Abstract

Stock market plays a key role in economical and social organization of a country. Stock market forecasting is highly demanding and most challenging task for investors, professional analyst and researchers in the financial market due to highly noisy, nonparametric, volatile, complex, non-linear, dynamic and chaotic nature of stock price time series. Prediction of stock market is a crucial task and prominent research area in financial domain as investing in stock market involves higher risk. However with the development of computational intelligent methods it is possible to reduce most of the risk. In this survey paper, our focus is on application of computational intelligent approaches such as artificial neural network, fuzzy logic, genetic algorithms and other evolutionary techniques for stock market forecasting. This paper presents an up-to-date survey of existing literature on stock market forecasting based on computational intelligent methods. In this article, the selected papers are organized and discussed according to six main point of view: (1) the stock market analyzed and the related dataset, (2) the type of input variables investigated, (3) the pre-processing techniques used, (4) the feature selection techniques to choose effective variables, (5) the forecasting models to deal with the stock price forecasting problem and (6) performance metrics utilized to evaluate the models. The major contribution of this work is to provide the researcher and financial analyst a systematic approach for development of intelligent methodology to forecast stock market. This paper also presents the outlines of proposed work with the aim to enhance the performance of existing techniques.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

Stock market is an open market in which equity securities or shares of company are traded publically to raise money for research and development, introducing new products, entry into new markets, financial growth, acquiring competitors etc. A share is the part of ownership of company. Economics and social organization of a country are strongly linked and heavily affected by the performance of the stock market. Stock market play a crucial role in world economy as economic development of many countries is influenced by various financial activities [1]. The up side of stock market is that it gives higher profits than other financial market and down side of stock investment is that it involves higher risk but smart decision can reduce most of the risk. So prediction of stock market is an emerging task before investing into it. Stock price time series forecasting is highly demanding and most challenging tasks for the investors and professional analyst in the time series and computational intelligence literature [2]. Successful and accurate prediction of stock market would yield significant profit for investors.

There are numbers of approaches that are utilized for forecasting of stock market. These approaches have been categorized into four classes (1) fundamental analysis, (2) technical analysis, (3) traditional statistical methods, (4) soft computing methods. Fundamental analysis and Technical analysis are two most commonly used approaches for analyzing and forecasting stock market behavior [3]. In the former approach the investors focus on various metrics that reflect the health of the company before purchasing its stock. Fundamental analyst study various metrics like turnover, expenses, annual and quarterly reports, profit and loss, income statements, assets and liabilities, balance-sheet etc. The fundamental analysis is mostly favored by long-term investors. Technical analysis is based on the study of statistics generated by market itself. The technical analyst believes that stock price already comprises all the fundamentals that affect it and model the historical behavior of stock market as a time series. Analyzing the shape of financial time series allows the technical analyst to predict future behavior based on past behaviors of time series believing that history may repeat in future [4].

Stock market’s fluctuations are influenced by various macro-economical factors including economic condition of company or country, bank rate, currency exchange rate, commodity price, gold price, movement of other stock market, investors’ expectations, political events, companies’ policies, psychology of investors etc. [5,6,7]. In the past several years, many other different approaches have been suggested to forecast stock market and to provide intelligent decision making system. Two most commonly used approaches that are used to predict stock price time series are statistical methods and soft computing approaches [8]. Traditional statistical forecasting methods like, autoregressive moving average (ARMA), exponential smoothing (ES), autoregressive integrated moving average (ARIMA), autoregressive conditional heteroskedasticity (ARCH) and generalized autoregressive conditional heteroskedasticity (GARCH) predicts the future stock prices on the basis of past stock prices [9]. These models are based on the assumption that financial time series under investigation are generated from linear process [10] and attempt to model the time series process in order to forecast the future value of series. However stock time series data are highly noisy, non-linear, complex, dynamic, nonparametric, and chaotic in nature [11, 12]. Therefore, traditional statistical techniques cannot be used to model the complexity and non-stationary nature of stock markets. So, several soft computing techniques have been proposed and used for stock market trend forecasting. Artificial neural networks (ANNs) and support vector machines (SVMs) are the extensively used algorithms among these techniques [13, 14].

The aim of this work is to review the recent computational intelligence approaches applied to solve stock market forecasting problem. This study is useful for guiding research scholar, investors and financial analyst for building an intelligent stock market forecasting methodology.

2 Previous Related Work

We started the survey by reviewing the existing literature by different authors that provided the review of relevance of computational intelligence techniques in financial market problems.

Atsalakis and Valavanis [15] have surveyed scientific articles that make use of neural and neuro-fuzzy techniques to solve stock market forecasting problem. In that study, each article was discussed with respect to five key perspectives (1) the stock market surveyed, (2) the input variables investigated in each model, (3) techniques and parameters utilized to build the prediction model, (4)different model comparisons, and (5) the performance measures used to measure accuracy of each model. Although this article provides the valuable contribution in organizing the literature in stock market forecasting using soft computing techniques but it is limited to particular class of soft computing. In contrast, our study investigate several area of computational intelligence applied in stock market forecasting. Primary studies from 2009 to 2015 examined by Cavalcante et al. [16], which illustrate the use of computational intelligence techniques in financial market. In this article the selected primary studies has been classified into five main aspects (1) application of soft computing in financial market, (2) the financial market examined, (3) the input variables used, (4) the intelligent trading system proposed and (5) whether the work discussed helps in development of trading system. They investigated the major financial problems such as forecasting of stock price, commodity price, exchange rate, electricity prices, and financial distress prediction among others. The other main contribution of this work was presentation of basic concepts mainly fundamental and technical analysis, pre-processing techniques, traditional statistical and soft computing approaches used for solving financial problem, and challenges and future scope of the related research. Although this survey covers the wide area of computational intelligence and financial market but it is relatively old and many advances have been made since 2016. Hence, our work presents an up-to-date survey of recent article in computational intelligence and stock market forecasting domain. Also some primary studies that have applied text mining approaches to extract qualitative information about companies and use these mined knowledge to predict the future behavior of stock prices based on the quality of the companies’ news are presented by Nikfarjam et al. [17]. A comparative analysis of various text mining approaches proposed in this article also discussed according to some characteristics of the primary studies: (1) the feature selection methods, (2) the feature representation approach, (3) the news source utilized, (4) the classification techniques applied, (5) the number of categories or target classes and (6) the directional accuracy. Our study also includes various text mining approaches for forecasting stock market but we provide the latest discussion in contract to this literature survey. Li and Ma [18] have reviewed the application of artificial neural networks in different financial markets. They examined some primary research work that implement ANN to forecast the future value of exchange rates, stock market, and forecasting of banking and financial crisis. In that short article, authors have provided no details of which ANN architectures or learning algorithms were used in the surveyed literature and have limited scope as they investigated only one class of class of computational intelligence. In contract, our survey has broader scope. Rivera et al. [19] presented the survey of application of evolutionary computation approaches to solve various financial problems. The evolutionary techniques based on Darwinian approach such as Genetic Programming (GP), Learning Classifier Systems (LCSs), Genetic Algorithm (GA), Multi-Objective Evolutionary algorithms (MOEAs), Co-evolutionary optimization scheme and competent evolutionary algorithm have been considered in this article. This review is more restricted to Darwinian approaches, since it has presented few evolutionary methods. Our study has a broader scope as we have discussed most of the nature inspired optimization techniques used in literature. Agrawal et al. [20] surveyed the existing techniques for forecasting of Indian stock market and discussed the related parameters, various advantages and limitations of these methods. In this article, authors have provided the brief introduction of fundamental and technical analysis used for stock market forecasting. Kumar and Ravi [21] reviewed research articles from 2000 to 2016 which deals with application of text mining in financial domain and highlight some of the issues, research gaps, key challenges in financial domain and future direction in related field. Soni [22] also reviewed the use of ANNs in stock market prediction. In this article author has provided the brief introduction of ANN and discussed the importance of ANN in prediction. Before presenting the survey of previous studies that use ANNs to solve the stock market prediction problem, author has presented some basic concepts of stock market.

