Abstract

Purpose

In recent years, the rising costs and infection control lead to an increasing use of disposable surgical instruments in daily hospital practices. Environmental impacts have risen as a result across the life cycle of plastic or stainless steel disposables. Compared with the conventional reusable products, different qualities and quantities of disposable scissors have to be taken into account. An eco-efficiency analysis can shed some light for the potential contribution of those products towards a sustainable development.

Methods

Disposable scissors made of either stainless steel or fibre-reinforced plastic were compared with reusable stainless steel scissors for 4,500 use cycles of surgical scissors used in Germany. A screening life cycle assessment (LCA) and a life cycle costing were performed by following ISO 14040 procedure and total cost of ownership (TCO) from a customer perspective, respectively. Subsequently, their results were used to conduct an eco-efficiency analysis.

Results and discussion

The screening LCA showed a clear ranking regarding the environmental impacts of the three types of scissors. The impacts of the disposable steel product exceeds those of the two others by 80 % (disposable plastic scissors) and 99 % (reusable steel scissors), respectively. Differences in TCO were smaller, however, revealing significant economic advantages of the reusable stainless steel product under the constraints and assumptions of this case study. Accordingly, the reusable stainless steel product was revealed as the most eco-efficient choice. It was followed by the plastic scissors which turned out to be significantly more environmentally sound than the disposable stainless steel scissors but also more cost-intensive.

Conclusions

The overall results of the study prove to be robust against variations of critical parameters for the prescribed case study. The sensitivity analyses were also conducted for LCA and TCO results. LCA results are shown to be reliable throughout all assumptions and data uncertainties. TCO results are more dependent on the choice of case study parameters whereby the price of the disposable products can severely influence the comparison of the stainless steel and the plastic scissors. The costs related to the sterilisation of the reusable product are strongly case-specific and can reduce the economic benefit of the reusable scissors to zero. Differences in environmental and economic break-even analyses underline the comparatively high share of externalised environmental costs in the case of the disposable steel product.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

1 Introduction

Medical industry is one of the important industrial sectors which are essential for our everyday life. Significant numbers of medical products are produced worldwide to satisfy the global demand. This includes “surgical instruments” which represent the specific and mostly hand-held instruments used during an operation or a surgery in a sterile environment (e.g. scalpels, clamps and forceps). In the market, reusable and disposable instruments as alternatives are available depending on the applications. The reusable products are commonly made from high-quality stainless steel which can be sterilised and reused for several years. The disposable products were originally intended for exceptional circumstances or conditions where proper disinfection is of utmost importance but cannot be guaranteed (e.g. disasters like earthquakes, areas with a high rate of HIV infection). They are made from either fibre-reinforced plastic and/or stainless steel. Traditionally, purchase decisions are mainly driven by the market price of a product, particularly for this case which relates to standard equipment and consumables. Often, the disposable products are perceived as a more economical option and selected in lieu of the reusable products. This is due to their significantly lower market price per piece, and they required no additional attentions and expenses for disinfection and repair processes. The benefits gained from the longevity of the reusable products are often neglected during the purchasing consideration (McGain et al. 2010). The rising infection control challenges and the cost pressure in health care systems (e.g. Campion et al. 2012; McGain et al. 2010; Laustsen 2007) also cause this trend of using the disposable or single-use products which continues to increase as they are supposedly a more cost-effective option. Many single-use products replaced the conventional long-lasting stainless steel products for daily hospital practices. Subsequently, the environmental consideration is increasingly gauged into one of the criteria of the consumer purchasing decisions due to the rising concerns in resource scarcity, human health and quality of ecosystem.

Therefore, the purchasing decision becomes complicated due to two reasons. First, ownership costs of the disposable and the reusable products have to be compared compatibly by considering all costs induced during a desired number of services in order to select the truly cost-effective products. Second, the environmental impacts of the disposable and reusable products can be different due variations of material and energy type and quantities consumed during operating different involved processes (Kummerer et al. 1996). On this occasion, to fulfil the same functional unit such as a number of use cycles, the reusable product has to undergo numerous elaborate cleaning and sterilisation processes during its lifetime whilst the disposable products require a repetition of the cradle-to-gate processes (e.g. raw materials, manufacturing process and transportation), resulting in considerably higher amounts of waste at their end of life stage (Conrady et al. 2010; Laustsen 2007; Gilden et al. 1992). Therefore, both ecological and economical performances of the product alternatives are essential to be assessed during the purchasing decision in order to ensure the best possible decision is made. The combination of these assessments is called the eco-efficiency (E/E) analysis. Although no standard definition of E/E portfolios has yet been concluded, one of the well-known E/E definitions was defined by the World Business Council for Sustainable Development (WBCSD) in 1992. The definition is written as “creating more value with less impact” or “the delivery of competitively-priced goods and services that satisfy human needs and bring quality of life, while progressively reducing ecological impacts and resource intensity throughout the life-cycle to a level at least in line with the earth estimated carrying capacity” (WBCSD 2000). Under this well-known framework, there are diverse approaches found in the literature (Saling et al. 2002; Oikawa et al. 2005; Lyrstedt 2005; Aoe 2007; Park and Tahara 2008; Rattanapana et al. 2012). A number of studies have used E/E methodologies to assess different products in various industries such as building materials, dairy industries, furniture production and electronic equipments (Bribián et al. 2011; Kerr and Ryan 2001; Michelsen et al. (2006); van Middelaar et al. 2011).

