Abstract

This study aims to provide a systematic literature review based on bibliometric analysis for scientific articles published between 1999 and 2019 extracted from Clarivate Analytics’ Web of Science (WOS) database. The current research project provides an overview of scientific publications, influential authors, and research journals. Our analysis reveals that the USA leads the academic research contribution, whereas China has provided the most research publications in recent years. Environmental and Resource Economics, University of London, and Barcena-Ruiz are the most productive journal, academic institution, and author in the field of environmental taxes, respectively. The degree of research contribution among researchers, institutional and national level, has an upward trend in recent years; however, the research contribution at the author level is higher than the institutional and national level. Furthermore, cocitation analysis suggests that research articles in the dataset are closely related. Pigou’s “The economics of welfare” published in 1920, is considered as the basic literature, and the “In defence of degrowth” authored by Giorgis Kallis is the most cited article. Our analysis of abstracts and keywords indicates that climate change, environmental taxes, double dividend, carbon tax, and environmental pollution are the hotspots within academic literature. We suggest that research collaboration between developed and developing nations and further coordination among environmental agencies such as IEA and IPCC will enhance the effectiveness of environmental reforms.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

Environmental taxes have become one of the hot topics in recent years as it attempts to tax economic activities, which generate negative externalities on the environment (Shahzad 2020). In recent times, public and political opinion on environmental and industrial policy initiatives has shifted towards establishing low-carbon economies (Sun and Ouyang 2016; Ouyang et al. 2019) as significant changes in environmental policies are required to preserve earth’s ecological system from GHG emissions and climate change (Bashir et al. 2020a; Chaabane et al. 2012; Ellerman and Buchner 2007), i.e., adverse weather conditions, excessive moisture, droughts, and rising sea levels. According to the Intergovernmental Panel on Climate Change (IPCC), in comparison with preindustrial revolution, environmental reforms must limit the rise in temperature to be less than 2 °C (Talbi et al. 2020; Pachauri et al. 2014). In this regard, the introduction of environmental taxes not only promote energy efficiency (Bachus et al. 2019; He et al. 2019), e.g., improvements in fuel efficiency, lower per capita fossil fuel consumption but also stimulates growth in the renewable energy sector, which allows energy-exporting countries to project higher foreign exchange reserves as the reduction in domestic fuel consumption can be converted into higher exports towards developing economies (Speck 2017; Wesseh and Lin 2020).

A plethora of studies has analyzed the effectiveness of environmental taxes. Arbolino and Romano (2014) argued that environmental taxes play an active role in preventing environmental degradation in 26 European economies. Freire-González and Ho (2018) found that Spain’s environmental tax reforms were key in limiting pollutant emissions in 39 key industries. Similarly, Rodríguez et al. (2019) proposed that environmental tax reforms improve energy–trade balance, as well as energy efficiency. From an economic perspective, environmental taxes can be divided into two categories: green dividend and blue dividend. The green dividend policies aim to decrease pollutant emissions. On the other hand, the blue dividend focuses on economic growth and encourages economic transformation. Researchers hold contradictory opinions concerning the effectiveness of the double dividend effect of environmental tax. Arbolino and Romano (2014) for European economies and Radulescu et al. (2017) in the case of Romania, articulated that environmental taxes only achieve green dividends. Carraro et al. (1996) and Glomm et al. (2008) were also skeptical and articulated that environmental taxes are just a policy tool to control GHG emissions. On the contrary, Patuelli et al. (2005) contended that environmental tax contributes to the blue dividend by promoting sustainable economic growth and employment opportunities in the renewable energy industry.

This study attempts to provide a comprehensive knowledge map of environmental taxes via bibliometric analysis. Bibliometric analysis is a vital quantitative analysis that provides a useful overview of the research trends in a given subject or field and is extensively used in various research fields (De Bakker et al. 2005; Hirsch 2005). Mao et al. (2015) used bibliometric analysis to evaluate the global research trend of renewable energy from 1994 to 2003. Chen et al. (2017) used bibliometric analysis to analyze research output, publication trends, and research methodologies on climate change publications. Zhang et al. (2016a) explored the impact of carbon taxation and pointed out that GHG emissions, renewable energy, and socioeconomic effects of environment-related taxes were the most discussed issues in the literature. However, most of the research work is limited to a specific environment-related policy instrument (e.g., carbon tax); hence motivating us to analyze environmental taxes, which consist of energy taxes, pollution taxes, transport taxes, and resource taxes, and provide policy recommendations to relevant stakeholders.

We contribute to environmental taxation literature by methodically evaluating the publishing hallmarks of environmental tax publications to comprehend research trends through bibliometric analysis. Our objective is to disclose the following issues: (1) analyze priorities and potential structure holes in the research agenda; (2) discuss the research contribution from the viewpoint of the country of publication, journals, and types of documents; (3) provide detail regarding the most productive authors and highly cited work; and (4) to deliberate environmental tax hot spots and key research directions. The rest of the paper is structured in the following sequence. The “Data and methodology” section represents methodology, the “Results and discussion” section narrates primary results and research trends, and the “Conclusion and policy implications” section presents conclusion and policy implications.

Data and methodology

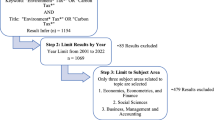

In order to determine the research trend of environmental tax publications, the dataset was obtained from the Web of science core collection by using field tags TS (=Topic), which consist of titles, abstracts, and keywords to create the query. The TS = (“environment tax(es)” OR “environmental tax(es)” was retrieved on April 28, 2020, to obtain the record 621 research papers. Following PRISMA guidelines (Fig. 1), we recruited 476 studies based on our inclusion criteria after carefully reading the full texts of the published articles. We further mention that in the current study, the UK refers to England, Scotland, Wales, and Northern Ireland; “China” refers to Mainland China only; and Hong Kong, Macao, and Taiwan are considered separate entities (Yu et al. 2016; Zhang et al. 2016a).

