Abstract

Over the last few decades, economic policy uncertainty (EPU) has surged across the globe. Furthermore, EPU affects economic activities, which may also generate strong CO2 emissions. The goal of this study is to explore the impact of EPU (measured by the world uncertainty index) on CO2 emissions in the case of the top ten carbon emitter countries, spanning the period 1990 to 2015. The findings from the PMG-ARDL modelling approach document that the world uncertainty index (WUI) affects CO2 emissions in both the short and the long run. In the short run, a 1% increase in WUI mitigates CO2 emissions by 0.11%, while a 1% rise in WUI escalates CO2 emissions by 0.12% in the long run. The findings could have some substantial practical effects on economic policies through which policy makers try to shrink any uncertainty by organizing and participating in international summits and treaties. In addition, international organizations could also launch certain programs to shrink uncertainties associated with economic policy. Finally, these countries should introduce innovation, renewable energy, and enforce alternative technologies that are environment friendly. Overall, governments must provide strong tax exemptions on the use of clean energy, while R&D budgets should also expand.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

Over the last few decades, concerns about economic policy uncertainty (EPU) have escalated across the globe. In addition, the country reports of IMF (International Monetary Fund) conclude that EPU is one of the main reasons behind meagre economic growth over the last few years. Moreover, there is plethora of studies that probe the effect of EPU on different economic indicators, such as economic growth (Baker et al. 2016; Sahinoz and Erdogan Cosar 2018), investment (Kang et al. 2014), stock markets (Rehman and Apergis 2019), and energy prices (Kang and Ratti 2013).

On the top of the economic effects of EPU, it may also have environmental effects. EPU may prompt producers to employ traditional and environment unfriendly means of production, which increase CO2 emissions. Moreover, EPU could affect consumption and investments, which in turn plunge CO2 emissions. Furthermore, decreases in R&D, innovations, and renewable energy consumption due to high EPU could increase CO2 emissions. Hence, the relationship between EPU and CO2 emissions should be explored in order to propose the policies related to environmental degradation.

There are several studies in the literature that explores the effect of EPU on CO2 emissions. Jiang et al. (2019) conclude that high EPU affects the decision-making of economic agents, increasing CO2 emissions in the USA. In addition, Adedoyin and Zakari (2020) conclude that EPU decreases energy consumption and economic growth, plunging CO2 emissions in the short run. Danish et al. (2020) note that EPU increases energy consumption, which surges CO2 emissions in both short and long run. Recently, Wang et al. (2020) and Adams et al. (2020) also note that EPU escalates CO2 emissions. Therefore, EPU can either increase or decrease CO2 emissions (environmental degradation).

Based on the above background, the goal of this study is to investigate the effect of EPU on CO2 emissions in top ten carbon emitter countries, namely, China, the USA, India, Russia, Japan, Germany, Iran, Saudi Arabia, South Korea, and Canada. The study contributes to the literature in three ways. First, there is limited literature that investigates the impact of EPU on CO2 emissions. The current study fills this gap by examining its impact on CO2 emissions in the top ten carbon emitter countries.

Second, previous studies employ the EPU index, developed by Baker et al. (2016), as an indicator for EPU. However, there are few limitations with respect to the EPU index. EPU index just covers the uncertainty related to economic policies (monetary policy, trade policy, and fiscal policy) and does not incorporate the uncertainty related to political events.Footnote 1 Moreover, the EPU index for different countries is not calculated from the single base, which creates the issues of accuracy, reliability, and ideological bias.Footnote 2 To overcome these limitations, Ahir et al. (2019) develop the world uncertainty index (WUI) for 143 countries. It is calculated on the basis of Economist Intelligence Unit (EIU) country reports. Furthermore, WUI is superior to EPU index as it is calculated from the single base (i.e., EIU reports) and incorporates both economic and political developments (events) in a country. This study, therefore, employs WUI as a proxy for EPU and examines the impact of WUI on CO2 emissions.

Third, the prior literature on determinants of CO2 emissions extensively employed first generation panel data methods, which do not incorporate the issues of cross-sectional dependence and heterogeneity. Also, these aforementioned issues may lead to unreliable results; therefore, present study employs second-generation panel data methods to overcome the issues of cross-sectional dependence and heterogeneity.

