Abstract

This work systematically examines the empirical interactions among foreign direct investment (FDI), renewable power generation (RPG), hydropower generation (HPG), non-hydropower generation (NHPG), and CO2 emissions in the long run and short run. To test the existence of long-run equilibrium association among those variables, Bayer-Hanck combined cointegration and autoregressive distributed lag (ARDL) model have been employed on time series of China for the period 1991–2017. The vector error correction model-based short-run impacts among the variables of interest are also estimated. Besides, Toda-Yamamoto causality and Granger causality are employed to confirm the direction of causal links. The existence of a long-run equilibrium relationship is revealed in case of all types of specification. The expansion of both FDI and CO2 emissions boosted RPG, HPG, and NHPG in the short run and long run, with greater intensity of impacts in the long run. To reflect comparisons, it is found that the renewables generation driving the impact of CO2 emissions and FDI on NHPG is greater than RPG, which further exceeds HPG. In turn, the RPG, HPG, and NHPG mitigated CO2 emissions both in the long run and short run, with stronger impacts in the long run. Moreover, the CO2 emissions inhibition impact of HPG dominated NHPG, which further exceeded that of RPG. The FDI boosted CO2 emissions in a way that the long-run pollution haven impact is revealed to be powerful than that of the short run. A unidirectional causality has been observed running from FDI to CO2 emissions, RPG, HPG, and NHPG. A bidirectional causality is found operative between CO2 emissions and RPG/HPG/NHPG. Interestingly, the long-run and short-run impacts remained homogeneous in terms of directionality. Nevertheless, strict heterogeneity is observed in terms of the degree of impacts. Based on empirics, both long-term and short-term policies on FDI, renewables generation, and CO2 emissions are vital for decision-makers in China.

Graphical abstract

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

In the current era of globalization and internationalization of investment markets, the trend of foreign investments has received worldwide prominence in terms of its spillover effects for the host nations. Those spillover effects may include positive as well as negative spillovers. Among positive spillovers, technology diffusion, pollution halo impact, human capital transmission, and rise in aggregate production of host nation exhibited prominence (Ferrier et al. 2016). However, a negative spillover effect of pollution havens has also been argued to be existent. The pollution havens states that poorly developed nations attract dirty and less efficient industries due to weakly stringent environmental regulations, which ends up with environmental deterioration (Sung et al. 2018). It is also opined that the foreign direct investment (FDI) increases the aggregate production that aggravates the energy demand in the host nation. In the same vein, massive non-renewable energy consumption brings about environmental threats and hence gives birth to human health hazards, thus indicating the negative spillover outcome (Zhou et al. 2018). Additionally, in order to cope with high energy demand and environmental problems in the host nation, FDI promotes renewable energy development through technology and knowledge diffusion and hence denoting the positive spillover outcome (Bekun et al. 2019). The Heckscher-Ohlin model, which builds on the theory of comparative advantage, the capital flows from a country with low capital returns to high capital returns (Buckley and Casson 2016).

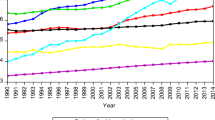

Since China became the fastest growing country in renewables, its promotion of renewable power generation is linked with the motive of meeting massive energy demand along with emissions mitigation in the country. As to China, its FDI expanded from 22.5 million USD in 1991 to 103.9 million USD in 2017 (World Bank 2017). Meanwhile, the renewable power generation from different sources of renewables grew at a different pace (Fig. 1). Among those renewable power generation sources, hydropower remained the major contributor, while geothermal power, recently, remained the least contributor to renewable power generation in China. In this regard, with motivation to curtail global CO2 emissions, the FDI contributed to renewable power generation, including wind power, hydropower, solar power, biomass, and geothermal power. It is noted that during 2004 to 2010, North America (USA and Canada), Europe (Germany, Spain, Italy, and Denmark), and Asia (China and Japan) remained among the largest FDI investors as well as FDI destinations in renewable energy. As to China, it invested in renewable power more than the whole of Europe until 2010 and emerged as a most wanted destination for FDI in renewable power generation (REN21 2018; UNCTAD 2018). From the theoretical jurisdiction and empirical work, the energy scientists and researchers around the globe strive to establish that FDI has been an integral part of renewable energy development as it works as a driving force of renewable power generation and its consumption. In this regard, on one hand, FDI can be considered as the potential driver to have an association with renewable power generation. Nevertheless, on the other hand, the flux of FDI inflows boosted the CO2 emissions in countries with weakly stringent environmental protection policies including China (Lee 2013). Concerning this, Fig. 2 sheds light on the development trends of CO2 emissions along with FDI, RPG, HPG, and NHPG in China during 1991–2017. The CO2 emissions in China, surged from 2457.3 in 1991 to 9232.6 Mt in 2017 indicating a significant contribution to air pollution domestically as well as internationally (BP Statistical Review on World Energy 2018).

Profile of renewable power generation in China from various sources for period 1991–2017. Data source: BP Statistical Review on World Energy (2018)

In order to craft the impacts among FDI, renewable energy, and CO2 emissions, the existing literature can be listed under following core headings: (i) impact analysis between FDI and renewable energy consumption (e.g., Khandker et al. 2018; Chen 2018; Pata 2018), (ii) impact analysis between FDI and CO2 emissions (e.g., Peng et al. 2016; Zhu et al. 2018; Kocak and Sarkgunesi 2018), and (iii) links between renewable energy consumption and CO2 emissions (e.g., Sbia et al. 2014; Mert and Boluk 2016; Baek 2016; Wang et al. 2017; Shahbaz et al. 2018). Those studies considered the mentioned linkages between FDI, renewable energy consumption, and CO2 emissions on a piecemeal basis without considering comprehensive interactions among the three. The literature under first heading took the impact analysis between FDI and renewable energy consumption into consideration. Concerning this, Doytch and Narayan (2016) examined the association between FDI and energy demand by disaggregating the FDI into manufacturing, mining, financial service, and total services. For this purpose, they estimated the long-run elasticities using the generalized method of moments (GMM) on 74 countries for the time span 1985–2012. They found varied impacts of FDI on renewable and non-renewable energy consumption, that FDI added to renewable energy consumption and reduced the non-renewable energy consumption. Similarly, Sbia et al. (2014) explored the connections among FDI, green energy, trade, and economic growth in UAE and confirmed the existence of a cointegrating relationship among those variables. Furthermore, there is a declining impact of FDI and trade on energy demand, whereas economic growth and clean energy have expansion impact on energy demand. Also, Lee (2013) studied the cointegrating association between FDI, clean energy, economic growth and carbon emissions for 19 countries from G20. FDI has been found to have a positive impact on economic growth, whereas its effect remained limited in case of carbon emissions. However, the research found no association of FDI with clean energy in the UAE. Nonetheless, those studies rarely discussed the long- and short-run impacts of FDI on renewable power generation.