Flow diagram of the study selection process

This research paper analyses the research trends by using bibliometrix R package as bibliometric analysis software (Aria and Cuccurullo 2017). It is essential to mention that general statistics such as the number of publications, journals, and productive authors, change over time. Furthermore, we rely on H-index, impact factor, and author and academic collaboration to determine each author and country’s contribution to the environmental tax literature. The abovementioned analytical methodology helped provide policy suggestions for different stakeholders. To identify the research hot spots, we selected keywords, research themes, and data methodologies, which form the essence of research literature. We achieved this by cluster and frequency analysis of keywords, which is an efficient technique to investigate the research trends in a given field (Haunschild et al. 2016; Deng et al. 2017).

Assessment of the academic influence

Impact factor and H-index are used in the current study to evaluate authors, journals, and research institutions’ academic influence. The impact factor, published by Journal Citation Reports, is an indicator of academic quality, which validates the evaluation of research references and journal selection. It is defined as “For any given year, the impact factor of a certain journal is the average number of citations gained by a per paper published in that journal during the two preceding years.” We utilize the 2019 Journal Citation Reports for the impact factor. H-index, first proposed by Hirsch in 2005, is defined as “A scientist has index H if H of his/her Np papers have at least H citations each, and the other Np-H papers have no more than H citations each.” H-Index’s evaluation criteria integrate the number of citations and the number of articles for precise academic contribution measurements, where a higher H-index means higher academic impact. Furthermore, it is a useful analytical approach to measure institutional strengths in specific disciplines (Molinari and Molinari 2008).

Academic collaboration

Academic collaboration is a significant indicator of academic development. One of the most distinguishing features is that collaboration for research projects at several levels is quite extensive (Price 1963). The degree of academic collaboration is useful in analyzing research collaboration (Wei et al. 2014). In current research work, we estimate the degree of academic collaboration from the aspects of authors, institutions, and countries, through following formulae (Wei et al. 2013):

where CAⅈ, CIⅈ, and CCⅈ are authors, institutional, and national degrees of collaboration, respectively; αⅈ, βⅈ, and γⅈ stands for numbers of authors, institutions, and countries for the year ⅈ; and N is the total publications in environmental tax(es).

Social network analysis

We further analyze cooperation among researchers along with citation analysis through social network analysis, which helps in determining inter-relationship among social actors. Where “points” represent various social actors, and “edge” illustrates the relationship among “points” (Zhou 2020). Social network analysis is an instrument used to quantify the association among “actors” of the social network (Li and Zhu 2008); which can further be divided into a matrix of social relations and a social network graph. In a matrix, rows and columns represent social elements and social actors, and matrix values signify the relationship between social actors. For network graphs, social actors are represented by nodes and relationships among actors by connecting leads between nodes (Li and Zhu 2008).

Keywords of cooccurrence analysis

Keywords represent core values of the document, and cooccurrence analysis creates an understanding of research trends within the discipline (Aimin 2008). For the current research project, keywords analysis is used to analyze popular research issues in environmental tax publications. The ideas of cocited notion and citation coupling helped develop keywords analysis, where the existence of two or more similar keywords reflect the research direction for a given topic or research area (Renlei 2011). Also, the coword analysis uses a noun phrase or terminology to highlight the research themes within the scientific literature under consideration (Lijia 2008). For the current research document, we use keywords analysis as a mean of coword analysis by using the most frequented keywords to examine current research themes in the environmental tax

Results and discussion

General statistics

The total sample size consists of 476 research papers, and in total, nine languages have contributed towards the scientific output. English is the most dominant contributor with 97% of contribution in scientific work, followed by Spanish (1.62%), Lithuanian (0.41%), Portuguese (0.41%), Czech (0.20%), French (0.20%), Polish (0.20%), Turkish (0.20%), and Ukrainian (0.20%). The annual growth in environmental tax publications demonstrated by Fig. 2 shows that environmental tax publications generally have an upward trend, and can be further subcategorized into two categories. The first category consists of 1999 until 2008, where the annual trend of publications shows progress but is at the initial stage of development. The second category of publications is from 2009 to 2019, displaying exponential growth in the scientific contribution.

The publication output performance of environmental tax(es) documents

Next, we sorted the existing economic literature according to country wise contribution. Research contribution to the sample size of 476 research articles originated from 63 countries and territories. Four articles were excluded from this analysis due to incomplete information. Table 1 summarizes the top 20 contributing regions in the field of environmental tax(es).

The USA contributed most in environmental tax research, with 91 research documents representing 19% of overall publications; followed by China (61; 12.8%) and the UK (45; 9.54%). Additionally, with an h-index of 27, the USA displays superior academic impact than the rest of the countries. In comparison, China is second for the number of publications but is ranked 5th for h-index (11), this points out that China’s influence in the environmental field is relatively low compared to the USA, UK, Spain, and France. On the other side, the publication trend of individual countries reveals a rather interesting trend. In general, the publication trend in the field of environmental taxes is upwards. During the selected sample time frame, the USA maintains its superiority in environmental research with a core focus on environmental taxes’ interaction with economic issues, i.e., the effect of environmental taxes on the industrial sector and its ability to maintain cost competitiveness with emerging economies such as China, Vietnam, and India. Other research areas indicate how environmental taxes can successfully limit fossil fuel consumption and preserve environmental ecology by promoting renewable energy sources. In comparison to the USA, China has shifted its focus in environmental taxes in recent years as the number of research papers published by Chinese researchers during 2016–2019 is greater than the rest of the years combined. This research trend was strongly influenced by the announcements from Ministry of Finance, and National Development and Reform Commission (NDRC) to use environmental taxes as a policy instrument to combat environmental degradation (Kim et al. 2010). Lastly, developed economies lead the research in environmental taxes as China is the only emerging economy in the top 10 countries.

