Abstract

The present study investigates various aspects of volatility behaviour of BRIC/BRICS nations in varying time regimes. The study has been divided into three regimes where the first regime represents the pre-formation period, the second regime signifies post-formation period, and the third regime symbolizes post-formation period after the entry of South Africa. CUSUMSQ test has been applied in the study to recognize the structural breaks in the conditional variance on the formation of BRIC and BRICS. The study has employed various GARCH family models, such as GARCH (p,q) model, EGARCH model, GJR GARCH model, PGARCH model and CGARCH model. GARCH (p,q) model has been employed to explore the level of volatility spillover among the nations in different regimes. With the assistance of CGARCH model, the study exhibited the behaviour of conditional variance of BRIC/BRICS nations and discovered the existence of the permanent and transitory components. EGARCH, GJR GARCH model and PGARCH model explored the existence of “low volatility anomaly” for all the nations in all the regimes. The outcomes of the study exhibit little scope of diversification in all the three regimes. The study confirms the impact of global recession on the performance and development of BRICS nations. Hence, the investors can strategize their investment decisions as per the volatility behaviours of respective stock markets and current market situations.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

In 2001, Goldman Sachs coined the term BRICs (Wilson et al. 2010) to describe the four large developing countries of Brazil, Russia, India and China. Goldman Sachs predict that BRIC will overtake G6 (US, Japan, UK, Germany, France and Italy) regarding GDP (in US$) by 2050 (Wilson and Purushothaman 2003). The acronym coined by O’Neill (2001) in his paper entitled “building better global economic BRICs” came into extensive utilization that apparently reallocated the focus from developed G7 economies towards developing world. The foreign ministers of initial four BRIC nations conducted a meeting in New York City in September 2006 continued with a series of high-level meetings and on 16th May 2008 BRIC was founded. In 2010, South Africa started making efforts to join BRIC and became a formal member of BRIC on 24 December 2010.

The emergence of BRICS symbolizes a significant revolutionary transformation in the global political economy. This new group experienced varied reactions ranging from extreme optimism to utter scepticism. The world had an anticipation that BRICS will discover their lessons on economic and social concerns at regional and global levels. There were serious doubts about nature and coherence of the group. Goldman Sachs argued that BRIC countries are developing rapidly but only by 2050 their combined economies can overtake current richest economies.

The present study focuses on the changing role of BRICS stock markets in each other’s stock market as well as on the performance of individual stock markets over the period of 8 years. The research explored the impact of stock returns volatility of one nation on another. The study has divided the empirical work into three major parts, such as before the formation of BRIC, on the formation of BRIC and the entry of South Africa (formation of BRICS). The study has employed GARCH (1,1) test to explore spillover effect among the BRICS nations in three segments. Moreover, CGARCH test has also been applied to examine the existence of the permanent and transitory components of conditional variance. EGARCH, GJR GARCH model and PGARCH model are also employed to investigate the existence of “low volatility anomaly”. In a nutshell, the study primarily focuses on the exploration of volatility behaviour of BRIC/BRICS nations in three regimes that represent the pre-formation period of BRIC, the post-formation period of BRIC and post-formation period of BRICS.

Literature review

Xu and Liu (2001) assessed the flow of information transmission between Chinese A and Chinese B shares and ultimately the discount effect of B shares. With the help of bivariate GARCH model, short run dynamic transmission of information flow is assessed between share A and B. The results further verify that cross-market volatility spillover effects are much weaker which suggest that different underlying forces drive A and B shares. The study developed an empirical model to probe out the probable reasons for identifying the reasons for the discount rate of share B.

Lee et al. (2004) explored the relationships between daily returns and volatility of NASDAQ and Asian board markets using EGARCH and VAR model. The study empirically discovered strong evidence of volatility spillovers from the US to Asian second board markets after controlling spillovers from NYSE. The purpose of the study was to examine that whether these cross-country spillovers are strong enough in comparison to corresponding main board markets or not.

Bhar and Nikolova (2007) explored the degree of integration among BRIC nations by applying daily equity index level data. The study employed GARCH-in-mean approach pioneered by Liu and Pan (1997) to investigate the international diffusion of equity index returns and volatility to the BRIC nations. The study assessed a high level of integration among BRIC nations and minimal integration with rest of the world. Regional trends followed by BRIC nations have much greater influence rather than rest of the world. On the other hand, world index and the US equity market have a significant impact on the variance of Brazil, Russia and India. Only China experienced an inverse relationship between volatility spillover effects on the regional and global basis.

Yilmaz (2010) investigated the degree of infectivity and interdependence among the East Asian equity markets. The data selected for the study comprised the period ranging from the early 1990s and compared the ongoing crisis with previous episodes. The study observed the return and volatility spillover among the nations for the rolling subsample windows. The study empirically observed considerable assortment in the behaviour of East Asian returns and volatility spillover over the time. The integration among return spillover has increased significantly while volatility spillover has shown significant bursts during the market crisis.

Filis et al. (2011) investigated time-varying correlation using DCCGARCH-GJR approach on the data of six oil importing and oil exporting countries. The study confirmed increased positive correlation between aggregate demand side shocks and oil price, whereas supply side shocks did not influence the correlation equation of two types of markets. The study experienced an exception to the results mentioned above at the time of financial crisis.

Ramasamy and Munisamy (2012) conducted the study to assess the predictive accuracy of GARCH, GJR and EGARCH model for selected exchange rates. The study compared the forecasted and actual rates with the help of Gaussian random numbers. The study confirms that prediction of highly volatile exchange rates can be done appropriately and precisely with the assistance of GARCH models. The study remained incapable in determining the best forecasting model because of a different number of iterations for different currencies.

Guesmi et al. (2013) assessed contagion effect among the US stock market and OECD ones during the financial crisis. The study explored a relatively new term called shift contagion that signifies increased correlation among stock prices after a shock. The study employed a structural break test called Bai and Perron (2003). Moreover, the study estimated correlation coefficient with the help of dynamic conditional correlation (DCC) multivariate GARCH model. The authors compared pre- and post-crisis period and concluded that the markets have a positive correlation in between pre- and post-crisis.

Bekiros (2013) estimated the global contagion effects of financial crisis. The study observed the nature of volatility spillover among the US, EU and the BRIC markets during the financial crisis. The study examined the linear and nonlinear causal relationships by applying vector auto regression and numerous multivariate GARCH models. The sample covered both US financial crisis and Eurozone debt crisis. The study further recommended that BRICS nations have become more of globally integrated after the global financial crisis.

Dasgupta (2013) examined the integration and dynamic associations in between BRICS and the US stock markets. VAR, cointegration and Granger causality tests have been applied from 1st January 1998 to 31st December 2012.

