Abstract

For the last three decades, both China and India are considered as the largest emerging market economies in the world. Both of these economies play an essential role in the global economy in terms of economic output and CO2 emissions. Hence, these countries are expected to play an important role in setting up environmental and sustainable development policies. Therefore, our paper aims to examine the role of natural gas and renewable energy consumptions on CO2 emissions and economic growth during 1965–2016 within a multivariate framework. The autoregressive distributed lag bounds testing approach to cointegration and vector error correction model (VECM) is employed to explore the long-run and causal nexus among the natural gas consumption, renewable energy consumption, coal and petroleum consumption, CO2 emissions, and economic growth, respectively. The empirical results show existence of long-run equilibrium association among the variables. The Granger causality results indicate that the short-run bidirectional causality between renewable energy consumption and economic growth in India, while no causality is found between these two variables in China. However, natural gas consumption causes economic growth in China whereas no causality is confirmed in India in the short-run. The findings further suggest that there is long-run bidirectional causality among the considered variables in both countries. Our paper addresses several important policy implications.

Similar content being viewed by others

Explore related subjects

Discover the latest articles, news and stories from top researchers in related subjects.Avoid common mistakes on your manuscript.

Introduction

Greenhouse gas (GHG) is one of the key causes of global warming and climate change, which are mainly affected by carbon dioxide (CO2) emissions. The proliferation of CO2 emissions comes from the combustion of fossil fuels, which account for 84% of the world energy consumption in 2012 (IEO 2013). Due to the pressure on the nations to reduce CO2 emissions, governments are formulating policies to encourage natural gas and renewable energy rather than fossil fuels. Therefore, the demand for natural gas and renewable energy has increased over the period in the world. Natural gas has several advantages over fossil fuels and for becoming the alternative future energy source. First, it is less carbon intensive than other non-renewable energy sources, i.e., coal and oil.Footnote 1 Second, it is used not only in the household sector, but also in the electric power and industrial sector. Third, unlike nuclear energy, natural gas is free from controversial issues.

Therefore, the demand for natural gas is increasing over the period in the world due to pressure on the nations to mitigate CO2 emissions. The world natural gas consumption has increased from 53.86 quadrillion Btu in 1980 to 120.72 quadrillion Btu in 2012. However, the consumption of natural gas has significantly increased in developing countries than in developed nations.Footnote 2 It has predicted that natural gas consumption will increase by 2.5% per year in the developing countries and 1.1% per year in the developed world during 2012–2040. Over the same period, the share of world natural gas consumption will grow from 52% in 2012 to 62% in 2040 (IEO 2016). Therefore, it is expected that the share of natural gas use will increase over than that of fossil fuels in developing countries.

Over the past two decades, China and India have been the fastest growing emerging economies in the world. During 1990–2010, these two countries accounted for average growth of gross domestic product (GDP) at 10.4% and 6.4% per annum, respectively. Globally, both countries accounted for 10% of world total energy consumption in 1990 and 24% in 2010, respectively. Further, it is predicted that both nation’s energy use will be accounted for 34% of world total energy consumption and the major emitters of the GHGs in the world by 2040 (Energy Information Administration 2013). Therefore, both nations’ energy use choices will have more influence on GHG emissions. Both countries have fixed their range in the target to reduce GHG emissions by 19 to 34% in China and 13 to 17% in India, below the 1990 level by 2030. Therefore, energy economists, environmental scientists, and policymakers are more emphasizing the role of natural gas and renewable energy use in reducing GHG emissions in both emerging market economies.

Natural gas is becoming a major source for both nations because of its low carbon intensity. According to the Central Intelligence Agency 2014 China is the third largest natural gas consumer in the world. In 2012, it accounted for 4.9% of total energy consumption and expected to grow by about 10% by 2020. The natural gas consumption of China will increase by 6.2% per annum, from 5.1 trillion cubic feet (Tcf) in 2012 to 27.5 Tcf in 2040. To meet its rising demand for natural gas, China has been increasing production as well as the import of natural gas over the past two decades. In 2012, it has produced 3.8 Tcf and imported 1.8 Tcf of natural gas, and toped sixth and fifth largest in production and import in the world, respectively. Similarly, India was the tenth largest natural gas consumer by utilizing about 8% of total energy consumption in 2012, almost double share in China’s energy mix. In India, natural gas consumption is expected to increase by 2.8% per annum, from 7.9 Tcf in 2012 to 17.2 Tcf in 2040. Due to inadequate natural gas infrastructure and domestic natural gas production to meet its domestic demand, India has been importing natural gas since 2004. However, India has occupied the 21 and 22 positions in natural gas production and natural gas import in the world, respectively.

Similarly, China and India are endowed with enormous renewable energy sources to meet their increasing demand for energy. Their share of renewable energy use has significantly increased over the period. Both nations had adopted targets for deployment of renewable energy by 2030. These targets are both in terms of total installed capacity and contribution of renewable energy in total electricity generation.Footnote 3 In 2014, renewable energy expanded significantly in terms of capacity installed and power generation in the world. However, the top five countries regarding the deployment of renewable energy capacity are China, the USA, Germany, Spain, and India. These countries accounted for more than half of the capacity added during the same period (REN 21 2015). The primary objective of the deployment of renewable energy is to mitigate CO2 emissions and energy efficiency for sustainable development. Further, these two emerging market economies have made a significant investment in renewable energy sources. Therefore, investigating the impact of natural gas and renewable energy consumption on CO2 emissions and economic growth in both emerging market economies is essential in the world and results to play a significant role for energy economists and policymakers.

With the growing emergence of natural gas and renewable energy use for sustainable economic development, the previous studies have investigated the impact of natural gas and renewable energy consumption on economic growth in both developed and developing countries. However, the existing literature on natural gas, renewable energy use, and economic growth in China is limited, and the results are ambiguous. For instance, Lin and Moubarak (2014) suggested that economic growth has a positive impact on renewable energy consumption. Bloch et al. (2015) reported that renewable energy use has a significant positive impact on economic growth in China. Long et al. (2015) documented that natural gas and renewable energy use have a positive impact on economic growth. Similarly, Salim and Rafiq (2012) found that renewable energy consumption has a positive effect on economic growth in India. More specifically, no study was conducted on the relationship between natural gas consumption and economic growth in the case of India. Therefore, the present study aims to fill the gap in the research by investigating the impact of natural gas and renewable energy use on CO2 emissions and economic growth in both emerging market economies.

