Abstract

This study investigates the effects of the decision-making style of angel investors on their investee businesses’ valuations with a particular focus on the early post-investment phase. Business angels not only provide new ventures with financial resources. By assuming different value-added roles, they also contribute considerable non-financial value to their investee companies during the post-investment phase. They not only act entrepreneurially through their hands-on involvement, but also often have their own distinct entrepreneurial experience. We hence draw on the emerging entrepreneurial decision-making theory of effectuation to explain their investment outcomes in an environment of uncertainty. This study links angels’ decision-making styles to their ventures’ valuations in the period between their initial investment and the first external follow-up investment in an investee business. Based on a sample of 73 angel investments, this study finds that informal investors experience a significant increase in their investments’ valuation if they emphasize the effectual principle of means-orientation in their decision-making.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

1 Introduction

Business angels and the informal equity capital market play a crucial role for the successful development of early-stage ventures (Wetzel 1983; Mason and Harrison 1995). Although the informal capital market “operates in almost total obscurity” (Prowse 1998, p. 785), we have begun to understand it over the last two decades. However, the post-investment phase of angel investments remains one of the most under-researched areas in angel research (Politis 2008) and many aspects of it are still unclear (Collewaert and Sapienza 2014). Conceptual and explorative studies find that angel investors become actively involved in their investee businesses in the post-investment phase (Ehrlich et al. 1994; Mason and Harrison 1996; Shepherd and Zacharakis 2001). Earlier empirical studies provide evidence on the outcomes of angel investments (Mason and Harrison 2002; Wiltbank et al. 2009). While some researchers doubt that informal business angels add significant value to investee businesses (Chemmanur and Chen 2002; Fairchild 2011), many other studies suggest that business angels’ active engagement on strategic and operational levels and their ability to support their startup investments in successfully acquiring follow-up financing are important value-creating contributions (Mason and Harrison 2002; Sørheim 2005; Politis 2008). However, so far, research has not yielded any empirical insights into whether business angel activity ultimately does have an evidently beneficial and quantifiable effect on investment companies’ value creation.

Conceptual studies, on the one hand, highlight that angels’ investments and their non-financial contributions provide the foundation for the ventures’ survival, future growth, and value creation over the time of the investment (e.g. Prowse 1998; Oetker 2003; Politis 2008). On the other hand, we can also expect that the effects of angels’ influence and contribution will be increasingly diluted once additional investors enter the company in subsequent financing rounds. The early post-investment phase—the period between an angel’s initial investment and the first external follow-up financing—is therefore of special importance and interest when measuring the outcomes of angel investors’ involvement in this timeframe.

One of the most prominent findings on the level of individual angel investors is that they mostly have considerable entrepreneurial experience of their own (Prowse 1998; De Clercq et al. 2006; Morrissette 2007). In combination with their active hands-on involvement during the post-investment phase (Mason and Harrison 1996), they are often regarded as co-entrepreneurs, much rather than as investors (Morrissette 2007). Angel investors, amongst other activities, share their experience, advise the founding team on important decisions (Politis 2008), and often even become engaged on an operational level (Oetker 2003). Therefore, their decision-making approach can substantially influence the future development of the venture as a whole. The emerging theory of effectuation addresses this cognitive decision-making process of entrepreneurs (Sarasvathy 2001). It has already been applied to some extent to the early-stage and angel investment contexts (Wiltbank et al. 2009; Appelhoff et al. 2016). Yet, its broad application to the level of angel investors, especially with the purpose of investigating investment outcomes, is still in its infancy and offers potential to increase our understanding. Hence, this study draws on it to explore and explain the outcomes of business angel investors’ decision-making activities with respect to the value creation in their investee businesses in the early post-investment phase.

We use the entrepreneurial theory of effectuation and related entrepreneurial decision-making patterns (Sarasvathy 2001; Dew et al. 2009) of business angels to predict their early-stage investment success, expressed as an increase in their investee businesses’ valuations. Applying one of the earliest objective and observable success measures in the angel financing context (Collewaert and Manigart 2016), this study intends to answer the following research question: Is an entrepreneurial decision-making style, expressed as a preference for effectual decision-making patterns, by business angels positively related to their investee businesses’ valuation development in the early post-investment phase?

To test our hypotheses empirically, we gathered primary data from German-speaking business angels. Our sample contained 73 complete responses, each representing an individual investor-venture setting. The study’s main finding is that business angels who emphasize the effectual decision-making principle of means-orientation experience a significant increase in the valuation of investee businesses, while the other effectual principles (i.e. affordable loss, partnerships, leveraging contingencies) did not show a significant effect.

This research contributes to the existing literature in four areas. The study sheds light on the little understood post-investment phase of angel investments (Politis 2008; Collewaert and Sapienza 2014). It also provides empirical evidence on how business angels add value to their investee businesses (Fairchild 2011). With its approach, the study also helps establish venture valuation as an early-stage success measure (Collewaert and Manigart 2016; Röhm et al. 2017). By discussing and applying the principle of effectuation to a new venture financing context, this study ultimately adds to the recent debate on the evolvement of effectuation as an entrepreneurship theory (Chandler et al. 2011; Perry et al. 2012; Arend et al. 2015; Welter et al. 2016). Beyond theoretical insights, our research provides practitioners with recommendations on the impact of decision-making patterns and on the selection of angel investors from an entrepreneur’s perspective.

2 Theoretical foundations

2.1 Decision-making principles under uncertainty

Over the past years, several theories have emerged that try to explain entrepreneurship and entrepreneurial decision-making in particular. Among others, there is the concept of entrepreneurial bricolage, which describes entrepreneurial behavior as “creating something from nothing” in situations of extreme resource scarcity (Baker and Nelson 2005). Shane and Venkataraman (2000) developed the entrepreneurial opportunity recognition framework. Sarasvathy’s (2001) effectuation approach is one of today’s most prominent and discussed entrepreneurship theories (Fisher 2012; Perry et al. 2012; Arend et al. 2015; Welter et al. 2016).

In line with Sarasvathy’s (2001) seminal work, Perry et al. (2012) summarize effectuation as a decision-making process in the entrepreneur’s pursuit of opportunities in uncertain environments. While managers often engage in “causal” goal-oriented processes, expert entrepreneurs have been shown to rely on “effectual” decision-making processes: they focus on a set of given means and their application towards the best alternative of achievable outcomes (Sarasvathy 2001). Based on the behaviors initially identified in Sarasvathy’s study, Dew et al. (2009) find five subdimensions of effectuation (vs. causation) amongst expert entrepreneurs: exercising non-predictive control (vs. prediction of the future); means-orientation (vs. goal-orientation); limiting downside risk by taking an approach of affordable loss (vs. orientation towards an expected return); establishing strategic partnerships (vs. competitive analyses); and leveraging unexpected contingencies (vs. avoiding them). Despite the current critical discussion (Arend et al. 2015), effectuation as an entrepreneurship theory finds many supporters (Fisher 2012). Critical reviews, however, encourage research to establish the theory further, for example, through continued empirical testing (Perry et al. 2012). This ongoing discussion and the number of published articles over the last decade appropriately indicate how important effectuation theory is to advance our understanding of entrepreneurial decision-making and of the overall respective outcomes. Hence, applying the principle to new and more specified entrepreneurial contexts such as informal angel investments will add substantially to this research stream.

2.2 Informal angel investors as potential effectual entrepreneurs

Effectuation has not only been established in the general entrepreneurship literature, it has also found its way into entrepreneurship’s venture-financing branch. In this context, investors in entrepreneurial ventures are often described as following the causal decision-making style: they are goal-oriented and strive to maximize the return on their investment (Read and Sarasvathy 2005). However, early-stage investors are not a homogeneous group.