Literature on the determinants of CO2 emissions

This section reports the prior literature on the determinants of CO2 emissions. The previous studies highlight several economic and non-economic influencing factors of CO2 emissions. However, economic growth is considered as one of the major determinants of CO2 emissions (Apergis and Payne 2010). In growth-emissions nexus, environmental Kuznets curve (EKC) has widely been explored, which is inverted U-shaped relationship between income and environmental degradation (Apergis and Ozturk 2015; Aslan et al. 2018; Narayan and Narayan 2010; Murshed et al. 2020). In addition to this, energy consumption is also regarded as one of the key determinants of CO2 emissions (Adedoyin and Bekun 2020; Zhang and Lin 2012). Also, several studies disaggregate energy consumption (i.e., renewable and non-renewable energy consumption) and highlight that non-renewable energy escalates CO2 emissions, whereas renewable energy consumption mitigates CO2 emissions (Alola et al. 2019; Baloch et al. 2019; Dogan and Seker 2016; Dogan and Ozturk 2017; Zaidi et al. 2018). Similarly, previous studies also note that natural resources are also driving factors of CO2 emissions (Bekun et al. 2019; Danish et al. 2019; Joshua and Bekun 2020). Additionally, prior literature also reveals that trade surges the level of CO2 emissions (Farhani and Ozturk 2015; Shahbaz et al. 2013). Further, there are several studies that note globalization and urbanization as one of the important determinants of CO2 emissions (Destek 2020; Sadorsky 2014; Shahbaz et al. 2017). In addition to this, population of the country also contributes to CO2 emissions (Begum et al. 2015; Mohsin et al. 2019). Moreover, economic policies (e.g., monetary policy and fiscal policy) also affect the level of CO2 emissions (Ullah et al. 2020a).

There are several studies that discern the determinants of CO2 emissions in top emitter countries. For instance, Amin et al. (2020) employ quantile regression approach to explore the impact of financial development on CO2 emissions in top ten emitter countries. The study highlights that EKC exists for top ten emitters, and financial development also escalates CO2 emissions. Ertugrul et al. (2016) explore that income, energy consumption, and trade are main determinants of CO2 emissions in top ten emitters from developing countries. Mohmmed et al. (2019) report that income, population, human development index (HDI), and energy intensity are the driving factors of CO2 emissions in top ten emitter countries. Similarly, Nejat et al. (2015) report that economic growth, population, and urbanization are the main causes of high level of CO2 emissions in top ten carbon emitter countries. Recently, Ullah et al. (2020b) highlight that there is asymmetric effect of oil prices on CO2 emissions in top ten emitter countries. Fatima et al. (2020) highlight that income, non-renewable energy, and renewable energy consumption are the major driving factors in top eight emitter countries. Li and Jiang (2020) explore research and development as one of the prime determinants in top six carbon emitter countries. In addition to this, Ali et al. (2020) highlight that eco-innovation, trade, and renewable energy effect CO2 emissions in top ten emitter countries.

Parallel to this, there are several studies that explore the relationship between economic policy uncertainty (EPU) and CO2 emissions. For instance, Jiang et al. (2019) employ granger causality in quantiles and report that EPU escalates CO2 emissions in the USA. Similarly, Adedoyin and Zakari (2020) conclude that EPU decreases CO2 emissions in the short run, whereas it escalates them in the long run. Danish et al. (2020) note that EPU increases energy consumption, which surges CO2 emissions in the USA. Pirgaip and Dinçergök (2020) also report that EPU increases CO2 emissions in the G7 countries. Recently, Adams et al. (2020) employ world uncertainty index (WUI), as a proxy for EPU, and explore the relationship between EPU and CO2 emissions in countries with high geopolitical risk. The study reveals that EPU (measured by WUI) escalates CO2 emissions. Similarly, Wang et al. (2020) also employ WUI (as a proxy for EPU) and report that EPU increases the CO2 emissions in the USA.

Given the above discussion, this can be seen that relationship between EPU and CO2 emissions has not been yet explored in top ten emitter countries. Moreover, there is dearth of literature that employs WUI (as a proxy for EPU) and investigates uncertainty-emissions relationship. Thus, the present study fills these gaps by probing the impact of WUI (i.e., proxy for EPU) on CO2 emissions in top ten carbon emitter countries.

Theoretical background

This section elaborates the theoretical linkages between EPU (economic policy uncertainty) and CO2 emissions. Jiang et al. (2019) describe that EPU effects CO2 emissions through direct policy adjustment effect and indirect economic demand effect. Direct policy adjustment effect explains that high EPU diverts the attention of policy makers from environmental protection measures to economic stabilization measures, which increases CO2 emissions. On the other hand, indirect economic demand effect describes that EPU alters the economic conditions and decision-making, which in turn effect energy consumption. Thus, the change in energy consumption ultimately effects CO2 emissions.