The present paper contributes to the energy growth literature in several ways. First, to the best of our knowledge, this is the first study that empirically examines the effect of natural gas and renewable energy consumption on CO2 emissions and economic output in China and India, spanning the period 1965–2016. Second, most of the previous studies are conducted on bivariate models which may give invalid results. Therefore, we apply the multivariate framework to get more reliable and better results. Third, we investigate the long-run equilibrium relationship among the variables using the ARDL bounds testing approach which is better for small sample properties and more reliable than the conventional cointegration tests. Finally, we examine the direction of causality among the considered variables to regulate appropriate policies based on the VECM.

The remainder of the paper is organized as follows. The “Literature review” section deals with a brief review of the literature related to the present study. The data, model specification, and estimation techniques are described in the “Date measurement and methodology” section, while the “Empirical results and discussion” section presents empirical results and discussion. Finally, the “Conclusions and policy implications” section provides conclusions and policy implications.

Literature review

Renewable energy use, gas consumption, and economic growth

Several studies have examined the relationship between renewable energy consumption and economic growth in both advanced and emerging market economies. However, the results are ambiguous. For instance, Apergis and Payne (2010b) investigated the nexus between renewable energy consumption and economic growth in 20 OECD countries over the period 1985–2005. They found that renewable energy consumption has a positive impact on economic growth. Their causality results indicated bidirectional causality between renewable energy consumption and economic growth. Further, they suggest that government policies should encourage renewable energy production by providing tax credits, renewable energy portfolio standards, and the establishment and expansion of a renewable energy system which reduces environmental degradation. Similar results were found by Apergis and Payne (2011) in 6 central American countries, Apergis and Payne (2012) in 80 countries, Ohler and Fetters (2014) in 20 OECD countries, Lin and Moubarak (2014) in China, and Bloch et al. (2015) in China. However, Menyah and Wolde-Rufael (2010) found unidirectional causality running from economic growth to renewable energy consumption in the USA. Salim and Rafiq (2012) documented that economic growth has significantly increased renewable energy in six emerging economies over the period 1980–2006. Further, they reported bidirectional causality between renewable energy consumption and economic growth in Brazil, China, the Philippines, and Turkey, while unidirectional causality from economic growth to renewable energy in India and Indonesia. Likewise, Ocal and Aslan (2013) found that renewable energy consumption has a negative impact on economic growth in Turkey covering the period 1990–2010. Further, they reported that unidirectional causality running from economic growth to renewable energy consumption. Finally, another strand of studies has not established any causal relationship between renewable energy consumption and economic growth. For example, using the Toda-Yamamoto causality test, Payne (2009) found that no causal relationship between renewable energy consumption and economic growth in the USA during 1949–2006. The same results were documented by Menegaki (2011) in 27 European countries and Ben Aïssa et al. (2014) in 11 African countries. Recently, few studies also reported that renewable energy consumption has a positive impact on economic growth. Inglesi-Lotz (2016) found that renewable energy consumption has a positive and significant impact on economic growth in 34 OECD countries. Similarly, Bhattacharya et al. (2016) also documented that renewable energy consumption has a positive impact on economic growth for 57% of top 38 renewable energy consuming countries in the world during the period 1991–2012. Paramati et al. (2017c) reported that renewable energy use has a positive impact on economic growth in Next 11 countries, spanning the period 1990–2012. Further, they could not establish any causal relationship between these two variables. Kutan et al. (2018) and Paramati et al. (2018) also revealed that renewable energy consumption has a positive and significant impact on economic output for major emerging market economies and across a panel of G20 nations, respectively. Further, their studies find an absence of any causal relationship between renewable energy consumption and economic output. Lee and Jung (2018) reported that renewable energy consumption has a negative impact on economic growth in South Korea during 1990–2012. Further, their Granger causality test results revealed unidirectional causality running from economic growth to renewable energy consumption. Recently, Gozgor (2018) reported that renewable energy consumption and economic complexity have a positive impact on economic growth in the USA during 1965–2016. Most recently, Gozgor et al. (2018) documented that renewable energy and non-renewable energy use and economic complexity have a positive impact on economic growth in a panel of 27 OECD countries, spanning the period 1990–2013.

Recent studies were conducted on the relationship between non-renewable energy consumption and economic growth in general, natural gas consumption and economic growth in particular. Some of the studies have examined the relationship between economic growth and energy consumption both in aggregate and disaggregate categories, including coal, oil, natural gas, and electricity. For instance, Yang (2000) investigated the causal relationship between economic growth and energy consumption both in aggregate and disaggregate, including coal, oil, natural gas, and electricity in Taiwan during the period 1954–1997. The author found unidirectional causality running from natural gas consumption to economic growth. Similar results were found by Lotfalipour et al. (2010) in Iran. However, Hu and Lin (2008) explored the nexus between disaggregate energy consumption and economic growth in Taiwan during the period 1982–2006. They found bidirectional causality between natural gas consumption and economic growth. At disaggregate analysis in Malaysia, Saboori and Sulaiman (2013) found unidirectional causality running from natural gas consumption to economic growth in the short-run, while bidirectional causality between two variables in the long-run. Similarly, Bildirici and Bakirtas (2014) examined the relationship between economic growth and disaggregate energy consumption in the BRICTS counties, spanning the period 1980–2011. They found natural gas consumption and economic growth cause each other in Brazil, Russia, and Turkey.

