Abstract

“Doubling up” (living with relatives or nonkin) is a common source of support for low-income families, yet no study to date has estimated its economic value relative to other types of public and private support. Using longitudinal data from the Fragile Families and Child Wellbeing Study, we examine the prevalence and economic value of doubling up among families with young children living in large American cities. We find that doubling up is a very important part of the private safety net in the first few years of a child’s life, with nearly 50 % of mothers reporting at least one instance of doubling up by the time their child is 9 years old. The estimated rental savings from doubling up is significant and comparable in magnitude to other public and private transfers.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

A large body of research shows that low-income families in the United States often rely on housing support from family and friends to make ends meet (e.g., Edin and Lein 1997; Hofferth 1984; Stack 1974; Tienda and Angel 1982). According to census data, about 20 % of children were living in a doubled-up household in 2010 (Mykyta and Macartney 2012), and this number likely underestimates the percentage of children that ever experience doubling up (defined here as households with an adult who is not the mother, the mother’s partner, or adult child). Despite its prevalence, no study has attempted to estimate the monetary value of this type of private transfer, and no research has compared the value of doubling up with other types of public and private income sources. This oversight is important: housing costs typically account for at least 30 % of a household’s budget and up to 50 % of total income among low-income families living in U.S. urban areas (Schwartz and Wilson 2007). To address this gap in the literature, we examine the prevalence of different types of doubling up, the characteristics of mothers who double up, and the estimated rental savings associated with doubling up. We pay special attention to whether a mother is married, cohabiting, or single because we expect the need and economic value of doubling up to vary by mothers’ relationship status.

Data, Measures, and Methods

We use data from the Fragile Families and Child Wellbeing Study (FFS), a nationally representative birth cohort study of ~5,000 children born in large U.S. cities between 1998 and 2000. Mothers were interviewed at the time of their child’s birth and again when the child was 1, 3, 5, and 9 years old. These data are well suited for our purposes because they allow us to study doubling up over time among urban families with young children—a population for whom doubling up may be particularly important. These data also include a large oversample of births to unmarried parents, which allows us to investigate heterogeneity in doubling up by mother’s relationship status: single, cohabiting, and married.

To describe the prevalence of doubling up by child’s age, we use data from each wave of the study. We pool the data to describe the characteristics of doubled-up households (N = 4,897; 21,147 person-waves). To describe the types of doubling up, we pool data from Waves 2–5 (N = 4,707; 16,249 person-waves). The analysis of rental savings to doubling up is restricted to Waves 3–5, when lease information is available (N = 4,589; 11,885 person-waves). Although item-specific missing data are rare (between 1 % and 3 % on any given variable), there is attrition from the study over time, especially among economically disadvantaged mothers, immigrant mothers, and Hispanic mothers. In the Discussion section, we consider ways in which attrition might affect our findings.

Doubling Up

Doubling up is coded as 1 if a grandparent, a parent/in-law, a sibling, an aunt/uncle, a nonrelated adult, or a niece/nephew over the age of 18 is living in the household. Following Mykyta and Macartney (2012), we do not consider a mother to be doubled up if she lives with a partner (either married or cohabiting), an adult biological or adoptive child, or other children or relatives younger than age 18. Although living with a partner is a form of doubling up, we do not include those cases because the underlying motivation for moving in with a partner (or moving out) is likely to differ for this group. We construct measures of doubling up (at wave) and a measure of whether a mother was ever doubled up (over all waves).

We also distinguish among different types of doubling up (e.g., living with a parent versus an adult sibling), and we count the number of other adults in the household. Transition patterns are assessed across all survey waves and are coded as follows: always doubled up; doubled up, then not; not doubled, then doubled; two transitions into and out of a doubled-up household; and three or four transitions.

Homeownership and Rent

If a mother reports owning a home, she is coded as homeowner; otherwise, she is coded as a renter (excluding mothers who live in a shelter/are homeless). Mothers who rent are asked, “How much rent do you pay each month?,” and this variable is used to construct yearly rental payments. Mothers who own their homes report annual mortgage payments. Mothers also report whether they live in a home owned by someone else; for rentals, mothers are asked whose name is on the lease. We construct a variable that distinguishes mothers who own their own home, live in a home owned by another and pay no rent, live in a home owned by another and pay rent, rent their own home (or partner rents), live in a home rented by another and pay rent, or live in a home rented by another and pay no rent.