Additionally, prior literature related to EPU highlights that EPU effects FDI, investment, trade, stock markets, economic development, innovations, and oil prices (Arouri et al. 2016; Canh et al. 2020; Kang et al. 2014; Sun et al. 2020; Tam 2018; Xu 2020). On the other hand, several studies report that FDI, investment, trade, stock market, economic development, innovations, and oil prices affect CO2 emissions (Alam et al. 2020; Danish et al. 2019; Hashmi and Alam 2019; Omri et al. 2014; Sadorsky 2009; Salahuddin et al. 2018; Shahbaz et al. 2013). Therefore, this can be concluded that EPU effects CO2 emissions through FDI, investment, trade, oil prices, etc.

Recently, Wang et al. (2020) conclude that EPU effects CO2 emissions through two channels (i.e., consumption effect and investment effect). Consumption effect explains that EPU plunges both energy consumption and pollution-intensive products’ consumption, which in turn mitigates CO2 emissions. On the contrary, investment effect concludes that EPU discourages the investment in R&D (research and development), renewable energy, and innovations. Meanwhile, the reduction in investment escalates CO2 emissions. Therefore, EPU can either increase or decrease CO2 emissions.

Methodology

Model

The analysis is principally based on the underlying intuition of the STIRPAT approach presented by Dietz and Rosa (1994). In fact, the STIRPAT model has been taken from the IPAT model, developed by Ehrlich and Holdren (1971), which probes the effects of socioeconomic determinants of environmental quality. In lieu of the fact that the IPAT has various advantages, there are also a few drawbacks of this approach. York et al. (2003) note that the hypothesis testing cannot be applied on the IPAT model because of its mathematical form. Next, the model assumes fixed proportionality across the independent variables, which is not realistically valid. In addition, the IPAT approach cannot make a distinction between the relative eminences of each factor. To overcome these drawbacks, the STIRPAT model remedies them and investigates the stochastic impact of population, affluence, and technology on environmental quality. The standard form of STIRPAT model is expressed as follows:

Moreover, we transform all variables into their logarithmic form to control heterogeneity (Farhani et al. 2014). The new model yields:

In (2), φ is the intercept, whereas εit is the error term. Additionally, α, β, and γ are coefficients, with i and t representing cross-section and time, respectively. The empirical model used is reported in Eq. (3):

CO2 denotes carbon dioxide emissions, GDP is GDP per capita, and GDP2 is square of GDP. Additionally, ENE denotes energy consumption, whereas POP is total population. WUI is the world uncertainty index (which is used as a proxy for economic policy uncertainty), εit shows the error term, and αi denotes country fixed effects. Further, β0 is intercept, and β1, β2, β3, β4, and β5 are slope coefficients.

In previous studies on the determinants of CO2 emissions for top emitters, GDP, energy consumption, and population have been extensively employed as major driving factor of CO2 (Fatima et al. 2020; Mohmmed et al. 2019). Therefore, we also use these aforementioned variables as control variables in the present study. We incorporate GDP and GDP2 to examine the existence of EKC (environmental Kuznets curve); therefore, the expected sign of GDP and GDP2 is positive and negative respectively (Apergis and Ozturk 2015). Next, energy consumption (e.g., fossil fuel energy) is considered as a prime reason of CO2 emissions. Therefore, the envisaged sign of ENE is positive, i.e., an increase in ENE yields higher CO2 emissions (Danish et al. 2020). Further, high population growth exerts pressure on demand for goods and services, which escalates CO2 emissions. Therefore, population and CO2 emissions are expected to be positively correlated (Alola et al. 2020). Moreover, the envisaged sign of WUI is positive, implying that WUI escalates CO2 emissions (Adams et al. 2020; Wang et al. 2020).

Next, to the best of our knowledge, there is no study that employs STIRPAT model to explore the impact of economic policy uncertainty (EPU) on CO2 emissions. Prior studies, for instance, Adams et al. (2020), Danish et al. (2020), and Wang et al. (2020) use well-known EKC model to probe the uncertainty-emissions relationship. This motivates the current study to employ STIRPAT model and investigate the uncertainty-emissions relationship.

Methodology

As the objective is to discern the dynamic relationship between WUI and CO2 emissions, the study employs the panel ARDL model developed by Pesaran and Smith (1995) and Pesaran et al. (1999). Pesaran et al. (1999) argue that panel ARDL approach is relatively efficient in long panel time series data. The methodology generates both short- and long-term coefficients, while it allows different lags for the dependent and independent variables. Further, the methodology is applicable if the variables are integrated at different orders (I(1) and/or I(0)). The panel ARDL model is reported in Eq. (4).