3 Basics Terminology of Stock Market and Computational Intelligence (CI)

This section presents the basic terminologies of stock market like what is stock market, Stock exchange, stock index, stock market forecasting and computational intelligence approaches that will act as foundation for the remainder of this article.

-

1.

Stock Market Stock market also called as equity market or share market is a publicly owned market for selling and buying the shares of company that issues them at an agreed price [22]. Selling and buying of shares is known as trading. A share is a portion of ownership of company and a stock is collection of shares. By owning a share means that one can share the part of company’s profit and loss. A stock is a type of security which is a financial instrument that has some monetary value and can be purchased or traded [23]. Securities may be private or public. If only selected individual can invest in stock it is known as private securities and if anyone can invest in them it is known as public securities. Individuals who invest in stock market must follow the rules and regulations of regulatory body that govern investors and investment. In India the rules for publicly traded securities are set and enforced by the Securities and Exchange Board of India (SEBI). It is the duty of the SEBI to ensure that investors are dealt fairly and that all investments have done honestly and inside the market there is no illegal dealing. Prices of share depend on supply and demand. If a stock have high demand, its price will increase, whereas stock that have low demand or heavily sold results in decrease in price. Companies that are allowed to trade in stock market are called listed companies [24].

-

2.

Stock Exchange A stock exchange is a place where shares of firm are traded. Stock exchange provides a marketplace which can be a corporation or mutual organization where stocks or other securities are traded by members of organization [22]. Shares are directly supplied by company through Initial Public Offer (IPO) or can be bought from stock exchange. Most of the world’s largest economic powers have their own stock exchanges. The New York Stock Exchange (NYSE) and NASDAQ are the two world’s largest stock exchanges. In India, there are 21 stock exchanges. Bombay Stock Exchange (BSE) and National Stock Exchange (NSE) are the two largest Indian stock exchanges. To trade the shares of company on certain stock exchanges, it has to be listed on particular stock exchange [24].

-

3.

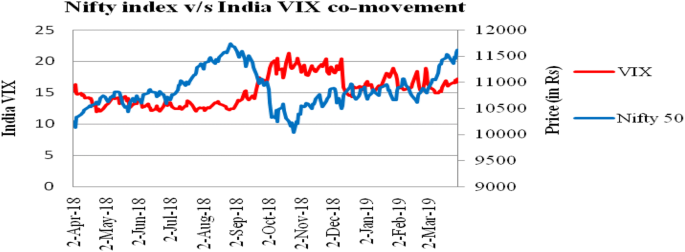

Stock Index An index is a statistical measure of performance of group of companies. An index Company choose a limited number of stocks of company that represent the performance of entire market, or particular sector within the market and average their performance to find a number that investors can use to analyze the performance of the market, or compare it with other stocks [23]. Dow Jones Industrial Average (DJIA), the Standard & Poor’s 500 (S&P 500) and the NASDAQ Composite are the three major stock indexes of US. Just like individual company stock, each stock index has its own chart which shows the opening price, closing price, low price, high price, average volume and number of shares traded. S&P BSE Sensex and Nifty 50 are two major stock indices of BSE and NSE respectively of Indian stock market. Instead of stock market index, another popular index given by Chicago Board Options Exchange (CBOE) known as Cboe market volatility index (VIX index) is an indicator of market’s expectations of future volatility in US equity market [25]. It is based on options of S&P 500 index and is considered as measure of global US stock market [25]. Volatility is a measure of frequency and magnitude of price movement both up-side and down-side, of financial instrument over given interval of time. The VIX index is recognized as investors fear gauze as low VIX readings indicates that investors are confident about future market rather than fearful and high VIX values implies that investors recognized higher risk and perceive that market would fluctuate frequently in either directions [26]. National stock exchange of India (NSE) offers its own volatility index based on Nifty index option pricing namely India VIX (INDIAVIX or Nifty VIX) which gauze the expected market volatility of Nifty 50 over next 30-days. Figure 1 shows the co-movement of Nifty 50 index and India VIX for period of one financial year from 2 April, 2018 to 29 March, 2019.

Fig. 1

Nifty 50 and India volatility index co-movement chart

-

4.

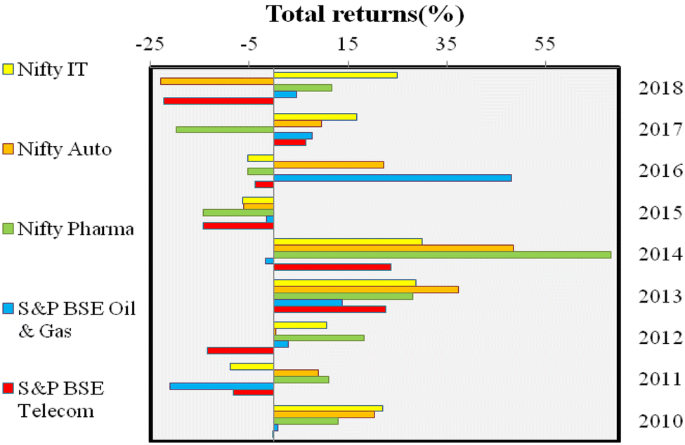

Kinds of stock There are numerous ways to classify stocks into different classes but usually stocks are classified by sector, and by market cap. In sector investing, investors buy stock in one industry, known as sector. For example some might invest in healthcare companies or IT sector, automobile sector, telecom sector and many others. In market cap investing stocks are classified according to company size by using formula called market capitalization (market cap) which is given by multiplying Current price of a single share and number of shares available on the market. Companies are classified according to their market cap by using different figures but the rule of thumb is: $50 million or less: nano cap, $50 million to $300 million: micro cap, $300 million to $2 billion: small cap, $2 billion to $10 billion: mid cap, $10 billion or more: large cap (also known as blue chip) [23]. Figures 2 and 3 depicts the 9 year performance comparison of three sectors of NSE and two sectors of BSE of Indian stock market. Sector indices capture the performance of companies that are listed in particular index. The Nifty IT index gauzes the performance of Indian IT companies such as TCS Ltd., Wipro Ltd., Infosys Ltd. etc. and S&P BSE oil and Gas index is designed to measure the performance of oil and gas companies of India such as ONGC, GAIL, Petronet LNG etc. Total return is the amount of profit in percentage, earns by investors from a security over certain period of time and it is a strong measure for analyzing the historical performance of companies [27]. Average daily return is the average amount an investor earns daily over specific period of time [28].

Fig. 2

Performance comparison of sector indices based on total returns

Fig. 3

Performance comparison of sector indices based on average daily returns

-

5.

Stock Market Forecasting Stock market forecasting is the process of predicting the future prices of stock market on the basis of previous historical data. Stock price time series is generally used for prediction task. Predicting stock market is an emerging task for investors, professional analyst and researchers as investing in stock market involve higher risk.

-

6.