Moreover, studies under the second heading conducted impact analysis between FDI and CO2 emissions. Among others, Sung et al. (2018) conducted a panel data study covering 28 sub-sectors of the Chinese manufacturing sector to investigate the impact of FDI on carbon emissions. For this, they applied the GMM method and found a positive impact of FDI on carbon emissions thus supporting the halo effect in the Chinese manufacturing sector. Then, Koçak and Şarkgüneşi (2018), based on data of the Turkish economy, evaluated the potential influence of FDI on CO2 emissions using the environmental Kuznets curve hypothesis. Their findings exposed the existence of a long-run balanced association among FDI, CO2 emissions, energy consumption, and economic growth. Likewise, they found the pollution haven hypothesis to be valid in the case of Turkey. Additionally, Omri et al. (2014) conducted simultaneous equation analysis for a panel of 54 countries covering the period from 1990 to 2011 on FDI, carbon emissions, and economic growth and found a bidirectional causal connection between FDI and economic growth. They further found unidirectional causal relationship from carbon emissions to economic growth.

Lastly, the researches under the third heading investigated the relationship between renewable energy consumption and CO2 emissions; however, none of those researches has been known to conduct this analysis for long-run and short-run empirical grounds. In this regard, Chen (2018) tested the links among trade, economic growth, carbon emissions, and renewable energy for Chinese panel based on 30 provinces and found a positive influence of economic growth and CO2 emissions on renewable energy consumption. Besides, imports and exports were found to have negative and positive impacts, respectively, on renewable energy consumption. Furthermore, Omri and Nguyen (2014) analyzed a panel of 64 countries around the globe for renewable energy, trade, population, and economic growth by employing GMM panel estimation. They found carbon emissions and trade as the main drivers of renewable energy consumption. Table 1 provides with the summary of selected studies reporting causal linkages among FDI, renewable energy and CO2 emissions.

Having a bird’s eye view of existing literature, a number of researches explored the links between FDI and renewable energy consumption, and FDI and CO2 emissions involving a variety of empirical findings. Despite the plethora of researches conducted in this domain, the current work is distinguished from the existing body of knowledge in several significant directions. First, unlike previous researches, this work explores the linkages among FDI, CO2 emissions, and various types of renewable power generation in the long run and short run (e.g., Dogan and Seker 2016; Bilgili et al. 2016; Danish et al. 2017; Dong et al. 2018; Inglesi-Lotz and Dogan 2018). Second, no single attempt has been known to investigate the interaction among hydropower and non-hydropower generation, FDI, and CO2 emissions in Stochastic Impacts by Regression on Population, Affluence, and Technology (STIRPAT) framework (e.g., Irandoust 2016; Mert and Boluk 2016; Ummalla and Samal 2018). Third, distinct from previous studies, this work establishes a comprehensive correlation analysis among FDI, CO2 emissions, and variety of renewables generation (e.g., Sbia et al. 2014; Peng et al. 2016; Khandker et al. 2018). Fourth, different from existing literature, this work modifies the STIRPAT to introduce FDI and RPG into the theoretical framework (e.g., Dogan and Ozturk 2017; Dong et al. 2018; Zhou et al. 2018). Fifth, unlike existing studies, this work reveals the heterogeneous nature of pollution haven impact across the long run and short run. Consequently, it seems a vital concern to reveal the long-run and short-run empirical interactions among FDI, aggregated as well as disaggregated measures of renewable power generation, and CO2 emissions.

The underlying objective of the current work is to systematically inspect the long-run and short-run linkages among FDI, renewable power generation, and CO2 emissions for Chinese time series from 1991 to 2017. In technical terms, this work attempts to contribute to the new pool of knowledge in following key aspects. First, the Stochastic Influence by Regressions on Population, Affluence, and Technology (STIRPAT) model has been modified to introduce FDI as a function of technology component, whereas RPG has been incorporated as a function of CO2 emissions. Second, the renewable power generation (RPG) has been considered in aggregated and disaggregated forms classified into hydropower generation and non-hydropower generation to have a comparative impact analysis. Third, for establishing correlation analysis, Pearson, Spearman, and Kendall’s correlation tests are employed. Fourth, in order to inspect the long-run equilibrium associations, the Bayer-Hanck combined cointegration and autoregressive distributed lag (ARDL) bounds testing methods have been employed. Further, the vector error correction model (VECM) has been applied to examine the short-run dynamics. Additionally, the Toda-Yamamoto causality and Granger causality tests are employed to identify the directions of linkages among the variables of interest. Moreover, vector autoregressive (VAR) model-based generalized impulse response functions (IRFs) are generated to predict the responses of FDI, RPG, and CO2 emissions. This work has provided with long-run and short-run based useful policy insights for China combined with policy lessons for the rest of the world economies.

The remaining work is structured as follows. “Data, methods, and empirics” section details the data description, methods, and empirics. It reports the pre-analysis and main methods of the work. Moreover, it documents the STIRPAT theoretical framework. Finally, “Preliminary methods and results” section comprises of conclusions and policy implications of this work.

Data, methods, and empirics

Data description

This work has made use of the annual frequency-based time series data on FDI (current USD), renewable power generation (RPG) (TwhFootnote 1) from different sources, carbon dioxide emissions (MtFootnote 2), and consumer price index (CPI) (preceding year = 100) inflation covering the time from 1991 to 2017. The data on FDI (current USD), gross domestic product (GDP) (current USD), and CO2 emissions (Mt) are sourced from World Bank (2017). The FDI and GDP in current USD form have been corrected for CPI inflation. The data on CPI are collected from China Statistical Yearbook (2016, 2017). Finally, the data on renewable power generation from different sources, including hydropower (Twh), wind power (Twh), solar power (Twh), geothermal power (Twh), and other renewable sources (Twh), are compiled from BP Statistical Review on World Energy (2018). For estimation purpose, the aggregate variable of RPG is calculated by summation of all renewable power generation sources given as:

where “i” is the index of renewable power generation sources, RS indicates the individual renewable power generation source, and RPG indicates the aggregate variable of renewable power generation. The renewable power generation sources constructing the variable of renewable power generation include hydropower, wind power, solar power, geothermal power, and other renewables. Furthermore, for comparative analysis, the renewable power generation has been further classified into hydropower generation (HPG) and non-hydropower generation (NHPG). The NHPG comprises of the individual renewable power generation sources excluding HPG. In other words, the RPG minus HPG constructs the NHPG. Additionally, as shown in Fig. 3, all the six data series have been subjected to natural logarithmic transformation for estimations purpose, so as to release them from measurement units thus making the interpretations parsimonious and logical.

Natural logarithmic transformed time series plots

Preliminary methods and results

Correlation analysis

As a primary step, the coefficient of the standard Pearson rank correlation test has been employed. Also, Kendall’s (1938) non-parametric test and Spearman’s rank correlation test are considered for robustness of correlation findings. The correlation coefficients based on those correlation tests are recorded in Table 2.

Moreover, the bivariate association among FDI, RPG, HPG, NHPG, and CO2, are demonstrated through scatter plots and the fitted log-linear functions within scatter plots (Fig. 4). For each pair of variables (Fig. 4 a–g), the scatter plots exposed monotonicFootnote 3 relationships and the high value of coefficients of determination revealed the best fit of the log-linear functions. Though all the pairs of variables displayed monotonic positive associations, nonetheless some pairs demonstrated relatively flatter slopes of log-linear functions (Fig. 4 a, b, d, and g) whereas some showed relatively steeper slopes (Fig. 4 c, e, and f). It implies that CO2 is slightly responsive to relatively big changes in RPG and NHPG, whereas it is relatively more responsive to moderate changes in FDI and HPG. Moreover, RPG and HPG exposed relatively small changes in response to relatively big changes in FDI.

