Abstract

The Environmental Kuznets Curve hypothesis is a theoretical proposition explicating the link between a locality’s income level and environmental degradation. Previous studies estimated the current relationship with an unchanging parameter. However, due to changes in global conomic and political conditions, natural disasters, technological shocks, and implemented policies, the link between income and environmental degradation is about to change. The study investigates the income-pollution nexus for G7 countries—Canada, France, Germany, Italy, Japan, the UK, and the USA—from 1970 to 2014 using a novel methodology: bootstrap panel rolling window causality. In this context, this approach is advantageous for determining the link between income and pollution level in sub-sample periods, rather than assuming an unchanging parameter, and captures the hidden causal linkages between income and environmental pollution. The results confirm the validity of the EKC hypothesis in Japan and the USA, whereas in the other countries, the relationship between EF and GDP exhibits no evidence for an inverted U-shaped pattern.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

Ongoing economic growth through rapid industrialization has generated immense environmental stress, resulting in a challenging trade-off between economic growth and environmental quality in this century. The increasing visibility of the immense effects of global environmental degradation has increased awareness of environmental problems and attracted worldwide attention because of rising environmental concerns (Destek and Sarkodie 2019). Total global carbon dioxide emissions increased by 63.15% between 1990 and 2014 (WDI 2018). Gill et al. (2018), citing Van den Bosch (2016), reported that environmental damage is harming the planet at a faster rate than before and that governments are trying to help the planet recover. These challenges and discussions have spurred scholars and policymakers to search for ways to relieve environmental pressures while achieving higher growth rates (Ozcan et al. 2018). Thus, the environmental impacts of economic growth have become a central issue in debates on globally sustainable economic growth, and scholars have started to examine the income–pollution nexus in recent decades (Dinda 2004).

The Environmental Kuznets Curve (EKC) hypothesis, the theoretical proposition explaining the link between income level and environmental pollution, has come to the forefront following Grossman and Krueger’s (1991) pioneering study. The EKC hypothesis posits that with the first stages of economic growth, environmental degradation increases up to a certain point; after this threshold is reached, the rise in income level leads to improvement in environmental quality. Grossman and Krueger (1995) argued that the EKC hypothesis can occur through three distinct channels: the scale effect, composition effect, and technique effect. The scale effect shows that in the early stages of economic development, increased use of natural resources to accelerate economic activity creates more environmental damage (Aslan et al. 2018). The composition effect underlines the role of modification in the production structure: In other words, the transformation may increase environmental quality when the economy moves toward the service sector (Akbostancı et al. 2009). Finally, the technique effect indicates that enhancements in production technologies may drive down the amount of pollution releaesed by industrial processes (Ang 2007). Thus, the EKC hypothesis assumes an inverted U-shaped relationship between income level and environmental pollution (Panayotou 1993).

Policymakers must recognize the character of the causal relationship between income and pollution. Thus, the main purpose of empirical studies intended to validate the EKC hypothesis is to clarify whether economic growth is the root of the problem or part of the solution (Coondoo and Dinda 2002; Dinda 2004). In this context, most such studies have used reduced-form polynomial equations to test the validity of the EKC hypothesis. These models attempt to explain the level of pollutant emissions (specifically CO2 emissions) using real GDP and square of real GDP in place of explanatory variables. However, reduced-form equations are based on certain assumptions: They are silent about causal mechanisms (Dinda 2004), and they suggest that the estimated parameters are stable in all sub-periods and reflect the whole sample; further, they imply that countries move along the predicted pattern (Aslan et al. 2018). Moreover, most studies on the income–pollution nexus have focused on a small group of pollutants, using CO2 emissions as a measure of environmental degradation. Although CO2 emission is largely responsible for the greenhouse effect (Shahbaz et al. 2016), it represents just a fraction of overall environmental degradation and embodies only one aspect of environmental pollution (Ozcan et al. 2018; Destek and Sarkodie 2019).

As a remedy, the current study suggests a bootstrap panel rolling window causality test and examines the income–pollution nexus for G7 countries—Canada, France, Germany, Italy, Japan, the UK, and the USA—from 1970 to 2014. Because global economic and political conditions, natural disasters, technological shocks, and policy changes may change the link between income and pollution over sub-sample periods (Shahbaz et al. 2016), this methodology is advantageous for determining the link between income and pollution in sub-sample periods rather than assuming an unchanging parameter (Aslan et al. 2018; Ozcan et al. 2018). In addition, this study employs a comprehensive measure for environmental degradation, namely the ecological footprint (EF) first proposed by Rees (1992) and developed further by Wackernagel and Rees (1996). The EF is computed as the sum of footprints of built-up land, carbon, cropland, fishing, grounds, forest products, and grazing land and serves as a metric for the country’s available biocapacity rather than carbon emissions alone. However, this study is limited in that it excludes the effects of other factors (i.e., energy consumption, financial development) on pollution level and focuses on testing the validity of the core EKC framework.

