Abstract

Maritime transport is responsible for about 2.5% of global greenhouse gas emissions representing around 1000 million tons of CO\(_2\) annually. The situation of shipping emissions that strongly depends on future economic grows is aggravated by the fact that global green house gas (GHG) emissions are predicted to increase between 50 and 250% by 2050. This is not compatible with the internationally agreed goal of keeping global temperature increase below to \(2\,^{\circ }\hbox {C}\) compared to pre-industrial levels, which requires worldwide emissions to be at least halved from 1990 levels by 2050. Furthermore, ship owners are facing barriers implementing energy efficiency technologies to reduce CO\(_2\) mainly due to reliability, and financial and economic constraints as well as due to the complexity of change. Energy consumption and CO\(_2\) emissions of ships could be reduced by applying operational measures and implementing existing technologies. Further reductions could be achieved by implementing new innovative technologies. The aim of this study is to compare and review low carbon and advanced technologies that may help to reach international GHG reduction goals. A comparison table describing the different technologies, the estimated capital cost, technology readiness as well as the potential GHG reduction is drawn. The table also indicates if the technology suits better to new projects or to retrofitting. The comparison may help the key players to select the most convenient technology for their new projects. It will also be helpful for conversion of existing vessels.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

In January 2017, the world ship merchant fleet dedicated to international trade grew by 4%, the fastest growth in five years, and reached 1.92 billion DWT that consisted of 94,171 sea-going vessels above 100 GT. The sea shipping industry is responsible for more than 80% of the world trade representing a total international cargo over 10.7 billion tons [1]. Consequently, it produces growth of fuel consumption and green house gas (GHG) emissions at sea. The GHG emissions of ship engines have raised the concern of the International Maritime Organization (IMO) on the consequences for the environment and human health.

The transport sector produced approximately 27% of GHG emissions primarily coming from burning fossil fuel for cars, trucks, ships, trains, and planes. Over 90% of fuel used for transportation is based on products derived from petroleum including gasoline and diesel [2].

Meanwhile, the maritime transport is responsible for about 2.5% of global GHG emissions, including mainly carbon dioxide (CO\(_2\)) with around 1000 million tons annually, methane (CH\(_4\)) and di-nitrogen oxide (N2O). The situation of shipping emissions that strongly depends on future economic grows is aggravated by the fact that global GHG emission is predicted to increase between 50% and 250% by 2050. Therefore, it would represent at that time about 17% of the global GHG emissions [3].

This increase is not compatible with the internationally agreed goal of “taking urgent action to combat climate change and its impacts,” this includes keeping global temperature increase below \(2\,^{\circ }\hbox {C}\), as agreed in the Copenhagen (2009) and Paris accords (2015), which requires worldwide emissions to be at least halved from 1990 levels by 2050 [4,5,6]. It is worst to be mentioned that future scenarios demonstrate that significant reductions are needed to mitigate emissions due to the predicted growth in seaborne trade [7]. For these reasons, shipping has been given increasing attention over the past few years and has been recognized as a growing problem by both policy-makers and scientists.

Merchant ships in international traffic are subject to International Maritime Organization (IMO) regulations. Emissions from ships in international trade are regulated by ANNEX VI of MARPOL 73/78 (the International Convention for the Prevention of Pollution from Ships). IMO has declared the goal of a 30% NOX reduction from internationally operating vessels and introduced a NOX limiting curve in Annex VI published in 1998, which depends on engine speed. From 1st January 2000, all new marine diesel engines for new vessels should comply with this regulation (NOX optimized engines). Annex VI entered into force in May 2005, and sets limits on sulphur oxide and nitrogen oxide emissions from ship exhausts and prohibits deliberate emissions of ozone-depleting substances. On the same day, a global cap of maximum 4.5% on the sulphur content of fuel oil became mandatory for all ships. In addition, the first sulphur emission control area (SECA, with a maximum fuel sulphur content of only 1.5% sulphur content) in the Baltic Sea entered into force in May 2006, while the North Sea and English Channel SECAs entered into force in August–November 2007. In 2012, limits on sulphur oxide have been set to 3.5%.