Scatter plot-based bivariate logarithmic associations among FDI, RPG, HPG, NHPG, and CO2 emissions in China from 1991 to 2017

Unit root analysis

The unit root testing is considered to meet the pre-condition to test the linkages among time series. For this purpose, this work has employed Augmented Dicky-Fuller Generalized Least Squares (ADF-GLS) test by Elliott et al. (1992) which is modified form of the Augmented Dicky-Fuller (ADF) test (1979). The ADF-GLS test executes estimations taking the asymptotic point optimality into consideration, hence it is considered to have statistical power more than ADF test.

As an empirical counterpart, Phillips-Perron (PP) (1988), and Kwiatkowski Phillips Schmidt and Shin (KPSS) (1992) tests have been employed for the robustness details. Based on the non-parametric property to correct t-statistic, PP test is robust to heteroscedasticity in the random process and autocorrelation problem (Davidson and MacKinnon 2004). Finally, the KPSS test considers testing the null hypothesis whether a time series is trend stationary against the alternative hypothesis of non-stationary series. According to trend stationary process, the series face transitory shocks which are mean reverting and hence keeping the process of the series convergent.

The application of a variety of unit root tests with slightly distinguished statistical properties has significantly enhanced the statistical reliability of the unit root analysis. The statistical outcomes of those tests at the level as well as the first difference are reported in Tables 3 and 4, respectively. The results in Table 3 illustrate that FDI, RPG, HPG, and NHPG are stationary in level form. However, CO2 emissions and GDP have unit root at level but turned stationary in first difference form i.e., integrated of order one. It is demonstrated through the rejection of null hypothesis of ADF-GLS stating that series follows a random walk. It is further exhibited through the rejection of the null hypothesis of PP test which states that series has a unit root. It is further validated by the retention of the null hypothesis of “stationary” in the KPSS test in Table 4. Furthermore, the technical roadmap of the empirical methods is recorded in Fig. 5.

Technical roadmap of empirical methods. Notes: STIRPAT, Stochastic Impacts by Regression on Population, Affluence, and Technology; BGLM, Breusch-Pagan Lagrange Multiplier; RESET, Regression Equation Specification Error; JB, Jarque-Bera; CUSUM, cumulative sum of recursive residuals; CB, Chow breakpoint; CF, Chow forecast

STIRPAT theoretical framework

The formulation of “Stochastic Impacts by Regression on Population, Affluence, and Technology” (STIRPAT) augmented by Dietz and Rosa (1994, 1997) integrated the stochastic component to acquire the environmental impacts through the following model:

where I establishes the environmental impacts (revealed by CO2 emissions), P symbolizes the population size, A means affluence i.e., gross domestic product (GDP), T denotes technology, and e signifies the stochastic measure. The post-transformation form of Eq. (2) after the logarithmic application is given as:

where “ln” means natural logarithm, while “t” in the subscript means the index of time.

Modified STIRPAT

This work transforms the STIRPAT in two new dimensions. First, it has been opined that CO2 emissions is a function of energy (Yazdi and Shakouri 2017; Ahmad et al. 2019a), thus the renewable power generation (RPG) can also be incorporated in the model. Second, the foreign direct investment (FDI) brings about advancement in terms of technology and hence transforms the structural skeleton of the host economy. Thus, FDI can be introduced as a function of the technology component in Eq. (3):

where “ν” denotes the random component of the model.

Main methods and results

Based on unit root analysis, the series of CO2 emissions and GDP are found to be integrated of order one thus ruling out the application of ordinary least squares (OLS) method. Further, it is found that not all the time series data are integrated of the same order, thus excluding the option of employing Johnson co-integration method. Since the variables of interest contained integration orders of mixed types, i.e., I(0) and I(1) and none of the series is I(2), the current scenario holds the application of Bayer-Hanck combined cointegration and ARDL bounds testing to be suitable.

Bayer-Hanck combined cointegration

For the inspection of long-run equilibrium association among RPG, HPG, NHPG, FDI, and CO2, a recently developed test of combined cointegration by Bayer and Hanck (2013) has been employed. For this purpose, Bayer and Hanck (2013) combined the non-cointegration tests to provide with consistent and more reliable findings. This test produces robust and more efficient results. The most parsimonious version of cointegration was devised by long-run regression-based Engle and Grager (1987) cointegration which is established on estimated residuals. Later, several different cointegration tests were proposed. In this regard, system-based Johansen (1988) test, F-statistics-based Boswijk (1994) test, and t-statistics-based Banerjee et al. (1998) test remained prominent. It has been opined that none of the cointegration tests may provide perfect outcomes in all situations due to having distinguishing characteristics (Elliott et al. 1992). For this reason, a combined cointegration (Bayer and Hanck 2013) of improved power has been employed to yield robust cointegration findings. This procedure, using Fisher (1932) formula, combines the p values of different cointegration tests to provide results having a concrete basis. The expressions following Bayer and Hanck (2013) are given as follows:

where E&G indicates Engle and Grager (1987), JN indicates Johansen (1988), BK indicates Boswijk (1994), and BJ indicates Banerjee et al. (1998) cointegration, whereas PE&G, PJN, PBK, and PBJ denote their respective p values. According to the decision rule, if computed Fisher statistics ˃ Bayer and Hanck (2013) critical values, the null hypothesis (H0) of no cointegration can be rejected. The results based on Bayer and Hanck (2013) are recorded in Table 5.

The results in Table 5 indicate that the calculated Fisher statistics for E&G-JN and E&G-JN-BK-BJ tests exceed the Bayer and Hanck (2013) critical values at both 5% and 10% levels of significance for all the three types of specifications (i.e., type-R, type-H, type-N). It leads to the rejection of the null hypothesis of no-cointegration, hence leading to confirmation of the existence of long-run equilibrium association among FDI, CO2 emissions, and RPG/HPG/NPG in all types of specifications.

Bounds test-based cointegration

As an empirical counterpart and robustness details, Pesaran et al.’s (2001) ARDL has been employed to empirically examine the long-run and short-run links among FDI, CO2 emissions, and RPG/HPG/NHPG. For this, ARDL is utilized as a general vector autoregressive model having pth order, represented by column vectors Y(R)t = [FDIt, RPGt, CO2t ]T, Y(H)t = [FDIt, HPGt, CO2t ]T, and Y(N)t = [FDIt, NHPGt, CO2t ]T for type-R, type-H, and type-N specifications, respectively. The ARDL is advantageous over other testing methods in terms of its application to the series with mixed order of integration. Moreover, even for small samples, ARDL yields more efficient and unbiased estimates than conventional methods. To determine the cointegrating association, this work estimates the following ARDL model:

where ∆Yt is a column vector with a 3 × 1 dimension. Likewise, λi, j and νi, j are the column vectors of intercept coefficients and residuals, respectively. The ARDL model term with η’s and φ’s nominate the long-run part and short-run dynamics, respectively. Additionally, λ’s and ν’s indicate the intercepts and white noise errors of the models, respectively. The null hypotheses of the long-run cointegrating equilibrium association denoted as η1j = η2j = η3j = 0 are tested against the alternative hypotheses provided as η1j ≠ η2j ≠ η3j ≠ 0 by making use of Pesaran et al.’s (2001) critical bound test statistic. The assumption for the critical lower bound statistic is that all the three variables in the ARDL model are I(0) while, the assumption based on which the critical upper bound statistic has been formed is that all the three variables are I(1).