There are various reasons for focusing on the income–pollution nexus for G7 countries. First, the G7 countries are the most developed and industrialized countries in the world and can directly affect global policies. Second, together they generated 24.26% of global CO2 emissions in 2014 (WDI 2018). With the exception of the USA, they have endorsed the Kyoto protocol’s goal to reduce their greenhouse gas emissions. Also, the G7 countries have enacted regulations for cleaner and more environmentally friendly production (Ajmi et al. 2015).

The rest of the paper is structured as follows. Section 2 gives a literature review. Section 3 describes the data used and defines the methodology. Section 4 provides empirical results. Section 5 presents the discussion. Section 6 concludes the study.

Literature review

The first set of empirical studies to test the validity of the EKC hypothesis were Grossman and Krueger (1991), Shafik and Bandyopadhyay (1992), and Panayotou (1993). Of these, Grossman and Krueger (1991) explored the link between various air pollution measures and income. They estimated a random effects model and found an inverted U-shaped relationship. Later, Shafik and Bandyopadhyay (1992) used 10 different pollution measures and estimated a set of panel regression models to investigate the income–pollution nexus in 149 countries over the period between 1960 and 1990. In their study, two out of ten pollution measures verified the EKC hypothesis. Panayotou (1993) verified the inverted U-shaped relationship between income per capita and various measures of environmental degradation by employing the cross-sectional data in 68 countries, calling it EKC.

Following these preliminary studies, researchers have paid more attention to the relationship between income and environmental degradation, and much has been written on this subject over the last three decades. The results of these studies examining the economic growth–environmental pollution nexus with several pollution measures were inconclusive because of differences in explanatory variables, model specifications, and various country-specific characteristics.

This study summarizes the existing literature on the validity of the EKC hypothesis in two main strands. In this context, the first group of studies employed time series and panel data regression models and focused on discovering the EKC by estimating the parameters of various income measures (lower and higher powers of income). Of these studies, Kaufmann et al. (1998) examined the link between spatial intensity of economic activity and SO2 measure in 22 countries over the period 1974–1989. Using a list of spatial economic intensity measures, they estimated fixed-effect and random-effect models to demonstrate an inverted U-shaped relationship that confirmed the EKC hypothesis. Richmond and Kaufmann (2006) further included both non-renewable and renewable energy consumption in EKC modeling. They estimated several models by applying the pooled ordinary least squares (OLS) approach to 20 developed and 16 emerging economies between 1973 and 1997. Their findings verified an inverted U-shaped relationship between income per capita and pollutant emissions with different turning points in developed and emerging countries.

By using province-level data, Song et al. (2008) explored the link between environmental deterioration and income level in 29 Chinese provinces over the period 1985–2005. They used three pollutant measures—waste gas, wastewater, and solid wastes—in per-capita terms and per-capita GDP in their analysis. According to Pedroni cointegration test results, all three measures exhibited an inverted U-shaped relationship and proved the EKC hypothesis. In an alternative province-level study, Akbostancı et al. (2009) examined the link between environmental pollution and income in 58 Turkish provinces over the period 1992–2001. Using the generalized least squares method, they found an N-shaped relationship between pollution measures and income per capita.

He and Richard (2010) argued that the fully parametric regression models fail to discover the exact form of the relationship. Instead, they performed semiparametric and nonlinear parametric models to estimate the EKC hypothesis in Canada from 1948 to 2004. They concluded that waiting for a threshold level for cleaner production is not a practical solution for Canada. Musolesi et al. (2010) criticized the slope homogeneity assumption across countries and allowed for cross-country heterogeneity. They employed a hierarchical Bayes estimator to investigate the EKC in a panel of 109 countries in five sub-samples between 1959 and 2001. They found that the G7, EU15, and OECD countries verified an inverted U-shaped association between per-capita emissions and per-capita income, whereas less-developed countries demonstrated a monotonically increasing pattern. In another panel data study, Apergis and Ozturk (2015) performed a dynamic estimation procedure that used generalized method of moments (GMM) in a multivariate framework, including measures of pollution, income, population density, industrial production, land, and institutional quality, to test the EKC hypothesis in 14 Asian countries. The results confirmed the inverted U-shaped relationship with the adoption of various measures.

Baek (2015) tested the EKC hypothesis by adding an energy consumption variable in seven Arctic countries for the period between 1960 and 2010. Their study used an autoregressive distributed lag (ARDL) model to overcome the aggregation bias while examining the EKC for linear, quadratic, and cubic functions. Individual country-level results exhibited mixed results across countries and functional forms. In a recent panel data analysis, Bilgili et al. (2016) examined the validity of the EKC hypothesis with the adoption of renewable energy consumption in 17 OECD countries from 1977 to 2010. They used the Pedroni panel cointegration test and got long-term individual country coefficients via panel DOLS and panel FMOLS estimations. Their findings provided evidence for the EKC hypothesis in the panel and demonstrated that renewable energy consumption reduces pollutant emissions. More recently, Liddle and Messinis (2018) discovered the association between per-capita emissions and per-capita GDP in 21 OECD countries from 1870 to 2010. They employed a reduced-form linear model that could handle multiple endogenous breaks and could approximate nonlinear relationships without any prior model specification. They concluded that the income–carbon emissions nexus is country-specific and that when a country attains a certain developmental level, the relationship between the two becomes less significant.