The decision to implement a global sulphur cap of 0.5% in 2020, revising the current 3.5% cap (outside SECAs), was announced by the IMO on 27th October 2016. This bunker change applies globally and will affect as many as 70,000 ships.

Recently, new initial strategy on the reduction of GHG emissions from ships has been defined during the 72nd. session of the Marine Environment Protection Committee (MEPC) of the IMO organized from 9 to 13 April 2018. The official statement from IMO says the following: “The vision confirms IMO’s commitment to reducing GHG emissions from international shipping and, as a matter of urgency, aims to phase them out as soon as possible in this century. More specifically, under the identified levels of ambition, the initial strategy envisages for the first time a reduction in total GHG emissions from international shipping which should peak as soon as possible and to reduce the total annual GHG emissions by at least 50% by 2050 compared to 2008, while, at the same time, pursuing efforts towards phasing them out entirely.”

2 The use of low carbon technologies

International and national regulations call for even more stringent limits than those presented in the introduction of this document. As a result, compliance with emission regulations through technological improvements will impact ship operators and the technology in use, and will thus impact on the emissions. Future scenarios that consider possible emission reductions and improvements of fuel efficiency should also be considered.

The potential for emission reductions through technological improvements, alternative fuels, and ship modifications is significant [7]. Several technologies and alternative fuels may reduce ship emissions for both new and existing engines. Emission control strategies for the shipping fleet have not been widely adopted in the absence of policy measures, making their ultimate performance across the fleet less certain. Policy-makers are debating the trade-off between regulations that are based on technology and performance

One currently observes that the maritime transport actors are facing obstacles to reduce emissions such as reliability of technologies, financial and economic constraints, and complexity of change to implement energy efficiency technologies.

Energy consumption and emissions of ships could be reduced by applying operational measures, implementing existing technologies or innovative solutions. The Intergovernmental Panel on Climate Change (IPCC) recommends that the impact of the projected growth in world trade on freight transport emissions may be partly offset in the near term by more efficient vehicles, operational changes, slow steaming (SS) of ships, and eco-driving and fuel switching [8]. Several studies refer to maritime transport and propose different ways to prevent or reduce pollution seeking to comply with IMO regulation and the recommendations of the IPCC.

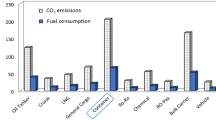

Optimization of various ship systems other than the engines such as propeller, rudder, and hull are promising options to reduce fuel consumption rates and, with them, \(\hbox {CO}_{2}\) emissions, see Fig. 1.

Potential fuel and \(\hbox {CO}_{2}\) reductions from various technology approaches for shipping vessels [9]

The energy-reduction potential, and therefore the emission reduction potential, of an optimized hull shape and a better propeller for a new ship are estimated to be up to 30% [10,11,12,13,14,15]. It is worth to be mentioned that some disruptive technologies are becoming available commercially such as bubble lubrication of the ship hull developed by Mitsubishi Motors. This system reduces the hull friction and fuel consumption.

Proper ship maintenance can ensure that the vessel operates efficiently [16]. As observed in Fig.1, the most effective way to reduce fuel consumption and CO\(_2\) emissions from ships is reducing and optimizing the vessel speed and adjust ship routes to avoid heavy wind [17,18,19].

There are important studies [20,21,22,23] that deal with the use of speed reduction practice in liner shipping focusing economic aspects. Some studies [19, 20, 24,25,26] refer on one positive effect of speed reduction also called slow steaming (SS) is the reduction of GHG emissions, that are proportional to the amount of fuel burned. This kind of operational measure can give positive effects on the fleet’s fuel consumption in a short time and consequently fewer emissions. Moreover, it has low investment cost and can be applied to all ships [27].

There are a number of alternative fuels that can be used in marine service. Primary fuel sources are fossil fuels, petroleum, goal, and gas. Fuels derived from petroleum are commonly considered alternate marine fuels to heavy residual oil (marine bunkers). These include low sulphur residual fuels, marine distillates and blends, bio-oils, and bio-diesels. However, the improvement of fuel quality or the use of innovative cleaner fuels (bio-gas, fuel cell and battery, hydrogen fuel and liquefied natural gas) may take considerable more time to be implemented [28,29,30,31,32,33]. Nonetheless, this trend will definitively conduce to the green shipping concept.