Research collaboration is a common source of sharing and transferring knowledge between research institutes and researchers. The highest collaboration was between China and the USA, which accounted for 12 research documents, followed by the USA and UK (7), USA and France (5), Switzerland and Germany (4), and UK and Germany (4). Our analysis also reveals that the USA and China were responsible for the most collaboration for environmental tax research. Figure 3 provides a detailed graphical outlook of research collaboration among different countries.

Country-wise research collaboration

The analysis of research institutes

For bibliometric analysis, publications of research articles for environmental taxes were contributed by 500 universities and academic institutions. The list for statistical information of the top 20 research institutes is presented in Table 2. Among this list, six research institutes belong to the USA, which is a testament to the USA’s leading position in the field of environmental taxes. France follows this with three research institutions; China and the UK with two representations each and South Korea, Netherlands, Romania, Spain, Sweden, Switzerland, and Taiwan, with one representation in Table 2. Additionally, Japan, Canada, Norway, Australia, Italy, Turkey, Belgium, Czech Republic, and Lithuania were among the top 20 productive countries but had no representation in the list of most productive research institutions. The University of London with 13 publications (h-index 8) is the highest-ranked research institution, followed by University of Basque Country (12), and the University of Maryland Park and University System of Maryland with ten publications each. Chinese universities of North China Electric Power University and Beijing Institute of Technology are positioned 9th and 14th, respectively.

Trend analysis of the top 5 contributing research institutions in terms of the number of papers published reveals a general publication trend in these research institutions. The top 5 research institution list comprises of two institutions from the USA and the UK and one from Spain. The publication trend can be further divided into two parts: pre-2008 and post-2008. The pre-2008 era is dominated by the University of Basque and University of Maryland; however, in the post-2008 era, University of London and University College London have the most significant research contribution, though in general all of the top 5 universities have shown an upward trend in research output.

The distribution of journals

The total sample size of 476 research papers was published in 179 academic journals. Table 3 highlights the top 20 most productive journals, representing 243 (52%) of total research papers. Environmental and Resource Economics is the most prolific journal with 40 (8.40%) research documents, positioning itself as a major research platform for environmental studies. Energy Policy is second (27; 5.67%) with being ranked in categories of economics, energy and fuels, and environmental sciences. Ecological Economics is third (22; 4.62%) and is ranked in the subject categories of ecology, economics, and environmental studies. Additionally, the Journal of Cleaner Production and Renewable and Sustainable Energy Reviews are ranked 8th and 16th in total publications with an impact factor of 7.246 and 10.556, respectively. Our analysis also highlighted that economics, environmental, and ecology studies were the top 3 categories for research publications.

We furthered our analysis by analyzing the trend of research contribution of the top 5 journals. Environmental and Resource Economics was ranked 1st as it had a leading position during the entire time frame. Though short-term volatility from 2003 to 2009 was observed in publications, the general trend of research contribution remains upwards. The rest of the top journals showed increased publications, albeit at less growth rate; Sustainability has published more research work than the rest of the journals from 2016 onwards. Figure 4 illustrates the growth of environmental tax publications in the top 10 journals.

Annual output of top 10 Journals over time

The performance of high-yielding authors

This section provides information about the research contribution of individual researchers by analyzing top 10 authors with the most publications (Table 4). According to statistical information, Barcena-Ruiz, Ekins, and Williams from the University of Basque country, University College London and Resources for the Future respectively are the top contributing researchers. Barcena-Ruiz is the highest contributing author, whereas Ekins and Williams are the most cited authors in the environmental tax literature, which extends their relevance as experts in environmental tax research. Also, out of the top 10 authors, only two authors belong to developing economies, showing that most of the research contributions come from developed economies.

Research collaboration allows researchers to promote research activities and is a source of sharing scientific ideas. Figure 5 reveals collaboration network analysis with a minimum of two edges, for which we used science mapping technology. Our analysis reveals that He PL has the highest collaboration network with seven authors, followed by Heerden (6), Hubacek (3), and Ekins (2). Figure 5 helps create a better understanding to follow research trends as the collaboration among authors is a crucial source of promoting scientific contribution at different levels.

