Abstract

This article uses firm level data from an SME survey conducted by Riinvest Institute in 2006 in order to examine the determinants of obtaining bank finance conditional upon applying. The results of the survey show that not all the firms receive credit they apply for, suggesting a slight excess of demand over supply of credit. Unlike some other studies in transition economies this article corrects for sample selection bias. Econometric evidence indicates that commercial banks base their decision to loan firms primarily on the basis of collateral. Well performing firms are more likely to ask for credit because of better business prospects in the future, but profitability as a measure of firm performance does not seem to be sufficient signaling for banks in order to allocate credits. Banks seems to prefer more to secure themselves from likely opportunistic behavior of potentially “bad borrowers” with use of collateral. Findings are in line with theoretical and empirical arguments that systematic use of collateral can mitigate the adverse selection by banks in choosing whom to allocate the credit especially in country with turbulent political environment and weak property right system. However, unlike other studies findings suggest that the rhetoric of financial constraints to some extent has been exaggerated in a transition context.

Similar content being viewed by others

Avoid common mistakes on your manuscript.

Introduction

In the recent years there has been a growing debate on whether the availability of external finance significantly hinders small firms’ investment capabilities, growth and performance.Footnote 1 In the long-run capital investment of firms is critical for productivity and growth of the private sector and the overall growth of any economy. The firm’s investment may be limited because of firm’s inability to obtain external finance despite the investment growth opportunities. The debate on the importance of external finance is influenced by the common view among economists about capital market imperfections that disproportionately affect small businesses in terms of their access to external finance. These imperfections as will be argued later in this paper are mainly due to the presence of information asymmetry in capital markets leading to credit rationing. If firms face limited access to external finance they may be unable to invest, despite their willingness to do so unless internal sources of finance are available. In these circumstances, larger firms that are able to obtain resources may not find profitable use for them; on the other hand small firms that can find the opportunities may not find the financial resources. This leads to the situation where economy is losing some of the potential benefits of potentially good projects that will not be implemented because of the lack of funds.

In addition to the general financial problems of SMEs in any economy, small firm financing in transition economies is impeded by the low level development of the banking systems and capital markets and shortage of available capital creating negative supply side effects leading to unfavourable conditions for growth of the SMEs. Various studies from transition economies pointed out the pivotal role of external finance on small firm growth in Albania (Hashi 2001), Slovenia (Bartlett and Bukvič 2001) Russia and Bulgaria (Pissarides et al. 2003) and Kosova (Krasniqi 2007). The non-availability of external finance becomes one of the main constraints to small business investment and hampers their growth potential. In the early transition period, in particular, there is a concern that de novo firms without business or credit history and track record because banks are reluctant to offer them loans (Bratkowski et al. 2000). Although important, there are only few studies that addressed firm’s access to bank finance. Some of these empirical studies suffer from sample selection bias, ignore demand-side factors or lack empirical rigour because are mainly based on research reports. These shortcomings may result to biased conclusions that firms access to external finance (in majority of cases a bank loan) is restricted because they failed to incorporate demand-side factors adequately in empirical analysis.

Then, the objective of this paper is to thoroughly investigate what factors influence firm’s access to external finance by incorporating both aspects—supply-side such as availability of capital as well as demand-side effects such as entrepreneur’s ability to absorb bank finance by fulfilling banks’ requirements. For this purpose we use firm level data based on survey of 600 SMEs aimed at highlighting business environment constrains faced by small firms in Kosova in order to estimate the likelihood of firms accessing bank finance. Our findings suggest high degree of self-selection after correcting for sample selection bias. That is, only entrepreneurs with good projects choose to apply for bank loan. The presence of information asymmetry places banks in a difficult position in screening process of applicants, so they use collateral to secure loans. Therefore, the paper contributes to the literature by providing better insights on small firms’ access to bank finance in transition economies. This analysis will help to explain cross-country variation because it is important to test determining factors of access to finance in different contexts, in particular for transition economies where studies of this kind are still scarce. Kosova as conflict-plagued makes a unique case for expanding model of entrepreneurship as an extreme environment for entrepreneurship (see Solymossy 2005). It also has some important theoretical implications for small firm literature in transitional economies because it provides new evidence on the debate whether the small firms are really credit constrained or simply has been overemphasized in the literature as shown in the next section. This paper raises an important question: whether the supply side obstacles faced by small firms to access bank finance in transition economies originate from failures of these empirical studies to adequately control for entrepreneur’s preferences over internal sources or failure to address the issue of ‘discouraged borrowers’. From policy perspective it suggests that government efforts should be concentrated at improving terms and conditions for loan users as well as facilitating access to bank loans by helping banking sector to reduce asymmetric information.

The paper is organized as follows. “Theory of small firm finance” critically discusses the theoretical literature on small firm finance and moreover places this theory in the context of small firms in transition economies by discussing both, factors affecting credit demand and credit supply. “Methodology” presents methodology, data and a brief overview of banking system and SME finance in Kosova. “Discussion of empirical findings” discusses empirical findings. “Conclusions and policy implications” draws conclusions and policy implications.