The use of low-sulphur but high-cost fuel will be a considerable improvement in the maritime industry. In the next years, this will probably change as ship fuels are progressively becoming de-sulphurized [34]. The higher oil prices and stricter regulations on emissions open a new market of alternatives fuels [35,36,37].

The aim of the study is to compare and review low carbon and advanced technologies that may help to reach international GHG reduction goals. In particular, this paper is focusing on the fuel switching from heavy fuel oil (HFO) to liquefied natural gas (LNG).

3 Methodology

In this section, the LNG is selected as a potential marine low emission fuel and compared with other traditional fuels. Then three case studies are reviewed and analysed to show the applicability of LNG as main propulsion fuel for different types of ships. Finally, the infrastructure facilities of the ports for LNG bunkering are reviewed.

3.1 LNG as maritime fuel

One of the driving factors behind the push towards alternative fuels like LNG from heavy fuel oil (HFO) can be owed to decisive environmental regulations set out by the International Maritime Organization (IMO). Starting January 2020, a global sulphur cap of 0.5% will be imposed on ships trading outside of emission control areas. Currently, this limit is capped at 3.5%.

When switching usage from HFO to LNG, there is a significant reduction of emissions. The sulphur oxides are completely removed, nitrous oxide is significantly reduced and the so-called local emissions particles are basically eliminated. That is clearly one of the major benefits which is enabling shipping to become more green.

LNG is a fossil fuel that contains methane as the primary component. The world production of natural gas is increasing by an average of 2.1% per year, while world consumption by 1.7% per year. This increment indicates that natural gas could be an alternative more sustainable than other traditional liquid fuels such as heavy fuel oil (HFO) [38].

Figure 2 illustrates the CO\(_2\) footprint of various fuels. GHG are measured as CO\(_2\)-equivalent emissions. As seen in Fig. 2, LNG as marine fuel could reduce greenhouse gas up to 21%.

However, the release of un-burned methane (so-called methane slip) could reduce the benefit of LNG over HFO and MGO because methane (CH\(_4\)) has 25 to 30 times the green house gas effect compared to CO\(_2\). Nevertheless, engine manufacturers claim that the Tank-to-Propeller (TTP)CO \(_2\)-equivalent emissions of Otto-cycle dual-fuel (DF) and pure gas engines are 10 to 20 percent below the emissions of oil-fuelled engines. Diesel-cycle gas DF engines have very low methane slip, and their TTP emissions are very close to those in the illustration [39].

CO\(_2\) emissions of fuel alternatives in shipping [39]

According to the fuel prices (March 2013), the price of natural gas in $/MMBtu is almost equal to half the price of crude oil. Natural gas gives the same crude oil energy. This means that the use of natural gas as a fuel source, for the transportation sector, including marine applications could be less expensive than using traditional crude oil fuel [28].

However, it is not all smooth sailing for LNG becoming the future shipping fuel. Many in the industry believe that competitive oil prices, as they are currently, may yet affect the interest in LNG as a fuel source. However, it is not all smooth sailing for LNG becoming the future shipping fuel. Many in the industry believe that competitive oil prices, as they are currently, may yet affect the interest in LNG as a fuel source.

The greatest resistance, though, to LNG being adopted globally is the lack of infrastructure and bunkering facilities. But there is a way around the problem. Leader companies are providing dual-fuel engines that can run on both LNG and conventional LFO, HFO, or liquid biofuels. LNG as fuel is now a proven and available solution. The commercial opportunities of LNG are interesting for various new build and conversion projects. In the last 13 years, the LNG-fueled ship fleet is growing, see Fig. 3 [40]. Figure 3 shows the development of LNG-fueled fleet that started in 2000. It can be observed that in 2015 around 76 ships were operating with LNG meanwhile 88 were operating in 2018. The forecast for 2026 is to reach a number of 357 LNG-fueled ships [40, 41].