Another strand of studies has explored the relationship between natural gas consumption and economic growth. Apergis and Payne (2010a) examined the nexus between natural gas consumption and economic growth in 65 countries, spanning the period 1992–2005. Using the panel Granger causality test, they found bidirectional causality between natural gas consumption and economic growth in both the short-run and the long-run. Kum et al. (2012) examined the relationship between natural gas consumption and economic growth in G7 countries over the period 1970–2008. They found unidirectional causality running from natural gas consumption to economic growth in Italy, while unidirectional causality running from economic growth to natural gas consumption in the UK and bidirectional causality between two variables in France, Germany, and the USA. Das et al. (2013) found unidirectional causality running from economic growth to natural gas consumption in Bangladesh during the period 1980–2010. However, Shahbaz et al. (2013) documented that natural gas consumption Granger causes economic growth in the short-run in Pakistan during 1972–2010. Shahbaz et al. (2014) examined the nexus between natural gas consumption and economic growth in Pakistan during 197Q1-2011QIV. They found no causal relationship between natural gas use and economic growth in the short-run, while bidirectional causal relationship in the long-run. Ozturk and Al-Mulali (2015) examined the relationship between natural gas consumption and economic growth in 7 Gulf Cooperation Council (GCC) Countries, spanning the period 1980–2012. Using the panel Granger causality test, they found bidirectional causality between natural gas consumption and economic growth in both the short-run and the long-run. Similar results were documented by Solarin and Shahbaz (2015) in Malaysia and Long et al. (2015) in China.

Recently, Balitskiy et al. (2016) examined the nexus between natural gas consumption and economic growth in 26 European Union countries over the period 1970–2011. They found bidirectional causality between natural gas consumption and economic growth. Similarly, Alam et al. (2017) explored the relationship between natural gas consumption, trade, and economic growth in top 15 natural gas consumers of developing countries, spanning the period 1990–2012. They found that natural gas consumption has a positive impact on economic growth. Further, they reported bidirectional causality between natural gas consumption and economic growth. However, Zhi-Guo et al. (2018) examined the nexus between natural gas consumption and economic growth in the Northeast Asian countries, namely, China, Japan, and Korea. The causality test results declared the short-run unidirectional causality running from natural gas consumption to economic growth in China, while no causality between these variables in Japan and Korea. Further, they found no long-run causal relationship between natural gas consumption and economic growth in China, Japan, and Korea.

Finally, a few of the studies found no causal relationship between natural gas consumption and economic growth. For example, Fatai et al. (2004) investigated the causal relationship between economic growth and disaggregate energy consumption in New Zealand and Australia during the period 1960–1999. They could not establish any causal relationship between natural gas consumption and economic growth. Similarly, Kum et al. (2012) found no causal relationship between these two variables in Japan and Canada during 1970–2008.

Renewable energy use, gas consumption, and CO2 emissions

It is widely accepted that energy consumption leads to CO2 emissions. Over the last two decades, numerous studies have reported that advanced and emerging market economies are consuming the higher level of energy to reach their targeted economic growth rates, in turn, leads to CO2 emissions. Therefore, in recent years, there has been increasing interest to examine the impact of renewable energy consumption and natural gas consumption on CO2 emissions. For instance, Salim and Rafiq (2012) investigated the determinates of renewable energy consumption in 6 emerging economies over the period 1980–2006. They found that renewable energy consumption was significantly determined by economic growth and CO2 emissions in emerging economies, including China and India. Further, they reported bidirectional causality between renewable energy and CO2 emissions in Brazil, China, and India. Lin and Moubarak (2014) examined the nexus between renewable energy consumption and economic growth by incorporating CO2 emissions in China during the period 1977–2011. They found no causal relationship between renewable energy consumption and CO2 emissions. Long et al. (2015) examined the impact of renewable energy and non-renewable energy consumption on CO2 emissions and economic growth in China during the period 1977–2011. They reported that renewable energy consumption has significantly reduced CO2 emissions. Similar results were documented by Jaforullah and King (2015) in the USA and Paramati et al. (2017b) in Next 11 countries. However, Menyah and Wolde-Rufael (2010) found that nuclear energy consumption helps reduce CO2 emissions, while renewable energy use does not significantly reduce CO2 emissions in the USA during the period 1960–2007. Further, the authors found that nuclear energy causes CO2 emissions, while no causality running from renewable energy consumption to CO2 emissions. Bloch et al. (2015) found coal consumption increases CO2 emissions, while renewable energy consumption reduces them in China. Similarly, Al-Mulali et al. (2016) found fossil fuel energy consumption has a positive effect on CO2 emissions, while renewable energy consumption significantly reduces CO2 emissions in Kenya during the period 1980–2012. Dogan and Seker (2016) examined the impact of renewable and non-renewable energy consumption on CO2 emissions in 15 European Union countries, spanning the period 1980–2012. They documented that renewable energy consumption has significantly reduced CO2 emissions, while non-renewable energy consumption increases them. Further, they found bidirectional causality between renewable energy consumption and CO2 emissions and unidirectional causality running from non-renewable energy consumption to CO2 emissions. Bhattacharya et al. (2017) investigated the impact of renewable energy use and institutions on economic growth and CO2 emissions in 85 developed and developing countries, spanning the period 1991–2012. They reported that renewable energy consumption has a positive impact on economic growth and a negative impact on CO2 emissions. Further, they documented that institutions also have a positive impact on economic growth and a negative impact on CO2 emissions. Most recently, Paramati et al. (2017b) found that renewable energy use reduces CO2 emissions and increases economic growth in a panel of G20 economies.

Several studies have examined the nexus between non-renewable energy consumption and CO2 emissions. However, only a few studies have explored the relationship between natural gas consumption and CO2 emissions in their analysis. For example, Lotfalipour et al. (2010) found that natural gas consumption has a positive impact on CO2 emissions in Iran. Further, they declared unidirectional causality running from natural gas consumption to CO2 emissions. Saboori and Sulaiman (2013) found bidirectional causality between natural gas consumption and CO2 emissions in Malaysia during the period 1980–2009. Long et al. (2015) reported that natural gas consumption has a positive impact on CO2 emissions in China during the period 1952–2012. Similar results were found by Solarin and Lean (2016) in China and India.