Other Variables

Mother’s characteristics include relationship status (married, cohabiting, single), race (non-Hispanic white, non-Hispanic black, Hispanic, other non-Hispanic race), education (less than high school, high school, some college, college or higher), foreign-born, household income-to-needs ratio (using the U.S. Census Bureau official poverty thresholds, adjusted by family composition and year), and whether the focal child is the first birth. Mother’s earnings, food stamps/Supplemental Nutrition Assistance Program, and private financial transfers (from relatives or friends) are reported in annual dollars. Receipt and annual amounts of public cash transfers include Temporary Assistance for Needy Families, Supplemental Security Income, and unemployment insurance/workers compensation.

To assess the economic value of doubling up, we estimate the yearly dollar value of the rent a mother saves by doubling up. Although there are other possible economic benefits (or costs) to doubling up, such as shared household expenses or childcare, this information is not available in the data, and thus we focus on rent. As outlined earlier, rent is ascertained by asking mothers how much they pay in rent, but it is not clear whether mothers report the full household rent or what they themselves pay in rent. Because of this ambiguity, we restrict our rental savings estimates to mothers who move in with others because it is much more likely that these mothers report the rent that they pay rather than that of the household.Footnote 1 Thus, we focus the estimated rental savings to doubling up on mothers who live in someone else’s household.

Using data on the rent paid by mothers who are not doubled up, we generate a predicted rent variable for the full sample of mothers for Waves 3–5, from which we have data on whether she lives in her own or someone else’s home. Our prediction equation includes basic demographic information, such as age, race, lagged measures of income, and city of residence. We then compare the actual rent that doubled-up mothers pay against their predicted rent to generate an estimate of the rental savings from doubling up. This estimate is equal to the difference between what mothers actually pay and what they would have paid in the absence of doubling up. About 90 % of mothers who are doubled up in someone else’s household have predicted rental savings greater than zero; that is, they would pay more than they currently pay if they were not doubled up. About 10 % of mothers have predicted savings less than zero; that is, they would pay less in rent if they were not doubled up. We include mothers with both positive and negative values because we believe that this approach provides a more conservative estimate of the value of doubling up. The value of doubling up is reported in annual dollars.

We also estimate the rental savings to doubling up in someone else’s home by looking at the same mother when she was doubled up and not doubled up and comparing her rental expenses in the two situations (for Waves 3–5). Because rental price is sensitive to the size of the household, we compare only those mothers who are in the same relationship status with the same number of children at the two points in time. For example, if a mother was doubled up at Year 3 but not doubled up at Year 5, we compare her rent payments at 3 and 5, provided that she has not had another child and has not changed relationship status. This individual-change method yields an alternative rental savings estimate.

Results

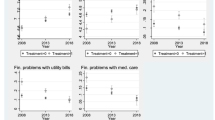

Doubling up is common among urban families with young children. As shown in Fig. 1, families are most likely to double up around the birth of a child (31 %), and doubling up declines substantially as children (and parents) age. Single mothers are the most likely to double up when their child is an infant (64 %), and they experience the sharpest decline over time. In contrast, married and cohabiting mothers are less likely to double up during infancy, but the decline over time is much less steep. Table 1 also provides weighted descriptive statistics on the prevalence of doubling up and the characteristics of mothers who double up by relationship status. Whereas 24 % of young children live in a doubled-up household at any point in time, nearly one-half (49 %) have lived in a doubled-up household at some point between birth and age 9. As before, single mothers are the most likely and married mothers are the least likely to have ever doubled up.