According to the decision principle, if F-statistic ˃ upper bound critical value then the null hypothesis of no co-integration should be rejected. On the contrary, the null hypothesis is retained if F-statistic ˂ lower bound critical value. Otherwise, if none of the two holds true then the test is considered inconclusive. The F-statistic values acquired from the Wald test and the bounds statistic (at 5% significance level) provided by Pesaran et al. (2001), and the calculated F-statistic values of ARDL regressions are documented in Table 6. The optimum lag length is selected based on AIC and SBC.

The bounds test results revealed that all the four equations are cointegrated for type-R specification. This is demonstrated from the F-statistic (test values) ˃ the upper bound tabulated values at 5% (3.91). Hence, it leads to rejection of the null hypothesis of no cointegration providing evidence that series of FDI, RPG, CO2 emissions, and GDP are cointegrated. However, in the case of type-H and type-N specifications, except equation for GDP, all the equations are cointegrated. Thus, it validates the robustness of cointegration results found by application of Bayer-Hanck cointegration test. Thus, the cointegration results confirmed the existence of a long-run equilibrium association among FDI, RPG, HPG, NHPG, and CO2 emissions.

Conditional ARDL model-based long-run elasticities

As the cointegration is proved, the conditional ARDL model specifications are estimated in the next step as given in the matrix form equation:

where AIC and SBC have been used to determine the ARDL optimal order for all the five variables reported in the matrix of specifications in Eq. (8). Those specifications are estimated making use of the ARDL. The empirical findings of the estimated models which are normalized for the RPG, HPG, NHPG, FDI, and CO2 emissions, respectively, are documented in Table 7.

Long-run impacts of renewable energy models

As far as the long-run elasticities are concerned, in all the three types of specifications (type-R, type-H, type-N), FDI, CO2 emissions, and GDP exerted a significant positive impact on RPG, HP, and NHPG, respectively. However, the degree of impact remained heterogeneous in three types of specifications. The FDI imparted the strongest impact on NHPG, medium impact on RPG, while demonstrated the weakest impact on HPG. In this regard, a 1% rise in FDI is likely to boost NHPG, RPG, and HPG by 0.95, 0.83, and 0.43%, respectively. The CO2 emissions also induced the strongest impact on NHPG, medium impact on RPG, while demonstrated weakest impact on HPG. Concerning this, a 1% rise in CO2 emissions is likely to boost NHPG, RPG, and HPG by 0.22, 0.16, and 0.15%, respectively. However, the impact of GDP on RPG, HPG, and NHPG varied from strongest to medium to relatively weak for the three specifications, respectively. The results entailed that both CO2 emissions and FDI promoted “RPG/HPG/NHPG driving impact.” These results are reported in Table 7.

Long-run impacts of FDI model

In case of all the three types of specifications, CO2 demonstrated an insignificant contribution to FDI implying that FDI remained neutral to changes in CO2 emissions. Furthermore, RPG in type-R specification, HPG in type-H specification, and NHPG in type-N specification exerted an insignificant impact on FDI. However, GDP displayed positive contribution to FDI in all the three type of specifications. In this regard, the degree of impact of GDP on FDI varied from strongest to medium to weakest in case of type-N, type-H, and type-R specifications, respectively. A 1% surge in GDP is expected to increase FDI by 0.23, 0.19, and 0.17% in the case of type-N, type-H, and type-R, respectively. These results are documented in Table 7.

Long-run impacts of CO2 emissions model

In all the three specifications, FDI induced significant positive contribution to CO2 emissions whereas RPG, HPG, NHPG, and GDP induced significant negative contribution to it. The impact of FDI remained diversified with the strongest impact in case of type-N specification, medium impact in case of type-R specification, and weakest impact in case of type-H specification. In this regard, a 1% increase in FDI is likely to raise CO2 emissions by 0.88, 0.59, and 0.38% for type-N, type-R, and type-H specifications, respectively. Thus, FDI promoted the “CO2 emissions injection impact” which is also known as “pollution haven impact.” Similarly, considering the impact of renewables, NHPG demonstrated the strongest impact on CO2 emissions. Next to NHPG, RPG showed the medium impact on CO2 emissions, whereas HPG revealed the weakest impact on it. In this regard, a 1% rise in NHPG, RPG, and HPG is likely to reduce the CO2 emissions by 0.56, 0.30, and 0.26%, respectively. In this way, RPG, HPG, and NHPG imparted a negative long-run impact on CO2 emissions inducing “CO2 emissions inhibition impact.” Based on results, the “CO2 emissions injection impact” exceeds the “CO2 emissions inhibition impact,” hence leading to an overall rise in CO2 emissions. Finally, GDP demonstrated negative impact on CO2 emissions with strongest impact (0.71) in case of type-N specification, medium impact (0.61) in type-R specification, and weakest impact (0.58) in type-H specification. These results are provided in Table 7.

VECM-based dynamics of the models

After the verification of long-run equilibrium linkages among the variables of interest, it is interesting to analyze the causal links among RPG, HPG, NHPG, FDI, and CO2 emissions in order to have useful policy implications for those variables. The short-run dynamics of the long run is tested by making use of the F-statistic and the error correction terms (ECT) in the lag form documented in the following matrix expression:

where φ’s are the short-run elasticities which demonstrate the dynamics of convergence, after confronting some arbitrary shock, to attain the equilibrium level and σ’s are the parameters of the speed of adjustment to equilibrium levels in the long run. The specifications in matrix form Eq. (9) are estimated by employing OLS method and the estimated elasticities demonstrating short-run dynamics are documented in Table 8.

The coefficients of lagged ECT are revealed to have a significant negative parameter in case of all the three types of specifications and for all the models, hence confirming the convergence of short-run dynamics in the long run. The magnitudes of ECT parameters indicate the speed of convergence after an arbitrary shock in RPG, HPG, NHPG, FDI, CO2 emissions, and GDP. For high magnitudes of ECT as in case of RPG model (− 0.69), NHPG model (− 0.71), and CO2 model of type-N specification (− 0.65), the shock would dissipate slowly and hence impact would last relatively longer. The F-statistic of ARDL-based regressions indicates that the estimated models are globally significant (at 5%) and hence are the best fit. Additionally, the measure of R2 demonstrates that predictor variables of the VECM-based renewable energy models and CO2 emissions model explained sufficient variations in the predictand variables. Likewise, the Durbin Watson statistic for all the three model specifications uncovered the absence of autocorrelation in the sample.

Short-run impacts of renewable energy models

Considering short-run elasticities, in all the three types of specifications, FDI, CO2 emissions, and GDP imparted a significant positive impact on RPG, HP, and NHPG, respectively, with the heterogeneous intensity of impacts in three types of specifications. In this regard, the impact of FDI on NHPG, RPG, and HPG varied from strongest to medium to weakest, with impact elasticities 0.098, 0.091, and 0.063 for NHPG, RPG, and HPG, respectively. Similarly, the CO2 emissions exerted the strongest impact on NHPG (0.032), medium impact on RPG (0.024), while exhibited relatively weak impact on HPG (0.017). Whereas, short-run impact of GDP on RPG, HPG, and NHPG varied from relatively strong to medium to relatively weak impact for the three types of specifications, respectively. The results implied that both CO2 emissions and FDI promoted “RPG/HPG/NHPG driving impact” in the short run. These results have been reported in Table 8.

