlighted that “These percentages may appear low to anyone whose sense of indirect loss is based primarily on a few well-publicized incidents where indirect losses were much larger than direct damages. From a statistical standpoint, however, such incidents are more than offset by the far more numerous incidents where indirect loss is either small or nonexistent” [82]. Alternatively, Hicks and Liebermann [101] postulated a generalized assumption that small fires typically generate small indirect losses, while large fires produce larger indirect losses, and consequently, the indirect loss can be measured as a fraction of the direct loss. A study on the Total Cost of Fire in the United States, adopted an economic forecasting tool to evaluate the indirect economic impact of fires [1]. Although the model works well for commercial facilities, the study also pointed out that it is not applicable to residential fires. In addition, it highlighted the need for statistically strong data samples with respect to each business affected by fire.

The cost related to function loss is a significant concern in structural design, particularly for buildings that play critical roles in emergencies or require high levels of serviceability. A study [79] estimated the cost of function loss due to structural failure as a normalized value of the initial construction cost for different occupation types, with values varying from 10% for residential buildings, 200% for nuclear power plants, up to 1000% for hospitals and fire stations.

The psychological impact of fires differs depending on the type of occupancy involved. For private houses, they are profound. Survivors of fires may face long-term emotional distress and sleep issues, experiencing trauma, anxiety, depression, and grief. The broader community also experiences a sense of loss and disruption. In the study [79], the psychological consequences of fires were estimated as low as 10–20% of the initial construction cost for most buildings, but 100% for private houses.

Quantifying and monetizing the environmental impact of building fires is challenging due to the difficulties in quantifying the release of toxic materials and air pollutants, water and soil contamination from firefighting efforts, carbon emissions, waste management issues, and impacts on local infrastructure and services [63, 96,97,98,99]. Additionally, the human health costs and broader economic consequences further complicate this assessment. The variability in materials involved, scale of a fire, and methodological differences in assessing these impacts also add to the complexity. Accurate assessment requires a multidisciplinary approach and detailed data, which may not always be readily available. A recent NFPA project [98] was conducted to compile a comprehensive summary of existing knowledge on the environmental impact of fire and suggest a research roadmap to fill in the identified knowledge gaps. This study reviewed the ISO 14008 standard which specifies a methodological framework for the monetary valuation of environmental impact and related environmental aspects [102]. Other studies suggested how any environmental damage can be converted into a monetary loss by defining a unit cost per ton of emitted CO2 [66]. In another study [96, 99], a tool has been developed to offer a consistent method for assessing fire department performance, particularly focusing on environmental and economic impacts. This tool, known as the Enveco assessment tool, shifts the focus from costs and losses to savings related to environmental emissions and economic value.

5 Compendium of Data Sources

To provide an overview of data availability for calculating fire costs necessary for the CBA analysis, data sources listed in the previous sections are grouped in Table 6 below.

6 Discussion

This study reviews methodologies for the estimation of the costs associated with fires. A number of limitations with currently existing studies were identified and alterations to currently existing methodologies were proposed to ameliorate some of these limitations. However, there are still some limitations existing in the process. Addressing those limitations can be the focus of future work, aiming to create well-functioning methods that can effectively support decision-making about investing in fire safety measures. These limitations are outlined below.

-

(1)

The current methodologies utilize prototype buildings for the estimation of cost multipliers applicable to a category of buildings to determine the cost of fire protections at the macro level. However, buildings are usually dissimilar even when designed for similar purposes. As such, the cost of fire protection for the different buildings can also be expected to differ, and selected prototypes may not have fire protection costs representative of the buildings in a category. To resolve this issue, a probabilistic approach for estimating multipliers can be developed where the multipliers would be computed for several prototype buildings in a category and the frequency distribution of the multipliers obtained. From the frequency distribution, the mean value of the multipliers can be selected as representative of the buildings in the category. If the multipliers differ greatly (e.g., if the frequency distribution has a high standard deviation), it may be necessary to create sub-categories and have a multiplier for each.