There is a dominant distinction between formal, or institutionalized, and informal sources of venture capital (Wetzel 1983; Prowse 1998). Venture capital firms (VCF) and related types (e.g., Corporate Venture Capital Firms) represent formal, institutionalized suppliers of venture capital, while business angels (BAs) and founders, friends and family generally represent informal investors. The latter are of rather low importance in terms of involvement and individual investment volumes (Riding 2008). BAs, in contrast, play a crucial role in the early-stage financing process and significantly differ from institutionalized VCF investors regarding their motivation and investment characteristics (Morrissette 2007); they also account for a much larger proportion in the total investment volume (Fairchild 2011). Three important domains help distinguish BAs clearly from institutional VCFs.

First, BAs’ main investment motivation ultimately is to achieve a financial return (Mason and Harrison 1996). Yet, BAs tend to invest for another important reason: they enjoy building and growing successful ventures through hands-on involvement, mostly without a predetermined investment horizon (Prowse 1998; Aernoudt 1999). This indicates that BAs act a lot in an entrepreneurial way and become actively involved on an operational level when entering a venture. This confirms the observation that “the distinction between entrepreneur and investor is often rather blurry” (Morrissette 2007, p. 59). VCFs, in contrast, invest dedicated funds and are intent on generating a certain minimum return on investment within a determined period to fulfill their business model (Bygrave and Timmons 1992). They are hence by definition forced to apply causal decision-making processes such as setting financial goals.

Second, other than VCFs, BAs typically invest in much earlier growth phases (De Clercq et al. 2006) in which the venture may not have realized first revenues or may not even have entered the market. In these early stages, uncertainty is especially high as there are no or only few indicators for the venture’s market success. Effectuation is “largely understood as a paradigm for decision-making under uncertainty” (Welter et al. 2016, p. 10)—the characteristic angel investment pattern should hence allow for an assessment of their early-stage investments from an effectuation perspective.

Third, literature investigating the professional backgrounds of BAs find that many are, or have been, entrepreneurs themselves, while investment managers at VCFs rarely have entrepreneurial experience of their own (e.g., Morrissette 2007). As Dew et al. (2009) point out, effectual decision-making processes are observable amongst expert entrepreneurs.

Following the reasoning above, investigating BA activity based on effectuation theory appears to be a promising field of research. This is especially true when considering that BAs behave like—and often still are to a certain extent—expert entrepreneurs themselves. In this context, it is noteworthy that BAs are not a very homogeneous group of investors either (Prowse 1998). Besides the various existing definitions of BAs (Avdeitchikova et al. 2008), there are several subtypes of informal equity investors who all differ in terms of motivation, experience, investment patterns, professional backgrounds, activity, and other aspects (Oetker 2003; Morrissette 2007; Lahti 2011). It hence seems plausible that different angel investors also practice different decision-making styles.

Given these results, it should be particularly interesting to investigate the effects of different angel investors’ behavioral traits. Building on these findings from effectuation and early-stage financing theory, this study therefore explores how the different decision-making styles of BAs affect the development of their investee businesses in the post-investment phase.

2.3 Effectuation and performance outcomes in early-stage investments

In their meta-analytic review of effectuation research and new venture performance, Read et al. (2009) identify a large number of studies investigating the effects of different effectual decision-making patterns on various objective and subjective performance measures in the new venture context; they mostly find a positive impact. Yet, it is surprising that most of the identified success measures seem somewhat suboptimal for the new venture context. Measuring performance in a new venture setting generally represents a special challenge to researchers (Chandler and Hanks 1993). Absolute figures such as sales and profits are often not available for several months or are only generated years after company inception. Relative measures such as market effectiveness are often hard to obtain due to non-existent or ambiguous peers and competitors, especially in highly innovative environments (Chandler and Hanks 1993). In the context of early-stage angel investments, such success measures are even more disputable as angels often invest even before a venture has been legally formed or has entered the market (De Clercq et al. 2006).

While research has established effectual decision-making principles as predictors for venture success in general, only one study has, to the best of the authors’ knowledge, so far investigated effectuation and causation theory in an informal equity financing context. Wiltbank et al. (2009) empirically verified that angel investment outcomes (i.e., return on investment realized upon exit) tend to be beneficial if non-predictive control is emphasized over predictive decision-making processes. As in Wiltbank et al.’s (2009) study, the applicability of an internal rate of return (IRR) as success measure requires the observation of a successful exit. Often, however, many years pass between the first investment of a BA and an exit (Morrissette 2007). In this period, new investors, team members, and other external resources usually enter the venture—provided it persists. This presumably leads to an increasing dilution of both an initial angel investor’s influence and impact on the outcome over time. As Mason and Harrison (2002, p. 221) point out, it is one of the main objectives and necessities for an angel investor to show “considerable support” towards achieving early venture growth, and it is also in their very own interest to enable the venture to acquire follow-up financing.

The prompt involvement and decision-making in the early stage of the angel investor’s post-investment phase hence play a crucial role for building a solid foundation for future success and an eventual exit out of the venture. Therefore, this very first phase between an angel’s initial investment and the first follow-up financing provided by new external investor can be considered the most important time for BA involvement. It should thus be in the focus when investigating the effects of their decision-making.

Corporate finance literature does pay attention to the aspect of valuation (Basse-Mama et al. 2013; Klobucnik and Sievers 2013), and valuation in the context of post-investment involvement has been covered in an explicit private equity/buyout setting (Meier et al. 2006). Research on venture valuation in an early-stage setting, however, is just emerging (Collewaert and Manigart 2016; Röhm et al. 2017). Current early-stage investment literature examines effects on valuation at a single point in time. Meier et al.’s (2006) concept, in contrast, offers an interesting starting point by defining the increase in valuation between two points in time as a success measure: The increase in an angel investment’s valuation in the early post-investment phase can be considered an early indicator for the angel’s investment success. From the firm’s perspective, a new investor’s willingness to pay a higher share price than previous investors is, de facto, a recognition of growth and value. For the informal angel investor, a follow-up financing round at a higher price might be proof for adequate success-bearing entrepreneurial decision-making in an uncertain environment.

3 Hypotheses

It is not undisputed whether BAs add value to a venture at all. Fairchild doubts that the value contribution of BAs is significant, especially compared to the value added by VCFs (Fairchild 2011). There is, however, also considerable evidence that BAs become more involved in their investee businesses than VCFs (Osnabrugge 2000) and that they do contribute through exercising certain value-added roles (Mason and Harrison 1992; Politis 2008). In his analysis of explorative literature, Politis (2008) summarizes that BAs contribute to their investee businesses through strategic involvement, monitoring, acquisition of resources, and mentoring of the founders. Brettel (2003) and Oetker (2003) emphasize in their early works on the German angel scene that value-added activities also include the transfer of know-how in functional areas (e.g., finance or marketing) and in the industry, which facilitates further financing, networking, and operational support. Prowse (1998) observes the same activities amongst BAs in the United States, to name another example. Although BA activity does resemble VCF activity on a higher level (Sapienza 1992; Haagen 2008), angels seem to focus much more on the operational level compared to VCFs with their rather strategic orientation. Ultimately, exercising their value-added roles through frequent involvement requires BAs to make frequent decisions.

We investigate which effectual decision-making patterns—in contrast to causal decision-making patterns—are beneficial for an angel’s contribution to the investee business. Wiltbank et al. (2009) explored whether an emphasis on non-predictive control (effectual) or prediction (causal) is more beneficial when dealing with an uncertain future. This study extends Wiltbank et al.’s research by analyzing additional effectual dimensions, as outlined by Dew et al. (2009): means-orientation, affordable loss, partnerships, and leveraging contingencies. On a general level, this paper follows Wiltbank et al. (2009) and presumes a positive relationship between an emphasis on effectual decision-making and BAs’ early post-investment success. In line with this argumentation, we describe in the following the reasoning for the respectively presumed positive effects of the effectuation subdimensions.

