Abstract

Purpose

The purpose of this study is to provide an integrated method to identify the resource consumption, environmental emission, and economic cost for mechanical product manufacturing from economic and ecological dimensions and ultimately to provide theoretical and data support of energy conservation and emission reduction for mechanical product manufacturing.

Methods

The applied research methods include environmental life cycle assessment (LCA) and life cycle cost (LCC). In life cycle environmental assessment, the inventory data are referred from Chinese Life Cycle Database and midpoint approach and EDIP2003 and CML2001 models of life cycle impact assessment (LCIA) are selected. In life cycle cost assessment, three cost categories are considered. The proposed environment and cost assessment method is based on the theory of social willingness to pay for potential environmental impacts. With the WD615 Steyr engine as a case, life cycle environment and cost are analyzed and evaluated.

Results and discussion

The case study indicates that, in different life cycle phases, the trend of cost result is generally similar to the environmental impacts; the largest proportion of cost and environmental impact happened in the two phases of “material production” and “component manufacturing” and the smallest proportion in “material transport” and “product assembly.” The environmental impact category of Chinese resource depletion potential (CRDP) accounted for the largest proportion, followed by global warming potential (GWP) and photochemical ozone creation potential (POCP), whereas the impacts of eutrophication potential (EP) and acidification potential (AP) are the smallest. The life cycle “conventional cost” accounted for almost all the highest percentage in each phase (except “material transport” phase), which is more than 80% of the total cost. The “environmental cost” and “possible cost” in each phase are relatively close, and the proportion of which is far below the “conventional cost.”

Conclusions

The proposed method enhanced the conventional LCA. The case results indicate that, in a life cycle framework, the environment and cost analysis results could support each other, and focusing on the environment and cost analysis for mechanical product manufacturing will contribute to a more comprehensive eco-efficiency assessment. Further research on the life cycle can be extended to phases of “early design,” “product use,” and “final disposal.” Other LCIA models and endpoint indicators are advocated for this environmental assessment. Environmental cost can also be further investigated, and the relevant social willingness to pay for more environmental emissions is advocated to be increased.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

Mechanical manufacturing industry is an important pillar of the economy of China. With the development of economy and technology, this industry should undertake ever-increasing environmental problems. Nowadays, energy consumption and pollutant emissions continue to increase, and environmental conditions are becoming more aggravated (Xu and Lin 2017; Al-Ayouty et al. 2017; Kucukvar et al. 2016). In addition, considering the resource and environmental constraints, the “high cost” time is coming, the costs of land, raw materials, labor, and energy, among others, are on the rise, and the sustainable development of the mechanical product manufacturing industry is facing huge challenges.

The improvement of eco-efficiency has become the practical way for the sustainable development of the mechanical product manufacturing industry. The eco-efficiency analysis (EEA) method proposed by BASF, a chemical firm, is a well-known quantitative tool used to provide life cycle assessment (LCA) for products or processes with regard to the environmental impact and cost-effectiveness (Landsiedel and Saling 2002; Saling et al. 2002; Saling et al. 2005; Uhlman and Saling, 2010). The method has been conducted in more than 600 studies (BASF 2015), e.g., the applications of environment and cost assessment for chemical processes and products (Shonnard et al. 2003) and the comparison of conventional polyol production with polyol manufacturing routes that utilize renewable or natural oils (Uhlman and Saling 2010). However, the method has some inevitable limitations, such as the violation of the well-founded rationality axiom independence from irrelevant alternatives, as discussed by Dyckhof et al. (2015), or stakeholders of eco-efficiency studies “are not as well versed in many of the common units of measurements” due to “not be able to adequately assess the relative significance of the measured impacts” as Saling (2015) mentioned. Nevertheless, EEA still seemed to be an effective method for the precise assessment procedure of ecological performance measurement.