The second group consists of the studies that concentrated on the causal linkage between income and environmental pollution, either solely or in addition to the parameter estimation while exploring the EKC. Of these studies, Ang (2007) discovered the dynamic relationship between environmental degradation, energy consumption, and income in France from 1960 to 2000. The study employed the ARDL bounds test and vector error correction mechanism. The author found a significant cointegration among the variables and a long-term bidirectional causal relationship between income and environmental pollution. These findings provided evidence for EKC. In an alternative study for France, Iwata et al. (2010) included consumption of electricity generated from nuclear energy in their EKC analysis. Using the ARDL method and Granger causality test to extract causal links among variables, they estimated a quadratic model that found evidence of an inverted U-shaped relationship for pollutant emissions.

Tiwari et al. (2013) included trade in their EKC analysis in India from 1966 to 2011 using ARDL for cointegration and VECM for causality analysis. Causality results indicated a bidirectional relationship between income and environmental pollution. Their findings demonstrated that the EKC hypothesis is valid in both the short and long runs. By including trade openness as one element in a dynamic multivariate framework, Arouri et al. (2013) also employed ARDL and VECM to test the EKC hypothesis in Thailand for the period 1971–2010. Using a quadratic model, they confirmed an inverted U-shaped relationship. In addition, unidirectional causality running from income to pollutant emissions verified the EKC hypothesis. Kivyiro and Arminen (2014) offered a test of the EKC hypothesis for six relatively low-income sub-Saharan African countries for the period 1971–2009. In the same vein, the ARDL cointegration technique confirmed the EKC hypothesis in three of the six countries. The results of the Granger causality analysis indicated a unidirectional causality running from income to emissions in two of the sample countries.

In another study, Jebli et al. (2016) used multivariate cointegration and a causality framework to confirm the EKC hypothesis in 25 OECD countries from 1980 to 2010. Their findings offered an inverted U-shaped relationship between CO2 emissions and GDP for OECD countries. Moreover, the causality results reported that the CO2 emissions exerted their effects on GDP in the short term. Bento and Moutinho (2016) explored the link between pollutant emissions, income, non-renewable electricity production, renewable electricity production, and international trade in Italy for the period 1960–2011. In the cointegration setting, they employed ARDL bounds testing to verify the validity of the EKC hypothesis. In the long-run causality framework, they used the Toda–Yamamoto causality test and highlighted the role of renewable electricity production to afford environmental quality over time. In an alternative study for Italy covering the period 1970–2006, Magazzino (2016) found a bidirectional causality between CO2 emissions and economic growth.

In the Japanese case, Rafindadi (2016) investigated the presence of the EKC hypothesis during environmental disasters over the period 1961–2012. ARDL bounds test findings verified the existence of the EKC hypothesis. The study also employed an innovative accounting approach to analyze the causal link between income and environmental degradation. This approach combined impulse–response and variance decomposition analyses. The results for the innovative accounting approach found a unidirectional causality running from income growth to CO2 emissions. Shahbaz et al. (2017) analyzed a long period between 1820 and 2015 to discover the association between environmental pollution and income in G7 countries. They argued that the form of the relationship may include nonlinearities over such a long period, and they employed parametric models that did not require a specific model form. Their findings favored the EKC hypothesis in all G7 countries except Japan.

More recently, Destek and Sarkodie (2019) handled ecological footprint data as a measure of environmental degradation and tested the presence of EKC in 11 newly industrialized countries for the period between 1977 and 2013. To this end, they employed the Dumitrescu and Hurlin (2012) heterogenous panel causality test and an augmented mean group estimator (AMG) that considered cross-country heterogeneity. The estimation results verified the inverted U-shaped relationship between ecological footprint and income in four of eleven countries. The heterogeneous panel causality test results demonstrated a bidirectional causality and verified the feedback hypothesis.

Relatively few studies have been concerned with the time-varying causal linkage between environmental pollution and income in a time-series context. The analysis of the time-varying causal relationship between income and pollution in the EKC framework is a novel approach. Of such studies, Ajmi et al. (2015) investigated the causal relationship between income, pollutant emissions, and energy consumption in G7 countries other than Germany based on a time-varying Granger causality test from 1960 to 2010. Their findings in individual countries confirmed an N-shaped relationship between income and CO2 emissions, which in turn did not favor the EKC hypothesis in these countries. In another study, using time-varying Granger causality, Shahbaz et al. (2016) also employed income, pollution measure, and energy consumption to test the validity of the EKC hypothesis in the next 11 countries for the period 1972–2013. They found a one-way causality running from economic growth to CO2 emissions in Indonesia and Turkey and verified the presence of the EKC hypothesis for these countries as well.