Overall, the review suggests that most of the previous studies have examined the relationship between renewable energy consumption, natural gas consumption, and economic growth. However, a few studies have explored the nexus among these variables by incorporating CO2 emissions in their analysis. Further, the previous studies largely rely on the bivariate models which may give invalid and misleading results. Finally, to date, no specific study examined the impact of natural gas and renewable energy consumption on CO2 emissions and economic growth in China and India. Therefore, it motivates us to empirically explore the nexus among the variables in these emerging market economies.

Data measurement and methodology

Data measurement

In light of the above discussion, our study considers annual data of China and India over the period 1965–2016. The variables in this study consist of per capita natural gas consumption (GAS, measured in millions of tonnes of oil equivalent (Mtoe)), per capita renewable energy consumption (REC, measured in Mtoe), per capita coal and petroleum consumption (CPC, measured in Mtoe), per capita GDP (GDP, measured in constant 2010 US$), and per capita CO2 emissions (CO2, measured in million metric tons). The data on natural gas consumption, renewable energy consumption, coal and petroleum consumption, and CO2 emissions are obtained from the BP Statistical Review of Worldinterpreted as elasticities Energy, 2017, and the data on population and per capita GDP are collected from the World Development Indicators (WDI) online database. Since the variables of this study are measured in different units, therefore, it is important to normalize the data series and transform all the variables into a uniform measurement. This transformation of data into natural logarithms helps to avoid the problems associated with their distributional properties. Therefore, the estimated coefficients in the regression model can be interpreted as elasticities (Paramati et al. 2016; Paramati et al. 2017a; Ummalla and Samal 2018).

Econometric model

The main objective of the present study is to explore the impact of natural gas and renewable energy consumption on CO2 emissions and economic growth for both China and India. To achieve this objective, our study use of following equations:

These functional relationships in Eqs. (1) and (2) can be expressed in log-linear functional form as:

where REC, CPC, GAS, GDP, and CO2 represent per capita renewable energy consumption, per capita coal and petroleum energy consumption, per capita natural gas consumption, per capita GDP, and per capita CO2, respectively. The ln is natural logarithm, α0 is the intercept, α1, α2, α3, and α4 are the slope coefficients of this model, and μ1t and μ2t are the error terms which is assumed to be normally distributed and white noise term.

Estimation techniques

Unit root test

We first aim to avoid the problem of spurious and invalid results associated with all the non-stationary data. For this purpose, our study uses Augmented Dickey-Fuller (ADF) and Phillips-Perron (PP) unit root tests to check the order of integration of all the selected variables. The null hypothesis is the presence of a unit root, and the alternative hypothesis is no unit root. If all the variables are stationary at first difference, i.e., I(1), then this indicates that all variables are non-stationary level but became stationary at their first difference. This result may suggest that these variables in our study have the long-run equilibrium.

ARDL cointegration test

In order to investigate the long-run equilibrium association among the natural gas consumption, renewable energy consumption, coal and petroleum energy consumption, CO2 emissions, and economic growth in the case of China and India, we employ autoregressive distributed lag (ARDL) bounds testing approach to cointegration, as proposed by Pesaran and Shin (1999) and Pesaran et al. (2001). This method is preferred over other conventional methods of cointegration for the following reasons: It can be applied irrespective of order of integration either I(1) or I(0) or mix of both; the unrestricted error correction models (UECM) of ARDL bounds testing approach can be obtained through the simple linear transformation; finally, it is very much suitable for small size sample. The unrestricted error correction models (UECM) of ARDL bounds testing approach can be represented as follows:

where ∆ denotes first difference operator, μt is the error term, and α0 is the constant. The confirmation of the long-run equilibrium association among the variables is based on Wald test or F-statistics which verify the null hypothesis of no long-run relationship against the alternative hypothesis of the presence of the long-run relationship among the variables. The null hypothesis of no cointegration relationship in Eq, (5) can be tested as H0 : αC = αG = αR = αGA = αCP = 0 against the alternative hypothesis of the presence of the long- run cointegration H1 : αC ≠ αG ≠ αR ≠ αGA ≠ αCP = 0. The similar procedure applied for Eqs. (6)–(9). The selection and rejection of the long- run relationship among the variables are decided based on upper critical bounds (UCB) and lower critical bounds (LCB). If the computed F-statistics is greater than the upper critical bounds (UCB), then we conclude that the long-run relationship is an existence among the variables. If the computed F-statistics is lower than lower critical bounds (LCB), then there is non-existence of cointegration relationship among the variables. We use Akaike information criteria (AIC) to select the optimal lag order of the underlining above-mentioned models.

The VECM granger causality test

Next, we aim to investigate the causal relationship among the natural gas consumption, renewable energy consumption, coal and petroleum energy consumption, CO2 emissions, and economic growth after confirming the long-run relationship among the variables. The specification of Granger causality model is as follows:

where ∆ is the difference operator; ECMt − 1 is the lagged error correction term, which is derived from the long-run cointegration relationship;λ1, λ2, λ3, λ4, and λ5 are the speed of adjustment parameter. μ1i, μ2i, μ3i μ4i,and μ5i are the random error terms. The negative and significant coefficients of the lagged error correction term indicate the presence of the long-run causality among the variables. However, the short-run causality is derived from the F-statistics on explanatory variables.

Empirical results and discussion

Preliminary analysis

We present average annual growth rates of selected variables from two emerging market economies, namely, China and India during 1965–2016. These growth rates are presented in Table 1. The growth rate of renewable energy consumption during 1965–1974 to 2005–2014 has increased from 7.80 to 13.52%, whereas growth rates of natural gas and coal and petroleum consumption have been experiencing a declining trend from 24.70 to 16.58% and 9.24 to 5.57%, respectively during 1965–1974 to 2005–2014. Therefore, the rate of growth of CO2 emissions is also reduced from 8.96 to 5.73%. It suggests that there is an inverse relationship between renewable energy consumption and CO2 emissions, and a positive relationship between natural gas, coal and petroleum consumption, and CO2 emissions in China. Further, it suggests that increasing the consumption of renewable energy has reduced CO2 emissions in China. During the same period, China’s economic growth has increased from 3.74 to 9.49%. From Table 1, it is also observed that on an average, China accounts for 7.43% of economic growth, 6.12% of CO2 emissions, 9.28% of renewable energy consumption, 11.36% of natural gas, and 6.23% of coal and petroleum consumption during 1966–2016.