Theory of small firm finance

The growing interest in the small firm finance is understandable having considered the critical role of firm’s access to external finance for the survival and growth of small firms which increasingly contribute to employment generation and economic growth. In this regard, banks, as major providers of such funding, play a key role in promoting firm survival (Saridakis et al. 2008). The debate on small firm finance is mostly focused on the market efficiency of supply of finance to small firms and the potential problem of credit rationing (Ang 1991; Berger and Udell 1998; Gregory et al. 2005; Hutchinson and Xavier 2006) while there is a comparatively little research on the demand and its effect on small firms capital structure (Low and Mazzarol 2006). Then, it is increasingly important to investigate both aspects of small firm finance in order to enhance our understanding of how small business owners-managers decide among financing options or whether they are constrained by the availability of external finance to do so or not? As emphasized by Hashi (2001) the inability (or unwillingness) of the financial institutions to deal with the financial needs of SMEs may explain this pattern to some extent, but the behavior of entrepreneurs asking for these funds must also play an important role. In what follows we will discuss both aspects, supply and demand-side factors.

Factors affecting credit supply

Small firms use various sources of funding in order to meet their financing needs. These funds can be supplied either by the company’s own resources, bank loans, new equity, or a grant from public sector assistance. The most commonly used source of external finance for small firms is bank loan (see Hughes and Storey 1991; Riinvest 2006) which is the focus of the reminder of this section. The resources of small firm owners are usually limited, especially for new and small businesses. Thus, the growth-oriented small firms will need external sources of finance supplied by banks. But, for a variety of reasons (not related to entrepreneur), especially information asymmetry, these funds are often not available to all firms. Although not directly attributed to the size (small firms), the ‘external finance gap’ usually is linked with asymmetric information which is not unique to small firms and even not to the capital markets. Despite that, information problems resulting from asymmetric information affect predominantly small firms.

Consequently, there is a common view that the capital markets are inefficient with respect to small business finance because of credit rationing stemming from asymmetric information (Stiglitz and Weiss 1981). They argue that in the situation where banks cannot observe the quality of the borrowers due to insufficient information adverse selection takes place. Under the asymmetric information conditions banks are uncertain about the future behavior of the borrower in terms of repaying the loan. Stated differently, banks cannot distinguish between potentially ‘good’ and ‘bad’ investment projects, thus, they may be encouraged to increase the interest rate. Firms with lower likelihood of success will be willing to pay higher interest rates. These are usually firms involved with high risk projects as they may not perform in manner consistent to a priory agreed contract, or in the worst case scenario these firms may choose not to repay the loan at all (moral hazard problem). Because of their inability to monitor investment projects banks will choose to increase interest rates leading to credit rationing problem and worsening position of good borrowers who might consider higher interest rates too risky and might chose not to apply for loan at all (although may have viable projects). Under these circumstances, banks will ration the supply of credit and in addition will tighten requirements such as collateral in order to protect themselves from likely opportunistic behavior of dishonest borrowers. In the presence of asymmetric information banks will incur relatively high transaction costs per unit (loan) if they deal with small firms compared to larger firms implying that banks’ administrative costs depend on the number of loans made rather than the size of loans (Parker 2004). Accordingly, cost minimization under competitive conditions obliges banks to make a few large loans rather than many small ones, yielding the required result. Storey (1994a) emphasizes two types of administrative costs—assessment and monitoring costs—that affect bank’s decision to be biased towards larger firms. Assessment costs are incurred prior to the bank decision to lending, and, monitoring costs are incurred when a bank makes sure that customer is acting according to contract. These costs usually are a decreasing proportion of the size of the loan. Under these circumstances banks are more biased toward lending larger businesses as their cost per unit will fall.

Following Stiglitz and Weiss (1981) a large number of studies in the field of small business show that markets for loans are imperfect and restricted in scope even in developed economies, and that the market mechanism fails to address the financing needs of small businesses adequately due to credit rationing resulting from information asymmetry (see, Storey 1994a; Ennew and Binks 1995; Chilosi 2001; Levenson and Willard 2000; Cressy and Toivanen 2001; Ortiz-Molina and Penas 2008).

Smaller firms are also affected by weak institutional environment. Various empirical studies have shown that firms in countries with better functioning financial institutions and stronger property rights system have increased levels of investment funded by external finance compared to internal finance (Berger and Udell 2006). In a cross country analysis, Beck et al. (2005) found that the effect of financial, legal and corruption problems posed more constrains on the growth of smaller firms compared to larger firms. Following same line of reasoning, one would expect that in transition economies characterized by slow development of financial institutions small firms are placed in a disadvantaged position with regard to access to finance. Some of the small growing firms will not be able to fund their project with internal fund.