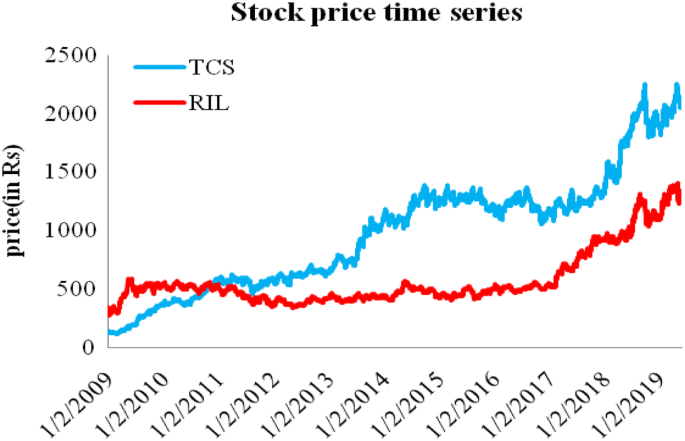

Time Series A time series is a set of observations generally collected at successive point of time such as: xt = {xt ∈ R|t = 1, 2, 3… N} where t is temporal index and N is the total number of observations and these observations are recorded at regular time interval such as daily, monthly, quarterly, and annually [29]. Figure 4 shows the stock price time series of closing price of two Indian companies namely Tata Consultancy Services Ltd. (TCS) and Reliance Industries Ltd. (RIL) for period of 10 years. Time series are usually plotted by line charts. Examples of time series are stock price, gold price, currency exchange rate, commodity price, oil price, monthly sale of company, population of country measured at regular point of time etc. Time series are used in diverse application such as econometrics, weather forecasting, signal processing, control engineering, earthquake prediction, pattern recognition, statistics, stock market prediction and other financial market prediction [30]. The main aim of time series forecasting techniques is to forecast the future values of the series on the basis of regular pattern present in past observations of the series itself.

Fig. 4

Indian companies stock price time series

-

7.

Fundamental Analysis Fundamental analysis is performed on the basis of economic data of companies and it involves forecasting stock markets using economic data of companies this is published at regular period of time for example price to earnings (P/E) ratio, turnover of company, profit and loss, annual and quarterly reports, assets and liabilities, balance sheet, income statements [3, 31]. It simply involves analyzing the performance of company based on certain fundamentals of company.

-

8.

Technical Analysis Technical analysis is in accordance with the time series data and it involves forecasting stock market using charts or technical indicators [3, 31]. It relies on the hypothesis that all information about the market is present in real time stock prices. Technical analysts use charts and modeling techniques to determine trends in stock price and it depends on previous data in order to predict future stock prices. It involves forecasting of the future stock price on the basis of past patterns of the stock through time-series analysis [32].

-

9.

Computational Intelligence (CI) It is collection of techniques that are applied to imitate the human thinking power in order to deal with complex problems of real world [33]. The taxonomy of CI is given in Fig. 5. Fuzzy logic, neural networks, genetic algorithms and other evolutionary computing techniques are collectively used in CI for representing knowledge and for simulating the decision-making and reasoning capability of human [34]. CI techniques have been applied in many applications such as pattern recognition [35], communications [36], heavy current system [37], intelligent speech recognition system [38], signal processing area [39], design and manufacturing [40], prediction and forecasting [14] and many diverse applications.

-

9.1

Artificial Neural Networks (ANNs) ANNs are massively parallel distributed system inspired by human brain [41]. It is a network of units known as artificial neuron that have a capability of processing and storing experiment knowledge. ANN imitate the human brain in two aspects (1) knowledge learned by the network using past experience(historical data) through learning process and (2) strength(synaptic weight) of connection between neurons is used to store the acquired knowledge. It is a connectionist model consists of three layers (1) input layer (2) hidden layer (3) output layer. Input is transmitted between layers by means of connection links. Each links posses an associated weight (connection strength) which is multiplied with the input coming from input layer to compute the net input (sum of all inputs at particular node). The net input is provided to the activation function to produce the output of the network. Connection models such as ANN are well suited for soft computing where connection weights are optimized to improve the performance of a network. Backpropagation algorithm (BP) is mostly used in artificial neural network to train the network [42, 43].

-

9.2

Fuzzy Logic Fuzzy Logic (FL) is an expansion of classical set theory and was proposed by Lotfi A. Zadeh and Dieter Klaua in 1965. Fuzzy logic is a method of representing human knowledge that is imprecise in nature in a particular area of application and in reasoning with that knowledge to take useful decision or make inferences [34, 44]. Fuzzy logic provides computational power to CI. In fuzzy logic, the knowledge is represented through if–then rules involving linguistic variables. Figure 6 shows the basic architecture of fuzzy logic system. The fuzzification interface translates the crisp input data into fuzzy linguistic data. In fuzzy logic system, fuzzification is necessary because existing data sources provide input in the form of crisp values. The inference engine uses the fuzzy input and fuzzy rules to generate fuzzy output. The defuzzification interface produces the crisp output action [33].

Fig. 5

Core CI approaches for stock market forecasting

Fig. 6

Basic architecture of fuzzy logic system [33]

-

9.3

Genetic Algorithm GA was invented by John Holland in the 1960s [34]. GA is derivative-free, parallel, adaptive and dynamic optimization method, which is inspired by biological evolution [33, 45]. It belongs to class of evolutionary computing. Evolutionary computing has the three main properties [34]: (1) it is population based stochastic search techniques as it is based on multiple searching points (2) it uses biological operations such as crossover and mutation to generate optimal solution (3) it is based on probabilistic operations. The basic process of genetic algorithm involves following steps:

-

1.

Initialization, where searching start with initial population which is created randomly.

-

2.

Evaluation, where each elements of population is evaluated and fitness of the members are computed using fitness function.

-

3.

Selection, where the members that fit the desired requirement are selected based on value of the fitness function.

-

4.

Crossover, where new generation known as offspring is generated by combining the best of the existing parents [46].

-

5.

Mutation, where a single bit within individual is changed to keep the diversity of population [46].

-

6.

In the next step, next generation is produced by changing the current population by newly generated off-springs.

-

1.

-

9.1

The process of evaluation–selection–reproduction is repeated until an optimal solution or near optimal solution is obtained or termination condition is satisfied.

4 Forecasting Work Flow

Stock market forecasting is an important research area. Developing an intelligent system that can forecast stock price is an emerging area of research for investors and financial analyst. Figure 7 depicts the generalized workflow for stock market forecasting adopted by different authors in the literature reviewed. Each chosen article is organized and investigated according to five main categories as shown below.

Generalized framework for stock market forecasting

A Systematic approach for forecasting the stock market comprised of following operational steps (1) selection of input variables, (2) data pre-processing, (3) feature selection and extraction, (4) training using prediction/classification model and (5) evaluating proposed model performance. The first step in forecasting process of stock market consists of selection of input features to be modeled by CI methods and output to be predicted. In the context of stock market forecasting various fundamental and technical input variables are available. Selection of input variables is main issue in the stock market forecasting and decision of which input variables to be used is not an easy task. Next step in the process is pre-processing of data selected in first step. Data is preprocessed in order to increase the prediction capability of models. Preprocessing mechanism can be used for noise removal, outlier detection, dealing with missing value and normalizing data. In the third phase, various feature selection or extraction techniques are applied to get the best representative variables of input data in order to reduce the dimensions of input data and reducing computational complexity of the model. In the next phase consists of determining the CI methods to be used for forecasting and training the model using training data. The last phase performance evaluation comprises selection of appropriate performance metrics and measuring the accuracy of model and taking the right decision. In this article each selected paper has been discussed according to generalized framework for stock market forecasting.

