Abstract

Environmental sustainability involves meeting current needs without compromising the abilities of future generations. Practical steps must be taken to prevent pollution, decrease waste, and utilize resources. This study investigates the predictors of environmental sustainability in SMEs, focusing on the role of environmental management accounting and environmental proactivity in linking pollution prevention strategies to environmental sustainability using the natural resource–based view theory. This study surveyed 308 Pakistani SMEs employees and tested the data using SPSS v28 and AMOS v26. The results show that pollution control initiatives increased the usage of environmental management accounting, which in turn had a positive impact on environmental sustainability. The study also finds that environmental proactivity is significantly moderate and that environmental management accounting mediates these associations. To the best of our knowledge, this study is unique in that it is the first to provide sustainable implications based on the current framework. This study highlights the importance of implementing pollution prevention strategies, integrating environmental management accounting practices, and fostering environmental proactivity to enhance environmental sustainability performance in SMEs in Pakistan, ultimately leading to improved business competitiveness, positive environmental impacts, and a sustainable future. SMEs can focus on implementing proactive pollution prevention strategies such as waste reduction, energy conservation, and resource optimization. By adopting a proactive approach to pollution prevention, SMEs can reduce their environmental impact and enhance their sustainability performance.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

Environmental sustainability (ES) implies meeting the immediate needs of the present generation in a way that does not jeopardize future generations’ abilities or the right to do the same. Actions instigating these rights and that should be performed include activities, such as preventing soil, water, and air pollution, reducing waste production and the usage of hazardous products, conserving resources, and reusing them when appropriate (Elleuch et al. 2018). ES is a broad measure that improves the reliability and legitimacy of reporting procedures on environmental issues. However, empirical research shows that using the same antecedents in several settings does not boost performance (Appannan et al. 2022). As a result, numerous studies on ES have produced conflicting findings, largely because of several methodological challenges. These challenges include a limited scope of research, small sample sizes, the utilization of outdated data, and the intricate nature of sustainable development (Appannan et al. 2022; Hsu et al. 2013). According to a 1987 UN report by the General Assembly, environmental pollution has negative effects on human health (Imperatives 1987). Moreover, the Paris Agreement has set forth the objective of curbing global warming to a maximum of 2.0 °C, with renewed efforts to limit it to 1.5 °C. Additionally, the United Nations 2030 Agenda for Sustainable Development underscores the vital responsibility of businesses in leveraging their financial, technological, and resource mobilization capabilities to promote sustainability, as highlighted in the Sustainable Development Report (2018).

Nevertheless, ongoing conflicts persist between economic progress, energy consumption, and environmental pollution. Raza et al. (2021) stated that Pakistan is the most polluted country in South Asia, responsible for 0.87% of global emissions in 2016. The industrial sector fueled by coal is the largest energy consumer, contributing over 49% of Pakistan’s CO2 emissions (Yearbook 2021). Over the past two decades, industrial CO2 emissions have skyrocketed from 17.21 to 95.2 Mt in 2019 (EDGAR 2020). Lin and Long (2016) stated that the rising energy demand for economic development is a major factor driving this pollution crisis. Immediate action is needed to explore sustainable alternatives and combat the severe pollution problems in Pakistan. The increasing industrial demand is expected to cause more pollution. SMEs are recognized as crucial cornerstones of the economy because of their substantial role in poverty reduction, economic growth, and employment creation. In Pakistan, SMEs account for approximately 92% of all business establishments, contribute to nearly 40% of the country’s GDP, make up approximately 26% of the manufacturing sector’s exports, and generate 79% of the country’s industrial employment (PBS 2021). In Pakistan, a lack of strict adherence to environmental regulations and policies in the manufacturing sector has resulted in widespread environmental degradation. SMEs often struggle to develop environmentally sustainable strategies, as their primary focus is on maximizing profits rather than environmental concerns (Ibrahim and Mahmood 2022). Implementing proactive environmental strategies that prioritize strict compliance with environmental regulations, emphasizing the significance of environmental issues, effectively managing environmental risks in daily operations, and promoting overall environmental protection can lead to improved environmental performance for SMEs.

However, the pollution caused by waste remains a critical concern for achieving sustainability. To effectively address this challenge, a proactive approach that focuses on preventing pollution from occurring in the first place is considered the most viable solution. This necessitates the creation of new methods of efficiency, judgment, and appreciation for every resource (Elleuch et al. 2018). Understanding the production and reduction of waste helps lessen trash and protect the environment. A pollution prevention (PP) strategy is a vital component of sustainability (Awan et al. 2019). This shows that in the modern world, there are countless natural disasters that, which despite being referred to as “natural calamities,” are caused by the unsustainable form of human behavior that has spread worldwide in recent decades (Appannan et al. 2022). Both non-profit and for-profit SMEs carry out a variety of tasks as socio-environmental systems undergo rapid changes that form their environmental strategies. This outlines the activities that eco-conscious businesses engage in to spread internal environmental knowledge to employees and consumers, with the goal of enhancing existing skills to produce effective operations (Appannan et al. 2022; Dyer and Singh 1998).

Early studies, such as those by Montabon et al. (2007), show that environmental strategies and company performance are interrelated. Graham and Potter (2015) also examined environmental strategies employing the PP process, demonstrating that these techniques have a strong relationship with firms’ environmental and financial success. Similar findings were shown by Zailani et al. (2012) and Prajogo (2016), who found that environmental policies forced businesses to comply with rules and pinpoint the core competencies driving improvements, which can lead to sustainability. Based on Banerjee’s (2002) definition of environmental strategy, Zhang et al. (2019) declared positive correlations of green human resource management on environmental performance. Scholars, such as Ferreira et al. (2020), Amir et al. (2020), and Chaudhry and Amir (2020), have investigated the role of environmental management accounting (EMA) in this regard, which is a particular innovation that highlights the range of conventional techniques and procedures to increase the efficacy of environmental management. Consequently, the EMA recognizes, gathers, and assesses financial and nonfinancial data to make environment-related decisions (Appannan et al. 2022). Studies have shown that using tools such as material flow cost accounting (MFCA), activity-based costing (ABC), or life cycle assessment (LCA) can inspire employees to adopt eco-friendly behaviors and enhance environmental performance (Duran and Afonso 2020; Ibrahim and Mahmood 2022; Sulong et al. 2015). These techniques can help identify emerging threats and opportunities, facilitate informed decision-making and coordination, align organizational goals and values, and promote a culture of learning (Ibrahim and Mahmood 2022).