CO2 indicates carbon dioxide emissions, whereas X is the vector of all independent controls (population, energy, and GDP). Moreover, τ and θ are the coefficients to be estimated, ρi indicates the cross-sectional effects, whereas εit is the error term. Subscripts i and t, respectively, show the cross-section and time. In addition, an error correction (ECM) model can be posted as follows:

In Eqs. (5) and (6), Δ denotes the first difference, and ECT is the error correction term. Next, ηi is the short-run coefficient, whereas θ is the long-run coefficient.

However, panel ARDL has three specifications, namely, PMG (pooled mean group), MG (mean group), and DFE (dynamic fixed effect) estimator. MG estimator, developed by Pesaran and Smith (1995), renders heterogonous estimated coefficients across all cross-sections in both short run and long run. Next, PMG estimator, presented by Pesaran et al. (1999), provides homogenous parameters for all cross-sections in long run. But, PMG gives heterogonous coefficients in short run. On the contrary, DFE estimator renders homogenous parameters across all cross-sections in both short run and long run. To compare the consistency and efficiency of these three aforementioned estimators, we apply Hausman (1978) specification test.

Data

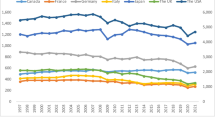

The analysis uses data for the top ten carbon emitter countries (China, the USA, India, Russia, Japan, Germany, Iran, Saudi Arabia, South Korea, and Canada), spanning the period 1990-2015. The dependent variable is CO2 emissions (metric ton per capita), whereas the control variables are GDP per capita (constant 2010$), energy consumption (oil equivalent per capita), and total population. Further, the key independent variable is world uncertainty index (WUI), which is used as a proxy for economic policy uncertainty (EPU). WUI is available on quarterly bases; therefore, we take average of four quarters to convert the data into annual frequency. The WUI is measured by calculating the frequency of word “uncertainty” (or its variants) in EIU (economic intelligence unit) reports. Next, high value of WUI implies high EPU. Also, WUI renders three quarter moving average. For instance, 2013Q4 = (2013Q4 × 0.6) + (2013Q3 × 0.3) + (2013Q2 × 0.1)/3. However, further details are given at worlduncertaintyindex.com. Figs. 1, 2, 3, 4, 5, 6, 7, 8, 9, and 10 illustrate the WUI for top ten emitters.

The WUI for China

The WUI for the USA

The WUI for India

The WUI for Russia

The WUI for Japan

The WUI for Germany

The WUI for Iran

The WUI for Saudi Arabia

The WUI for Korea

The WUI for Canada

In Figs. 1, 2, 3, 4, 5, 6, 7, 8, 9, and 10, blue line is the actual WUI whereas black line is the trend line. As can be seen in Figs. 1, 2, 3, 4, 5, 6, 7, 8, 9, and 10, WUI increases over the time in most of the top ten emitter countries. However, on average, WUI plunges in Canada and India. The variables used are reported in Table 1, whereas Table 2 renders some descriptive statistics.

All data series are negatively skewed except POP, which is positively skewed. Jarque-Bera test reports that all series are not normally distributed.

Results and discussion

Unit root tests

To restrain from any spurious regression results, this first part of the empirical analysis employs the CIPS (cross-sectionally augmented IPS) unit root test by Pesaran (2007) to examine stationarity in the data. The CIPSunit root test incorporates the issues of cross-sectional dependence and heterogeneity; therefore, it is superior to other panel unit root tests (e.g., Levin et al. (2002) test and augmented dickey fuller-Fisher chi-square test). The findings from the CIPS test are reported in Table 3.

The findings clearly highlight that all series are non-stationary in their levels, as we could not reject the null hypothesis of a unit root at the 1% significance level. In contrast, the null of a unit root is rejected in their first differences.

Westerlund (2007) co-integration test

We also employ Westerlund (2007) co-integration test to examine the long-run relationship between dependent and independent variables of our study. Westerlund (2007) test renders reliable results even in the presence of cross-sectional dependence and heterogeneity (Dogan et al. 2020). This advantage of the test compels to employ Westerlund (2007) test. The findings from the test are reported in Table 4.

As can be seen, the null hypothesis of no co-integration can be rejected. Therefore, there exists a long-run relationship across carbon emissions and selected independent variables (i.e., GDP, WUI, POP, and ENE,).