Percentage doubled up by child’s age and mother’s relationship status. Statistics are weighted using city weights. The sample is restricted to mothers who responded in all waves. All differences by relationship status are significant at p < .05 except (1) married versus cohabiting at the birth and age 3 and (2) single versus cohabiting at age 9

Differences in mother’s characteristics by doubled-up status are large. On average, mothers in doubled-up households are more likely than other mothers to be renters, pay lower rent, be younger, be Hispanic, have lower earnings, and have lower levels of education. Although average income is lower among doubled-up households, this difference is driven by married mothers; single and cohabiting mothers have similar incomes regardless of whether they are doubled up. Except for married mothers, mothers in doubled-up households are also more likely to be having their first birth. Last, although public cash transfers and food stamp receipt is slightly higher among doubled-up mothers overall, public cash transfers are lower among doubled-up cohabiting and single mothers.

Table 2 provides additional descriptive information on doubled-up households. Living with a parent (in-law) is the most common type of doubling up. Nearly two-thirds of doubled-up households include at least one parent. Doubling up with a sibling is also common (25 %), as is living with nonkin (22 %). Differences by relationship status reveal that cohabiters are significantly less likely to live with a parent and are significantly more likely to live with nonkin than are single or married mothers. Most doubled-up mothers live with only one additional adult (54 %), but 31 % live with two, 10 % live with three, and 5 % live with four or more additional adults. Patterns are similar by relationship status; however, married mothers are significantly more likely than single or cohabiting mothers to have only one additional adult in the household.

Transition patterns show that few households are stably doubled up over the nine-year period: only 8 % are always doubled up. Single mothers are significantly more likely to be stably doubled up (14 %), compared with cohabiting (7 %) or married (4 %) mothers. Married mothers are the least stable: 53 % have two or more transitions, compared with 48 % of cohabiting and 38 % of single mothers. Last, Table 2 shows the breakdown of doubled-up households by whether the mother is the householder (her name/partner’s name is on the lease/mortgage). More than one-half (56 %) of doubled-up mothers live in their own home, whereas 44 % live in someone else’s home. Differences by relationship status show that 76 % of doubled-up married mothers, 64 % of cohabiting, and 41 % of single mothers live in their own home. Overall, 16 % of doubled-up mothers own their own home, whereas only 5 % live in a home that is owned by another. Among doubled-up mothers, 41 % rent their home, whereas 39 % live in a household that is rented by another (28 % pay rent, and 11 % do not). Single mothers are more likely to live in a home rented by another (56 %), compared with cohabiting (35 %) or married (18 %) mothers.

In Table 3, we present estimates of the rental value of doubling up for mothers who live with others. The average savings is about $4,040 per year. Married mothers receive the largest rental savings ($5,350), followed by cohabiting ($4,670) and single mothers ($3,530). Table 3 also provides estimates of the rental savings based on comparing the same mother in different statuses (doubled up and not). Although these figures are estimated on a small subsample of mothers who changed statuses between Waves 3 and 5 (n = 143), they serve as a robustness check. On average, mothers who double up save about $4,640 per year. Differences by relationship status show a similar pattern as the predicted estimates: married mothers save the most ($5,665), followed by cohabiting mothers ($4,450) and then by single mothers ($2,780). The individual-change approach yields slightly lower average savings for single mothers and slightly higher savings for married mothers; however, the similarity in the findings between the two approaches give us more confidence in the predicted estimates.

As shown in Table 3, the rental savings to doubling up is worth more than one-fourth of mother’s yearly earnings ($15,000). Among mothers who receive public cash transfers (22 % of the sample), the average transfer is about $3,940 per year. For food stamps, the value among receivers (29 % of mothers) is about $2,700. Last, the value of private financial transfers among receivers (28 % of the mothers) is about $2,900 per year. Although the average savings to doubling up is larger than the average benefit of these other transfers, fewer mothers (11 % overall) are doubled up in someone else’s home than receive transfers. That said, many mothers who are doubled up in their own households (13 %), for whom we do not estimate rental savings, are likely to receive some economic benefit from doubling up.

Discussion

The goal of this research was to describe the prevalence of doubling up among families in large cities and to estimate the rental savings to mothers who were doubled up in someone else’s household. Doubling up is very common. On average, 24 % of mothers are doubled up at any survey wave, and nearly one-half of mothers are doubled up at some point during the first nine years of their child’s life. Doubling up with parents is most common, many families live with more than one additional nonnuclear adult, and transitions into and out of doubled-up households are frequent. Somewhat surprisingly, we find that many mothers (56 %) bring others into their homes.