-

(2)

Existing methods (including the updated one) utilizing multipliers to estimate the macro-level fire protection expenditure fail to differentiate between new construction and improvements of existing buildings. A potential solution is the introduction of distinct sub-categories for new construction and improvements, each with its own set of multipliers. As the U.S. Census Bureau annual construction spending does not differentiate between new construction cost and improvement expense for most building categories except private residential buildings [49], there's also a need to segregate national building improvement expenses from new construction costs. If such data isn't readily available, improvement costs can be approximated as a portion of new construction expenses.

-

(3)

A meticulous categorization of buildings according to their occupancy types can enhance the accuracy of estimating the expenditure of fire protection at the macro level. However, even the modified U.S. Census Bureau Categories (shown in Table 2) are not adequately detailed. The present categorization of residential buildings still predominantly aligns with available data, not the specific fire protection requirements. Additionally, the U.S. Census Bureau doesn't provide sperate macro-level construction expenditure data for high-rise and low-rise multi-family constructions. Other categories also demand further refinement. For instance, while both storage facilities and shopping malls are categorized as commercial buildings, their fire protection needs differ. However, the U.S. Census Bureau only reports annual construction expenditure in the commercial category as a lump sum.

-

(4)

Maintenance costs are usually estimated as a percentage of the installation cost in previous studies. However, maintenance costs vary across fire protection measures, building types, locations, and maintenance needs. As such, in improving the method of estimating the cost of fire, a more refined and general method of computing the maintenance cost of fire protection measures is identified, as shown in Equations 3 and 5. But data for each component is not always available.

-

(5)

This literature review focuses on the cost components associated with building fires and does not encompass methodologies for estimating all cost components, such as the costs of firefighting services. While some studies have explored the costs of firefighting services in an effort to define methods for quantifying these costs [107, 108], this review does not cover them. Additionally, costs related to training, monitoring, and enforcement are beyond the scope of this study. However, some methodologies discussed here may be adaptable for estimating these costs. This review also does not delve into details for certain components, like the cost of environmental damage due to fires. As mentioned in Sect. 4.4.2, various studies have addressed the determination of fire-related environmental costs, developing tools for their estimation [66, 98, 99, 102]. Future research should conduct a comprehensive literature review of methodologies for estimating these specific cost components and focus on developing methodologies for aspects not yet fully explored.

-

(6)

Current fire statistics face limitations, such as the subjectivity in selecting fires to include and challenges in data verification. This often results in only accounting for significant fires reported to public fire services while neglecting those prevented by building-level fire protection measures. These limitations hinder the analysis of fire protection measures' impact, underscoring the need for more comprehensive, structured, and detailed statistics. Additionally, despite the EU FireStat project [59] offering a thorough overview of European fire statistics, global standardization is still lacking, with many essential parameters seldom collected, as highlighted in [109]. Comprehensive cost–benefit analyses using a statistics-based approach require higher quality and more structured fire data. This would facilitate the correlation between various fire protection measures and the differing frequencies and severities of fire events, as well as direct and consequential losses. In the absence of such data, adopting a modelling-based approach becomes necessary.

-

(7)

Improvements to the process of determining cost of indirect losses from fire are also required. Estimation of the indirect losses from fires can be quite challenging, and these losses can vary significantly between fire incidences. To this end, an accurate estimation of (the probability distribution describing) this cost would require identifying and computing the indirect losses from each fire event. In addition, some of the losses such as psychological effects and environmental damage are very difficult to establish a monetary value for.

7 Conclusion

This study reviews methodologies for estimating the cost of fire protection measures and the losses from fire incidences, both necessary components for a CBA of fire safety measures. Different categories of costs and losses are identified and currently used methodologies for estimating each are outlined. To estimate losses for the CBA, methods for estimating direct and indirect losses are examined, including processes for computing property and human losses, as well as existing concepts for computing indirect losses. Data sources offering the necessary information and data for making the estimations are carefully compiled. Limitations with the existing methodologies, data sources and fire statistics were also recognized and highlighted. In addition, the literature review features a recent study by the authors that improves fire protection cost estimation methods at national and sub-national levels. The study proposes updated building categories, guidance on calculating accurate multipliers, and a method for computing maintenance costs. These refined categories utilize regularly updated U.S. Census Bureau construction cost data, ensuring timely multiplier updates. The findings and recommendations made in this literature review would ultimately help improve the practice of selecting fire protection schemes that will optimize the net benefit of fire protection measures to both private decision makers and society as a whole.