Similarly, the development of proactive environmental strategies, such as environmental proactivity (EP), for manufacturing SMEs in Pakistan deserves investigation. This is because the cumulative environmental impact of the manufacturing SME sector could surpass overall health and biodiversity concerns, global economic stability (Dey et al. 2020), and environmental performance (Anwar and Li 2021; Mamun 2021). However, there is a lack of research and varying opinions on the relationship between environmental proactivity (EP) and environmental sustainability. Some studies (Ahmad et al. 2021; Ibrahim and Mahmood 2022; Ong et al. 2019) support a significant positive relationship, while other studies (Chaudhry and Amir 2020; Reyes-Rodríguez et al. 2020; Shah and Soomro 2021) do not support this relationship. Previous research has revealed that several shortcomings may have a substantial impact on ES. Kumar et al. (2021) recommended that future scholars broaden the scope of the environmental literature to include other components of business models to delineate their impacts on sustainability. Scholars have also repeatedly urged to view sustainability beyond organizational boundaries (Kotzé et al. 2017) and examine how a business organization can utilize control to achieve sustainability through environmental accounting procedures (Appannan et al. 2022; Tumpa et al. 2019). Studies claim that EMA presents long-term sustainability with profitable outcomes that advance toward enhanced sustainability (Gibassier and Alcouffe 2018). Moreover, other proactive measures of pollution avoidance lessen adverse environmental effects while enhancing corporate profitability and sustainability, which is a major gap in the literature for developing nations and requires further investigation (Christ and Burritt 2017). Recent studies have highlighted the need to explore the mechanisms underlying ES (Awan et al. 2019; Ferreira et al. 2020; Sturiale et al. 2020).

Therefore, this study aims to fill these gaps in the literature on ES using PP, EMA, and EP under the theoretical support of the NRBV in the SMEs of Pakistan. Therefore, in line with this research gap, this study assesses the effects of PP strategies on the ES of firms operating in Pakistan’s SMEs, with the mediating role of EMA and the moderating role of EP. This study has many benefits to the theory as it establishes the underlying and boundary mechanisms for the path connecting PP strategies and ES. The findings of this study also contribute to the theoretical foundations by providing a unique model that integrates the study variables. Likewise, this study allows managers of firms to understand how their companies’ ES can be enhanced by inculcating PP strategies, managing their EMA, and being proactive in activities linked to the betterment of the environment.

Literature review and conceptual framework

The current study is based on the natural resource–based view theory (NRBV) and conceptualizes ES using the theory proposed by Hart (1995). This is a well-known management theory used by businesses to analyze their resources and gain a competitive edge (Hart 1995). This is ahead of the resource-based view (RBV), in which organizational, physical, and human resources comprise the three primary resource categories for firms (Barney 1991). The NRBV suggests that SMEs strategically manage their resources and capabilities in relation to PP, EP, EMA, and ES and can create a competitive advantage by developing unique and valuable environmental management capabilities that contribute to their overall performance and sustainability. The NRBV fills the gaps left by the RBV theory in its contempt for the natural world (Appannan et al. 2022). Hence, NRBV suggests that PP is the main strategy for overcoming natural environmental issues. Therefore, the present study expands upon previous research by examining the strategies described in the NRBV theory. Prior investigations have mainly focused on only a few dimensions, and the NRBV literature has primarily addressed the first two environmental strategies, namely, PP and EMA (Ibrahim and Mahmood 2022). This study proposes that all three main strategies, including EP, should be considered as part of overall environmental solutions and contribute to environmental sustainability.

Pollution prevention strategies, EMA, and environmental sustainability

Controlling pollutants reduces the amount of pollution generated by processes, such as industry, agriculture, and consumers (Elleuch et al. 2018). PP strategies seek to increase the effectiveness of a process to reduce the amount of pollution produced at its source (Appannan et al. 2022). Hence, the first phase of the internal strategy for performance improvement is outlined by NRBV as a PP strategy. Businesses must have a PP program at the internal operation level to lessen negative production-related environmental actions. This can be achieved by stopping the emissions before they begin. According to Ibrahim and Mahmood (2022), eliminating waste products from manufacturing processes boosts productivity by reducing compliance and responsibility costs, minimizing the need for raw materials, and streamlining operations (Appannan et al. 2022). By lowering operating expenses, innovation in pollution avoidance can increase production. According to Graham and Potter (2015), PP strategies directly affect environmental performance and increase sustainability. These strategies develop product design-based technologies to lower costs while maintaining current revenues. Among the strategies for preventing pollution utilized by firms include SWM, which stands for “structured waste management priority and monitoring”; EEM that implies “employee readiness, empowerment, and motivation”; CAF that stands for “compliance adherence focus”; and EMF which means “expertise, methods, and financial goal setting” (Appannan et al. 2022; Patwary et al. 2023a, b). Therefore, these strategies revolve around how firms manage and monitor waste materials through structured plans and systems. It also encompasses the extent to which employees are ready, motivated, and empowered to take environment-related initiatives, the compliance of these actions, and the setting of environment-related goals and methods. To ensure competitive advantages, environmental techniques require support from internal systems and structures (Burritt et al. 2019). By adopting EMA, managers can take advantage of potential PP strategies. Ngwakwe (2011) established a connection between PP investment and waste costing in Nigerian firms. Likewise, Agustia et al. (2019) found a significant impact of EMA on SMEs’ performance. The implementation of a prevention strategy requires support from internal structures and systems to secure competitive advantage (Bhupendra and Sangle 2015; Chaudhry and Amir 2020; Graham and McAdam 2016; Graham and Potter 2015; Zhang et al. 2019). Furthermore, Appannan et al. (2022) noted that an informed choice regarding an anti-pollution remedy is made while considering environmental costs. Studies support the positive link between PP strategies and sustainability (e.g., Appannan et al. 2022; Awan et al. 2019; Elleuch et al. 2018), indicating that a positive association may exist between the incorporation of PP strategies in firms with EMA and ES. Hence, the following hypotheses are proposed based on this debate:

-

H1: The impact of PP strategies on EMA is positive and significant.