Factors affecting credit demand

Small firm obstacles in accessing external finance are caused not only by supply side factors or market imperfections, but also by other demand-side factors such as characteristics related to the firm and entrepreneur. Two central points are important to address here. First one is related to the entrepreneur’s willingness to growth and his/her consequent decision whether to apply for a bank credit or choose to finance its project by internal funds. Second point is related to the ability of firms to fulfill bank requirements such as sound financial information, business plan, collateral, and the ability to absorb these loans.

Going back to the financing option of entrepreneur, it is argued that capital structure is similar amongst small firms. For majority of them, internal finance is the major source of funding compared to external funds (see Hughes and Storey 1991). Earlier work by Myers (1984) and Myers and Majluf (1984) have shown that in the presence of information asymmetries firms will prefer internal to external sources of capital suggesting that profitable firms will tend to finance their investment needs with retained profits. Although these authors studied the corporate investment behavior, their approach based on the hierarchy of sources of finance can be easily applied to the small firms (Holmes and Kent 1991; Hamilton and Fox 1998). They suggest that SME managers that are usually shareholders of these companies do not like to decrease either the degree of ownership or control over these firms.

In addition, more recent contribution by Kon and Storey (2003) suggest that it is important to investigate the ‘discouraged borrowers’, something that has been ignored in Stiglitz-Weiss model. They argue that application costs incurred mean that a proportion of good borrower may not apply for a loan to a bank at all, because they feel they will be rejected. Evidence from USA (2000) suggest that more than twice as many small firms are “discouraged borrowers” (in total 6.36% of total sample) as are rejected for loans implying the importance of that “discouragement” (Levenson and Willard 2000).

Many researchers believe that small firms find it difficult to borrow from banks due to lack or insufficient collateral, particular organizational legal form or unstable cash flows (Storey 1994a). A firm operating as limited liability rather than other legal forms has more credibility compared to other legal forms. The limited liability form of business plays a key role in accessing external finance because of increased reputation, in terms of collateral required from owners’ personal property creating synergy effect and indicates the involvement in higher risk than usually and hence higher expected return (e.g. Storey 1994b). Empirical evidence in general supports these propositions. In their study of 11,000 German enterprises covering all sectors Harhoff et al. (1998) suggest that firms registered as limited liability companies have shown higher growth rates because of the entrepreneurs’ choice of legal status reflects the riskiness of projects undertaken and can affect the ability to access external finance.

In developed countries, banks use extensively the owner’s characteristics as a measure of borrower credibility and ability (Berger and Udell 1998; Hartarska and Gonzales-Vega 2006). Education of entrepreneur is among most important factors influencing bank’s lending decision. Existing studies have shown that human capital affects firm’s likelihood to start-up, survive, grow and successfully perform in the market (Brown et al. 2005; Bartlett and Bukvič 2001; Chandler and Hanks 1998; McPherson 1996; Bates 1990). For example, Bates’s (1990) study of a sample of people who entered self-employment in the period of 1976–1982 shows that education of owner-managers can facilitate access to loan inputs. More recent study by Parker and van Praag (2006) also shows that each year of additional schooling decreases capital constraints by 1.18 percentage points. Their study shows that both workers’ and entrepreneur’s education seem to impact the entrepreneurial performance directly or indirectly. To put it differently, both studies suggest that the education of owner/manager increases the chance of a firm to receive a loan. This is because educated owner-managers can prepare better business plans and presumably can provide more sophisticated and sound financial information, thus facilitating screening process by banks. For instance, firms that perform well and have audited their financial statements are less likely to be credit constrained (Jappelli 1990; Levenson and Willard 2000). The education of the owner-manager can act also as a signaling for good reputation which may enhance chances for successful loan application.

The provision of sufficient collateral by firms is viewed as one of the solutions in preventing the opportunistic behavior of bad borrowers under asymmetric information conditions. Use of collateral can serve banks as a device to screen out high risk from low risk borrowers. However, if collateral is limited in supply, the financing gap would continue to persist. Therefore, relatively larger firms are more likely to have access to debt finance because of their ability to provide collateral and to meet the bank’s requirements. This means that not all applicants with high quality investment projects, especially the start-up businesses will be able to meet the banks’ requirements and obtain a loan. In the next section we present methodology and data used in this paper.

Methodology

Description of the sample and data

The data used in this paper was collected as part of a wide-ranging Survey of 600 SMEs in Kosova. The survey was conducted by the Riinvest Institute for Development Research at the end of 2006. The answers regarding financial issues provided by owners/managers of SMEs relate to 2005. The sample is drawn randomly from the business register kept at the Statistical Office of Kosova (SOK). The sample represents about 2 percent of the total population of the SMEs. This random sample enables to draw generalized conclusions about the whole population of SMEs. The sample includes SMEs across all regions of Kosova. The sample is stratified by three main sectors in order to reflect the differences between trade, production, and services. Statistical stratification was done also in terms of size in order to ensure the representation of SME sector. The interviews were conducted face-to-face with the key people in each enterprise, mainly owner /managers or financial managers. The respondents were asked to provide qualitative (their perceptions of the business environment and future prospects) and quantitative answer on internal characteristics of the respective firm (years in the business, location, size of the company in terms of employment, value of assets, sector of activity, etc), financial information performance indicators (profitability and level of investment, etc) and information on their successful and unsuccessful loan applications.