References

Zhuang J, Payyappalli VM, Behrendt A, Lukasiewicz K (2017) Total cost of fire in the United States. Fire Protection Research Foundation Quincy, MA, USA

Hall J (1993) The total cost of fire in the United States. Fire Protection Research Foundation Quincy, MA, USA

Hall J (2014) The total cost of fire in the United States. Fire Protection Research Foundation Quincy, MA, USA

Ashe B, McAneney KJ, Pitman AJ (2009) Total cost of fire in Australia. J Risk Res 12:121–136

Schaenman P, Stern J, Bush R (1995) Total cost of fire in Canada: an initial estimate. National Research Council of Canada, Ottawa, Canada

Pickering J, Beall W, Phillips W (2023) Economic and social cost of fire. London, UK

Jones-Lee M, Aven T (2011) ALARP—What does it really mean? Reliab Eng Syst Saf 96:877–882

Van Coile R, Jomaas G, Bisby L (2019) Defining ALARP for fire safety engineering design via the life quality index. Fire Saf J 107:1–14

Lundin J, Frantzich H (2002) Cost-benefit and risk analysis-basis for decisions in the fire safety design process. In: Proceedings from the 4th International Conference on Performance based codes and Fire Safety Design Methods. pp 370–381

Banks J, Reichard K, Crow E, Nickell K (2009) How engineers can conduct cost-benefit analysis for PHM systems. IEEE Aerosp Electron Syst Mag 24:22–30

Eigner M, Huwig C, Dickopf T (2015) Cost-Benefit Analysis in Model-Based Systems Engineering: State of the Art and Future Potentials. In: DS 80–7 Proceedings of the 20th International Conference on Engineering Design (ICED 15) Vol 7: Product Modularisation, Product Architecture, systems Engineering, Product Service Systems, Milan, Italy, 27–30.07. 15. pp 227–236

Ramachandran G (2002) The economics of fire protection. Routledge, London

Hopkin D, Spearpoint M, Arnott M, Van Coile R (2019) Cost-benefit analysis of residential sprinklers–Application of a judgement value method. Fire Saf J 106:61–71

Johansson N, Van Hees P, MacNamee MS, Strömgren M (2012) A Cost-Benefit Analysis of Fire Protection Systems Designed to Protect Against Exterior Arson Fires in Schools. In: 9th International Conference on Performance-Based Codes and Fire Safety Design Methods. Society of Fire Protection Engineers

Newport Partners LLC (2014) Home Fire Sprinkler Cost Assessment. Springer, New York, USA

Duncan CR, Wade CA, Saunders NM (2000) Cost effective domestic fire sprinkler systems. BRANZ, New Zealand

Butry DT, Brown MH, Fuller SK (2007) Benefit-Cost Analysis of Residential Fire Sprinkler Systems. US Department of Commerce, National Institute of Standards and Technology, Gaithersburg, MD

Palmer D, Caldwell C, Fleischmann C (2000) Risk Assessment & Cost Benefit Analysis of Corridor Smoke Detectors in Rest Homes. New Zealand

Hasofer AM, Thomas IR (2008) Cost benefit analysis of a fire safety system based on the life quality index. Fire Saf Sci 9:969–980

Simonson M, Van den Berg M, Andersson P (2006) A cost benefit analysis model for fire safety: Methodology and TV case study. Swedish National Testing and Research Institute, Boras, Sweden

van Coile R, Lucherini A, Chaudhary RK, et al (2023) Economic Impact of Fire: Cost and Impact of Fire Protection in Buildings. Quincy, MA, USA

De Sanctis G, Fontana M (2016) Risk-based optimisation of fire safety egress provisions based on the LQI acceptance criterion. Reliab Eng Syst Saf 152:339–350

Aldrich R, Arena L (2013) Evaluating ventilation systems for existing homes. National Renewable Energy Lab. (NREL), Golden, CO, USA

Brown MH (2005) Economic analysis of residential fire sprinkler systems. US Department of Commerce, Technology Administration, National Institute of Standards and Technology, Gaithersburg, MD, USA