4.1 Stock Market Surveyed

In this section we have presented list of various stock market authors have investigated and acquired data for evaluating the performance of their models along with corresponding stock exchange, stock index and sources of dataset as shown in Table 1. Reza et al. [47], Thakur et al. [48] and Wang and Wang [49] model DAX index of German stock market traded in Frankfurt stock exchange. Lu [50], Thakur et al. [48], Asadi et al. [51], Chang and Liu [52] and Esfahanipour and Aghamiri [53] has taken TAIEX stock index of Taiwan of stock exchange for case study. Dai et al. [54], Qiu and Song [55], Qiu et al. [56], Liu et al. [57], Cheng and Yang [58] and Lei [59] attempted to predict NIKKEI 225 index of Tokyo stock exchange. Kara et al. [60], Boyacioglu and Avci [61] and Yolcu and Lam [62] studied the ISE national index of Turkey stock exchange. The BSE Sensex and Nifty 50 indices of Indian stock market are forecasted by Thakur et al. [48], Patel et al. [63], Pathak and Shetty [64], Senapati et al. [65], Chopra et al. [66], Rather et al. [67], Patel et al. [68], Dash and Dash [69, 70], Rout et al. [71], Pradeepkumar and Ravi [72], Pal and Kar [73] and Rajab and Sharma [74]. The DJIA S&P 500, IXIC and SPDR S&P 500 indices of New York stock exchange (NYSE) and NASDAQ of USA market are most common studied indices among the studies surveyed in this article by Niall and Madden [75], Asadi et al. [51], Wang and Wang [76], Liu and Wang [77], Chien and Chen [78], Zhang and Wu [79], Niaki and Hoseinzade [80], Hu et al. [81], Kazem et al. [82], Chien and Chen [83], Zhong and Enke [84], Chiang et al. [85], Liu et al. [57], Dash and Dash [69, 70], Sheta et al. [86], Sadaei et al. [87], Jiang et al. [88], Chang et al. [89], Rout et al. [71], Fischer and Krauss [90], Nayak et al. [91], Pradeepkumar and Ravi [72], Xiong et al. [92], Wang and Wang [49], Seo et al. [93], Lei [59], Rajab and Sharma [74] and Zhou et al. [94]. de Oliveira et al. [95] and Brasileiro et al. [96] examined Petrobras stock PETR4, traded in BM&FBOVESPA for case study. Asadi et al. [51], Esfahanipour and Aghamiri [53], Hadavandi et al. [97], Rezaee et al. [98] and Ghasemieh et al. [99] forecasted Tehran stock exchange. The major indices of China stock market are forecasted by Dai et al. [54], Wang and Wang [76], Liu and Wang [77], Wang et al. [100], Pang et al. [101], Tan et al. [102], Mo et al. [103], Pal and Kar [73], Lei [59], Yang et al. [104], and Zhou et al. [94]. Vanstone et al. [105] and Lei [59] predicted the ASX200 index of Australian stock market. Pullido et al. [106] have performed the prediction of Mexican stock exchange time series of Mexico stock market. Inthachot et al. [107, 107] attempt to predict the trend in SET50 index of Thailand stock exchange. Gocken et al. [108] model the BIST100 index of Turkish stock market. Wang et al. [100], Kim et al. [109] and Chung and Shin [110] attempt to forecast the Korean stock market. The Financial times stock exchange (FTSE) index of London stock market is forecasted by Nayak et al. [91] and Wang and Wang [49]. From south central European country Croatia’s Zagreb stock exchange was examined by Svalina et al. [111]. The Athens stock exchange (ASE) general index of Greece was studied by Chouemouziadis et al. [112].

Table 2 includes the articles that focus on forecasting of price of individual stocks instead of particular stock market indices. Ticknor [121] and Chang et al. [89] shows the ability of network to predict the major stocks of US. Mabu et al. [122] selected 16 main companies with high market capitalization from Tokyo stock exchange in Japan. Fazel et al. [123] evaluated the capability of proposed model by applying it on daily stock price data collected from IBM and Dell Corporation of IT sector and British airways and Ryanair of airline sector. Pang et al. [101] predicted the stock price of Petroleum and Chemical Corporation of China stock market. Xiong et al. [92], Shynkevich et al. [124], Laboissiere et al. [125], Pimenta et al. [126], Weng et al. [127], Gocken et al. [128], Zhang et al. [129], Shah et al. [130] and Chander [131] attempted to predict stock prices of varying number of companies instead of stock indices.

4.2 Input Variables

The first stage in stock market forecasting is selection of input variables. In the literature different authors have utilized varying number of input variables. Two most common types of features that are widely used for predicting stock market are fundamental indicators and technical indicators. Benjamin Graham used the fundamental analysis in 1928 and mentioned that investors have to analyze various fundamental factor of a firm before investing into it, like size of company, assets, liabilities, profit, loss, price-earnings ratio, capitalization, turnover, annual reports and other financial factors that reflect the overall health of company [132]. Technical analysis does not depend on the intrinsic and extrinsic fundamental attributes of the company in the field of stock market forecasting. According to technical analyst most of the fundamentals that affect the stock market are reflected in the stock price itself [4]. Technical analyst model stock prices as time series and try to identify future patterns on the basis of past values of time series. Teixeira et al. [133] used technical indicators which are determined by applying mathematical formulas to stock prices such as open price, close price, low price and high price and try to find future stock prices. Tsinaslanidis and Kugiumtzis [134] used various technical indicators viz. moving averages, relative strength index, momentum, rate of change, on balance volume, directional movement indicators among others factors for stock market prediction. Table 1 summarizes the input variable used by various authors in their article along with period and number of instances of dataset. Articles in Table 1 have been divided into various classes. The first class includes articles that utilize stock prices as input data, the second class focuses on articles that use stock prices and volume of shares traded. Third category comprises papers that use stock prices with Google trends, fourth category includes articles that use fundamentals indicators as input, fifth category consists of articles that use technical indicators as input variables, sixth category of articles use technical indicators with stock prices and last category includes articles that use both, fundamental and technical indicators. Wang and Wang [76], Kazem et al. [82], Senapati et al. [65], Yolchu and Lam [62] and Zhou et al. [94] used the daily stock price such as open price, high price, close price and low prices as input variables for proposed prediction model. The price at which a share is traded upon the opening of a stock exchange on a given trading day is known as open price. The closing price is the last price at which a share is traded on the closing of an exchange on a given trading day. High and Low prices are the daily highest and lowest price at which a share is traded on a specific trading day. Reza et al. [47] have used quarterly data for period of 40 years from April, 1972 to July, 2012 containing 163 instances. Lu [50] have used daily data for a period from Jan 2,2003 to Feb 27,2006 for TAIEX index comprising 781instances and Feb 2,2004–Feb 29,2008 for NIKKEI index containing 1000 instances Liu and Wang [77] and Chander [131] have selected open, close, high, low prices and volume of share traded as input to the model. Hu et al. [81] and Zhou et al. [94] utilized Google trend with and without open price, high price, closing price and lowest price and volume of share traded to develop prediction model.

Figure 8 shows the OHLC (open-high-low-close) chart of S&P BSE sensex for period of one financial year from April 2018 to March 2019 and depicts the movement in stock price over given time period. In OHLC chart, open-high-low-close prices are represented by two types of bar namely up-bar and down-bar. Each bar comprises of two horizontal lines and one vertical line. The bottom and top value in up-bar represent lowest and highest stock price and lowest and upper horizontal line represent daily opening and closing price on a given trading day and in down-bar, close price is lower than high price.