3.1 Means-orientation

In an environment of high uncertainty, expert entrepreneurs have been shown to focus on given means and use these towards the most beneficial achievable outcome. This pattern stands in contrast to predetermining a goal and acquiring the means necessary to accomplish it—an approach applied rather by novices and “MBA students” (Dew et al. 2009). Given means refers to the entrepreneur’s identity and traits (“who I am”), experience and skills (“what I know”), and network (“whom I know”) (Sarasvathy 2001). Startups operate in environments of high uncertainty, especially at the earliest stages, and focusing on dedicating available means towards the most desirable and achievable outcome appears to be a more beneficial approach than setting a goal that they most likely cannot achieve. The same logic should apply to angel investors who invest at the earliest stages in startups (i.e., high uncertainty) and contribute to the business through hands-on involvement (i.e., act entrepreneurially). By basing their decisions on available means while contributing to the startup, angels presumably create more value than by predetermining a goal at an early stage and attempting to acquire the means necessary to fulfill it.

Hypothesis 1

A business angel’s preference for the effectual means-orientation principle is positively associated with investee businesses’ value creation in the early post-investment phase.

3.2 Affordable loss

The affordable loss principle refers to the practice of investing only as much as one is willing and can afford to lose instead of making an investment decision based on calculating an expected return (Sarasvathy 2001). In an entrepreneurial environment subject to high uncertainty, resources (financial, human, time, etc.) are highly limited, and predictability is practically not existent. Founders thus often cannot refrain from exercising a trial-and-error approach when developing their ventures (Dew et al. 2009). As it is only natural that some approaches (e.g., technologies or market entry strategies) will fail, entrepreneurs must consider and should expect to have enough resources to try different strategies. Experienced expert entrepreneurs know that one should not bet all resources on the first idea or strategy only because it promises high returns. Hence, following the affordable loss principle will allow entrepreneurs to engage in multiple attempts when pursuing a business idea.

For BAs, the affordable loss principle can be considered beneficial in two ways. First, it is relevant in the pre-investment phase. BAs invest their own money and can only dedicate a limited amount of their personal time per investee business (Osnabrugge 2000). Therefore, they had better select their investment cases carefully instead of playing a portfolio game. Wiltbank et al. (2009) confirm the assumption that effectual BAs experience fewer investment failures than causal investors do. This implies that the application of the affordable loss principle might lead to sounder investment decisions, resulting in a more valuable investment portfolio—even before the angel has started contributing to the venture. Second, following the affordable-loss decision-making style while involved in the post-investment phase might help establish a culture of “fail fast, fail often,” rather than “fail late, but once and for all.” Post-investment decision-making based on this principle will hence lead to a more sustainable value creation process. That way, a venture will be able to evaluate practically multiple approaches to executing its business idea, which increases the chance that it ultimately discovers the most promising and valuable one.

Hypothesis 2

A business angel’s preference for the effectual affordable loss principle is positively associated with investee businesses’ value creation in the early post-investment phase.

3.3 Partnerships

The causal behavior of conducting competitive analyses is rarely beneficial to expert entrepreneurs when pursuing a new business opportunity. They much rather focus on building a network of strategic partnerships with customers and suppliers (Dew et al. 2009), thereby ensuring early pre-commitments of outsiders (Sarasvathy 2001). Causation-oriented managers instead tend to prefer analyzing their competition and positioning their companies accordingly. In early-stage environments, strong partnerships are especially beneficial as partners can perform or facilitate many steps in the value chain, allowing the founding team to focus on its core idea and core competencies.

Successful BAs not only tend to have experience as a personal trait; they also have a large number of network contacts at their disposal through which they either generate deal flow in the pre-investment phase (Sørheim 2003; Garbotz et al. 2010) or acquire additional resources in the post-investment phase (Sørheim 2005; Politis 2008). Garbotz et al. (2010) found that strong network ties (i.e., network quality) outweigh the potential benefits of weak network ties regarding an angel’s deal flow quantity and quality. In other words, close relationships, which can be understood as strategic partnerships, will lead to more and better deal flow to the angel. This implies that by building strategic partnerships, an angel will not only get access to more investment cases, but will also invest more often in provided investment cases. This leads to the assumption that a focus on this effectual principle will allow the angel to select better investments with a higher potential for a strong valuation development. In the post-investment phase, in contrast, angels with an emphasis on building strategic partnerships should know and convey the ability how to build a network to ensure pre-commitments from outsiders. They will also be able to secure follow-up financing at better conditions through their network. A BA with a tendency to build strategic partnerships can hence be assumed to transmit greater value to a startup than one assisting the entrepreneur in analyzing the venture’s competition.

Hypothesis 3

A business angel’s preference for the effectual partnerships principle is positively associated with investee businesses’ value creation in the early post-investment phase.

3.4 Leveraging contingencies

Unexpected events are part of every entrepreneur’s daily life. Expert entrepreneurs have learned not only to cope with these contingencies, but to leverage them and turn them into opportunities (Dew et al. 2009). While new venture creation is already a highly unstable endeavor entailing many surprises, early-stage venture financing has its very own potential for unforeseen circumstances and events, especially from an investor’s point of view. Taking a principal-agent perspective in this dimension, the new venture financing context can be considered highly exposed to information asymmetries between investor and entrepreneur (Akerlof 1970). An investor can overcome these asymmetries in the pre-investment phase through intensive due diligence processes and elaborate contracts and intensive monitoring in the post-investment phase (Osnabrugge 2000). Other than VCFs, BAs, however, often tend to invest based on a “gut feeling” without spending too much time and effort on due diligence and contracts; to bridge the information gap, they place stronger emphasis on a close relationship (Morrissette 2007, p. 59). As most of BAs’ identified investment criteria appear to have a rather soft and subjective character (Brush et al. 2012), such as entrepreneur/team (Brettel 2003; Maxwell and Lévesque 2014) or customer/market attractiveness (Brettel 2003; Maxwell et al. 2011), surprises in the post-investment phase are likely to occur, both on a micro- (investor-entrepreneur) and on a macro-level (firm-market). At an early stage, a venture can be considered rather unstable, and minor turbulences can put the entire company at stake. Knowing how to address, solve, and turn inconvenient issues around rather than sitting them out or trying to avoid them can therefore be seen as a valuable practice aimed at ensuring a venture’s survival and building a solid foundation for future growth.

Hypothesis 4

A business angel’s preference for the effectual leveraging contingencies principle is positively associated with investee businesses’ value creation in the early post-investment phase.

4 Method

4.1 Sample

Collecting data from BAs represents a special challenge as the informal capital market operates mostly in anonymity (Prowse 1998). Even though the Internet has increased transparency and facilitates the identification of some BAs, many can still only be found and reached by personal references and introduction. Following the multi-method approaches by Wiltbank et al. (2009) and Harrison and Mason (1992), we proceeded as follows to conduct this quantitative study. First, the overall research proposal was discussed with several BAs and experts. Subsequently, the applied measures were pretested with a group of 20 personally known informal angel investors to ensure high validity and detect potential sources for misconceptions. The development of the sample and the distribution of the online survey took place between June 2015 and January 2016; to this end, multiple approaches and channels were used. First, 25 angel networks and other related organizations in Germany, Austria, and Switzerland (DACH area) were contacted and asked for their support. 7 of those agreed to distribute the survey among their members; however, they did not provide a list or number of angels who received the invitation to participate. Second, the largest German professional social network Xing.com was searched for BAs (applying the search terms ‘business angel’, ‘angel’, and ‘angel investor’), which were contacted with direct and personalized messages. The authors also leveraged their personal networks and the university chair’s connections to angels and angel-backed startups. Furthermore, all participating angels were asked to provide references to other BAs in their personal networks, or to forward the survey to them. As the participating angels and networks were in most cases not able or—understandably—not willing to disclose the names and numbers of referenced angel investors, it was not possible to calculate an initial sample size; any estimations would most likely be inaccurate and would not contain any valuable information. Consequently, it was not possible to arrive at a true response rate, which presents a limitation for this study. However, as multiple channels were used to obtain the sample, sufficient randomness should be ensured and potential selection biases within the sample should be reduced (Avdeitchikova et al. 2008). Yet, the online survey method does bear a risk of common method and self-selection biases, which will be discussed later.