In recent years, LCA and life cycle cost (LCC) have been developed as the effective and operative tools to evaluate the eco-efficiency of the product life cycle. The literature has presented some examples by combining LCA and LCC to product evaluations from economic and ecological dimensions. Typical applications of the LCA and LCC integration were used by several researchers. For example, Mistry et al. (2016) conducted potential environmental impacts and reinforced the structure of the net present cost of the stainless steel through the combination of LCA and LCC. Lee et al. (2010) identified the environmental and economic aspects of the wind–hydrogen system using LCA and LCC methodologies. Luo et al. (2009) conducted environmental and economic analyses of the Brazilian ethanol industries, which are of crucial importance based on the theories of LCA and LCC. Islam et al. (2015) described LCA and life cycle cost analysis for typical Australian houses. Chiesa et al. (2016) performed the life cycle environmental impact and environmental LCC assessment for three different high-efficiency residential pellet boilers manufactured by an Austrian company. Kjær et al. (2015) proposed an environmental and economic input–output model, which avoided cut-offs in the LCA; this model was used to verify the efficacy of a tanker ship. Bovea and Vidal (2004) proposed a model to add value to a product by means of the integration of environment, cost, and customer valuation during the design process. Kim et al. (2011) evaluated the food waste disposal options by LCC analysis from the perspective of global warming and energy and/or resource recovery. Tapia et al. (2008) conducted an environmental, financial, and quality assessment of six alternative processes of drinking water processes based on LCA and LCC theories. Barrios et al. (2008) performed LCA and LCC theories to an environmental and financial impact assessment of an existing water treatment facility. Lindahl et al. (2014) quantified environmental and economic benefits of the Integrated Product Service Offering in real practice from a life cycle perspective using LCA and LCC. Ristimäki et al. (2013) analyzed LCC and carbon emissions of a district energy system for a new residential development in Finland. Heijungs et al. (2013) provided an explicit and transparent description of how to calculate the life cycle cost. Further studies on LCC and LCA integrations have been introduced (Senthil et al. 2003; Hoogmartens et al. 2014; Ferreira et al. 2014; Cerria et al. 2014; Norris 2001; Kannan et al. 2004), but these studies were not detailed.

Although fruitful results have been achieved in LCC and LCA integration, the applications are not comprehensive enough and are rarely applied to mechanical product manufacturing in China. However, large resource consumption, environmental emission, and economic cost are generated in the process of mechanical product manufacturing, and the effective and accurate evaluation method is not available by now. To overcome the research gap, this study proposed an integrated environment and cost assessment method by employing LCC and LCA for mechanical product manufacturing. The aims of the present study are to examine and identify the resource consumption, environmental emission, and economic cost for mechanical product manufacturing process; to ultimately provide theoretical and data support of energy conservation and emission reduction for more environmental-friendly and cost-effective measures; and by focusing on the environment and cost analysis in the mechanical product manufacturing process, to contribute to a comprehensive assessment of eco-efficiency.

2 Integrated method of life cycle cost and environmental assessment

2.1 Research methods

In this study, the applied research methods include environmental LCA and LCC. The former is used for environmental assessments, whereas the latter is for purely economic assessments. LCA quantifies and evaluates the environmental impacts throughout the whole life cycle of industrial system or product through the “cradle to grave” approach. LCA contains four phases: goal and scope definition, life cycle inventory (LCI) analysis, life cycle impact assessment (LCIA), and interpretation (ISO 14044 international standard 2006). LCC refers to the costs incurred in the product life cycle, and the aim of LCC analysis is to provide a comprehensive evaluation of product cost, reduce the life cycle cost, and improve the product performance.

Referred to the standard of ISO 14045 international standard 2012 for Eco-efficiency assessment of product systems, the environment and cost calculation method presented in this study is based on potential environmental impacts, and the theory of social willingness to pay is a useful innovation to life-cycle cost analysis.

2.2 Objective and scope

2.2.1 Objective

The objective of this study is to qualify and quantify the energy and material consumption, environmental emission, and economic cost of mechanical product manufacturing process; to identify the main types of life cycle environmental impact and cost in different phases; and to propose effective measures of energy saving, emission reduction, and cost minimization.

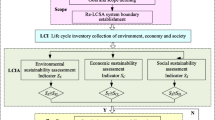

2.2.2 System boundary

Generally, the entire life cycle is usually “from cradle to grave.” In this study, the system boundary is restricted to the product manufacturing phases, and the relevant life cycle mainly includes material production (MA), material transport (MT), component manufacturing (CM), product assembly (PA), and product sale (PS), whereas the two phases of use and disposal are not relevant. The system boundary is shown in Fig. 1.

The system boundary of this integrated method based on LCA and LCC

2.3 Life cycle inventory (LCI)

2.3.1 Environmental LCI

The environmental LCI data of mechanical product mainly include raw materials (steel, alloy, and rubber, to name a few), energy (electricity, natural gas, diesel, and coal), and environmental emissions (CO2, SO2, CO, CH4, dust, and other forms of exhaust waste).