Open-high-low-close price of S&P BSE Sensex index

Vanstone et al. [105] have applied four fundamental indicators namely price earnings ratio (P/E), dividend payout ratio return on equity (ROE) and book value for forecasting of Australian stock market. Boyacioglu and Avci [61] used 6 macro-economic factors such as consumer price index, interest rates on deposits, US Dollar exchange rates, industrial production index, republic gold selling price, interest rates on Treasury bill and closing price of 4 indices namely DJI, ISE National 100. DAX and BOVESPA and Niaki and Hoseinzade [80] have used 27 economical and financial factors as input and select 20 factors that have considerable effect on movement of S&P 500 index. Rezaee et al. [98] used 7 fundamental variables belongs to Tehran stock exchange market such as total debt by total assets (TDTA), cash flow divided by total assets (CFTA), current liabilities divided by total assets (CLTA), working capital divided by total assets (WCTA), earnings before interest and taxes divided by total assets (EBTA) and net income divided by total assets (NITA), current assets divided by total assets (CATA) as input for the proposed prediction model for six consecutive years. Qiu et al. [56] have used 71 financial and macroeconomic indicators to develop a prediction model of Nikkei 225 index. The entire dataset comprises 237 monthly observations for a period from November 1993 to July 2013. Kara et al. [60] use 10 technical indicators viz. Simple 10-day moving average, Momentum, weighted 10-day moving average, Stochastic K%, Relative strength index (RSI), Stochastic D%, Moving average convergence divergence (MACD), A/D (Accumulation/Distribution) Oscillator, Larry William R%, and CCI (Commodity Channel Index) for a period of 11 years containing 2733 working days. Thakur et al. [48] have used a combination of fifty-five technical indicators as input variables to forecast the future movement of stock indices over the period from January 2008 to December 2013. Niall and Madden [75] investigated the capability of using external indicators like commodity prices and currency exchange rates with other technical indicators to foresee the movements in the Dow Jones Industrial Average (DJIA) index. Patel et al. [63] and Zhang and Wu [79] have chosen ten technical indicators as inputs to the proposed prediction models. Bisoi and Dash [135] in the proposed model used normalized data of four stocks for a period from 3rd Jan 2005 to 13th August 2008. Dai et al. [54] have applied four indicators such as low price, close price, previous day’s cash market high, and today’s opening cash index for forecasting Nikkei 225 closing index and B-share stock index’s closing price. Ticknor [121] have used 6 technical indicators namely 5 day and 10 day exponential moving average (EMA), stochastic K%, Stochastic D% relative strength index (RSI) and William R%, along with three daily stock prices namely open, high and low prices for a period of 2 years comprising 734 instances. Chien and Chen et al. [78] make use of 10 technical indicators including Moving Average (MA), Relative Strength Index (RSI), Stochastic Oscillator (K, D), Williams Overbought/Oversold Index (WILLIAM%R), Moving Averages Convergence and Divergence (MACD), Directional Movement Index (DMI), Commodity Channel Index (CCI), Rate of Change (ROC), and Average Directional Movement Index (ADX). Qiu and Song [55] performed the comparison of two types of input variables named as Type I and Type II to predict the movement of stock market index. Type I input comprised of 12 technical indicators and Type II input consists of 9 technical indicators. Experiment results show that Type II inputs variables generates higher prediction accuracy as compared to Type I input variables. In this article, authors have suggested that it is possible to enhance the accuracy of prediction model by choosing the appropriate input variables. Inthachot et al. [107] utilized 11 technical indicators for finding 44 input variables, where each technical indicator is represented by 4 different indicators on the basis of past 4 time spans as 3, 5, 10 and 15 days. Bisio and Dash [135], Chiang et al. [85], Cheng and Yang [58] and Chung and Shin [110] used technical indicators along with stock prices. Reza et al. [47], Niall and Madden [75], Zarandi et al. [136] and Weng et al. [127] employed both fundamental and technical indicators to provide the inputs to the model. de Oliveira et al. [95] have combined technical analysis, analysis of time series and fundamental analysis and to predict price and use monthly observations of PETR4 index containing a total of 144 observations (Table 3).

In this survey work, it is depicted that authors have used different types of input variables for prediction models. Figure 9 shows the distribution of different input variables used in the surveyed articles. Among various input variables, technical indicators are found to be used most often, followed by stock prices, fundamental indicators, technical indicators and stock prices, combination of technical and fundamental indicators and stock prices with volume and Google trends.

Input variables used in surveyed articles

4.3 Data Pre-processing

In stock market prediction quality of data is main factor because accuracy and reliability of prediction model depends upon the quality of data. In many soft computing applications real world data prone to be incomplete, noisy and contains outliers [138]. Any unwanted anomalies in the dataset are known as noise. Outliers are the set of observations that does not obey the general behavior of dataset [139]. Presence of noise and outliers may results in poor prediction accuracy of forecasting models. The data must be prepared such that it covers the range of inputs for which the network is going to be used. Data pre-processing techniques attempt to reduce error and removing outlier, hence improving the accuracy of prediction models. One of the data pre-processing techniques is data transformation. Transformation of data from one scale to another is useful in most heuristic approach especially when solving prediction problems [140]. Transformation or mapping of data from one scale to another is known as data normalization. It is necessary to retransform the pre-processed data to original scale for obtaining actual results using post-processing techniques [51]. In the literature, authors have used various kinds of normalization techniques for transforming data from one scale to another. Reza et al. [47] authors have used various data preprocessing techniques like min–max normalization for normalizing data and three statistical based information criteria(IC) such as Bayesian information criteria (BIC), Schwarz Bayesian information criteria(SBIC) and Akaike information criteria (AIC) for lag selection because stock market feature show their effects with lag of time. Lu [50] presented an integrated independent component analysis (ICA) to remove noise contained in dataset. The output of ICA containing less noise is used as input of backpropagation neural network (BPN) to create forecasting model. Asadi et al. [51] and Hadavandi et al. [97] have used Min–Max normalization for mapping the data in the range [− 9, 0.9]. Normalization of data in neural network is necessary to avoid learning of irrelevant pattern in data [51]. If the input to artificial neural network (ANN) is not scaled in small range, then the network may not give useful results or cannot converge on training [141]. Dai et al. [54] original time series is processed by the logarithmic data smoothing technique for removing noise. Wang and Wang [76], Liu and Wang [77], Qiu et al. [56], Senapati et al. [65], Chopra et al. [66], Wang et al. [100], Chiang et al. [85], Dash and Dash [69, 70], Pang et al. [101], Chang et al. [89], Rout et al. [71], Wang and Wang [49], Chung and Shin [110] and Chander [131] in order to minimize the impact of noise in stock market data and to increase the accuracy, have normalized original dataset in the interval [0, 1] using Min–Max normalization techniques. Wang et al. [8] suggested hybrid forecasting model called Wavelet De-noising-based Back Propagation (WDBP) by combining wavelet transform (WT) for removing noise as pre-processing step and back propagation neural network (BPNN). WT is a technique for removing noise from dataset before training the model. In this study WT decompose the closing price time series into low frequency component and high frequency component. The high frequency component has been discarded as it represents noise and low frequency component is used as input to WDBP for predicting future stock price. Hu et al. [81] and Inthachot et al. [107] mapped original dataset into interval [− 1 1] using min–max normalization techniques. Kazem et al. [82] in the preprocessing phase of their study, firstly applied mutual information (MI) function is utilized to identify the time delay constant, secondly, false nearest neighbors (FNN) is used to find out minimum embedding dimension and then using the best time delay and embedding dimension they reconstruct the time series phase space to show its hidden dynamics and at last they applied min–max normalization technique to transform the data in the range [0 1]. Zhong and Enke [84] presented the stock price time series forecasting model by employing three dimensionality reduction techniques namely principal component analysis (PCA), kernel-based principal component analysis (KPCA) and fuzzy robust principal component analysis (FRPCA) with artificial neural network (ANN). In this article, authors first preprocessed the raw data to handle missing values, mismatched samples and outliers. They used the average of existing values on both sides of Table’s cell consisting of missing values to fill missing values. To deal with outliers, authors have defined an interval and a value that lies outside the interval is regarded as outlier. In that study, from 60 financial and economic factors, 36 most influential and correlated variables are selected by three version of PCM. Chiang et al. [85] used wavelet transformation to smoothed stock prices and volume of stock before providing data to proposed model. Wavelets are useful techniques for mining information from different types of data. Zarandi et al. [123] applied self-organizing map neural network method as a preprocess step for forming cluster of input data. Ghasemieh et al. [99] used two normalizing methods namely linear normalization and stochastic normalization to map data in the interval [− 1 1]. Nayak et al. [91] and Gocken et al. [128] applied sigmoid function to normalize the data in the interval [0 1]. Pimenta et al. [126] employed locally weighted scatterplot smoothing (LOWESS) mechanism to detect and remove outliers from stock market dataset. According to him, outliers in stock price time series are the observations which show abnormal variations of the stock price that indicates the presence of extrinsic factor which could not be modeled without the availability of restricted information and these outliers need to be removed as these observations can lead to serious problem in training phase.