In the case of India, there is an increasing trend of all the selected variables except natural gas consumption from 1965–1974 to 2005–2014. The growth rates of renewable energy consumption and coal and petroleum consumption have increased from 7.12 to 7.92% and 3.91 to 6.18%, respectively, whereas the growth rate of natural gas consumption has been declining from 16.73 to 6.18% during the same period. However, the rates of growth of CO2 emissions and economic growth have increased from 4.12 to 6.43% and 0.91 to 6.21%, respectively from 1965–1974 to 2005–2014. On an average, India accounts for 3.51% of economic growth, 5.28% of CO2 emissions, 5.42% of renewable energy consumption, 12.49% of natural gas consumption, and 5.18% coal and petroleum consumption during 1966–2016. It depicts that there is a positive relationship between renewable energy consumption and coal and petroleum consumption with CO2 emissions in India since both the renewable energy consumption and coal and petroleum consumption are increasing along with CO2 emissions over the period, whereas there is a negative relationship between natural gas consumption and CO2 emissions.

Results of unit root tests

We use ADF and PP unit root tests in order to examine the integration properties of all the selected variables, and results are documented in Table 2. The results of unit root tests suggest that the null hypothesis of a unit root cannot be rejected at a level for all variables. However, on their first difference, the null hypothesis of a unit root can be strongly rejected for the considerable variables at the 5% and 1% level of significance for both countries. Hence, these results suggest that all these variables are following the first order of integration, i.e., I(1). Therefore, we employ the ARDL bounds testing approach to investigate the long-run equilibrium association among the variables.

Results of the ARDL cointegration test

As we find that all the variables are integrated of order I(1) and none of the variables follow I(2), we apply ARDL bounds testing approach to cointegration to examine the long-run relationship among the natural gas consumption, renewable energy consumption, coal and petroleum consumption, CO2 emissions, and economic growth in both countries. The optimal lag length is selected based on AIC and SBC criterion. The results of the ARDL bounds test are reported in Table 3. The results illustrate that the computed F-statistics (6.397) which are higher than the upper critical bounds at the 1% level of significance when GDP is a dependent variable. It indicates that there is a long-run relationship between the variables in China. Similarly, computed F-statistics (7.123 and 5.120) are also higher than upper critical bounds at the 1% level of significance when natural gas consumption and renewable energy consumption are the dependent variables. The results also suggest that there exists a long run relationship among the variables when natural gas and renewable energy consumption are the dependent variables. However, the study failed to establish the long-run relationship when CO2 emissions and coal and petroleum energy consumption are the dependent variables since computed F-statistics (1.085 and 1.617) are lower than the lower critical bounds. Therefore, we could not reject the null hypothesis of no cointegration relationship among the variables.

However, the results are quite the opposite in the case of India. The results suggest that the computed F-statistics (4.278) which is higher than the upper critical bound at the 5% level of significance when CO2 emissions is a dependent variable. It implies that there is a long-run relationship between the variables in India. Similarly, computed F-statistics (7.308, 3.876, and 3.812) are also higher than upper critical bounds at the 1% and 10% level of significance, respectively when GDP, coal and petroleum energy consumption, and renewable energy consumption are the dependent variables. These results also suggest that there is an existence of the long-run relationship among the variables. However, when natural gas consumption is a dependent variable, computed F-statistics (1.655) are lower than the lower critical bounds, this implies the non-existence of a long-run relationship among the variables.

Next, we have conducted the diagnostics test of the long-run bounds testing approach to cointegration, and tests results are displayed in Table 4. The diagnostics test reveals that the models satisfy all the diagnostic tests of no serial correction and the absence of heteroscedasticity for both countries.

Results of Granger causality

In determining the short-run as well as the long-run causal nexus among the natural gas consumption, renewable energy consumption, coal and petroleum energy consumption, CO2 emissions, and economic growth in two major emerging market economies, this study applies the VECM Granger causality test. The short-run causality results are derived from the F-statistics of lagged explanatory variables, whereas the results of long-run causality are obtained from the negative and significant coefficients of t-statistics of lagged error correction term. The results of the short-run and long-run Granger causality test in China and India are reported in Table 5. We find in the short-run bidirectional causality between coal and petroleum energy consumption and CO2 emissions in China. We also find that unidirectional causality running from coal and petroleum energy consumption to economic growth, whereas causality running from renewable energy consumption to natural gas consumption in the short run. However, the study failed to establish any causal relationship between renewable energy consumption, economic growth, and CO2 emissions, and natural gas consumption, economic growth, and CO2 emissions in the short-run in China. With regard to the long-run causality, the results show that coefficients of lagged error correction terms are negative and significant in all the five estimated equations from Eqs. (10) to (14). It indicates evidence of bidirectional causality between natural gas consumption, renewable energy consumption, coal and petroleum energy consumption, CO2 emissions, and economic growth.

In the case of India, the results of Granger causality test show that there is an existence of bidirectional causality between coal and petroleum energy consumption and CO2 emissions, and renewable energy consumption and economic growth in the short-run. The study also reveals the short-run unidirectional causality running from natural gas consumption to coal and petroleum energy consumption and causality running from coal and petroleum energy consumption to renewable energy consumption. However, no causal relationship was found between natural gas consumption, economic growth, and CO2 emissions in the case of India. Further, the results also indicate that there is bidirectional causality among natural gas consumption, renewable energy consumption, coal and petroleum energy consumption, CO2 emissions, and economic growth in the long run.