2.3.2 Life cycle cost inventory

The cost includes material cost, energy fee, labor, depreciation cost, transport, office, management expenses, sales expenses, personnel injury, pollutant removal, and fines, among others. However, the cost should also include environmental costs. Although comprehensive evaluation for a particular product is difficult, in this study, an environmental cost calculation method based on the potential environmental impacts and social willingness to pay is proposed, in which the environmental cost is quantified by the environmental input, output, and environmental currency payment intention for a given product or system.

2.4 Life cycle impact assessment

2.4.1 Life cycle environmental impact

The life cycle impact assessment (LCIA) attempts to link LCI data to the potential environmental impacts. In LCIA, midpoint approach is used to illustrate the environmental impact because of the strong scientific robustness of the midpoint indicators (Bare et al. 2000), and the EDIP2003 and CML2001 models are selected. According to UNEP/SETAC (2011), LCIA should include at least three steps, namely, classification, characterization, and normalization.

Classification: LCI results are organized into relevant impact categories. The selection of LCIA categories depends on the main substances of recourse consumption and waste emission in LCI. According to EDIP2003, CML2001, and IPCC2007, the main LCIA categories include Chinese resource depletion potential (CRDP), global warming potential (GWP), eutrophication potential (EP), acidification potential (AP), photochemical ozone creation potential (POCP), ozone depletion potential (ODP), and human toxicity (HT), among others. What needs illustration is that, CRDP is not a common resource depletion factor, it is expressed as ADP index divided by the self-sufficiency rate of the resource in China, and the resource characteristic factors are indicated by the substance of “antimony” (USGS Minerals Yearbook 2005; China nonferrous metal industry yearbook 2006). CRDP is often used to describe the scarcity of resources in China.

Characterization: The potential contribution of different pollutants to an environmental impact category is calculated. The characterization factors in this study are based on GB/T2589-2008, IPCC2007/2002, and CML 2002 (de Bruijn et al. 2002), supposing that the environmental impact potential is expressed as S, which is given by Eq. (1):

where Sk is the kth environmental impact potential result, Qi is the quantity of the ith substance emission, and EP (i) is the characterization factor of the ith substance.

Normalization: Environmental impact potential is quantified according to the standard of the selected environmental impact equivalent year, which provides a unified comparison standard of different environmental impact potentials. In this study, normalization factor is adapted from Wenzel et al. (1997). Based on the assumption that the normalization result is expressed by N, the calculated method is shown in Eq. (2):

where Nk is the kth environmental impact normalization result and Rk is the normalization factor of the kth environmental impact potential.

2.4.2 Life cycle cost classification

Life cycle cost can be classified by different standards. In this study, based on the work of Leng (2007), three categories of life cycle costs are classified by capital uses: conventional cost (Co1), possible cost (Co2), and environmental cost (Co3). Conventional cost is associated with the common financial debt, including general funding, operating costs, or tax (funds, equipment, labor, and energy supply and use). Possible costs depend on the possibility of future events, which is not directly considered by policymakers, such as personnel injury, removal of pollutants, and unforeseeable management cost. Environmental costs are associated with the impact of human activities on the natural environment. Unlike conventional costs and possible costs, policymakers believe that the environmental cost is the typical intangible costs and cannot be accurate and quantitatively expressed.

Table 1 shows the three cost classifications, in which conventional cost and possible cost can be obtained through company financial accounting. For the environmental cost, this study proposes an analysis method based on the potential environmental impacts and the theory of social willingness to pay (see Sect. 2.4.3).

2.4.3 Environmental cost analysis method

Social willingness to pay is the willingness to pay for a certain amount of money to avoid (or exchange) some kind of change. In this study, the environmental cost is expressed as social paying money for the environmental impacts. The money quantity of social willingness to pay for environmental impact is obtained from Li et al. (2005). Monetary factors of the five main environmental impacts are shown in Table 2, in which only coal, oil, and natural gas are considered in the environmental costs of CRDP, due to the missing environmental monetary factors of metals. Five environmental cost analysis steps are involved, namely:

-

1.

Construction of environmental output matrix, as shown in Eq. (3):

where eij represents the substance quantity of the ith environmental output in the jth unit process, subjected to eij ≥ 0; m is the total number of environmental emissions; and n is the total number of unit processes.