A few studies on health care products analysed both environmental and economic aspects as well as other related sustainability perspectives (e.g. Adler et al. 2005; McGain et al. 2010; Overcash 2012). For instance, Vercalsteren et al. (2010) compared the eco-efficiency of disposable and reusable cups, and Rattanapana et al. (2012) recently reported the framework of assessing E/E indicator for a rubber glove. However, none of these E/E studies have yet been conducted for the case of medical-related products. There are other variable products and factors that contribute different environmental impacts and costs associated with the operation of a hospital. Surgical scissors are one of the products that are ubiquitous standard instruments. They are constantly used in all departments of a hospital including operating room, diagnostic imaging department, laboratories, outpatient clinic and ward which make up a relevant share of the production volume of surgical instrument suppliers as well as of the entity of instruments that need sterilisation in, e.g. a hospital. Therefore, this research aims to demonstrate the eco-efficiency of different types of compatible case studies for surgical scissors which are disposable and reusable surgical instruments. These case studies of the surgical scissors highlight the fixed environmental impacts, and costs that can be reduced significantly by carefully managing the consideration on the impacts will be induced during the whole life cycle of the products. Assessment results reveal potential goal conflicts regarding their environmental and economic performances. The E/E analysis was conducted by firstly calculating a screening life cycle assessment (LCA) and a total cost of ownership (TCO) of the scissors’ life cycle in order to later diagnose the ratio of economic value and environmental burden. The product systems under investigation are described in detail in “Section 2.1” followed by sections on methodology, results, discussion and conclusion.

2 Methodology and case study

2.1 Case study

This E/E analysis aims to investigate the whole life cycle of the following three types of surgical scissors which are (1) disposable scissors made of plastics (fibre reinforced), (2) disposable scissors made of stainless steel and (3) reusable scissors made of stainless steel. A consistent functional unit of 4,500 use cycles of surgical scissors during 18 years was chosen for LCA, TCO and E/E analysis, based on the technical lifetime of the reusable product (Schulz et al. 2011). This number is in the same range as the number of use cycles assumed for a surgical instrument in a comparable study of Campion et al. (2012).

Figure 1 presents activities involved during the life cycles of the disposable and the reusable scissors. The products are manufactured in a global supply chain of raw material sourcing and manufacturing operations. The material stage for both types of scissors includes raw material provision and associated transportation. The manufacturing processes cover all process involved in transforming the raw materials into a finished product which are distributed from Europe to worldwide customers. For this case study, Germany was chosen as a customer location. During use phase, the reusable scissors undergo numerous cycles of washing, disinfection, sterilisation and usage, periodically interrupted by a routine repair (sharpening) process every 750 use cycles including the associated transportation. Conversely, the disposable products require no further activities during usage as they are single-use products. The end-of-life stage comprises the transportation travels from the customer to a disposal site and the disposal processes which are either recycling or incineration processes.

Life cycle activities of the disposable and the reusable surgical scissors (on the basis of Schulz et al. 2011)

2.2 Methodology overview

As mentioned earlier in “Section 1”, E/E analysis can be defined in different ways. For this study, the analysis considers the ratio between the economic value and the environmental burdens of the life cycle for the three surgical scissors as shown in Eq. 1 (WBCSD 2000).

On this occasion, the calculated TCO represents the economic value, and the LCA results portray the environmental burden as written in Eq. 2. Most of these E/E studies commonly display an E/E portfolio in a two-dimensional diagraph for a single environmental score and an economic (cost) score. Therefore, the E/E ratio is represented in a chart by comparing both variable values for the three products in “Section 5”.

These values represent both economic aspect and ecological impact incurred during the material, manufacturing process, usage and end-of-life stages for the 4,500 use cycles of the customer located in Germany.

Therefore, “Sections 3” and “4” subsequently present the screening LCA and TCO calculations, and results which are then used to produce the E/E results. This is to demonstrate the benefits in using three different types of surgical scissors. The break-even of LCA and TCO are also presented followed by a discussion of uncertainties and limitation.

3 Screening life cycle assessment

3.1 Methodology

A screening LCA was conducted to assess the environmental burdens along the life cycle of the scissors. The assessment was carried out following the ISO14040:2006 procedure (ISO14000 2006). Accordingly, goal and scope definition; inventory analysis; impact assessment and interpretation are documented. No external critical review was commissioned for this study.

Goal and scope

As stated earlier, this study aims to assess the environmental impacts along the life cycle of three distinctive types of scissors in order to compare their eco-efficiencies. Disposable plastic and disposable steel scissors are opposed to reusable steel scissors under a functional unit of 4,500 use cycles at a German customer location during 18 years. The life cycle activities in Fig. 1 represent the scope of this study which is described further in Table 1.