Robbani et al. (2013) explored the volatility transmission in the financial markets of G-8 countries using VAR-EGARCH model. The study was conducted from 1995 to 2007 where the markets of Canada, France, Italy, the UK and the US have significantly affected by the volatility of other markets. The study has also employed impulse response function to explore the nature of shock persistence in stock returns. Granger causality test has also been employed to explore the direction of price movement.

Gomez and Ahmad (2014) conducted the study to examine that whether volatility is transmitted by friends, foes or stronger economies of the world. The authors analysed the daily stock returns of fourteen economies from July 1997 to October 2013. With the help of EGARCH model, it has been discovered that friendly countries demonstrate volatility transmission while rivals do not exhibit any such transmission.

Junior et al. (2014) compared and contrasted the performance of the large industrialized economies with emerging economies. Advanced economies consist of USA, Japan, UK and Germany, whereas, BRIC (Brazil, Russia, India and China) nations symbolized emerging markets. The study employed daily stock returns of eight markets for the period of 5 years ranging from 2006 to 2010. The selected period covered the financial crisis of 2008. The study has employed ARIMA and GARCH family models for analysing the performance of returns and volatility. Researchers have also employed higher GARCH family models, such as TGARCH and EGARCH to upgrade the results.

Zhong et al. (2014) employed advanced nonparametric cointegration test pioneered by Bierens (1997). The test re-explored the long run advantages of international equity diversification between the USA and BRICS nations from July 1997 to March 2012. The study suggested that the two profound indexes of the United States, namely, Dow Jones 30 and S&P 500 were pairwise cointegrated with the stock markets of the BRICS countries. The study explored the previous phenomenon by numerous financial researchers that two efficient markets cannot be integrated. Furthermore, the study recommended that if another stock market can predict stock prices of one country, then there is no scope for international diversification.

Guesmi and Fattoum (2014) explored the co-movements and dynamic volatility spillover between the stock prices and oil prices of oil exporting and importing countries. The five oil importing countries selected for the study are USA, Italy, Germany, The Netherlands and France and four oil exporting countries are United Arab Emirates, Kuwait, Saudi Arabia and Venezuela. The study employed multivariate GJR-DCCGARCH approach pioneered by Glosten et al. (1993). The study confirmed the positive correlation between oil prices and stock prices for both oil exporting and importing countries. The study confirmed cross-market co-movement through conditional correlation coefficient in response to oil price shocks as a part of the global business shock.

Motivation of the study and economic intuition

Due to consistent volatile situations, the prices of the securities do not depict an exact measure of its actual value. Volatility is a measure of risk, which plays a critical role in economics. Stock prices are characterized by a term called “volatility clustering” that suggests that substantial volatility is followed by significant volatility and low volatility is followed by low volatility. Thus, volatility can be predicted by its immediate past values.

To emphasize the contribution of the present study, the existing literature review is segregated into four broad categories on the basis of their restrictions that are undertaken in this study. First, the introduction of BRICS is expected to bring changes in the structure of conditional volatility. However, it is necessary to check the existence of structural changes in conditional variance around the time when BRIC/BRICS was formed. Prior studies have not assessed the structural changes and to overcome this shortcoming CUSUMSQ test has been employed in the study.

Secondly, GARCH (p,q) model introduced by Bollerslev (1986) suggests that conditional variance of stock returns is a linear function of lagged conditional variance and past squared error terms. The standard GARCH (p,q) model assumes that the retort of volatility to “good” and “bad” news is symmetric. However, it is not the case always. Three significant variants of the GARCH family (Zivot 2009), capable of capturing the said asymmetry in response of volatility to new information, are considered in the study, namely EGARCH model proposed by Nelson (1991), the GJR GARCH model proposed by Glosten et al. (1993) and periodic GARCH (PGARCH) model proposed by Ding et al. (1993). The primary reasons that are placed forward for the existence of such a phenomenon are leverage effect and volatility feedback. As per leverage effect (Black 1976; Christie 1982), a negative return shock leads to a fall in prices and a rise in stock return volatility. Ultimately, the bad news gets integrated into the prices and consequently contributes to the augmented riskiness of the stocks that reduce the prices of stocks and amplify the volatility. There is another theory of volatility feedback (Pindyk 1984; French et al. 1987; Campbell and Hentschel 1992) which declares that an ordinary increase in future volatility leads to elevated expected return (as compensation to bear this risk) and thereby declining the stock prices. The two presumptions have diverse approaches, where, leverage effect hypothesized that present negative returns amplify future volatility, whereas, feedback effect hypothesized that anticipated future volatility results in present negative returns. At the firm level, it is empirically well established that asymmetric response of volatility is primarily due to volatility feedback hypothesis (Bekaert and Wu 2000). Volatility feedback or time-varying expected return occurs because not all investors react in a rational manner (Antonious et al. 1998). Such behaviour is typical of market player (investors) who have lower access to information (noise traders), and these noise traders react stronger to “bad” news than to “good” news (Nair 2011).

Thirdly, CGARCH model further distinguishes between the permanent and transitory components of conditional variance which subsequently improves the goodness of fit. Many traditional models assume that variance of stock prices is constant over time, whereas GARCH model states that variance of stock prices changes over the period. On studying the sample autocorrelation of the squared returns, it has been observed that it reduces much faster exponentially in initial phases and reduces much slower in later stages. Such behaviour of volatility clearly indicates towards varying volatility components over the period. CGARCH model is explored to study such permanent and transitory behaviour of volatility.

Fourth, to identify the best-fitted model among EGARCH, GJR GARCH and PGARCH model, dynamic forecasting process has been applied. This process estimates the difference between actual and expected time series with the help of RMSE, MAE, MAPE and Theil’s U/Theil’s inequality criterion.

Objectives of the study

On the basis of motivation drawn from the literature review, the following are the primary objectives of the study:

-

1.

To discover the existence of structural changes in the conditional variance of stock returns of BRIC/BRICS nations on the commencement of treaty,

-

2.

To identify the changes in the transitory and permanent components of conditional variance of BRIC/BRICS nations,

-

3.

To assess the performance of different switching GARCH family models and identify the best model out of them.

Research methodology

The present study has explored the behaviour of the volatility of BRIC/BRICS nations with the assistance of GARCH (p,q) model, EGARCH model, GJR GARCH model, PGARCH model and CGARCH model. Data considered in the study range from 1st September 2006 to 31st October 2014 divided into three regimes. The first meeting of the foreign ministers of respective nations took place in New York City in September 2006 and after that a range of continuous meetings took place and finally BRIC was formed on 16th May 2008 because of which this period is considered as pre-BRIC formation period, and hence the first regime ranges from 1st September 2006. Later on, South Africa formally joined BRIC on 23rd December 2010, and BRIC became BRICS, and hence the third regime starts from 24th December 2010. The third regime exhibits the changes in relationships between the BRIC countries after the entry of South Africa. The purpose of considering these three regimes is to identify the changing role of respective nations in each other’s stock markets as well as in their own volatility behaviour before the formation of BRIC, on the formation of BRIC and on the formation of BRICS. The detailed analysis and duration of regimes are explained in “Structural changes in the conditional variance of BRIC/BRICS nations using CUSUMSQ test” of the study.