-

H2: The impact of PP strategies on ES is positive and significant.

Role of environmental management accounting

The EMA system is a comprehensive framework that facilitates the monitoring, analysis, and reporting of potential environmental impacts and consequences within an organizational context (Burritt et al. 2019). It addresses prevalent issues in conventional accounting systems, such as excessive waste and losses, suboptimal resource utilization, inefficient labor and energy usage, and escalation of input costs. The EMA system offers a systematic approach to identifying, quantifying, and managing these environmental concerns, thereby promoting more sustainable business practices and improving overall environmental performance. According to Abdullah et al. (2019), the EMA concept was initially categorized into physical and monetary information, and it was developed as a part of sustainability. The output of physical components such as materials, energy, and water occurs gradually, without ignoring important information, as noted by Burritt et al. (2019) in their study. However, financial environmental information outlines the financial effects resulting from environmental expenses (Rounaghi 2019). The inclusion of these features simplifies the process by which employees acquire new knowledge and engage in innovative initiatives, ultimately transforming the way a business is conducted by minimizing inefficiencies and enhancing sustainability practices (Appannan et al. 2022). EMA tools such as MFCA, ABC, and LCA discriminate between unaccounted environmental costs (Appannan et al. 2022). For instance, studies have investigated how the EMA accounting tool can change the system to carbon free; hence, adopting EMA lessens the significant environmental impacts in a variety of industries and turns into an important prospect that helps SMEs achieve their economic and environmental goals (Sulong et al. 2015). It also enhances environmental performance and makes it possible for current strategies to increase profitability and reduce the massive environmental impacts in a variety of industries (Graham and Potter 2015; May and Guenther 2020). Moreover, pollution control makes firms more environmentally friendly (Chowdhury and Hamid 2013; Hoque and Clarke 2013). Results based on NRBV techniques have improved performance, and several studies have used indirect mechanisms to investigate this connection. For instance, studies have stated that EMA, as a mediator, improves the link between firm performance and PP methods (Graham and McAdam 2016; Solovida and Latan 2017). Additionally, previous research has used several ways to illustrate various notions of business strategies that followed the trajectory of sustainability. PP strategies that utilize EMA techniques can contribute to the sustainable development of businesses and enhance ES, particularly when proactive measures are taken to prevent pollution (Nath and Ramanathan 2020). However, only a few studies have examined the connection in which a strong EMA process can assist businesses in making wise decisions based on accurate, current, updated, and integrated financial and physical information for PP and to improve organizational performance and environmental sustainability (Appannan et al. 2022; Gibassier and Alcouffe 2018; Graham ad Potter 2015). Similarly, Agustia et al. (2019) find a positive correlation between the adoption of PP and firm value, with EMA serving as an intervening variable. Hence, the PP strategies incorporated by firms can help better control and manage the EMA, which leads to enhanced ES. This shows that EMA directly and indirectly and significantly affects sustainability and may serve as a mediating variable between PP strategies and ES. Therefore, we propose the following hypothesis:

-

H3: The impact of EMA on ES is positive and significant.

-

H4: EMA significantly mediates between PP strategies and ES.

Role of environmental proactivity

Corporate environmental commitment is a crucial factor in today’s highly competitive business landscape. Scholars have identified two contrasting approaches: environmental reactivity, in which companies comply with minimal regulatory requirements, and environmental proactivity, in which companies voluntarily adopt measures to reduce their impact on the natural environment. Therefore, previous research has revealed a spectrum of corporate environmental practices and firms’ performance, ranging from reactive to proactive or vice versa (Ahmed et al. 2021; González-Benito and González-Benito 2005). Conceptual works by renowned scholars such as Hunt and Auster (1990), Winsemius and Guntram (1992), and Naeemah and Wong (2022) propose progressive stages that depict a linear path from reactivity to the highest level of proactivity. These studies suggest that as corporations progress along this path, they tend to implement more voluntary environmental management practices. However, there is limited discussion on whether the emphasis on specific sets of voluntary practices leads to different proactive environmental strategies. This shows that, rather than being reactive to environmental threats, proactive businesses that manage the environment were distinguished by early scholars. According to Sturiale et al. (2020), a proactive environmental strategy refers to the deliberate development and implementation of environmental protection activities by an organization driven by its internal motivations and objectives (Sturiale et al. 2020). No rules govern these self-driven environmental measures. In terms of processes and goods, these proactive environmental protection techniques include preserving waste materials and lowering energy, smoke, hazardous materials, and chemical waste (Seroka-Stolka and Fijorek 2020). EP is often considered a proactive and forward-thinking approach to environmental management, as it aims to prevent or minimize environmental damage before it occurs rather than simply reacting to incidents after they occur. It is seen as a more sustainable and responsible approach to environmental management as it focuses on long-term ES and considers the potential impacts of business activities on the environment. By using a proactive approach to environmental management, a firm may reduce environmental degradation through green technologies, procedures, and products (Ahmed et al. 2021). Recently, EP has gained increasing attention in the environmental management literature, as SMEs and individuals recognize the importance of addressing environmental issues proactively to ensure the sustainability of our planet for future generations. The existing literature has extensively explored the relationship between EP and firm performance, that is, economic and environmental. Using empirical approaches, the influence of EP on these performance outcomes was found to be significant (Alrazi et al. 2015; Barba-Sánchez and Atienza-Sahuquillo 2016; González-Benito and González-Benito 2005). However, more recently, some studies (Brulhart et al. 2019b; Chaudhry and Amir 2020; Patwary et al. 2023a, b) have shifted their focus to EP as a moderating variable, revealing diverse findings regarding its influence on firm performance. Consequently, to address the ambiguity of results in the literature, the current study not only examines the direct effect of EP on environmental sustainability, but also aims to fill the gaps in the existing discussion by considering EP as a moderating variable. EP approaches have been found to exert a significant impact on the operational effectiveness and sustainability of SMEs (Ahmed et al. 2021; Amir and Chaudhry 2019; Do and Nguyen 2020). These findings suggest that EP not only directly contributes to sustainability but may also facilitate alignment between PP strategies and ES. Thus, we posit the following hypotheses based on these insights:

-

H5: The impact of EP on ES is positive and significant.