-

2.

Construction of one-order summation matrix, as shown in Eq. (4):

-

3.

Construction of monetary matrix of social willingness to pay, as shown in Eq. (5):

where \( {d}_{i1}^i \) is the monetary factor of social willingness to pay for the ith environmental emission in the jth phase.

-

4.

iv. Creation of future cost value coefficient matrix.

Because of the dynamic and time-varying LCI, capital time value should be considered, and the final cost value coefficient k can be determined by Eq. (6):

where P is the discounted present value, F is the future cost, ic is the benchmark discount rate of the product industry, and n is the time period (unit: year).

Therefore, the future cost value coefficient matrix K can be expressed in Eq. (7):

where \( {k}_i^{t_1+{t}_2+\dots +{t}_j} \) represents the future cost value coefficient of the ith environmental output in the jth phase.

v. Hadamard integration of matrixes E, D, and K is given in Eq. (8), and the calculation of the environmental cost matrix CT is expressed in Eq. (9):

2.5 Result interpretation

The main purpose of this section is to explain and analyze the results of life cycle environment and cost in different phases for mechanical product manufacturing and search for more environmental friend and cost-effective measures.

3 Case study

In this study, a Steyr engine is selected as the case to evaluate the environmental and economic performance of the proposed method. Steyr engines are mature products that are commonly used in heavy-duty trucks in China. Steyr engines account for more than 50% production of China’s heavy-duty vehicle engines, with large recourse consumption and environmental emissions generated in the manufacturing process each year.

3.1 Objective and scope

3.1.1 Research objective

The objective of the study is to analyze the resource consumption, environmental emission, and cost of the Steyr engine manufacturing as well as to qualify and quantify the main environmental impacts and cost in different phases.

3.1.2 Function unit and system boundary

In this study, the functional unit is defined as a “WD615 Steyr engine” produced by Jinan Fuqiang Power Co. Ltd., and the components of the engine include “seven pieces,” namely, cylinder head, cylinder block, connection rod, timing gear box, crankshaft, fly wheel housing, and fly wheel. Other accessories are purchased from providers. The technical parameters of WD615 Steyr engine are shown in Table 3.

The life cycle involves five phases, namely, material production, material transport, component manufacturing, product assembly, and product sale. The system boundary is shown in Fig. 1.

3.2 Life cycle inventory

3.2.1 Life cycle environmental inventory

Material production

Steel, cast iron, aluminum, and alloy constitute the main materials of engine components, including 185.05 kg steel, 594.64 kg cast iron, 41.23 kg aluminum, and 35.32 kg alloy.

Material transport

The main raw material supplier for engine component manufacturing is Shanghai Baosteel Group Corporation. The materials are transported by truck using gasoline fuel, with load of 10 t. The total distance is 880 km, and transportation distance inside the factory is ignored.

Component manufacturing and product assembly

The related data of engine component manufacturing and product assembly are obtained from the company production site, mainly including energy consumption of the “seven pieces” of manufacturing and engine assembly, which have total energy consumption of 2296.21 kWh.

Product sale

The engines are sold separately or along with the heavy truck. They are sold in 4S shops or markets near the provinces. The average distance between Jinan Fuqiang Power Co. Ltd. and the selling spots is 400 km.

3.2.2 Chinese life cycle database

The unit process inventory data of electric power, transportation, raw material production, and environmental emissions are obtained from the Chinese Life Cycle Database (CLCD). CLCD is currently the only publicly available Chinese local LCA database and was developed by Sichuan University and IKE Co. Ltd. The data represent the average Chinese production technology and market. CLCD contains more than 600 types of Chinese life cycle data, such as inventory data of energy consumption, mineral resource consumption, greenhouse gases, acidification, and solid waste, among others. At the same time, CLCD contains the common characteristic factor, China 2005 and 2010 normalized factors, and weighting factor of energy conservation and emission reduction. The LCI data of the engine are shown in Table 4.

3.2.3 Life cycle cost inventory

Conventional cost (Co1) and possible cost (Co2) of engine

The conventional cost and possible cost of WD615 Steyr engine in different phases are shown in Table 5, of which only legal adviser, personal injury, and property loss are considered in the possible cost. In this study, capital time value of the two costs is also considered. If the time span from raw material production to engine sale is 1 year, and the benchmark discount rate of the product industry is 5%, then k = (F/P, 5%, 1) = 1.05. According to Table 5, the total future value of the conventional and possible costs is calculated as

Engine life cycle environmental cost Co3

According to the environmental cost analysis steps in Sect. 2.4.3, the life cycle environmental cost of the engine is calculated as follows:

-

1.