The indices selected for the study are IBOVESPA (Brazil), MICEX (Russia), BSE (India), SSE (China) and JSE (South Africa). Daily market prices of these nations are collected from 1st September 2008 to 31st October 2014 except South Africa whose prices are evaluated from 24th December 2010. The data have been collected from official websites of the respective stock markets and Yahoo finance. The market prices are converted into returns with the assistance following formula:

where R t indicates returns at time t, whereas P t and P t−1 are the stock prices at time t and t − 1. The stationarity of the time series has been assessed using augmented Dickey Fuller test. The null hypothesis of ADF test states that the “return has unit root” which is rejected in all the regimes for all the nations. The results are depicted in Table 16 in Appendix.

Model development for stock return volatility (extent of change in the structure of conditional volatility)

GARCH (1,1) model

The paradigm of GARCH (p,q) model has been pioneered by Bollerslev (1986) who recommends that conditional variance of any stock return is a linear function of its own lagged conditional variance and past squared error terms. The conditional mean equation of GARCH (1,1) model can be specified as follows:

Conditional volatility equation can be represented as follows:

In Eq. (2), R t is the logged stock returns and α is the impact of one period lagged returns on current returns. Here, standardized ε t is supposed to be independent and identically distributed (i.i.d) with zero mean and constant variance. Equation (3) represents the conditional variance equation where ht represents conditional variance of ε t which keeps on varying over the period of time. α 1 represents “news coefficient” (ARCH effect) which assesses the impact of one time period old information on current returns, whereas β 1 is called “persistence coefficient” (GARCH effect) which explores the impact of news older than one time period. In GARCH (p,q) model, p stands for ARCH effect and q stands for GARCH effect.

In the present study, generalized autoregressive heteroscedastic model (GARCH) is employed to investigate the flow of volatility or volatility spillover effect among the BRICS nations in three regimes. First of all, the residual series is extracted from the time series data of BRICS nations for the three time regimes. Furthermore, the extracted time series are squared to remove the negativity and then placed these residual series as shock originators in the volatility equation of other indices as a variance regressor. Significant coefficients of these variance regressors indicate successful spillover effect from one nation to another. GARCH (1,1) model for spillover effect has the following specifications:

The above equation identifies h t as the conditional variance of the specific stock indices which is intended to be regressed, furthermore, which is the function of ω 0 (mean). α 1 and β 1 represents “news coefficients” and “persistence coefficients”, whereas ψ represents the coefficient of residual series of stock returns of other time series incorporated in the variance equation. To select the best GARCH (p,q) model, AIC and SIC criterion are observed and it is assumed that the lowest the AIC and SIC, better the model is.

The standard GARCH (1,1) model assumes to have a symmetric response of volatility towards “good” and “bad” news; however, it is not the usual case which has been well exhibited by other GARCH family models.

Exponential GARCH (1,1) model

The fundamental GARCH model experiences certain difficulties and complexities which question the reliability and authenticity of this model. Firstly, certain restrictions are imposed on the conditional variance of the time series, and it is obligatory to keep it affirmative. Secondly, GARCH model failed to elaborate the asymmetric behaviour of volatility, because the conditional variance is the function of magnitude only and not the improvements in stock returns. Last but not the least, GARCH model does not elaborate cyclic and non-cyclic movements of volatility.

To conquer the above revealed obligations of fundamental GARCH model, Nelson (1991) pioneered the exponential GARCH model that considers logarithmic expressions of conditional variance. This model identifies the asymmetric affiliations among the conditional variance and the mean. EGARCH model can be specified as the following under normal distribution:

One of the most important advantages of EGARCH model lies in its non-negativity restrictions due to exponential form of conditional variance. The leverage effect is understood through the coefficient of λ where if λ ≠ 0, then it implies that the impact is asymmetric in nature. Fundamentally, this model assists in investigating “low volatility anomaly” that opposes the traditional CAPM theory that elaborates that higher risk results in higher returns.

GJR GARCH or TGARCH model

The next switching point is GJR GARCH or TGARCH model (Glosten et al. 1993; Zakoian 1994) which assists in incorporating structural changes in various regimes.

In this model, good news, ε t−i > 0, and bad news ε t−i < 0 have differential effects on the conditional variance. Here, α i has an impact of good news while α i + γ i have an impact of bad news. If γ i > 0, bad news has a greater impact of conditional variance, whereas if γ i ≠ 0, news impact is asymmetric.

PGARCH model

Taylor (1986) and Schwert (1989) introduced PGARCH model which considered standard deviation rather than variance. The following is the equation of PGARCH model:

The symmetric model has γ i = 0 and asymmetric if γ i ≠ 0.

Component GARCH model

In the present study, component GARCH model has been utilized to disintegrate between long-term and short-term memory, by empowering transitory departures of conditional variance around the time-varying trend. The model segregated conditional variance into permanent and transitory components. The following is the specification of CGARCH model:

Swift advancements in computer technology have given rise to analytical tractability of consecutively higher frequencies of financial market data. Models observing multiple volatility components are important to fully characterize the complex intraday volatility dependencies. CGARCH model captures different features of conditional variance, where the volatility is decomposed into two parts, namely permanent (trend) component and transitory (short term) component. The component model also provides a natural extension of the GARCH model in terms of generalizing the latter’s ARIMA representation for squared residuals (Puttaswamaiah 2009). Engle and Lee (1999) decompose the conditional variance into permanent and transitory components that is mean reverting towards the trend component. Such behaviour of CGARCH model explains the long run and short run behaviour of volatility.

CUSUMSQ test for identifying structural changes in BRIC/BRICS nations

Cumulative sum of squares (CUSUMSQ) process is applied to identify structural breaks in the conditional variance of BRICS nations. Cumulative sum of squares statistics was first pioneered by Inclan and Tiao (1994) and subsequently developed by Kim et al. (2000), Kokoszka and Leipus (2000) and Lee and Park (2001). A CUSUMSQ test is a cumulative difference between successive values and targeted values.