-

H6: EP significantly moderates the relationship between PP strategies and ES.

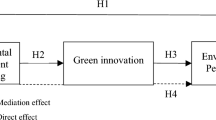

Figure 1 depicts the conceptual framework for the study, which illustrates the hypothesized connections among the study variables based on existing literature and theoretical foundations. It serves as a visual representation of the proposed research model and provides a roadmap for the empirical analysis conducted in this study.

Research model

Research methodology

In this study, a descriptive research design was employed to investigate the impact of PP strategies on ES, with a particular focus on the roles of EMA and EP. The study’s target population was employees working in firms in the SME sector in Pakistan, and convenience sampling was used to select the study sample, which consisted of 308 employees from various SMEs in Pakistan. Data were collected using a survey method with a questionnaire that incorporated scale-inspired items from previous studies. The collected data were analyzed using the most recent version, AMOS v26, for model fitness, validity assessment, and hypothesis testing, while SPSS v28 was utilized for descriptive statistics and the screening process. The choice of a descriptive research design allowed for the investigation of the relationships among the variables in the study in a systematic and structured manner. The use of quantitative data collected through a survey and a large sample size provided a robust foundation for data analysis and statistical testing. Convenience sampling was employed because of practical considerations, although it may limit the generalizability of the findings to a broader population. The population targeted for this study was unknown, as we only considered employees of SMEs who are White in color and have sufficient knowledge of the practices and firm-level strategies. Therefore, determining the exact sample size is challenging. To address this, we referred to Hulland (1999) for sample size calculation to achieve the aims and research objectives. Based on these considerations, a sample size of around 300 is sufficient to generalize the results; therefore, we set a target of 350 in order to avoid incomplete and missing responses. Finally, a usable sample size of 308 employees was deemed appropriate to attain the desired level of precision in estimating the population parameters and addressing the research objectives. Nevertheless, the findings of this study contribute to the existing body of knowledge on PP strategies, EMA, and EP in Pakistan’s SME sector. Further research with diverse samples and research designs is warranted to validate and extend these findings.

Questionnaire and construct measurements

The questionnaire employed in this study consisted of three sections: introductory, demographic, and objective. A 5-point Likert-type scale was used to measure the variables. The respondents were asked to rate their level of agreement or disagreement with a series of statements. A score of 1 denoted “strongly disagree” or “not at all,” whereas a score of 5 represented “strongly agree” or “to a very great extent,” depending on the specific wording of the question. Responses to the study variables were measured using previously established scales. PP strategies were measured using the scales of Bhupendra and Sangle (2015) and Ibrahim and Mahmood (2022). To measure EP, the scale of Brulhart et al. (2019a) was employed, also employed by Chaudhry and Amir (2020), and it was comprised of eight items. EMA and ES were measured using the 13 items and nine items from Latan et al. (2018) and Sambasivan et al. (2013) respectively.

Empirical findings

The sample’s gender, age, education, marital status, and experience were covered in the first portion of the demographics. The sample had a decent gender balance, with men making up around 52% of the sample and women making up 48%. The sample was well qualified, with 12% of the participants holding an undergraduate degree and approximately 43.5% holding a post-graduate degree. A total of 104 employees had a master’s degree, whereas 33 had other qualifications (Table 1).

As far as experience is concerned, 11% of employees had worked for the firm for less than 3 years, while 49 individuals had worked for 4–8 years. Moreover, 30% of the sample respondents were working for 9–12 years, and 131 workers were part of the firm for more than 12 years. Hence, the sample had good experience working in SME firms. Most of the sample comprised young and middle-aged individuals, with 24% of individuals up to the age of 30 years. Twenty-nine percent of the sample falls in the age bracket of 31–40 years, whereas 31.5% of workers were 41–50 years of age. Only 49 workers were above the age of 50 years.

Table 2 presents the descriptive statistics, which summarize the characteristics of the dataset, including measures of central tendency (e.g., mean, median, and mode) and measures of dispersion (e.g., range, standard deviation). Skewness is a measure of the asymmetry of a dataset’s distribution, indicating the degree to which it deviates from a symmetrical, bell-shaped normal distribution.

Table 2 shows that the mean values of the variables are around 3, which indicates the agreement of respondents to the sample items. The mean values ranged between 3.3229 and 3.4858, whereas the standard deviations were close to 1. The skewness values from this table indicate that the values fall from + 1 to − 1; therefore, these data are free from bias due to skewness.

Table 3 shows the KMO values and Bartlett’s test of sphericity, which identify the adequacy of the sample for factor analysis.

Table 3 indicates that the KMO value is 0.945, which is above 0.7. Moreover, Bartlett’s test of sphericity was significant, as the p-values were zero. These results show that the sample was adequate for running the EFA) (Table 4).

The results of the RCM showed that four components were generated, and all items of the study constructs had factor loadings greater than 0.5, which is in accordance with the required threshold. Hence, all these factors were retained to measure the variables and appropriately loaded into the respective components.

Table 5 shows the values of composite reliability (CR) and average variance extracted (AVE) for determining the reliability and convergent validity of the scales, while inter-item correlations were used to confirm the discriminant validity.