Short-run impacts of FDI model

For all the three types of specifications, FDI remained neutral to variation in CO2 emissions. Additionally, FDI also remained neutral to changes in RPG in type-R specification, HPG in type-H specification, and NHPG in type-N specification. Nevertheless, GDP exhibited positive contribution to FDI in all the three types of specifications. Concerning this, the intensity of the impact of GDP on FDI varied from relatively strong (0.019) to medium (0.010) to relatively weak (0.007) in case of type-N, type-H, and type-R specifications, respectively. These results have been detailed in Table 8.

Short-run impacts of CO2 emissions model

For all the three types of specifications, the FDI introduced significant positive short-run impact on CO2 emissions whereas RPG, HPG, NHPG, and GDP negatively contributed to it. The impact of FDI remained diversified with a relatively high degree of impact for type-N specification (0.084), medium degree of impact for type-R specification (0.073), and relatively weak degree of impact for type-H specification (0.058). Based on its intensity of impact, the “CO2 emissions injection impact” or “pollution haven impact” remained weaker in the short run than that of the long run. Taking the short-run impacts of renewables, NHPG exhibited relatively strong impact (− 0.056), RPG showed medium impact (− 0.045), whereas HPG revealed the relatively weak impact (− 0.031) on CO2 emissions. In this way, RPG, HPG, and NHPG exerted a negative short-run impact on CO2 emissions introducing “CO2 emissions inhibition impact.” Eventually, GDP imparted short-run negative impact on CO2 emissions. These results have been documented in Table 8.

VAR-based impulse response analysis

For further testing of the interlinkages among the variables in a multivariate framework, the VAR model is employed. The VAR models are primarily evolved from the univariate autoregressive processes to involve the multiple time series variables. According to Wang et al. (2016), the VAR models establish linear functions of “k” (where k = 5) variables for only past values of those variables. A 3rd order VAR model is given as follows:

where the left-hand side of Eq. (10) shows the column vector of exogenous variables, whereas the right-hand side indicates the column vectors of parameters, endogenous (lagged) variables, and white noise error terms. The impulse response functions (IRFs) in Figs. 6 a–c elaborate the reactions of variables (RPG, HPG, NHPG, FDI, and CO2) as a function of the time in response to some external one standard deviation (SD) shock to those variables, thus exposing the dynamicity of the VAR modeling framework. The impulse responses are generated for optimal lag length (lags = 6) selected by AIC and SBIC.

a VAR model-based impulse response functions of FDI, RPG, and CO2. The upper and lower dotted lines in each of the nine graphs denote the 95% confidence interval. b VAR model-based impulse response functions of FDI, HPG, and CO2. c VAR model-based impulse response functions of FDI, NHPG, and CO2

The IRFs indicated that some positive shocks in FDI lead to a slight decline in CO2 emissions during the first half of the time, whereas it raised the CO2 emissions in the later half period in case of models with RPG and HPG. However, in the case of a model with NHPG, CO2 emissions showed a declining trend and even in later periods, it did not boost. Next, shock in RPG and HPG in the first half of time raised the CO2 emissions, and in later half they reduced it. Whereas, the CO2 emissions are slightly boosted in response to shock in NHPG which dissipates quickly. In response to positive shock in FDI, RPG deceases in the first quarter of time while it slightly increases in the remaining three-quarters of the time. Then, HPG increases gradually all along the time periods in response to positive shock in FDI. On the contrary, the NHPG meets slight reduction in response to positive shock in FDI, for all the time periods. Finally, a positive shock in CO2 emissions leads to a rapid boost in RPG, HPG, and NHPG during all the periods of time.

Granger and Toda-Yamamoto causality

The VAR-based Granger (1969) causality models are estimated to identify the directions of relationships in the bivariate framework. The models to be estimated for this testing process are given as follows:

where i = 1, 2,…,l and j = 1, 2,…m. The null hypothesis (H0) given as δi = δj = 0 has been tested against the alternative hypothesis (H1) given as δi ≠ δj ≠ 0. Based on estimations of these models, the F-statistic values on regressors declared that bidirectional Granger causality is operative between RPG and CO2 emissions, HPG and CO2 emissions, and NHPG and CO2 emissions. On the other hand, FDI Granger causes RPG, HPG, NHPG, and CO2 emissions. The FDI is Granger caused by none of the variables. These results are reported in Table 9.

Moreover, a more advanced procedure robust to integration and cointegration was proposed by Toda and Yamamoto (1995) which estimates the augmented VAR yet keeping the simple formation of the estimation procedures. The Toda-Yamamoto causality allows the asymptotic distribution-based Wald test statistic. Hence, the causality results based on the Toda-Yamamoto causality test are reported in Table 10. The chi-square values and probability values indicate that there is unilateral causality running from FDI to RPG, HPG, NHPG, and CO2 emissions. Whereas, a bidirectional causality is operational between RPG and CO2 emissions, HPG, and CO2 emissions, and NHPG and CO2 emissions.

Empirical summary and discussion

Overall, in light of the empirics, the rise in FDI adds to RPG, HPG, and NHPG in the short run and in the long run; however, the long-run impacts are much stronger (9.1, 6.8, and 9.7 times for RPG, HPG, and NHPG, respectively) than short-run impacts. The similar result is reported by Khandker et al. (2018) for renewable energy consumption. Further, this result is consistent with that of Kahouli (2018) for electricity consumption and compatible with Gorus and Aydin (2019) for energy consumption. Considering the comparative intensities of impacts, it has been observed that the renewables generation driving impact of FDI on NHPG > RPG > HPG. The CO2 emissions also bring a boost in RGP, HPG, and NHPG both in the long run and short run, with more powerful impacts (6.9, 8.9, and 6.8 times for RPG, HPG, and NHPG, respectively) in the long run than those revealed in the short run. Further, the renewables generation driving impact of CO2 emissions on NHPG > RPG > HPG. In turn, the RPG, HPG, and NHPG mitigated CO2 emissions both in the long run and short run, with significantly powerful impact in the long run (6.8, 8.5, and 10 times of short-run impact for RPG, HPG, and NHPG, respectively). Moreover, the CO2 emissions inhibition impact of HPG > NHPG > RPG. Based on the underlying mechanism, the negative feedback response of RPG, HPG, and NHPG to CO2 emissions is dominant since the rise in RPG, HPG, and NHPG directly contributes to curtailment in CO2 emissions and hence substituting renewables for fossil fuel energy use. However, any addition to RPG, HPG, and NHPG in response to the rise in CO2 emissions is based on policy response which may induce policymakers and government bodies to promote renewables so as to attain the CO2 emissions curtailment targets.