4.4 Feature Selection and Extraction

Feature selection simply means choosing important features and discarding irrelevant ones. Feature selection is applied to choose best optimized features and it is the key issue in stock market forecasting task [142]. The emphasis of feature selection approaches is to choose subset of features from the input dataset which can effectively represent the input data while minimizing the impacts of noise or irrelevant variables and still produce good prediction results and minimizing computational complexity such as running time [143]. Selection of irrelevant and incorrect feature can result in model which cannot predict the real behavior of stock market. Feature selection algorithms determine a reduced set of important features that can be used as input in prediction model for minimizing the error and selected features are best representatives of data [51]. These methods results in lower accuracy and involves higher computational scalability.

Feature extraction method which is different from feature selection method involve mapping from original higher dimensional feature space to lower dimensional feature set which is more informative with respect to the task performed [144]. The advantage of feature extraction techniques is that hidden information in the original dataset can be retrieved. Based on the operation both method, feature selection and feature extraction method are classified into filter method and wrapper method [142]. According to Lee [143] filter methods are those which accomplish the selection of key variables independent of any classification or regression method. These methods simply analyze the input data on the basis of some statistics and determine some key features. On the other hand wrapper methods depends on accuracy measure of given soft computing method and involves high computational costs but perform better [145]. Correlation, F-score, stepwise regression, principal component analysis (PCA) and many others have been utilized in literature to select optimum set of features.

Lee [143] developed a hybrid feature selection approach by combing filter and wrapper methods to forecast stock market trend in two stages. In the first stage they used F-score statistics as filter to determine the optimum subset from given set of features. In the second stage, they applied support vector machine (SVM) classification technique as wrapper prediction method to generate set of key features. Kao et al. [146] developed a stock price prediction approach by applying non-linear independent component analysis (NLICA) for extracting key features known as independent components (IC) from input dataset and using extracted IC as input to support vector regression (SVR). NLICA is a feature extraction method which is based on the assumption that data are nonlinear aggregation of latent source signal and is used to find independent component which contains hidden information and is more suitable for stock price forecasting. Reza et al. [47] have used cross correlation feature selection technique for choosing important features from 20 features and select 13 features that are appropriate for predicting stock market. Thakur et al. [48] proposed four hybrid prediction models by combining four different feature selection approaches for selecting optimal set of indicators such as Linear Correlation (LC), Regression Relief (RR). Rank Correlation (RC) and Random Forest (RF), with proximal support vector machine (PSVM) classifier for trend (bullish or bearish) forecasting in stock market. They evaluated the performance of the proposed model for 12 different stock indices, on the basis of certain number of performance metrics. The performance obtained on a set of stock market indices from several international markets demonstrate that all hybrid models show good performance than the individual PSVM prediction technique. The comparison among the proposed models shows RF-PSVM outperforms all other prediction approaches. The highest accuracy on S&P BSE Sensex dataset is achieved when 48 technical indicators are selected. de Oliveira et al. [95] developed a neural network model for the prediction of stock’s close price future behavior. They have conducted the market analysis to find the parameters that governs the stock market and found 46 total variables and performs the cross-correlation of all the variables with closing price to find the optimized subset of variables containing 18 variables. Asadi et al. [51], Esfahanipour and Aghamiri [53], Hadavandi et al. [147, 97], Hsieh et al. [148] and Chang et al. [89] employed stepwise regression analysis (SRA) for choosing the important variables that have increased the accuracy of forecasting model of stock market. SRA technique finds a set of input variables that have most effects on output variables. Chang and Liu [52] applied stepwise regression analysis and K-means clustering techniques for enhancing the performance of proposed model. Dai et al. [54] used Nonlinear independent component analysis (NLICA) to transform the time series data into the feature space comprises of independent components (ICs) describing key information of the original data. After that, the ICs are used as the input of the neural network to construct prediction model named as NLICA-BPN. Simulation results show that the proposed prediction model has improved the performance of the neural network and also outperforms the PCA–BPN, LICA–BPN and single BPN approach. Wang and Wang [76] proposed the use of principal component analysis (PCA) in combination of stochastic time effective functional neural network (STNN) for analyzing stock price time series. In the proposed model they first implied PCA for to withdraw principal components (PC) from input dataset and then use these components as input to STNN. They compared the result of PC–STNN model with backpropagation neural network (BPNN) model, PC–BPNN model and STNN and show that prediction performance of proposed model is better than others. Niaki and Hoseinzade [80] employed a factorial design and concept of grouping to conduct a design of experiment in order to determine most influential factors among 27 financial and economical variables. The statistically significant factors selected through design of experiments are used as input to artificial neural network (ANN) to foresee the daily movement of S&P 500 index. Results from study shows that proposed methodology perform effectively better than buy and hold approach. Qiu et al. [56] utilized fuzzy surfaces for extracting effective set of input variables from original variables set. Inthachot et al. [107] used genetic algorithm to find the effective subset of features from a set of 44 features and used the optimized set of features as input to neural network. Zahedi and Rounaghi [149] performed the prediction of Tehran stock exchange by applying ANN model and principal component analysis (PCM). PCM is used in this study for extracting key features from 20 accounting variables. Gocken et al. [108] utilized genetic algorithm (GA) and harmony search (HS) for selecting the most appropriate features for Turkish stock market forecasting model. In this study, they firstly considered 45 technical indicators and at the end selected 26 and 23 variables by GA and HS model respectively. Tan et al. [102] and Weng et al. [127] utilized PCA to reduce dimensionality of the original dataset and obtaining various components which provides more valuable information. Laboissiere et al. [125] proposed the combined use of correlation analysis and multi-layer perceptron (MLP) model to learn the input features that have most impact on stock market to deal with the problem of forecasting maximum and minimum daily stock prices of three Brazil power distribution companies. Lei [59] proposed an integrated method by combining rough set (RS) and wavelet neural network (WNN) to enhance the accuracy in predicting stock market trend. In that work, firstly RS is applied to reduce the dimensions of input features set in addition to determine the optimal architecture of WNN. Then selected features are provided as input to optimized WNN prediction model to forecast the trend in five stock market indices. The simulation results show that by reducing the attributes through RS the prediction accuracy of WNN can be significantly improves to model the forecasting problem. Pimenta et al. [126] proposed a features selection approach on the basis of trading rules generated from technical indicators in his research work using genetic programming.

4.5 Forecasting Models

Forecasting stock price time series is one of the challenging task in time series and CI domain [2]. Forecasting models depends on the choice of task performed by authors’ i.e. whether they want to forecast trend (up or down) in stock market which is modeled as classification task or prediction of numeric value i.e. stock price or stock index which is modeled as regression task. In the past several years, a number of approaches have been proposed that can be applied for stock market time series forecasting. In this survey paper, our focus is on core CI approaches such as neural network, genetic algorithm, fuzzy logic and other evolutionary computing approaches.