A total of 88 German-speaking informal angel investors answered the survey. They all had made at least one early-stage investment in the past 10 years. 15 of these BAs had not yet made an investment that underwent a follow-up financing round and hence were eliminated. This resulted in a final sample of 73 complete responses for this study. Given the fact that angels had to provide sensitive investment information and that other studies use comparable sample sizes (Vanacker et al. 2013; Collewaert and Manigart 2016), the sample size of 73 investment observations can be considered appropriate. Table 1 summarizes the sample’s investor and deal characteristics.

The angels in the sample are on average 52 years old, are almost exclusively male (only two female respondents); all have a university degree. They each engaged in between 1 and 40 angel investments, with the median investment experience being ten investments. The number of total investments in the sample amounts to 775. Besides their angel investor commitments, we also asked for their experience within a startup environment. The sample’s respondents have a median startup experience of 10 years. The angel investors hold their investments for about 5 years on average (20 respondents did not report their investment horizon). A more detailed look at their performance history indicates that the data in this sample are in line with other reports (Brettel 2002): The aggregated data show that about 50% of the investors have exited 10% or fewer of their past investments successfully. As far as downside performances (e.g., defaults) are concerned, we find that about 50% of the investors have experienced defaults within at least 30% of their past investments. This suggests that the majority of investments have remained active and have not been liquidated, neither in a positive nor in a negative way. The overall success and failure rates in the sample are in line with reported figures in other studies (Mason and Harrison 2002; Wiltbank et al. 2009) and hence indicate a low risk of self-selection bias.

The observed investee businesses received an initial angel investment of about €188,500 (median = €50,000) on average at an average pre-money valuation of €2,334,000 (median = €1,500,000). The BAs sourced the deals mostly through direct personal contacts (private and business) (68%) and invested mainly in the seed or startup stages (89%). While the data indicate a general representativeness of the sample (Prowse 1998; Morrissette 2007; Wiltbank et al. 2009), they also reveal that angel investors in this sample seem to favor the very early stages of ventures. In the follow-up financing round, the average valuation of investments increased to €6, 538,000 (median = €3,300,000); the ventures on average had reached the next growth stage. Follow-up investments were mostly provided by institutional venture capital investors at the startup and expansion growth phases. This is in line with previous research, which finds that BAs typically invest in earlier stages than VCFs (Prowse 1998; De Clercq et al. 2006; Morrissette 2007).

Overall, the collected data match those of previous angel investor research. Even though the sample used in this study is exclusively composed of respondents in the DACH area, it still reflects the personal and investment characteristics found in other studies investigating angel investors in the U.S. (Wiltbank et al. 2009) and the UK (Mason and Harrison 2002).

4.2 Dependent variable

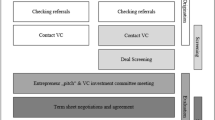

The dependent variable for this study is the increase in valuation between the angel’s initial investment and the first follow-up investment through an external investor. This increase in valuation represents a simple multiple on the investee company’s share price at which the angel invested. Value increase is an appropriate early-stage success measure for angel investments: it not only reflects the mindset of angel investors (Mason and Harrison 2002), but also is one of the first measures that can be objectively assessed (Mason and Harrison 2002; Wiltbank et al. 2009; Collewaert and Manigart 2016). Angels were asked whether one or more of their investee companies had received follow-up financing through a new external investor. If that was the case, they were asked to answer the next questions in the survey with reference to the last investment that had received follow-up financing (angels who did not experience a follow-up financing in one of their investee businesses yet were excluded from the sample). This specific instruction to select a deal of interest to this study served to ensure that angels provided the most valuable data and to reduce the risk of self-selection bias. In that way, respondents did not choose the venture on their own; instead, they had to submit information on the last one matching the above criterion—regardless of its outcome (otherwise, they might have picked a particularly well-performing one). Furthermore, pretests revealed that angels prefer focusing on one and on the latest appropriate investment. It is rather unlikely that they are willing to consult the entire documentation of all their past investments to answer an online survey. We also chose this one-investment approach to enhance the likelihood of obtaining correct information, to reduce the risk of angels’ confusion when trying to remember several past investments, and to increase response rates for this critical survey item.

Valuation was measured in terms of pre-money valuation, i.e., the firm value prior to a new investment by a new investor. This is common and in line with other literature investigating early-stage firm valuation (Hsu 2004; Collewaert and Manigart 2016). Based on the resulting two valuation figures (Vt1 = pre-money valuation at initial investment and Vt2 = pre-money valuation at follow-up investment), a simple cash multiple (Valuation Increase = VI) was calculated (VI = Vt2/Vt1). The resulting VI multiples were clustered in three categories, which allows for a certain margin of error amongst reported valuation figures (which were rounded to the full €10,000 or even €100,000) and facilitates the interpretability of results. The clustering comprises one category for losses (VI below 1), one category for medium performance (VI between 1 and 2), and one category for outperformance (VI above 2). This approach is in line with the only two other studies that have previously measured and reported BA investment performance (Mason and Harrison 2002; Wiltbank et al. 2009).

4.3 Independent variables

We measured effectual decision-making patterns with Brettel et al.’s (2012) construct, which was originally applied to a corporate R&D context. This construct covers individual behavior and has been used in an entrepreneur-investor context (Appelhoff et al. 2016). It employs effectual and the corresponding causal decision-making items in four subscales: means-orientation, affordable loss, partnerships, and leveraging contingencies. In line with the study of Brettel et al. (2012), effectuation and causation items were measured on a bipolar scale. Respondents were asked to rate on a 7-point Likert scale which of the corresponding behaviors in each item (causal = 1; effectual = 7) of the respective scales better describes their own conduct as early-stage investor and active BA.

Before pre-testing the scale, the wording of some of the items was slightly adapted to fit the BA early-stage investment context. After the pre-test, the scale was once again slightly adjusted, which resulted in the final construct for the study. A few items had to be eliminated during the exploratory factor analysis; all four scales, however, showed high Cronbach’s alphas of 0.91, 0.88, 0.92, and 0.91, respectively. Appendix A provides additional information on the construct, including the items’ wording and the results of the confirmatory factor analysis for each scale.

One might argue that measuring BAs’ individual preference for applying effectual or causal decision-making may not be suited to predict the observed increase in valuation on the firm level, as many other factors may have a stronger and more direct influence. To address this concern, we took two specific measures. First, the wording in the questionnaire’s construct was carefully chosen; it explicitly puts the investigated effectuation and causation items in context with the respondents’ decision-making activity in the investee businesses. Second, besides a number of other controls, the degree of investors’ active involvement in the observed investment cases was included in the regression models. Based on these measures, the observed decision-making preferences allow to draw conclusions on effects within the investee businesses. Moreover, measuring individual-level decision-making patterns to interpret organizational outcomes is a common approach which has been applied to various other contexts (Read et al. 2009; Wiltbank et al. 2009; Brettel et al. 2012).

4.4 Controls

In this study, we observe two different valuations for the same company at different times. Besides the hypothesized independent predictors, we chose several control variables to account for other influencing factors. A multitude of attributes can affect the absolute valuation in any individual financing round, such as investor and founder traits (e.g., human capital, social capital, investor/founder relationship), company-level characteristics (e.g., revenue, profit, stage), or external influences (e.g., market situation, interest rates, competition). As it is nearly impossible to cover all potential influences with the comparably small datasets obtainable in angel research, we selected certain controls with respect to their potential influence, especially on the investigated relative change in valuation. Furthermore, some proxy controls were calculated to capture and combine several potential effects over time.

The first set of controls relates to investor traits. Research has shown that investor experience has a potential effect on valuation (Collewaert and Manigart 2016). Two types of experience were measured and included in the model: investor experience (i.e., the number of investors’ angel investments) and startup experience (i.e., the number of years the investor has worked in a startup environment).