The FDI boosted CO2 emissions in the long run and short run; however, its long-run degree of impact remained 8.1 times stronger than that of the short run. It revealed that long-run CO2 emissions injection impact or pollution haven impact remained powerful than that of the short run. This finding is in accordance with the previous literature (e.g., Solarin et al. 2017; Shahbaz et al. 2018; Zhou et al. 2018). The similar results are found by Hanif et al. (2019) for fossil fuel energy and FDI in Asian economies. A unidirectional causality has been observed running from FDI to CO2 emissions, RPG, HPG, and NHPG. A bidirectional causality is found operative between CO2 emissions and RPG/HPG/NHPG. In view of empirical findings, it is noted that long-run and short-run impacts remained homogeneous in terms of directionality of those linkages; nevertheless, strict heterogeneity has been observed in terms of degree of impacts. On the whole, the long-run impacts are found stronger than short-run impacts. The summary of long-run and short-run impacts for the three types of specifications (with RPG, HPG, and NHPG, respectively) is documented in Figs. 7 a, b, and c, respectively.

a Long-run and short-run impacts among RPG, FDI, and CO2. RPG, renewable power generation; FDI, foreign direct investment; CO2, carbon dioxide emissions. b Long-run and short-run impacts among HPG, FDI, and CO2. HPG, hydropower generation; FDI, foreign direct investment; CO2, carbon dioxide emissions. c Long-run and short-run impacts among NHPG, FDI, and CO2. NHPG, non-hydropower generation; FDI, foreign direct investment; CO2, carbon dioxide emissions

Post-estimation test results

The estimated models passed the post-estimation tests documented in Table 11. Furthermore, the stability of long-run elasticities is confirmed by analyzing the dynamics of the long-run. The CUSUMFootnote 4 and CUSUM-square tests are executed to analyze the parameters’ stability found through specifications in matrix Eq. (9) having the ECT. For all the three types of specifications, Figs. 8a, b, and c, respectively plotted the CUSUM and CUSUM-square plots. It is depicted that the plotted lines are retained within the critical domain (at 5%) in case of both CUSUM and CUSUM-square, for all the variables of interest, and hence confirmed the structural stability of the ARDL models.

a CUSUM and CUSUM-square test results (Model with RPG). The left panel shows results of CUSUM test, while the right panel shows results of CUSUM-square test for renewable power generation (RPG), foreign direct investment (FDI), and carbon dioxide emissions (CO2). b CUSUM and CUSUM-square test results (Model with HPG). The left panel shows results of CUSUM test, while the right panel shows results of CUSUM-square test for hydropower generation (HPG), foreign direct investment (FDI), and carbon dioxide emissions (CO2). c CUSUM and CUSUM-square test results (Model with NHPG). The left panel shows results of CUSUM test, while the right panel shows results of CUSUM-square test for non-hydropower generation (NHPG), foreign direct investment (FDI), and carbon dioxide emissions (CO2)

During 2008–2009, financial instability and growth slowdown appeared in China because of the roaring wave of the global financial crisis (Ahmad et al. 2019b). Though Chinese FDI inflows in the same period, it did not fall much as compared to the rapid decline in the FDI worldwide. In order to examine the presence of any significant structural break in 2008 and the periods afterward (2008 to 2017), the Chow breakpoint and Chow forecast tests are employed. Based on LLRFootnote 5 and F-stat values, the existence of structural break is not confirmed. These results are documented in Table 12.

Conclusions and policy implications

Unlike previous works, this work has examined the empirical interactions among FDI, CO2 emissions, and various types of renewable power generation in the long run and short run. In this regard, this work investigated the interaction among hydropower and non-hydropower generation, FDI, and CO2 emissions in the STIRPAT modeling framework. A comprehensive correlation analysis has been conducted employing a variety of tests for robust statistical findings. For the purpose to examine the long-run and short-run interactions among the variables of interest, Bayer-Hanck combined cointegration and autoregressive distributed lags (ARDL) approach have been employed on time series data of China for the period 1991–2017. Furthermore, Toda-Yamamoto causality, as well as Granger causality within the vector error correction model (VECM), has been employed to examine the directions of the causal linkages.

The empirical findings revealed the existence of long-run equilibrium links in case of type-R (with renewable power generation), type-H (with hydropower generation), and type-N (with non-hydropower generation) model specifications. The rise in both FDI and CO2 emissions added to RPG, HPG, and NHPG in the short and in the long run; however, the intensity of long-run impacts remained much stronger than that of short-run impacts. Considering the comparative intensities of impacts, it has been observed that the renewables generation driving impact of CO2 emissions and FDI on NHPG > RPG > HPG. In turn, the RPG, HPG, and NHPG mitigated CO2 emissions both in the long run and short run, with relatively powerful impacts in the long run. Moreover, the CO2 emissions inhibition impact of HPG > NHPG > RPG. Besides, the negative feedback, response of RPG, HPG, and NHPG to CO2 emissions is dominant since the surge in renewables generation may contribute to curtailment in CO2 emissions and hence substituting renewables for fossil fuel energy use. However, any addition to RPG, HPG, and NHPG in response to the rise in CO2 emissions is based on policy response which may induce policymakers and authorities to promote renewables so as to attain the CO2 emissions curtailment goals. The FDI boosted CO2 emissions in the long run and short run; however, its long-run degree of impact remained relatively stronger than that of short run. Additionally, a unidirectional causal connection has been found running from FDI to CO2 emissions, RPG, HPG, and NHPG. A bidirectional causal link is found operative between CO2 emissions and RPG/HPG/NHPG. It revealed that long-run CO2 emissions injection impact or pollution haven impact is expected to be powerful than that of the short run. Interestingly, the long-run and short-run impacts remained homogeneous in terms of directionality of those linkages; nevertheless, strict heterogeneity has been found in terms of degree of impacts. Also, on the whole, the long-run impacts are found stronger than the short-run impacts.

Based on these empirics, it is implied that impact of FDI policies influenced the non-hydropower generation (i.e., solar power, wind power, geothermal power, other renewables) more than the aggregated measure of renewable power generation as well as individual hydropower generation. The intensity of long-run impacts is found powerful than that of the short run. It implicated that the policymakers should attach more importance to the long run than the short run in terms of CO2 emissions mitigation policies and renewables generation policies. It is further implied that high levels of CO2 emissions may induce the policymakers to suggest the policies to promote renewables generation. Besides, the heterogeneous intensity of impacts in the long run and short run entailed the degree of importance attached to short-term and long-term policies. These empirical findings guided the policymakers to give core consideration to the long-run policies about renewables generation and emissions mitigation.

According to the 13th 5-year plan, the Chinese government aims to further promote foreign investment inflows in the key sectors including new technology, environmental protection, and energy conservation. In this regard, the deviation of FDI from fossil-based energy production to renewable power generation and its consumption be the way forward for emissions mitigation in China domestically as well as globally.

As a future research, the analysis can be conducted at regional level. The regional findings may provide with heterogeneous nature of those relationships of FDI with CO2 emissions and renewable power generation. Those findings may lead to regionally focused heterogeneous policy suggestions. Moreover, the consideration of regional details would allow to take large samples ensuring the robustness of empirical results. Furthermore, sometimes, inclusion of aggregated data may lead to aggregation bias findings. In this regard, the analysis conducted based on disaggregated analysis would yield more reliable findings.