4.5.1 Artificial Neural Networks (ANNs)

ANN is one of the efficient techniques to forecast stock market as it does not comprised complex formulas as compared to traditional liner and non-linear models [150]. ANNs have become popular technique used for forecasting stock market forecasting since last decade. The wide use of ANNs for forecasting stock market time series is due to capability of ANNs for handling data that are characterized by nonlinearity, high-frequency polynomial components and discontinuity [77]. ANNs are self-organizing, data-driven and self-adaptive techniques that have capability to adopt nonlinearity of time series without considering any statistical assumption about data [151]. Many types of ANNs have been employed in literature for forecasting stock market time series. Kara et al. [60] perform the prediction of upward and downward trend in ISE National 100 index using artificial neural network (ANN) and support vector machine (SVM). On comparing the performance of these techniques and showed that prediction accuracy of ANN model is higher than SVM model. In the experiments presented in Niall et al. [75], feed-forward neural network has been used to predict the next day DJIA index close price. They started the experiment by feeding neural network with current day opening price and previous 5 day opening price of DJIA. Then they gradually increase the input by introducing 10-day and 30-day moving average (MA), Previous 5 days’ daily gradients of DJIA, crude oil price, crude oil price and currency data, crude oil, currency data and gradient of DJIA. Experiment results show that neural network trained on 31 variables including external factors resulted in a return on investment (ROI) of 23.5% per annum at a time when the DJIA index increased by 13.03% per annum. Dhar et al. [152] use an ANN to foresee 1 day ahead closing stock price of Indian stock market. They used back propagation algorithm to train three layer neural networks. In this article, aim of the authors was to find the best ANN parameters by performing multiple experiments with different combinations of ANN parameters such as number of hidden layers, and number of nodes in each layer and learning rate. Vanstone et al. [105] employed multilayer Perceptron (MLP) to develop automatic trading system for Australian stock market. They used four fundamentals indicators such as return on equity (ROE), book value, dividend payout ratio and price to earnings ratio (P/E) as input for MLP. The output of neural network is a signal whose strength gives the expected return in 1 year time frame. Ticknor [121] implemented feedforward neural network (FFNN) combined with Bayesian regularization to foresee the movement in stock market. In Bayesian network the weight between the layers of network is considered as random variable and thus their density functions are represented using Bayes rule. During training, weights are adjusted by finding the probability density function of each weight. The proposed prediction technique minimizes the impact of overfitting and overtraining and improves prediction accuracy and generalization of network. Mabu et al. [122] investigated the use of ensemble learning paradigm by combining a rule based evolutionary technique and artificial neural network to take buy or sell decision in stock trading. In this article, a genetic network programming has been used for generating large number of stock rule pool and multilayer Perceptron (MLP) is used to select the best rule for making good decision in stock market. Guresen et al. [150] assess the performance of different neural network model for stock market index prediction. In that study, they have used multi-layer perceptron (MLP), dynamic artificial neural network (DAN2) and hybrid neural network by combining autoregressive conditional heteroscedasticity (GARCH) and exponential autoregressive conditional heteroscedasticity (EGARCH) with MLP. Liu and Wang [77] have presented a predictive approach for forecasting price fluctuation in stock market which is based upon Legendre neural network and random time strength function (LNNRT). They have also introduced the Brownian motion in proposed model to model the effect of random movement. Adebiyi et al. [153] compared the prediction capability of ANN approach with conventional Box–Jenkins autoregressive integrated moving average (ARIMA) and ANN model for the prediction of New York stock exchange. The experiment results reveal that neural network model perform better than ARIMA model. Chopra et al. [66] examined the capability of ANN to predict the Indian stock market before and after demonetization. In this article, backpropagation neural network (BPNN) is trained by Levenberg–Marquardt algorithm. Patel et al. [68] perform the comparison of four trend prediction techniques namely artificial neural network (ANN), naive-bayes classifier, random forest, and support vector machine (SVM) to predict the direction of movement of two stocks and two indices of Indian stock market. In this study, they considered two scenarios for input. In the first scenario, they used ten technical indicators and in the second scenario they represent these technical indicators as trend deterministic data. Zhong and Enke [84] applied artificial neural network (ANN) along with three version of principle component analysis (PCM) as a classification model to forecast the daily movement of stock market return. Wang et al. [100] developed a prediction model (ST-ERNN) which integrate Elman recurrent neural network (ERNN) with stochastic time effective function to predict stock market indices. In this article, they have analyzed the proposed model with the complexity invariant distance (CID), linear regression and multi-scale CID (MCID) and compared the result of prediction model with backpropagation neural network (BPNN), Elman recurrent neural network and the stochastic time effective neural network (STNN). The experiment results reveal that proposed model give the superior performance among other neural networks in stock price time series forecasting. Dash and Dash [70] developed a decision support system by combining learning capability of computational efficient functional link artificial neural network (CEFLANN) with the set of rules created from technical indicators for generating trading signals. In this article, extreme learning machine (ELM) method is used to train the CEFLANN network instead of traditional backpropagation algorithm and forecasting ability of proposed method has been compared with other machine learning techniques. Kristjanpoller and Minutolo [120] developed a hybrid volatility forecasting model by combining artificial neural network (ANN), generalized autoregressive conditional heteroskedasticity (GARCH), technical analysis and principal component analysis to forecast price volatility of bitcoin. Sheta et al. [86] explored the application of artificial neural network (ANN), support vector machine (SVM) and traditional multiple linear regression model (MLR) to build a prediction model for prediction of S&P 500 stock index and compared the performance of three approaches. In this study, the SVM outperforms MLR and ANN models. Pang et al. [101] developed an innovative neural network approach by proposing the deep long short-term memory neural network (LSTM) with embedded layer and the long short-term memory neural network with automatic encoder for stock market prediction. In this paper, they introduced the idea of stock vector in which input is not a single stock index but group of stock indices. In the two models embedded layer and automatic encoder are used to form vector of the stock market data. Simulation results demonstrate that deep LSTM with embedded layer provide better prediction accuracy than LSTM with automatic encoder. Fischer and Krauss [90] deployed long short term memory (LSTM) networks, a class of recurrent neural networks whose network structure is composed of at least one cycle and hidden layer is characterized by memory cell to predict the directional movement in financial time series. Prediction results of proposed method and memory- free classification techniques such as deep neural network, random forest and logistics regression classifier reveal that LSTM networks provide superior accuracy. Shynkevich et al. [124] utilized artificial neural network (ANN), K-nearest neighbor (KNN) and support vector machine (SVM) classifiers to investigate the impact of input window length on the future stock price trends. Input window length is a time span parameter which indicates how many past values in stock price time series can be utilized to compute the technical indicators which are provided as input to forecasting models for predicting the direction of future stock market. Results depict that maximun forecasting performance is achieved when the window length is approximately same as forecast horizon i.e. n-days ahead. Wang and Wang [49] suggested the use of stochastic time strength neural network (STNN) in combination with empirical mode decomposition (EMD) to enhance the prediction accuracy of stock price movement. In this research, EMD which is processing technique is used to extract all the oscillatory components present in stock price time series by decomposing original time series into various high and low frequencies subseries known as intrinsic mode functions (IMFs). The STNN forecasting model is applied for each IMF to obtain predicted value of each subseries and the predicted value of each subseries is aggregated to obtain the prediction of original stock price time series. Seo et al. [93] combined artificial neural network with different versions of generalized autoregressive conditional heteroscedasticity models (GARCH) and Google domestic trends (GDTs) to foresee the volatility of stock price time series. A Google domestic trend is open source services provided by Google to analyze the various sectors of finance and economics. In this work, the authors firstly estimated the volatility using family of GARCH model and then used output of GARCH family and GDTs as input to neural network for accurate forecasting of volatilities of S&P500 index. Mo et al. [103] introduced an exponent type connection into back propagation neural network (BPNN) to create an exponent back propagation neural network (EBPNN) for forecasting cross correlations between Chinese shanghai stock exchange (SSE) and Shenzhen stock exchange (SZSE) composite indexes in China stock market. In EBPNN information is processed by performing the dot product of exponent of input vector and weight vector. This research is motivated by concept that exponential type function captures more fluctuations in non-stationary data. The experiments result reveals that the EBPNN outperforms BPNN. Weng et al. [127] developed an expert system based on ensemble of machine learning methods such as artificial neural network, support vector regression, boosted regression tree and random forest regression that utilizes the features from multiple online sources to predict short term stock prices. The key idea of this work is to incorporate data from various sources such as historical stock prices, technical indicators, articles about given stocks published in news, Google search about given stocks and number of visited Wikipedia pages for related stocks. After data collection and preprocessing, the authors have applied principal component analysis to take off the effective features which are used as input to forecasting model. Results showed that use of features from online sources improved the accuracy of ensemble methods. Gocken et al. [128] combined harmony search (HS) with the architecture of artificial neural network (ANN), extreme learning machine (ELM), Jordan recurrent neural network (JRNN), recurrent extreme learning machine (RELM), regression tree (RT), generalized linear model (GLM), and Gaussian process regression (GPR) for short term and middle term stock price prediction. In this work, HS is utilized for feature selection and tuning the parameters of various proposed hybrid model. The parameters to be optimized are transfer function, number of hidden and context neurons in different models. Zhou et al. [94] developed a two-stage novel strategy based on empirical mode decomposition (EMD) and factorization machine based neural network (FNN) named as EMD2FNN to forecast the stock market trend. In the first stage, an efficient method to deal with non-stationary data namely EMD is used to bread down the original stock price time series data into number of components known as intrinsic mode functions (IMFs) which contains an oscillatory components within narrow range. In the second stage, each extracted IMF is provided as input to FNN to predict future stock price. Experiment result of proposed model provide better performance with respect to other models such as neural network (NN) model, the factorization machine based neural network (FNN) model, the wavelet de-noising- based back propagation (WDBP) neural network model, the empirical mode decomposition based neural network (EMD2NN) model.