Banking sector and SME finance in Kosova

In the aftermath of the War (1999), Kosova’s banking system started from the scratch. Old banks were no longer functional and there was a gap until first bank started to operate. Currently there are seven commercial banks which continue to spread their branches and sub-branches around all regions of Kosova (Table 1). More importantly the crediting role of the banking sector has improved since 2002 as the bank credit to private sector has increased from 3.8% in 2002 to 14.7% in 2006. This improvement can be observed also in terms of the increase of the loan to deposit ratio (in the beginning this ratio was too low as main banks i.e. foreign-owned have invested some of their assets in foreign capital markets, especially in EU countries).

Now we turn to the discussion of the SME survey results, Table 2 shows an overview of firms’ investment activities over the period 2001–2005.Footnote 2 The number of firms that made investment in 2005 has decreased significantly compared to 2004 (from 60.7% to 49.2% of firms in the sample). However, the average value of investment in the sample has slightly increased compared to previous years. As a result the average value of investments per enterprise has increased, suggesting that investment is being concentrated in a small number of enterprises. In 2005 the average investment has fallen in the trade sector while showing a significant increase in manufacturing which might be due to a substantially increased competition within the trade sector.

One important change found in the survey is that, the share of the manufacturing sector in total value of investment has increased significantly in 2005 compared to previous years (despite massive fall earlier), although the share of these enterprises in the overall sample remained the same. Services have shown an increase in investment too, while trade sector has experienced a decline.

The survey contains information about the sources of finance for funding investment. The survey findings reported in Table 3 show that about 72% of investment in SMEs has been financed by internal sources, suggesting the importance of internal funds for SME growth. The share of internal funds on SME investment seems to have remained stable over time despite the development of banking sector and growing external finance opportunities. On the other hand, we find that share of other sources of finance in funding SME investment has decreased. Such sources mainly include borrowing from family and friends and finance through foreign investment. Most interestingly, the share of banks in SMEs’ investment has increased continually from about 14% in 2002 to about 22% in 2005.

In addition, the survey evidence also shows that not all the firms that asked for loans received such loans. Of all firms in the sample that applied for loan 241, 199 (82.6%) of them received a loan while only 42 firms (17.4%) were rejected. Although high, the rejection rate is much lower for developed economies. For example, in similar study for UK SMEs, Fraser (2006) reports outright rejection rate of 9%.Footnote 3 These differences might emerge from particular features of transition economies which are characterized with higher rates of growth than in developed economies and, therefore, the demand for external funding will be higher and (given the relatively restricted amount of bank funding available as in Kosova) rejection rates will, therefore, also be higher.

In the survey, we included a question about the reasons of loan refusal. The survey data shows that in the majority of cases, low turnover (59.2%) and lack of collateral 22.4%) are the most frequently emphasized reasons for rejection of applicants. Not only the access to external finance but also the terms and conditions of those who received the loan are important for SME investment and growth. Vast majority of firms who received credit reported unfavorable credit terms and conditions such as high annual interest rates (73% reported interest rates of 10–15%, while 10% reported an interest rates of 16–20%, both in annual terms) and short average repayment period (sample average of 2 years). These terms and conditions of loans, especially short repayment period and lack of grace period hinder mostly the long term investment projects of SMEs.

Model

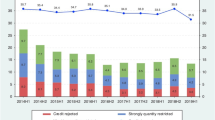

Many empirical studies in transition economies, including Bratkowski et al. (2000) ignore sample selection bias in their empirical studies. In this section we take into account selectivity issue. In our survey we ask firms whether they were able to finance their projects with external funds (bank loan) differentiating between firms that applied for loan from those who did not apply. However, we can observe whether they were selected by banks to receive a loan only if they applied for it. As shown in Fig. 1, from overall sample only 241 firms applied for loan. If we focus only on loan recipients we are ignoring the selection issue. Presumably, not all firms decide to apply for a loan even if they need one. Some of them chose not to apply at all because they believe that will be rejected because they do not fulfill banks requirements i.e. discouraged borrower. In addition banks do not choose the loan applicants at random. We cannot, therefore, observe all pool of applicants for loan and hence cannot estimate the demand function for loan.

The credit demand and supply in SME sector in Kosova

Given this limitation, we can estimate the probability of firm receiving a loan conditional upon applying. In order to account for this sample selection bias one should consider a model of sample selection bias as the usual probit estimation method is not appropriate (see e.g., Rand 2007; Hartarska and Gonzales-Vega 2006).Footnote 4 We follow Wooldridge (2005) to explain the procedure of dealing with such methodological concerns. Accordingly, we can estimate the binary response model with sample selection if we assume that the latent errors are bivariate normal and independent of the explanatory variables.