Dynamic forecasting process for model comparison

Besides estimation of conditional volatility, it is important to forecast volatility so that one can conduct the comparison among the models to identify the best model. Dynamic forecasting analysis has been carried out in the study to estimate the difference between actual and forecasted values. The lesser the gap between actual and forecasted values, the better is the model. The lower the forecasting error, the better is the predictive power of the model. To evaluate and compare the forecasting ability of the models, different evaluation criterions are calculated, such as root mean square error, mean absolute error, mean absolute percentage error and Theil’s U/Theil’s inequality coefficient. RMSE is the square root of the variance of the residuals which designates the closeness of the observed data points to the predictive values. It explains the absolute fit of the model. It is also known as the standard deviation of the unexplained variable. The lower the value of RMSE, the better is the model. Mean absolute error identifies the average magnitude of the errors in a set of forecasts, devoid of taking their directions into account. It tells how large of an error we can expect from the forecast on an average. Again the lower the value of MAE, the better is the model. RMSE and MAE both can be used to identify the best-fitted model. The RMSE will always be greater or equal to MAE; the greater difference between them symbolizes more significant variance in the individual samples. Again the mean absolute percentage error explains the same thing as described by MAE but in percentage manner. Theil’s U/Theil’s inequality coefficient measures how well a time series of the estimated values are near to the actual value. This coefficient is useful in comparing different models. The near the value to zero, the better is the model.

Empirical results and analysis

The present section of the study depicts the results of structural changes in the conditional variance of respective nations on the formation of BRIC/BRICS treaty through CUSUMSQ test, spillover effect using GARCH (p,q) model, leverage effect using EGARCH model, GJR GARCH model and PGARCH model and permanent and transitory behaviour of volatility using CGARCH in three regimes. Dynamic forecasting process is employed to assess the best-fitted model among EGARCH, GJR GARCH and PGARCH model.

Structural changes in the conditional variance of BRIC/BRICS nations using CUSUMSQ test

Before assessing the impact of BRIC/BRICS treaty on the conditional variance of select nations, it is important to discover that whether there exist any structural changes in the volatility behaviour of the stock returns or not. For the very purpose, CUSUMSQ test is applied to determine the existence of structural changes in the conditional variance of stock returns of select nations.

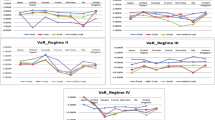

On observing the results of CUSUMSQ test in the form of graphical representations of all the nations, it has been observed that all the nations experience structural changes in the conditional variance on the formation of BRIC treaty, whereas none of the nations depict structural changes in the conditional variance on the entry of South Africa. Structural break is observed on 1st October 2008 for Brazil, 30th September 2008 for Russia, 16th July 2008 for India and 15th January 2008 for China in graphical representation of CUSUMSQ test for BRIC which suggests that conditional variance of Brazilian, Russian, Indian and Chinese stock returns experienced structural breaks, not on the exact date of BRIC formation but few months before or after the formation. On the other hand, South Africa depicts many structural breaks in the conditional variance after its entry in BRICS. However, all the countries report the existence of the structural break in February/March 2014 which is not considered for testing as it is not related to BRICS formation. It may be due to global events taking place in world economies.

Graphs representing results of CUSUMSQSQ statistics for BRICS nations from 1st September 2006 to 31st October 2014

On the basis of the above results, the three regimes are redefined where the first regime ranges from 1st September 2006 to 1st October 2008 for Brazil, 1st September 2006 to 30th September 2008 for Russia, 1st September 2006 to 16th July 2008 for India and 1st September 2006 to 15th January 2008 for China. Structural breaks are not visible on the entry of South Africa; that is why the second structural break is considered exogenously on 24th December 2010, whereas the first break is considered as endogenously. The second Regime ranges from 2nd October 2008 to 23rd December 2010 for Brazil, 1st October 2008 to 23rd December 2010 Russia, 17th July 2008 to 23rd December 2010 for India and 16th January 2008 to 23rd December 2010 for China and third regime ranges from 24th December 2010 to 31st October 2014 for BRICS.

On the basis of the above results, the three regimes are redefined where the first regime ranges from 1st September 2006 to 1st October 2008 for Brazil, 1st September 2006 to 30th September 2008 for Russia, 1st September 2006 to 16th July 2008 for India and 1st September 2006 to 15th January 2008 for China. Structural breaks are not visible on the entry of South Africa; that is why the second structural break is considered exogenously on 24th December 2010, whereas the first break is considered as endogenously. The second Regime ranges from 2nd October 2008 to 23rd December 2010 for Brazil, 1st October 2008 to 23rd December 2010 Russia, 17th July 2008 to 23rd December 2010 for India and 16th January 2008 to 23rd December 2010 for China and third regime ranges from 24th December 2010 to 31st October 2014 for BRICS.

Volatility spillover among BRIC/BRICS nations using GARCH (p,q) model

The present section of the study examines the volatility spillover effect using GARCH (p,q) model in three regimes, where the first regime ranges from 1st September 2006 to 1st October 2008 for Brazil, 1st September 2006 to 30th September 2008 for Russia, 1st September 2006 to 16th July 2008 for India and 1st September 2006 to 15th January 2008 for China, which signifies pre-formation period of BRIC for Brazil, Russia, India and China. The second regime ranges from 2nd October 2008 to 23rd December 2010 for Brazil, 1st October 2008 to 23rd December 2010 for Russia, 17th July 2008 to 23rd December 2010 for India and 16th January 2008 to 23rd December 2010 for China, which designates post-formation period and the third regime ranges from 24th December 2010 to 31st October 2014 which symbolizes post-formation period after the entry of South Africa.

Before applying GARCH (p,q) model, best GARCH model is selected by the least value of AIC and SIC. Lowest the coefficient of SIC and AIC, better the model is. The results of AIC is given preference in case the results of AIC and SIC do not demonstrate similar results. The best-fitted models are depicted in Table 1. (The detailed results of AIC and SIC are provided in Table 17 in Appendix).

Table 2 illustrates the results of the spillover effect in regime 1 using GARCH model. Different GARCH (p,q) model has been applied as per the AIC and SIC. The results confirm that Brazil receives volatility from Russia (−0.063), Russia from Brazil (0.088) and India (−0.061), India from Brazil (0.064) and China from Brazil (0.095), Russia (0.052) and India (−0.070). On observing the other side of the coin, it is noticed that Russia is transmitting volatility towards Brazil (−0.063) and China (0.052), India towards Russia (−0.061) and China (−0.070) and Brazil towards Russia (0.088), India (0.064) and China (0.095). In a nutshell, it is observed that Brazil is transmitting volatility towards all the nations, whereas China is incapable of transmitting volatility towards any of the nations. India and Brazil are the least contagious among all the member nations.

Table 3 depicts the results of regime-2 for BRIC nations using the best selected GARCH model. In regime-2, Brazil receives volatility spillover from Russia (0.020), Russia from Brazil (0.062) and India (0.030), India from Brazil (−0.017) and Russia (0.010) (at 10 % level of significance) and China from Brazil (0.061) and India (0.018). On observing the results, it is noticed that Russia, India and China receive volatility from two nations, whereas Brazil receives volatility spillover from one nation only. On the other hand, Brazil and Russia are transmitting volatility spillover towards all the three nations, India towards one nation only and China does not transmit volatility towards any of them.