Earlier studies reveal that angel investors also differ in their level of involvement (Lahti 2011). Although their overall contribution is broadly accepted, the beneficial effects of carrying out value-added roles depend on the degree of their involvement. Therefore, we adopted Sapienza’s (1992) approach and measured the frequency of interactions between investors and founding teams. Furthermore, including and controlling for investor involvement in the model is a necessary link in terms of different levels of measurement (investor level vs. firm level) and is in line with other studies on investors’ decision-making outcomes (Wiltbank et al. 2009; Appelhoff et al. 2016).

On the level of the venture, a company’s industry can play an important role for its valuation. Different investment requirements in different industries in the early stages typically bear different potentials for economies of scale; hence, market valuation multiples also vary considerably (Damodaran 2016). With “new economy” business models—typically seen in telecommunications, the media, and most predominantly the Internet industries—small investments can yield overproportional growth and return. Hence, we included a dummy control for “new economy” sectors in the study.

In addition, the age of the venture at the time of the initial investment can influence the level and development of valuation; the same is true for the period of time until a follow-up investment is acquired. Accordingly, the control variables “venture age at initial investment” and “time to follow-up financing” were included.

Furthermore, the venture’s performance at both points of investment (initial by angel and follow-up by other investors) should be considered as a predictor of venture valuation. Measuring performance in entrepreneurship is, however, challenging, as many subjective and objective measures exist and not all of them are appropriate at different stages (Chandler and Hanks 1993; Davidsson 2008). This study hence includes a proxy to capture the effects of various performance indicators. A company’s growth stage can reflect numerous performance indicators, such as levels of growth, revenues, team size, market position, etc. (Gupta and Sapienza 1992; Jain 2001). While direct performance effects such as revenues or profits may also depend on the venture’s industry, its growth stage reflects other qualitative and industry-independent characteristics, such as an existing prototype or a completed market entry. Advancing quickly from earlier to later stages can also be considered a successful company performance. To take into account the connected performance implications of a company’s stage at both points of investment, we included change in organizational growth stage as a proxy control variable for the venture’s overall performance during an angel investor’s post-investment phase. Like Wiltbank et al. (2009), we assume five growth stages from seed to buyout.

Lastly, the type of the largest investor in the follow-up investment controls for valuation effects at the second point of investment that can arise from different investor types. It is known that angel investors and VCFs assess value differently and hence arrive at different valuation levels (Hsu 2004; Collewaert and Manigart 2016). Strategic investors presumably pay a premium on valuation due to their potential to realize additional synergies.

4.5 Data quality considerations

As the data for this study were collected with a single survey, there might be a risk of common method variance. To reduce this risk, we took several measures. First, we were very thorough in our questionnaire design. The online survey displays distinct pages, each with a focus on individual constructs and measures. Established constructs were used to capture the main variables. They were arranged in such a way as to reduce to a minimum the risk of direct connections with presumably desirable outcomes. Prior to and during the survey, we repeatedly assured the BAs of the highly confidential treatment of the provided personal data. We also highlighted the importance of veritable answers for a successful outcome of the study. Ultimately, Harman’s single-factor test, an unrotated exploratory factor analysis restricted to one factor, was performed. The extracted single factor accounted for only 36% of total variance. The introduction of a common latent factor during the factor analysis revealed a minor risk of common method variance, which has been addressed by imputing it into the study’s data. Based on these measures and findings, the risk of common method and self-selection biases can be regarded as considerably low.

5 Findings

Table 2 reports the means, standard deviations, and Pearson correlations for all variables. Despite fairly high intercorrelations among the independent effectuation variables (between 29 and 47), the risk of multicollinearity is considerably low, given a maximum variance inflation factor of 1.90 among all variables. Furthermore, eliminating individual predictor variables from the regression model did not result in an increased significance of the remaining predictor constructs.

Apart from a fairly strong correlation between the two experience control variables, the growth proxy variable correlates significantly with venture age and the time to follow-up financing, which is not very surprising.

In the regression analysis, two models were investigated; one baseline model incorporating only the control variables, and one effectuation model to which the four effectuation dimensions were added. Both models were analyzed using hierarchical ordinary least squares regression with standardized values. The baseline model yields an R 2 value of 0.23; the effectuation model yields an R 2 value of 0.39. Both models are significant at the 0.05 level (F = 2.41; p < 0.05) and the 0.001 level (F = 3.20; p < 0.001), respectively. Table 3 reports the results of the regression analysis for both models.

Amongst the control variables, only the new economy dummy has a positive and significant relationship with valuation increase in the baseline model. This effect hardly changes after introducing the independent predictor variables in the effectuation model. In the effectuation model, the controls of investor involvement and second-round lead investor show an association with valuation increase, significant at the 0.05 level. This was expected and is in line with our earlier argumentation. In contrast to the findings of earlier studies, all other controls do not have a significant relationship with the development of the venture’s valuation as an outcome of the angel’s early stage investment activity.

For the independent variables in the effectuation model, only the dimension of means-orientation shows a strong and significant relationship with valuation increase (β = 0.46, p < 0.001), while all other effectuation dimensions’ effects are insignificant. Since the effectuation items were measured on a bipolar scale against causation principles, this positive effect (β > 0) implies that a focus on the effectual principle rather than on the causal principle has a positive effect on the observed dependent variable. A negative effect (β < 0) would have implied that a preference for effectuation actually has a detrimental effect, which is not the case in this observation. Focusing on available means and leveraging them for the most desirable and achievable outcome is therefore highly beneficial for early-stage angel investors if they want to increase the valuation of their investee businesses. All other predictors, however, do not only show very weak effects, they are also not significant and hence do not explain a change in the venture’s valuation. Hypothesis 1 can therefore be confirmed, while all other hypotheses have to be rejected.

6 Discussion

6.1 Effectuation and valuation increase

This study was conducted to shed light on the under-researched post-investment phase of BA investments. It aimed to advance our understanding of whether an angel investor’s decision-making style has any observable effects on their investment’s outcomes. Based on theory from the fields of entrepreneurship and entrepreneurial finance, informal angel investors and entrepreneurs share important traits in their thinking and acting. By applying the entrepreneurial decision-making concept of effectuation to the angel investor’s pre- and post-investment behavior, this study shows empirically how BAs can add traceable value to their investee businesses. In particular, we observe that the effectual principle of means-orientation is a strong driver for the development of a venture’s valuation after an angel’s initial investment. An emphasis on means-orientation, the starting point of the entrepreneurial process itself (Sarasvathy 2001), evidentially plays an important role also in the early-stage investment setting. Being aware of one’s available means in terms of personal traits, knowledge, and contacts as well as of the means available in the investee business and using these to achieve the best possible outcome is a recommendable approach for BAs' active involvement in their ventures. Our study furthermore empirically confirms the positive influence of the much discussed and presumed value of BAs’ “hands-on” attitude (Gaston 1989; Shepherd and Zacharakis 2001; Mason and Harrison 2002).

Hypotheses 2, 3, and 4 could not be confirmed as the analysis did not show any robust effects of the three other effectual principles (affordable loss, partnerships, leveraging contingencies) on valuation increase. To discuss the lack of effect, one has to revert to each dimension’s initial context in effectuation theory and take another precise look at the angels’ early post-investment phase context.

The effectual affordable loss principle stands in contrast to the causal expected return principle and refers to the attitude towards risk and resources (Sarasvathy 2001). Expert entrepreneurs have been shown to apply the affordable loss principle to limit their downside risk (Dew et al. 2009). From the perspective of an entrepreneur, it makes perfect sense to ponder carefully how many and where to dedicate one’s limited resources. After all, entrepreneurs’ personal well-being strongly depends on the development of their venture, and they are affected directly and severely if their company and basis of existence fail. BAs—even though financial motives do play a role—invest to a large extent because they enjoy becoming involved (Morrissette 2007). Furthermore, they are mostly wealthy individuals and only invest a small portion of their wealth into the risky asset class of early-stage ventures (Prowse 1998). In this context—and considering the missing effect in this study—applying the affordable loss principle to reduce risk does not appear to be that important for BAs trying to create additional value for their investments. In addition, many angels are not even able to quote an expected or target return (Morrissette 2007). Hence, the corresponding causal principle does not seem to play an important role either. In sum, these considerations might explain the insignificance in the second dimension.