Life cycle inventory (LCI) analysis

According to the input data in Table 1, the data were obtained from a medical company in Europe where missing data such as sterilisation processes were replaced by information found in literature. The LCI databases used in this analysis are Ecoinvent 2.2 (Frischknecht et al. 2007) and Australian data 2007 databases. There were some modifications for the unavailable electricity process cases of Pakistan and another country in Asia by mapping the energy sources of their “Electricity/heat” data recorded in International Energy Agency database (IEA 2010a). A recycling process of the Australian Data 2007 was used as it highlights the benefit gained from material recovery; however, this may not reflect the recycling situation in Germany. For the end-of-life stage, incineration processes for plastics, cardboard and municipal solid waste were assumed. The incineration processes were based on Ecoinvent 2.2 database which derived from Swiss municipal solid waste plants in 2000. Air and water emissions from incineration and auxiliary material consumption were included. For stainless steel, the recycling process from the Australian Data 2007 database was assumed which mainly based on the primary material and energy consumption during the steel recycling process.

Impact assessment

Three life cycle impact assessment (LCIA) methods were applied for this screening LCA to highlight the environmental impacts as well as the embodied energy. The methods include the cumulative energy demand (CED), World ReCiPe midpoint (WRM) and World ReCiPe endpoint (WRE).

Results of an individual environmental impact category were calculated by the corresponding LCIA methods integrated in the SimaPro software (Pre Consultants BV 2008). CED serves as an input–oriented indicator which assesses the primary energy consumption. WRM and WRE methods were developed in 2008 (Goedkoop et al. 2009) and since, have increasingly been used (Belboom et al. 2011; Jones and McManus 2010). These methods bear the risk of concealing goal conflicts as they deliver single score indicators. Thus, WRM results of 18 explicit impact categories in different units such as kilograms CO2eq and kilograms oileq are presented to highlight the tradeoffs amongst themselves. WRE generates the single score results which are simple to communicate and can be summed into three different damage categories (Recipe 2011). Such results convey not only the potential environmental impacts such as the global warming potential that represents the amount of emitted greenhouse gases but also the damage imposed to human health, ecosystem quality and resource use. There was no allocation procedure applied to this LCA as no multi–output processes appear in the three observed product systems as depicted in Fig. 1.

3.2 Results

LCA results for the 4,500 use cycles of the three types of surgical scissors are presented in this subsection. Overall, Fig. 2 shows the total cradle-to-grave WRE and CED results which indicate that the 4,500 pairs of stainless steel disposable scissors have the highest environmental impact. The 4,500 pairs of plastic disposable scissors and a pair of stainless steel reusable scissors are equivalent to approximately 20 % and 2 % of the stainless steel disposable scissors scenario for both WRE and CED results. Figure 3 highlights the single score results for the three main damage categories. The results are presented in a contribution percentage of the total environmental impact results of the stainless steel disposable scissors which have the highest value. On this occasion, the human health damage category of each product across the life cycle stages contributes in a range of 50 % to 60 %. This follows the slightly lower values of the resource use damage category which vary from 44 % to 47 %. The ecosystem quality damage category has the least value of 3 % to 4 %.

The contribution percentage results for the environmental impact (WRE) and the embodied energy (CED) results for cradle-to-grave processes of 4,500 use cycles

The contribution percentage results for the WRE damage category results for cradle-to-grave processes of 4,500 use cycles

Figures 2 and 3 reflect the hotspots of the stainless steel disposable scissors at the manufacturing process stage caused by forging, annealing and sheet rolling processes which require high energy consumption. The material stage is another hot spot found which is induced mainly by the steel extraction process.

On a contrary, the plastic disposable scissors from both charts have the highest contribution at the material stage due to the processing of composites that contain different raw materials such as plastic resin, fibre and additives. The manufacturing process stage is the next hot spot which is almost half the value of the material stage. It is predominately inherited from the injection moulding and punching processes.

Noticeably, only stainless steel reusable scissors have high energy consumption during the usage stage due to the fact that the other products do not require any supporting activities. The reusable scissors require washing, disinfection and sterilisation processes before each use; therefore, 4,500 cycles of these activities were performed. The sterilisation process contributes up to 85 % of this hot spot mainly due to the electricity consumption where the rest of the contribution comes from steam-making and waste water treatment processes. The washing and disinfection process is based on steam, electricity and deionised water which contribute 81 %, 16 % and 3 %, respectively. The end-of-life stage of the plastic disposable scissors in Fig. 2 has the highest environmental impact at approximately 0.8 % while the stainless steel disposable (−0.8 %) and reusable scissors gained benefits from recycling process. This is due to the fact that 100 % recycling was assumed for steel parts while 100 % incineration was assigned for the remaining materials.

As can be observed, the environmental and embodied energy hot spots of these three surgical scissors vary across the life cycle stages. Figure 4 explicitly highlights the cradle-to-grave results for an individual impact category using the characteristic results from WRM method. Likewise, most of the impact categories clearly show that the stainless steel disposable scissors have the highest environmental impact. Their values are significantly higher than the other two products at approximately two to ten times higher than the plastic disposable scissors and more than 13 times higher than the stainless steel reusable scissors. The exceptions are found in the agricultural occupation and the water depletion impact categories where the plastic disposable scissor results are higher than those of both stainless steel products. In the former category, this is caused by the packaging which contains cardboard material whereas the latter is influenced by water used during processing of the fibre for composites and of the stainless steel.