Table 4 demonstrates the results of volatility spillover of BRICS nations on the entry of South Africa into BRIC treaty in December 2010. The results confirm that Brazil does not receive volatility spillover from any of the nation, whereas Russia receives volatility spillover from all the nations, namely Brazil (−0.028), Russia (−0.082) (at 10 % level of significance), China (−0.087) and South Africa (−0.059). India receives volatility spillover from Brazil (0.012) Russia (−0.006) and South Africa (0.014). China receives volatility spillover from Brazil (−0.012) and India (0.054). South Africa receives volatility spillover from Russia (−0.011) and India (−0.085). Here, Brazil does not receive volatility from any of the nation, Russia from all the nations, India from three and China and South Africa from two. On the other hand, Brazil and India are transmitting volatility spillover towards three nations, Russia and South Africa towards two and China towards one.

Comparative analysis of three regimes

On comparing the performance of all the nations in the three regimes, considerable volatility spillover is observed in all the nations in regime one and with the passage of time the level of volatility spillover increased considerably. Volatility spillover is the highest in regime three but not as per the expectations. India receives volatility spillover from Brazil in regime one, whereas it started receiving volatility spillover from Brazil and Russia in regime two. On the other hand, Brazil receives volatility spillover from Russia only in the first two regimes but on reaching the third regime it does not receive volatility from any of the nation. Russia has also demonstrated an increasing pattern in receiving the volatility spillover. China has quite a scattered impact of other nations on its volatility. South Africa has experienced maximum structural breaks as per CUSUMSQ test. But there is a possibility that South Africa must have been received volatility spillover from rest of the world rather than only from BRIC/BRICS nations. South Africa is the new entry in BRICS, which influenced the volatility equation of rest of the nations considerably.

Existence of permanent and transitory components of volatility among BRIC nations using component GARCH model

The second segment of this section reports the results of CGARCH model to exhibit the presence of permanent and transitory components of conditional variance in three regimes for BRIC/BRICS nations.

Table 5 exhibits the results of CGARCH model for the first regime where five parameters namely α 0, ρ, μ, α 1, and δ 1 are identified. The positive coefficients of α 1 for the markets, such as IBOVESPA (0.128) and SSE (0.095) [except for MICEX (−0.228)], indicate towards the positive preliminary impact of any news on the transitory component. The coefficient of δ 1 is significant only for Brazil (IBOVESPA) [0.753 (0.000)] and China (SSE) [0.839 (0.000)]. A positive coefficient of δ 1 for Brazil and China designates the positive degree of memory in transitory component of conditional variance. A less than one coefficient of α 1 and δ 1 identifies persistence of conditional variance in the transitory component. In regime-1, the sum of α 1 and δ 1 is less than one for all the indices but significant only for Brazil (IBOVESPA) (0.881) and China (SSE) (0.934). Furthermore, the coefficient of ρ < 1 and ρ > α 1 + δ 1 signifies long memory component of conditional variance. The coefficient of μ is significant for Russia (0.234), India (0.126) and China (−0.056), which indicates towards mounted permanent component of conditional variance.

Table 6 reports the results of CGARCH model for the second regime. The coefficient of μ is significant for Brazil (−0.162) and India (−0.131) which supports increased permanent component of conditional variance. The coefficient of δ 1 is positive and significant for Brazil (0.623) which supports the positive degree of memory in its transitory component, whereas it is negative and significant for Russia (−0.964) and India (−0.550) which supports the negative degree of memory in its transitory component. The sum of α 1 and δ 1 for Brazil (1.066) is more than the coefficient of ρ (0.109) and 1, which does not indicate towards long memory component of conditional variance. The coefficient of α 1 is positive and significant for Brazil (0.150) which signifies positive preliminary impact of any news on the conditional variance.

Table 7 represents that the result of CGARCH model for the 3rd regime ranges from 24th December 2010 to 30th October 2014. The significant coefficient of μ for all the markets (0.085, 0.453, 0.058, 0.017 and 0.036) signifies the existence of augmented permanent component of conditional variance. The coefficient of δ 1 is positive and significant for Russia (1.346) which indicates towards the positive degree of memory in its transitory component, whereas it is negative for Brazil (−0.748) and South Africa (−0.811) which signifies the negative degree of memory in its transitory component. The sum of α 1 and δ 1 is significant and less than ρ for Brazil (−0.804), Russia (0.933) and South Africa (−0.765) and coefficient of ρ is less than one for all the markets that designate towards long memory component of conditional variance. Here, the coefficient of α 1 is negative and significant for Brazil (−0.056), Russia (−0.413) and China (−0.042) which supports the negative preliminary impact of any news on its conditional variance and positive and significant for South Africa (0.046) which claims the positive preliminary impact of any news. However, it is insignificant for India [−0.042 (0.074)].

Comparative analysis of permanent and transitory components of conditional volatility

In the first regime, Brazil and China exhibited a positive preliminary impact of any news on the conditional variance, whereas Russia reported negative preliminary impact on the conditional variance. Brazil is the only country that demonstrated a positive preliminary impact of any news on the conditional variance in the second regime. In the third regime, the situations transformed completely, and all the markets started reacting to the market news. Brazil, Russia and China started responding to market news and a negative preliminary impact on the conditional variance has been observed in the third regime for these three markets. India also reported a negative preliminary impact on the conditional variance, but it is not significant at 5 %. South Africa is the only country that exhibits positive preliminary impact of any news on the conditional variance of stock returns in the third regime. South Africa has gone against the flow by demonstrating a positive preliminary impact of any news on the conditional variance, as other countries have exhibited negative preliminary impact on conditional variance. In the first regime, Brazil and China have a positive degree of memory. In the second regime, Brazil experienced a negative, whereas Russia and India have a positive degree of memory. In the third regime, Brazil and South Africa have a negative degree of memory and Russia has a positive degree of memory. The results exhibit more of a positive degree of memory in conditional variance in the first regime, whereas the second and third regimes support a negative degree of memory. In all the three regimes, most of the countries experienced the permanent and transitory components of conditional variance.

Leverage effect

Leverage effect using exponential GARCH model

Nelson (1991) pioneered one of the prominently employed model named exponential GARCH to ascertain the behaviour of volatility in rising and declining returns. EGARCH model assists in understanding the “leverage effect” which states that “leverage effect is the tendency for volatility to decline when returns rise and to rise when returns fall” (Sah 2011). EGARCH model comes up with four major parameters known as ω, β, α and λ that further contribute to ascertain symmetric and asymmetric behaviour of volatility.