4.5.2 Fuzzy Logic

Fuzzy logic approaches have been applied by many authors with relatively high success rate for modeling and forecasting stock price time series. Hadavandi et al. [147] proposed a combined approach by integrating genetic fuzzy system (GFS) and artificial neural network (ANN) to create an intelligent system for stock price prediction. They applied stepwise regression analysis for determining key features that have most influence on stock price and selected features are categorized into multiple clusters using self-organizing map (SOM). Finally all the clusters are used as input to GFS for extracting rule base. Results showed that the proposed model depicts better performance as compared to other approaches like ARIMA and ANN. Chang and Liu [52] developed a Takagi–Sugeno–Kang (TSK) type fuzzy rule based approach for stock market forecasting. They applied simulated annealing (SA) for determining the set of best parameters of fuzzy system. To justify the prediction accuracy they showed that TSK fuzzy rule system performs better than back propagation neural network (BPNN) and multiple regression technique. Esfahanipour and Aghamiri [53] implemented Neuro-Fuzzy inference system by adopted on a TSK type fuzzy rule base system for stock market forecasting and applied Fuzzy C-Mean clustering for determining number of rules. Boyacioglu and Avci [61] examined the capability of adaptive network based fuzzy inference system (ANFIS) for predicting stock market return. The experiments results show that ANFIS can be efficiently used for solving stock market prediction problems. Pathak and Shetty [64] generated fuzzy rule base for forecasting stock faith (high or low) which is strength of recommendation for buying or selling stocks. The proposed model has been implemented in three modules. In the first module, they used machine learning algorithms for predicting close price of stock. In the second module, they obtain sentiment value of latest news headlines about each stock. In the third module, outputs from both the modules are used as input to fuzzy logic module for generating fuzzy rule base. Zarandi et al. [136] applied a type-2 fuzzy system for stock price prediction by using both fundamental and technical indicators as input to the proposed model. In this study, the parameters of membership function are refined by genetic algorithm. Liu et al. [57] investigated the benefit of type-2 neuro-fuzzy system to model the stock price prediction problem. In this article, the given dataset is segmented into clusters using self-constructing clustering method and then a rule base of type-2 TSK rule is generated from each cluster. The parameters associated with type-2 neuro fuzzy model are tuned by particle swarm optimization and least square estimation. Zarandi et al. [123] presented a four-layer fuzzy multiagent system (FMAS) to create a hybrid intelligent system that combines the multiple intelligent agents to predict the next day stock price. The first layer is used to collect relevant information about the problem domain using expert knowledge. The second layer is dedicated to feature selection and cluster formation. The role of third layer is to build a model for all clusters using genetic fuzzy system and optimizing the built model to select the best fuzzy system for every cluster. The aim of fourth layer is analyzing the model and knowledge representation. Svalina et al. [111] created a prediction model which employs an adaptive neuro-fuzzy inference system (ANFIS) for prediction of close price of stock market, 5 days in advance, individually for each day. Dash and Dash [69] proposed a self evolving recurrent fuzzy inference system (SERFIS) for enhancing the prediction power traditional neuro-fuzzy system. The model is created by using the first order Takagi–Sugeno–Kang (TSK) type fuzzy system with two variant of feedback connection i.e. by providing the firing strength of the fuzzy rule back to it and introducing time delay feedback loops in the output layer. In this article, authors proposed a modified differential harmony search (MDHS) to optimize the feedback loop, antecedent and consequent parameters of proposed approach. In order to compare the result of proposed model, another network namely recurrent functional link artificial neural network (RCEFLANN) is also presented in this paper. Su and Cheng [116] presented a novel stock price prediction model by employing adaptive neuro fuzzy inference system (ANFIS) and integrated nonlinear feature selection (INFS) techniques. This study used INFS method to select the key technical indicators which are utilized as input to ANFIS forecasting model to obtain primary forecasted value and at last, adaptive expectation model is used to further increase the performance of prediction model. Sadaei et al. [87] initially used differential fuzzy time series logic to forecast trend in stock market data and then introduced a novel evolutionary technique namely imperialist competitive algorithm (ICA) to further enhance forecasting accuracy of initial model by optimizing the model parameters. Chouemouziadis and Chatzoglou [112] presented a short term trading fuzzy model by using Mamdani fuzzy system and mixture of commonly used and rarely used technical indicators for generating trading signals in stock market. Jiang et al. [88] presented an interval type-2 fuzzy logic system (IT2FLS) to forecast stock indices on the basis of fuzzy time series and a fuzzy logic relationship map (FLRM). In this article, proposed model works in five steps. First step involves finding the variation within time series. Second step includes fuzzification of time series and defining fuzzy set. In the third step, input interval type-2 fuzzy sets (IT2FSs) and output intervals of interval type-2 fuzzy logic system (IT2FLS) are defined. Fourth step includes creating fuzzy logic relationships (FLRs) and the fuzzy logical relationship map (FLRM) and finally foresee the future values. Zang et al. [118] suggested a novel approach based on fuzzy logic and combination of visibility graph and link prediction to enhance the accuracy of time series prediction problem. In the proposed method, time series is firstly transformed into visibility graph then link prediction technique is applied to obtain initial prediction and finally fuzzy logic is utilized to further enhance prediction accuracy by determining fuzzy rules based on relationship between historical data. On the basis of comparison between previous studies, authors showed that proposed method have better predictability. Cheng and Yang [58] proposed the use of fuzzy time series model and rough set rule induction to forecast stock index. In this work, the authors have applied rough set rule induction algorithm namely LEM2 (Learning from Examples Module version 2) to extract forecasting rules of selling or buying from time series to obtain initial forecast. After that, the adaptive expectation model is utilized to enhance forecasting performance of initial forecast. The adaptive expectation model is a reasonable forecast model in time series forecasting. In stock price time series forecasting, by using adaptive expectation model the future stock prices are generated by the past single period of stock price and forecasting error for last one period. Chander [131] formulated the stock price time series prediction model based on fusion of wavelet transform (WT) with adaptive neuro fuzzy inference system (ANFIS). In this work Haar wavelet transform is utilized to split the normalized time series data into two components viz. approximation components and detail coefficients to construct feature vector which is provided as input to ANFIS model to generate future stock price as outcome of proposed model. Results from comparison of proposed model with ANN and hybrid of ANN with wavelet transform show the superiority of the model.

4.5.3 Genetic Algorithms (GA)