Regarding their attitude towards outsiders, expert entrepreneurs have been shown to partner with them rather than consider them as competition (Dew et al. 2009). As shown by this study and other explorative literature, BAs focus on adding value with their own hands-on involvement and by committing time and resources to the venture (Politis 2008). With their network already part of their available means (Sarasvathy 2001), angels might not need to focus on outsiders (i.e., strangers) that much to build new partnerships or fight off competitors in order to add direct value to their investments. Against this background, it seems plausible that neither an angel’s emphasis on building new partnerships nor competition have a significant effect on value creation in the post-investment phase.

Of the rejected hypothesized effects, the one for leveraging contingencies appears to be most surprising. To follow up on Dew et al. (2009), overcoming the unexpected can be understood as a truly proactive approach of expert entrepreneurs aiming to create value. Instead of the causal reactive approach of avoidance and overcoming, the effectual entrepreneur imaginatively rethinks, continuously transforms, and therefore creates and opens up new opportunities for growth and value creation (Dew et al. 2009). An angel investor with the same mindset would hence be expected to amplify the startup’s value creation process. This study’s results, however, tell a different story. Apparently, neither an emphasis on leveraging nor an emphasis on avoiding contingencies turns out to have a significant effect on value creation. In other words: the development of a venture’s valuation appears as somewhat independent from its angel investor’s approach towards unforeseen events.

The bottom line for this study is that an angel investor should ideally pursue an effectual means-orientation approach to foster the entrepreneurial process when contributing to an investee business in the early post-investment phase. This approach positively influences the valuation development of investee businesses.

6.2 Theoretical and practical implications

By linking entrepreneurial decision-making patterns of angel investors to a new and valuation-based early post-investment success measure for venture performance, this study complements the fields of entrepreneurship research in general and those of venture capital literature in particular. Despite the strong academic interest in early-stage financing processes, most studies have focused on the institutional venture capital side; Nofsinger and Wang (2011) state that, compared to research on VCFs, only few studies have examined angel investors. BAs, however, differ in some respects quite substantially from VCFs. We hence need to understand better the informal side of early-stage financing. Over the past decade, interest in behavioral perspectives in venture capital research has risen. Research, initiated by Shepherd et al. (2000), pondered the question of how early-stage investors can manage the higher risks related to this asset class. Given this development, it is surprising that studies have largely neglected angel investors. In this context, Paul et al. (2007) explicitly note that research on the informal investors’ decision-making could improve our understanding of the venture financing market. However, only very little work on that very aspect has been published so far; recently, Collewaert and Manigart (2016) have described the persistent lack of behavioral angel studies. This study addresses this gap by providing the first comprehensive approach to investigating BAs’ behavior and their decision-making patterns from an entrepreneurial perspective. It thus contributes empirical insights advancing our understanding of the effects of angels’ strategy when addressing and managing entrepreneurial uncertainty in the early-stage financing context.

BAs represent more than mere financial investors: they also act as entrepreneurial decision-makers. Hence, the application of effectuation to the field of informal early-stage investors and early-stage financing furthermore advances effectuation theory itself as well as the field of venture capital research. As an emerging theory, effectuation has quickly caught broad attention since it was first proposed by Sarasvathy (2001). In the process of theory advancement, empirical testing, however, has so far largely been limited to founder-focused cases. Despite calls to sample more “subjects who are representative of the individuals who are in the process of starting businesses” (Perry et al. 2012, p. 849) and to investigate effectuation dimensions as a predictor of performance (Chandler et al. 2011; Perry et al. 2012), only Wiltbank et al. (2009) have applied this theory to an early-stage financing and performance context. Wiltbank et al.’s (2009) work, however, only examines the effectual dimension of control versus prediction, covering only a small fraction of the total concept. In contrast, this study provides the first comprehensive analysis of all identified effectual decision-making dimensions as outlined by Dew et al. (2009) in the so far mostly unobserved context of entrepreneurial opportunity creation. We thus validate a recent approach to measure effectual decision-making dimensions (Brettel et al. 2012). In addition, this study responds to the latest calls in prominent reviews and discussions to contribute to the evolvement and establishment of the emerging entrepreneurial effectuation theory (Fisher 2012; Perry et al. 2012; Arend et al. 2015; Welter et al. 2016).

Ultimately, this study complements the ongoing debate on measuring angels’ post-investment success. Not only does it shed light on the early post-investment phase of informal investors, which has largely remained a white spot on the landscape of venture capital research (Large and Muegge 2008; Politis 2008; Collewaert and Sapienza 2014). The study also contributes to the recent evolvement of developing venture valuation as an objective early-stage success measure (Collewaert and Manigart 2016; Röhm et al. 2017). Incorporating earlier work from the private equity buyout context (Meier et al. 2006), this study defines valuation increase as a new type of early post-investment success measure, which appears to be particularly appropriate in the setting of angel investments. In doing so, this study is furthermore among the first to add empirical evidence to the unresolved dispute on how angel investor activity promotes the post-investment value creation in investee businesses (Chemmanur and Chen 2002; Fairchild 2011).

Linking to the recommendations for practitioners, this study also complements recent theoretical considerations on investor choice and early firm growth as in Schwienbacher (2013), who postulates that “understanding this impact [on follow-up rounds], however, is crucial from the perspective of entrepreneurs for whom involvement and sufficient resources in early stages may help ensure future growth opportunities of the venture” (Schwienbacher 2013, p. 530). This study’s key take-away for practitioners is that certain investor behaviors, manifested in the decision-making pattern of means-orientation, can have a positive impact on value appreciation in investee businesses in the early post-investment phase. For angel investors, this implies that pursuing the effectual pattern of means-orientation should clearly be favored over the causal behavior of setting and following predetermined goals. Means-orientation is manifested in starting the entrepreneurial opportunity creation process by focusing on assets and resources directly at one’s disposal. For an angel investor, this can include own skills, knowledge, network, or funds as well as the physical and intangible assets available in the ventures they invest in. Instead of following the causal principle of planning, goal determination, and monitoring, angel investors should take an active part in co-creating the most beneficial outcome, which is achievable with the available means. A preference for this behavioral pattern has been shown to result in a significantly higher appreciation of value in investee businesses. As a strong equity growth-story should also be favored by entrepreneurs, founders in early stages should hence look for investors who display the just outlined behavioral pattern. Especially in angel financing rounds, entrepreneurs, if given the choice, should actively choose investors who show an interest in co-creating opportunities by leveraging their own and the venture’s assets and who actively look for new beneficial outcomes which can be achieved with available means. Angel investors who rather show a strong interest in following plans and monitoring schemes should, in contrast, be treated with caution as they may not be able to contribute as much to the venture’s increase in valuation.

6.3 Limitations and avenues for further research

Like all empirical studies, this work is subject to limitations, especially because the data were obtained from informal angel investors. As outlined earlier, there is a certain risk of certain biases, a non-response bias and a self-selection bias in particular. Although several measures have been taken to reduce the risk of common method and self-selection biases, the results of this study should be interpreted taking into account its limitations. It relies on self-reported data originating from angel investors in the DACH area. Hence, the conclusions drawn from this study—especially with regard to the reported valuations (e.g., compared to valuations in the Anglo-Saxon world, which are typically higher)—must be treated carefully, always bearing in mind its setting and context. To address these issues, future angel research should attempt to validate data by gathering information from both the investor and the company perspective. Ideally, future angel research should also be conducted in international settings, which allows for a comparison of different cultures. Another limitation is the study’s sample size. Although a sample size of 73 responses is not uncommon in angel and new venture research, a larger sample would have been desirable. Future research should hence invest considerable time in building larger high quality, responsive, traceable, and representative samples. The effort necessary to generate such a sample should not be underestimated. While this study applied a one-investment-case approach per respondent to increase response rates and response accuracy, it still represents a potential source of selection bias. To avoid such a risk and to improve our understanding of investment performance over the entire holding period, future research should attempt to gather data not only on one investment, but ideally on angels’ entire portfolio. Furthermore, data should be collected not only for the first follow-up financing round, but for all subsequent financing rounds. While that approach will require researchers to work closely and intensely together with a large group of BAs, probably over several years, and hence entails substantial challenges and efforts, it will result in a very valuable, detailed, representative, and longitudinal picture of venture valuation in BAs’ post-investment phases. This study confirms that a certain behavioral pattern of investors leads to early-stage investment success in a very specific context. Our study presents a first step in understanding and quantifying how angel investors sustainably promote their investee businesses. Empirically delineating angel investor pre- and post-investment activity and their interactions with founders and other stakeholders still bears substantial research potential. Ultimately, future works might connect each of these activities to antecedents and organizational outcomes.