Development of LNG-fueled ship fleet, published in 2018 [40]

It is expected that the price of the 0.5% sulphur cap fuel is going to be somewhere in between HFO and marine gas oil (MGO). This will offer an additional incentive to ship owners thinking about switching to LNG, in order to achieve compliance with the upcoming sulphur cap [32]. In ECAs, restrictions on the use of more efficient and less polluting fuels are already a requirement. In these areas, the use of MGO is also beneficial. The use of LNG-fueled ships as a less contaminant vehicle is also a strong argument for fuel switching, especially in coastal and sensitive ecosystems; it offers multiple advantages to both human health and the environment.

Several studies analysed the cost of LNG implementation in the ships and the effect on emissions with this fuel switching. Some case studies on the implementation of LNG as fueled ship are going to be presented in the next section.

3.2 Case studies

This study is reviewing how the implementation of LNG as fuel improves the reduction of emissions in maritime transport and their economic advantages.

3.2.1 LNG as marine fuel for fishing vessels

The potential use of LNG in Norwegian waters by fishing vessels is an important alternative because this type of ship is contributing to approximately 10.2% of the fuel consumed by ships in 2013 [29].

The regulations and agreements in Norwegian waters are incentivizing to reduce the emissions from fishing vessels and to develop greener fisheries. The main parameters of the case study are listed in Table 1 [29].

The main parameters present in Table 1 refer on a coastal shrimp trawler operating in Norway, it operates within 250 nautical miles of shore and its engine power is greater than 750 kW, it is liable to NOX, SOX, and CO2 taxes.

Therefore, fuel switching by LNG can reduce these costs. The emissions and fuel annual costs are resumes in Table 2.

The calculation of NOX emissions and total fuel cost show that the use of LNG fuel is more convenient than MGO, see Table 2. In this analysis, the additional cost by LNG implementation is covered by the Norwegian NOX tax and fund system promotes switching to LNG propulsion.

The annual fuel saving from the use of LNG instead of MGO was approximately 49%. Therefore, the saving in emissions annual tax is about 64,800 USD, see Table 2.

Finally, the case study shows a net present value (NPV) and life cycle cost (LCC) calculations. It concludes that an investment of LNG is economically more beneficial than a conventional investment, and the payback time is around 4 years.

3.2.2 LNG as marine fuel for RORO cargo vessel

The potential use of LNG in medium-speed RORO cargo vessel operating in the Red Sea is a solution from environmental and economic improvements [33].

The use of LNG option, for reducing exhaust gas emissions from ships to comply with IMO new regulations are evaluated. The main parameters of the case study are listed in Table 3 [33].

The main parameters present in Table 3 refer on a medium-speed RORO cargo vessel operating in the coats of Red Sea between Hurghada port in Egypt and Duba port in Saudi Arabia.

The economic and environmental benefits using LNG conversion system and Dual-fuel engine (DFDE) are discussed in this study and compared with standard diesel engines (DE). The proposed DFDE will operate with a mixture of 95% of natural gas and 5% of pilot diesel fuel oil in manoeuvring and cruise modes.

The SOX and NOX emissions are calculated for the two engines types, then they are compared with IMO SOX rates required for 2020, and IMO NOX (TIER III) rates required for 2016, see Fig. 4.

Comparison of SOX and NOX emissions with IMO rates

Figure 4 shows the environmental benefits of the DFDE compared with DE. The annual emissions of SOX and NOX show the advantage of DFDE in the particular case of this RORO ship. The converted engine used in the study has a lowered rate of emissions and comply with the IMO regulation, see Table 4.

In this case study, NOX, SOX, CO2, and PM emission rates are calculated for DFDE and the percentage of emissions compared with the DE are also shown in Fig. 5.

Relative emissions of DE and DFDE for RORO ship and emissions rates per trip for DFDE

Finally, LNG conversion proved to be economically viable and considerably reduces the NOX and SOX emissions, see Table 4 and Fig. 5.

3.2.3 LNG as marine fuel for CO2 carrier

The potential shipping routes of CO2 carriers are in ECAs where HFO is not accepted as a marine fuel. This assessment is based on a comparison study with CO2 carriers utilizing MGO and LNG as fuel. The main parameters of the case study are listed in Table 5 [32, 42].

The main parameters present in Table 6 of the CO2 shipping scenario are referring on a previous report by Skagestad et al. [42] showing previous researches about CO2 shipping in Europe. The ship price, total CO2 emissions, and the study of the annual cost index are resumed in Table 6.