Differences by relationship status show that single mothers are far more likely to double up than married or cohabiting mothers, although a substantial share of married mothers double up. Cohabiting mothers are more likely to live with nonkin than single or married mothers, which is consistent with research suggesting that kin were more willing to help single mothers and married-parent households than cohabiting families (Setlzer et al. 2012). As expected, single mothers are much less likely to bring others into their home (41 %) than married (76 %) or cohabiting (64 %) mothers.

The estimated rental savings to moving into someone else’s home is substantial. Average annual savings in rent is more than $4,000, suggesting that doubling up is an important and valuable safety net for low-income families. The estimated savings is largest for married mothers ($5,300), followed by cohabiting ($4,450) and single mothers ($3,500). This difference is in keeping with differences in rental costs; married and cohabiting mothers likely need larger homes (as their families contain more adults) and therefore pay more rent when they are not doubled up. For mothers who double up, the estimated economic value is greater than the value of food stamps and private cash transfers.

Note that we estimate only the rental saving associated with doubling up for mothers who move into someone else’s homes. Mothers who double up by receiving others into their home are also likely to receive an economic benefit. There are also many other potential economic benefits to doubling up (such as shared utilities or informal childcare) as well as non-economic benefits (such as emotional or parenting support) that are excluded from these estimates. There may also be excluded economic costs (such as additional food expenses) or non-economic costs (such as the loss of privacy or household crowding). Future studies that capture information on rent paid by boarders (for mothers who bring others into their home) as well as other household expenses and in-kind services (such as childcare) would make it possible to obtain a more comprehensive estimate of the value of doubling up.

This study has other limitations. First, the findings here are limited to families in large urban cities with young children. Second, the periodicity of the panel means we are missing spells of doubling up that occur between waves, and therefore our estimates are likely to understate the frequency of doubling up. Third, attrition may affect our findings. In general, mothers who attrite from the study are more economically disadvantaged and more likely to be Hispanic. Mothers who leave the sample are more likely to have doubled up, suggesting again that our estimates understate the prevalence of this transfer.

Despite these limitations, our research suggests that overall, doubling up serves as an important private safety net: it is used frequently and is economically valuable. Research and public policy need to consider the implications that these living arrangements have for the well-being of families with children.

Notes

Cross tabulations show that rent for mothers who bring others into their home is $8,200 per year versus $3,240 per year for mothers moving into someone else’s home.

References

Edin, K., & Lein, L. (1997). Making ends meet: How single mothers survive welfare and low-wage work. New York, NY: Russell Sage Press.

Hofferth, S. L. (1984). Kin networks, race, and family structure. Journal of Marriage and the Family, 46, 791–806.

Mykyta, L., & Macartney, S. (2012). Sharing a household: Household composition and economic well-being (Current Population Reports P60-242). Washington, DC: U.S. Census Bureau.

Schwartz, M., & Wilson, E. (2007). Who can afford to live in a home?: A look at data from the 2006 American Community Survey (Report). Washington, DC: U.S. Census Bureau.

Setlzer, J., Lau, C. Q., & Bianchi, S. (2012). Doubling up when times are tough: A study of obligations to share a home in response to economic hardship. Social Science Research, 41, 1307–1319.

Stack, C. (1974). All our kin: Strategies for survival in a black community. New York, NY: Basic Books.

Tienda, M., & Angel, R. (1982). Headship and household composition among blacks, Hispanics, and other whites. Social Forces, 61, 508–531.

Acknowledgments

The authors thank the Eunice Kennedy Shriver National Institute of Child Health and Human Development for supporting this research through Grant Nos. R01HD066054, R01HD036916, and R24HD058486; the Fragile Families Working group; and the anonymous reviewers for helpful feedback on earlier drafts.

Author information

Authors and Affiliations

Corresponding author

Rights and permissions

About this article

Cite this article

Pilkauskas, N.V., Garfinkel, I. & McLanahan, S.S. The Prevalence and Economic Value of Doubling Up. Demography 51, 1667–1676 (2014). https://doi.org/10.1007/s13524-014-0327-4

Published:

Issue Date:

DOI: https://doi.org/10.1007/s13524-014-0327-4