Characterisation results produced by the World ReCipe midpoint method for cradle-to-grave processes of 4,500 use cycles

Additionally, the break-even of the embodied energy in Fig. 5 was also analysed in order to show the point where the higher initial efforts for the reusable scissors are outweighed. The analysis was compared by varying the number of use cycles. Figure 5 shows that one use cycle of the stainless steel reusable scissors has the highest embodied energy (83 %), followed by the stainless steel (60 %) and the plastic (11 %) disposable scissors, respectively. Between first- to eighth-use cycles, the plastic disposable scissors have the lowest embodied energy (11 % to 91 %), and after that, the stainless steel reusable scissors is then break-even.

Embodied energy break-even analysis for the three surgical scissors

3.3 Uncertainties and limitations

LCA for the three surgical scissors was based on several data sources which were obtained from various data sources. For the plastic disposable scissors and the stainless steel reusable scissors, company data were mainly used while data for the comparable stainless steel disposable scissors were obtained from relevant literature (Schulz et al. 2011). Due to the limitation of the input data, other data sources were used to substitute any missing data. These sources were expert opinions from different companies, literature review related to medical practices and the LCI databases. The additional assumptions that may contribute to identify hot spots are briefly elaborated as follows.

At the material stage, the same process case from the Ecoinvent 2.2 database was assumed to represent the stainless steel used for both disposable and reusable scissors. In reality, the stainless steel disposable scissors are made of a lower-grade material than the reusable version which indicates that their mineral contents would be different.

For the manufacturing process stage, there are two modified electricity mix process cases which are unavailable in the available Ecoinvent 2.2 database as the locations of the manufacturing plants were located in two Asian countries. The modification was based on the ‘Electricity, production mix US/US U’. The carbon dioxide emissions of the modified electricity case were validated with the carbon dioxide emissions reported by the IEA (IEA 2010b). As the electricity consumption was the hot spot for the manufacturing process, the sensitivity analysis was conducted to observe the variations of carbon dioxide emissions produced by the modified electricity processes and another additional option by comparing with the IEA reported data (IEA 2010b). The analysis compares the current scenario with another scenario where the modified electricity case was based on another possible electricity case, the ‘Electricity, production mix CN/CN U’. The comparison results which are presented in Fig. 6 highlight that the variation is in the range of 0.3 % to 19 %. Two sterilisation processes namely gamma and gas sterilisation were also included in the manufacturing process and usage stages. Their material and electricity consumption were theoretically assumed on the basis of the company data, expert opinion and literature such as machine manual and medical document, etc. As a consequence, the actual situation may show an altered consumption as it depends on the efficiency and conditions of the sterilisation machines.

A sensitivity analysis of the carbon dioxide emission produced by two alternative modifications of the available electricity mix processes used in the manufacturing processes

Lastly, the end-of-life options were based on company data and common practices where medical wastes are often incinerated after use. Recycling was based on Australia 2007 data to reflect the recycling benefits; nonetheless, this situation may not reflect the German situation. Sensitivity was made by changing the 100 % recycling rate to 100 % incineration; small variations were found. These aforementioned limitations and uncertainties may vary the results accordingly.

4 Life cycle costing

4.1 Methodology

Cost effectiveness of reusable and disposable options of healthcare products have been discussed for many years (e.g. Schooleman 1993; Apelgre et al. 1994; Morrison and Jacobs 2004; Adler et al. 2005; Baykasoglu et al. 2009; McGain et al. 2010; Klar et al. 2011; Overcash 2012). These studies investigated specific products under variations of the goal, scope and types of products. Their findings were rather ambiguous and did not lead to any generic conclusion. As a result, a life cycle costing (LCC) approach was taken to estimate the E/E of the different types of surgical scissors. LCC can be performed either from the point of view of a producer or a customer (Herrmann 2010). A society perspective can be additionally included to account the externalities or social costs that are induced by an environmental impact of the product (Silalertruksa et al. 2012).

As cost aspect is one of the main criteria that customers consider when purchasing a product, higher cost of a product would impact their purchasing decision which may lead to a variation of the market share of the three different surgical scissors. Therefore, this paper estimates the TCO for the three types of scissors by focusing on a customer perspective. TCO concept was applied by considering all costs that customers have to pay during purchasing, using and disposing the product (Blanchard 1978; Wübbenhorst 1984). Table 2 summarises the cost elements and their amounts utilised for the base scenario of the disposable and reusable surgical scissors. These costs can be described as follows.

-

Purchase cost. The purchasing prices in Table 2 were obtained for straight scissors of 14.0 to 14.5 cm length with one sharp and one blunt end blade (without gilded handles) for a number of 1,000 or 1,250 pairs of the disposable scissors and 100 pairs of the reusable scissors. For these discounted prices, no additional delivery fees were applicable. These comparable market prices represent the median prices of the data found from ten diverse medical companies in Germany (Mercateo 2012) via online media. Two purchase prices of the fibre-reinforced plastic and stainless steel surgical scissors were selected as they represent a sterile single-use product in a median price range. For the reusable steel scissors, high quality differences lead to a broad price span. According to the assumed technical lifetime (4,500 use cycles), four products within a price range of 21.90 €/piece and 29.40 €/piece have been taken into account. An average price of 26.23 €/piece is used as displayed in Table 2.