Panel ARDL results

The present study employs Hausman (1978) test to discern the appropriate specification of panel ARDL model. The findings from the test are reported in Table 5.

As can be seen in Table 5, we fail to reject all null hypotheses. Therefore, in our case, PMG-ARDL specification is appropriate. The findings from the PMG-ARDL model are reported in Table 6; they illustrate the impact of WUI on CO2 emissions in both the short and long run. The short-run estimates are presented with one lag, since higher lags turned out to be statistically insignificant.

More specifically, they highlight that in the short run, the coefficient of WUI is negative and statistically significant. A 1% increase in WUI plunges CO2 emissions by 0.11%, or a 1% increase in WUI decreases carbon emissions by 0.93 metric tons per capita. In addition, coefficient of GDP and GDP2 is positive and negative, respectively. Moreover, the aforementioned coefficients are also statistically significant; thus, we validate the existence of environmental Kuznets curve. Also, a 1% increase in ENE escalates CO2 emissions by 0.31%. In addition, we do not report all those coefficients which are statistically insignificant (e.g., POP). The ECT is also negative and statistically significant, implying that any deviation from the long-run equilibrium is corrected by 76% each year.

In the long run, the coefficient for WUI is positive and statistically significant. The value of WUI is 0.12, indicating that a 1% increase in WUI increases CO2 emissions by 0.12% or that 1% increase in WUI compels CO2 emissions to increase by 1.01 metric tons per capita. In addition, the coefficients for POP and ENE are positive and statistically significant, indicating that increases in population and energy consumption also escalate CO2 emissions. Furthermore, coefficient of GDP and GDP2 is positive and negative, respectively. Thus, we conclude that EKC does exist in top 10 carbon emitter countries.

Discussion

The findings reveal that WUI affects CO2 emissions in both the short and long run. In the short run, WUI ameliorates environmental quality, as it plunges CO2 emissions. There are two potential channels behind this result. First, high WUI (EU) may discourage energy consumption, investments at the firm level, firm’s earnings and cash flows, and tourism and GDP growth (Ali 2001; Kang et al. 2014; Adams et al. 2018; Akadiri et al. 2020), which mitigate CO2 emissions (Danish et al. 2019; Dogan and Ozturk 2017). Second, high WUI may affect the decision-making of economic agents, which further plunges CO2 emissions. Moreover, we also report that consumption effect is dominant in short run. These findings are in line with the conclusion of Adedoyin and Zakari (2020). The US-China trade war has increased economic policy uncertainty, which affect the decision-making about economic activities (FDI and trade). The ambiguity and inconsistency in decision-making also affect CO2 emissions.

By contrast, in the long run, WUI increases CO2 emissions, implying that WUI contributes to environmental degradation. There are two possible mechanisms behind this finding. First, WUI may discourage R&D, innovations, and renewable energy consumption, which escalate CO2 emissions. The political tensions of the USA with other countries (e.g., China, Iran, and Korea) compel the USA to cut expenditures on R&D, innovations, and investments in renewable energy. Recently, President Trump cut 21% in R&D expenditure, aggravating CO2 emissions. Second, WUI also prompts producers to employ traditional (outdated) and environment unfriendly means of production (machines that use oil as an input, while they have a low capital to output ratio), which surge CO2 emissions (Jiang et al. 2019). Further, we conclude that investment effect is dominant in long run. These findings are backed by the conclusion of Pirgaip and Dinçergök (2020), Adams et al. (2020), and Wang et al. (2020). However, economic growth, energy consumption, and population are also responsible for environmental degradation, as they increase CO2 emissions.

Conclusion

In the last few decades, the economic policy uncertainty (EPU) has experienced profound upsurge. In addition to the economic effects of EPU, there are also environmental effects as well. On this basis, the present study explored the impact of EPU (measured by world uncertainty index) on CO2 emissions for the top ten carbon emitter countries. The findings from the PMG-ARDL modelling approach documented that WUI (world uncertainty index) affected CO2 emissions in both the short and long run.

Based on these findings, a few policy implications can be deduced. First, economic policies should be very clear and transparent, with government officials trying to shrink any policy uncertainty through international summits and treaties. Second, the international organizations like UNO, WTO, and the World Bank should launch programs to shrink the economic policy uncertainties. Third, in the short run, curbing CO2 emissions in the top ten carbon emitter countries is also possible at the cost of WUI. Therefore, if these countries crave to mitigate environmental pollution and WUI simultaneously, they should introduce innovation, renewable energy, and enforcement alternative technologies that would be employment friendly. Governments are urged to give tax exemptions on the use of clean energy, while R&D budgets should increase. In addition, grants and projects on innovations and clean energy technologies should be awarded, while subsidies should be provided on the import of renewable energy products.