To sum up this Granger causality test results between all considerable variables, we can highlight that there is short-run and long-run bidirectional causality between coal and petroleum energy consumption and CO2 emissions in China. These results suggest that China is highly reliant on coal and petroleum to achieve economic growth. However, any change in this energy use can effect on CO2 emissions. Similarly, there is evidence of short-run unidirectional and long-run bidirectional causality between coal and petroleum energy consumption and CO2 emissions in India. Therefore, we argue that both countries’ governments should take appropriate energy policies to mitigate CO2 emissions without compromising in economic growth. Besides, there is a long-run bidirectional causality between renewable energy consumption and economic growth in China. Similar results are drawn in the case of India in both the short-run and long-run. These findings suggest that renewable energy consumption positively affects economic growth, and on the other hand, an increase in economic growth can promote renewable energy consumption through various economic activities. It indicates that any energy conservation policies which reduce renewable energy consumption can affect economic growth adversely.

Similarly, there is long-run bidirectional causality between natural gas consumption and economic growth in both China and India. This bidirectional causality between natural gas consumption, renewable energy consumption, coal and petroleum, and economic growth indicates that economic growth in China and India has a strong influence on the use of these energy sources. On the other way, all of these selected energy sources lead to economic growth, and conservative policies on these energy sources are reduce economic growth in the one hand; on the other hand, economic growth supports the consumption of these energy sources in two emerging market economies. However, China and India should increase the consumption of natural gas and renewable energy to reduce CO2 emissions for sustainable development. Further, the Granger causality test shows that natural gas consumption, coal and petroleum energy, renewable energy, and CO2 emissions have long-run bidirectional causality in China and India. This result is consistent with Solarin and Lean (2016) who documented bidirectional causality among natural gas use, economic growth, and CO2 emissions in China and India. Similarly, this finding is also similar to Saidi and Ben Mbarek (2016) who found bidirectional causality among the renewable energy consumption, economic growth, and CO2 emissions in nine developed countries.

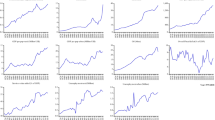

Further, the study also checked the stability of the models which are explained by CUSUM and CUSUMSQ test. The results of CUSUM and CUSUMSQ test are presented in Figs. 1 and 2 for China and Figs. 3 and 4 for India. The results of CUSUM and CUSUMSQ test indicate the stability of the models over the period in both counties because both the lines are lies within the critical bound at the 5% level of significance.

Plot of cumulative sum of recursive residuals for China. The straight lines represent critical bounds at the 5% significance level

Plot of cumulative sum of squares of recursive residuals for China. The straight lines represent critical bounds at the 5% significance level

Plot of cumulative sum of recursive residuals for India. The straight lines represent critical bounds at the 5% significance level

Plot of cumulative sum of squares of recursive residuals for India. The straight lines represent critical bounds at the 5% significance level

Conclusions and policy implications

The present study investigates the impact of natural gas and renewable energy consumption on CO2 emissions and economic growth in two major emerging market economies during 1965–2016. Using the ARDL bounds testing approach to cointegration, the study finds the existence of the long-run relationship among the variables. The results of Granger causality test show that there is evidence of short-run unidirectional causality running from coal and petroleum energy consumption to economic growth. It suggests that coal and petroleum energy consumption plays a significant role in promoting economic growth in China. The study also finds unidirectional causality running from renewable energy consumption to natural gas consumption in the short run. However, no causality was found between renewable energy consumption, economic growth, and CO2 emissions in China. This finding contradicts with Salim and Rafiq (2012) who found bidirectional causality among renewable energy, economic growth, and CO2 emissions in their study countries, especially Brazil and China.

In the case of India, the results reveal the existence of bidirectional causality between renewable energy consumption and economic growth in the short-run. This result is consistent with Apergis and Payne (2010b) in OECD countries and Bloch et al. (2015) in China. Therefore, we argue that an increase in renewable energy consumption positively affects economic growth, and an increase in economic growth can promote renewable energy consumption through various economic activities on the other hand. It also indicates that any energy conservation policies which reduce renewable energy consumption can affect economic growth adversely. The study also reveals the short-run unidirectional causality running from natural gas consumption to coal and petroleum energy consumption and causality running from coal and petroleum energy consumption to renewable energy consumption. It suggests that the consumption of coal and petroleum energy leads to increase the CO2 emissions. Therefore, additional use of coal and petroleum energy has led to shifting the consumption towards renewable energy consumption which reduces CO2 emissions and helps to achieve rapid and sustainable economic growth. Further, there is an existence of bidirectional causality between coal and petroleum energy consumption and CO2 emissions in the short-run for both China and India, which suggests that coal and petroleum energy consumption promotes CO2 emissions, and at the same time an increase in CO2 emissions further increases the demand for coal and petroleum energy for both China and India.

However, in the short-run, no causal relationship was found between natural gas consumption, economic growth, and CO2 emissions for both India and China. The finding of this study is consistent with Fatai et al. (2004) and Kum et al. (2012) who documented that no causal relationship was established between natural gas consumption and economic growth. With regard to the long-run causality, the results indicate that there is bidirectional causality among natural gas consumption, coal and petroleum energy consumption, renewable energy consumption, CO2 emissions, and economic growth for both China and India. All these variables play a preeminent role in the process of adjustment to bring them into equilibrium when there is disequilibrium in the long run. These findings suggest that the feedback hypothesis is established among the variables.