In the case of the USA, Tzeremes (2018) examined the relationship between income, environmental pollution, and energy consumption for the 50 US states spanning the period 1960–2010. In most states, the time-varying Granger causality test indicated an N-shaped pattern for income and environmental pollution and energy consumption, albeit with mixed results for all states. Similarly, Aslan et al. (2018) used a bootstrap rolling window causality analysis to test the presence of the EKC hypothesis in the USA over the period 1966–2013. Their findings confirmed the inverted U-shaped relationship and proved the EKC hypothesis. In the same vein, Ozcan et al. (2018) used a bootstrap rolling window causality to test the EKC hypothesis in Turkey from 1961 to 2013. They handled ecological footprint as a measure of environmental pollution and real GDP per capita as an income measure. They reported a bidirectional causal linkage between income and ecological footprint with no room for the existence of the EKC hypothesis.

In conclusion, unlike most of the previous studies, this study analyzes the income-pollution nexus in the EKC framework, considering the possibility of changes in the causal relationship in sub-sample periods in the panel data settings. In other words, rather than assuming an unchanging parameter for the timespan, the time varying ootstrap rolling window causality test estimates the current relationship in sub-sample periods.

Data and econometric methodology

Data

This study investigated the causal relationship between income and environmental degradation in G7 countries from 1970 to 2014. The measure of the income level is the per-capita GDP, and the measure for environmental degradation is the per-capita EF. Here, GDP is measured in constant 2010 USD and obtained from the World Bank’s World Development Indicators. The EF—computed as the sum of footprints of built-up land, carbon, cropland, fishing, grounds, forest products, and grazing land—is expressed in global hectares and obtained from the Global Footprint Network (2019). Both variables have been transformed into natural logarithmic form before exposure to econometric tests and analysis.

Econometric methodology

Cross-sectional dependence tests

Ignoring cross-sectional dependence among panel members may lead to biased results. Thus, before examining the causality, we first tested the cross-sectional dependence among G7 countries. To this end, we have estimated the following equations, to compute the cross-sectional dependence tests:

where T and N show, respectively, the number of panel members and the time period. We have tested the null hypothesis of no dependency among the cross sections against the alternative of dependency between at least two cross sections. First, we computed the Lagrange multiplier test statistic developed by Breusch and Pagan (1980), suitable for a small-number cross-sectional unit (N) and sufficiently large period of time (T), using the following formula:

where \( {\hat{\rho}}_{ij} \) shows a sample estimate of the correlation coefficient obtained from the residuals of Eqs. 1 or 2. The LM test statistic is distributed as chi-square with n(n − 1)/2 degrees of freedom. However, for the cases where N is large relative to time period, the LM test statistic is not applicable. To address this shortcoming, Pesaran (2004) suggested a scaled version of the test statistic:

The LMS test statistic is distributed as N(0, 1)under the null. Both LM and LMS test statistics exhibit substantial size distortions. Thus, Pesaran (2004) proposed the following test statistic based on the average \( {\hat{\rho}}_{ij} \)s:

Pesaran et al. (2008) showed that reaching a conclusion about the null using critical values from standard normal distribution in CD test leads to size distortion, so they introduced the following test statistic:

where k is the number of regressors, and μ and V show the expected value and variance of \( {\hat{\rho}}_{ij} \). LMadj is distributed as normal.

Panel causality test

Most empirical studies testing the validity of the EKC hypothesis through causality analysis have not focused on the form of the relationship within sub-samples. This study has discovered the causal link between income and environmental degradation in the EKC framework via a bootstrap rolling window causality approach to clarify the causal link in sub-samples.

To this end, this study employed the panel causality test proposed by Kónya (2006). This test does not require a pretest for unit root and cointegration before the causality analysis, so it does not suffer from pretesting bias. On the other hand, this test accounts for cross-sectional dependence and considers the heterogeneity for the panel, so it is possible to test the causality relationship individually in the panel data context. To implement the causality test, we estimated the following set of equations via Zellner’s (1962) SUR estimator:

and

where l is the optimal lag length, which we have determined using Akaike information criteria. To test for causality from EF to GDP for the first member of the panel, we tested the significance of γ1, 1, l using the Wald test in Eq. 3, with cross-section-specific bootstrap critical values. Similar causality relationships can be examined by testing the associated terms.

Global economic and political events may change the pattern of causality relationship events (see Tang 2008). However, Konya’s (2006) bootstrap panel causality test shows only the results for the full sample. Therefore, we investigated the stability of the causality relationship using the bootstrap panel causality test in rolling subsamples for t = τ − 1 + l, τ − 1, τ = l, l + 1, ..., T where l shows the fixed size of subsamples. We obtained the necessary critical values and p values by bootstrap simulations to control small-sample bias.

Empirical results

In the first step of this analysis, we explored the cross-sectional dependence across G7 countries. We have tabulated the test results in Table 1.

The results of the CD tests support evidence for cross-sectional dependence. Next, to see the causal link between GDP and EF in a full sample, we employ a bootstrap panel causality test and report individual country results in Table 2.