Data availability

Data will be available upon request.

References

Adams S, Klobodu EKM, Apio A (2018) Renewable and non-renewable energy, regime type and economic growth. Renew Energy 125:755–767

Adams S, Adedoyin F, Olaniran E, Bekun FV (2020) Energy consumption, economic policy uncertainty and carbon emissions; causality evidence from resource rich economies. Econ Anal Pol 68:179–190

Adedoyin FF, Bekun FV (2020) Modelling the interaction between tourism, energy consumption, pollutant emissions and urbanization: renewed evidence from panel VAR. Environ Sci Pollut Res 27(31):38881–38900

Adedoyin FF, Zakari A (2020) Energy consumption, economic expansion, and CO2 emission in the UK: the role of economic policy uncertainty. Sci Total Environ 738:140014

Ahir H, Bloom N, Furceri D (2019) The world uncertainty index. Stanford mimeo

Akadiri SS, Alola AA, Uzuner G (2020) Economic policy uncertainty and tourism: evidence from the heterogeneous panel. Curr Issues Tourism 23(20):2507–2514

Alam MS, Apergis N, Paramati SR, Fang J (2020) The impacts of R&D investment and stock markets on clean-energy consumption and CO2 emissions in OECD economies. Int J Fin Econ 2020:1–14

Ali AM (2001) Political instability, policy uncertainty, and economic growth: an empirical investigation. Atl Econ J 29(1):87–106

Ali S, Dogan E, Chen F (2020) Khan Z (2020) International trade and environmental performance in top ten-emitters countries: the role of eco-innovation and renewable energy consumption. Sustain Dev 2020(1):2–28

Alola AA, Yalçiner K, Alola UV, Saint Akadiri S (2019) The role of renewable energy, immigration and real income in environmental sustainability target. Evidence from Europe largest states. Science of The Total Environment 674:307–315

Alola AA, Arikewuyo AO, Ozad B, Alola UV, Arikewuyo HO (2020) A drain or drench on biocapacity? Environmental account of fertility, marriage, and ICT in the USA and Canada. Environ Sci Pollut Res 27(4):4032–4043

Amin A, Dogan E, Khan Z (2020) The impacts of different proxies for financialization on carbon emissions in top-ten emitter countries. Sci Total Environ 740:140127–140127

Apergis N, Ozturk I (2015) Testing environmental Kuznets curve hypothesis in Asian countries. Ecol Indic 52:16–22

Apergis N, Payne JE (2010) The emissions, energy consumption, and growth nexus: evidence from the commonwealth of independent states. Energy Policy 38(1):650–655

Arouri M, Estay C, Rault C, Roubaud D (2016) Economic policy uncertainty and stock markets: long-run evidence from the US. Financ Res Lett 18:136–141

Aslan A, Destek MA, Okumus I (2018) Bootstrap rolling window estimation approach to analysis of the Environment Kuznets Curve hypothesis: evidence from the USA. Environ Sci Pollut Res 25(3):2402–2408

Baker SR, Bloom N, Davis SJ (2016) Measuring economic policy uncertainty. Q J Econ 131(4):1593–1636

Baloch MA, Mahmood N, Zhang JW (2019) Effect of natural resources, renewable energy and economic development on CO2 emissions in BRICS countries. Sci Total Environ 678:632–638

Begum RA, Sohag K, Abdullah SMS, Jaafar M (2015) CO2 emissions, energy consumption, economic and population growth in Malaysia. Renew Sust Energ Rev 41:594–601

Bekun FV, Alola AA, Sarkodie SA (2019) Toward a sustainable environment: Nexus between CO2 emissions, resource rent, renewable and nonrenewable energy in 16-EU countries. Sci Total Environ 657:1023–1029

Canh NP, Binh NT, Thanh SD, Schinckus C (2020) Determinants of foreign direct investment inflows: the role of economic policy uncertainty. Int Econ 161:159–172

Danish, Baloch MA, Mahmood N, Zhang JW (2019) Effect of natural resources, renewable energy and economic development on CO2 emissions in BRICS countries. Sci Total Environ 678:632–638

Danish Ulucak R, Khan SUD (2020) Relationship between energy intensity and CO2 emissions: does economic policy matter? Sustain Dev 28(5):1457–1464

Destek MA (2020) Investigation on the role of economic, social, and political globalization on environment: evidence from CEECs. Environ Sci Pollut Res 27(27):33601–33614