The first equation denotes the probability of firm receiving a loan while second equation is the sample selection equation and y 1 or the information whether the firm has received a loan or not is observed only if y 2 = 1. As can be noted we can loose information about the firms that are eligible to receive a loan but they did not choose to apply, if we use Eq. 2 which can lead to an inconsistent estimator of β 1. We assume that error terms in both equations (u 1,u 2) are independent of x and with zero-mean normal distribution and unit variances u 1 ∼ N(0,1) and u 2 ∼ N(0,1). What we need is the density of y 1 conditional on x and y 2 = 1. The correlation between the error terms of both equations is corr = (u 1,u 2) = ρ. The probit estimation of the Eq. 2 produces inconsistent β coefficients if ρ ≠ 0 suggesting that two error terms are correlated. According to Wooldridge (2002), a joint distribution of y 1 and y 2 (y received and y applied , respectively) given x is needed for estimation. In this particular case is expressed as follows:

where y received stands for credit supply, y applied stands for firms that applied for a loan; and x is a vector of several variables that affect credit supply. Therefore, δ in Eq. 2 is estimated by probit of y applied on x while β and ρ is estimated based on Eq. 1. Specifically x includes a measure of firm’s growth, profitability, entrepreneurial ability indicators (education, gender, and age), transparency (use of international accounting standards), value of the assets and other control variables such as firm age and industry type (see Tables 6 and 7 in the Appendix for details).

To properly identify how factors affecting the probability of demand for loan, differ from factors affecting the probability of supply, the number of explanatory variables included in the second equation should be added to the group of explanatory variables included in first equation. These explanatory variables are expected to affect the probability of applying for loan but not the probability of receiving a loan. As suggested, by Wooldridge (2002) the number of explanatory variables included in selection equation x should be greater than number of explanatory variables included in x 1 at least by one.

Discussion of empirical findings

Econometric findings from probit model with sample selection are presented in the Table 4. The first panel refers to the ‘main equation’ where the dependent variable is dichotomous equal 1 if firms received a loan and 0 otherwise. The second panel (B) refers to the ‘selections equation’ where the dependent variable is dummy equal to 1 for firms that applied for loan and 0 otherwise.

According to estimated \( {\chi^2}_{(1)} \), the estimated ρ presented at the bottom of the panel B for three models is significantly different from zero suggesting that firms that have received the loan are not randomly selected by banks from the group of firms that applied for loan. In addition to above diagnostics, we tested for multicollinearity using Variance Inflated Factor (VIF) in STATA which suggested that multicollinearity was not a problem in our estimations (see StataCorp 2003). The correlation matrix, presented in Table 8 in the Appendix, confirms this as the correlations between individual variables are very low. All maximum likelihood models have passed the statistical test for joint statistical significance of explanatory variables (see Wooldridge 2005). Now we turn to the discussion of the findings for both, main equation and selection equation.

Findings from main equation: credit supply

Table 4 presents findings for three estimated models. As can be noted there is no qualitative difference between three models, except that in model 2 in which we included variables indicating owner-manager characteristics such as age and gender whereas in model three we exclude those variables and include the dummy variable indicating whether the firm previously had access to an informal loan. Findings suggest that only three coefficients are statistically significant in the main credit supply equation (at 10% level of significance across almost all specifications). The findings from three models suggest high degree of self-selection among the firms that choose to apply for loans. Borrower’s transparency and ability to provide more qualitative information to banks seems to alleviate the asymmetric information between the bank and borrower. Those firms that provide informative accounts enable lenders to evaluate creditworthiness of firm easier and more accurately. Firms that are more transparent in the sense of keeping accounts in accordance to modern international accounting standards increases the likelihood to receive a loan from banks.

One of the characteristics of credibility is education of the owner/manager. Findings suggest that from personal characteristics of the owner/manager, bank’s lending decision in Kosova is based only on education of owner-managers having positive and statistically significant impact credit allocation. This may suggest that more educated owners can write good business plans and provide good financial information, increasing their chances of receiving loans. This finding contradicts the study of Hartarska and Gonzales-Vega (2006) for young firms in Russia who found that education does not play an important role for bank lending decision. However, Rand (2007) found a negative effect of education on accessing credit, justifying it on the basis that educated owner-managers are more likely to know when their application will be rejected and therefore are more discouraged and refrain from applying. Regarding age and gender we do not find statistically significant support.

Findings also support the view that bank’s lending decision also is based on size of the firm (measured as value of the assets) indicating that banks try as much as possible to mitigate opportunistic behavior and information asymmetry by using collateral. Private sector in Kosova is of recent origin with majority of firms being very young (average less than 9 years) which creates information problems for banks to use past performance records. Therefore, banks require collateral in order to deal with such problems suggesting that larger firms with more fixed assets are more likely to access bank funds. This is supported by statistically significant effect of the firm size on successful loan application which may capture the effects of reputation and the availability of collateral. Holding other things equal the larger the firm is the better known it is to the market, therefore more able to provide capital/collateral which serves as a signaling for quality of projects to banks.