-

Disinfection, washing and sterilisation. The costs associated with the preparation activities of the reusable product including disinfection, washing, control, maintenance, packaging, sterilisation and documentation were estimated for an exemplary case in Table 3 as 1.70 € per pair of scissors (Sisolefyky 2012). It was assumed that the case study uses a central sterile service department of a hospital with an annual preparation volume of approximately 50,000 sterilisation units. A sterilisation unit has a volume unit of 60 × 30 × 30 cm3 with a maximum weight of 10 kg (DIN EN 285:2009-08). It can sterilise 60 to 80 pairs of scissors per operation depending on sizes and types of packaging of the scissors (Sisolefyky 2012). The sterilised scissors are subsequently packaged in a single-layered plastic bag and labelled with one marker. The preparation cost is contributed by 52 % of labour; 25 % of packaging, consumables, chemicals and energy; 18 % of depreciation of equipment and 5 % of maintenance and calibration of the equipment (Sisolefyky 2012).

Table 3 Assumptions of the preparation processes for the reusable scissors -

Repair. As mentioned in “Section 2.1”, the reusable product requires a repair process at every 750 use cycles. Cost for this process was approximately assumed as 75 % of the purchase price of the scissors to represent a worst-case scenario of the reusable product; hence, it equals to 0.03 € per use cycle (see Table 2). If its repair cost is higher than this, the purchase of a new product would be an attractive option to a customer.

-

Logistics. Internal logistic costs (within the hospital) were excluded due to unavailability of the data. The costs would include internal transports of the reusable product to and from the central sterile services department as well as the effort for the higher frequency of purchase activities and the higher demand of storage room of the disposable products.

-

Disposal. The used scissors are often discarded with the cut bandaging material and therefore can be classified under the EWC (European Waste Catalogue) code 180104 which means waste whose collection and disposal are not subject to special requirements in order to prevent infection (EPA 2002). A case study for a German university medical centre identified waste treatment costs for this non-infectious medical waste of roughly 334 €/t. This value divides into 180 €/t for disposal fees and 154 €/t for disposal media (Schubert 2009). The disposal costs in Table 2 were derived from the multiplication of this rate (334 €/t) with the different weight of the three targeted scissors. For the case of the application in Germany, no disposal fees for packaging materials were applied because their redistribution and recycling or disposal processes are covered by the Duales System Deutschland GmbH.

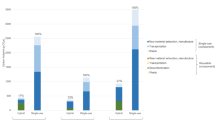

4.2 Results

Under the constraints and assumptions stated above, TCO for the three different scissors in 4,500 use cycles amounts are plotted in Fig. 7. As predicted from the purchase price differences, the choice of the disposable steel product leads to a slightly lower TCO of approximately 12,375 € when compared with the disposable plastic product (14,085 €). This equals to a 12 % reduction. In contrast, the consumer can significantly reduce the TCO when using the reusable product (7,811 €) instead. Under the base scenario, approximately 45 % cost savings were associated to the usage stage of the disposable plastic scissors.

Total cost of ownership for the base scenario (4,500 use cycles)

An economic break-even analysis for this base scenario in Fig. 8 reveals that the payback period of the reusable product is valid at 19 use cycles when compared with the plastic disposable product and at 25 use cycles when compared with the stainless steel disposable product.

An economic break-even analysis for the base scenario

4.3 Uncertainty and limitation

The TCO calculation for the three different scissors is based on an exemplary use case and a number of assumptions. Those cost types with a low share on the overall TCO—either non-recurring and seldom recurring costs like purchase and repair costs of the reusable product or costs with a low rate per use cycle (e.g. disposal costs)—did not show the potential to invert the results. The recurring purchase costs for the disposable products seem more crucial. Therefore, they have been validated with an actual product price published in a cost–benefit analysis by a medical instrument manufacturer (EHS Medizintechnik 2009). The published price (2.87 €) falls in between the prices of the disposable products reported in Table 2 (3.12 € and 2.74 €). However, a decline of their market prices will directly prolong the payback period of the reusable scissors (found in Fig. 8). The general advantage of the reusable scissors over the 4,500 use cycles remains, unless the purchase prices of the disposable products are lower than the sterilisation cost of the reusable scissors.

The other two main influencing factors—the lifetime of the reusable product and the cost for its disinfection, washing and sterilisation before every use cycle—have been scrutinised in sensitivity analyses. The first sensitivity analysis encompasses a variation of the cost related to disinfection, washing and sterilisation of the reusable product (the preparation cost). A number of parameters have to be taken into account to determine the preparation cost including, e.g. the sizes of the sterile services department, types of the packaging, logistics and labour forces. This underlines the case specificity of TCO calculations for reusable surgical instruments. Therefore, as the input data taken in this study are based on this specific case, most parameters of this base scenario remain the same for this sensitivity analysis, except for the types of packaging which have been varied.