Notes

Terawatt-hours

Million tons

It states that the correlated series move in the same direction i.e. either decrease or increase.

cumulative sum of recursive residuals

Log Likelihood Ratio

Abbreviations

- FDI:

-

Foreign direct investment

- RPG:

-

Renewable power generation

- HPG:

-

Hydropower generation

- NHPG:

-

Non-hydropower generation

- Type-R:

-

Specifications with RPG

- Type-H:

-

Specifications with HPG

- Type-N:

-

Specifications with NHPG

- τ:

-

Kendall’s coefficient

- CC:

-

Pearson’s coefficient

- ρ :

-

Spearman’s coefficient

- ARDL:

-

Autoregressive distributed lag

- VECM:

-

Vector error correction model

- VAR:

-

Vector autoregressive

- GLS:

-

Generalized Least Squares

- PP:

-

Phillips-Perron

- KPSS:

-

Kwiatkowski Phillips Schmidt and Shin

- RESET:

-

Regression equation specification error test

- ARCH:

-

Autoregressive conditional heteroscedasticity

- LM:

-

Lagrange multiplier

- CUSUM:

-

Cumulative sum of recursive residuals

- STIRPAT:

-

Stochastic Impacts by Regression on Population, Affluence and Technology

References

Ahmad M, Zhao ZY, Li H (2019a) Revealing stylized empirical interactions among construction sector, urbanization, energy consumption,economic growth and CO2 emissions in China. Sci Total Environ 657:1085–1098. https://doi.org/10.1016/j.scitotenv.2018.12.112

Ahmad M, Zhao ZY, Irfan M, Mukeshimana MC (2019b) Empirics on influencing mechanisms among energy, finance, trade, environment, and economic growth: a heterogeneous dynamic panel data analysis of China. Environ Sci Pollut Res 26(14):14148–14170. https://doi.org/10.1007/s11356-019-04673-6

Baek J (2016) Do nuclear and renewable energy improve the environment? Empirical evidence from the United States. Ecol Indic 66:352–356. https://doi.org/10.1016/j.ecolind.2016.01.059

Balibey M (2015) Relationships among CO2 emissions, economic growth and foreign direct investment and the environmental kuznets curve hypothesis in Turkey. Int J Energy Econ Policy 5(4):1042–1049

Banerjee A, Dolado J, Mestre R (1998) Error-correction mechanism tests for cointegration in a single-equation framework. J Time Ser Anal 19(3):267–283

Bayer C, Hanck C (2013) Combining non-cointegration tests. J Time Ser Anal 34(1):83–95

Bekun FV, Alola AA, Sarkodie SA (2019) Toward a sustainable environment: nexus between CO2 emissions, resource rent, renewable and nonrenewable energy in 16-EU countries. Sci Total Environ 657:1023–1029. https://doi.org/10.1016/j.scitotenv.2018.12.104

Bilgili F, Kocak E, Bulut U (2016) The dynamic impact of renewable energy consumption on CO2 emissions: a revisited environmental kuznets curve approach. Renew Sust Energ Rev 54:838–845

Blanco L, Gonzalez F, Ruiz I (2013) The impact of FDI on CO2 emissions in Latin America. Oxf Dev Stud 41(1):104–121. https://doi.org/10.1080/13600818.2012.732055

Boswijk HP (1994) Testing for an unstable root in conditional and structural error correction models. J Econ 63(1):37–60

BP (2018) BP Statistical Review on World Energy. https://www.bp.com/content/dam/bp/businesssites/en/global/corporate/pdfs/energy-economics/statistical-review/bp-stats-review-2018-full-report.pdf. Accessed 23 Oct 2018

Buckley PJ, Casson M (2016) The future of the multinational enterprise. Springer, New York, USA

Chen Y (2018) Factors influencing renewable energy consumption in China: an empirical analysis based on provincial panel data. J Clean Prod 174:605–615

Danish, Bin Zhang, Bo Wang, Zhaohua Wang (2017) “Role of Renewable Energy and Non-Renewable Energy Consumption on EKC : Evidence from Pakistan.” Journal of Cleaner Production 156:855–64. https://doi.org/10.1016/j.jclepro.2017.03.203

Davidson R, MacKinnon JG (2004) Econometric theory and methods. Oxford University Press, New York, pp 623–624

Dicky DA, Fuller WA (1979) Distribution of the estimators for autoregressive time series with a unit root. J Am Stat Assoc 74(366):427–431

Dietz T, Rosa EA (1994) Rethinking the environmental impacts of population, affluence and technology. Hum Ecolo Rev 1:277–300

Dietz T, Rosa EA (1997) Effects of population and affluence on CO2 emissions. Proc Natl Acad Sci U S A 94:175–179

Dogan E, Ozturk I (2017) The influence of renewable and non-renewable energy consumption and real income on CO2 emissions in the USA: evidence from structural break tests. Environ Sci Pollut Res Int 24(11):10846–10854. https://doi.org/10.1007/s11356-017-8786-y

Dogan E, Seker F (2016) The influence of real output, renewable and non-renewable energy, trade and financial development on carbon emissions in the top renewable energy countries. Renew Sust Energ Rev 60:1074–1085. https://doi.org/10.1016/j.rser.2016.02.006

Dong K, Sun R, Hochman G (2017) Do natural gas and renewable energy consumption lead to less CO2 emission? Empirical evidence from a panel of BRICS countries. Energy 141:1466–1478. https://doi.org/10.1016/j.energy.2017.11.092

Dong K, Hochman G, Zhang Y, Sun R, Li H, Liao H (2018) CO2 emissions, economic and population growth, and renewable energy: empirical evidence across regions. Energy Econ 75:180–192. https://doi.org/10.1016/j.eneco.2018.08.017

Doytch N, Narayan S (2016) Does FDI influence renewable energy consumption? An analysis of sectoral FDI impact on renewable and non-renewable industrial energy consumption. Energy Econ 54:291–301. https://doi.org/10.1016/j.eneco.2015.12.010

Elliott, G., Rothenberg, T.J. and Stock, J.H., 1992. Efficient tests for an autoregressive unit root

Engle RF, Grager CW (1987) Co-integration and error correction: representation, estimation, and testing. Econometrica 55(2):251–276

Ferrier GD, Reyes J, Zhu Z (2016) Technology diffusion on the international trade network. J Public Econ Theory 18(2):291–312

Fisher R (1932) Statistical methods for research workers. Oliver and Boyd, London

Gökmenoğlu K, Taspinar N (2015) The relationship between Co2emissions, energy consumption, economic growth and FDI: the case of Turkey. J Int Trade Econ Dev 25(5):706–723. https://doi.org/10.1080/09638199.2015.1119876

Gorus MS, Aydin M (2019) The relationship between energy consumption, economic growth, and CO2 emission in MENA countries: causality analysis in the frequency domain. Energy 168:815–822. https://doi.org/10.1016/j.energy.2018.11.139

Granger CWJ (1969) Investigating causal relations by econometric models and cross spectral methods. Econometrica 37:424–438

Hanif I, Faraz Raza SM, Gago-de-Santos P, Abbas Q (2019) Fossil fuels, foreign direct investment, and economic growth have triggered CO2 emissions in emerging Asian economies: some empirical evidence. Energy 171:493–501. https://doi.org/10.1016/j.energy.2019.01.011

Inglesi-Lotz R, Dogan E (2018) The role of renewable versus non-renewable energy to the level of CO2 emissions a panel analysis of sub- Saharan Africa’s Βig 10 electricity generators. Renew Energy 123:36–43. https://doi.org/10.1016/j.renene.2018.02.041

Irandoust M (2016) The renewable energy-growth nexus with carbon emissions and technological innovation: evidence from the Nordic countries. Ecol Indic 69:118–125. https://doi.org/10.1016/j.ecolind.2016.03.051

Johansen S (1988) “STATISTICAL ANALYSIS OF COINTEGRATION VECTORS.” J Econ Dyn Control 12:231–54