Unlike other studies we do not find evidence that bank’s lending decision is based on performance indicators such as profitability and employment growth. This may be explained by the findings from selection equation because these variables are highly significant suggesting that self-selection mechanism works very well in credit market in Kosova—only good performers choose to apply for loans as we will argue in the next section.

Findings from the selection equation: credit demand

Findings from the selection equation show a high degree of the self-selection mechanism. Note that all variables measuring performance of the firm are statistically significant at conventional level of significance (employment growth, profitability) in all specifications. This finding suggests that firms that perform well regarding their growth and profitability are those who seek access to external finance reflecting a self-selection of firms towards good performers. This is supported by EBRD (2006) data for commercial banks showing very low default rate of borrowers in Kosova compared to other transition economies, especially compared to neighboring countries such as Serbia and Montenegro and Macedonia (see Table 9 in Appendix).

Finding from selection equation also suggest that firms who have future expansion plans have the higher probability of applying for a loan suggesting the need of external funds for financing investment projects for growth-oriented entrepreneurs. Finally, size of the firm is statistically significant indicating that larger firms apply more for loans. Larger firms maybe more confident in their ability for fulfilling bank’s requirements, and thus are more likely to apply for loans. This outcome also may suggest that firms with greater assets are more likely to receive a loan and also tend to experience less discouragement since they have more collateral to offer lenders.

The variable firm age is statistically insignificant in both equations. This may indicate that majority of firms are new which is insufficient for establishing reputation and hence provision of information in terms of firm’s pervious performance which can serve as signaling to banks to screen out applicants.Footnote 5 Sector dummies are insignificant, as well. In model 3 we have included the dummy variable indicating whether or not firms have access to informal loan. Results suggest high statistical significance for this coefficient. Contrary to findings from small firm sector for Russia (Hartarska and Gonzales-Vega 2006) we find that firms that had access to informal loan (family and friends) actually are more likely to apply for loan. The same coefficient is not significant in supply equation which may suggest that owners that had informal loans are more certain in their ability to access a loan while for banks this is not an important indicator measuring reputation of the borrower which of course is not easily observable by banks as can be for informal providers of such loans (e.g. family and friends) which may have insider information about the project. However, in this survey we lack the data on past credit history.

In Table 5 we report corresponding marginal probabilities of receiving a loan conditional on applying. Holding everything constant, firms that apply for loan on average have 0.86 probability of receiving it suggesting high degree of self-selection.

Conclusions and policy implications

This paper examined the determinants of obtaining bank credit conditional upon applying based on SME survey. The results of the SME survey show that not all the firms receive credit they apply for, suggesting a slight excess of demand over supply of credit. Not only the access to external finance but the credit terms and conditions are important barriers for growth of small firms that accessed bank loan. The vast majority of firms who received credit in the sample reported inadequate credit terms and conditions, high annual interest rates and short average repayment period. The main reasons for rejecting small firm credit applications by banks are firm’s low turnover and lack of collateral.

In addition to survey results, econometric evidence (credit demand and supply regressions) indicates that commercial banks base their decision to loan firms primarily on the basis of collateral. Firms with high value of assets are more likely to access external sources compared to the rest of firms. The profitable firms are more likely to ask for loans but in addition the profitability does not seem to be sufficient signalling for banks in order to allocate credits. Banks prefer more to secure themselves from likely opportunistic behaviour of potentially “bad borrowers” with use of collateral in a country where business history of firms is of recent origin. Econometric results are in line with theoretical and empirical arguments that systematic use of collateral can mitigate the adverse selection by banks in choosing whom to allocate the credit. The results also suggest that entrepreneurs who have optimistic expectations about future of their business are more likely to ask for loans as those firms are eager to exploit these business opportunities. Also firms that have received an informal credit in the past they are more likely ask for loans again but less likely to receive it.

Education of owner/manager seems to be an important variable influencing positively the probability of the bank’s decision to allocate a loan. Education increases entrepreneur’s ability to fulfilling bank’s requirements and possibly preparing a better business plan which may act as a good signal to banks. Age of the firm is not significant variable in explaining the likelihood of receiving a loan. This finding reinforces the importance of the short history of firms on creating past financial performance indicators which are crucial in screening process of applicants. When controlling for sectors our evidence suggests that sector activity is not significant variable explaining neither probability to apply for loan nor probability to receive a loan. The idea that manufacturing firms incur higher investment does not hold in case of Kosova. Although, banks seems to prefer short term financing because of risk dispersion and manageability they seems not to discriminate between firms operating in different sectors.