References

Aernoudt R (1999) Business angels: Should they fly on their own wings? Ventur Cap 1:187–195. doi:10.1080/136910699295965

Akerlof GA (1970) The market for “lemons”: quality uncertainty and the market mechanism. Q J Econ 84:488–500. doi:10.2307/1879431

Appelhoff D, Mauer R, Collewaert V, Brettel M (2016) The conflict potential of the entrepreneur’s decision-making style in the entrepreneur-investor relationship. Int Entrep Manag J 12:601–623. doi:10.1007/s11365-015-0357-4

Arend R, Sarooghi H, Burkemper A (2015) Effectuation as ineffectual? Applying the 3E theory-assessment framework to a proposed new theory of entrepreneurship. Acad Manag Rev 40:630–651. doi:10.5465/amr.2014.0455

Avdeitchikova S, Landstrom H, Månsson N (2008) What do we mean when we talk about business angels? Some reflections on definitions and sampling. Ventur Cap 10:371–394. doi:10.1080/13691060802351214

Baker T, Nelson RE (2005) Creating something from nothing: resource construction through entrepreneurial bricolage. Adm Sci Q 50:329–366. doi:10.2189/asqu.2005.50.3.329

Basse-Mama H, Koch N, Bassen A, Bank T (2013) Valuation effects of corporate strategic transactions in the cleantech industry. J Bus Econ 83:605–630. doi:10.1007/s11573-013-0665-5

Brettel M (2002) German business angels in international comparison. J Priv Equity 5:53–67. doi:10.3905/jpe.2002.320008

Brettel M (2003) Business angels in Germany: a research note. Ventur Cap 5:251–268. doi:10.1080/1369106032000122095

Brettel M, Mauer R, Engelen A, Küpper D (2012) Corporate effectuation: entrepreneurial action and its impact on R&D project performance. J Bus Ventur 27:167–184. doi:10.1016/j.jbusvent.2011.01.001

Brush CG, Edelman LF, Manolova TS (2012) Ready for funding? Entrepreneurial ventures and the pursuit of angel financing. Ventur Cap 14:111–129

Bygrave W, Timmons J (1992) Venture capital at the crossroads. Harvard Business School, Boston

Chandler GN, Hanks SH (1993) Measuring the performance of emerging businesses: a validation study. J Bus Ventur 8:391–408. doi:10.1016/0883-9026(93)90021-V

Chandler GN, DeTienne DR, McKelvie A, Mumford TV (2011) Causation and effectuation processes: a validation study. J Bus Ventur 26:375–390. doi:10.1016/j.jbusvent.2009.10.006

Chemmanur TJ, Chen Z (2002) Angels, venture capitalists, and entrepreneurs: a dynamic model of private equity financing. Bost Coll Unpubl Manuscr 1:54. doi:10.2139/ssrn.342721

Collewaert V, Manigart S (2016) Valuation of angel-backed companies: the role of investor human capital. J Small Bus Manag 54:356–372. doi:10.1111/jsbm.12150

Collewaert V, Sapienza HJ (2014) How does angel investor-entrepreneur conflict affect venture innovation? It depends. Entrep Theory Pract 40:573–597. doi:10.1111/etap.12131

Damodaran A (2016) Price earnings multiples [.xlsx file download]. http://www.stern.nyu.edu/~adamodar/New_Home_Page/data.html. Accessed 07 February 2016

Davidsson P (2008) Interpreting performance in entrepreneurship research. In: Davidsson P (ed) The entrepreneurship research challenge. Elgar, Cheltenham

De Clercq D, Fried VH, Lehtonen O, Sapienza HJ (2006) An entrepreneur’s guide to the venture capital galaxy. Acad Manag Perspect 20:90–113. doi:10.5465/AMP.2006.21903483

Dew N, Read S, Sarasvathy SD, Wiltbank R (2009) Effectual versus predictive logics in entrepreneurial decision-making: differences between experts and novices. J Bus Ventur 24:287–309. doi:10.1016/j.jbusvent.2008.02.002

Ehrlich SB, De Noble AF, Moore T, Weaver RR (1994) After the cash arrives: a comparative study of venture capital and private investor involvement in entrepreneurial firms. J Bus Ventur 9:67–82. doi:10.1016/0883-9026(94)90027-2

Fairchild R (2011) An entrepreneur’s choice of venture capitalist or angel-financing: a behavioral game-theoretic approach. J Bus Ventur 26:359–374. doi:10.1016/j.jbusvent.2009.09.003

Fisher G (2012) Effectuation, causation, and bricolage: a behavioral comparison of emerging theories in entrepreneurship research. Entrep Theory Pract 36:1019–1051. doi:10.1111/j.1540-6520.2012.00537.x

Garbotz C, Engelen A, Niemann P (2010) A social network perspecitve on the deal flow of business angels. In: Academy of Management Annual Meeting Proceedings. pp 1–6

Gaston RJ (1989) Finding private venture capital for your firm: a complete guide. Wiley, New York

Gupta AK, Sapienza HJ (1992) Determinants of venture capital firms’ preferences regarding the industry diversity and geographic scope of their investments. J Bus Ventur 7:347–362. doi:10.1016/0883-9026(92)90012-G

Haagen F (2008) The role of smart money: what drives venture capital support and interference within biotechnology ventures? Zeitschrift für Betriebswirtschaft 78:397–422. doi:10.1007/s11573-008-0023-1

Harrison RT, Mason CM (1992) International perspectives on the supply of informal venture capital. J Bus Ventur 7:459–475. doi:10.1016/0883-9026(92)90020-R

Hsu DH (2004) What do entrepreneurs pay for venture capital affiliation? J Finance 59:1805–1844. doi:10.1111/j.1540-6261.2004.00680.x

Jain B (2001) Predictors of performance of venture capitalist-backed organizations. J Bus Res 52:223–233. doi:10.1016/S0148-2963(99)00112-5

Klobucnik J, Sievers S (2013) Valuing high technology growth firms. J Bus Econ 83:947–984. doi:10.1007/s11573-013-0684-2

Lahti T (2011) Categorization of angel investments: an explorative analysis of risk reduction strategies in Finland. Ventur Cap 13:49–74. doi:10.1080/13691066.2010.543322

Large D, Muegge S (2008) Venture capitalists’ non-financial value-added: an evaluation of the evidence and implications for research. Ventur Cap 10:21–53. doi:10.1080/13691060701605488

Mason CM, Harrison RT (1992) The supply of equity finance in the UK: a strategy for closing the equity gap. Entrep Reg Dev 4:357–380. doi:10.1080/08985629200000020

Mason CM, Harrison RT (1995) Closing the regional equity capital gap: the role of informal venture capital. Small Bus Econ 7:153–172. doi:10.1007/BF01108688

Mason CM, Harrison RT (1996) Informal venture capital: a study of the investment process, the post-investment experience and investment performance. Entrep Reg Dev 8:105–126. doi:10.1080/08985629600000007