Dietz T, Rosa EA (1994) Rethinking the environmental impacts of population, affluence and technology. Hum Ecol Rev 1(2):277–300

Dogan E, Ozturk I (2017) The influence of renewable and non-renewable energy consumption and real income on CO 2 emissions in the USA: evidence from structural break tests. Environ Sci Pollut Res 24(11):10846–10854

Dogan E, Seker F (2016) The influence of real output, renewable and non-renewable energy, trade and financial development on carbon emissions in the top renewable energy countries. Renew Sust Energ Rev 60:1074–1085

Dogan E, Ulucak R, Kocak E, Isik C (2020) The use of ecological footprint in estimating the environmental Kuznets curve hypothesis for BRICST by considering cross-section dependence and heterogeneity. Sci Total Environ 723:138063

Ehrlich PR, Holdren JP (1971) Impact of population growth. ObstetGynecolSurv 26(11):769–771

Ertugrul HM, Cetin M, Seker F, Dogan E (2016) The impact of trade openness on global carbon dioxide emissions: evidence from the top ten emitters among developing countries. Ecol Indic 67:543–555

Farhani S, Ozturk I (2015) Causal relationship between CO 2 emissions, real GDP, energy consumption, financial development, trade openness, and urbanization in Tunisia. Environ Sci Pollut Res 22(20):15663–15676

Farhani S, Shahbaz M, Sbia R, Chaibi A (2014) What does MENA region initially need: grow output or mitigate CO2 emissions? Econ Model 38:270–281

Fatima T, Shahzad U, Cui L (2020) Renewable and nonrenewable energy consumption, trade and CO2 emissions in high emitter countries: does the income level matter? J Environ Plann Manag 2020:1–25. https://doi.org/10.1080/09640568.2020.1816532

Hashmi R, Alam K (2019) Dynamic relationship among environmental regulation, innovation, CO2 emissions, population, and economic growth in OECD countries: a panel investigation. J Clean Prod 231:1100–1109

Hausman JA (1978) Specification tests in econometrics. Econometrica 46(6):1251–1271

Jiang Y, Zhou Z, Liu C (2019) Does economic policy uncertainty matter for carbon emission? Evidence from US sector level data. Environ Sci Pollut Res 26(24):24380–24394

Joshua U, Bekun FV (2020) The path to achieving environmental sustainability in South Africa: the role of coal consumption, economic expansion, pollutant emission, and total natural resources rent. Environ Sci Pollut Res 27(9):9435–9443

Kang W, Ratti RA (2013) Structural oil price shocks and policy uncertainty. Econ Model 35:314–319

Kang W, Lee K, Ratti RA (2014) Economic policy uncertainty and firm-level investment. J Macroecon 39:42–53

Levin A, Lin CF, Chu CSJ (2002) Unit root tests in panel data: asymptotic and finite-sample properties. J Econ 108(1):1–24

Li R, Jiang R (2020) Does increase in R & D investment reduce environmental pressures? Empirical research on the global top six carbon emitters. Sci Total Environ 740:140053

Mohmmed A, Li Z, Arowolo AO, Su H, Deng X, Najmuddin O, Zhang Y (2019) Driving factors of CO2 emissions and nexus with economic growth, development and human health in the top ten emitting countries. Resour Conserv Recycl 148:157–169

Mohsin M, Abbas Q, Zhang J, Ikram M, Iqbal N (2019) Integrated effect of energy consumption, economic development, and population growth on CO 2 based environmental degradation: a case of transport sector. Environ Sci Pollut Res 26(32):32824–32835

Murshed M, Nurmakhanova M, Elheddad M et al (2020) Value addition in the services sector and its heterogeneous impacts on CO2 emissions: revisiting the EKC hypothesis for the OPEC using panel spatial estimation techniques. Environ Sci Pollut Res 27:38951–38973. https://doi.org/10.1007/s11356-020-09593-4

Narayan PK, Narayan S (2010) Carbon dioxide emissions and economic growth: panel data evidence from developing countries. Energy Policy 38(1):661–666

Nejat P, Jomehzadeh F, Taheri MM, Gohari M, Majid MZA (2015) A global review of energy consumption, CO2 emissions and policy in the residential sector (with an overview of the top ten CO2 emitting countries). Renew Sust Energ Rev 43:843–862

Omri A, Nguyen DK, Rault C (2014) Causal interactions between CO2 emissions, FDI, and economic growth: evidence from dynamic simultaneous-equation models. Econ Model 42:382–389