Empirical findings have some important policy implications for a country. High degree of self-selection of firms when applying for loans suggests to some extent the exaggeration of the issue of restricted access to external finance in transition economies. Nevertheless, finance remains an important ingredient for growth of small firms because one should take into consideration not only access to loans but in addition terms and conditions for loans that have a vital role once firm accessed loan. This include short loan repayment period and high interest rates which mostly affect the firms belonging to manufacturing which are usually involved in longer term investment projects may act as impediment to growth of private sector which consequently hinders economic growth of Kosova. Findings signal the need that government should make efforts in stimulating supply side of credit and implement other measures to assist banks in reducing risk. For example government may support banks via small firm guaranty schemes, may give various certificates to small firms which have met certain quality standards in technology, passed successfully certain examination by quality assurance institutions or won competition (see Kon and Storey 2003). This will help banks to screen best applicants. On the other hand Government can support firms with various services such as dissemination of information on interest rates, support and advice in writing business plans. Both these aspects can help reduce information asymmetry and create better conditions for society not loosing potentially good projects.

Finally, this paper identifies a number of limitations and areas of future research. The key limitation of our empirical investigation arises from qualitative nature of survey data. First, some of our variables of interest are self-reported rather than exact figures taken from company accounts. Majority of companies in our sample are not subject to the stricter reporting requirement of joint stock companies and thus it is not possible to obtain their official accounts. Second, profitability measure is qualitative type of self-reported data by owner/managers, although it is likely that qualitative measure of profitability is more realistic in this kind of studies in transition economies but not a first best for regression analysis. Finally, we do not have a panel data in order to have dynamic approach in investigating the relationship between investment and sources of finance. Also, this would enable to investigate bank-firm relationships and their role on provision of bank finance. The study also points to further research on empirical investigation of ‘discouraged borrowers’ as well as issue of preference of entrepreneurs over internal funds compared to external sources of supply. Both these aspects can shed light on better understanding of supply and demand for credit especially in economies with weak institutional environment.

Notes

The term ‘small firm’ and ‘SME’ will be used interchangeable in this paper. Enterprises that employ less than 250 employees are considered SMEs (OECD and European Commission). Medium enterprises are considered those with 50–249 employees, small enterprises with 10–49 employees and micro enterprises up to 9 employees.

For more details on the SME Survey results see Riinvest (2006).

There are three types of loan rejection (Fraser 2006, p.6): outright rejection, partial rejection (i.e., the businesses were offered less than they wanted) and discouragement (i.e., the businesses did not apply for new finance because they believed they would be rejected). In this paper we have data only on first type of rejection.

The sample selection bias was first introduced by Heckman (1979).

Note that all firms in Kosova had to reregister in aftermath of the War (1999) so there were changes in the names of the companies creating more difficulties for banks to track performance of the companies in the past (before the War) as banking system was destroyed completely.

References

Ang, J. S. (1991). Small business uniqueness and the theory of financial management. The Journal of Small Business Finance, 1(1), 1–13.

Bartlett, W., & Bukvič, B. (2001). Barriers to SME growth in Slovenia. Economic Policy in Transition Economies, 11(2), 177–195.

Bates, T. (1990). Entrepreneur human capital inputs and small business longevity. The Review of Economics and Statistics, 72(4), 551–559.

Beck, T., Demirguc-Kunt, A., & Maksimovic, V. (2005). Financial and legal constraints to firm growth: does firm size matter? Journal of Finance, 60, 137–177.

Berger, A. N., & Udell, G. F. (1998). The economics of small business finance: the roles of private equity and debt markets in the financial growth cycle. Journal of Banking & Finance, 22(6–8), 613–673.

Berger, A. N., & Udell, G. F. (2006). A more complete conceptual framework for SME finance. Journal of Banking and Finance, 30, 2945–2966.

Bratkowski, A., Grosfeld, I., & Rostwoski, I. (2000). Investment and finance in de novo private firms: empirical evidence from the Czech Republic, Hungary and Poland. Economics of Transition, 8(1), 101–116.

Brown, D., Earle, S., & Lup, D. (2005). What makes small firm grow? Finance, human capital, technical assistance, and the business environment in Rumania. Economic Development and Cultural Change, 54(1), 33–70.

Central Banking Authority of Kosova CBAK (2007). Annual report. Prishtinë: Central Banking Authority of Kosova.

Chandler, G., & Hanks, S. (1998). An examination of the substitutability of founder’s human and financial capital in emerging business ventures. Journal of Business Venturing, 13(5), 353–369.

Chilosi, A. (2001). Entrepreneurship and transition. Economic Policy in Transitional Economies, 11(4), 327–357.

Cressy, R., & Toivanen, O. (2001). Is there adverse selection in the credit market? Venture Capital: An International Journal of Entrepreneurial Finance, 3(3), 215–238.

Ennew, Ch, & Binks, M. (1995). The provision of finance to small businesses: does the banking relationship constrain performance. The Journal of Small Business Finance, 4(1), 57–73.

European Bank for Reconstruction and Development EBRD. (2006). Transition report. London: EBRD.

Fraser, S. (2006). Finance for small and medium-sized enterprises: a report on the 2004 UK survey of SME finances. Coventry: Centre for Small and Medium-sized Enterprises, Warwick Business School.