The upper part of Table 2 shows the results for testing the null hypothesis that economic growth (GDP) does not cause environmental degradation (EF), whereas the lower part indicates the converse. The causality running from GDP to EF seems not to be in tune for the sample countries. However, the individual results between EF and GDP show that in only two of seven countries—Japan and the UK—a unidirectional causality runs from EF to GDP. The null of non-causality cannot be rejected for the remaining countries.

In addition to the unit root properties and cointegration relationship, economic, structural, and technological changes also affect causality tests. That is, the nature and/or the existence of a causal linkage may change over time. This study considered this instability by testing the causality between EF and GDP in sub-samples by rolling sample coefficients to test the validity of the Environmental Kuznets Curve hypothesis. In this sense, the study sets the sub-sample size as 15 years and determined the optimal lag length in subsamples using Akaike information criteria.

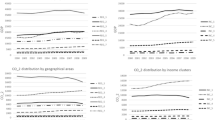

With the bootstrap full sample panel causality analysis finding no causal relationship running from GDP to EF and quite weak unidirectional causality running from EF to GDP, Fig. 1 illustrates the bootstrap p values for the test of causality from GDP to EF along with the 10% critical level in the rolling windows.

Bootstrap p values for causality from GDP to EF in rolling window estimation

The results for bootstrap rolling window causality from GDP to EF in Fig. 1 demonstrate no causal link running from GDP to EF in Canada, France, or Germany. These results align with the findings of the bootstrap panel causality in these countries. However, in the remaining countries, the study used the bootstrap rolling window panel causality test to advantage because the test captures the hidden causality in some periods. Figure 1 confirms that GDP causes EF in Germany in 1989, 1991, 1996, 2002–2005, and 2009–2010; in Japan in 1990–1995, 2002–2005, 2007, and 2010–2014; in the UK in 1998–1999, 2004–2006, and 2012–2013; and in the USA in 1995–1996, 2001, and 2009–2014.

In the same sense, Fig. 2 depicts the test results for the bootstrap rolling window causality relationship from EF to GDP in the subsamples.

Bootstrap p values for causality from EF to GDP in rolling window estimation

The findings for bootstrap rolling window causality are quite different from those for full-sample pane causality. The results in Fig. 2 indicate no causal relationship running from EF to GDP in France, Germany, and Italy. However, in the remaining countries, the study benefitted from the use of the bootstrap rolling window panel causality test, which captures the hidden causality in some periods. Figure 2 shows that the null of EF does not cause the GDP to be rejected over some sub-sample periods. The results suggest a unidirectional causality running from environmental deterioration to economic growth in Germany in 1986–1987, 2001, and 2003; in Italy in 2013; in Japan in 1984, 2007–2008, 2011, and 2014; in the UK in 1984, 1987, 1992–1993, and 1998–1999; and in the USA in 1992–1993 and 2009. Based on these results, we can conclude that a feedback causality exists between GDP and EF in Germany in 2002–2003, in Japan in 2007 and 2014, in the UK in 1992–1993 and 1998–1999, and in the USA in 2003. Here, the presence of feedback causality indicates that economic growth and environmental quality have similar trends because they have a simultaneous impact on each other. Also, no causal relationship is evident between income and environmental degradation in France and Italy, even in sub-sample periods.

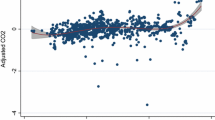

Additionally, by following the studies of Ozcan et al. (2018) and Aslan et al. (2018), this study documented the impact of GDP on EF in subsamples. Figure 3 depicts the impact of GDP on the EF:

Rolling window estimation results for the impact of GDP on EF

When the impact of GDP on EF is interpreted in terms of trend, Fig. 3 offers the following implications: In Japan, the effect of GDP on EF increased between 1986 and 1995. After reaching its peak in 1995, this trend alternates in sign. Thus, these results exhibit an inverted U-shaped relationship in Japan and verify the EKC hypothesis. Similarly, in the case of the USA, the effect of GDP on EF first increases and reaches its peak and then starts to decrease, which in turn provides evidence for the EKC hypothesis.

Conversely, findings on the impact of GDP on EF do not favor the EKC hypothesis in Canada, France, Germany, Italy, or the UK. The impact of GDP on EF first decreases to the trough up to 2003 and then it begins to increase. Thus, the effect of GDP on EF exhibits a U-shaped pattern. However, in France and the UK, the pattern of the impact of GDP on EF demonstrates the upswing in EKC. Here, the U-shaped curve indicates that the impact of an income on environmental pollution changes over the different stages of economic development. In the case of Canada and Italy, the results are inconclusive that the impact of GDP on EF is negative in some periods and positive in others, which in turn rejects the EKC hypothesis.

In the next step, this study presents the impact of environmental pollution on income in seven countries in sub-samples. In this sense, Fig. 4 shows the effect of EF on GDP.