Given these findings, we highlight the following important policy implications: (i) Since bidirectional causality existed between coal and petroleum use and CO2 emissions in the short-and long-run, both the Chinese and Indian governments should formulate effective short-and long-term energy policies to mitigate CO2 emissions. (ii) The establishment of bidirectional causality between natural gas consumption, renewable energy consumption, and economic growth implies that conservative policies on natural gas and renewable energy use are detrimental to economic growth and reduction in the economic growth will adversely affect the demand for natural gas and renewable energy. Therefore, expansionary natural gas and renewable energy policies are boosts to these two emerging market economies. (iii) Natural gas and renewable energy are promoting CO2 emissions in the long-run for both countries. Hence, the policymakers should change the energy structure by increasing the share of clean energy in the total energy mix to reduce CO2 emissions. (iv) Policymakers of these countries should take appropriate policy measures to attract huge funds in clean and renewable energy projects (Alam et al. 2015). (v) The establishment of the public and private partnership would help in transferring the technology in the process of market accessibility for clean and renewable projects. Further, the government should focus on investing in renewable energy sources which not only expand the energy consumption capacity but also increases demand for clean and renewable energy consumption. Therefore, increasing the consumption of clean and renewable energy reduces the dependence on fossil fuel consumption and minimizes the macroeconomic problem of oil price volatility which eventually reduces CO2 emissions and helps for attending sustainable economic development.

The main limitation of our study is that it was conducted on two emerging market economies, i.e., China and India because these economies play a major role in the world in terms of economic growth and CO2 emissions. However, considering the significance of natural gas and renewable energy use, a study may be conducted in other developed and developing regions of the world. Further, this study has not incorporated other drive factors of CO2 emissions and economic growth in the model. In spite of these limitations, this study makes a significant contribution to the body of knowledge from both policy and literature perspectives. Besides these limitations, our study also provides direction for future research. Researchers may also examine the dynamic relationship among natural gas consumption, renewable energy consumption, CO2 emissions, and economic growth in developed and developing countries by incorporating other potential determinates of CO2 emissions and economic growth such as foreign direct investment and stock market development in the model.

Notes

In 2012, CO2 emissions from coal consumption accounted for 43%, while natural gas accounted for 20% of the world CO2 emissions (IEO 2016).

During 1980–2012, natural gas consumption has increased from 20.45 quadrillion Btu to 64.70 quadrillion Btu in the developing countries, while it has increased from 33.40 quadrillion Btu to 59.33 quadrillion Btu in the developed world (The citation “EIA 2015” has been changed to “Energy Information Administration, 2015” to match the author name/date in the reference list. Please check if the change is fine in this occurrence and modify the subsequent occurrences, if necessary.Energy Information Administration 2015).

China and India had targeted renewable energy of 30% and 40%, respectively.

References

Alam MS, Paramati SR, Shahbaz M, Bhattacharya M (2015) Dynamics of natural gas consumption, output and trade: empirical evidence from the emerging economies. Discussion paper 21/15. Department of Economics, Monash University

Alam MS, Paramati SR, Shahbaz M, Bhattacharya M (2017) Natural gas, trade and sustainable growth: empirical evidence from the top gas consumers of the developing world. Appl Econ 49(7):635–649

Al-Mulali U, Solarin SA, Ozturk I (2016) Investigating the presence of the environmental Kuznets curve (EKC) hypothesis in Kenya: an autoregressive distributed lag (ARDL) approach. Nat Hazards 80(3):1729–1747

Apergis N, Payne JE (2010a) Natural gas consumption and economic growth: a panel investigation of 67 countries. Appl Energy 87:2759–2763

Apergis N, Payne JE (2010b) Renewable energy consumption and economic growth: evidence from a panel of OECD countries. Energy Policy 38:656–660

Apergis N, Payne JE (2011) The renewable energy consumption–growth nexus in Central America. Appl Energy 88:343–347

Apergis N, Payne JE (2012) Renewable and non-renewable energy consumption-growth nexus: evidence from a panel error correction model. Energy Econ 34:733–738

Balitskiy S, Bilan Y, Strielkowski W, Štreimikienė D (2016) Energy efficiency and natural gas consumption in the context of economic development in the European Union. Renew Sust Energ Rev 55:156–168

Ben Aïssa MS, Ben Jebli M, Ben Youssef S (2014) Output, renewable energy consumption and trade in Africa. Energy Policy 66:11–18

Bhattacharya M, Paramati SR, Ozturk I, Bhattacharya S (2016) The effect of renewable energy consumption on economic growth: evidence from top 38 countries. Appl Energy 162:733–741

Bhattacharya M, Awaworyi Churchill S, Paramati SR (2017) The dynamic impact of renewable energy and institutions on economic output and CO2 emissions across regions. Renew Energy 111:157–167

Bildirici ME, Bakirtas T (2014) The relationship among oil, natural gas and coal consumption and economic growth in BRICTS (Brazil, Russian, India, China, Turkey and South Africa) countries. Energy 65:134–144

Bloch H, Rafiq S, Salim R (2015) Economic growth with coal, oil and renewable energy consumption in China: prospects for fuel substitution. Econ Model 44:104–115

Central Intelligence Agency (2014), The CIA world factbook, U.S. Retrieved from https://www.cia.gov/library/publications/download

Das A, McFarlane AA, Chowdhury M (2013) The dynamics of natural gas consumption and GDP in Bangladesh. Renew Sust Energ Rev 22:269–274

Dogan E, Seker F (2016) Determinants of CO2 emissions in the European Union: the role of renewable and non-renewable energy. Renew Energy 94:429–439

Energy Information Administration (2013) International energy outlook. EIA, U.S.

Energy Information Administration (2015) International energy outlook. EIA, U.S.

Fatai K, Oxley L, Scrimgeour FG (2004) Modelling the causal relationship between energy consumption and GDP in New Zealand, Australia, India, Indonesia, the Philippines and Thailand. Math Comput Simul 64:431–445

Gozgor G (2018) A new approach to the renewable energy-growth nexus: evidence from the USA. Environ Sci Pollut Res 25(17):16590–16600

Gozgor G, Lau CKM, Lu Z (2018) Energy consumption and economic growth: new evidence from the OECD countries. Energy 153:27–34

Hu J-L, Lin C-H (2008) Disaggregated energy consumption and GDP in Taiwan: a threshold co-integration analysis. Energy Econ 30:2342–2358

IEO (2013) International energy outlook. U.S. International Energy Administration, Washington, DC

Inglesi-Lotz R (2016) The impact of renewable energy consumption to economic growth: a panel data application. Energy Econ 53:58–63