“The α parameter represents a magnitude effect or the symmetric effect of the model, the “GARCH” effect. β measures the persistency in conditional volatility irrespective of anything happening in the market. When β is relatively large, then volatility takes a long time to die out following a crisis in the market.” (Alexander 2009). The coefficient of λ supports in enumerating the leverage effect and scrutinizing asymmetries in conditional variance. “If λ = 0, then the model is symmetric. If λ < 0, then positive shocks (good news) generate less volatility than negative shocks (bad news). When λ > 0, it implies that positive innovations are more destabilizing than negative innovations.” (Sah 2011). “If λ < 0, then the model is asymmetric and leverage effect assists in the market.” (Saeed et al. 2013).

Table 8 identifies the results of leverage effect for the first regime. The coefficient of λ is less than one and significant for Brazil, Russia and India (−0.220, −0.130 and −0.223). The results suggest that arrival of any bad news increases the volatility of stock returns in comparison to any good news. This behaviour of volatility assures the existence of “low volatility anomaly”, which states that low volatility results in higher returns.

Table 9 declares the results of leverage effect for regime-2 using EGARCH model where the coefficient of λ is less than one and significant in all the markets (−0.088, −0.035, −0.067 and −0.030). The results confirm the existence of “low volatility anomaly” in all the markets after the formation of BRIC also. As a result, no change in the behaviour of volatility has been observed.

Table 10 represents the results of EGARCH model for the 3rd regime for all the BRICS nations. The coefficient of λ is less than one for Brazil (−0.081), Russia (−0.140), India (−0.078), China (−0.053) and South Africa (−0.001). However, the coefficient of South Africa is not significant. The less than one coefficient of selected markets indicates towards the existence of “low volatility anomaly” which states that arrival of any bad news destabilizes the volatility of stock returns to a greater extent in comparison to the arrival of a good news.

Leverage effect using GJR GARCH model

GJR GARCH model was introduced by Glosten et al. (1993) which assesses the asymmetry in conditional variance. This section of the study elaborates the results of GJR GARCH model to find out leverage effect in the stock returns in three regimes.

Table 11 reports the results of leverage effect using GJR GARCH model for Brazil, Russia, China, India and South Africa in three regimes. The coefficient of γ is assessed to interpret the asymmetry in conditional variance. The coefficient of γ is significant for all the markets in three regimes, but it is less than zero in the case of South Africa [−0.747 (0.000)] which confirms that bad news failed to destabilize the conditional variance more than good news. A negative coefficient of γ in the case of South Africa reports that good news has greater impact on the conditional variance in comparison to bad news and hence opposes the leverage effect. However, the coefficients of Brazil, Russia, India and China are greater than zero (γ > 0) in all the regimes that confirm the existence of leverage effect. Moreover, the coefficients of γ ≠ 0 for all the nations in each regime signify asymmetric conditional variance. Here, South Africa is the only country that does not demonstrate leverage effect.

Leverage effect using PGARCH model

This section of empirical analysis depicts the results of PGARCH model introduced by Taylor (1986) and Schwert (1989) which consider standard deviation rather than variance. The results are depicted in Table 12 in three regimes.

Table 12 reports the results of PGARCH model to assess the existence of leverage effect among BRICS nations in three regimes. Model is asymmetric if the coefficient of γ ≠ 0. On assessing the results, it has been recognized that none of the coefficients are equal to zero which confirms the fact that conditional variance of all the nations is asymmetric.

Comparative analysis of leverage effect

The overall analysis of leverage effect exhibits that negative information destabilizes the conditional variance to a greater extent in comparison to positive information. Only South Africa remained indifferent in the third regime due to insignificant λ coefficient in EGARCH model and GJR GARCH model. However, the three models collectively confirm the asymmetric behaviour of conditional variance, and there is no change in this behaviour of conditional variance.

Dynamic forecasting for model comparison

The present section of the study declares the results of dynamic forecasting analysis with the help of RMSE, MAE, MAPE and Theil’s U/Theil’s inequality coefficient.

Table 13 reports the results of dynamic forecasting for BRIC nations in regime-1 through RMSE, MAE, MAPE and Theil’s U criterion. On comparing the performance of EGARCH, GJR GARCH and PGARCH model for Brazil, it is observed that RMSE (1.978) (which is a measure of standard deviation) is same in all the three models and MAE (which is a measure of mean) is the lowest in PGARCH model (1.442). On assessing the value of MAPE, EGARCH model is considered to be the best model with the lowest MAPE (101.032). Theil’s U statistic also declares PGARCH (0.968) to be the best model with the lowest value among the rest, however, not satisfactory as per standard rule.

In the case of Russia, RMSE is similar in all the three tests, whereas MAE (1.467) and MAPE (104.092) are the least in GJR GARCH model and Theil’s inequality is the least in PGARCH (0.973).

In the case of India, RMSE is the least in PGARCH (1.781), MAE is the lowest in GJR GARCH and EGARCH model (1.261), MAPE is the least in PGARCH model (108.095), and Theil’s U is the least in GJR GARCH model (0.944).

For China, the lowest RMSE is observed in EGARCH and GJR GARCH model (1.987), the least MAE is reported in PGARCH model (1.410), the least MAPE is observed in EGARCH (159.940) and the least Theil’s U is recorded for PGARCH (0.748).

On comparing the overall performance of all the models in regime-1, it is observed that PGARCH model has an upper edge in comparison to GJR GARCH and EGARCH model.

Table 14 reports the results of dynamic forecasting analysis for BRIC nations in regime-2. In the case of Brazil, Russia and India the values of RMSE are same for all the three tests, so a comparison could not be done by this criterion, Whereas in the case of China, the value of RMSE is the least in the case of GJR GARCH (2.128). MAE is the least in GJR GARCH model for Brazil (1.474), Russia (2.046) and China (1.508). India registered similar coefficient of MAE for all the three models. MAPE is the least in EGARCH model (103.975) for Brazil, PGARCH (117.590) for Russia, PGARCH (109.979) for India and GJR GARCH (95.043) for China. Theil’s U is the least in the case of GJR GARCH for Brazil (0.975), Russia (0.953) and India (0.0957). EGARCH registered the lowest Theil’s U coefficient for China (0.984). Here, GJR GARCH model is observed to be the best model with a maximum number of the lowest coefficient.