Rolling window estimation results for the impact of EF on GDP

Figure 4 shows that in most of the sub-sample periods, environmental degradation negatively affects economic growth in Canada, France, and the UK and positively affects economic growth in Italy, Japan, and the USA.

As a conclusion, these findings indicate that most of the countries in our sample (five of seven countries) do not verify the EKC hypothesis and the impact of environmental degradation on income level does not provide conclusive results for sample countries.

Discussion

This study first employed the full-sample bootstrap panel causality test and then used a bootstrap panel rolling window causality approach to test whether causality relationship changes in sub-sample periods.

The empirical results of the full sample bootstrap panel causality indicate a one-way causality running from EF to GDP in Japan and the UK. In other words, implemented environmental policies can affect the output level in these countries. In the case of Japan, these results differ from the findings of Ajmi et al. (2015) and Shahbaz et al. (2017). In the UK, our findings are in line with Shahbaz et al. (2017) but inconsistent with that of Ajmi et al. (2015).

This study rejects the causal relationship in either direction in Canada, France, Germany, Italy, and the USA. These findings do not favor the previous studies of Ang (2007) or Iwata et al. (2010) for France; Ajmi et al. (2015) for Canada, France, or Italy; Shahbaz et al. (2017) for Canada, Germany, or the USA; or Magazzino (2016) for Italy. However, findings on full-sample causality are similar to that of Ajmi et al. (2015) for France and the USA and to Bento and Moutinho (2016) for Italy.

In addition to full-sample bootstrap panel causality results, the study benefitted from using bootstrap panel rolling window causality. The sub-sample results indicate a bidirectional feedback causality between EF and GDP in some sub-samples in Germany, Japan, the UK, and the USA. Economic growth in industrialized countries activates the depletion of more natural resources, harms the environment, and reduces biocapacity (Bilgili et al. 2016).

This study has verified an inverted U-shaped relationship between EF and GDP and provides evidence for the existence of the EKC hypothesis in Japan and the USA. In the case of Japan, the results are consistent with those of Rafindadi (2016) and dissimilar with those of Shahbaz et al. (2017). In the case of the USA, our findings are similar to those of Shahbaz et al. (2017) and Aslan et al. (2018) but are inconsistent with those of Baek (2015). Thus, when income level increases in these countries, environmental awareness increases and people demand cleaner production. Higher economic growth tends simultaneously to mitigate environmental degradation and produce better environmental performance. In other words, the existence of the EKC hypothesis indicates that the good economic performance may go hand in hand with a cleaner environment.

In Germany, the relationship between EF and GDP appears U-shaped, which does not favor the findings of Shahbaz et al. (2017). The existence of a so-called U-shaped relationship may be due to traditional production technologies (Destek and Sarkodie 2019). The upswing of the EKC in France and the UK indicates the difficulty of maintaining efficiency improvements as the economy grows over time (Dinda 2004). By providing evidence against the existence of the EKC hypothesis, the findings of this study are not in line with Bilgili et al. (2016) or Shahbaz et al. (2017) but are consistent with Ajmi et al. (2015). Finally, by indicating no particular relationship between income and pollution for Canada and Italy, our results are the opposite, respectively, of Bilgili et al. (2016) and Bento and Moutinho (2016). However, for Canada, we reach conclusions similar to those of He and Richard (2010).

Although the EKC hypothesis is the one that claims an inverted U-shaped relationship between environmental pollution and income, this linkage might not exhibit some definite relations in different stages of economic growth. Thus, one can conclude that sub-samples in such advanced countries yield various conclusions.

Conclusion

This study investigated the causal relationship between environmental degradation and income level in the EKC context in G7 countries from 1970 to 2014. To this end, the paper employed ecological footprint as a measure of environmental degradation and the per-capita real GDP as an income measure.

The study makes several contributions to the existing literature. First, it contributes to the literature by using Konya’s (2006) bootstrap panel causality test in a time-varying framework. To the best of our knowledge, this is the first study to employ time-varying bootstrap panel causality. This methodology takes advantage of discovering causal linkage in sub-sample periods. Second, this study has employed a more comprehensive measure of environmental degradation in testing the validity of the EKC hypothesis. Third, the use of the bootstrap technique mitigates the size distortions for small samples.

The bootstrap full-sample panel causality test results show that there is no causality running from GDP to EF in all G7 countries. The findings of the study indicate a one-way causality running from EF to GDP in Japan and the UK. However, the study benefitted from using a bootstrap rolling window panel causality test, which captured the hidden causal linkages between GDP and EF in some periods for several countries. In the next step, the study confirmed the EKC hypothesis in Japan and the USA, whereas in the remaining countries, the relationship between EF and GDP exhibits no evidence for an inverted U-shaped pattern.

The confirmation of the EKC hypothesis in Japan and France implies that these countries may realize higher economic growth rates with little harm to the environment. For the remaining countries, the impact of income on environmental degradation changes over the different stages of economic development. Hence, the pivotal point is to find a delicate balance between economic growth and environmental sustainability. To mitigate the harmful effects of economic development and make it sustainable, governments must (i) replace the new technologies in production to improve environmental quality, (ii) integrate climate change measures into national policies, and (iii) enhance global partnership and international collaborations among countries (Sarkodie and Strezov 2019).