Construction of engine environmental output matrix E = (eij)m × n.

The row vector of matrix E is the corresponding environmental output factor for CRDP, GWP, AP, EP, and POCP. According to Table 4, the environmental output of the engine can be set up, as shown in Table 6. The environmental output matrix E is expressed as

-

2.

Construction of one-order summation matrix:

-

3.

Construction of monetary matrix:

According to Table 2, environmental monetary factors are

which is converted to 15 × 5 matrix D* and expressed as

-

4.

Future cost value coefficient matrix.

In this study, the time span from raw material production to engine sale is 1 year, and we set n = 1. The benchmark discount rate is 5% and k = (F/P, 5%, 1) = 1.05. The future cost value coefficient matrix K is expressed as

-

5.

The total environmental cost matrix Co3 can be obtained as follows:

Therefore, we can obtain the following future environmental cost values: 345.58 RMB in the material production phase, 28.62 RMB in the material transport phase, 273.42 RMB in the component manufacturing phase, 11.12 RMB in the product assembly phase, and 13.01 RMB in the product sale phase, which amount to a total of 671.74 RMB. Furthermore, the environmental costs of CRDP, GWP, AP, EP, and POCP in different phases are calculated, as shown in Table 7. The total future environmental cost value in the life cycle is

To sum up, the total value of conventional cost, possible cost, and environmental cost in life cycle is

3.3 Life cycle impact assessment

3.3.1 Life cycle environmental impact analysis

Five main environmental impact categories are selected considering the main substances of recourse consumption and waste emission in engine manufacturing, namely, CRDP, GWP, EP, AP, and POCP. CRDP is mainly determined by the energy consumption of steel, aluminum, coal, oil, and natural gas. GWP is expressed in kg CO2-eq. AP is expressed in kg SO2-eq. POCP is expressed in kg C2H4-eq. EP is expressed in kg NO3−-eq. Other environmental impact categories are not considered because of their minimal impact. Moreover, solid wastes are mainly dust and metal filings whose weight accounts for more than 90% of the total waste emissions. Treatment methods include discharge, which can minimize the environmental impact. Therefore, solid wastes are also not considered.

The characterization and normalization results of five environmental impacts can be obtained by Eqs. (1)–(2), as shown in Table 8, and the normalization results for five environmental impacts in different phases can be obtained, as shown in Table 9. Figures 2 and 3 present the pie charts and histograms of the engine life cycle environmental impacts in different phases. Due to the long range of the data values, a log scale is used to pull it down to a more tractable range.

Percentage of five environmental impact categories

Environmental impacts comparison in different stages

3.3.2 Life-cycle cost analysis

Based on the cost inventory, the conventional cost, possible cost, and environmental cost of the engine in different phases are shown in Table 10, and the comparison of the cost results is illustrated in Figs. 4 and 5, in which a log scale is also used.

Costs comparison in different stages

Radar chart of three costs comparison

3.3.3 Comprehensive environmental and cost analysis

To compare the environmental impact and cost in different phases comprehensively, the unit of cost is converted to 10,000 RMB, which makes the cost numerical order close to the environmental impact results. The result of the comparison of cost and environmental impact is shown in Table 11 and Fig. 6.

Results comparison of cost and environment impact

3.4 Result discussion

3.4.1 Environmental impact result

As shown in Fig. 2 and Table 8, the environmental impact category of CRDP accounts for the largest proportion of 45.49%, followed by GWP and POCP, which account for 19.15 and 18.23%, respectively. The impacts of EP and AP are smallest at 5.16 and 11.97%, respectively. The environmental impact comparisons in different stages are shown in Fig. 3 and Table 9, material production and component manufacturing have strong impacts on the environment, and CRDP in component manufacturing is the largest, followed by GWP. The environmental impacts on material transport and product sales are the smallest, especially for AP and EP; however, the two phases produce the most POCP.