Pesaran MH (2007) A simple panel unit root test in the presence of cross-section dependence. J Appl Econ 22(2):265–312

Pesaran MH, Smith R (1995) Estimating long-run relationships from dynamic heterogeneous panels. J Econ 68(1):79–113

Pesaran MH, Shin Y, Smith RP (1999) Pooled mean group estimation of dynamic heterogeneous panels. J Am Stat Assoc 94(446):621–634

Pirgaip B, Dinçergök B (2020) Economic policy uncertainty, energy consumption and carbon emissions in G7 countries: evidence from a panel Granger causality analysis. Environ Sci Pollut Res Int 27:30050–30066

Rehman M, Apergis N (2019) Sensitivity of economic policy uncertainty to investor sentiment: evidence from Asian, developed and European markets. Stud Econ Fin 36(2):114–129

Sadorsky P (2009) Renewable energy consumption, CO2 emissions and oil prices in the G7 countries. Energy Econ 31(3):456–462

Sadorsky P (2014) The effect of urbanization on CO2 emissions in emerging economies. Energy Econ 41:147–153

Sahinoz S, Erdogan Cosar E (2018) Economic policy uncertainty and economic activity in Turkey. Appl Econ Lett 25(21):1517–1520

Salahuddin M, Alam K, Ozturk I, Sohag K (2018) The effects of electricity consumption, economic growth, financial development and foreign direct investment on CO2 emissions in Kuwait. Renew Sust Energ Rev 81:2002–2010

Shahbaz M, Hye QMA, Tiwari AK, Leitão NC (2013) Economic growth, energy consumption, financial development, international trade and CO2 emissions in Indonesia. Renew Sust Energ Rev 25:109–121

Shahbaz M, Khan S, Ali A, Bhattacharya M (2017) The impact of globalization on CO2 emissions in China. Singapore Econ Rev 62(04):929–957

Sun X, Chen X, Wang J, Li J (2020) Multi-scale interactions between economic policy uncertainty and oil prices in time-frequency domains. North Am J Econ Fin 51:100854

Tam PS (2018) Global trade flows and economic policy uncertainty. Appl Econ 50(34-35):3718–3734

Ullah S, Ozturk I, Sohail S (2020a) The asymmetric effects of fiscal and monetary policy instruments on Pakistan’s environmental pollution. Environ Sci Pollut Res. https://doi.org/10.1007/s11356-020-11093-4

Ullah S, Chishti MZ, Majeed MT (2020b) The asymmetric effects of oil price changes on environmental pollution: evidence from the top ten carbon emitters. Environ Sci Pollut Res 27:29623–29635

Wang Q, Xiao K, Lu Z (2020) Does economic policy uncertainty affect CO2 emissions? Empirical evidence from the United States. Sustainability 12(21):9108

Westerlund J (2007) Testing for error correction in panel data. Oxf Bull Econ Stat 69(6):709–748. https://doi.org/10.1111/j.14680084.2007.00477.x

Xu Z (2020) Economic policy uncertainty, cost of capital, and corporate innovation. J Bank Financ 111:105698

York R, Rosa EA, Dietz T (2003) STIRPAT, IPAT and IMPACT: analytic tools for unpacking the driving forces of environmental impacts. Ecol Econ 46(3):351–365

Zaidi SAH, Hou F, Mirza FM (2018) The role of renewable and non-renewable energy consumption in CO 2 emissions: a disaggregate analysis of Pakistan. Environ Sci Pollut Res 25(31):31616–31629

Zhang C, Lin Y (2012) Panel estimation for urbanization, energy consumption and CO2 emissions: a regional analysis in China. Energy Policy 49:488–498

Author information

Authors and Affiliations

Contributions

M.K. Anser: Conceptualization and data analysis

Q.R.Syed: Drafting

N. Apergis: Supervision

Corresponding author

Ethics declarations

Ethics approval

Not applicable.

Consent to participate

Not applicable.

Consent for publication

Not applicable.

Competing interests

The authors declare no competing interests.

Additional information

Responsible Editor: Philippe Garrigues

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Anser, M.K., Apergis, N. & Syed, Q.R. Impact of economic policy uncertainty on CO2 emissions: evidence from top ten carbon emitter countries. Environ Sci Pollut Res 28, 29369–29378 (2021). https://doi.org/10.1007/s11356-021-12782-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-021-12782-4

Keywords

- Economic policy uncertainty

- World uncertainty index

- CO2 emissions

- Environmental Kuznets curve

- Top ten emitters