References

Ajmi AN, Hammoudeh S, Nguyen DK, Sato JR (2015) On the relationships between CO2 emissions, energy consumption and income: the importance of time variation. Energy Econ 49:629–638. https://doi.org/10.1016/j.eneco.2015.02.007

Akbostancı E, Türüt-Aşık S, Tunç Gİ (2009) The relationship between income and environment in Turkey: is there an environmental Kuznets curve? Energy Policy 37(3):861–867. https://doi.org/10.1016/j.enpol.2008.09.088

Ang JB (2007) CO2 emissions, energy consumption, and output in France. Energy Policy 35(10):4772–4778. https://doi.org/10.1016/j.enpol.2007.03.032

Apergis N, Ozturk I (2015) Testing environmental Kuznets curve hypothesis in Asian countries. Ecol Indic 52:16–22. https://doi.org/10.1016/j.ecolind.2014.11.026

Arouri M, Shahbaz M, Onchang R, Islam F, Teulon F (2013) Environmental Kuznets curve in Thailand: cointegration and causality analysis. J Energy Dev 39(1/2):149–170

Aslan A, Destek MA, Okumus I (2018) Bootstrap rolling window estimation approach to analysis of the environment Kuznets curve hypothesis: evidence from the USA. Environ Sci Pollut Res 25(3):2402–2408. https://doi.org/10.1007/s11356-017-0548-3

Baek J (2015) Environmental Kuznets curve for CO2 emissions: the case of Arctic countries. Energy Econ 50:13–17. https://doi.org/10.1016/j.eneco.2015.04.010

Bento JPC, Moutinho V (2016) CO2 emissions, non-renewable and renewable electricity production, economic growth, and international trade in Italy. Renew Sustain Energy Rev 55:142–155. https://doi.org/10.1016/j.rser.2015.10.151

Bilgili F, Koçak E, Bulut Ü (2016) The dynamic impact of renewable energy consumption on CO2 emissions: a revisited environmental Kuznets curve approach. Renew Sustain Energy Rev 54:838–845. https://doi.org/10.1016/j.rser.2015.10.080

Breusch T, Pagan A (1980) The Lagrange multiplier test and its application to model specification in econometrics. Rev Econ Stud 47(1):239–253. https://doi.org/10.2307/2297111

Coondoo D, Dinda S (2002) Causality between income and emission: a country group-specific econometric analysis. Ecol Econ 40(3):351–367. https://doi.org/10.1016/S0921-8009(01)00280-4

Destek MA, Sarkodie SA (2019) Investigation of environmental Kuznets curve for ecological footprint: the role of energy and financial development. Sci Total Environ 650:2483–2489. https://doi.org/10.1016/j.scitotenv.2018.10.017

Dinda S (2004) Environmental Kuznets curve hypothesis: a survey. Ecol Econ 49(4):431–455. https://doi.org/10.1016/j.ecolecon.2004.02.011

Dumitrescu EI, Hurlin C (2012) Testing for granger non-causality in heterogeneous panels. Econ Model 29(4):1450–1460. https://doi.org/10.1016/j.econmod.2012.02.014

Gill AR, Viswanathan KK, Hassan S (2018) The environmental Kuznets curve (EKC) and the environmental problem of the day. Renew Sustain Energy Rev 81:1636–1642. https://doi.org/10.1016/j.rser.2017.05.247

Grossman GM, Krueger AB (1991) Environmental impacts of a north American free trade agreement (no. w3914). National Bureau of Economic Research

Grossman GM, Krueger AB (1995) Economic growth and the environment. Quart J Econ 110(2):353–377

He J, Richard P (2010) Environmental Kuznets curve for CO2 in Canada. Ecol Econ 69(5):1083–1093. https://doi.org/10.1016/j.ecolecon.2009.11.030

Iwata H, Okada K, Samreth S (2010) Empirical study on the environmental Kuznets curve for CO2 in France: the role of nuclear energy. Energy Policy 38(8):4057–4063. https://doi.org/10.1016/j.enpol.2010.03.031

Jebli MB, Youssef SB, Ozturk I (2016) Testing environmental Kuznets curve hypothesis: the role of renewable and non-renewable energy consumption and trade in OECD countries. Ecol Indic 60:824–831. https://doi.org/10.1016/j.ecolind.2015.08.031

Kaufmann RK, Davidsdottir B, Garnham S, Pauly P (1998) The determinants of atmospheric SO2 concentrations: reconsidering the environmental Kuznets curve. Ecol Econ 25(2):209–220. https://doi.org/10.1016/S0921-8009(97)00181-X

Kivyiro P, Arminen H (2014) Carbon dioxide emissions, energy consumption, economic growth, and foreign direct investment: causality analysis for sub-Saharan Africa. Energy 74:595–606. https://doi.org/10.1016/j.energy.2014.07.025