The calculation of emissions and total cost index is showing that the use of LNG fuel is more convenient than MGO, see Table 6. In this analysis, the annual cost index does not include other OPEX factors.

The cost of the LNG system can vary between + 10 and + 25% of the reference cost, see Table 7.

Table 7 shows that in this particular case the fuel switching from MGO to LNG is not convenient economically. Nevertheless, the total annual cost index per ton of CO2 avoided of LNG-fueled ship is lower than that of reference scenario, see Fig. 6.

Comparison of the calculated annual costs for the 4 scenarios of LNG fuel and the reference case using MGO

The potential of emission reductions and total annual cost index in the first 3 scenarios propose an attractive economical alternative for the ship owners, see Fig. 6.

In the three ships cases studies reviewed above, the comparison tables described the different technologies, the cost, and the potential GHG reduction.

3.3 Port infrastructure facilities for bunkering of LNG in ports

Some forecasts are revealing that in 2025 shipping could account for an LNG consumption of between 7.5 and 20 million tons. It represents about 1.7 to 4.4% of global demand of 450 million tons [43]. Therefore, it is required that the facilities grow proportionally.

Ports are taking action to ensure that the supply of LNG fuel is going to meet the demand.

In addition, the countries that have LNG can promote the LNG bunkering to ships. For example, there are two LNG stations (Damietta and Alexandria) which can be used for natural gas bunkering through transferring LNG from one of these stations to Hurghada or Safaga ports [33].

Other studies propose the implementation of new LNG bunkering ports an analysis of the growth of local ships demands. Results for all these major ports should provide a good indication of LNG demand across the European ECAs [43].

The study by Lloyds Register about the LNG infrastructure shows the existence of 22 ports on the provision of LNG bunkering facilities in North America (4), Europe (15), and Asia (3). 77% of the ports are in ECAs and the remaining 23% are in non-ECA areas [44].

4 Discussion and conclusions

The result of the first case study related to a fishing vessel shows that LNG as a ship’s fuel technology is an attractive alternative that may reduce the cost to replace the MGO. The annual fuel saving from the use of LNG was approximately 49% in this case.

Although the LNG is not used in 100% due to the requirement of a pilot liquid fuel, the second case study proves that a considerable reduction of emissions may be achieved. The use of the DFDE alternative reduced the CO2 (− 14.5%), NOX (− 77.6%), SOX (− 92.5%), and PM (− 90.7%) emissions in the case of a RORO cargo vessel.

The third case study has proven that the LNG used as marine fuel might be economically attractive for potential European projects involving the CO2 transport by ships.

The selected case studies were effective in comparing and reviewing the use of LNG as a low carbon technology that may help to reach international GHG reduction goals. The natural gas can be successfully used as an alternative to replacing the currently used diesel fuels in marine transport. For short-term development, natural gas provides an ideal solution for marine applications. The comparison presented in this paper may help the key players to select the most convenient technology for their new projects. It will also be helpful for conversions of existing vessels.

However, to attend the LNG demand in several parts of the world there is a need to develop a new logistic approach and evaluate the offer of this fuel in each region. Several ports in Europe have been adapted to operate with this new reality. Another point that need to be considered is the fact that ships have a limitation to use only LNG as the main fuel source. It is due to the storage capacity of LNG tanks. Nowadays, ships that need to realize large voyages can be affected with LNG storage capacity and will need to use more than one type of fuel during operation.

Abbreviations

- CH\(_4\) :

-

Methane

- CO2 :

-

Carbon dioxide

- DE:

-

Diesel engine

- DFDE:

-

Dual-fuel engine

- ECA:

-

Emission control area

- GHG:

-

Green house gas

- HFO:

-

Heavy fuel oil

- IMO:

-

International maritime organization

- IPCC:

-

Intergovernmental panel on climate change

- LCC:

-

Life cycle cost

- LNG:

-

Liquefied natural gas

- MGO:

-

Marine gas oil

- N2O:

-

Di-nitrogen oxide

- NOX :

-

Nitrogen oxide

- NPV:

-

Net present value

- OPEX:

-

Operational expenditure

- PSV:

-

Platform supply Vessel

- PM:

-

Particulate matter

- RORO:

-

Roll on, Roll off

- SECA:

-

Sulphur emission control area

- SOX :

-

Sulphur oxide

- SS:

-

Slow steaming

References

UNCTAD/RMT. Review of maritime transport 2018. Report, UNITED NATIONS, Geneva (2018)

EPA. Sources of greenhouse gas emissions. Technical report, United States Environmental Protection Agency (2015)

IMO. Third imo ghg study 2014. Technical report, International Maritime Organization, London (2015)

UN United Nations. Transforming our world: the 2030 agenda for sustainable development. Technical Report 70/1, United Nations (2015)

UNFCCC. Report of the conference of the parties on its fifteenth session, held in copenhagen from 7 to 19 december 2009. fccc/cp/2009/11/add.1. Technical report, United Nations, Copenhagen (2009)

UNFCCC. Adoption of the paris agreement. fccc/cp/2015/l.9/rev.1. Technical report, United Nations, Paris (2015)

V. Eyring, H.W. Kohler, A. Lauer, B. Lemper, Emissions from international shipping: 2 impact of future technologies on scenarios until 2050. J. Geophys. Res. 110(D17), (2005)

IPCC. Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press (2014)

H. Wang, N. Lutsey, Long-term potential for increased shipping efficiency through the adoption of industry-leading practices. Int. Counc. Clean Transp. 1–27 (2013)

J. Gille, J. Harmsen, Cost savings through energy efficiency gains in iwt. Assoc. Eur. Transp. Contrib. 1, 1–17 (2011)

Hydrex. Ship hull performance in the post-tbt era. Technical report, Hydrex Group, Antwerp (2010)

MGM Innova, The FReMCo Corporation Inc., and International Paint Ltd. Reducing Vessel Emissions Through the use of Advanced Hull Coatings. The Gold Standard (2012)

MARINTEK. Study of greenhouse gas emissions from ships. final report to the international maritime organization. Technical report, Norwegian Marine Technology Research Institute (2000)

Transport Research Support. The International Bank for Reconstruction and Development. DEFID, International Bank for Reconstruction and Development/The World Bank (2011)

A.S. Husain, in Proceeding of Ocean, Mechanical and Aerospace Science and Engineering, Pekanbaru (2014)

M.A.F. Cepeda, in Proceedings of World Maritime Technology Conference 2015 ed. by SNAME (SNAME, Rhode Island, 2015), pp. 1–11

M.A.F. Cepeda, Jean-David Caprace, Data envelopment analysis of navigation records improve ship fleet management. In Proceedings of Offshore Technology Conference, number OTC-26298-MS in 1, pages 1–17, Rio de Janeiro, Brazil, 2015. Offshore Technology Conference

M.A.F. Cepeda, J.-D. Caprace, in Proceedings of XXVIX Congress ANPET 2015, ed. by ANPET (ANPET, Ouro Preto, 2015), pp. 1052–1062

M.A.F. Cepeda, L.F. Assis, L.G. Marujo, J.-D. Caprace, Effects of slow steaming strategies on a ship fleet. Mar. Syst. Ocean Technol. 12(3), 178–186 (2017)

P. Cariou, Is slow steaming a sustainable means of reducing CO2 emissions from container shipping. Transp. Res. D 16, 260–264 (2011)

David Ronen, The effect of oil price on the optimal speed of ships. J. Oper. Res. Soc. 33(11), 1035–1040 (1982)

H.-H. Tai, D.-Y. Lin, Comparing the unit emissions of daily frequency and slow steaming strategies on trunk route deployment ininternational container shipping. Transp. Res. D 21, 26–31 (2013)

E.Y.C. Wong, A.H. Tai, H.Y.K. Lau, M. Raman, An utility-based decision support sustainability model in slow steaming maritime operations. Transp. Res. E 78, 57–69 (2015)

J. Faber, M. Freund, M. Kopke, D. Nelissen, Going Slow to Reduce Emissions. Can the Current Surplus of Maritime Transport Capacity be Turned into an Opportunity to Reduce ghg Emissions. Seas at Risk (2010)