The reasons for the above results are that in the material production and component manufacturing phases, large amounts of energy (electricity) and materials (steel, aluminum, and alloy, among others) are consumed, and the production of electric power would consume an amount of natural resources of coal, crude oil, and natural gas, which contribute a great to the CRDP, and as a result, the whole proportion of CRDP is much higher than other categories. At the same time, a large amount of CO2, CO, and other greenhouse gases are generated by electric power and metal materials of alloy and aluminum production, which leads to the rise of the whole GWP. On the other hand, the distance of material transport and product sale is relatively far from the engine production company, which resulted in a large number of CO in the truck transportation and leads to the increase of GWP and POCP in the two phases. By contrast, less emissions of SO2 and HCl, especially NH4 and COD, are generated in the five phases, and therefore, the impact proportion of AP and EP is relatively lower.

Accordingly, the raw materials of alloy and aluminum are suggested to be reduced as much as possible during engine manufacturing. Then, alternative materials, which could produce low environmental impact, improve the efficiency of component manufacturing, and reduce the consumption of electric power, are advocated to choose, through which CRDP and GWP could be reduced largely. Moreover, in the material transport and product sale processes, the suppliers and selected 4S shops should be near the engine production company to shorten the total transportation distance and reduce the environmental impact of POCP and GWP.

3.4.2 Cost result

Figures 4 and 5 and Table 10 indicate that the total costs in the three phases of material production, component manufacturing, and product sales are much higher than those of the other two phases. Conventional cost accounts for almost the highest percentage in each phase (except the material transport phase), which accounts for more than 80% of the total cost. Environmental cost and possible cost are higher in the material production and component manufacturing phases. However, in the material transport phase, the three types of cost are approximately in the same magnitude order. The environmental cost and possible cost in each phase are relatively close, and the proportion of which is far below that of the conventional cost.

The reasons for the preceding results are that the large conventional cost of capital, labor, equipment energy, and material are placed in the material production and component manufacturing phases. Based on the analysis presented in Sect. 3.3.1, the environmental impacts in the two phases are higher than those of the other phases, and consequently, the environmental costs are higher. In the product sale phase, more sale fees and taxes are expended, which raises the conventional cost. In the product assembly and material transport phases, energy and material inputs are less, which reduced the total cost.

Although environmental cost accounts for a small proportion of the total, it should not be ignored as the growing concerns for environmental protection and the potential cost paid for environment pollution have become urgent problems faced by companies and governments, and therefore necessitate serious thinking to ensure eco-efficiency improvement. For the production program with large environmental impact, the backward technology should be eliminated and advanced cleaning production technology should be used. In addition, company management should be strengthened, and the unnecessary utilization of resources and energy should be maximized.

3.4.3 Comprehensive result

Figure 6 shows that, in different phases, the trend of cost result is generally close to the environmental impact. In the material production and component production phases, the cost and environmental impact results are the largest and smallest material transport and product assembly phases, respectively. In the material production and component manufacturing phases, the cost result is inconsistent with that of environmental impact; the former is much higher than the latter, and the environmental impact result is opposite. The cost of component manufacturing is close to that of product sale, but the environmental impact result is much higher.

In conclusion, the material production and component manufacturing phases should be given high attention, and certain measures should be taken to minimize the use of raw materials and improve the processing efficiency of raw materials and components. In the product sale phase, the sales expense and transport distance should be reduced and therefore the cost and environment pollution should decrease.

4 Conclusions

An integrated environment and cost assessment method based on LCA and LCC for mechanical product manufacturing is proposed in this study. The differences of LCA and LCC in functional unit, system boundary, and inventory analysis are overcome. In the environmental assessment, inventory data of energy consumption and environmental emissions are analyzed in different phases, and the midpoint approach of LCIA is selected. Through classification, characterization, and normalization, the LCIA results in different phases can be obtained and evaluated. Three cost types are selected in life cycle cost analysis, namely, conventional cost, possible cost, and environmental cost. The theory of “social willingness to pay” is introduced to analyze the life cycle environmental cost. Finally, this integrated method is applied to the environmental and cost assessment for the WD615 Steyr engine, which proved the validity and practicality of this method. The case results could provide a reference for similar mechanical product manufacturing in China.

The case of this study shows that, in a life cycle framework, the environment and cost analysis results could support each other. Consequently, by combining LCC and LCA, the economic and ecological performance evaluation appears viable to a more comprehensive eco-efficiency assessment. Nowadays, our modern society is continually dependent on the machinery manufacturing industry. With the increase in ecological problems caused by environmental pollution and insufficient resources, effective environmentally friendly and cost-effective measures for mechanical product manufacturing should be taken, which are done through the effective and accurate evaluation of resource consumption, environmental emission, and economic cost.