Gregory, B. T., Rutherford, M. W., Oswald, S., & Gardiner, L. (2005). An empirical investigation of the growth cycle of small firm financing. Journal of Small business Management, 43(4), 382–393.

Hamilton, R. T., & Fox, M. A. (1998). The financing preferences of small firm owners. International Journal of Entrepreneurial Behaviour & Research, 4(3), 239–248.

Harhoff, D., Stahl, K., & Woywode, M. (1998). Legal form growth and exit of west German firms-empirical results for manufacturing, construction, trade and service industries. The Journal of Industrial Organization, 46, 453–488.

Hartarska, V., & Gonzales-Vega, C. (2006). What affects new established firms’ expansion: evidence from small firms in Russia. Small Business Economics, 27, 195–206.

Hashi, I. (2001). Financial and institutional barriers to SME growth in Albania: results of an enterprise survey. Economic Policy in Transitional Economies, 11, 221–238.

Heckman, J. J. (1979). Sample selection bias as a specification error. Econometrica, 47, 153–161.

Holmes, S., & Kent, P. (1991). An empirical analysis of the financial structure of small and large Australian manufacturing enterprises. The Journal of Small Business Finance, 2, 141–154.

Hughes, A., & Storey, D. (1991). Finance and small firm. London: Routledge.

Hutchinson, J., & Xavier, A. (2006). Comparing the impact of credit constraints on the growth of SMEs in a transition country with an established market economy. Small Business Economics, 27(2–3), 169–179.

Jappelli, T. (1990). Who is credit constrained in the U. S. economy? Quarterly Journal of Economics, 55(1), 219–34.

Kon, Y., & Storey, D. (2003). A theory of discouraged borrowers. Small Business Economics, 21, 37–49.

Krasniqi, A. B. (2007). Barriers to entrepreneurship and SME growth in transition: case of Kosova. Journal of Developmental Entrepreneurship, 12(1), 71–94.

Levenson, A., & Willard, K. (2000). Do firms get the financing they want? Measuring credit rationing experienced by small business in the U.S. Small Business Economics, 14, 83–94.

Low, C., & Mazzarol, T. (2006). Owner-managers’ preferences for financing: A study of Singaporean SME. ICSB, World Conference 2006, Melbourne. 19–21 June.

McPherson, M. (1996). Growth of micro and small enterprises in southern Africa. Journal of Development Economics, 48, 253–277.

Myers, S. C. (1984). The capital structure puzzle. The Journal of Finance, XXXIX(3), 575–592.

Myers, S. C., & Majluf, N. S. (1984). Corporate financing and investment decisions when firms have information that investors do not have. Journal of Financial Economics, 13, 187–221.

Ortiz-Molina, H., & Penas, F. M. (2008). Lending to small businesses: the role of loan maturity in addressing information problems. Small Business Economics, 30, 361–383.

Parker, S. (2004). Economics of self-employment and entrepreneurship. Cambridge: Cambridge University Press.

Parker, S., & van Praag, M. (2006). Capital constraints and entrepreneurial performance: the endogenous triangle. Journal of Business and Economic Statistics, 24(4), 416–431.

Pissarides, F., Singer, M., & Svejnar, J. (2003). Objectives and constraints of entrepreneurs: evidence from small and medium size enterprises in Russia and Bulgaria. Journal of Comparative Economics, 31(3), 503–531.

Rand, J. (2007). Credit constraints and determinants of cost of capital in Vietnamese manufacturing. Small Business Economics, 29, 1–13.

Riinvest Institute for Development Research. (2006). SME development in Kosova. Research report, Riinvest, Prishtinë: Riinvest.

Saridakis, G., Mole, K., & Storey, D. (2008). New small firm survival in England. Empirica, 35, 25–39.

Solymossy, E. (2005). Entrepreneurship in extreme environments: building an expanded model. The International Entrepreneurship and Management Journal, 11(4), 501–518.

StataCorp. (2003). Stata statistical software: release 8.0. College Station: Stata Corporation.

Stiglitz, J., & Weiss, A. (1981). Credit rationing in markets with imperfect information. American Economic Review, 71(3), 912–927.

Storey, D. (1994a). Understanding small business sector. London: International Thomson Business.

Storey, D. (1994b). The role of legal status in influencing bank financing and new firm growth. Applied Economics, 26, 129–136.

Wooldridge, J. (2002). Econometric analysis of cross section and panel data (2nd ed.). London: The MIT Press.

Wooldridge, J. (2005). Introductory econometrics: A modern approach (3rd ed.). Mason: Thompson Higher Education.

Author information

Authors and Affiliations

Corresponding author

Appendix

Appendix

Rights and permissions

About this article

Cite this article

Krasniqi, B.A. Are small firms really credit constrained? Empirical evidence from Kosova. Int Entrep Manag J 6, 459–479 (2010). https://doi.org/10.1007/s11365-010-0135-2

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11365-010-0135-2