Research collaboration network diagram

Citation analysis

The most authoritative environmental tax publications help create a better understanding of the developments in academic literature, this can be analyzed from two perspectives: first, if it is among the most cited in the literature regarding environmental tax; second, if it is the most cited among environmental tax work. The first perspective includes the studies which are commonly referenced in the environmental tax documents, which may or may not be related to the environmental taxes, i.e., the study may address the general economics of environmental taxes. This provides information about what researchers read while completing the research projects. The second perspective points towards the most cited environmental tax studies, which may or may not be cited in the relevant research work (Bobicki et al. 2012). Determining this trend will share light on the characteristics of popular environmental tax studies. Citation analysis will share the light from these two aspects. For this, Bibliometrix R package software extracted the academic research dataset to present a visual analysis (Fig. 6) of the most frequently cited literature. As shown in the diagram, Pigou (1920), “the economics of welfare” is the earliest cited work in the literature. Pigou proposed that in order to compensate for the gap between social and private capital linked with the production process; polluters should be taxed for the harm caused during the production process; this argument is known as “Pigovian tax.” Next, Armington (1969), “a theory of demand for products distinguished by place of production” is considered the next authoritative contribution. Armington suggested a hypothesis that permits imperfect substitutability among imports and domestic output sold internally. This hypothesis is often cited to support the analytical framework of environmental taxes’ impact on economic activities. In recent literature, Dresner et al. (2006) explored the economic and social implications of environmental taxes and the likelihood of social and political acceptance. They suggested that a proportion of revenue from environmental taxes should be earmarked for environmental projects, and the rest should be used to subsidize labor taxes so that domestic industries remain cost competitive.

Most frequent cited studies

Next, Table 5 presents the top 10 most cited research work in the field of environmental taxes (Bosquet 2000; Ekins 1999; Fullerton and Heutel 2007; Kallbekken and Saelen 2011; Kallis 2011; Krass et al. 2013; Metcalf 1999; Nyborg et al. 2006; Parry and Bento 2000; West and Williams 2012). Of these ten studies, five publications belong to the USA, two to Norway, while Canada, Spain, and the UK have one representation each. The most cited research work is “In defence of degrowth” written by Giorgos Kallis (2011) and was published in Ecological Economics with 324 total citations. Kallis (2011) defended sustainable degrowth by analyzing the premise that if degrowth is inevitable, we could make it socially sustainable and further suggested that the price mechanisms such as environmental taxes need to be complemented by institutional policies to achieve desired outcomes. “Environmental Taxes and the Choice of Green Technology” authored by Krass et al. (2013) and published in Production and Operations Management, is second in total citations (242). Krass et al. (2013) analyzed the use of environmental taxes to promote “green technologies.” Under his proposed model, a profit-maximizing firm reliant upon price-dependent demand chooses emission controlling technology after the introduction of environmental reforms.

Trend analysis

To further analyze the research trends, we use strategic diagrams (Fig. 7) to present research themes within environmental tax publications (Callon et al. 1991; He 1999). According to Callon et al. (1991), the strategic diagram represents four research themes. “Motor themes”, situated in the upper right quadrant of the strategic diagram, carry a high degree of internal development and have a strong relationship with other research concepts. “Highly developed and isolated themes”, upper left quadrant, have higher internal development, but their relevance is marginal to the rest of scientific contribution. “Emerging or declining themes”, lower left quadrant, indicates emerging concepts which do not have sufficient relevance to research contribution and may not be able to achieve relevance in the research contribution. On the other hand, declining themes, despite having internal development, become irrelevant because of the latest developments in the theoretical literature. Lastly, “basic and transversal themes”, lower right quadrant, despite having low internal development show relevance with current issues under investigation. The strategic diagram is enriched based on the size of the circle that showcases the topic and qualitative or quantitative measures adopted, i.e., number of documents published, key references in research work, and number of researchers in a given field. In our sample size, climate change and carbon tax are motor themes. Energy, sustainability, and environmental taxation are highly developed and isolated themes. Pigouvian taxes are declining themes, and environmental regulation can be classified into emerging themes. Finally, environmental tax(es), environmental tax reform, climate policy, and endogenous growth are highlighted as basic and transversal research themes.

Strategic diagram representing research trends of environmental tax(es) documents

Next, we further the academic discussion by highlighting quantitative trends of environmental taxes research. Figure 8 provides a graphical illustration of research trends on a year-on-year basis. Generally, environmental publication trends can be divided into two categories. The first research trend focuses on the time frame of 2006–2011, where the primary focus on research publications analyzed how environmental taxes impact international trade, optimal taxation, and macroeconomic indicators, i.e., endogenous growth (9 frequencies), unemployment (9 frequencies), and imperfect competition (5 frequencies). The second category of environmental publications consists of 2012–until now, where the focus of environmental taxation has been shifted towards environmental regulations and how environment-related taxes can be effectively utilized to curb environmental pollution and achieve sustainable economic development. In this regard, the main research interests have been environmental policy (29 frequencies), double dividend (27 frequencies), carbon tax subsidies (21 frequencies), climate change (12 frequencies), energy taxation (10 frequencies), environmental externalities (9 frequencies), and sustainable development (9 frequencies). Lastly, our analysis of recent environmental tax publications points out that green and clean production regulations, industrial structures’ energy efficiency, and the development of environmental technologies are the future research trends for environmental tax publications (Bashir et al. 2020a).

Analysis of research trends for environmental tax publications

Analysis of research hotspots of environmental taxes

As stated earlier in the “Data and methodology” section, the frequency of keywords in academic publications helps identify the hallmarks of academic research. Most of the keywords in the sample of 476 academic publications are not commonly employed, whereas there is a repetition of a small group of keywords that are widely used. After the initial consolidation of frequent keywords, we utilized the cooccurrence network to draw high-frequency keywords in the Environmental tax literature. Figure 9 shows the interaction of research references, countries, and keywords.

The cooccurrence network of researchers, keywords, and countries

Climate change

“Climate change” is one of the most cited keywords, indicating that environmental tax studies frequently address it. Since the industrial revolution, global climate change has negatively impacted the earth’s ecosystem due to continuous GHG emissions (Bowen et al. 2012). As a result, policymakers in recent times have introduced several policy instruments, i.e., environmental reforms, promoting developments in the environmental technologies and subsidies if necessary, to mitigate climate change. However, there is increased focus in industrial economies to use price incentive policy mechanisms, which requires polluters to pay for environmental pollution through emission trading schemes or environmental taxes. Lastly, as fossil fuel consumption is the primary source of GHG emissions, price mechanisms such as environmental taxes result in higher cost of these resources and ultimately help create shift towards renewable energy consumption.