Mason CM, Harrison RT (2002) Is it worth it? The rates of return from informal venture capital investments. J Bus Ventur 17:211–236. doi:10.1016/S0883-9026(00)00060-4

Maxwell AL, Lévesque M (2014) Trustworthiness: a critical ingredient for entrepreneurs seeking investors. Entrep Theory Pract 38:1057–1080. doi:10.1111/j.1540-6520.2011.00475.x

Maxwell AL, Jeffrey SA, Lévesque M (2011) Business angel early stage decision making. J Bus Ventur 26:212–225. doi:10.1016/j.jbusvent.2009.09.002

Meier D, Hiddemann T, Brettel M (2006) Wertsteigerung bei buyouts in der post investment-phase-der beitrag von private equity-firmen zum operativen erfolg ihrer portfoliounternehmen im europäischen vergleich. Zeitschrift für Betriebswirtschaft 76:1035–1066. doi:10.1007/s11573-006-0050-8

Morrissette SG (2007) A profile of angel investors. J Priv Equity 10:52–66. doi:10.3905/jpe.2007.686430

Nofsinger JR, Wang W (2011) Determinants of start-up firm external financing worldwide. J Bank Financ 35:2282–2294. doi:10.1016/j.jbankfin.2011.01.024

Oetker R (2003) Erfahrungen mit innovativen start-ups aus sicht eines business angels. In: Albach H, Pinkwart A (eds) Von der gründung bis zur insolvenz erfahrungen von start-up-unternehmen. Gabler Verlag, Wiesbaden, pp 85–93

Paul S, Whittam G, Wyper J (2007) Towards a model of the business angel investment process. Ventur Cap 9:107–125. doi:10.1080/13691060601185425

Perry JT, Chandler GN, Markova G (2012) Entrepreneurial Effectuation: a review and suggestions for future research. Entrep Theory Pract 36:837–861. doi:10.1111/j.1540-6520.2010.00435.x

Politis D (2008) Business angels and value added: what do we know and where do we go? Ventur Cap 10:127–147. doi:10.1080/13691060801946147

Prowse S (1998) Angel investors and the market for angel investments. J Bank Financ 22:785–792. doi:10.1016/S0378-4266(98)00044-2

Read S, Sarasvathy SD (2005) Knowing what to do and doing what you know. J Priv Equity 9:45–62. doi:10.3905/jpe.2005.605370

Read S, Song M, Smit W (2009) A meta-analytic review of effectuation and venture performance. J Bus Ventur 24:573–587. doi:10.1016/j.jbusvent.2008.02.005

Riding A (2008) Business angels and love money investors: segments of the informal market for risk capital. Ventur Cap 10:355–369. doi:10.1080/13691060802351222

Röhm P, Köhn A, Kuckertz A, Dehnen HS (2017) A world of difference? The impact of corporate venture capitalists’ investment motivation on startup valuation. J Bus Econ. doi:10.1007/s11573-017-0857-5

Sapienza HJ (1992) When do venture capitalists add value? J Bus Ventur 7:9–27. doi:10.1016/0883-9026(92)90032-M

Sarasvathy SD (2001) Causation and effectuation: toward a theoritical shift from economic inevitability to entrepreneurial contingency. Acad Manag Rev 26:243–263. doi:10.2307/259121

Schwienbacher A (2013) The entrepreneur’s investor choice: the impact on later-stage firm development. J Bus Ventur 28:528–545. doi:10.1016/j.jbusvent.2012.09.002

Shane S, Venkataraman S (2000) The Promise of Entrepreneurship as a Field of Research. Acad Manag Rev 25:217–226. doi:10.2307/259271

Shepherd DA, Zacharakis A (2001) The venture capitalist-entrepreneur relationship: control, trust and confidence in co-operative behaviour. Ventur Cap 3:129–149. doi:10.1080/13691060110042763

Shepherd DA, Douglas EJ, Shanley M (2000) New venture survival. J Bus Ventur 15:393–410. doi:10.1016/S0883-9026(98)00032-9

Sørheim R (2003) The pre-investment behaviour of business angels: a social capital approach. Ventur Cap 5:337–364. doi:10.1080/1369106032000152443

Sørheim R (2005) Business angels as facilitators for further finance: an exploratory study. J Small Bus Enterp Dev 12:178–191. doi:10.1108/14626000510594593

Van Osnabrugge M (2000) A comparison of business angel and venture capitalist investment procedures: an agency theory-based analysis. Ventur Cap 2:91–109. doi:10.1080/136910600295729

Vanacker T, Collewaert V, Paeleman I (2013) The relationship between slack resources and the performance of entrepreneurial firms: the role of venture capital and angel investors. J Manag Stud 50:1070–1096. doi:10.1111/joms.12026

Welter C, Mauer R, Wuebker R (2016) Bridging behavioural models and theoretical concepts: effectuation and bricolage in the opportunity creation framework. Strateg Entrep J 10:5–20. doi:10.1007/s13398-014-0173-7.2

Wetzel W (1983) Angels and informal risk capital. Sloan Manage Rev 24:23–34

Wiltbank R, Read S, Dew N, Sarasvathy SD (2009) Prediction and control under uncertainty: outcomes in angel investing. J Bus Ventur 24:116–133. doi:10.1016/j.jbusvent.2007.11.004

Author information

Authors and Affiliations

Corresponding author

Ethics declarations

Conflict of interest

The authors declare they have no conflict of interest.

Appendix A: Information on effectuation construct

Appendix A: Information on effectuation construct

Effectuation (Brettel et al. 2012)—pretested, adapted wording, translated to German for survey and re-translated to English for report | ||

|---|---|---|

Please indicate on a scale from 1 to 7 with which of the following statements you agree more (fully agree with statement 1 = 1, fully agree with statement 2 = 7) when you think about your activity as investor and active business angel | ||

Dimension 1: Means-orientation (a = 0.91; CR = 0.91; AVE = 0.68) | ||

1: Causal Statements (goal orientation) | 2: Effectual Statements (means orientation) | |

Item (1) | My decisions are based on given targets | I reach decisions on the basis of given resources |

Item (2) | The goal of my investments is clearly defined from early on | The targets of my investments are vaguely defined in the beginning |

Item (a) | Starting point of my activity is concisely given targets | Starting point of my activity is available resources |

Item (4) | Starting with given targets, the required means/resources were defined | I define targets based on available resources |

Item (5) | A clearly defined goal is the starting point for my investment activity | Available resources are much rather the starting point for my activity than concisely defined target |

Item (6) | Precise targets strongly influence the scope of my investment activity | Available resources strongly influence the scope of my investment activity |

Dimension 2: Affordable loss (a = 0.88; CR = 0.89; AVE = 0 0.66) | ||

|---|---|---|

1: Causal Statements (expected return) | 2: Effectual Statements (affordable loss) | |

Item (1) | Decisive for the selection of my investments are considerations about potential returns | Decisive for the selection of my investments are considerations about potential losses. |

Item (2) | The selection of my investments is mostly based on calculations of potential returns | The selection of my investments is mostly based on risk reduction (i.e. limitation of costs) |

Item (3) | I mainly consider the potential chances of an investment | I mainly consider the potential risk of an investment |

Item (a) | My investment volumes are primarily based on potential returns | My investment volumes are primarily based on potential losses |

Dimension 3: Partnerships (a = 0.92; CR = 0.92; AVE = 0. 79) | ||

|---|---|---|

1: Causal Statements (competitive analysis) | 2: Effectual Statements (partnerships) | |

Item (1) | I try to identify risks thorough market analyses | I try to reduce risks of investments through internal or external partnerships and agreements |

Item (2) | I reach decisions on the basis of systematic market analyses | I jointly make decisions together with partners/stakeholders on the basis of our competences |

Item (a) | My focus is rather on the early identification of risks through market analyses in order to be able to adopt my approach | My focus is rather on the reduction of risks by approaching potential partners and customers |

Item (4) | In order to reduce risks, I focus on market analyses and forecasts | In order to reduce risks, I start partnerships and receive early pre-commitments |