Jaforullah M, King A (2015) Does the use of renewable energy sources mitigate CO2 emissions? A reassessment of the US evidence. Energy Econ 49:711–717

Kum H, Ocal O, Aslan A (2012) The relationship among natural gas energy consumption, capital and economic growth: bootstrap-corrected causality tests from G-7 countries. Renew Sust Energ Rev 16:2361–2365

Kutan AM, Paramati SR, Ummalla M, Zakari A (2018) Financing renewable energy projects in major emerging market economies: evidence in the perspective of sustainable economic development. Emerg Mark Financ Trade 54(8):1761–1777

Lee, SH, Jung Y (2018) Causal dynamics between renewable energy consumption and economic growth in South Korea: empirical analysis and policy implications. Energy Environ 29 (7):1298–1315

Lin B, Moubarak M (2014) Renewable energy consumption – economic growth nexus for China. Renew Sust Energ Rev 40:111–117

Long X, Naminse EY, Du J, Zhuang J (2015) Non-renewable energy, renewable energy, carbon dioxide emissions and economic growth in China from 1952 to 2012. Renew Sust Energ Rev 52:680–688

Lotfalipour MR, Falahi MA, Ashena M (2010) Economic growth, CO2 emissions, and fossil fuels consumption in Iran. Energy 35:5115–5120

Menegaki AN (2011) Growth and renewable energy in Europe: a random effect model with evidence for neutrality hypothesis. Energy Econ 33:257–263

Menyah K, Wolde-Rufael Y (2010) CO2 emissions, nuclear energy, renewable energy and economic growth in the US. Energy Policy 38:2911–2915

Ocal O, Aslan A (2013) Renewable energy consumption–economic growth nexus in Turkey. Renew Sust Energ Rev 28:494–499

Ohler A, Fetters I (2014) The causal relationship between renewable electricity generation and GDP growth: a study of energy sources. Energy Econ 43:125–139

Ozturk I, Al-Mulali U (2015) Natural gas consumption and economic growth nexus: panel data analysis for GCC countries. Renew Sust Energ Rev 51:998–1003

Paramati SR, Ummalla M, Apergis N (2016) The effect of foreign direct investment and stock market growth on clean energy use across a panel of emerging market economies. Energy Econ 56:29–41

Paramati SR, Apergis N, Ummalla M (2017a) Financing clean energy projects through domestic and foreign capital: the role of political cooperation among the EU, the G20 and OECD countries. Energy Econ 61:62–71

Paramati SR, Mo D, Gupta R (2017b) The effects of stock market growth and renewable energy use on CO2 emissions: evidence from G20 countries. Energy Econ 66:360–371

Paramati SR, Sinha A, Dogan E (2017c) The significance of renewable energy use for economic output and environmental protection: evidence from the Next 11 developing economies. Environ Sci Pollut Res 24(15):13546–13560

Paramati SR, Apergis N, Ummalla M (2018) Dynamics of renewable energy consumption and economic activities across the agriculture, industry, and service sectors: evidence in the perspective of sustainable development. Environ Sci Pollut Res 25(2):1375–1387

Payne JE (2009) On the dynamics of energy consumption and output in the US. Appl Energy 86:575–577

Pesaran MH, Shin Y (1999) An autoregressive distributed lag modelling approach to cointegration analysis. In: Strom S (ed) Econometrics and economic theory in 20th century: the Ragnar Frisch centennial symposium, chapter 11. Cambridge University Press, Cambridge

Pesaran MH, Shin Y, Smith RJ (2001) Bounds testing approaches to the analysis of level relationships. J Appl Econ 16(3):289–326

REN 21 (2015) Renewable energy policy networks for the 21 century, Renewables, Global Status Report, Paris

Saboori B, Sulaiman J (2013) Environmental degradation, economic growth and energy consumption: evidence of the environmental Kuznets curve in Malaysia. Energy Policy 60:892–905

Saidi K, Ben Mbarek M (2016) Nuclear energy, renewable energy, CO2 emissions, and economic growth for nine developed countries: evidence from panel granger causality tests. Prog Nucl Energy 88:364–374

Salim RA, Rafiq S (2012) Why do some emerging economies proactively accelerate the adoption of renewable energy? Energy Econ 34:1051–1057

Shahbaz M, Lean HH, Farooq A (2013) Natural gas consumption and economic growth in Pakistan. Renew Sust Energ Rev 18:87–94

Shahbaz M, Arouri M, Teulon F (2014) Short- and long-run relationships between natural gas consumption and economic growth: evidence from Pakistan. Econ Model 41:219–226

Solarin SA, Lean HH (2016) Natural gas consumption, income, urbanization, and CO2 emissions in China and India. Environ Sci Pollut Res 23(18):18753–18765

Solarin SA, Shahbaz M (2015) Natural gas consumption and economic growth: the role of foreign direct investment, capital formation and trade openness in Malaysia. Renew Sust Energ Rev 42:835–845

Ummalla M, Samal A (2018) The impact of hydropower energy consumption on economic growth and CO2 emissions in China. Environ Sci Pollut Res 25(35):35725–35737

Yang H-Y (2000) A note on the causal relationship between energy and GDP in Taiwan. Energy Econ 22:309–317

Zhi-Guo L, Cheng H, Dong-Ming W (2018) Empirical research on the relationship between natural gas consumption and economic growth in the Northeast Asia. Energy Environ 29(2):216–231

Author information

Authors and Affiliations

Corresponding author

Additional information

Responsible editor: Muhammad Shahbaz

Publisher’s note

Springer Nature remains neutral with regard to jurisdictional claims in published maps and institutional affiliations.

Rights and permissions

About this article

Cite this article

Ummalla, M., Samal, A. The impact of natural gas and renewable energy consumption on CO2 emissions and economic growth in two major emerging market economies. Environ Sci Pollut Res 26, 20893–20907 (2019). https://doi.org/10.1007/s11356-019-05388-4

Received:

Accepted:

Published:

Issue Date:

DOI: https://doi.org/10.1007/s11356-019-05388-4