The table shows that all CR values for the scales were greater than 0.7, indicating that these scales have high composite reliability (Hair et al. 2019). Next, the AVE values are greater than 0.5, which, together with the CR values, confirm that the scales have high convergent validity. The inter-item correlations of the latent variables are less as compared to the square root of AVE, which demonstrates that these variables have high discriminant validity, satisfying the criteria of Fornell and Larcker (1981).

Mode fitness is a widely used statistical technique in social sciences, psychology, and other fields to assess the validity and reliability of measurement models (Byrne 2016). To assess model fitness through the model fit indices of CMIN/DF, CFI, RMSEA, and p-close, CFA was conducted, as shown in Table 6.

The results show that the model is a good fit, as the CMIN/df falls between 1 and 3, which is an excellent value. Moreover, the CFI value was 0.945, which was less than 0.95. RMSEA and p-close have shown acceptable fit, as their values are 0.060 and 0.051, which fall under 0.06 and close to 0.05 respectively, supporting model fitness. The model is illustrated in Fig. 2.

Measurement model

Table 7 shows the SEM results by which the decision to accept or reject the hypothesis is made according to the beta estimates, t-statistics, and p-values (Byrne 2016). If the p-value is greater than 0.05, then the results are considered insignificant, or vice versa (Fig. 3).

SEM estimation

Table 7 shows that all hypotheses of the study were accepted, except for the path from PP to ES. The first hypothesis shows a positive relationship between PP and EMA as the p-value is zero, thus accepting it. The second hypothesis relates PP to ES, for which the hypothesis is rejected when the significance level is higher than 0.05, rendering the linkage statistically insignificant. Hypothesis 3 links EMA with ES, and this hypothetical path is significant as the p-value is less than 0.05. The fourth hypothesis relates EP to ES, which is also accepted as the p-value is zero, justifying the statistical significance of this relationship. The fifth hypothesis presents a mediating role played by EMA in the association between PP and ES, which is also accepted when the significance level is less than 0.05. The last hypothesis explains the moderating power of EP on the linkage between PP and ES, as shown in Fig. 4. The table shows the acceptance of this hypothesis, with a p-value of 0.04. Figure 3 illustrates the SEM estimation model.

Moderation analysis

EP acts as a strong moderator between PP and ES, providing a strong influence on ES through PP. As shown in Fig. 4, EP moderates the relationship between PP and ES.

Discussion

The present study aimed to investigate the impact of PP strategies on ES, both directly and indirectly, through the mediating role of EMA, while also examining the moderating role of EP in this relationship. The study was conducted using a quantitative approach to collect data from white-collar employees working in SMEs in Pakistan. The findings of the empirical analysis support the acceptance of five of the six hypotheses proposed in this study and are aligned with RQs. PP strategies direct with EMA, and the mediating role of EMA is supported by the significant positive estimate and acceptance of H1, H3, and H6, which suggests that EMA acts as a mechanism through which PP strategies influence ES. This finding is consistent with prior research highlighting the importance of EMA as a key factor in translating PP strategies into improved sustainability outcomes (Agustia et al. 2019; Appannan et al. 2022; Chaudhry and Amir 2020).This implies that SMEs implementing effective EMA practices may be better positioned to achieve higher levels of ES by integrating environmental considerations into their management accounting processes. Furthermore, the moderating role of EP is supported by the significant positive estimate and acceptance of H4 and H6, indicating that EP plays a significant role in influencing the relationship between PP strategies and ES. This finding is in line with previous research highlighting the importance of EP as a facilitating factor that can enhance the effectiveness of PP strategies in achieving sustainability goals (Ahmed et al. 2021; Seroka-Stolka and Fijorek 2020; Zhang et al. 2019). This implies that SMEs with higher levels of EP may experience amplified positive effects of PP strategies on ES, indicating that proactive environmental initiatives can strengthen the link between PP strategies and sustainable outcomes. Interestingly, the analysis also revealed that EP directly enhances sustainability, whereas PP strategies do not. This implies that EP may have a more direct and immediate impact on ES, whereas PP strategies may primarily influence ES indirectly through the mediating role of EMA. Based on the findings and discussion, this study has several research implications.

Conclusion

This study examines the role of PP strategies, EMA, and EP in the ES of SMEs. This study concludes that adopting such actions and designing processes that aim to prevent pollution enables firms to engage in robust EMA practices to ensure ES. The findings also conclude that firms that take initiatives and are more proactive in taking care of the environment also enhance sustainability. The significant roles of EMA and EP in sustainability are also demonstrated by the results. Hence, the importance of these activities must be recognized by firms in all sectors so that they can reduce detrimental effects on the environment, and natural resources can be preserved for future generations. In conclusion, this study has important theoretical, practical, and policy implications.

Research implications

The study’s outcomes have significant research implications that can be understood in theoretical, practical, and policy-making aspects, as mentioned below.

Theoretical implications

Theoretically, this study contributes to the existing literature by advancing our understanding of the complex relationships among the study variables. This study addresses the gaps in the literature by establishing a framework among PP strategies, EMA, EP, and ES within the context of the NRBV theory. The findings highlight the mediating role of EMA in the relationship between PP strategies and ES, emphasizing the importance of incorporating environmental accounting practices into management processes to improve sustainability outcomes. The study also reveals the moderating role of EP, indicating that higher levels of EP can enhance the effectiveness of PP strategies in achieving sustainability goals and that proactive environmental initiatives can strengthen the link between PP strategies and sustainable outcomes.