Kahouli B (2018) The causality link between energy electricity consumption, CO2 emissions, R&D stocks and economic growth in Mediterranean countries (MCs). Energy 145:388–399. https://doi.org/10.1016/j.energy.2017.12.136

Keho Y (2016) Trade openness and the impact of foreign direct investment on CO2 emissions: econometric evidence from ECOWAS countries. J Econ Sustain Dev 18(7):151–157

Kendall M (1938) A new measure of rank correlation. Biometrika 30(12):81–89

Khandker LL, Amin SB, Khan F (2018) Renewable energy consumption and foreign direct investment: reports from Bangladesh. J Acc Fin Econ 8(3):72–87

Kılıçarslan Z, Dumrul Y (2017) Foreign direct investments and CO2 emissions relationship: the case of Turkey. Bus Econ Res J 8(4):647–660. https://doi.org/10.20409/berj.2017.73

Koçak E, Şarkgüneşi A (2018) The impact of foreign direct investment on CO2 emissions in Turkey: new evidence from cointegration and bootstrap causality analysis. Environ Sci Pollut Res Int 25(1):790–804. https://doi.org/10.1007/s11356-017-0468-2

Kwiatkowski D, Phillips PC, Schmidt P, Shin Y (1992) Testing the null hypothesis of stationarity against the alternative of a unit root: how sure are we that economic time series have a unit root. J Econ 54(1–3):159–178

Lee JW (2013) The contribution of foreign direct investment to clean energy use, carbon emissions and economic growth. Energy Policy 55:483–489. https://doi.org/10.1016/j.enpol.2012.12.039

Mavikela N, Khobai H (2018) Investigating the link between foreign direct investment, energy consumption and economic growth in Argentina. Munich Personal RePEc Archive, No. 83960. https://mpra.ub.uni-muenchen.de/83960/

McNown R, Sam CY, Goh, SK (2018) Bootstrapping the autoregressive distributed lag test for cointegration. Applied Economics, 50(13):1509–1521

Mert M, Boluk G (2016) Do foreign direct investment and renewable energy consumption affect the CO2 emissions? New evidence from a panel ARDL approach to Kyoto annex countries. Environ Sci Pollut Res Int 23(21):21669–21681. https://doi.org/10.1007/s11356-016-7413-7

Omri A, Nguyen DK (2014) On the determinants of renewable energy consumption: international evidence. Energy 72:554–560. https://doi.org/10.1016/j.energy.2014.05.081

Omri A, Nguyen DK, Rault C (2014) Causal interactions between CO2 emissions, FDI, and economic growth: evidence from dynamic simultaneous-equation models. Econ Model 42:382–389. https://doi.org/10.1016/j.econmod.2014.07.026

Pata UK (2018) Renewable energy consumption, urbanization, financial development, income and CO2 emissions in Turkey: testing EKC hypothesis with structural breaks. J Clean Prod 187:770–779

Peng H, Tan X, Li Y, Hu L (2016) Economic growth, foreign direct investment and CO2 emissions in China: a panel Granger causality analysis. Sustainability 8(3). https://doi.org/10.3390/su8030233

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econ 16:289–326

Phillips PC, Perron P (1988) Testing for a unit root for time series regression. Biometrika 75(2):335–346

REN21 (2018) Renewables 2018 global status report. http://www.ren21.net/wp-content/uploads/2018/06/17-8652_GSR2018_FullReport_web_-1.pdf. Accessed 11 Nov 2018

Sarkodie SA, Strezov V (2018) Assessment of contribution of Australia’s energy production to CO2 emissions and environmental degradation using statistical dynamic approach. Sci Total Environ 639:888–899. https://doi.org/10.1016/j.scitotenv.2018.05.204

Sarkodie SA, Strezov V (2019) Effect of foreign direct investments, economic development and energy consumption on greenhouse gas emissions in developing countries. Sci Total Environ 646:862–871. https://doi.org/10.1016/j.scitotenv.2018.07.365

Sbia R, Shahbaz M, Hamdi H (2014) A contribution of foreign direct investment, clean energy, trade openness, carbon emissions and economic growth to energy demand in UAE. Econ Model 36:191–197. https://doi.org/10.1016/j.econmod.2013.09.047

Shahbaz M, Nasir MA, Roubaud D (2018) Environmental degradation in France: the effects of FDI, financial development, and energy innovations. Energy Econ 74:843–857. https://doi.org/10.1016/j.eneco.2018.07.020

Solarin SA, Al-Mulali U, Musah I, Ozturk I (2017) Investigating the pollution haven hypothesis in Ghana: an empirical investigation. Energy 124:706–719. https://doi.org/10.1016/j.energy.2017.02.089

Sung B, Song W-Y, Park S-D (2018) How foreign direct investment affects CO2 emission levels in the Chinese manufacturing industry: evidence from panel data. Econ Syst 42:320–331

Toda, H.Y., Yamamoto, 1995. Statistical inference in vector autoregressions with possibly integrated processes. J Econ 66, 225–250

Ummalla M, Samal A (2018) The impact of hydropower energy consumption on economic growth and CO2 emissions in China. Environ Sci Pollut Res Int 25(35):35725–35737. https://doi.org/10.1007/s11356-018-3525-6

UNCTAD (2018) The least developed countries report 2018: entrepreneurship for structural transformation: beyond business as usual. New York and Geneva

Wall R, Grafakos S, Gianoli A, Stavropoulos S (2018) Which policy instruments attract foreign direct investments in renewable energy? Clim Pol 19(1):59–72. https://doi.org/10.1080/14693062.2018.1467826

Wang S, Zhou C, Li G, Feng K (2016) CO2 , economic growth, and energy consumption in China’s provinces: investigating the spatiotemporal and econometric characteristics of China's CO2 emissions. Ecol Indic 69:184–195. https://doi.org/10.1016/j.ecolind.2016.04.022

Wang H, Ang BW, Su B (2017) A multi-region structural decomposition analysis of global CO 2 emission intensity. Ecol Econ 142:163–176. https://doi.org/10.1016/j.ecolecon.2017.06.023

World Development Indicators (2017) World Bank database. https://data.worldbank.org/indicator/bx.klt.dinv.cd.wd

Yazdi KS, Shakouri B (2017) The effect of renewable energy and urbanization on CO2 emissions: a panel data. Energy Sources Part B 13(2):121–127. https://doi.org/10.1080/15567249.2017.1400607

Zhou Y, Fu J, Kong Y, Wu R (2018) How foreign direct investment influences carbon emissions, based on the empirical analysis of Chinese urban data. Sustainability 10(7). https://doi.org/10.3390/su10072163

Zhu Y, Shi Y, Wu J, Wu L, Xiong W (2018) Exploring the characteristics of CO2 emissions embodied in international trade and the fair share of responsibility. Ecol Econ 146:574–587. https://doi.org/10.1016/j.ecolecon.2017.12.020

Acknowledgements

This work is supported by Beijing Natural Science Foundation (8192043).

Author information

Authors and Affiliations

Corresponding authors

Additional information

Responsible editor: Nicholas Apergis

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Ahmad, M., Zhao, ZY., Rehman, A. et al. Revealing long- and short-run empirical interactions among foreign direct investment, renewable power generation, and CO2 emissions in China. Environ Sci Pollut Res 26, 22220–22245 (2019). https://doi.org/10.1007/s11356-019-05543-x

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-019-05543-x