California Utilities Statewide Codes and Standards Team (CSUCS) (2011) Control of Egress Lighting. California Public Utilities Commission, California, USA

Ghosh B (2009) Assessment of the benefits of Fire Extinguishers as fire safety precautions in New Zealand Buildings. University of Canterbury, Christchurch, NZ

National Fire Sprinkler Association (NFSA) (2020) The true cost to install a residential sprinkler system. https://nfsa.org/2020/09/15/the-true-cost-to-install-a-residential-sprinkler-system/. Accessed 25 Jul 2023

Russell M, Sherman M, Rudd A (2007) Review of residential ventilation technologies. Taylor & Francis, Milton Park, USA

Zega M (2018) Best practices for emergency lighting: Explore how to implement safe, code-compliant, and cost-effective emergency lighting systems. Consult Specif Eng 55:28–33

Chapman RE, Butry DT, Huang AL, Thomas DS (2010) Economics of Egress Alternatives and Life-Safety Costs. Gaithersburg, MD, USA

Quarles SL, Pohl K (2018) Building a wildfire-resistant home: Codes and costs. Headwaters Economics

Esposito DC (2004) Economic impact of fires in buildings. MSc Thesis Carleton University

Napier TR (2013) Costs and benefits of resilient construction. Construction Engineering Research Laboratory, Champaign, IL, USA

Gordian (2021) Facilities Construction Costs with RSMeans Data, 36th ed. RS Means Company, Rockland, MD, USA

Gordian (2021) Residential Costs with RSMeans Data, 40th ed. RS Means Company, Rockland, MD, USA

Gordian (2021) RSMeans Data Online. https://www.rsmeans.com/products/online/tiers. Accessed 11 Jan 2022

Construction | BCIS. https://bcis.co.uk/products/construction/. Accessed 22 Oct 2022

Lange D, Devaney S, Usmani A (2014) An application of the PEER performance based earthquake engineering framework to structures in fire. Eng Struct 66:100–115

Hicks SJ (2004) Comparative structure cost of modern commercial buildings. Steel Construction Institute

Group R (2006) Rawlinson’s Australian Construction Handbook 2006, 24th edn. Rawlhouse Publishing, Perth, Australia

Xactimate | Insurance Claims Estimating Software | Verisk. https://www.verisk.com/insurance/products/xactimate/. Accessed 22 Oct 2022

Lufkin PS, Pepitone AJ (2010) The Whitestone Building Maintenance and Repair Cost Reference 2010. Whitestone Research, Santa Barbara, USA

Gordian (2021) Facilities Maintenance and Repair Costs with RSMeans Data, 28th ed. RS Means Company, Rockland, MD, USA

Apostolow JJ, Bowers DL, Sullivan III CM (1978) The nation’s annual expenditure for the prevention and control of fire. Worcester Polytechnic Institute, Worcester, MA, USA

Meade WP (1991) A first pass at computing the cost of fire safety in a modern society. Fire Technol 27:341–345

Hanscomb Consultants Inc (1993 and 1992) Input into Economic Model of Capital and Maintenance Cost for Fire Protection. National Research Council, Ottawa, Canada

Standohar-Alfano CD, van de Lindt JW, Holt EM (2018) Comparative residential property loss estimation for the April 25–28, 2011, tornado outbreak. J Archit Eng 24:04017026

Wiebe DM, Cox DT (2014) Application of fragility curves to estimate building damage and economic loss at a community scale: a case study of Seaside, Oregon. Nat Hazards 71:2043–2061

U.S. Census Bureau (2021) US Census: Construction Spending. https://www.census.gov/construction/c30/c30index.html. Accessed 18 Oct 2021

International Code Council (2020) International Building Code 2021. International Code Council, Incorporated, Washington DC, USA

NFPA (2021) NFPA 101-Life safety code. National Fire Protection Agency, Quincy, MA

Federal Emergency Management Agency (2003) Multi-Hazard Loss Estimation Methodology: Earthquake Model, HAZUS-MH MR4, Washington, D.C.

Lam C, Robbins A (2021) Comparison of component categorizations used in international total cost of fire estimates. Fire Saf J 120:103142