Practical implications

This study has practical implications for businesses, particularly SMEs, because it provides insights into the benefits of adopting EMA tools. Efficient EMA can enable businesses to gather data on clients and suppliers and make informed decisions, which can enhance their reputation and improve the overall ES. Managers should recognize the impact of adopting environmental strategies and consider implementing EMA practices to better understand and monitor the environmental impact of their SMEs. In addition, wise investment decisions that prioritize environmental protection should be made. Integrating pollution prevention and proactive strategies into managerial control systems can reduce costs and improve environmental performance. This, in turn, contributes to the achievement of environmental goals, such as those outlined in SDGs Agenda 2030, and promotes SMEs’ environmental sustainability. Given the critical role of EMA highlighted in the findings, managers should focus on enhancing their environmental management capabilities. This could involve hiring managers with high levels of environmental management expertise or providing professional development opportunities centered on capability enhancement for current managers. SMEs can effectively implement environmental strategies and engage in successful environmental collaboration by improving managerial capabilities. This study suggests that auditors and consultants can benefit from understanding how SMEs perceive and implement environmental strategies in practice. This understanding can assist auditors and consultants in providing relevant guidance and support to SMEs regarding their environmental management efforts. Furthermore, the study emphasizes the importance of increasing the theoretical understanding of environmental tools, such as pollution prevention technologies, partner collaboration in the supply chain, and the types of EMA used to monitor environmental performance outcomes in SMEs.

Policy implications

Policymakers can use these findings to design targeted regulations and policies for the SME sector aimed at improving environmental conditions and helping businesses better manage the environmental impacts of their operations. This can include incentives for adopting the EMA and effective PP strategies to promote sustainable business practices. This study can be helpful for Pakistani government bodies and business strategists in understanding the role of EMA and PP strategies in determining ES. This can inform the development of effective plans and guidelines to address the increasing pollution levels caused by economic activities and promote environmentally responsible business practices. Business strategists can benefit from these findings by gaining insights into the significance of laws, regulations, norms, and standards related to PP, as well as competitors’ compliance with sustainability levels. This can inform their decision-making and strategic planning and promote the adoption of sustainable practices in the business sector. From a policy-making perspective, this study also emphasizes the importance of integrating environmental considerations, such as PP strategies and EMA, into policy frameworks and guidelines aimed at promoting sustainable business practices. This study highlights the need for policymakers to create a supportive environment for businesses to integrate environmental considerations into their operations and to promote proactive environmental initiatives that can strengthen the link between PP strategies and sustainable outcomes. They can also use these findings to raise awareness among businesses about the benefits of adopting EMA and green practices and to incentivize their implementation through policy measures such as tax incentives, subsidies, and recognition programs.

Study limitations and future recommendations

In the closing remarks, this study acknowledges its limitations and highlights potential avenues for future research.

Study limitations

This study has a few limitations that should be acknowledged. Firstly, the findings are limited to the SME sector in Pakistan, which restricts their generalizability to enterprises in other sectors or countries. Therefore, caution should be exercised when applying these results to different contexts. Additionally, the focus of the study primarily centers around the moderating role of environmental proactivity, neglecting other influential factors such as environmental ethics and environmental orientation. Future research should explore these variables to provide a more comprehensive understanding of their impact on the relationship between pollution prevention strategies and environmental sustainability.

Future recommendations

To address the limitations and advance research in this area, several future directions can be considered. Firstly, conducting cross-sector and cross-cultural studies will help validate and generalize the observed findings. By examining different industries and countries, researchers can gain a broader perspective on the relationship between PP strategies, environmental proactivity, and sustainability. Secondly, future studies should incorporate additional variables such as environmental regulations, corporate social responsibility initiatives, and technological advancements to gain a more comprehensive understanding of their influence on environmental management practices and environmental sustainability. These recommendations will contribute to a deeper understanding of effective environmental strategies and their implications for sustainable business practices.

Data availability

All data generated or analyzed during this study are included in the supplementary materials.

References

Abdullah WSW, Osman M, Ab Kadir MZA, Verayiah R (2019) Energies 12(12):2437

Agustia D, Sawarjuwono T, Dianawati W (2019) The mediating effect of environmental management accounting on green innovation-firm value relationship. Int J Energy Econ Policy 9(2):299–306

Ahmad N, Ullah Z, Arshad MZ, waqas Kamran H, Scholz M, Han H (2021) Relationship between corporate social responsibility at the micro-level and environmental performance: the mediating role of employee pro-environmental behavior and the moderating role of gender. Sustain Prod Consum 27:1138–1148

Ahmed RR, Kyriakopoulos GL, Streimikiene D, Streimikis J (2021) Drivers of proactive environmental strategies: evidence from the pharmaceutical industry of Asian economies. Sustainability 13(16):9479

Alrazi B, De Villiers C, Van Staden CJ (2015) A comprehensive literature review on, and the construction of a framework for, environmental legitimacy, accountability and proactivity. J Clean Prod 102:44–57

Amir M, Chaudhry NI (2019) Linking environmental strategy to firm performance: a sequential mediation model via environmental management accounting and top management commitment. Pak J Commer Soc Sci (PJCSS) 13(4):849–867

Amir M, Rehman SA, Khan MI (2020) Mediating role of environmental management accounting and control system between top management commitment and environmental performance: a legitimacy theory. J Manag Res 7(1):132–160

Anwar M, Li S (2021) Spurring competitiveness, financial and environmental performance of SMEs through government financial and non-financial support. Environ Dev Sustain 23:7860–7882

Appannan JS, Mohd Said R, Ong TS, Senik R (2023) Promoting sustainable development through strategies, environmental management accounting and environmental performance. Business Strategy and the Environment 32(4):1914–1930. https://doi.org/10.1002/bse.3227

Awan U, Kraslawski A, Huiskonen J (2020) Progress from Blue to the Green World: Multilevel Governance for Pollution Prevention Planning and Sustainability. In: Hussain C (ed) Handbook of Environmental Materials Management. Springer, Cham. https://doi.org/10.1007/978-3-319-58538-3_177-1

Banerjee SB (2002) Corporate environmentalism: The construct and its measurement. J Bus Res 55(3):177–191

Barba-Sánchez V, Atienza-Sahuquillo C (2016) Environmental proactivity and environmental and economic performance: evidence from the winery sector. Sustainability 8(10):1014