Haakon Lindstad, Bjorn E. Asbjornslett, Anders H. Stromman, Reductions in greenhouse gas emissions and cost by shipping at lower speeds. Energy Policy 39(6), 3456–3464 (2011)

R.A. Schiller, F. Ruggeri, K. Nishimoto, C.M.P. Sampaio, R.P. da Fonseca, Shuttle tanker fuel consumption numerical analysis for improving ship efficiency. Mar. Syst. Ocean Technol. 1, 1–13 (2017)

H. Winnes, L. Styhre, E. Fridell, Reducing ghg emissions from ships in port areas. Res. Transp. Bus. Manag. 17, 73–82 (2015).

M.M.E. Gohary, I.S. Seddiek, Utilization of alternative marine fuels for gas turbine power plant onboard ships. Int. J. Naval Archit. Ocean Eng. 5, 21–32 (2013)

S. Jafarzadeh, N. Paltrinieri, I.B. Utne, H. Ellingsen, Lng-fuelled fishing vessels: a systems engineering approach. Transp. Res. D 50, 202–222 (2017)

R. Raj, S. Ghandehariun, A. Kumar, J. Geng, M. Linwei, A techno-economic study of shipping lng to the asia-pacific from western canada by lng carrier. J. Nat. Gas Sci. Eng. 34, 979–992 (2016)

O. Schinas, M. Butler, Feasibility and commercial considerations of lng-fueled ships. Ocean Eng. 122, 84–96 (2016)

B.-Y. Yoo, Economic assessment of liquefied natural gas (lng) as a marine fuel for co2 carriers compared to marine gas oil (mgo). Energy 121, 772–780 (2017)

N.R. Ammar, I.S. Seddiek, Eco-environmental analysis of ship emission control methods: case study ro-ro cargo vessel. Ocean Eng. 137, 166–173 (2017)

IEA International Energy Agency. Transport, energy and CO2. Moving Toward, chapter 8: Maritime Transport, page 418. OECD/IEA, Paris (2009)

U. Roupe, M. Borgh, E. Molitor, Green shipping—from hull improvements to alternative fuels. SSPA 48, 6–7 (2009)

W. Sihn, H. Pascher, K. Ott, S. Stein, A. Schumacher, G. Mascolo, A green and economic future of inland waterway shipping. Procedia CIRP 29, 317–322 (2015)

L. van Biert, M. Godjevac, K. Visser, P. Aravind, A review of fuel cell systems for maritime applications. J. Power Sources 327, 345–364 (2016)

U.S. Energy Information Administration EIA. International Energy Outlook. EIA, Washington (2016)

DNV GL. Assessment of selected alternative fuels and technologies. DNV GL—Maritime (2018)

DNV GL. Lng regulatory update. best fuel of the future, conference & study tour. Technical report, DNV GL (2018)

DNV GL. Lng as Ship Fuel. Latest Developments and Projects in the lng Industry. IN FOCUS—DNV GL Maritime Communications (2015)

R. Skagestad, N. Eldrup, H.R. Hansen, S. Belfroid, A. Mathisenand A. Lach, H.A. Haugen, Ship transport of co2. status and technology gaps. Technical Report 2214090, Tel-Tek, Porsgrunn (2014)

R. Aronietis, C. Sys, E. van Hass, T. Vanelslander, Forecasting port-level demand for lng as a ship fuel: the case of the port of antwerp. J. Shipp. Trade 1(2), 1–22 (2016)

LR Lloyds Register, Marine. Lloyds register lng bunkering infrastructure survey 2014. The outlook of ports on provision of lng bunkering facilities. Technical report, Lloyds Register Marine, Southampton (2014)

Acknowledgements

This study was financed in part by the “Coordenação de Aperfeiçoamento de Pessoal de Nível Superior” - Brazil (CAPES) - Funding grant 001.

Author information

Authors and Affiliations

Corresponding author

Additional information

Publisher's Note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Fun-sang Cepeda, M.A., Pereira, N.N., Kahn, S. et al. A review of the use of LNG versus HFO in maritime industry. Mar Syst Ocean Technol 14, 75–84 (2019). https://doi.org/10.1007/s40868-019-00059-y

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40868-019-00059-y