Table 15 demonstrates the results of dynamic forecasting for the BRICS nations in the third regime. RMSE and MAE cannot be compared in case of Brazil, Russia, India and China as their coefficients are same in all the three tests, except in the case of South Africa where RMSE (1.292) and MAE (0.930) are the least in GJR GARCH model and PGARCH model. MAPE is the least in PGARCH model (105.122) for Brazil, EGARCH and GJR GARCH (106.643) for Russia, PGARCH (115.550, 105.770 and 96.060) for India, China and South Africa. Theil’s U is the least in EGARCH model (0.965) for Brazil, PGARCH (0.976) for Russia, GJR GARCH (0.971) for India, EGARCH (0.980 and 0.957) for China and South Africa. On comparing the overall performance, EGARCH reported the least values for a maximum number of times.

The three different regimes registered different models to be the best one. Regimes one, two and three reported PGARCH, GJR GARCH and EGARCH models to be the best one, respectively. Hence, the results are incapable of declaring the best model.

Managerial implications

The present study contributes in assessing the performance and interlinkages of BRIC/BRICS nations in varying time regimes. The study contributes to explore the changing relationships among the nations after entering into any treaty. The study has been divided into three regimes that represent the pre-formation period of BRIC, the post-formation period of BRIC and the post-formation period of BRICS on the entry of South Africa. The study discovered that initially the markets were a little contagious towards each other, and the reasons could be increased trade opportunities among member nations or inflated enthusiasm among investors. Till 2010, BRIC nations entered into a lot of many trade associations, such as exports/imports and FDI. The GDP of all the nations has increased considerably. But the inter-relationships among the nations have not demonstrated the expected level of bondages. The probable reason explored is the impact of the global recession which affected Brazil the most, whereas Russian and Chinese economies were very contagious in the beginning and also demonstrated weaker signs of integration and development. It is observed that as the treaty became old, the ties among them start loosening up due to the global recession. Hence, the diversification opportunities have also increased in later stages. The study suggests that in initial stages of treaty formation, the prediction was quite easy because of inflated herding among the investors but later on herding behaviour of investors did not increase as per the expectations, and more of diversification opportunities were available. The study assists investors in strategizing their investment plans on the formation of the treaty. Investors can gain superior profits by accurately predicting stock prices and volatility by the stock prices and volatility of member nations. Herdism among member nations reduced gradually with time and prediction becomes more difficult on the arrival of the global recession. In such situations, investors can diversify their portfolio and minimize their risk exposure. Such situations give rise to an opportunity for investors for “global portfolio diversification”. The study recommends an important implication that in shinning phase all the member nations illustrate a high level of integration due to inflated business opportunities but on the arrival of the global slowdown, economies start moving individually because of the reduced level of trade opportunities. However, the entry of South Africa rejuvenated the spillover effect. Hence, investors can strategize their investments according to both current relationships among the member nations as well as global market situations.

Findings

The present study exemplifies the volatility behaviour of BRIC/BRICS nations in three regimes, representing the pre-formation period, post-formation period and post-formation period on the entry of South Africa. The study has employed various GARCH family models to probe out varying volatility patterns and behaviours in diverse time regimes. The study has employed GARCH (p,q) model, EGARCH model, GJR GARCH model, PGARCH model and CGARCH model for assessing the volatility behaviour of BRICS stock markets in three eras of pre-BRIC, post-BRIC and post-BRICS. The above-mentioned advanced econometric models assess the volatility behaviour of BRICS nations. GARCH (p,q) model has been applied to assess spillover effect among BRICS nations in three respective eras. EGARCH model, GJR GARCH model and PGARCH model assisted in exploring “low volatility anomaly” which confirms that bad news destabilizes the volatility up to a greater extent in comparison to good news, whereas CGARCH model explored the existence of the permanent and transitory components of conditional variance.

The study explored varying affiliations among BRIC/BRICS nations, where it has been assessed that all the nations were extremely influenced by each other at initial stages of the treaty. The BRIC group demonstrates some of the remarkable trends in its foreign trade figures, such as exports increased from 13.3 to 49.8 % from the mid-1990s up to 10 years. In 2002–2010, worldwide FDI flow increased from USD 10 Billion to USD 146 Billon. In each regime, India is discovered to be the least influenced by the volatility of other nations and Russia is seemed to be the most contagious. Hence, the prediction for Indian stock market by other BRICS nations was not possible in the first regime, while prediction for Russian stock market was feasible in each of the regimes. South Africa’s share in total numbers is rather negligible, Brazil and India account for about 10 % each while China and Russia claim more than 75 % of total BRICS’ FDI in 2010. Overall, Russian flows sum up to USD 265 billion during the last decade, putting China in the second place with USD 251 billion. But Chinese FDI has increased the most and is likely to outnumber Russia over the next years (Morazan et al. 2012). BRICS has initiated many development financing plans, particularly from China and India. It comes in the form of larger packages which include large grants, where concessional and non-concessional loans were accumulated to trade and investment engagements. On reaching the third regime, Indian market became contagious while Brazilian market was least contagious.

On reaching the third regime, the equations of all the nations changed completely, and there was a significant recovery in the volatility spillover among the nations that was diminished due to the global recession. UNCTAD-statistics show a steadily growing tendency in outward FDI for all BRICS, despite a decline in 2009 due to the financial crisis during which especially Brazil suffered from a recession (Morazan et al. 2012). Diversification opportunities among BRIC nations were moderate due to augmented spillover effect during the first regime, whereas diversification opportunities have increased a little during the second regime due to reduced spillover effect in the case of few nations. Third regime experienced greater volatility transmission but not as per the expectations.

One of the imperative behaviours of volatility is acknowledged as “leverage effect” or “low volatility anomaly”. Low volatility anomaly has been observed in all the nations (except South Africa) in each regime which states that bad news destabilizes the volatility to a larger extent in comparison to positive news. The study has also assessed the varying preliminary reactions to any market news on the conditional variance. In the first regime, only Brazil and China demonstrated a positive preliminary impact of any news on the conditional variance, while in the second and third regime, all the nations demonstrated negative preliminary impact of any news on the conditional variance (except South Africa in the third regime and Brazil in second regime). All the nations exhibit the existence of the permanent and transitory components of conditional variance in each regime. The outcomes of the study display rejuvenated interlinkages among the BRICS stock markets after the entry of South Africa, whereas all the nations depict almost simultaneous volatility behaviour in all the regimes.

The study has compared the performance of EGARCH model, GJR GARCH model, PGARCH model with the assistance of dynamic forecasting, where the statistics, such as RMSE, MAE, MAPE and Theil’s U/Theil’s inequality criterion, are compared to identify the best model. The results did not declare the superiority of any of the model because PGARCH model outperformed in regime one, GJR GARCH model in regime two and EGARCH model in regime three. However, none of the models performed as per the expectations that leave room for future scope of the study.