Barney J (1991) Firm resources and sustained competitive advantage. J Manag 17(1):99–120

Bhupendra KV, Sangle S (2015) What drives successful implementation of pollution prevention and cleaner technology strategy? The role of innovative capability. J Environ Manage 155:184–192

Brulhart F, Gherra S, Quelin BV (2019) Do stakeholder orientation and environmental proactivity impact firm profitability? J Bus Ethics 158(1):25–46

Brulhart F, Gherra S, Quelin BV (2019) Do stakeholder orientation and environmental proactivity impact firm profitability? J Bus Ethics 158:25–46

Burritt RL, Herzig C, Schaltegger S, Viere T (2019) Diffusion of environmental management accounting for cleaner production: evidence from some case studies. J Clean Prod 224:479–491

Byrne BM (2016) Structural Equation Modeling With AMOS: Basic Concepts, Applications, and Programming, 3rd edn. Routledge. https://doi.org/10.4324/9781315757421

Chaudhry NI, Amir M (2020) From institutional pressure to the sustainable development of firm: role of environmental management accounting implementation and environmental proactivity. Bus Strateg Environ 29(8):3542–3554

Chowdhury A, Hamid K (2013) Present status of corporate environmental accounting (CEA) in Bangladesh: a study based on some selected textile companies. Res J Finan Account 4(17):122–129

Christ KL, Burritt RL (2017) What constitutes contemporary corporate water accounting? A review from a management perspective. Sustain Dev 25(2):138–149

Dey PK, Malesios C, De D, Budhwar P, Chowdhury S, Cheffi W (2020) Circular economy to enhance sustainability of small and medium-sized enterprises. Bus Strateg Environ 29(6):2145–2169

Do B, Nguyen N (2020) The links between proactive environmental strategy, competitive advantages and firm performance: an empirical study in Vietnam. Sustainability 12(12):4962

Duran O, Afonso PSLP (2020) An activity based costing decision model for life cycle economic assessment in spare parts logistic management. Int J Prod Econ 222:107499

Dyer JH, Singh H (1998) The relational view: cooperative strategy and sources of interorganizational competitive advantage. Acad Manag Rev 23(4):660–679

EDGAR - Emissions Database for Global Atmospheric Research (2020), Fossil CO2 emissions of all world countries (Report). Retrieved from https://edgar.jrc.ec.europa.eu/overview.php?v=booklet2020

Elleuch B, Bouhamed F, Elloussaief M, Jaghbir M (2018) Environmental sustainability and pollution prevention. Environ Sci Pollut Res 25:18223–18225

Ferreira JJ, Fernandes CI, Ferreira FA (2020) Technology transfer, climate change mitigation, and environmental patent impact on sustainability and economic growth: a comparison of European countries. Technol Forecast Soc Chang 150:119770

Fornell C, Larcker DF (1981) Structural Equation Models with Unobservable Variables and Measurement Error: Algebra and Statistics. Journal of Marketing Research 18(3):382–388. https://doi.org/10.1177/002224378101800313

Gibassier D, Alcouffe S (2018) Environmental management accounting: the missing link to sustainability? Soc Environ Account J 38(1):1–18

González-Benito J, González-Benito Ó (2005) Environmental proactivity and business performance: an empirical analysis. Omega 33(1):1–15

Graham S, McAdam R (2016) The effects of pollution prevention on performance. Int J Oper Prod Manag 36(10):1333–1358

Graham S, Potter A (2015) Environmental operations management and its links with proactivity and performance: a study of the UK food industry. Int J Prod Econ 170:146–159

Hair JF, Risher JJ, Sarstedt M, Ringle CM (2019) When to use and how to report the results of PLS-SEM. Eur Bus Rev 31(1):2–24

Hart SL (1995) A natural-resource-based view of the firm. Acad Manag Rev 20(4):986–1014

Hoque A, Clarke A (2013) Greening of industries in Bangladesh: pollution prevention practices. J Clean Prod 51:47–56

Hsu C-W, Lee W-H, Chao W-C (2013) Materiality analysis model in sustainability reporting: a case study at LITE-ON Technology Corporation. J Clean Prod 57:142–151

Hulland J (1999) Use of partial least squares (PLS) in strategic management research: a review of four recent studies. Strateg Manag J 20(2):195–204

Hunt CB, Auster ER (1990) Proactive environmental management: avoiding the toxic trap. MIT Sloan Manag Rev 31(2):7

Ibrahim M, Mahmood R (2022) Proactive environmental strategy and environmental performance of the manufacturing SMEs of Karachi City in Pakistan: role of green mindfulness as a DCV. Sustainability 14(19):12431

Imperatives S (1987) Report of the World Commission on Environment and Development: Our common future. Link: https://sustainabledevelopment.un.org/content/documents/5987our-common-future.pdf. Accessed Feb, 10, 2020 1-300.

Kotzé T, Botes A, Niemann W (2017) Buyer-supplier collaboration and supply chain resilience: a case study in the petrochemical industry. S Afr J Ind Eng 28(4):183–199

Kumar S, Sureka R, Lim WM, Kumar Mangla S, Goyal N (2021) What do we know about business strategy and environmental research? Insights from Business Strategy and the Environment. Bus Strateg Environ 30(8):3454–3469

Latan H, Jabbour CJC, de Sousa Jabbour ABL, Wamba SF, Shahbaz M (2018) Effects of environmental strategy, environmental uncertainty and top management’s commitment on corporate environmental performance: the role of environmental management accounting. J Clean Prod 180:297–306

Lin B, Long H (2016) Emissions reduction in China׳ s chemical industry–based on LMDI. Renew Sustain Energy Rev 53:1348–1355

Mamun AMA (2021) Assessing the impact of green supply chain management on environmental performance of Bangladeshi manufacturing firms. Saudi J Bus Manag Stud 6:187–198

May N, Guenther E (2020) Shared benefit by material flow cost accounting in the food supply chain–the case of berry pomace as upcycled by-product of a black currant juice production. J Clean Prod 245:118946