For the base scenario, a simple packaging has been modelled (in accordance with the LCA modelling) which is appropriate for a frequently used instrument like surgical scissors. This base scenario is compared with three alternative scenarios as listed in Table 4. Scenarios a, b and c encompass a double-packaging, a long-term packaging and a preparation rate found in literature (EHS Medizintechnik 2009), respectively. As can be seen in Fig. 5, the preparation cost rate has a potential to significantly reduce the economic benefit of the reusable scissors. The base scenario is modelled for a standard packaging which requires no extra precaution due to the least storage time. This type of packaging gives a high profitability scenario for the reusable product. On the contrary, the packaging of scenarios a and b have higher TCO (9,566 € and 10,781 €, respectively) which lowers the economic benefits gained for customers from choosing a reusable product. The TCO of scenario (c) as presented in the far right column of Fig. 9 (12,221 €) is nearly as high as that of the disposable steel product (12,375 €). This means there is no significant economic advantage of buying the reusable product under that scenario. In summary, the economic attractiveness of the reusable product highly depends on the price difference between preparation costs and purchase price of the disposable products.

A sensitivity analysis for total cost of ownership of different preparation cost scenarios

Last sensitivity analysis was performed by varying the number of use cycles until the reusable product is disposed from 4,500, 3,000 and 750 use cycles. The durability of the reusable product clearly influences the absolute economic benefit gained from using the reusable scissors. However, the cost-reduction percentage stays nearly the same and varies only from 45 % (base scenario) to 44 % (3,000 and 750 use cycles, respectively).

5 Eco-efficiency analysis

5.1 Results

The E/E results for the 4,500 use cycle scenario are presented in Fig. 10a and b where the environmental burdens are presented in two different LCA results. They are the single score result from WRE in a unit of points and the embodied energy from CED in a unit of MJeq. According to both figures, a pair of stainless steel reusable scissors has the lowest environmental impact which 11 and 52 times less than the plastic and stainless steel disposable scissors, respectively. This reusable scissor is the most cost-effective option. The 4,500 pairs of stainless steel disposable scissors produce the highest environmental impact, but they are 1.2 % cheaper than the 4,500 pairs of the plastic disposable scissors. Lastly, the plastic disposable scissors are the most expensive option which is 45 % higher than the reusable scissors but with a moderate environmental impact. As it can be observed, these results are based on the 4,500 use cycles. If the number of use cycle is varied, the decision in using the three surgical scissors would be shifted as demonstrated in the sensitivity analyses (see Figs. 6 and 9). In addition to these prescribed embodied energy and economic break-even analyses, the E/E of the three surgical scissors would also vary upon the changes of the number of use cycles. According to the two figures, the customers are better off to use the reusable product at least 25 times in order to sustain the eco-efficiency ratio found in Fig. 10.

An eco-efficiency analysis of the total environmental impact and the embodied energy results. a Total environmental impact. b Embodied energy

5.2 Uncertainties and limitations

The uncertainties of the E/E are inherited from the uncertainties embedded in the assessments of LCA and TCO which can vary according to the quantitative sensitivity analyses discussed in “Sections 3.3” and “4.3”. Apart from that, additional uncertainties may be imposed by the consistencies of both assessments which can be described qualitatively as follows. Firstly, the material and manufacturing costs were not considered, as the focus of this study is on TCO. For TCO, only the price for purchasing is relevant and the follow-up costs. In contrast, LCA focused on the environmental impacts incurred from the raw materials and the main manufacturing processes that consume electricity. Secondly, the usage stage of LCA specifically considered the impacts from the delivery activities while the TCO included this cost which inherited within the purchases price. Nonetheless, if the number of purchased order is reduced below the threshold of the discounted delivery rate, then the TCO may vary accordingly. Finally, the variations of LCA and TCO for the usage and end-of-life stages can be altered as they predominantly depend on the actual practices in the real world.

6 Conclusions

The eco-efficiency analysis was carried out by conducting the screening LCA and the estimation of TCO for the 4,500 use cycle scenario of the three different types of disposable and reusable surgical scissors. The methodologies, results and uncertainties of LCA and TCO were presented and used to analyse the eco-efficiency. Results show that the reusable stainless steel product produced the lowest environmental impact followed by the plastic disposable and the stainless steel disposable scissors. The ecological hotspots were found in the material and the manufacturing process stages for the plastic disposable and the stainless steel disposable scissors whereas the stainless steel reusable scissors had an additional hotspot in the usage phase. The human health damage category contributed the most where the agricultural occupation and the water depletion impact categories of the plastic disposable scissors were higher than the stainless steel. TCO results revealed that the stainless steel reusable scissors are the cheapest option followed by the stainless steel and the plastic disposable scissors under the constraints and assumptions of the analysed case study. Variations in the differences between purchase price of the disposable products and the sterilisation costs for the reusable products have a direct influence on these results. Finally, the eco-efficiency results indicated that the pair stainless steel reusable scissors is the lowest environmental impact and cheapest option. The stainless steel disposable scissors give the highest environmental impact, but they are cheaper than that of the plastic disposable scissors. The plastic disposable scissors are the most expensive option but with a moderate environmental impact. In addition to this, the break-even analysis was also performed. Break-even results showed that the benefits of using reusable scissors will outweigh both economic and ecological impacts of both disposable scissors at the 25th use cycle. This underlines the comparatively high share of externalised environmental costs in case of the disposable steel product. Even though multiple emissions such as greenhouse gases occur along the life cycle of this product compared with the two alternatives, it can be purchased and used with the lowest price. This cost advantage could be different, if fees for using the atmosphere as a sink/storage for those emissions or the costs for the damage potentially caused by those emissions (externalities) are included in the purchase price similarly to the fees of disposing of waste to landfill. Without such consideration, the purchase price or TCO will not reflect the “true price” of a product. In this sense and neglecting the contribution of non-resource-related costs (e.g. human labour, tax and profit margin), E/E results can be understood as an indicator to which degree producer and consumer of the scissors depend on society to pay for the aftermath of the scissors’ life cycle. Future work can be continued by enhancing the input data used of LCA and TCO such as collecting detailed input data of stainless steel contents, forging and annealing process and logistics. The variations of the usage intensities and the disposal practices in different customer locations can also be investigated in order to fully understand the eco-efficiency of the three products.