Environmental tax reforms

Environmental taxes are policy mechanisms intended to prevent environmental degradation, reduce fossil fuel consumption, and provide additional revenue sources to local and federal authorities (Bye and Bruvoll 2008). Economists have long theorized that environmental sustainability can only be achieved by environmental reforms, which was amplified by task force report on the environment (1989), EU economic instruments hearings (1990) and Rome decision (1990) to devise proposals for implementation of environmental taxes. Meanwhile, the Dublin Declaration (1990) and Fifth Environmental Action Program (Europea and Fifth 1992) made formal approaches to adopt such measures as policy instruments. Simultaneously, Delors’ White Paper on growth, competitiveness, and employment specified how such environmental policies create macroeconomic validations. Though the 1990s limited progress gave the impression that the shift in policymaking was more about discussion than practicality, such an impression undervalues the policy contribution since the beginning of the twenty-first century. Environmental awareness has seen environmental taxes as a feasible policy option, especially among Scandinavian and Benelux regions. More recently, industrial economies such as Germany, France, Italy, and the UK have followed this path. Developing economies such as Estonia, Poland, China, and Hungary have integrated environmental and economic initiatives (Tracey and Anne 2008). Asian industrial nations such as Singapore, Korea, Taiwan, and Malaysia in the last decade have also implemented market-based instruments with the traditional command and control regulations (Shinwell and Cohen 2020).

Double dividend

In recent decades, developing economies and industrial countries have faced several constraints in their drive for sustainable development. Their primary concerns include stabilizing energy supply, stable economic growth, and promoting environmental sustainability (Bashir et al. 2015). In this regard, a significant portion of environmental research has analyzed the “double dividend” hypothesis of environmental policies (Patuelli et al. 2005). The “double dividend” hypothesis suggests that implementation of environmental tax policies contributes in both economic and environmental benefits and subsequently recycling of revenues generated from environmental taxation helps lower labor taxes (Fernández et al. 2011; Bento and Jacobsen 2007; Patuelli et al. 2005; Bovenberg and Goulder 2002). A large number of economic studies support the existence of environmental taxes (Pereira et al. 2016; Allan et al. 2014; Fraser and Waschik 2013; Carbone et al. 2013; Orlov et al. 2013; Ciaschini et al. 2012; Saveyn et al. 2011; Bor and Huang 2010); though at the same time, some researchers found no evidence of the double dividend (Zhang et al. 2016b; Li and Lin 2013; Lu et al. 2010) while some have even ruled out such possibility (Wesseh and Lin 2016; Goulder 2013; Oates 1995).

Pollution

Fossil fuel consumption is the most common GHG emissions source, which has a significant contribution to climate change and environmental degradation. The development of cleaner energy sources is an important measure to tackle environmental pollution and climate change (Li et al. 2018; Hu et al. 2019). As stated earlier, environmental taxes introduce additional taxation on fossil energy sources (Shahzad 2020), which leads to the adoption of cleaner energy sources and preserves environmental quality. Several economic studies suggest that adequate environmental policies help promote alternative energy sources and a cleaner environment (Bashir et al. 2020b; Shahzad 2020). Consequently, several studies have analyzed the differences between regulatory policy and incentives of environmental taxes to eliminate pollution and arrived at the similar conclusions that environment-related taxes help reduce environmental pollution in the short as well as long run (Shinwell and Cohen 2020; Sun and Wan 2019; Wesseh and Lin 2016).

The computable general equilibrium model

Computable general equilibrium is the most often used analytical model, which on one side allows feedback and interactions between economy-energy-environment systems to create a linkage mechanism. And on the other side, it is based on a neoclassical microeconomic foundation and can characterize the interaction between variables. The computable general equilibrium (CGE) model can also simulate the interactions between all variables that exist within an economic system (Zhang et al. 2016b). These characteristics enable the CGE model to analyze the criteria that the analysis of environmental tax policies should consider the overall economic system. Because of this, recent studies have used CGE models to investigate the effects of environment tax in industrialized as well as in emerging economies (Asafu-Adjaye and Mahadevan 2013; Allan et al. 2014; Zhang et al. 2016b).

Conclusion and policy implications

The current research work analyzed the performance of environmental tax research by using the Web of Science database through the bibliometric methodology. We summarize our findings in two parts. Part one details the characteristics and evolution of environmental tax literature. Part two outlines research suggestions, policy implications, and possible actions to advance environmental taxes, reduce GHG emission, and protect the environment.

Discussion and summary

Based on bibliometrics analysis, the current research project analyzed environmental tax literature from 1999 to 2019 involving references, keywords, and author information; thus, providing a complete review of environmental tax literature. We have determined that this timeframe oversaw enormous contributions in scientific work, and the number of citations related to environmental taxes grew exponentially. English is the most dominant language for contributing 97% of research work. The USA, as a country, produced the most research contribution; however, China experienced the highest growth for any country in recent years and stands at second position for research contribution. University of London (UK) produced most literature as a research institute, closely followed by the University of Basque (Spain) and the University of Maryland (USA). Also, five out of the top ten research institutes belong to the USA. Higher academic collaboration in recent years means that researchers and institutions are coordinating research activities.