The objective of this study is to provide an integrated method to depict the economic and environmental performance of mechanical product manufacturing process and ultimately propose effective measures to improve eco-efficiency. The proposed methodology enhanced the conventional LCA. Additionally, the LCA framework can be used in decision-making processes. Further research on the system boundary can be extended to the early design, product use, and final disposal phases by taking a life cycle perspective that focuses on the economic and ecological aspects. Other LCIA models and endpoint indicators are advocated for the environmental assessment. Environmental cost can also be further studied by employing a more effective method, and the relevant social willingness to pay for more environmental emissions is also advocated to increase.

References

Al-Ayouty I, Hassaballa H, Rizk R (2017) Clean manufacturing industries and environmental quality: the case of Egypt. Environ Dev 21:19–25

Bare JC, Hofstetter P, Pennington DW, Haes H (2000) Midpoints versus endpoints: the sacrifices and benefits. Int J Life Cycle Assess 5(6):319–326

Barrios R, Siebel M, Helm A, Bosklopper K, Gijzen H (2008) Environmental and financial life cycle impact assessment of drinking water production at Waternet. J Clean Prod 16:471–476

BASF (2015) Homepage “eco-efficiency analysis”, available at: https://www.basf.com/en/company/sustainability/management-and-instruments/quantifying-sustainability/eco-efficiency-analysis.html

Bovea MD, Vidal R (2004) Increasing product value by integrating environmental impact, costs and customer valuation. Resour Conserv Recycl 41:133–145

Cerria D, Taischa M, Terzi S (2014) Proposal of a model for life cycle optimization of industrial equipment. Procedia CIRP 15:479–483

Chiesa M, Monteleone B, Venuta ML, Maffeis G, Greco SA (2016) Integrated study through LCA, ELCC analysis and air quality modelling related to the adoption of high efficiency small scale pellet boilers. Biomass Bioenergy 90:262–272

China nonferrous metal industry yearbook (2006) Available at: http://www.shujuku.org/china-nonferrous-metals-industry-yearbook.html

de Bruijn H, van Duin R, Huijbregts M (2002) Handbook on life cycle assessment: operational guide to the ISO standards. Springer-Verlag, New York

Dyckhoff H, Quandel A, Waletzke K (2015) Rationality of eco-efficiency methods: is the BASF analysis dependent on irrelevant alternatives? Int J Life Cycle Assess 20:1557–1567

Ferreira S, Cabral M, da Cruz NF, Marques RC (2014) Economic and environmental impacts of the recycling system in Portugal. J Clean Prod 79:219–230

Heijungs R, Settanni E, Guinée J (2013) Toward a computational structure for life cycle sustainability analysis: unifying LCA and LCC. Int J Life Cycle Assess 18:1722–1733

Hoogmartens R, Van Passel S, Van Acker K, Dubois M (2014) Bridging the gap between LCA, LCC and CBA as sustainability assessment tools. Environ Impact Assess Rev 48:27–33

Islam H, Jollands M, Setunge S, Haque N, Bhuiyan MA (2015) Life cycle assessment and life cycle cost implications for roofing and floor designs in residential buildings. Energ Buildings 104:250–263

ISO 14044 international standard (2006) In: Environmental Management—life cycle assessment—requirements and guidelines. International Organization for Standardization, Geneva, Switzerland

ISO 14045 international standard (2012) In: Environmental management—eco-efficiency assessment of product systems—principles, requirements and guidelines. International Organization for Standardization, Geneva, Switzerland

Kannan R, Tso CP, Osman R (2004) LCA–LCCA of oil fired steam turbine power plant in Singapore. Energy Convers Manag 45:3093–3107

Kim MH, Song YE, Song HB, Kim JW, Hwang SJ (2011) Evaluation of food waste disposal options by LCC analysis from the perspective of global warming: Jungnang case, South Korea. Waste Manag 31:2112–2120

Kjær LL, Pagoropoilos A, Hauschild M, Birked M, Schmidt JH, McAloone TC (2015) From LCC to LCA using a hybrid input output model-a maritime case study. Procedia CIRP 29:474–479

Kucukvar M, Cansev B, Egilmez G, Onat NC, Samadi H (2016) Energy-climate-manufacturing nexus: new insights from the regional and global supply chains of manufacturing industries. Appl Energy 184:889–904