Abbreviations

- CED:

-

Cumulative energy demand

- E/E:

-

Eco-efficiency

- GRP:

-

Glass-reinforced plastics

- LCA:

-

Life cycle assessment

- LCIA:

-

Life cycle impact assessment

- LCI:

-

Life cycle inventory

- TCO:

-

Total cost of ownership

- WBCSD:

-

World business council for sustainable development

- WRE:

-

World ReCiPe midpoint

- WRM:

-

World ReCiPe endpoint

References

Adler S, Scherrer M, Rückauer KD, Daschner FD (2005) Comparison of economic and environmental impacts between disposable and reusable instruments for laparoscopic cholecystectomy. Surg Endosc 19:268–272

Aoe T (2007) Eco-efficiency and ecodesign in electrical and electronic products. J Clean Prod 15:1406–1414

Apelgre KN, Blank ML, Slomski CA, Hadjis NS (1994) Reusable instruments are more cost-effective than disposable instruments for laparoscopic holecystectomy. Surg Endosc 8:32–34

Baykasoglu A, Dereli T, Yilankirkan N (2009) Application of cost/benefit analysis for surgical gown and drape selection: a case study. Am J Infect Control 37:215–226

Belboom S, Renzoni R, Verjans B, Léonard A, Germain A (2011) A life cycle assessment of injectable drug primary packaging: comparing the traditional process in glass vials with the closed vial technology (polymer vials). Int J Life Cycle Assess 16:159–167

Blanchard BS (1978) Design and manage to life cycle cost. Virginia Polytechnic Institute and State University, Portland, M/A Press

Bribián IZ, Capilla AV, Usón AA (2011) Life cycle assessment of building materials: comparative analysis of energy and environmental impacts and evaluation of the eco-efficiency improvement potential. Build Environ 46(5):1133–1140

Campion N, Thiel CL, DeBlois J, Woods NC, Landis AE, Bilec MM (2012) Life cycle assessment perspectives on delivering an infant in the US. Sci Total Environ 425:191–198

Conrady J, Hillanbrand M, Myers S, Nussbaum G (2010) Reducing medical waste. AORN J 91:711–721

DIN EN 285:2009-08: Sterilization—steam sterilizers—large sterilizers. German version EN 285:2006+A2:2009

EHS Medizintechnik (2009) Aesculap SUSI-Eine Kosten-Nutzen-Analyse, http://www.ehs.de/home/fachdisziplinen-produkte/zentralsterilisation/aesculap-susi/susi-kosten-nutzen-analyse.html. Accessed 3 October 2012

Environmental Protection Agency (2002) European waste catalogue and hazardous waste list. Valid from 1 January 2002, ISBN: 1-84095-083-8, Ireland

Frischknecht R, Jungbluth N, Althaus H-J, Doka G, Dones R, Hischier R, Hellweg S, Nemecek T, Rebiter G, Spielmann M (2007) Overview and methodology. Final report Ecoinvent data v2.0 No.1. Swiss Centre for Life Cycle Inventories, Duebendorf, Switzerland

Gilden DJ, Scissors KN, Reuler JB (1992) Disposable products in the hospital waste stream. West J Med 156:269–272

Goedkoop M, Heijungs R, Huijbregts M, Schryver AD, Struijs J, Van Zelm R (2009) ReCiPe 2008. A life cycle impact assessment method which comprises harmonised category indicators at the midpoint and the endpoint level. VROM, The Hague

Herrmann C (2010) Ganzheitliches Life-Cycle-Management-Nachhaltigkeit und Lebenszyklusorientierung in Unternehmen. Springer, Berlin

International Energy Agency (2010a) Electricity/heat in 2010. www.iea.org/stats/index.asp. Accessed 4 September 2012

International Energy Agency (2010b) CO2 emissions from fuel combustion highlights, 2010th edn. IEA, Paris

ISO 14040 (2006) Environmental management—life cycle assessment—principles and framework. ISO, Geneva

Jones CI, McManus MC (2010) Life-cycle assessment of 11 kV electrical overhead lines and underground cables. J Clean Prod 18:1464–1477

Kerr W, Ryan C (2001) Eco-efficiency gains from remanufacturing: a case study of photocopier remanufacturing at Fuji Xerox Australia. J Clean Prod 9(1):75–81