Furthermore, we determine that the top twenty journals were accountable for 52% of environmental tax literature contribution. Environmental and Resource Economics is the most prolific journal, followed by Energy Policy, Ecological Economics, Journal of Environmental Economics and Management, and Sustainability. Additionally, environmental taxes are an interdisciplinary research area with economics, environmental sciences, and environmental studies ranked as the top three categories in the research publications. Barcena-Ruiz and Ekins are the most prolific researchers. Our analysis also found that “welfare economics”, written by Pigou in 1920 is the earliest quoted literature in environmental taxes publications. Climate change, environmental tax(es), double dividend, and pollution are the hot topics in the literature. Lastly, the CGE model is the most widely used analytical methodology.

Policy implications

Based on our analysis of environmental tax literature, we provide the following suggestions to improve environmental tax literature (i) adoption of uniform research policy under UN sustainable development goals will be significant in improving cross-directional and interdisciplinary research contribution. (ii) Research collaboration among academicians and institutions from developed and developing countries should be promoted to eliminate the knowledge gap. (iii) Coordination among organizations such as IEA and IPCC should be promoted to protect the environment. (iv) Establishment of joint research initiatives with compulsory sharing of findings is another way to promote research in environmental issues; (v) lastly, findings of research institutions should be integrated into policymaking to eliminate environmental pollution and climate change.

Despite providing a comprehensive review of environmental tax documents, the current research project has certain noteworthy limitations. First, we have not analyzed the optimal level of environmental taxes and how they can influence economic activities. We also encourage future research to investigate the relationship between environmental taxes and energy efficiency among different economic sectors, i.e., manufacturing, transportation, and services. Lastly, the association between environmental reforms and technological development will also be a significant addition to the academic literature.

Data availability

Research data can be obtained from the corresponding author through email.

References

Aimin Z (2008) The cluster analysis of co-occurrence strength in the field of knowledge management in 2006. Modern Information 28(5):30–33

Allan G, Lecca P, McGregor P, Swales K (2014) The economic and environmental impact of a carbon tax for Scotland: a computable general equilibrium analysis. Ecol Econ 100:40–50

Arbolino R, Romano O (2014) A methodological approach for assessing policies: the case of the environmental tax reform at European level. Procedia Economics and Finance 17:202–210

Aria M, Cuccurullo C (2017) Bibliometrix: an R-tool for comprehensive science mapping analysis. Journal of Informetrics 11(4):959–975

Armington PS (1969) A theory of demand for products distinguished by place of production. Staff Papers 16(1):159–178

Asafu-Adjaye J, Mahadevan R (2013) Implications of CO2 reduction policies for a high carbon emitting economy. Energy Econ 38:32–41

Bachus K, Van Ootegem L, Verhofstadt E (2019) 'No taxation without hypothecation': towards an improved understanding of the acceptability of an environmental tax reform. J Environ Policy Plan 21(4):321–332

Bashir MF, Shahzad U, Latif S, Bashir M (2015) The nexus between economic indicators and economic growth in Brazil. Nexus 13(1)

Bashir MF, Ma B, Shahbaz M, Jiao Z (2020a) The nexus between environmental tax and carbon emissions with the roles of environmental technology and financial development. PLoS One 15(11):e0242412. https://doi.org/10.1371/journal.pone.0242412

Bashir MF, MA B, Shahzad L, Liu B, Ruan Q (2020b) China’s quest for economic dominance and energy consumption: can Asian economies provide natural resources for the success of one belt one road? Manag Decis Econ. https://doi.org/10.1002/mde.3255

Bento AM, Jacobsen M (2007) Ricardian rents, environmental policy and the 'double-dividend'hypothesis. J Environ Econ Manag 53(1):17–31

Bobicki ER, Liu Q, Xu Z, Zeng H (2012) Carbon capture and storage using alkaline industrial wastes. Prog Energy Combust Sci 38(2):302–320

Bor YJ, Huang Y (2010) Energy taxation and the double dividend effect in Taiwan's energy conservation policy—an empirical study using a computable general equilibrium model. Energy Policy 38(5):2086–2100

Bosquet BT (2000) Environmental tax reform: does it work? A survey of the empirical evidence. Ecol Econ 34(1):19–32

Bovenberg AL, Goulder LH (2002) Environmental taxation and regulation handbook of public economics, vol 3. Elsevier, pp 1471–1545

Bowen A, Cochrane S, Fankhauser S (2012) Climate change, adaptation and economic growth. Clim Chang 113(2):95–106

Bye T, Bruvoll A (2008) Multiple instruments to change energy behaviour: the emperor’s new clothes? Energy Efficiency 1(4):373–386

Callon M, Courtial JP, Laville F (1991) Co-word analysis as a tool for describing the network of interactions between basic and technological research: the case of polymer chemsitry. Scientometrics 22(1):155–205

Carbone JC, Morgenstern RD, Williams III RC, Burtraw D (2013) Deficit reduction and carbon taxes: budgetary, economic, and distributional impacts. Resources for the Future

Carraro C, Galeotti M, Gallo M (1996) Environmental taxation and unemployment: some evidence on the ‘double dividend hypothesis’ in Europe. J Public Econ 62(1–2):141–181

Chaabane A, Ramudhin A, Paquet M (2012) Design of sustainable supply chains under the emission trading scheme. Int J Prod Econ 135(1):37–49

Chen L, Zhao X, Tang O, Price L, Zhang S, Zhu W (2017) Supply chain collaboration for sustainability: a literature review and future research agenda. Int J Prod Econ 194:73–87