References

Alexander C (2009) Practical financial econometrics. John Wiley and Sons Ltd

Antonious A, Holmes P, Priestley R (1998) The effects of stock market futures trading on stock index volatility: an analysis of the stock market response of volatility to news? J Futures Markets 18:151–166

Bai J, Perron P (2003) Computation and analysis of multiple structural change models. J Appl Econom 18(1):1–22

Bekaert G, Wu G (2000) Asymmetric volatility and risk in equity markets. Rev Financ Stud 13:1–42

Bekiros SD (2013) Decoupling and the spillover effects of the US financial crisis: evidence from BRIC markets. The Rimini centre for economic analysis. Working paper 13–21

Bhar R, Nikolova B (2007) Analysis of mean and volatility spillover using BRIC countries, regional and world equity index returns. J Econ Integr 22(2):369–381

Bierens HJ (1997) Nonparametric cointegration analysis. J Econ 77:379–404

Black F (1976) Studies in stock price volatility changes. In: proceedings of 1976 meetings of the American Statistical Association. Business and economics statistics section. American Statistical Association, pp 177–181

Bollerslev T (1986) Generalized autoregressive conditional heteroskedasticity. J Econ 33:307–327

Campbell JY, Hentschel L (1992) No news is good news: an asymmetric model of changing volatility in stock returns. J Financ Econ 31:281–318

Christie A (1982) The stochastic behaviour of common stock variance: value, leverage and interest rate effects. J Financ Econ 10:407–432

Dasgupta R (2013) BRICS and US integration and dynamic linkages: an empirical study for international diversification strategy. Interdiscip J Contemp Res Bus 5(7):536–563

Ding Z, Granger CWJ, Engle RF (1993) A long memory property of stock market returns and a new model. J Empir Finance 1:83–106

Engle R, Lee G (1999) A permanent and transitory component model of stock return volatility. In: Engle RF, White H (eds) Cointegration, Causality, and Forecasting: A Festschrift in Honor of Clive W.J. Granger. Oxford University Press, p 475–497

Filis G, Degiannakis S, Floros C (2011) Dynamic correlation between stock market and oil prices: the case of oil-importing and oil-exporting countries. Int Rev Financ Anal 20(3):152–164

French KR, Schwert GW, Stambaug R (1987) Expected stock returns and volatility. J Financ Econ 19:3–29

Glosten LR, Jagannathan R, Runkle DE (1993) On the relations between the expected value and the volatility of nominal excess returns on stocks. J Finance 48:1779–1791

Gomez S, Ahmad H (2014) Volatility transmission between PALS, FOES, MINIONS and TITANS. IOSR J Bus Manag 16(1):122–128

Guesmi K, Fattoum S (2014) Return and volatility transmission between oil prices and oil-exporting and oil-importing countries. Econ Modell 38:305–310

Guesmi K, Kaabia O, Kazi IA (2013) Does shift contagion exist between OECD Stock markets during the financial crisis. J Appl Bus Res 29(2):469–484

Inclan C, Tiao GC (1994) Use of cumulative sum of squares for retrospective detection of changes in variance. J Am Stat Assoc 89:913–923

Junior TP, Lima FG, Gaio LE (2014) Volatility behaviour of BRIC capital markets in the 2008 international financial crisis. African J Bus Manag 8(11):373–381

Kim S, Cho S, Lee S (2000) On the CUSUMSQ test for parameter changes in the GARCH (1,1) models. Comm Stat Theory methods 29:445–462

Kokoszka P, Leipus R (2000) Change point estimation in ARCH models. Bernoulli 6:1–28

Lee S, Park S (2001) The CUSUMSQ of squares test for scale changes in infinite order moving order average processes. Scand J Stat 28:625–644

Lee B, Rui OM, Wang SW (2004) Information transmission between the NASDAQ and Asian second board markets. J Bank Finance 28(1):1637–1670

Liu YA, Pan MS (1997) Mean and volatility spillover effects in the US and Pacific-Basin stock markets. Multinatl Finance J 1:47–62

Morazan et al (2012) The role of BRICS in the developing world. Directorate-General for external policies of the union. European Parliament. http://www.ab.gov.tr/files/ardb/evt/1_avrupa_birligi/1_9_politikalar/1_9_8_dis_politika/The_role_of_BRICS_in_the_developing_world.pdf. European Union, Apr 2012

Nair AS (2011) Existence and extent of impact of individual stock derivatives on spot market volatility in India. Applied Financ Econ 21:563–600

Nelson DB (1991) Conditional heteroskedasticity in asset returns: a new approach. Econometrica 59(2):347–370

O’Neill J (2001) Building better global economic BRICs. Goldman Sachs Glob Econ Pap 66:1–16

Pindyk RS (1984) Risk, inflation and stock market. Am Econ Rev 74:334–351

Puttaswamaiah (2009) Recent developments in modelling of financial market volatility. Future of Econ Sci 507

Ramasamy R, Munisamy S (2012) Predictive accuracy of GARCH, GJR and EGARCH models select exchange rates application. Glob J Manag Bus Res 12(15):89–100

Robbani MG, Bhuyan R, Sbeiti WM (2013) On the dynamics of volatility transmission: an empirical investigation on G-8 countries. Invest Manag Financ Innov 10(1):166–173

Saeed SK, Riaz K, Ayub U (2013) Financial contagion in South Asia: an EGARCH approach. Am J Sci Res (85):105–111

Sah AN (2011) Behaviour of stock return volatility in India: a study in the context of US subprime crisis. Decision 38(3):26–38

Schwert W (1989) Threshold heteroskedastic models. J Econ Dyn Control 18:931–944

Taylor S (1986) Modelling financial time series. John Wiley & Sons, New York

Wilson D, Purushothaman R (2003) Dreaming with BRICS, the path to 2050. Goldman Sachs Glob Econ Pap 99:1–22

Wilson D, Kelston AL, Ahmed S (2010) Is this BRICs decade? BRICS Mon 10(3):1–4

Xu XE, Liu J (2001) Short term dynamics transmission and long term foreign share discount: evidence from the Chinese stock markets. Int J Bus 6(2):33–51

Yilmaz K (2010) Return and volatility spillovers among the East Asian equity markets. J Asian Econ 21:304–313

Zakoian JM (1994) Threshold heteroskedastic models. J Econ Dyn Control 18(5):931–955

Zhong M, Chang T, Tzeng H (2014) International equity diversification between The United States and BRICS countries. Rom J Econ Forecast 17(1):123–138

Zivot E (2009) Practical issues in analysis of univariate GARCH models. In: Anderson TG, Davis RA, Krei JP, Mikosch T (eds) Handbook of financial time series. Springer, Berlin, pp 113–155

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Narula, I. Dynamics of volatility behaviour and transmission: evidences from BRICS countries. Decision 43, 31–51 (2016). https://doi.org/10.1007/s40622-015-0119-8

Published:

Issue Date:

DOI: https://doi.org/10.1007/s40622-015-0119-8