Klar M, Haberstroh J, Timme S, Fritzsch G, Gitsch G, Denschlag D (2011) Comparison of a reusable with a disposable vessel-sealing device in a sheep model: efficacy and costs. Fertil Steril 95:795–798

Kummerer K, Dettenkofer M, Scherrer M (1996) Comparison of reusable and disposable laparotomy pads. Int J Life Cycle Assess 1:67–73

Laustsen G (2007) Reduce–recycle–reuse: guidelines for promoting perioperative waste management. AORN J 85(4):717–728

Lyrstedt F (2005) Measuring eco-efficiency by a LCC/LCA ratio an evaluation of its applicability A case study at ABB. MSc. Thesis, Chalmers University of Technology

McGain F, McAlister S, McGavin A, Story D (2010) The financial and environmental costs of reusable and single-use plastic anaesthetic drug trays. Anaesth Intensive Care 38:538–544

Mercateo (2012) Chirurgische schere bei mercateo online kaufen. Mercateo Deutschland, http://www.mercateo.com/kw/chirurgische%2820%29schere/chirurgische_schere.html. Accessed 28 September 2012

Michelsen O, Fet AM, Dahlsrud A (2006) Eco-efficiency in extended supply chains: a case study of furniture production. J Environ Manag 79:290–297

Morrison JE, Jacobs VR (2004) Replacement of expensive, disposable instruments with old-fashioned surgical techniques for improved cost-effectiveness in laparoscopic hysterectomy. JSLS 8:201–206

Oikawa S, Ebisu K, Fuse K (2005) Fujitsu’s approach for eco-efficiency factor. Fujitsu Sci Tech J 41(2):236–241

Overcash M (2012) A comparison of reusable and disposable perioperative textiles: sustainability state-of-the-art. Anesth Analg 114(5):1055–1066

Park PJ, Tahara K (2008) Quantifying producer and consumer-based eco-efficiencies for the identification of key ecodesign issues. J Clean Prod 16:95–104

PRe Consultants BV (2008) SimaPro 7 user’s manual. The Netherlands

Rattanapana C, Suksaroj TT, Ounsaneha W (2012) Development of eco-efficiency indicators for rubber glove product by material flow analysis. Procedia - Social Behav Sci 40:99–106

Recipe, introduction (2011) http://sites.google.com/site/lciarecipe/project-definition. Accessed 4 September 2012

Saling P, Kircherer A, Dittrich-Krämer B, Wittlinger R, Zombik W, Schmidt I, Schrott W, Schmidt S (2002) Eco-efficiency analysis by BASF: the method. Int J Life Cycle Assess 7(4):203–218

Schooleman S (1993) OR industry split on merits of disposable/reusable instruments. Health Ind Today 56(5):1

Schubert K (2009) Abfallmanagement an einem krankenhaus mit maximalversorgung - ein praxisbericht. presentation at 5. Umwelttag NRW – Bochum 15.09.2009, http://www.ak-umwelt-im-krankenhaus.de/unterlagen/umwelttag/2009/Vortragsunterlagen/WS%204_5%20schubert%20Vortrag%20Bochum%2015092009.pdf. Accessed 28 September 2012

Schulz J, Pschorn J, Kara S, Herrmann C, Ibbotson S, Dettmer T, Luger T (2011) Environmental footprint of single-use surgical instruments in comparison with multi-use surgical instruments. 18th CIRP Conference on Life Cycle Engineering, Braunschweig, Germany, pp 623–628

Silalertruksa T, Sébastien Bonnet S, Gheewala SH (2012) Life cycle costing and externalities of palm oil biodiesel in Thailand. J Clean Prod 28:225–232

Sisolefyky J (2012) Written communication. Vanguard Integrierte Verorgungssysteme GmbH, Accessed 28 August 2012

van Middelaar CE, Berentsen PBM, Dolman MA, de Boer IJM (2011) Eco-efficiency in the production chain of Dutch semi-hard cheese. Livest Sci 139:91–99

Vercalsteren A, Spirinckx C, Geerken T (2010) Life cycle assessment and eco-efficiency analysis of drinking cups used at public events. Int J Life Cycle Assess 15:221–230

WBCSD (2000) Eco-efficiency—creating more value with less impact, ISBN 2-940240-17-5, http://www.wbcsd.org/web/publications/eco_efficiency_creating_more_value.pdf. Accessed 28 September 2012

Wübbenhorst K (1984) Konzept der lebenszykluskosten. Grundlagen, Problemstellungen und technologische Zusammenhänge. Verlag für Fachliteratur Darmstadt, Darmstadt, Germany

Acknowledgments

The authors especially thank Jörg Sisolefsky (Vanguard Integrierte Verorgungssysteme GmbH) for his contribution to this study.

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Marzia Traverso

Rights and permissions

About this article

Cite this article

Ibbotson, S., Dettmer, T., Kara, S. et al. Eco-efficiency of disposable and reusable surgical instruments—a scissors case. Int J Life Cycle Assess 18, 1137–1148 (2013). https://doi.org/10.1007/s11367-013-0547-7

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11367-013-0547-7