Ciaschini M, Pretaroli R, Severini F, Socci C (2012) Regional double dividend from environmental tax reform: an application for the Italian economy. Res Econ 66(3):273–283

De Bakker FG, Groenewegen P, Den Hond F (2005) A bibliometric analysis of 30 years of research and theory on corporate social responsibility and corporate social performance. Bus Soc 44(3):283–317

Deng J, Zhang Y, Qin B, Yao X, Deng Y (2017) Trends of publications related to climate change and lake research from 1991 to 2015. J Limnol 76(3)

Dresner S, Jackson T, Gilbert N (2006) History and social responses to environmental tax reform in the United Kingdom. Energy Policy 34(8):930–939

Ekins P (1999) European environmental taxes and charges: recent experience, issues and trends. Ecol Econ 31(1):39–62

Ellerman AD, Buchner BK (2007) The European Union emissions trading scheme: origins, allocation, and early results. Rev Environ Econ Policy 1(1):66–87

Europea C, Fifth E (1992) Environmental action program (towards sustainability: COM (92) 23). Commissione Europea, Bruxelles

Fernández E, Pérez R, Ruiz J (2011) Optimal green tax reforms yielding double dividend. Energy Policy 39(7):4253–4263

Fraser I, Waschik R (2013) The double dividend hypothesis in a CGE model: specific factors and the carbon base. Energy Econ 39:283–295

Freire-González J, Ho M (2018) Environmental fiscal reform and the double dividend: evidence from a dynamic general equilibrium model. Sustainability 10(2):501

Fullerton D, Heutel G (2007) The general equilibrium incidence of environmental taxes. J Public Econ 91(3–4):571–591

Glomm G, Kawaguchi D, Sepulveda F (2008) Green taxes and double dividends in a dynamic economy. J Policy Model 30(1):19–32

Goulder LH (2013) Climate change policy's interactions with the tax system. Energy Econ 40:S3–S11

Haunschild R, Bornmann L, Marx W (2016) Climate change research in view of bibliometrics. PLoS One 11(7):e0160393

He Q (1999) Knowledge discovery through co-word analysis

He P, Sun Y, Shen H, Jian J, Yu Z (2019) Does environmental tax affect energy efficiency? An empirical study of energy efficiency in OECD countries based on DEA and logit model. Sustainability 11(14):3792

Hirsch JE (2005) An index to quantify an individual's scientific research output. Proc Natl Acad Sci 102(46):16569–16572

Hu X, Sun Y, Liu J, Meng J, Wang X, Yang H, Cu J, Yi K, Xiang S, Li Y (2019) The impact of environmental protection tax on sectoral and spatial distribution of air pollution emissions in China. Environ Res Lett 14(5):054013

Kallbekken S, Saelen H (2011) Public acceptance for environmental taxes: self-interest, environmental and distributional concerns. Energy Policy 39(5):2966–2973

Kallis G (2011) In defence of degrowth. Ecol Econ 70(5):873–880

Kim W, Chattopadhyay D, Park JB (2010) Impact of carbon cost on wholesale electricity price: a note on price pass-through issues. Energy 35(8):3441–3448

Krass D, Nedorezov T, Ovchinnikov A (2013) Environmental taxes and the choice of green technology. Prod Oper Manag 22(5):1035–1055

Li A, Lin B (2013) Comparing climate policies to reduce carbon emissions in China. Energy Policy 60:667–674

Li L, Zhu QH (2008) An empirical study of Coauthorship analysis using social network analysis [J]. Inf Sci 4(200)

Li Y, Yang P, Wang H (2018) Collecting coal fired power environmental tax to promote wind power development and environmental improvement. Acta Sci Malays 2:05–08

Lijia ZW (2008) The research of co-word analysis (1)—the process and methods of co-word analysis [J]. Journal of Information 5

Lu C, Tong Q, Liu X (2010) The impacts of carbon tax and complementary policies on Chinese economy. Energy Policy 38(11):7278–7285

Mao G, Liu X, Du H, Zuo J, Wang L (2015) Way forward for alternative energy research: a bibliometric analysis during 1994–2013. Renew Sust Energ Rev 48:276–286

Metcalf GE (1999) A distributional analysis of green tax reforms. Natl Tax J:655–681

Molinari JF, Molinari A (2008) A new methodology for ranking scientific institutions. Scientometrics 75(1):163–174

Nyborg K, Howarth RB, Brekke KA (2006) Green consumers and public policy: on socially contingent moral motivation. Resour Energy Econ 28(4):351–366

Oates WE (1995) Green taxes: can we protect the environment and improve the tax system at the same time? South Econ J 61:915–922

Orlov A, Grethe H, McDonald S (2013) Carbon taxation in Russia: prospects for a double dividend and improved energy efficiency. Energy Econ 37:128–140

Ouyang X, Mao X, Sun C, Du K (2019) Industrial energy efficiency and driving forces behind efficiency improvement: evidence from the Pearl River Delta urban agglomeration in China. J Clean Prod 220:899–909

Pachauri RK, Allen MR, Barros VR, Broome J, Cramer W, Christ R, Church JA, Clarke L, Dahe Q, Dasgupta P (2014) Climate change 2014: synthesis report. Contribution of working groups I II and III to the fifth assessment report of the Intergovernmental Panel on Climate Change, 151

Parry IW, Bento AM (2000) Tax deductions, environmental policy, and the “double dividend” hypothesis. J Environ Econ Manag 39(1):29

Patuelli R, Nijkamp P, Pels E (2005) Environmental tax reform and the double dividend: a meta-analytical performance assessment. Ecol Econ 55(4):564–583