Landsiedel R, Saling P (2002) Assessment of toxicological risks for life cycle assessment and eco-efficiency analysis. Int J Life Cycle Assess 7(5):261–268

Lee JY, An S, Cha K, Hur T (2010) Life cycle environmental and economic analyses of a hydrogen station with wind energy. Int J Hydrog Energy 35:2213–2225

Leng RB (2007) Study on product life cycle 3E+S assessment and methodology of decision analysis. Shanghai Jiaotong University, Shanghai

Li XD, Wu X, Zhang ZH (2005) Study on social WTP for environmental impacts based on the LCA theory. J Harbin Inst Tech 37(11):1507–1510

Lindahl M, Sundin E, Sakao T (2014) Environmental and economic benefits of integrated product service offerings quantified with real business cases. J Clean Prod 64:288–296

Luo L, Voet E, Huppes G (2009) Life cycle assessment and life cycle costing of bioethanol from sugarcane in Brazil. Renew Sust Energ Rev 13:1613–1619

Mistry M, Koffler C, Wong S (2016) LCA and LCC of the world’s longest pier: a case study on nickel-containing stainless steel rebar. Int J Life Cycle Assess 21:1637–1644

Norris GA (2001) Integrating life cycle cost analysis and LCA. Int J Life Cycle Assess 6(2):118–120

Ristimäki M, Säynäjoki A, Heinonen J, Junnila S (2013) Combining life cycle costing and life cycle assessment for an analysis of a new residential district energy system design. Energy 63:168–179

Saling P (2015) Sustainability improvements and life cycle approaches in industry partnerships, Life cycle Management, LCA Compendium - The Complete World of Life cycle Assessment. Springer, Dordrecht

Saling P, Kicherer A, Dittrich-Krämer B, Wittlinger R, Zombik W, Schmidt I, Schrott W, Schmidt S (2002) Eco efficiency analysis by BASF: the method. Int J Life Cycle Assess 7(4):203–218

Saling P, Maisch R, Silvani M, König N (2005) Assessing the environmental-hazard potential for life cycle assessment, eco-efficiency and SEE balance. Int J Life Cycle Assess 10(5):364–371

Senthil KD, Onga SK, Nee AYC, Tan RBH (2003) A proposed tool to integrate environmental and economical assessments of products. Environ Impact Assess Rev 23:51–72

Shonnard DR, Kicherer A, Saling P (2003) Industrial applications using BASF eco-efficiency analysis: perspectives on green engineering principles. Environ Sci Technol 37(23):5340–5348

Tapia M, Siebel MA, Helm AWC, Baars ET, Gijzen HJ (2008) Environmental, financial and quality assessment of drinking water processes at Waternet. J Clean Prod 16:401–409

Uhlman BW, Saling P (2010) Measuring and communicating sustainability through eco-efficiency analysis. CEP December 2010, special expanded web-only version, American institute of chemical engineers, CEP magazine article, December 2010: 17–26

UNEP/SETAC (2011) Life cycle initiative. Towards a life cycle sustainability assessment. Making informed choices on products. UNEP, Paris

USGS Minerals Yearbook 2005 (2005) Volume III-China. Available at: https://minerals.usgs.gov/minerals/pubs/commodity/myb/

Wenzel H, Hauschild MZ, Alting L (1997) Environmental assessment of products. In: COL. 1: Methodology, tools and case studies in product development. Chapman & Hall, London

Xu RJ, Lin B (2017) Why are there large regional differences in CO2 emissions? Evidence from China's manufacturing industry. J Clean Prod 140:1330–1343

Acknowledgments

The authors would like to thank the editor and reviewers for their constructive suggestions of the paper.

Funding

Support was from Jinan Fuqiang power Co., LTD and the 2017 Liaoning Province Natural Science Fund Guidance Project (energy efficiency, emissions and environmental impact model research of equipment remanufacturing system, Grant No. 20170540080).

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Zbigniew Stanislaw Klos

Rights and permissions

About this article

Cite this article

Shi, J., Wang, Y., Fan, S. et al. An integrated environment and cost assessment method based on LCA and LCC for mechanical product manufacturing. Int J Life Cycle Assess 24, 64–77 (2019). https://doi.org/10.1007/s11367-018-1497-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11367-018-1497-x