Montabon F, Sroufe R, Narasimhan R (2007) An examination of corporate reporting, environmental management practices and firm performance. J Oper Manag 25(5):998–1014

Naeemah AJ, Wong KY (2022) Positive impacts of lean manufacturing tools on sustainability aspects: a systematic review. J Ind Prod Eng 39(7):552–571

Nath P, Ramanathan R (2020) Impact of environmental initiatives on environmental performances: evidence from the UK manufacturing sector. In: Encyclopedia of renewable and sustainable materials. Elsevier, Amsterdam, pp. 408–413. ISBN 9780128131961

Ngwakwe CC (2011) Waste costing as a catalyst in pollution prevention investment decisions. J Ind Ecol 15(6):951–966

Ong TS, Magsi HB, Burgess TF (2019) Organisational culture, environmental management control systems, environmental performance of Pakistani manufacturing industry. Int J Product Perform Manag 68(7):1293–1322

Patwary AK, Aziz RC, Hashim NAAN (2023) Investigating tourists’ intention toward green hotels in Malaysia: a direction on tourist sustainable consumption. Environ Sci Pollut Res 30(13):38500–38511

Patwary AK, Sharif A, Aziz RC, Hassan MGB, Najmi A, Rahman MK (2023) Reducing environmental pollution by organisational citizenship behaviour in hospitality industry: the role of green employee involvement, performance management and dynamic capability. Environ Sci Pollut Res 30(13):37105–37117

PBS (2021) Pakistan Bureau of Statistics—National Accounts Data. 2021. Islamabad: government of Pakistan Retrieved from https://www.pbs.gov.pk/national-accounts

Prajogo DI (2016) The strategic fit between innovation strategies and business environment in delivering business performance. Int J Prod Econ 171:241–249

Raza MY, Lin B, Liu X (2021) Cleaner production of Pakistan’s chemical industry: perspectives of energy conservation and emissions reduction. J Clean Prod 278:123888

Report SD (2018) SDG index and dashboards report 2018: implementing the goals global responsibilities. Retrieved from www.sdgindex.org/reports/sdg-index-and-dashboards-2018/

Reyes-Rodríguez JF, González-Bueno J, Rueda-Barrios G (2020) Influence of organisational and information systems and technologies resources and capabilities on the adoption of proactive environmental practices and environmental performance. Entrep Sustain Issues 8(2):875

Rounaghi MM (2019) Economic analysis of using green accounting and environmental accounting to identify environmental costs and sustainability indicators. Int J Ethics Syst 35(4):504–512. https://doi.org/10.1108/IJOES-03-2019-0056

Sambasivan M, Bah SM, Jo-Ann H (2013) Making the case for operating “green”: impact of environmental proactivity on multiple performance outcomes of Malaysian firms. J Clean Prod 42:69–82

Seroka-Stolka O, Fijorek K (2020) Enhancing corporate sustainable development: proactive environmental strategy, stakeholder pressure and the moderating effect of firm size. Bus Strateg Environ 29(6):2338–2354

Shah N, Soomro BA (2021) Internal green integration and environmental performance: the predictive power of proactive environmental strategy, greening the supplier, and environmental collaboration with the supplier. Bus Strateg Environ 30(2):1333–1344

Solovida GT, Latan H (2017) Linking environmental strategy to environmental performance: mediation role of environmental management accounting. Sustain Account Manag Policy J 8(5):595–619

Sturiale L, Scuderi A, Timpanaro G, Matarazzo B (2020) Sustainable use and conservation of the environmental resources of the etna park (unesco heritage): evaluation model supporting sustainable local development strategies. Sustainability 12(4):1453

Sulong F, Sulaiman M, Norhayati MA (2015) Material flow cost accounting (MFCA) enablers and barriers: the case of a Malaysian small and medium-sized enterprise (SME). J Clean Prod 108:1365–1374

Tumpa TJ, Ali SM, Rahman MH, Paul SK, Chowdhury P, Khan SAR (2019) Barriers to green supply chain management: an emerging economy context. J Clean Prod 236:117617

Winsemius P, Guntram U (1992) Responding to the environmental challenge. Bus Horiz 35(2):12–21

Yearbook PE (2021) Pakistan Energy Yearbook. HDIP (Hydrocarbon development institute of Pakistan) Retrieved from https://hdip.com.pk/pakistan-energy-yearbook

Zailani SHM, Eltayeb TK, Hsu CC, Tan KC (2012) The impact of external institutional drivers and internal strategy on environmental performance. Int J Oper Prod Manag 32(6):721–745

Zhang S, Wang Z, Zhao X (2019) Effects of proactive environmental strategy on environmental performance: mediation and moderation analyses. J Clean Prod 235:1438–1449

Author information

Authors and Affiliations

Contributions

• Dr. Kamran Ali: supervision, project administration, and final expert editing.

• Naila Kausar: review and editing and methodology and data curation.

• Muhammad Amir: writing (review and editing) and software application.

Corresponding author

Ethics declarations

Ethical approval

All work in this research was completed by the authors, and all procedures were performed in accordance with ethical standards.

Consent to participate

We affirm that all authors participated in the research and are fully aware of their ethical responsibilities.

Consent for publication

We affirm that all authors have agreed to submit the paper to ESPR and are fully aware of the ethical responsibilities.

Competing interests

The authors declare no competing interests.

Additional information

Responsible Editor: Arshian Sharif

Publisher's note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

Springer Nature or its licensor (e.g. a society or other partner) holds exclusive rights to this article under a publishing agreement with the author(s) or other rightsholder(s); author self-archiving of the accepted manuscript version of this article is solely governed by the terms of such publishing agreement and applicable law.

About this article

Cite this article

Ali, K., Kausar, N. & Amir, M. Impact of pollution prevention strategies on environment sustainability: role of environmental management accounting and environmental proactivity. Environ Sci Pollut Res 30, 88891–88904 (2023). https://doi.org/10.1007/s11356-023-28724-1

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-023-28724-1