Pereira AM, Pereira RM, Rodrigues PG (2016) A new carbon tax in Portugal: a missed opportunity to achieve the triple dividend? Energy Policy 93:110–118

Pigou AC (1920) The economics of welfare: London

Price DJ (1963) Little science, big science. Columbia University Press, New York

Radulescu M, Sinisi C, Popescu C, Iacob S, Popescu L (2017) Environmental tax policy in Romania in the context of the EU: double dividend theory. Sustainability 9(11):1986

Renlei YSZJ (2011) Research hotspots analysis of digital library based on keywords co-occurrence analysis and social network analysis [J]. Journal of Academic Libraries 4

Rodríguez M, Robaina M, Teotónio C (2019) Sectoral effects of a green tax reform in Portugal. Renew Sust Energ Rev 104:408–418

Saveyn B, Van Regemorter D, Ciscar JC (2011) Economic analysis of the climate pledges of the Copenhagen Accord for the EU and other major countries. Energy Econ 33:S34–S40

Shahzad U (2020) Environmental taxes, energy consumption, and environmental quality: theoretical survey with policy implications. Environ Sci Pollut Res Int 27:24848–24862

Shinwell M, Cohen G (2020) Measuring countries’ progress on the sustainable development goals: methodology and challenges. Evolutionary and Institutional Economics Review 17(1):167–182

Speck S (2017) Environmental tax reform and the potential implications of tax base erosions in the context of emission reduction targets and demographic change. Econ Polit 34(3):407–423

Sun C, Ouyang X (2016) Price and expenditure elasticities of residential energy demand during urbanization: an empirical analysis based on the household-level survey data in China. Energy Policy 88:56–63

Sun R, Wan W (2019) Government strategy for environmental pollution prevention and control based on evolutionary game theory. Nat Environ Pollut Technol 18(2):563–567

Talbi B, Jebli MB, Bashir MF, Shahzad U (2020) Does economic progress and electricity price induce electricity demand: a new appraisal in context of Tunisia. J Public Aff:e2379

Tracey S, Anne B (2008) OECD insights sustainable development linking economy, society, environment: linking economy, society, environment. OECD Publishing

Wei Y, Mi Z, Zhang H (2013) Progress of integrated assessment models for climate policy. Syst Eng Theory Pract 33(8):1905–1915

Wei Y, Yuan X, Wu G, Yang L (2014) Climate change risk assessment: a bibliometric analysis based on web of science. Bulletin of National Natural Science Foundation of China 28(5):347–356

Wesseh PK Jr, Lin B (2016) Modeling environmental policy with and without abatement substitution: a tradeoff between economics and environment? Appl Energy 167:34–43

Wesseh PK Jr, Lin B (2020) Does improved environmental quality prevent a growing economy? J Clean Prod 246:118996

West SE, Williams III RC (2012) Estimates from a consumer demand system: implications for the incidence of environmental taxes fuel taxes and the poor (pp. 98-125): RFF Press

Yu H, Wei YM, Tang BJ, Mi Z, Pan SY (2016) Assessment on the research trend of low-carbon energy technology investment: a bibliometric analysis. Appl Energy 184:960–970

Zhang K, Wang Q, Liang QM, Chen H (2016a) A bibliometric analysis of research on carbon tax from 1989 to 2014. Renew Sust Energ Rev 58:297–310

Zhang X, Guo Z, Zheng Y, Zhu J, Yang J (2016b) A CGE analysis of the impacts of a carbon tax on provincial economy in China. Emerg Mark Financ Trade 52(6):1372–1384

Zhou W (2020) In defence of the WTO: why do we need a multilateral trading system? Legal Issues of Economic Integration 47(1):9–42

Funding

We acknowledge the financial support by the Ministry of Education-China Mobile Joint Laboratory Grant Number: 2020MHL02005.

Author information

Authors and Affiliations

Contributions

Authors’ contributions are the following.

Muhammad Farhan Bashir—writing—review and editing, data curation.

Benjiang MA—supervision, project administration.

Bilal—methodology.

Bushra Komal—resources.

Muhammad Adnan Bashir—investigation, formal analysis.

Corresponding author

Ethics declarations

Ethical approval

We certify that the manuscript titled. “Analysis of Environmental taxes publications: A bibliometric and systematic literature review” (hereinafter referred to as “the Paper”) has been entirely our original work except otherwise indicated, and it does not infringe the copyright of any third party. The submission of the Paper to Environmental Science and Pollution Research implies that the paper has not been published previously (except in the form of an abstract or as a part of a published lecture or academic thesis), that it is not under consideration for publication elsewhere, that its publication is approved by all authors and that, if accepted, will not be published elsewhere in the same form, in English or any other language, without the written consent of the Publisher.

Copyrights for articles published in Environmental Science and Pollution Research are retained by the author(s), with first publication rights granted to Environmental Science and Pollution Research.

Consent to participate

We affirm that all authors have participated in the research work and are fully aware of ethical responsibilities.

Consent to publish

We affirm that all authors have agreed for submission of the Paper to ESPR and are fully aware of ethical responsibilities.

Competing interests

The authors declare that they have no conflict of interest.

Additional information

Responsible Editor: Baojing Gu

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Bashir, M., MA, B., Bilal et al. Analysis of environmental taxes publications: a bibliometric and systematic literature review. Environ Sci Pollut Res 28, 20700–20716 (2021). https://doi.org/10.1007/s11356-020-12123-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-020-12123-x

Keywords

- Environmental tax

- Bibliometric analysis

- Massive literature data

- Frequency and cooccurrence analysis

- Research trends