Kónya L (2006) Exports and growth: granger causality analysis on OECD countries with a panel data approach. Econ Model 23(6):978–992. https://doi.org/10.1016/j.econmod.2006.04.008

Liddle B, Messinis G (2018) Revisiting carbon Kuznets curves with endogenous breaks modeling: evidence of decoupling and saturation (but few inverted-us) for individual OECD countries. Empir Econ 54(2):783–798. https://doi.org/10.1007/s00181-016-1209-y

Magazzino C (2016) The relationship between CO2 emissions, energy consumption and economic growth in Italy. Int J Sustain Energy 35(9):844–857. https://doi.org/10.1080/14786451.2014.953160

Musolesi A, Mazzanti M, Zoboli R (2010) A panel data heterogeneous Bayesian estimation of environmental Kuznets curves for CO2 emissions. Appl Econ 42(18):2275–2287. https://doi.org/10.1080/00036840701858034

Ozcan B, Apergis N, Shahbaz M (2018) A revisit of the environmental Kuznets curve hypothesis for Turkey: new evidence from bootstrap rolling window causality. Environ Sci Pollut Res 25(32):32381–32394. https://doi.org/10.1007/s11356-018-3165-x

Panayotou T (1993) Empirical tests and policy analysis of environmental degradation at different stages of economic development (no. 992927783402676). International Labour Organization

Pesaran MH (2004) General diagnostic tests for cross section dependence in panels. University of Cambridge, Faculty of Economics, Cambridge Working Papers in Economics No. 0435

Pesaran MH, Ullah A, Yamagata T (2008) A bias-adjusted LM test of error cross-section independence. Econ J 11(1):105–127. https://doi.org/10.1111/j.1368-423X.2007.00227.x

Rafindadi AA (2016) Revisiting the concept of environmental Kuznets curve in period of energy disaster and deteriorating income: empirical evidence from Japan. Energy Policy 94:274–284. https://doi.org/10.1016/j.enpol.2016.03.040

Rees WE (1992) Ecological footprints and appropriated carrying capacity: what urban economics leaves out. Environ Urban 4(2):121–130. https://doi.org/10.1177/095624789200400212

Richmond AK, Kaufmann RK (2006) Is there a turning point in the relationship between income and energy use and/or carbon emissions? Ecol Econ 56(2):176–189. https://doi.org/10.1016/j.ecolecon.2005.01.011

Sarkodie SA, Strezov V (2019) A review on environmental Kuznets curve hypothesis using bibliometric and meta-analysis. Sci Total Environ 649:128–145. https://doi.org/10.1016/j.scitotenv.2018.08.276

Shafik N, Bandyopadhyay S (1992) Economic growth and environmental quality: time-series and cross-country evidence (Vol. 904). World Bank Publications

Shahbaz M, Mahalik MK, Shah SH, Sato JR (2016) Time-varying analysis of CO2 emissions, energy consumption, and economic growth nexus: statistical experience in next 11 countries. Energy Policy 98:33–48. https://doi.org/10.1016/j.enpol.2016.08.011

Shahbaz M, Shafiullah M, Papavassiliou VG, Hammoudeh S (2017) The CO2–growth nexus revisited: a nonparametric analysis for the G7 economies over nearly two centuries. Energy Econ 65:183–193. https://doi.org/10.1016/j.eneco.2017.05.007

Song, T., Zheng, T., and Lianjun, T. 2008. An empirical test of the environmental Kuznets curve in China: a panel cointegration approach. China Economic Review, 19(3), 381-392. https://doi.org/10.1016/j.chieco.2007.10.001

Tang CF (2008) A re-examination of the role of FDI and exports in Malaysia’s economic growth: a time series analysis, 1970-2006. Int J Manag Stud 15:47–67

Tiwari AK, Shahbaz M, Hye QMA (2013) The environmental Kuznets curve and the role of coal consumption in India: cointegration and causality analysis in an open economy. Renew Sustain Energy Rev 18:519–527. https://doi.org/10.1016/j.rser.2012.10.031

Tzeremes P (2018) Time-varying causality between energy consumption, CO2 emissions, and economic growth: evidence from US states. Environ Sci Pollut Res 25(6):6044–6060. https://doi.org/10.1007/s11356-017-0979-x

Van den Bosch M (2016) UNEP/UNECE GEO-6 assessment for the pan-European region

Wackernagel M, Rees W (1996) Our ecological footprint: reducing human impact on the earth. New Society Publishers, The New Catalyst Bioregional Series

Zellner A (1962) An efficient method of estimating seemingly unrelated regressions and tests for aggregation bias. J Am Stat Assoc 57(298):348–368

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Philippe Garrigues

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Yilanci, V., Ozgur, O. Testing the environmental Kuznets curve for G7 countries: evidence from a bootstrap panel causality test in rolling windows. Environ Sci Pollut Res 26, 24795–24805 (2019). https://doi.org/10.1007/s11356-019-05745-3

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-019-05745-3